Embed Size (px)

Citation preview

248

Chapter Eight

SEBI’S PERFORMANCE: THE PERCEPTION OF BROKERS AND INVESTORS

In this chapter the perceptions of the brokers and investors has been presented. This was in

fulfillment of one the objectives of the required the study of brokers and investors’

perceptions about SEBI and its performance in the Indian Capital Market. As a result, an

attempt has been made to present the viewpoints of Brokers and investors on their perception

of the performance of SEBI. For this purpose, data was collected from 102 brokers and 70

investors all of them located in the Ludhiana Stock Exchange and its environs. Section A of

this chapter presents the survey of the Capital Market Intermediaries as registered members

of the Securities and Exchange Board of India (SEBI). Section B presents the survey of the

investors. Their views were expressed on a wide variety of issues concerning the Capital

Market regulator in India. Their views were carefully analysed and presented, using figures

and tables in this chapter.

There have not been any survey studies on this aspect, of SEBI, where both the brokers and

investors have been surveyed for their opinions. This research, however, represent the first

joint opinion survey of brokers and investors. It is necessary for SEBI to know and

understand how they feel. The fact that SEBI is out to serve them as participants of the

capital market warrants that, they are listened to. SEBI in attempting to assess its

performance must receive input from the people being served.

249

SECTION A

BROKERS’ PERCEPTION REGARDING THE PERFORMANCE OF SEBI IN THE

INDIAN CAPITAL MARKET

Section A presents the perceptions of brokers as registered members of the Securities and

Exchange Board of India (SEBI). It started by looking at the nature of the brokers’ firms

operating in the Indian capital market.

Table 8.1: The Nature of the Firm

S.N Type *Number Percentage

1 Sole Proprietorship 73 71.57

2 Partnership 1 0.98

3 Limited Company 26 25.49

4 Nil Responses 2 1.96

Total 102 100.00

Source: Primary Data Analysis (2009), *Number of Responses

250

Fig.8.1

The Nature of the Firm

Source: Primary Data Analysis (2009)

Table 8.1 provides information about the nature of the firm in which the Capital Market

Intermediaries carry out their operations. Table 8.1 reveals that out of 102 respondents

contacted, 73 are operating in a Sole Proprietorship environment, making a percentage rate of

71.57%. The private limited company comes second with 26 members holding a percentage

rate of 25.49% (see Fig.8.1). The partnership firm is not very popular in the Indian Capital

Market. For this reason, only 4 partners were seen to be present (see Table 8.2 and Fig.8.2).

Table 8.2: Number of Partners

S.N Gender Number Percentage

1 Male 4 100

2 Female

3 Nil Responses 101

Total 100

Source: Primary Data Analysis (2009)

251

Fig.8.2

Number of Partners

Source: Primary Data Analysis (2009)

Table 8.3: Number of Members

S.N Gender Number Percentage Members %

1 Male 82 45.30 77.36

2 Female 24 13.26 22.64

3 Nil Responses 75 41.44

Total 181 100.00 100.00

Source: Primary Data Analysis (2009)

The Private Company setup is presented in Table 8.3 showing the number of members

present. Out of the 106 members in the private limited companies 82 members are male,

making a percentage rate of 77.36% and Female members are 24, making a percentage rate

of 22.64% (see Fig. 8.3).

252

Fig.8.3

Number of Members

Source: Primary Data Analysis 2009

In Table 8.4 the number of employees is stated as 423. This is an indication that Capital

Market employees’ composition is made up 88.89 % being male and the reminder, 11.11 %

employees being female. The Indian Capital Market is a male dominated society. Looking at

the ratio between males and Females in the working environment the sole proprietor,

partnership business and the private company, one is forced to draw the conclusion that men

are risk takers. This means that the female members are more risk averse (see Fig. 8.4).

253

Table 8.4: Number of Employees in the Firm

S.N Gender Number Percentage Employees %

1 Male 376 87.44 88.89

2 Female 47 10.93 11.11

3 Nil Responses 7 1.63

Total 430 100.00 100.00

Source: Primary Data Analysis (2009)

Fig.8.4

Number of Employees in the Firm

Source: Primary Data Analysis (2009)

254

Table 8.5: Type of Capital Market Intermediary

S.N Type of Intermediary Number Percentage

1 Merchant Banker 1 0.85

2 Registrar and Transfer Agent 2 1.69

3 Underwriter/Broker to Issue 4 3.39

4 Adviser to Issue 4 3.39

5 Banker to Issue 1 0.85

6 Depository 2 1.69

7 Depository Participant 3 2.54

8 Brokerage House 96 81.36

9 Nil Responses 5 4.24

Total 118 100.00

Source: Primary Data Analysis (2009)

Table 8.5 presents information about the types of Capital Market intermediaries. Out of 118

responses, 96 are Brokerage houses. In the Indian Capital Market, the Brokerage Houses are

the most popular (see Fig. 8.5).

Fig.8.5

Types of Capital Market Intermediary

Source: Primary Data Analysis 2009

255

Table 8.6: Number of Client Companies for which firm is Intermediary

S.N Type of Company Number Percentage Clients %

1 Manufacturers 206 8.49 8.59

2 Wholesalers 95 3.91 3.96

3 Retailers 2031 83.68 84.70

4 Foreign International Investors 0.00 0.00

5 Service Companies 66 2.72 2.75

6 Nil Responses 29 1.19

Total 2427 100.00 100.00

Source: Primary Data Analysis (2009)

Table 8.6 reveals a total of number of 2398 clients for which the Capital Market

Intermediaries handle their operations. In the list of clients, the Retailers are at the top with

84.70%, followed by Manufacturers with 8.59% (see Fig. 8.6). Looking at the situation of

Individual Investors, the figures reveal that a total of 11,140 (see Table 8.6) are actively

involved in the Indian Capital Market investment. The figures reveal that out of this number,

78.97% are male and only 21.03 being women. Again women show evidence of risk

averseness in the Indian Capital Market (see Fig.8.7).

Fig.8.6

Number of Client Companies for which firm is Intermediary

Source: Primary Data Analysis (2009)

256

Table 8.7: Number of Individual Investors

S.N Gender Number Percentage Investors%

1 Male 8797 78.79 78.97

2 Female 2343 20.99 21.03

3 Nil Responses 25 0.22

Total 11165 100.00 100.00

Source: Primary Data Analysis (2009)

Fig.8.7

Number of Individual Investors

Source: Primary Data Analysis (2009)

257

Table 8.8: Movement of Individual Investors

S.N Direction Number Percentage Ind. Investors

1 Increasing 63 61.76 67.02

2 Decreasing 31 30.39 32.98

3 No change 1 0.98

4 Nil Responses 7 6.86

Total 102 100.00 100.00

Source: Primary Data Analysis (2009), *Number of Responses

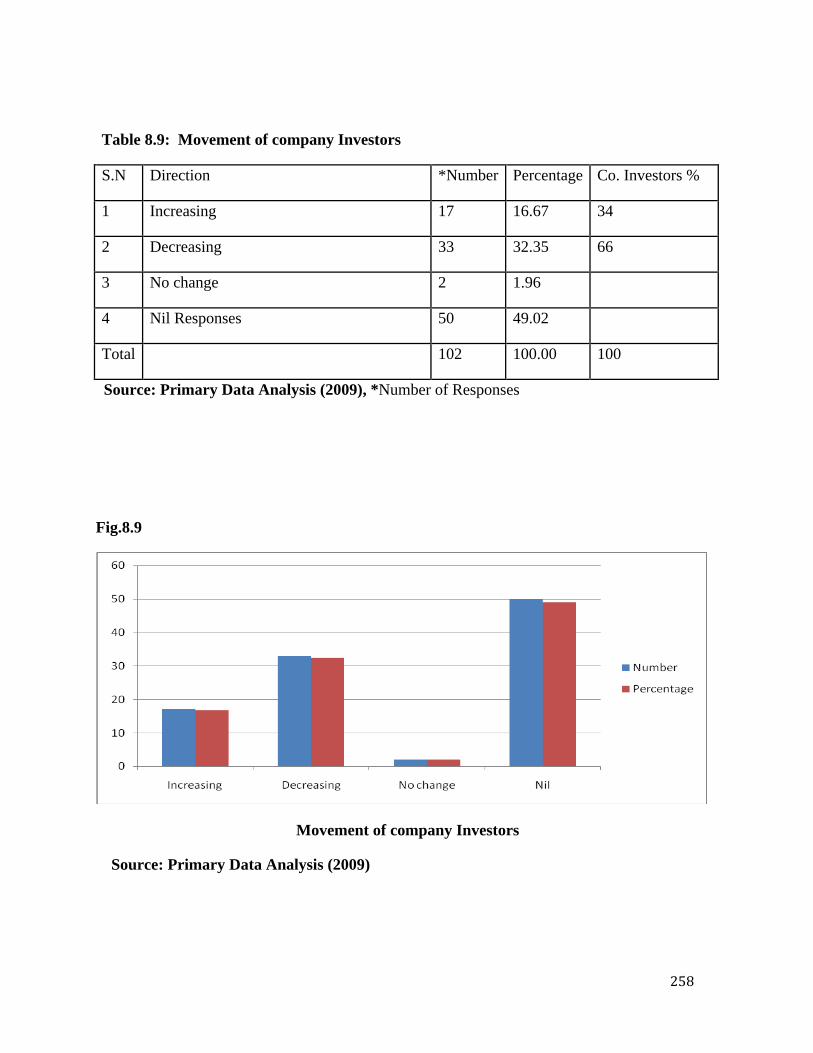

Looking at the movement in the direction of the Capital Market transactions, the primary

data analysis indicates that number of individual investors in recent years is increasing (Table

8.8 and Fig. 8.8). As the trend in individual investors show an increase, the movement in

company or institutional investors shows a decreasing trend (Table 8.9 and Fig. 8.9).

Fig.8.8

Movement of Individual Investors

Source: Primary Data Analysis (2009)

258

Table 8.9: Movement of company Investors

S.N Direction *Number Percentage Co. Investors %

1 Increasing 17 16.67 34

2 Decreasing 33 32.35 66

3 No change 2 1.96

4 Nil Responses 50 49.02

Total 102 100.00 100

Source: Primary Data Analysis (2009), *Number of Responses

Fig.8.9

Movement of company Investors

Source: Primary Data Analysis (2009)

259

Table 8.10: Assessment of margin control safe-guard

S.N Opinion Number Percentage

1 Good 92 90.20

2 Bad 2 1.96

3 Nil

Respons

es

8 7.84

Total 102 100.00

Source: Primary Data Analysis (2009)

The Indian Capital Market primary data analysis indicates that respondents see the margin

control instituted in the Capital Market as a very good control device. More than 90% of the

respondents contacted have the opinion that the margin control is a very essential device

(Table 8.10 and Fig. 8.10). It provides ready financial safety and discipline in Capital Market

dealings (see Table 8.11 and Fig. 8. 11).

Fig.8.10

Assessment of margin control safe-guard

Source: Primary Data Analysis (2009)

260

Table 8.11: Reasons for good margin control

S.N Opinion Number Percentage

1 Control of high volatility 6 6

2 Less default risk 9 9

3 Financial safety and discipline 42 41

6 Capital Protection for Brokers 4 4

7 Hedge against future losses 3 2

8 Nil Responses 38 38

Total 102 100

Source: Primary Data Analysis (2009)

The margin control is necessary evil, it keeps the market stable, but at the same time it

reduces the operating margins of the market dealers. Table 8.12 and Fig. 8.12 present the

reasons why margin control is seen to be a bad device. However, the arguments for margin

control outweigh the arguments against its operation.

Fig.8.11

Reasons for good margin control

Source: Primary Data Analysis (2009)

261

Table 8.12: Reasons why margin control is bad

S.N Opinion Number Percentage

1 Excess Margin 1 50

2 No Proper Warning Systems 1 50

3 Nil Responses

Total 2 100

Source: Primary Data Analysis (2009)

Fig.8.12

Reasons why Margin Control is bad

Source: Primary Data Analysis (2009)

262

Table 8.13: The percentage of Intermediary’s Capital blocked up in the Margin System

S.N Quota Number Percentage

1 More than 25 % 44 43.14

2 About 25 % 30 29.41

3 Less than 25 % 22 21.57

4 Nil Responses 6 5.88

Total 102 100.00

Source: Primary Data Analysis (2009)

Margin control forms part of market the dealer’s permanent capital. As shown in Table 8.13

and Fig. 8.13, some dealers have to sacrifice more than 25% of their working capital, in order

to fulfill the Capital Market Margin control conditions. This is all in a bid to protect the

investors’ interest in the Capital Market. This Action has averagely adversely affected the

market dealers’ trading position (Table 8.14 and Fig. 8.14).

Fig.8.13

The percentage of Intermediary’s capital blocked up in the margin system

Source: Primary Data Analysis (2009)

263

Table 8.14: The Effect of the margin system of Trading on Business

S.N Description Number Percentage

1 Very Badly 3 2.94

2 Badly 2 1.96

3 Averagely 51 50.00

4 Not at all 40 39.22

5 Nil Responses 6 5.88

Total 102 100.00

Source: Primary Data Analysis (2009)

Fig.8.14

The Effect of the margin system of Trading on Business

264

Source: Primary Data Analysis (2009)

Table 8.15: Problems Concerning SEBI as a Capital Market Intermediary

S.N Answer Number Percentage

1 Yes 16 15.69

2 No 78 76.47

3 Nil Responses 8 7.84

Total 102 100.00

Source: Primary Data Analysis (2009)

The Capital Market Intermediaries indicate that most of them do not have any problems with

SEBI. 76.47% of the respondents indicated no problems, while 15.69% indicated that they

had problems and 7.84% abstaining (Table 8.15 and Fig. 8.15)

Fig.8.15

Problems Concerning SEBI as a Capital Market Intermediary

Source: Primary Data Analysis (2009)

265

Table 8.16: Other SEBI Related Problems of Capital Market Intermediaries

S.N Nature of problem Number Percentage

1 Auction of shares (Price Rigging) 1 0.95

2 Hedging 1 0.95

3 Securities Transaction Tax (STT) 1 0.95

4 Margin and Cross Margin 1 0.95

5 Lengthy client registration forms 1 0.95

6 No proper warning systems 4 3.81

7 SEBI is Dictatorial 2 1.90

8 Nil Responses 94 89.52

Total 105 100.00

Source: Primary Data Analysis (2009)

Fig.8.16

Other SEBI related Problems of Capital Market Intermediaries

Source: Primary Data Analysis (2009)

266

Table 8.16 and Fig. 8.16 reveals that even though SEBI is doing its best in regulating the

Indian Capital Market, there were still some shortcomings amongst which the respondents

identified, amongst them, the lack of an appropriate warning system. As shown on Table

8.17 and Fig. 8.17, some of the respondents had some minor problems which needed

addressing by SEBI. Such problems were non-payment for shares, delisting of shares, non-

transfer of shares, non-refund of Initial Public Offer (IPO) money, sudden changes in margin

and poor accounts matching. Such grievances were reported to SEBI individually. Very few

were reported in batches (Table 8.18 and Fig. 8.18).

Table 8.17: Client Problems Requiring the Assistance of SEBI

S.N Nature of problem Number Percentage

1 Non-payment for shares 5 4.90

2 Delisting of shares 1 0.98

3 Non-transfer of shares 2 1.96

4 Non-refund of IPO money 4 3.92

5 Sudden changes in Margin 2 1.96

6 Poor Account matching 1 0.98

7 None 13 12.75

8 Nil Responses 74 72.55

Total 102 100.00

Source: Primary Data Analysis (2009)

267

Fig.8.17

Client Problems Requiring the Assistance of SEBI

Source: Primary Data Analysis (2009)

Table 8.18: The Mode of Reporting Problems to SEBI

S.N Mode Number Percentage

1 Individually 38 37.25

2 In Batches 12 11.76

3 Nil Responses 52 50.98

Total 102 100.00

Source: Primary Data Analysis (2009)

268

Fig.8.18

The Mode of Reporting Problems to SEBI

Source: Primary Data Analysis (2009)

Table 8.19: The Nature of SEBI’s Response to Problems

S.N Description Number Percentage

1 Very slow to react 15 14.71

2 Slow to react 29 28.43

3 Take immediate Action 19 18.63

4 No Action taken 2 1.96

5 Nil Responses 37 36.27

Total 102 100.00

Source: Primary Data Analysis (2009)

269

Fig.8.19

The Nature of SEBI’s Response to Problems

Source: Primary Data Analysis (2009)

The majority of respondents believed that SEBI was slow to react to their problems. This fact

is revealed in Table 8.19 and Fig. 8.19. 14.71% of the respondents said that SEBI was very

slow to react to problems. 28.43% thought that SEBI was slow to react and 18.63% revealed

that they received immediate reaction to their problems. The mixture of fastness and delays in

reaction indicated that SEBI carried out proper investigations before reacting to problems. As

a result, SEBI is seen as an effective regulator of the Indian Capital Market (Table 8.20 and

Fig. 8.20). 54.90% of the respondents thought that SEBI is an effective Market Regulator,

while 16.67% thought the opposite and 28.43% abstained.

270

Table 8.20: Rating the Effectiveness of SEBI’s Response to Complaints

S.N Description Number Percentage

1 Effective 56 54.90

2 Not effective 17 16.67

3 Nil Responses 29 28.43

Total 102 100.00

Source: Primary Data Analysis (2009)

Fig.8.20

Rating the Effectiveness of SEBI’s Response to Complaints

Source: Primary Data Analysis (2009)

271

Table 8.21: The Type of Solutions Offered by SEBI to Complaints

S.N Type Number Percentage

1 Complete solution 31 30.39

2 Partial solution 34 33.33

3 None 3 2.94

4 Nil Responses 34 33.33

Total 102 100.00

Source: Primary Data Analysis (2009)

Fig.8.21

The Type of Solutions Offered by SEBI to Complaints

Source: Primary Data Analysis (2009)

272

Looking at the completeness of SEBI solutions to problems presented by Capital Market

Intermediaries, 30.39% of the respondents said SEBI handled their problems and provided

complete solutions. 33.33% of them said they received only partial solution, 2.94% of the

respondents received no solution at all and 33.33% of abstained (Table 8.21 and Fig. 8.21).

Concerning problem lodging and processing fee, 64.71% of the respondents said that no fee

was paid. 11.76% of them said they had to pay for lodging and processing of their problems,

while 23.53% of the respondents abstained (Table 8.22 and Fig. 8.22).

Table 8.22: Payment of a Fee before Lodging a Complaint with SEBI

S.N Answer Number Percentage

1 Yes 12 11.76

2 No 66 64.71

3 Nil Responses 24 23.53

Total 102 100.00

Source: Primary Data Analysis (2009)

273

Fig. 8.22

Payment of a Fee before Lodging a Complaint with SEBI

Source: Primary Data Analysis (2009)

SEBI regulates the activities of Capital Market Intermediaries as well as the companies they

represent. Looking at the number of clients who had received warnings from SEBI for the

violation of rules and regulations, it was revealed that 6.80% of those who received warnings

were companies and 0.97% of them were Institutional Investors. 33.01% of the respondents’

clients had not received any warning from SEBI, while 59.22% abstained (Table 8.23 and

Fig. 8.23).

274

Table 8.23: Number of clients who have Received Warnings from SEBI for the

Violation of Rules and Regulations

S.N Description Number Percentage

1 Companies 7 6.80

2 Institutional investors 1 0.97

3 Institutional foreign investors 0.00

4 None 33 33.01

5 Nil Responses 61 59.22

Total 102 100.00

Source: Primary Data Analysis (2009)

Fig..8.23

Number of clients who have Received Warnings from SEBI for the Violation of Rules

and Regulations

Source: Primary Data Analysis (2009)

In total, only 8% of the respondents’ clients had received warnings, that is, 7.84% of the

respondents. 45.10% had no warning, while 47.06% abstained (Table 8.24 and Fig. 8.24).

275

Table 8.24: Number of warnings received by the firms from SEBI for violation of Rules and

Regulations

S.N Answer Number Percentage

1 Yes 8 7.84

2 No 46 45.10

3 Nil Responses 48 47.06

Total 102 100.00

Source: Primary Data Analysis (2009)

Fig..8.24

Number of warnings received by the firms from SEBI for violation of Rules and

Regulations

Source: Primary Data Analysis (2009)

276

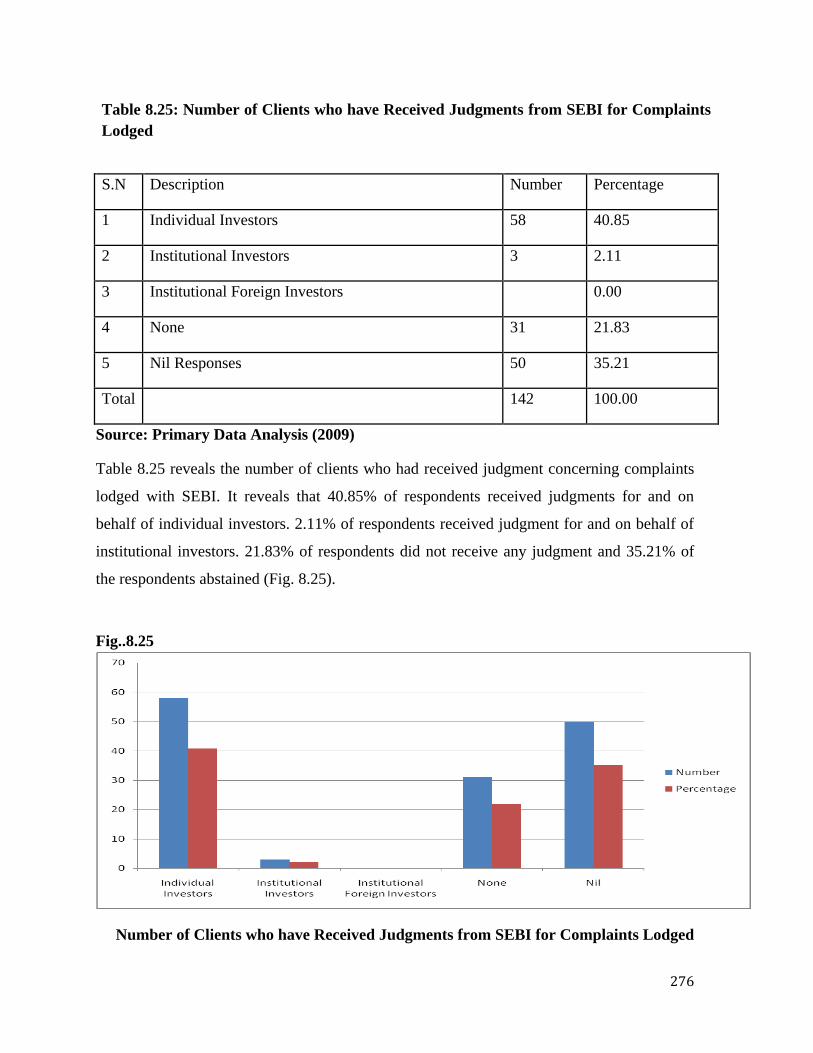

Table 8.25: Number of Clients who have Received Judgments from SEBI for Complaints

Lodged

S.N Description Number Percentage

1 Individual Investors 58 40.85

2 Institutional Investors 3 2.11

3 Institutional Foreign Investors 0.00

4 None 31 21.83

5 Nil Responses 50 35.21

Total 142 100.00

Source: Primary Data Analysis (2009)

Table 8.25 reveals the number of clients who had received judgment concerning complaints

lodged with SEBI. It reveals that 40.85% of respondents received judgments for and on

behalf of individual investors. 2.11% of respondents received judgment for and on behalf of

institutional investors. 21.83% of respondents did not receive any judgment and 35.21% of

the respondents abstained (Fig. 8.25).

Fig..8.25

Number of Clients who have Received Judgments from SEBI for Complaints Lodged

277

Source: Primary Data Analysis (2009)

Table 8.26: The Nature of Judgment Accorded to Clients by SEBI

S.N Description Number Percentage

1 Favourable 28 27.45

2 Not favourable 6 5.88

3 Nil Responses 68 66.67

Total 102 100.00

Source: Primary Data Analysis (2009)

27.45% of the respondents revealed that the judgments received from SEBI were favourable,

while only 5.88% of the judgments received were not favourable. A total of 66.67% of the

respondents abstained (Table 8.26 and Fig. 8.26).

Fig. 8.26

The Nature of Judgment Accorded to Clients by SEBI

Source: Primary Data Analysis (2009)

The research reveals that the presence of SEBI in the Indian Capital Market has made the

Indian Capital Market a much improved place for securities’ trading. 48.04% of the

278

respondents indicated that there is much improvement, with 34.31% of the respondents

having a view that the presence of SEBI just averagely improved securities’ trading. 3.92%

of respondents believe that there has been no improvement, with 13.73% abstaining (Table

8.27 and Fig. 8.27).

Table 8.27: The Effect of the Presence of SEBI in the Indian Capital Market

S.N Opinion Number Percentage

1 Much improvement 49 48.04

2 Averagely improved 35 34.31

3 No improvement 4 3.92

4 Nil Responses 14 13.73

Total 102 100.00

Source: Primary Data Analysis (2009)

Fig. 8.27

The Effect of the Presence of SEBI in the Indian

Capital Market

Source: Primary Data Analysis (2009)

279

Table 8.28: Reasons for Much Improvement

S.N Reasons Number Percentage

1 Transparency 19 25.33

2 Screen based trading 5 6.67

3 No defaulters for many years 5 6.67

4 Flow of foreign investment 1 1.33

5 T+2 settlement system 3 4.00

6 Effective margin system 3 4.00

7 Nil Responses 39 52.00

Total 75 100.00

Source: Primary Data Analysis (2009)

Fig.8.28

Reasons for Much Improvement

Source: Primary Data Analysis (2009)

280

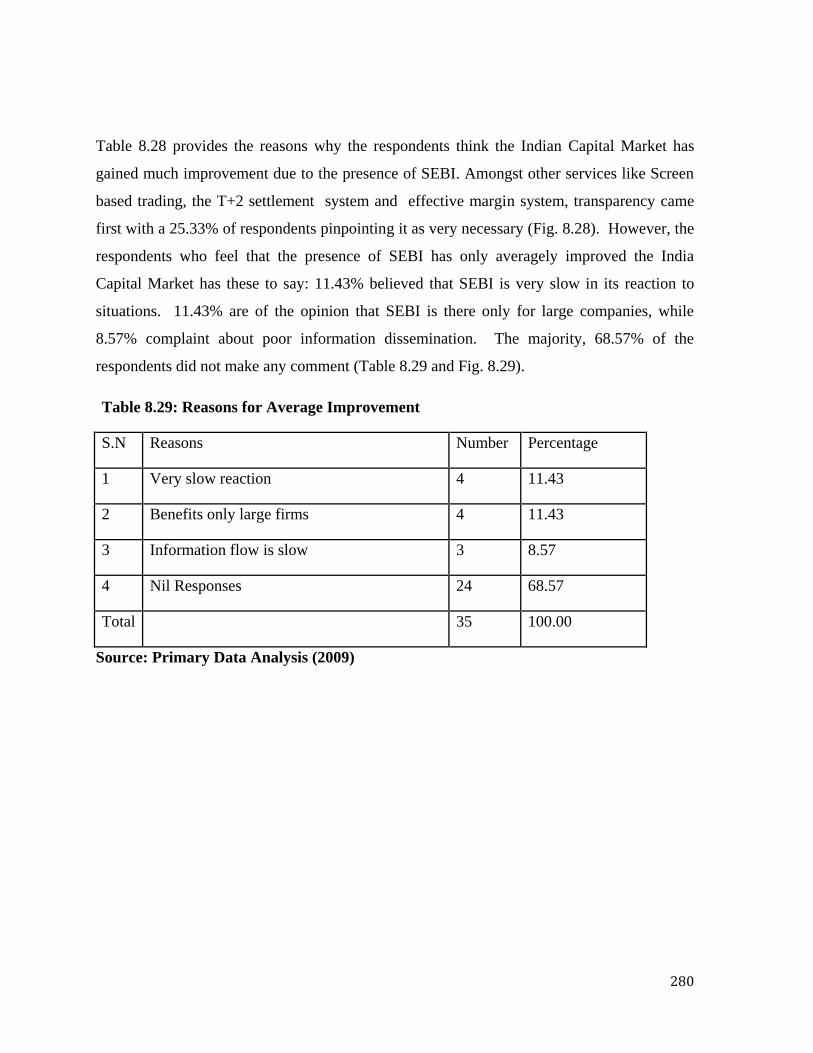

Table 8.28 provides the reasons why the respondents think the Indian Capital Market has

gained much improvement due to the presence of SEBI. Amongst other services like Screen

based trading, the T+2 settlement system and effective margin system, transparency came

first with a 25.33% of respondents pinpointing it as very necessary (Fig. 8.28). However, the

respondents who feel that the presence of SEBI has only averagely improved the India

Capital Market has these to say: 11.43% believed that SEBI is very slow in its reaction to

situations. 11.43% are of the opinion that SEBI is there only for large companies, while

8.57% complaint about poor information dissemination. The majority, 68.57% of the

respondents did not make any comment (Table 8.29 and Fig. 8.29).

Table 8.29: Reasons for Average Improvement

S.N Reasons Number Percentage

1 Very slow reaction 4 11.43

2 Benefits only large firms 4 11.43

3 Information flow is slow 3 8.57

4 Nil Responses 24 68.57

Total 35 100.00

Source: Primary Data Analysis (2009)

281

Fig. 8.29

Reasons for Average Improvement

Source: Primary Data Analysis (2009)

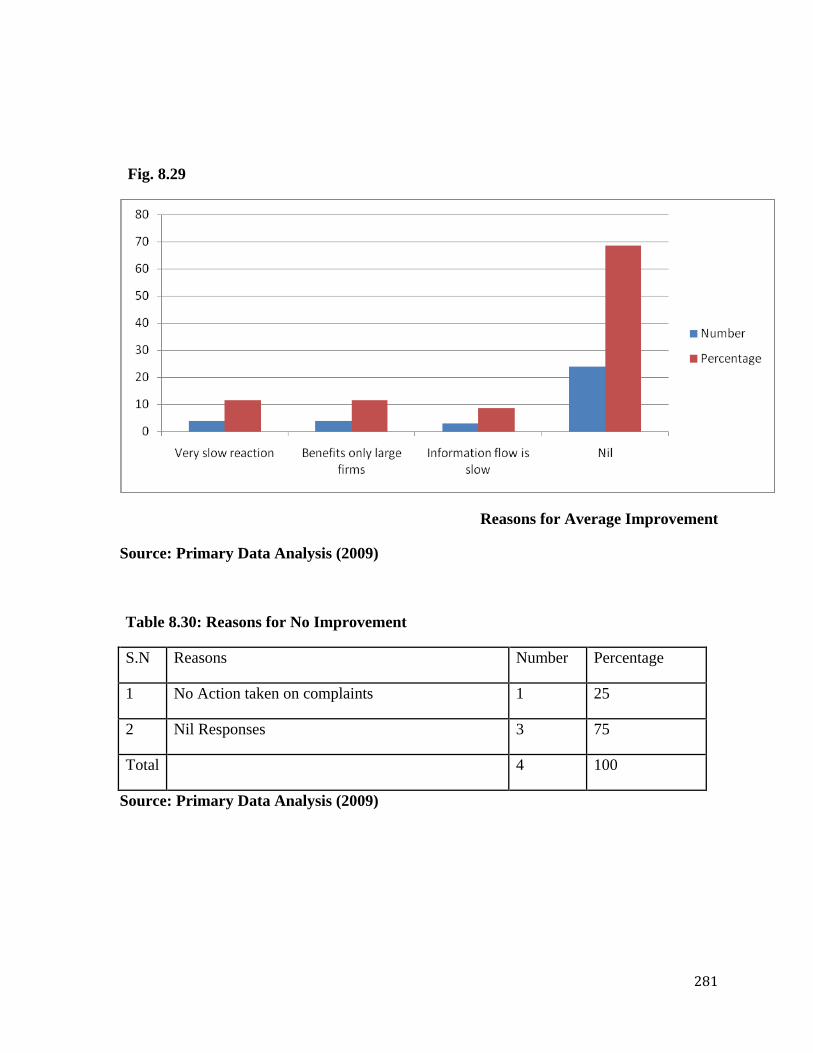

Table 8.30: Reasons for No Improvement

S.N Reasons Number Percentage

1 No Action taken on complaints 1 25

2 Nil Responses 3 75

Total 4 100

Source: Primary Data Analysis (2009)

282

Fig.8.30

Reasons for No Improvement

Source: Primary Data Analysis (2009)

Only one respondent was of the opinion that the presence of SEBI has not brought with it any

improvement. This was a subjective rather than an objective view of the aggrieved persons

(Table 8.30 and Fig. 8.30). Despite this, most of the respondents were of the opinion that

SEBI was doing a job.

On rating the services of SEBI in its capacity as the Indian Capital Market Regulator, 16.67%

of the respondents were of opinion that SEBI was handling the Indian Capital Market in a

very good way, that is, the proper formulation of Capital Market Rules and Regulations

(policies). 36.27% of the respondents were of the opinion that SEBI’s services in the

283

formulation of Capital Market policies were good services yielding good results (Table 8.31

and Fig. 8.31). On the whole, therefore, 52.94% of respondents appreciated the services of

SEBI as good and necessary for the smooth running of the Indian Capital Market.

Table 8.31: Rating of the services of SEBI in formulating Capital Market Policies

(R&R)

S.N Rating Number Percentage

1 Very good 17 16.67

2 Good 37 36.27

3 Average 27 26.47

4 Fair 2 1.96

5 Poor 4 3.92

6 Nil Responses 15 14.71

Total 102 100.00

Source: Primary Data Analysis (2009)

Fig. 8.31

Rating of the Services of SEBI in formulating Capital Market Policies (R&R)

Source: Primary Data Analysis (2009)

284

On rating the services of SEBI in the handling of investors’ complaints, 10.78% of the

respondents stated that SEBI provided very good services, while 24.51% thought that the

services are good. This means that a total of 35.29% of respondents appreciate the work

done by SEBI in the Indian Capital Market in handling of investors’ complaints. Here

39.22% of the respondents were of the opinion that SEBI’s services of handling investors’

complaint can only be rated as average, 21.57% of the respondents abstained (Table 8.32

and Fig. 8.32).

Table 8.32: Rating of the Services of SEBI in the Handling of investors’ Complaints

S.N Rating Number Percentage

1 Very good 11 10.78

2 Good 25 24.51

3 Average 40 39.22

4 Fair 2 1.96

5 Poor 2 1.96

6 Nil Responses 22 21.57

Total 102 100.00

Source: Primary Data Analysis (2009)

285

Fig.8.32

Rating of the Services of SEBI in the Handling of investors’ Complaints

Source: Primary Data Analysis (2009)

Table 8.33: The adequacy of SEBI’s Rules and Regulations in helping the investors to sort

out their investment difficulties.

S.N Opinion Number Percentage

1 Very adequate 17 16.67

2 Fairly adequate 47 46.08

3 Not adequate 18 17.65

4 Nil Responses 20 19.61

Total 102 100.00

Source: Primary Data Analysis (2009)

286

Fig.8.33

The adequacy of SEBI’s Rules and Regulations in helping the investors

to sort out their investment difficulties

Source: Primary Data Analysis (2009)

Table 8.34: SEBI ‘s means of Educating the Investors as to their

Rights and Obligations

S.N Opinion Number Percentage

1 Seminars 51 25.76

2 Press Releases 36 18.18

3 Newspapers 39 19.70

4 Television 35 17.68

5 Radio 10 5.05

6 Nothing 9 4.55

7 Nil Responses 18 9.09

Total 198 100.00

Source: Primary Data Analysis (2009)

287

On the adequacy of SEBI’s Rules and Regulations in helping the investors to sort out their

investment difficulties, 16.67% of the respondents thought that SEBI was very adequate.

46.08% thought that SEBI was fairly adequate, 17.65% of the respondents thought that SEBI

was not adequate and they were 16.61% abstained (Table 8.33 and Fig 8.33).

The research revealed that SEBI was embarked in the process of educating investors on their

rights and obligations, when dealing with the Capital Market. The respondents suggested that

investor education should be done through the organizing of seminars. This was closely

followed be the newspapers with 19.70% and press releases came third with 18.18% ranking

(Table 8.34 and Fig. 8.34)

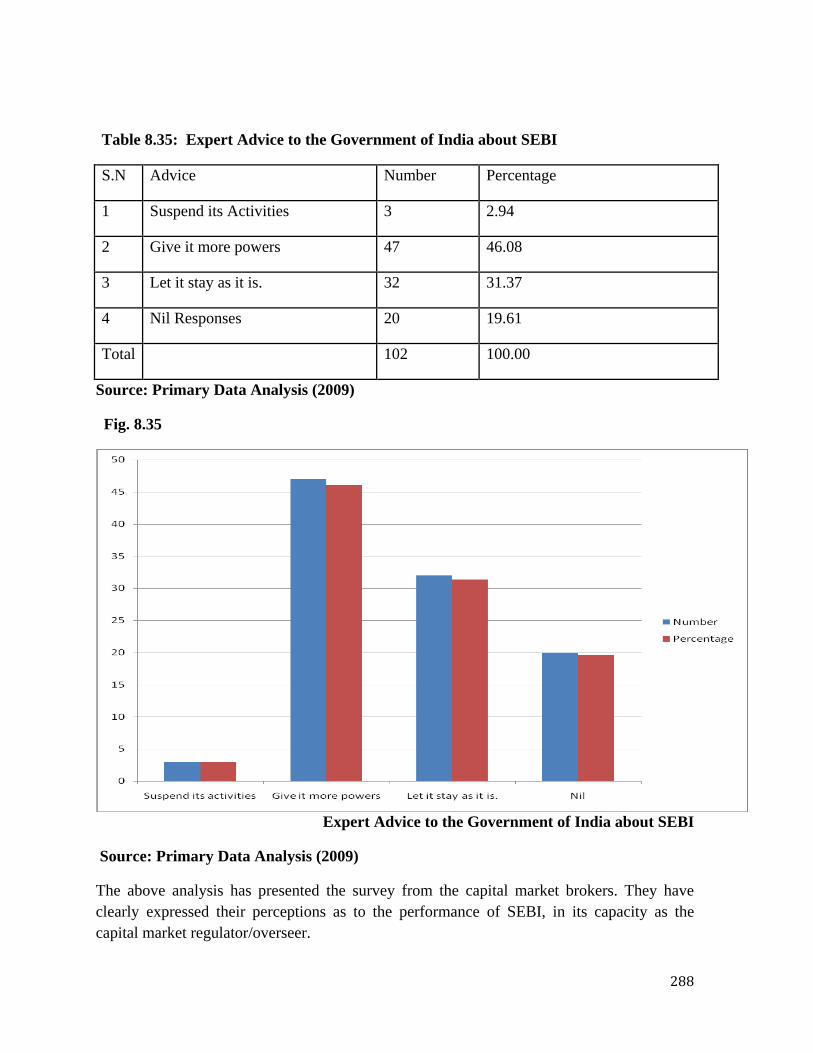

The respondents advised the Government of India to give SEBI more powers, both judicial

and administrative. 46.08% of respondents advocated for more powers (Table 8.35 and Fig.

8.35). The giving of more powers to SEBI meant that its verdicts should be final and not

contended or repealed by any court of law.

Fig. 8.34

SEBI‘s means of Educating the Investors as to their Rights and Obligations

Source: Primary Data Analysis (2009)

288

Table 8.35: Expert Advice to the Government of India about SEBI

S.N Advice Number Percentage

1 Suspend its Activities 3 2.94

2 Give it more powers 47 46.08

3 Let it stay as it is. 32 31.37

4 Nil Responses 20 19.61

Total 102 100.00

Source: Primary Data Analysis (2009)

Fig. 8.35

Expert Advice to the Government of India about SEBI

Source: Primary Data Analysis (2009)

The above analysis has presented the survey from the capital market brokers. They have

clearly expressed their perceptions as to the performance of SEBI, in its capacity as the

capital market regulator/overseer.

289

SECTION B

INVESTORS’ PERCEPTION REGARDING THE PERFORMANCE OF SEBI IN

THE INDIAN CAPITAL MARKET

The preceding analyses presented the Stock Brokers’ survey about SEBI. Section B of this

chapter presents the survey of investors as consumers of the Securities and Exchange Board

of India (SEBI) services. Their views have been expressed on a wide variety of issues

concerning their investment activities in the Indian Capital Market. Their views were

carefully analysed and presented, using figures and tables as seen below:

Table 8.36: Duration of Dealing in the Indian Capital Market (Investors)

S.N Duration Respondents Percentage (%)

1 1 to 2 years 34 48.57

2 3 to 4 years 19 27.14

3 5 to 6 years 4 5.71

4 6 to 10 years 5 7.14

5 More than 10 years 7 10.00

6 Nil 1 1.43

Total 70 100.00

Source: Field Analysis (2009)

Table 8.36 reveals that only 10% of Investors had been investing in the Indian Capital

Market for more than 10 years. 7.14% of Investors had been dealing in the Market for 10

years, 5.71% for 6 years, 27.14% for 4 years and 48.57% for 2 years (see Fig. 8.36).

290

Fig.8.36

Duration of Dealing in the Indian Capital Market (Investors)

Source: Field Analysis (2009)

Table 8.37: Area of the Capital Market in which the Investor has Investment

S.N Details Responses Percentage (%)

1 PSU Bonds 1 0.83

2 Equity Shares 64 53.33

3 Derivatives 5 4.17

4 Life Insurance 17 14.17

5 Debenture Stock 3 2.50

6 Savings Bonds 6 5.00

7 Mutual Funds 21 17.50

8 Any other 0 0.00

9 Nil 3 2.50

Total 120 100.00

Source: Field Analysis (2009)

291

There are a variety of products in the Indian Capital Market. Table 8.37 reveals that most

investors preferred to invest in Equity Shares. 53.33% of investors preferred to invest in

Equity Shares. The second most preferred product was the Mutual Funds, with 17.50% and

the third was Life Insurance, with 14.17% (see Fig.8.37). Equity shares are easily

transferable and they are therefore, attractive to many investors. SEBI is there to oversee that

the market moves smoothly and investors’ interest well protected.

Fig.8.37

Area of the Capital Market in which the Investor has Investment

Source: Field Analysis (2009)

292

Table 8.38: Amount of Current Investment in the Indian Capital Market

S.N Amount Respondents Percentage (%)

1 Rs 5,000 – 50,000 19 27.14

2 Rs 50,000 – 100,000 17 24.29

3 Rs 100,000 – 150,000 10 14.29

4 Rs 150,000 – 200,000 16 22.86

5 Rs 200,000 – 250,000 4 5.71

6 Rs 250,000 and Above 3 4.29

7 Nil 1 1.43

Total 70 100.00

Source: Field Analysis (2009)

The research revealed that on average, investors in the Indian Capital Market had an average

investment of Rs 1, 00,000. A detailed analysis showed that 5.71% of investors own

investment of up to Rs 2, 50,000 in the Capital Market, 22.86% of investors own investment

of up to Rs 2,00,000, 14.29% own investment of up to Rs 1,50,000, 24.29% own investment

of up to Rs 1,00,000 and 27.14% own investment of up to Rs 50,000 (see Table 8.38 and

Fig.8.38).

293

Fig.8.38

Amount of Current Investment in the Indian Capital Market

Source: Field Analysis (2009)

Table 8.39: Investors’ Knowledge or have Heard about SEBI?

S.N Response Respondents Percentage (%)

1 Yes 65 92.86

2 No 5 7.14

3 Nil 0 0.00

Total 70 100.00

Source: Field Analysis (2009)

Table 8.39 reveals that 92.86% of the investors have heard about SEBI (see Fig.8.39). They

understood the role of SEBI and why it was in existence.

294

Fig. 8.39

Investors’ Knowledge or have Heard about SEBI

Source: Field Analysis (2009)

Table 8.40: The Position held by SEBI in the Indian Capital Market

S.N Position Respondents Percentage (%)

1 Investor 5 7.14

2 Broker 3 4.29

3 Regulator 55 78.57

4 Underwriter 1 1.43

5 Merchant Banker 2 2.86

6 Nil 4 5.71

Total 70 100.00

Source: Field Analysis (2009)

The majority of investors had heard about SEBI, but did they know the position of SEBI in

the Indian Capital Market? Table 8.40 reveals that 78.57% of the Investors knew that SEBI

295

was the Regulator of the Indian Capital Market. Very few of them doubted the existence of

the Regulator (see Fig.8.40).

Fig.8.40

The Position held by SEBI in the Indian Capital Market

Source: Field Analysis (2009)

Table 4.41: Opinion whether it is Necessary to have SEBI in the Indian

Capital Market

S.N Response Respondents Percentage (%)

1 Yes 58 82.86

2 No 11 15.71

3 Nil 1 1.43

Total 70 100.00

Source: Field Analysis (2009)

296

Most investors stated that in their opinion, it was necessary to maintain SEBI in the Indian

Capital Market as the Regulator. This fact was revealed in Table 8.41 and Fig. 8.41. It was an

indication that SEBI was doing its best to protect the investors and also regulating the Indian

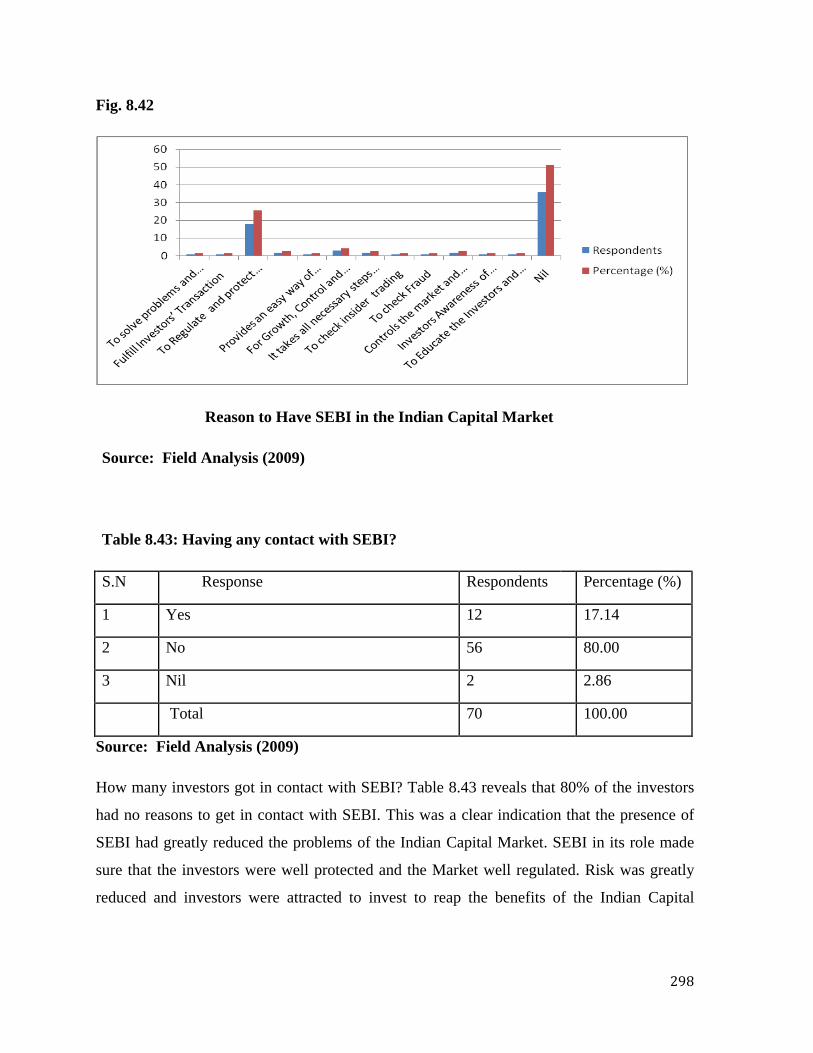

Capital Market as required (see also Table 8.42 and Fig. 8.42).

Fig.8.41

Opinion whether it is Necessary to have SEBI in the Indian Capital Market

Source: Field Analysis (2009)

297

Table 8.42: Reason to have SEBI in the Indian Capital Market

S.N Opinion Respondents Percentage (%)

1 To solve problems and Eliminate Fake

Brokers

1 1.43

2 Fulfill Investors’ Transaction 1 1.43

3 To Regulate and protect Investors 18 25.71

4 Helpful in the Investment World 2 2.86

5 Provides an easy way of Trading 1 1.43

6 For Growth, Control and functioning of the

market

3 4.29

7 It takes all necessary steps to regulate the

Exchange NSE and BSE

2 2.86

8 To check insider trading 1 1.43

9 To check Fraud 1 1.43

10 Controls the market and eyes on Stock

Exchange

2 2.86

11 Investors Awareness of Market 1 1.43

12 To Educate the Investors and Brokers 1 1.43

13 Nil 36 51.43

Total 70 100.00

Source: Field Analysis (2009)

298

Fig. 8.42

Reason to Have SEBI in the Indian Capital Market

Source: Field Analysis (2009)

Table 8.43: Having any contact with SEBI?

S.N Response Respondents Percentage (%)

1 Yes 12 17.14

2 No 56 80.00

3 Nil 2 2.86

Total 70 100.00

Source: Field Analysis (2009)

How many investors got in contact with SEBI? Table 8.43 reveals that 80% of the investors

had no reasons to get in contact with SEBI. This was a clear indication that the presence of

SEBI had greatly reduced the problems of the Indian Capital Market. SEBI in its role made

sure that the investors were well protected and the Market well regulated. Risk was greatly

reduced and investors were attracted to invest to reap the benefits of the Indian Capital

299

Market (see Fig. 8.43). The 17.14% of the investors who contacted SEBI had assorted

grievances (see Table 8.44 and Fig. 8.44).

Fig.8.43

Having any contact with SEBI

Source: Field Analysis (2009)

300

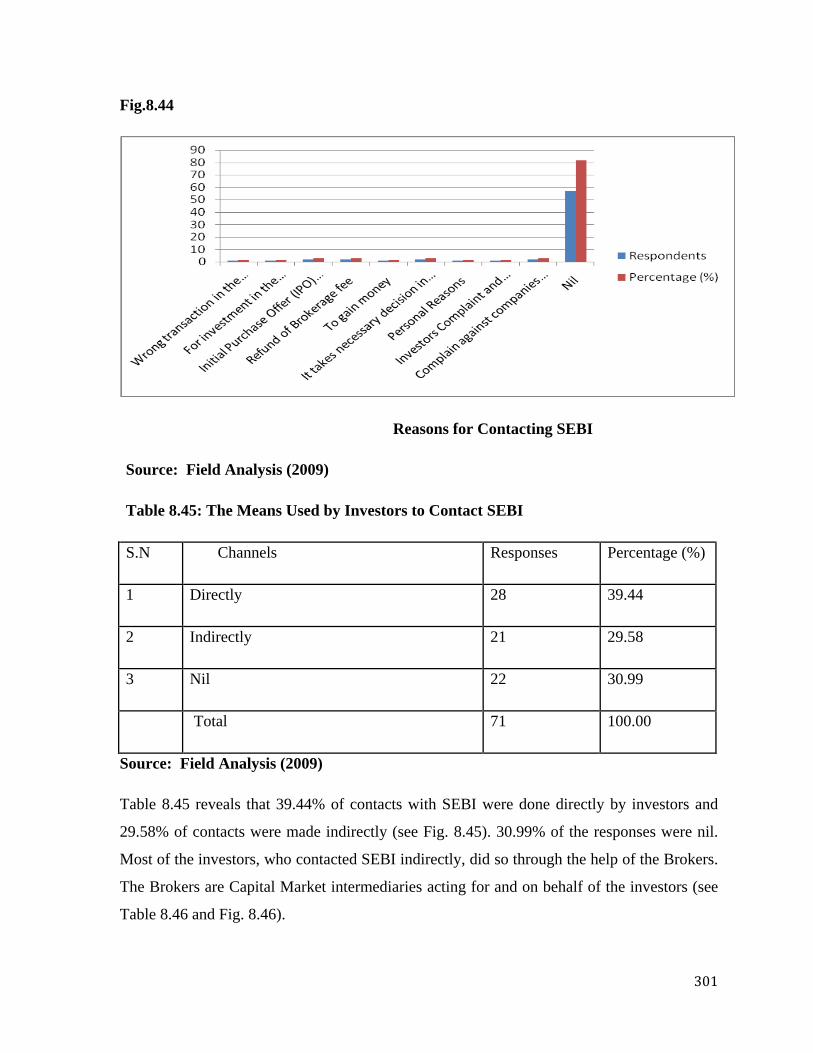

Table 8.44: Reasons for Contacting SEBI

S.N Response Respondents Percentage

(%)

1 Wrong transaction in the Investor’s Account 1 8.33

2 For investment in the Market or project in the market 1 8.33

3 Initial Purchase Offer (IPO) Problems 2 16.67

4 Refund of Brokerage fee 2 16.67

5 To gain money 1 8.33

6 It takes necessary decision in Indian Capital Market 2 16.67

7 Personal Reasons 1 8.33

8 Investors Complaint and investors Awareness 1 8.33

9

Complain against companies working against small

investors 1

8.33

Total 12 100.00

Source: Field Analysis (2009)

301

Fig.8.44

Reasons for Contacting SEBI

Source: Field Analysis (2009)

Table 8.45: The Means Used by Investors to Contact SEBI

S.N Channels Responses Percentage (%)

1 Directly 28 39.44

2 Indirectly 21 29.58

3 Nil 22 30.99

Total 71 100.00

Source: Field Analysis (2009)

Table 8.45 reveals that 39.44% of contacts with SEBI were done directly by investors and

29.58% of contacts were made indirectly (see Fig. 8.45). 30.99% of the responses were nil.

Most of the investors, who contacted SEBI indirectly, did so through the help of the Brokers.

The Brokers are Capital Market intermediaries acting for and on behalf of the investors (see

Table 8.46 and Fig. 8.46).

302

Fig.8.45

The Means Used by Investors to Contact SEBI

Source: Field Analysis (2009)

Table 8.46: The Indirect Means Used in Contacting SEBI

S.N Response Respondents Percentage (%)

1 Through a Broker 6 8.57

2 Mutual Fund Adviser 1 1.43

3 Through the Company 1 1.43

4 Circulars coupon published By SEBI 2 2.86

5 Investor Awareness Association 1 1.43

6 Nil 59 84.29

Total 70 100.00

Source: Field Analysis (2009)

303

Fig.8.46

The Indirect Means Used in Contacting SEBI

Source: Field Analysis (2009)

Table 8.47: The Frequency of Contacts before Problem is Solved

S.N Frequency Respondents Percentage (%)

1 Very Often 10 14.29

2 Often 10 14.29

3 Less Often 33 47.14

4 Nil 17 24.29

Total 70 100.00

Source: Field Analysis (2009)

In the issue of how frequently the investors had to contact SEBI before their problems were

solved, Table 8.47 reveals that 14.29% of respondents had to contact SEBI very often. Again

14.29% contacted often and 47.14% made less often contacts to get their problems solved

304

(Fig. 8.47). There were less often contacts, because on average SEBI took between one to

two months in solving some of the investors complaints (Table 8.48 and Fig. 8.48). The

Table reveals that 50% of the investors had their complaint redressed within one to two

months. It was an indication that SEBI did not keep investors waiting for a long time. The

balance of the 50% went to solving cases that required careful investigation and elaborate

evidence to redress.

Fig.8.47

The Frequency of Contacts before Problem is Solved

Source: Field Analysis (2009)

305

Table 8.48: Duration of Waiting for the Redressal of Problems

S.N Duration Respondents Percentage (%)

1 1 to 2 months 35 50.00

2 3 to 4 months 7 10.00

3 5 to 6 months 1 1.43

4 More than 6 months 6 8.57

5 Nil 21 30.00

Total 70 100.00

Source: Field Analysis (2009)

Fig.8.48

Duration of Waiting for the Redress of Problems

Source: Field Analysis (2009)

306

Table 8.49: Level of Satisfaction about Grievance Handling

S.N Level Respondents Percentage (%)

1 Highly Satisfied 7 10.00

2 Satisfied 44 62.86

3 Not Satisfied 4 5.71

4 Nil 15 21.43

Total 70 100.00

Source: Field Analysis (2009)

After the redress of grievances by SEBI, 72.86% of the investors felt satisfied, amongst

whom 10% were highly satisfied (Table 8.49 and Fig. 8.49). This was a very remarkable

level of satisfaction which was indicative of SEBI’s level of efficiency and effectiveness in

helping to protect the interest of the investors and properly regulating the Capital Market.

Fig.8.49

Level of Satisfaction about Grievance Handling

Source: Field Analysis (2009)

307

Table 8.50: Attending SEBI Organised Seminars for Investors

S.N Response Respondents Percentage (%)

1 Yes 21 30.00

2 No 46 65.71

3 Nil 3 4.29

Total 70 100.00

Source: Field Analysis (2009)

In a bid to create awareness in the investors as to what was happening in the Indian Capital

Market, SEBI was engaged in organizing seminars for the education of investors. Table 8.50

reveals that 30% of investors had attended these seminars. This meant that 70% were not

bothered or were too busy to attend the seminar (see Fig. 8.50).

Fig.8.50

Attending SEBI Organised Seminars for Investors

Source: Field Analysis (2009)

308

Table 8.51: The Facilitators of SEBI Organised Seminars

S.N Facilitators Responses Percentage (%)

1 SEBI’s Investors Education Dept 8 10.13

2 The Stock Exchange 12 15.19

3 Investors’ Watch Organisation 6 7.59

4 Stock Brokers 9 11.39

5 Nil 44 55.70

Total 79 100.00

Source: Field Analysis (2009)

Table 8.51 shows the investors opinion as to the various facilitators of the SEBI organized

seminars. It reveals that in their opinion, 10.13% of the responses stated that SEBI’s

Investors Education Department was responsible for the offering of the seminars. 15.19%

thought that the Stock Exchanges were responsible, 7.59% were looking at the Investors’

Watch Organisation and 11.39% had the opinion that Stock Brokers were responsible (see

Fig. 8.51).

309

Fig.8.51

The Facilitators of SEBI Organised Seminars

Source: Field Analysis (2009)

Table 8.52: Opinion as to whether the Seminar was worth Attending

S.N Response Respondents Percentage (%)

1 Yes 20 28.57

2 No 17 24.29

3 Nil 33 47.14

Total 70 100.00

Source: Field Analysis (2009)

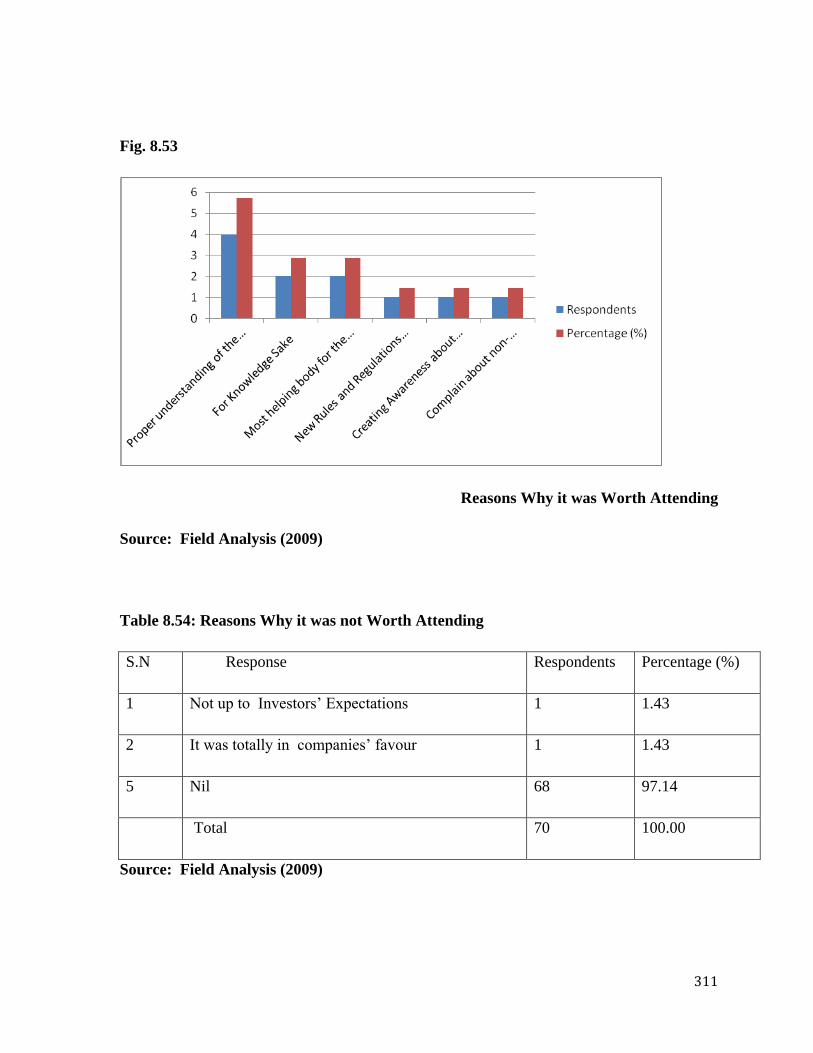

Most of the investors thought that the seminars were worth attending, with 28.57% saying

yes (Table 8.52 and Fig. 8.52). Table 8.53 displays reasons why the investors thought it was

310

worth attending (Fig. 8.53). Some of the investors thought it was not worth attending the

seminars and the reasons given by them are displayed in Table 8.54 and Fig. 8.54.

Fig.8.52

Opinion as to whether the Seminar was worth Attending

Source: Field Analysis (2009)

Table 8.53: Reasons Why it was Worth Attending

S.N Reason Respondents Percentage (%)

1 Proper understanding of the Market and Mutual funds 4 5.71

2 For Knowledge Sake 2 2.86

3 Most helping body for the Investors and Brokers 2 2.86

4 New Rules and Regulations and making people aware about

them

1 1.43

5 Creating Awareness about the market 1 1.43

6 Complain about non-payment of dividends 1 1.43

7 Nil 59 84.29

Total 70 100.00

Source: Field Analysis (2009)

311

Fig. 8.53

Reasons Why it was Worth Attending

Source: Field Analysis (2009)

Table 8.54: Reasons Why it was not Worth Attending

S.N Response Respondents Percentage (%)

1 Not up to Investors’ Expectations 1 1.43

2 It was totally in companies’ favour 1 1.43

5 Nil 68 97.14

Total 70 100.00

Source: Field Analysis (2009)

312

Fig.8.54

Reasons why it was not Worth

Source: Field Analysis (2009)

Table 8.55: Opinion as to the Role of SEBI in the Indian Capital Market

S.N Is the Role Respondents Percentage (%)

1 Over emphasized? 3 4.29

2 As per requirement? 56 80.00

3 Under emphasized? 5 7.14

4 Nil 6 8.57

Total 70 100.00

Source: Field Analysis (2009)

313

The issue as to the opinion concerning the role of SEBI in the Indian Capital Market, 80% of

the respondents stated that its role was not over emphasized nor was it under emphasized.

They stated that the emphasis was as per requirements (Table 8.55 and Fig. 8.55).

Fig.8.55

Opinion as to the Role of SEBI in the Indian Capital Market

Source: Field Analysis (2009)

Table 8.56: Feelings about the Reforms in the Primary Market for Investors’

Safeguard

S.N Feeling Respondents Percentage

(%)

1 Satisfied 50 71.43

2 Highly Satisfied 6 8.57

3 Dissatisfied 4 5.71

4 Highly Dissatisfied 2 2.86

5 Can’t Say 6 8.57

6 Nil 2 2.86

Total 70 100.00

Source: Field Analysis (2009)

314

The investors had a very positive opinion about the reforms in the Primary Market. The

reforms are designed to protect the investors and enable the smooth running of the Indian

Capital Market. Table 8.56 reveals that 71.43% of the investors feel satisfied about the level

of reforms in the Primary Market. 8.57% of them highly satisfied making a total of 80% of

investors who welcome the Capital Market reforms. The reforms have contributed a lot to the

stability and good performance of the Indian Capital Market (see Fig. 8.56).

Fig.8.56

Feelings about the Reforms in the Primary Market for Investors’

Safeguard

Source: Field Analysis (2009)

315

Table 8.57: Feeling about the Settlement and Fund Trading Systems

in the Capital Market

S.N Feeling Respondents Percentage (%)

1 Satisfied 55 78.57

2 Highly Satisfied 7 10.00

3 Dissatisfied 1 1.43

4 Highly Dissatisfied 0.00

5 Can’t Say 6 8.57

6 Nil 1 1.43

Total 70 100.00

Source: Field Analysis (2009)

The Indian Capital Market reforms brought in two prominent things, the T+2 Settlement

System and Fund Trading Systems. They made the market more accessible to investors, that

is, the Market is more liquid and less risky. With these active reforms, 88.57% of investors

felt satisfied and highly satisfied (Table 8.57 and Fig. 8.57). 78.57% felt satisfied and 10%

felt highly satisfied.

316

Fig.8.57

Feeling about the Settlement and Fund Trading Systems in the Capital Market

Source: Field Analysis (2009)

Table 8.58: Screen Based Trading has Brought Transparency in the Capital

Market.

S.N Opinion Respondents Percentage

(%)

1 Agree 48 68.57

2 Strongly Agree 16 22.86

3 Disagree 1 1.43

4 Strongly Disagree 0.00

5 Can’t Say 4 5.71

Nil 1 1.43

70 100.00

Source: Field Analysis (2009)

The Screen Based Trading system is a very valuable asset in the Indian Capital Market.

91.43% of the investors agree that the screen based trading has brought transparency in the

Capital Market. Amongst the 91.43%, 22.86% strongly agree. This is one of the reasons why

the Indian Capital Market has received a very good ranking from the world’s financial

environment (Table 8.58 and Fig. 8.58).

317

Fig.8.58

Screen Based Trading has Brought Transparency in the Capital Market

Source: Field Analysis (2009)

Haven carefully analysed the secondary and primary data into information, the findings have

been extracted which are presented in the next chapter, that is chapter nine. It presents the

summary of findings, conclusion and suggestions for further research.