Embed Size (px)

Citation preview

Chapter 9Chapter 9

Setting Your Personal Setting Your Personal Financial House in OrderFinancial House in Order

22

Learning ObjectivesLearning Objectives After reading and studying the chapter, you After reading and studying the chapter, you

should be able to:should be able to: Define gross income; taxes; net spendable income; Define gross income; taxes; net spendable income;

and the tithe.and the tithe. Describe a budget and identify rough percentages Describe a budget and identify rough percentages

to be spent on housing, food, automobile and to be spent on housing, food, automobile and insurance.insurance.

Describe some cautions in the use of credit cards.Describe some cautions in the use of credit cards. Define and demonstrate the ability to calculate Define and demonstrate the ability to calculate

present value.present value. Describe the major types of insurance and the Describe the major types of insurance and the

purpose for each.purpose for each. Describe and differentiate between Social Security, Describe and differentiate between Social Security,

401K plans, IRAs and mutual funds.401K plans, IRAs and mutual funds. Define Check 21 and how it governs check floating Define Check 21 and how it governs check floating

and kiting.and kiting.

33

BudgetingBudgetingIn preparing a budget, a person should consider their gross income, In preparing a budget, a person should consider their gross income, tithing and tax obligations to obtain what Larry Burkett referred to as tithing and tax obligations to obtain what Larry Burkett referred to as “Net Spendable Income.”“Net Spendable Income.”

Gross IncomeGross Income: : The amount of money that you earn—the total of your The amount of money that you earn—the total of your salary or wages.salary or wages.

TaxTax: : The obligation you have to pay taxes on your income keeping with The obligation you have to pay taxes on your income keeping with the principle to render unto Caesar what is Caesar’s. Most states have the principle to render unto Caesar what is Caesar’s. Most states have income taxes and federal income taxes are collected for the purpose of income taxes and federal income taxes are collected for the purpose of supporting a national defense and other federally funded programs supporting a national defense and other federally funded programs including Social Security.including Social Security.

Net Spendable Income (NSI)Net Spendable Income (NSI):: Defined by Larry Burkett and Crown Defined by Larry Burkett and Crown Financial Ministries, NSI refers to the amount of income you have after Financial Ministries, NSI refers to the amount of income you have after you have tithed and paid your taxes. This is the amount Crown you have tithed and paid your taxes. This is the amount Crown recommends using in determining a budget.recommends using in determining a budget.

44

BudgetingBudgeting Tithe: Tithe: Derived from the Hebrew, Derived from the Hebrew, asairasair, meaning to give the tenth , meaning to give the tenth

part (part (Strong's Exhaustive Concordance) Strong's Exhaustive Concordance) it is a principle introduced it is a principle introduced in the Old Testament involving setting aside a tenth of the first fruitsin the Old Testament involving setting aside a tenth of the first fruits—the best—of a person’s income, for the purpose of giving to the —the best—of a person’s income, for the purpose of giving to the Lord. Lord. The first recorded instance of the tithe was from Abraham to The first recorded instance of the tithe was from Abraham to

King Melchizedek of Salem (Genesis 14:20).King Melchizedek of Salem (Genesis 14:20). Eventually the tithe was codified in Mosaic Law, examples Eventually the tithe was codified in Mosaic Law, examples

including: Deuteronomy 14:22-23, Numbers 18:21, including: Deuteronomy 14:22-23, Numbers 18:21, Deuteronomy 14:28-29, Deuteronomy 26:12, and Malachi 3:10. Deuteronomy 14:28-29, Deuteronomy 26:12, and Malachi 3:10.

Tithing is not a requirement restated in the New Testament but Tithing is not a requirement restated in the New Testament but the principle of giving is. See: Acts 2:44-45; Acts 4:32-37; the principle of giving is. See: Acts 2:44-45; Acts 4:32-37; Romans 13:7; 1 Corinthians 16:1-2; 2 Corinthians 9:7; 2 Romans 13:7; 1 Corinthians 16:1-2; 2 Corinthians 9:7; 2 Corinthians 8:12Corinthians 8:12

There is no set percentage of income demanded, except for the There is no set percentage of income demanded, except for the principle that 100% of all the Believer has been given to steward principle that 100% of all the Believer has been given to steward belongs to the Lord.belongs to the Lord.

55

BudgetingBudgetingCrown Ministries Budget WorksheetCrown Ministries Budget Worksheet

Gross Income:Gross Income: $88,000.00$88,000.00Tithe:Tithe: 8,800.00 8,800.00Tax:Tax: 14,500.00 14,500.00

Budget Category Budget Category Suggested PercentageSuggested Percentage Annual AmountAnnual Amount Monthly Monthly AmountAmount

Net Spendable:** $64,700.00$64,700.00 $5,391.67$5,391.67 Housing: 30 % 30 % 19,410.00 19,410.00 1,617.50 1,617.50 Food: 11 % 11 % 7,117.00 7,117.00 593.08 593.08 Auto: 13 % 13 % 8,411.00 8,411.00 700.92 700.92 Insurance: 5 % 5 % 3,235.00 3,235.00 269.58 269.58 Debt:Debt: 5 % 5 % 3,235.00 3,235.00 269.58 269.58Ent/ Rec: Ent/ Rec: 7 % 7 % 4,529.00 4,529.00 377.42 377.42 Clothing:Clothing: 7 % 7 % 4,529.00 4,529.00 377.42 377.42 Savings: Savings: 5 % 5 % 3,235.00 3,235.00 269.58 269.58 Med/Dental:Med/Dental: 4 % 4 % 2,588.00 2,588.00 215.67 215.67 Misc:Misc: 8 % 8 % 5,176.00 5,176.00 431.33 431.33 School/Childcare:School/Childcare:**** 5 % 5 % 3,235.00 3,235.00 269.58 269.58 Investments:Investments: 5 % 5 % 3,235.00 3,235.00 269.58 269.58

[1] See Crown Financial Ministries website for more information. Budget worksheet and calculator available at: http://www.crown.org/tools/budgetguide.asp. [1] See Crown Financial Ministries website for more information. Budget worksheet and calculator available at: http://www.crown.org/tools/budgetguide.asp.

66

Crown’s Four Minimum StandardsCrown’s Four Minimum Standards

Crown Financial Ministries teaches four Crown Financial Ministries teaches four minimum standards in personal finances for minimum standards in personal finances for couples. couples.

God owns everythingGod owns everything. We are simply stewards . We are simply stewards of that which we “own.”of that which we “own.”

Think ahead and avoid problemsThink ahead and avoid problems. Plan ahead . Plan ahead and establish a budget.and establish a budget.

Keep good recordsKeep good records. Write down and track your . Write down and track your spending. Know how much you owe.spending. Know how much you owe.

Get educatedGet educated. Learn how borrowing and interest . Learn how borrowing and interest workwork

77

Loans and InterestLoans and Interest

There are different types of loans and different types of There are different types of loans and different types of interest rates.interest rates. Loans: Loans: An agreement to borrow a set amount of money and to An agreement to borrow a set amount of money and to

repay the principal with interest. Loans may be for homes repay the principal with interest. Loans may be for homes (mortgages), or for personal purchases including everything (mortgages), or for personal purchases including everything from cars (usually made through banks or credit unions) to from cars (usually made through banks or credit unions) to household supplies or even musical instruments (too often, household supplies or even musical instruments (too often, unfortunately, made on credit cards). unfortunately, made on credit cards).

Interest:Interest: The amount of money a person pays on a loan which The amount of money a person pays on a loan which is in addition to the principal amount borrowed. Two common is in addition to the principal amount borrowed. Two common types of interest charged on loans include variable and fixed.types of interest charged on loans include variable and fixed.

Variable interest rates go up or down throughout the term of the Variable interest rates go up or down throughout the term of the loan depending on market conditions. loan depending on market conditions.

Fixed interest is set at a specific rate for the term of the loan.Fixed interest is set at a specific rate for the term of the loan.

88

Comparison of Payment PlansComparison of Payment PlansConsider a $2,000 credit card balance with an interest rate 13% and making only the Consider a $2,000 credit card balance with an interest rate 13% and making only the minimum monthly payment. minimum monthly payment.

Minimum payment Option:Minimum payment Option:

The first five months minimum payments will be:$ 44.00 month 1The first five months minimum payments will be:$ 44.00 month 1$ 43.51 month 2$ 43.51 month 2$ 43.02 month 3$ 43.02 month 3$ 42.54 month 4$ 42.54 month 4$ 42.07 month 5$ 42.07 month 5

In addition to the 5 payments listed, another 190 payments will be required to pay off the In addition to the 5 payments listed, another 190 payments will be required to pay off the debt. After all 195 payments have been made, you will have paid debt. After all 195 payments have been made, you will have paid $1,674.11 in interest, plus the original balance of $2,000.00 (a total of $3,674.11 ). $1,674.11 in interest, plus the original balance of $2,000.00 (a total of $3,674.11 ).

A Better Option: A Better Option: Make the same payment of $44.00 until the debt is paid in full. The Make the same payment of $44.00 until the debt is paid in full. The payment schedule will be:payment schedule will be:

$ 44.00 month 1$ 44.00 month 1$ 44.00 month 2$ 44.00 month 2$ 44.00 month 3 ...$ 44.00 month 62 $ 44.00 month 3 ...$ 44.00 month 62

You pay $756.37 in interest (versus $ 1,674.11 above). You pay off your debt completely in You pay $756.37 in interest (versus $ 1,674.11 above). You pay off your debt completely in 62 months (versus 195 months above) and save $917.74 in interest62 months (versus 195 months above) and save $917.74 in interest ..[1][1]

[1] Source: To view Crown Financial Ministry’s credit card payment calculator, go to: http://www.crown.org/Tools/creditcard.asp[1] Source: To view Crown Financial Ministry’s credit card payment calculator, go to: http://www.crown.org/Tools/creditcard.asp

99

Applying Present ValueApplying Present Value Present ValuePresent Value: Current value of an amount of money to be : Current value of an amount of money to be

received in the future, or the current value of a future cash received in the future, or the current value of a future cash flow. Helps address questions of investing. The basic flow. Helps address questions of investing. The basic calculation for present value is calculation for present value is PV=FV/(1+i)PV=FV/(1+i)nn.. An alternative An alternative expression is P=S/(1+rt). expression is P=S/(1+rt).

Suppose you needed $25,000 in four years. Using present Suppose you needed $25,000 in four years. Using present value, determine how much you need to invest now to attain value, determine how much you need to invest now to attain that amount assuming a simple interest rate of 5%. that amount assuming a simple interest rate of 5%.

Divide $25,000 by (1 + 0.05)4 to get $21,370 for our initial Divide $25,000 by (1 + 0.05)4 to get $21,370 for our initial investment: investment: PV=FV/(1+i)PV=FV/(1+i)nn or P = S / (1+rt) or P = S / (1+rt)

= $25,000 / (1+ .05)4 = $25,000 / (1+ .05)4 = $25,000 / 1.1699 = $21,370= $25,000 / 1.1699 = $21,370

So, if you had $21,370 to invest today, in four years you So, if you had $21,370 to invest today, in four years you would have accumulated the target of $25,000; you’ve would have accumulated the target of $25,000; you’ve calculated present value. calculated present value.

1010

Insurance Fact SheetInsurance Fact SheetHaving insurance is critical. Following are basic facts in Having insurance is critical. Following are basic facts in planning appropriately.planning appropriately.

Health InsuranceHealth Insurance: Some employers provide health insurance : Some employers provide health insurance coverage that offer group rates. Two common types of health coverage that offer group rates. Two common types of health plans include HMOs, Health Maintenance organizations and plans include HMOs, Health Maintenance organizations and PPOs, a Preferred Provider Organization. PPOs, a Preferred Provider Organization. HMOHMO: Prepaid health care plan in which you use doctors : Prepaid health care plan in which you use doctors

who are members of the HMO. In an HMO, the physician is who are members of the HMO. In an HMO, the physician is paid a flat fee every month for each of the patients on his paid a flat fee every month for each of the patients on his list, whether the doctor actually sees the patient that month list, whether the doctor actually sees the patient that month or not. or not.

PPOPPO: Hospitals and doctors agree to provide clients with : Hospitals and doctors agree to provide clients with health services at a discounted rate. Insurance company health services at a discounted rate. Insurance company pays doctors a discounted rate each time they provide pays doctors a discounted rate each time they provide services to a patient.services to a patient.

1111

Insurance Fact SheetInsurance Fact Sheet

Life InsuranceLife Insurance: Life insurance needs depend on your : Life insurance needs depend on your obligations to others and the risk you are willing to assume. obligations to others and the risk you are willing to assume. As couples marry and have children they have a greater As couples marry and have children they have a greater need for providing money to sustain survivors. Two of the need for providing money to sustain survivors. Two of the most common types include most common types include termterm and and whole lifewhole life. . Term life insuranceTerm life insurance is a no-frills policy with no savings is a no-frills policy with no savings

element. Relatively inexpensive, premiums typically element. Relatively inexpensive, premiums typically increase as you get older. Term life is a policy that is increase as you get older. Term life is a policy that is bought for a specific term or period of time. bought for a specific term or period of time.

Whole life insuranceWhole life insurance has a cash value that accumulates has a cash value that accumulates over the years it is held. If you cancel the policy, you over the years it is held. If you cancel the policy, you receive a lump sum. It combines a death benefit with cash receive a lump sum. It combines a death benefit with cash value accumulations and so is used by some as a savings value accumulations and so is used by some as a savings plan or investment plan.plan or investment plan.

1212

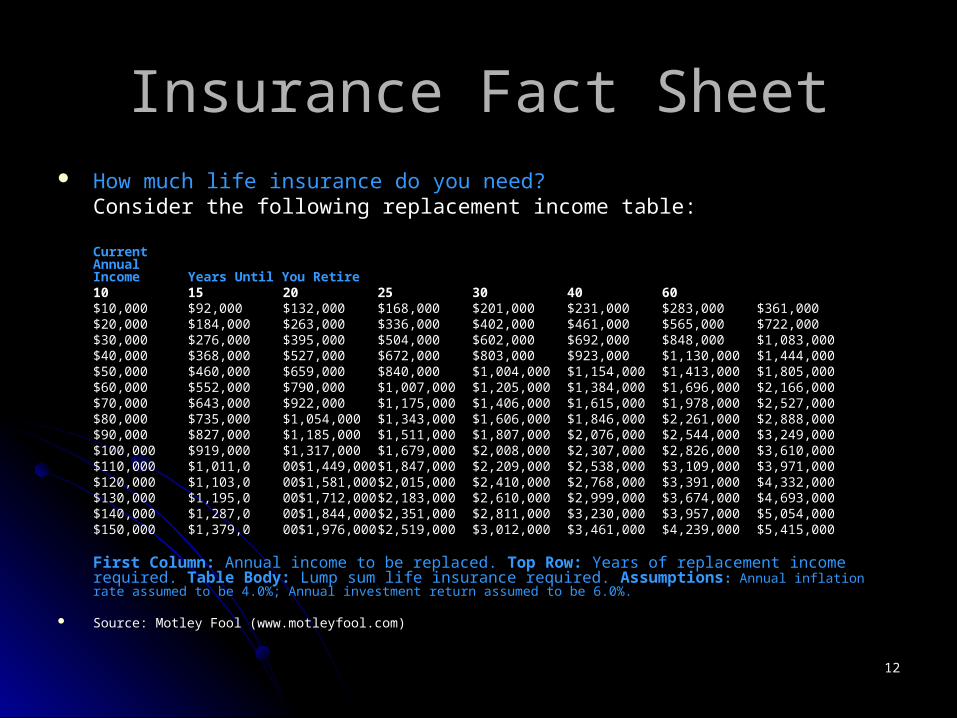

Insurance Fact SheetInsurance Fact Sheet How much life insurance do you need? How much life insurance do you need?

Consider the following replacement income table:Consider the following replacement income table:

CurrentCurrentAnnualAnnualIncomeIncome Years Until You RetireYears Until You Retire

1010 1515 2020 2525 3030 4040 6060$10,000$10,000 $92,000$92,000 $132,000$132,000 $168,000$168,000 $201,000$201,000 $231,000$231,000 $283,000$283,000 $361,000$361,000$20,000$20,000 $184,000$184,000 $263,000$263,000 $336,000$336,000 $402,000$402,000 $461,000$461,000 $565,000$565,000 $722,000$722,000$30,000$30,000 $276,000$276,000 $395,000$395,000 $504,000$504,000 $602,000$602,000 $692,000$692,000 $848,000$848,000 $1,083,000$1,083,000$40,000$40,000 $368,000$368,000 $527,000$527,000 $672,000$672,000 $803,000$803,000 $923,000$923,000 $1,130,000$1,130,000 $1,444,000$1,444,000$50,000$50,000 $460,000$460,000 $659,000$659,000 $840,000$840,000 $1,004,000$1,004,000 $1,154,000$1,154,000 $1,413,000$1,413,000 $1,805,000$1,805,000$60,000$60,000 $552,000$552,000 $790,000$790,000 $1,007,000$1,007,000 $1,205,000$1,205,000 $1,384,000$1,384,000 $1,696,000$1,696,000 $2,166,000$2,166,000$70,000$70,000 $643,000$643,000 $922,000$922,000 $1,175,000$1,175,000 $1,406,000$1,406,000 $1,615,000$1,615,000 $1,978,000$1,978,000 $2,527,000$2,527,000$80,000$80,000 $735,000$735,000 $1,054,000$1,054,000 $1,343,000$1,343,000 $1,606,000$1,606,000 $1,846,000$1,846,000 $2,261,000$2,261,000 $2,888,000$2,888,000$90,000$90,000 $827,000$827,000 $1,185,000$1,185,000 $1,511,000$1,511,000 $1,807,000$1,807,000 $2,076,000$2,076,000 $2,544,000$2,544,000 $3,249,000$3,249,000$100,000$100,000 $919,000$919,000 $1,317,000$1,317,000 $1,679,000$1,679,000 $2,008,000$2,008,000 $2,307,000$2,307,000 $2,826,000$2,826,000 $3,610,000$3,610,000$110,000$110,000 $1,011,0$1,011,0 00$1,449,00000$1,449,000 $1,847,000$1,847,000 $2,209,000$2,209,000 $2,538,000$2,538,000 $3,109,000$3,109,000 $3,971,000$3,971,000$120,000$120,000 $1,103,0$1,103,0 00$1,581,00000$1,581,000 $2,015,000$2,015,000 $2,410,000$2,410,000 $2,768,000$2,768,000 $3,391,000$3,391,000 $4,332,000$4,332,000$130,000$130,000 $1,195,0$1,195,0 00$1,712,00000$1,712,000 $2,183,000$2,183,000 $2,610,000$2,610,000 $2,999,000$2,999,000 $3,674,000$3,674,000 $4,693,000$4,693,000$140,000$140,000 $1,287,0$1,287,0 00$1,844,00000$1,844,000 $2,351,000$2,351,000 $2,811,000$2,811,000 $3,230,000$3,230,000 $3,957,000$3,957,000 $5,054,000$5,054,000$150,000$150,000 $1,379,0$1,379,0 00$1,976,00000$1,976,000 $2,519,000$2,519,000 $3,012,000$3,012,000 $3,461,000$3,461,000 $4,239,000$4,239,000 $5,415,000$5,415,000

First Column:First Column: Annual income to be replaced. Annual income to be replaced. Top Row:Top Row: Years of replacement income required. Years of replacement income required. Table Body:Table Body: Lump sum Lump sum life insurance required. life insurance required. AssumptionsAssumptions:: Annual inflation rate assumed to be 4.0%; Annual investment return assumed to be 6.0%. Annual inflation rate assumed to be 4.0%; Annual investment return assumed to be 6.0%.

Source: Motley Fool (www.motleyfool.com)Source: Motley Fool (www.motleyfool.com)

1313

Insurance Fact SheetInsurance Fact SheetDisability InsuranceDisability Insurance: Some people : Some people

rely solely on Social Security’s disability rely solely on Social Security’s disability insurance, but this does not protect all insurance, but this does not protect all of a person’s income. Disability of a person’s income. Disability insurance is designed to replace insurance is designed to replace anywhere from 45-60% of income anywhere from 45-60% of income should a worker suffer an injury or should a worker suffer an injury or illness that prevents him or her from illness that prevents him or her from working and earning an income.working and earning an income.

1414

Insurance Fact SheetInsurance Fact Sheet Property and Casualty InsuranceProperty and Casualty Insurance: A person should : A person should

consider holding policies that provide 100 percent of the consider holding policies that provide 100 percent of the replacement cost of a home and belongings if the replacement cost of a home and belongings if the insured owns a home. insured owns a home. Renters should insure belongings through renter’s Renters should insure belongings through renter’s

insurance. insurance. It is advisable to inventory and even videotape the It is advisable to inventory and even videotape the

contents of one’s home. contents of one’s home. Common types of losses often covered include fire, Common types of losses often covered include fire,

tornado and natural disaster, and burglary. tornado and natural disaster, and burglary. Flood insurance is not available through private Flood insurance is not available through private

insurers but may be obtained through the federal insurers but may be obtained through the federal government’s national flood insurance program.government’s national flood insurance program.

1515

Insurance Fact SheetInsurance Fact Sheet Automobile InsuranceAutomobile Insurance: Insuring against losses related : Insuring against losses related

to driving and your vehicle.to driving and your vehicle. LiabilityLiability: States require drivers to carry liability : States require drivers to carry liability

insurance on their automobiles. This type of insurance on their automobiles. This type of insurance covers damages the owner’s vehicle insurance covers damages the owner’s vehicle causes to others. causes to others.

CollisionCollision: Insurance against damages that result from : Insurance against damages that result from an accident, even if it’s the policy holder’s own fault, is an accident, even if it’s the policy holder’s own fault, is called collision insurance. called collision insurance.

ComprehensiveComprehensive: Similar to collision insurance, : Similar to collision insurance, comprehensive insurance provides coverage against comprehensive insurance provides coverage against damage caused by an unknown party or an “Act of damage caused by an unknown party or an “Act of God.” Vandalism, theft or fire damages are examples God.” Vandalism, theft or fire damages are examples of potential losses covered by comprehensive of potential losses covered by comprehensive insurance plans.insurance plans.

1616

Personal FinancePersonal FinanceRetirement PlanningRetirement Planning

Bear MarketBear Market:: a trend in the stock market in which a trend in the stock market in which prices are falling over several months; investors prices are falling over several months; investors who make decisions based on a belief that the who make decisions based on a belief that the market is going to continue downward are called market is going to continue downward are called “bears” or are said to be “bearish” on the market.“bears” or are said to be “bearish” on the market.

Bull MarketBull Market:: a trend in the stock market in which a trend in the stock market in which prices are rising over several months; investors prices are rising over several months; investors who make decisions on a belief that the market who make decisions on a belief that the market is trending upward are called “bulls” or are said is trending upward are called “bulls” or are said to be “bullish” on the market.to be “bullish” on the market.

1717

Retirement Planning Fact Sheet Retirement Planning Fact Sheet Many estimate that a person should plan on utilizing about 80 percent of their Many estimate that a person should plan on utilizing about 80 percent of their pre-retirement income in order to live in a manner to which they’ve grown pre-retirement income in order to live in a manner to which they’ve grown accustomed. Following are some basic means of planning for retirement years.accustomed. Following are some basic means of planning for retirement years.

Social SecuritySocial Security: June 8, 1934, President Franklin D. Roosevelt, announced his : June 8, 1934, President Franklin D. Roosevelt, announced his intention to provide a program for a social insurance plan similar to those that intention to provide a program for a social insurance plan similar to those that began in Europe in the 19th century and first adopted in Germany in 1889 under began in Europe in the 19th century and first adopted in Germany in 1889 under the leadership of Chancellor Otto von Bismarck. the leadership of Chancellor Otto von Bismarck.

Under Roosevelt’s plan, the U.S. began social security payments of monthly Under Roosevelt’s plan, the U.S. began social security payments of monthly benefits in January 1940, authorized for aged male retired workers, their aged benefits in January 1940, authorized for aged male retired workers, their aged wives or widows, any children under age 18 and surviving aged parents. wives or widows, any children under age 18 and surviving aged parents.

Since then, Disability, Medicare, and Supplemental Security Income (SSI) Since then, Disability, Medicare, and Supplemental Security Income (SSI) programs have been added to the entitlements offered through the Social programs have been added to the entitlements offered through the Social Security AdministrationSecurity Administration. . [1][1]

Social Security is an Social Security is an unfunded pension planunfunded pension plan, paid for with cash flows from , paid for with cash flows from individuals currently taxed to cover the payments to those receiving benefits. individuals currently taxed to cover the payments to those receiving benefits. Social Security Benefits Calculators: Social Security Benefits Calculators: To calculate your own Social Security To calculate your own Social Security benefits, access the Social Security Online “Benefits Calculators” at benefits, access the Social Security Online “Benefits Calculators” at http://www.ssa.gov/planners/calculators.htmhttp://www.ssa.gov/planners/calculators.htm

[1][1] For more information, see the Social Security Administrations website at: http://www.ssa.gov/history/briefhistory3.html For more information, see the Social Security Administrations website at: http://www.ssa.gov/history/briefhistory3.html

1818

Retirement Planning Fact SheetRetirement Planning Fact Sheet 401K Plans401K Plans: Employer-sponsored retirement plans in which : Employer-sponsored retirement plans in which

employees defer a portion of their salary into an investment employees defer a portion of their salary into an investment choice, usually selecting from several options. Employers choice, usually selecting from several options. Employers often contribute to the employee’s 401k by matching a portion often contribute to the employee’s 401k by matching a portion of the investment. of the investment. For example if an individual invests 5% of his or her income, For example if an individual invests 5% of his or her income,

the employer may also match that up to 5%. If the person the employer may also match that up to 5%. If the person put in 10% of his or her income into a 401K plan, his or her put in 10% of his or her income into a 401K plan, his or her initial investment would actually be a 15% contribution with initial investment would actually be a 15% contribution with the 5% match.the 5% match.

Investment options may include stocks (including the Investment options may include stocks (including the company’s stock), bonds and money market funds. company’s stock), bonds and money market funds.

All of the funds in the 401k are allowed to increase tax-free All of the funds in the 401k are allowed to increase tax-free and may be withdrawn when the employee reaches age 59 and may be withdrawn when the employee reaches age 59 ½. When withdrawn, income tax must be paid on the funds. ½. When withdrawn, income tax must be paid on the funds.

For nonprofit organizations, such plans are referred to as For nonprofit organizations, such plans are referred to as 403B Plans.403B Plans.

1919

Retirement Planning Fact SheetRetirement Planning Fact Sheet Individual Retirement Account (IRA):Individual Retirement Account (IRA): There are There are

two predominant types of individual retirement two predominant types of individual retirement accounts, the Traditional IRA and the Roth IRA. accounts, the Traditional IRA and the Roth IRA. Traditional IRATraditional IRA: a tax deductible option—that is, the : a tax deductible option—that is, the

contribution you make is not taxed as income until you contribution you make is not taxed as income until you withdraw funds. withdraw funds.

Roth IRARoth IRA: named for Senator William V. Roth, Jr. of : named for Senator William V. Roth, Jr. of Delaware, became effective in 1998. A Roth IRA is one Delaware, became effective in 1998. A Roth IRA is one in which your contributions are made after the taxes on in which your contributions are made after the taxes on it are already paid. Money earned on it is tax free, it are already paid. Money earned on it is tax free, meaning that no taxes are due on the funds withdrawn meaning that no taxes are due on the funds withdrawn from it as long as the IRA has been open five years or from it as long as the IRA has been open five years or longer and the holder is at least 59 ½ years old.longer and the holder is at least 59 ½ years old.

2020

Retirement Planning Fact SheetRetirement Planning Fact Sheet

Mutual FundsMutual Funds: There are an estimated 12,000 or more : There are an estimated 12,000 or more different mutual funds in which an individual may invest different mutual funds in which an individual may invest for retirement. Mutual funds allow a group of investors to for retirement. Mutual funds allow a group of investors to pool their money which is managed by a fund manager pool their money which is managed by a fund manager who invests in specific securities, usually stocks or who invests in specific securities, usually stocks or bonds. bonds. Investing in a mutual fund is actually purchasing shares or units Investing in a mutual fund is actually purchasing shares or units

of the mutual fund. of the mutual fund. Pooling money in a mutual fund allows an investor to diversify Pooling money in a mutual fund allows an investor to diversify

money across several types of investments, providing greater money across several types of investments, providing greater protection against loss should a single company’s stock plunge. protection against loss should a single company’s stock plunge.

Mutual funds allow buyers to purchase stocks or bonds at lower Mutual funds allow buyers to purchase stocks or bonds at lower trading costs than buying and trading individually.trading costs than buying and trading individually.

2121

Personal Finance: Check 21Personal Finance: Check 21

Check FloatingCheck Floating: the practice of issuing a check before the : the practice of issuing a check before the funds are actually deposited in the account; individuals who funds are actually deposited in the account; individuals who float their checks, do so believing they will be able to make float their checks, do so believing they will be able to make the needed deposit before the check clears.the needed deposit before the check clears.

Check KitingCheck Kiting: a type of fraud in which money is drawn from a : a type of fraud in which money is drawn from a bank account that does not have sufficient funds and to cover bank account that does not have sufficient funds and to cover it, a second check is drawn from another checking account. In it, a second check is drawn from another checking account. In some cases, there is no money in the second account either some cases, there is no money in the second account either but the scheme operates in hope that the “lag” allows them to but the scheme operates in hope that the “lag” allows them to draw on the account before the check is cleared.draw on the account before the check is cleared.

Check 21Check 21: Check 21 is a federal law, passed on October 28, : Check 21 is a federal law, passed on October 28, 2004. Designed to speed up the check clearing process, it 2004. Designed to speed up the check clearing process, it allows banks to discard the paper check and substitute an allows banks to discard the paper check and substitute an electronic check. This allows the bank to debit your account electronic check. This allows the bank to debit your account for the amount within minutes of them receiving your check. for the amount within minutes of them receiving your check.

2222

Personal FinanceUsury and Interest: A Christian Perspective

Psalm 15 outlines principles which should characterize the believer. One of the Psalm 15 outlines principles which should characterize the believer. One of the prohibitions given is the charging of usury. Some translations simply refer to interest. prohibitions given is the charging of usury. Some translations simply refer to interest. Usury is charging exorbitant interest rates above what is customary or reasonable. Usury is charging exorbitant interest rates above what is customary or reasonable.

Deuteronomy 23:19 states: “Do not charge your brother interest on money, food, or Deuteronomy 23:19 states: “Do not charge your brother interest on money, food, or anything that can earn interest.” Nehemiah was particularly incensed when it was anything that can earn interest.” Nehemiah was particularly incensed when it was discovered that the Jews were not abiding by this prohibition (See Nehemiah 5:7-11). discovered that the Jews were not abiding by this prohibition (See Nehemiah 5:7-11). In addition to Psalm 15:4-6 and the passages from Deuteronomy and Nehemiah, In addition to Psalm 15:4-6 and the passages from Deuteronomy and Nehemiah, other references to this prohibition include: Exodus 22:25; Leviticus 25:37; Ezekiel other references to this prohibition include: Exodus 22:25; Leviticus 25:37; Ezekiel 18:7-9; Esekiel 18:12-14 and Ezekial 22:12. 18:7-9; Esekiel 18:12-14 and Ezekial 22:12.

Prohibition against interest does not seem to hold when dealing with those outside Prohibition against interest does not seem to hold when dealing with those outside the family of faith however. Deuteronomy 23:20 states: “You may charge a foreigner the family of faith however. Deuteronomy 23:20 states: “You may charge a foreigner interest, but you must not charge your brother interest, so that the LORD your God interest, but you must not charge your brother interest, so that the LORD your God may bless you in everything you do in the land you are entering to possess.” may bless you in everything you do in the land you are entering to possess.”

Usury is always prohibited. For example, "You must not exploit a foreign resident or Usury is always prohibited. For example, "You must not exploit a foreign resident or oppress him, since you were foreigners in the land of Egypt” (Exodus 22: 21). Even in oppress him, since you were foreigners in the land of Egypt” (Exodus 22: 21). Even in dealing with “strangers” or “foreigners,” the Jews were commanded to be fair in dealing with “strangers” or “foreigners,” the Jews were commanded to be fair in charging interest on loans.charging interest on loans.

The New Testament refers to the collection of interest on money deposited with a The New Testament refers to the collection of interest on money deposited with a bank or lender. But are the parables in which this is mentioned meant to condone the bank or lender. But are the parables in which this is mentioned meant to condone the practice? After all, the parables were not about interest or usury. In Matthew 5:42, practice? After all, the parables were not about interest or usury. In Matthew 5:42, Jesus urges His followers to lend to whoever asks for a loan. Should the Christian Jesus urges His followers to lend to whoever asks for a loan. Should the Christian refrain from charging interest? refrain from charging interest?

2323

Personal FinanceUsury and Interest: A Christian Perspective

General Guidelines:General Guidelines:

Neither lending nor borrowing is specifically condemned Neither lending nor borrowing is specifically condemned in the Bible. Jesus taught His followers (Matthew 5:42): in the Bible. Jesus taught His followers (Matthew 5:42): “Give to the one who asks you, and don't turn away from “Give to the one who asks you, and don't turn away from the one who wants to borrow from you.” Christians may the one who wants to borrow from you.” Christians may lend to anyone as in Luke 6:34-35: “And if you lend to lend to anyone as in Luke 6:34-35: “And if you lend to those from whom you expect to receive, what credit is those from whom you expect to receive, what credit is that to you? Even sinners lend to sinners to be repaid in that to you? Even sinners lend to sinners to be repaid in full. But love your enemies, do [what is] good, and lend, full. But love your enemies, do [what is] good, and lend, expecting nothing in return. Then your reward will be expecting nothing in return. Then your reward will be great, and you will be sons of the Most High. For He is great, and you will be sons of the Most High. For He is gracious to the ungrateful and evil.” gracious to the ungrateful and evil.”

2424

Personal FinanceUsury and Interest: A Christian Perspective

In making a loan, Christians should not charge In making a loan, Christians should not charge interest on loans made to other Christians. This interest on loans made to other Christians. This would keep with the general teaching of Scripture and would keep with the general teaching of Scripture and is consistent with teachings in both the Old and New is consistent with teachings in both the Old and New Testament. Testament.

2525

Personal FinanceUsury and Interest: A Christian Perspective

In the practice of lending, it can be argued that In the practice of lending, it can be argued that charging interest on a loan made to a non-believer is charging interest on a loan made to a non-believer is permissible, but that under no circumstance should permissible, but that under no circumstance should the interest be outside of normal, accepted rates. the interest be outside of normal, accepted rates. Usury is prohibited in the practice of lending in all Usury is prohibited in the practice of lending in all situations. situations.

2626

Personal FinanceUsury and Interest: A Christian Perspective

These principles are intended primarily for individual These principles are intended primarily for individual believers in their personal decision making. They believers in their personal decision making. They may not directly apply to an institution such as a bank may not directly apply to an institution such as a bank or mortgage company in which a person is employed or mortgage company in which a person is employed and made responsible for granting loans. In such a and made responsible for granting loans. In such a case, the Christian is not making decisions to lend case, the Christian is not making decisions to lend from his or her personal supply, but on behalf of a from his or her personal supply, but on behalf of a corporation; they are investing the money of others. corporation; they are investing the money of others. There appears to be no prohibition for a Christian There appears to be no prohibition for a Christian working at a bank to make a loan consistent with the working at a bank to make a loan consistent with the rules and regulations set forth by their employer, state rules and regulations set forth by their employer, state and professional codes of conduct, and as long as the and professional codes of conduct, and as long as the employer is not using unethical practices or charging employer is not using unethical practices or charging usury. usury.

2727

Setting Your Personal Financial House in Order Setting Your Personal Financial House in Order

Discussion QuestionsDiscussion Questions What is the difference between gross income What is the difference between gross income

and NSI?and NSI? Describe and differentiate between the four Describe and differentiate between the four

retirement planning options outlined in the retirement planning options outlined in the chapter.chapter.

Define check kiting; check floating; and Check Define check kiting; check floating; and Check 21.21.

Describe the major types of insurance discussed Describe the major types of insurance discussed in the chapter.in the chapter.

Briefly describe why the practice of making the Briefly describe why the practice of making the minimum monthly payment on a credit card debt minimum monthly payment on a credit card debt is poor stewardship.is poor stewardship.

2828

Setting Your Personal Financial House in Order Setting Your Personal Financial House in Order

ActivitiesActivities Construct a personal budget for you or your family. Construct a personal budget for you or your family.

Check it against the budget guideline in the text. Point Check it against the budget guideline in the text. Point out any significant changes in your percentages and in out any significant changes in your percentages and in one to two sentences describe your reasoning for each one to two sentences describe your reasoning for each line item.line item.

Use the formula for present value to calculate the amount Use the formula for present value to calculate the amount of money you need to invest right now in order to have of money you need to invest right now in order to have $50,000 in ten years. Assume a six percent interest rate.$50,000 in ten years. Assume a six percent interest rate.

Use the Replacement Income Table from Motley Fool to Use the Replacement Income Table from Motley Fool to identify the recommended insurance needs for the identify the recommended insurance needs for the following individuals (assume a retirement age of 65):following individuals (assume a retirement age of 65):

a. a 25 year-old who makes $30,000 per year;a. a 25 year-old who makes $30,000 per year;b. a 40 year-old who makes $85,000 per year;b. a 40 year-old who makes $85,000 per year;c. a 50 year-old who makes $120,000 per year.c. a 50 year-old who makes $120,000 per year.

2929

Setting Your Personal Financial House in Order Setting Your Personal Financial House in Order

Integrating Faith and DisciplineIntegrating Faith and Discipline Read the short chapter notes on usury and interest. In Read the short chapter notes on usury and interest. In

your opinion, should a Christian charge another Christian your opinion, should a Christian charge another Christian interest on a loan? What about charging a non-interest on a loan? What about charging a non-Christian? Relative to deciding whether to charge a non-Christian? Relative to deciding whether to charge a non-Christian interest, what are some guidelines to consider? Christian interest, what are some guidelines to consider?

Explore the website of Crown Financial Ministries Explore the website of Crown Financial Ministries (www.crown.org). Select an article about personal (www.crown.org). Select an article about personal financial planning and write a one-page summary of the financial planning and write a one-page summary of the article in a memorandum format.article in a memorandum format.