Embed Size (px)

Citation preview

Chapter 8

The Efficient Market

Hypothesis

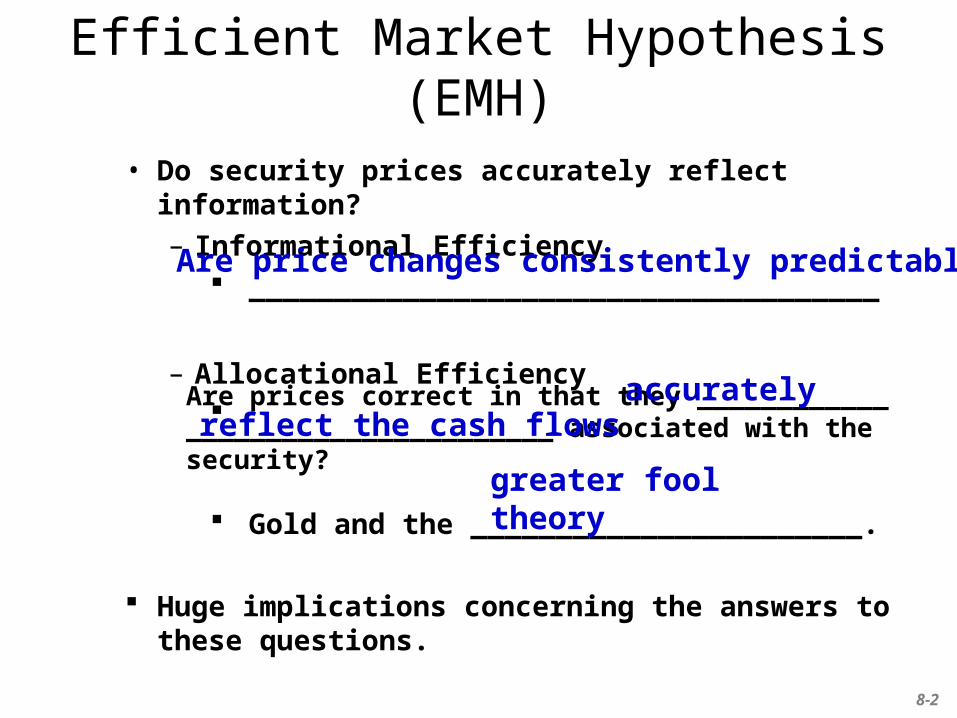

Efficient Market Hypothesis (EMH)• Do security prices accurately reflect information?

– Informational Efficiency _____________________________________

– Allocational Efficiency

Gold and the _______________________.

Huge implications concerning the answers to these questions.

greater fool theory

8-2

Are price changes consistently predictable?

Are prices correct in that they ____________ _______________________ associated with the security?

accuratelyreflect the cash flows

Implications of efficiency

8-3

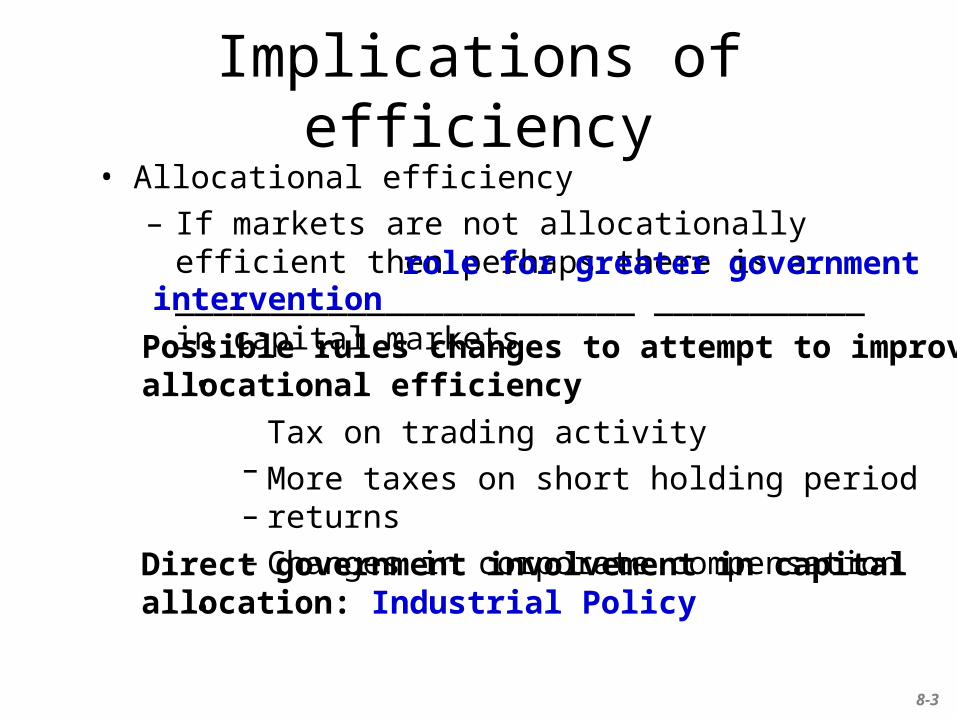

• Allocational efficiency– If markets are not allocationally efficient then

perhaps there is a ________________________ ___________ in capital markets.

•

– – –

•

role for greater government intervention

Possible rules changes to attempt to improve allocational efficiency

Tax on trading activity

More taxes on short holding period returns

Changes in corporate compensationDirect government involvement in capital allocation: Industrial Policy

Implications of efficiency

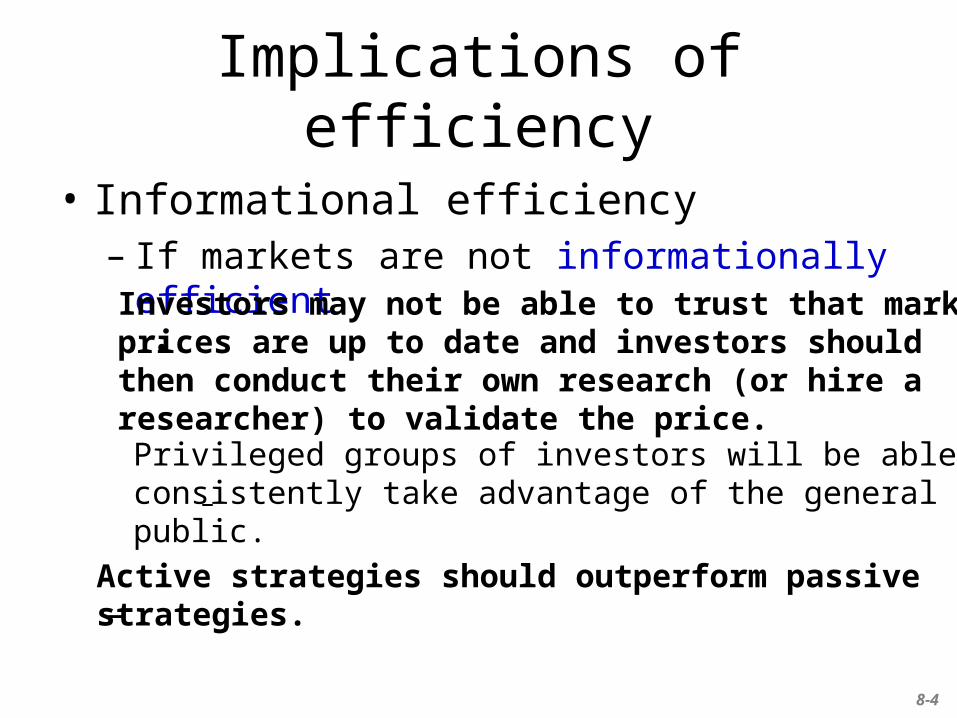

• Informational efficiency– If markets are not informationally efficient

•

–

–

Investors may not be able to trust that market prices are up to date and investors should then conduct their own research (or hire a researcher) to validate the price.

Privileged groups of investors will be able to consistently take advantage of the general public.

Active strategies should outperform passive strategies.

8-4

Implications of efficiency

• Informational efficiency– If markets are not informationally efficient

•

–

–

Maximize shareholder wealth maximize share price, so how does one go about maximizing shareholder wealth in this case?

Lack a benchmark to evaluate corporate decisions.

Corporations have to rethink their goals and how best to achieve them.

8-5

EMH and Competition

•

•

•

Competition among investors should imply that stock prices fully and accurately reflect publicly available information very quickly. Why?

Else there are unexploited profit opportunities.

Once information becomes available, market participants quickly analyze it & trade on it & frequent, low cost trading assures prices reflect information.

Questions arise about efficiency due to:

• Unequal access to information

• Structural market problems

• Psychology of investors (Behavioralism)8-6

• Why are price changes random?–

– –

Random Price Changes

In very competitive markets prices should react to only NEW information

Flow of NEW information is random

Therefore, price changes are random (submartingale process)Random Walk with Positive Trend

Idea that stock prices follow a “Random Walk” or Market is Efficient

8-7

Forms of the EMH• Prices reflect all relevant information• Vary the ________________

– WeakThe relevant information is historical prices and other trading data such as trading volume. If the markets are weak form efficient, use of such information provides no benefit “at the margin.”

information set

8-8

Forms of the EMH– Semi-strong

The relevant information is "all publicly available information, including past price and volume data."

If the markets are semi-strong form efficient, then studying past price and volume data & studying earnings and growth forecasts provides no net benefit in predicting price changes at the margin.

8-9

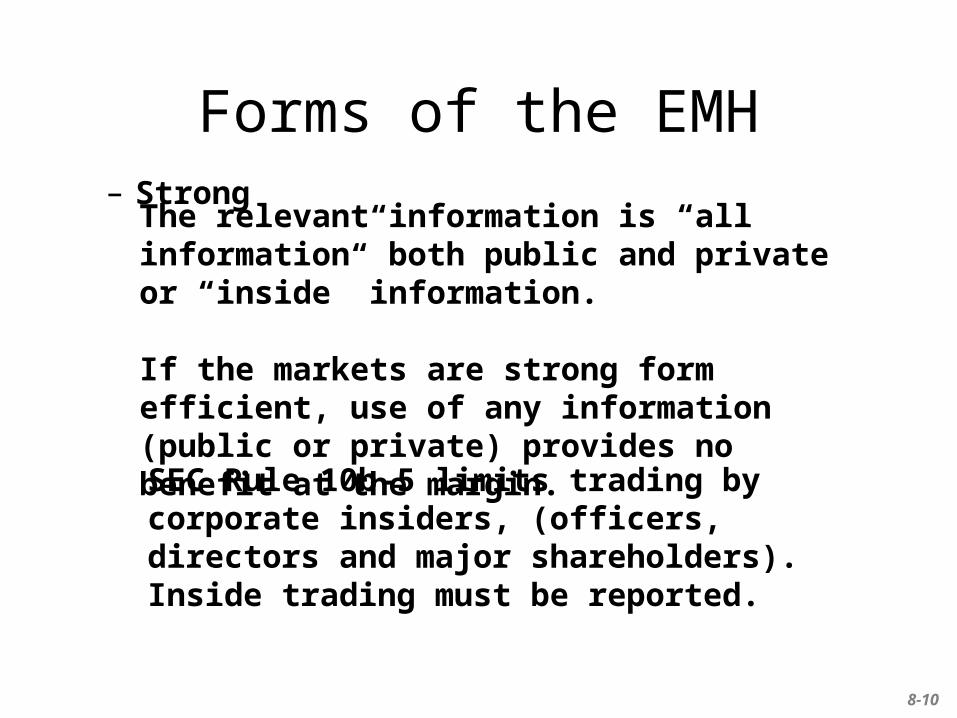

Forms of the EMH– Strong

The relevant information is “all information” both public and private or “inside” information.

If the markets are strong form efficient, use of any information (public or private) provides no benefit at the margin.

SEC Rule 10b-5 limits trading by corporate insiders, (officers, directors and major shareholders). Inside trading must be reported.

8-10

Types of Stock Analysis & Relationship to the EMH

• Technical Analysis:

– If the markets are weak form efficient or semi-strong form efficient or strong form efficient will technical analysis be able to consistently predict price changes? NO +

However

Technical Analysis or TA is using prices and volume information to predict future price changes

TA assumes prices follow predictable trends

8-11

Fundamental Analysis

• Fundamental analysis assumes that stock prices should be equal to

• Fundamental analysis is thus the

the discounted value of the expected future cash flows the stock is expected to provide to investors.

“art” of identifying over- and undervalued securities based on an analysis of the firm's financial statements and future prospects.

8-12

Fundamental Analysis• If the estimated price is ______ than the current price

an investor should ___ the stock since it is ___________ and since its price should ________ to the "true" or "fundamental" value uncovered by the analyst.

• If the estimated price is ____ than the current price the stock should be ____ because the stock is currently __________ by the market.

• In either case if the analyst is correct the investor should receive an ________________.

undervalued increasebuy

greater

lesssold

overvalued

“abnormal return”

8-13

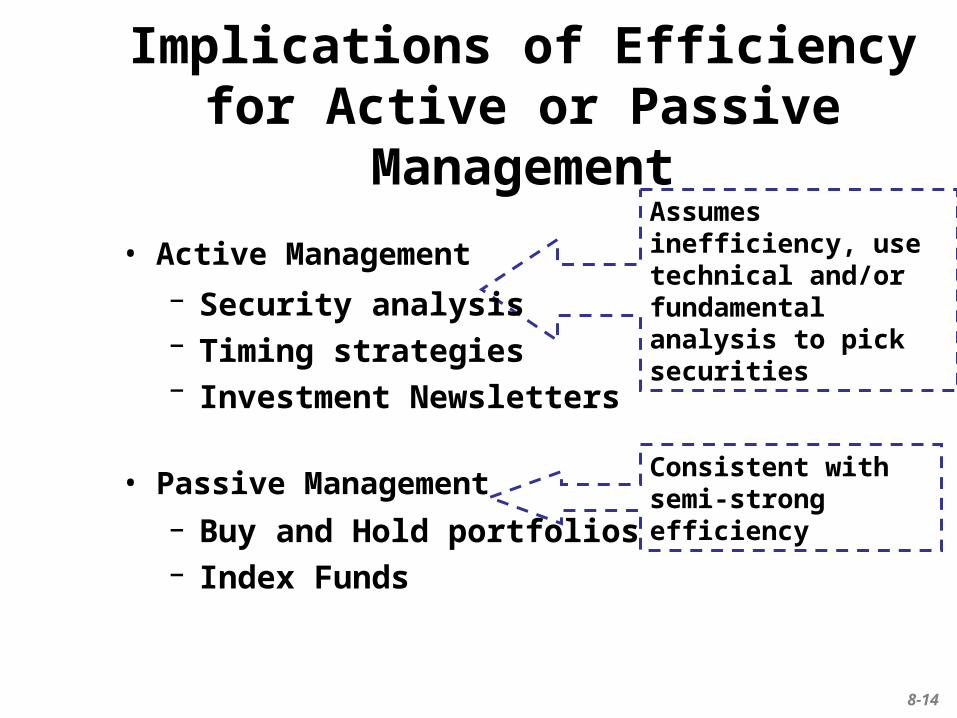

• Active Management– – –

• Passive Management– –

Implications of Efficiency for Active or Passive Management

Assumes inefficiency, use technical and/or fundamental analysis to pick securitiesSecurity analysis

Timing strategies

Investment Newsletters

Buy and Hold portfolios

Index Funds

Consistent with semi-strong efficiency

8-14

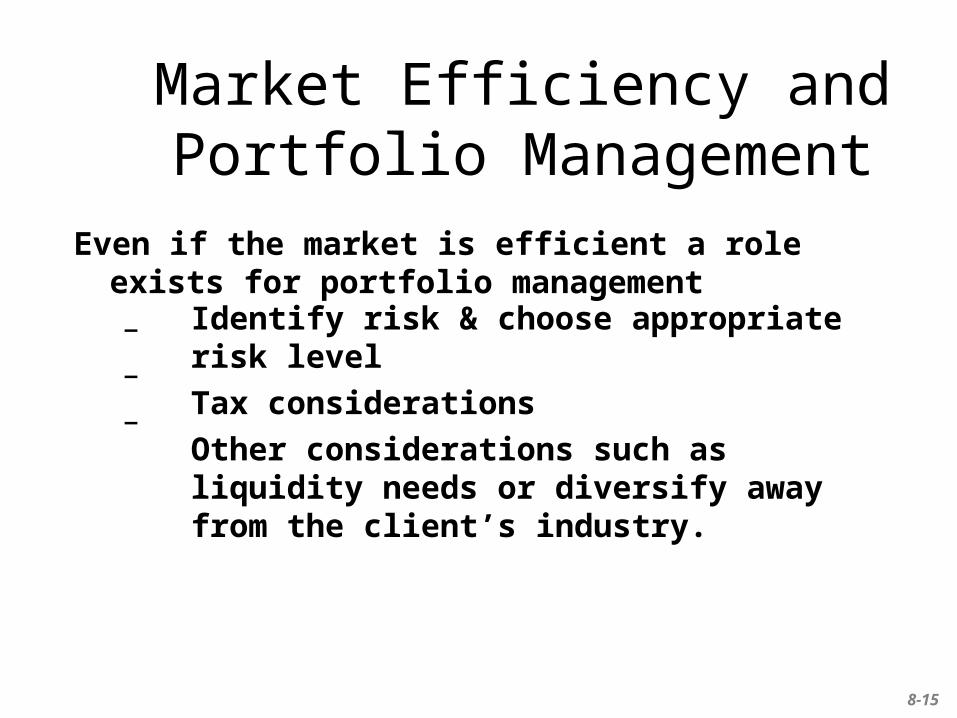

Even if the market is efficient a role exists for portfolio management– – –

Market Efficiency and Portfolio Management

Identify risk & choose appropriate risk level

Tax considerations

Other considerations such as liquidity needs or diversify away from the client’s industry.

8-15

8.3 Are Markets Efficient?

8-16

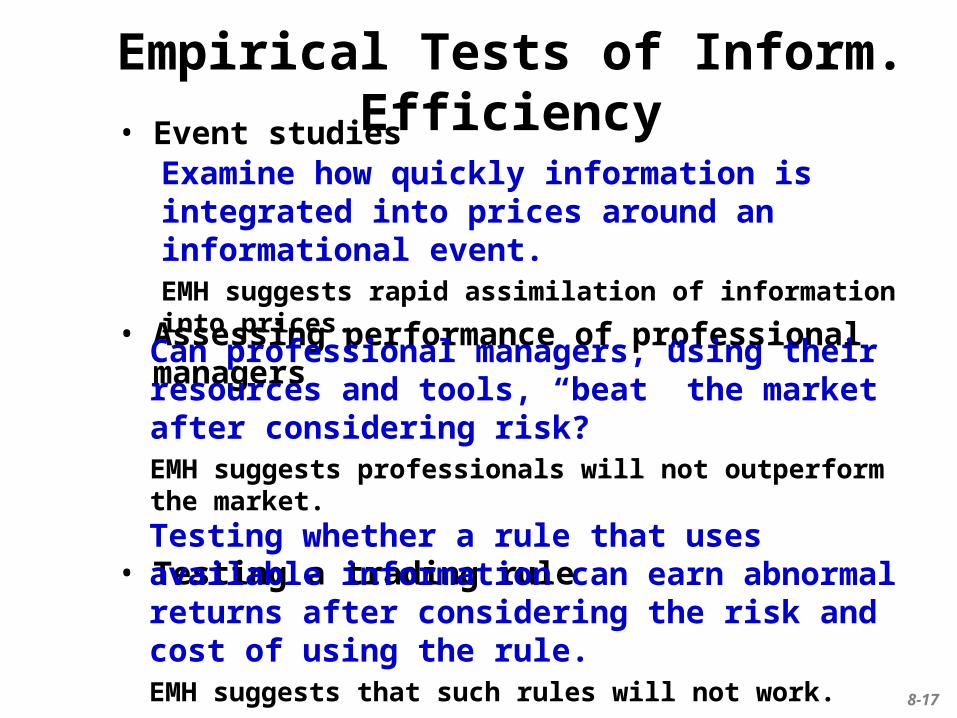

• Event studies

• Assessing performance of professional managers

• Testing a trading rule

Empirical Tests of Inform. Efficiency

Examine how quickly information is integrated into prices around an informational event.EMH suggests rapid assimilation of information into prices.

Can professional managers, using their resources and tools, “beat” the market after considering risk?EMH suggests professionals will not outperform the market.

Testing whether a rule that uses available information can earn abnormal returns after considering the risk and cost of using the rule.EMH suggests that such rules will not work.

8-17

• Magnitude Issue

Issues in Examining the Results

Even _____________________________ may be worthwhile for managers of large investments.

Eg.

The problem is that these __________________________ would be _________________ to measure since the standard deviation of many portfolios ______________.

small changes in performance

$5 billion dollar portfolio. Use research to improve results by 1/10 of a percent per year = $5 million in value.

small changes in performancevirtually impossible

is 20% or more

8-18

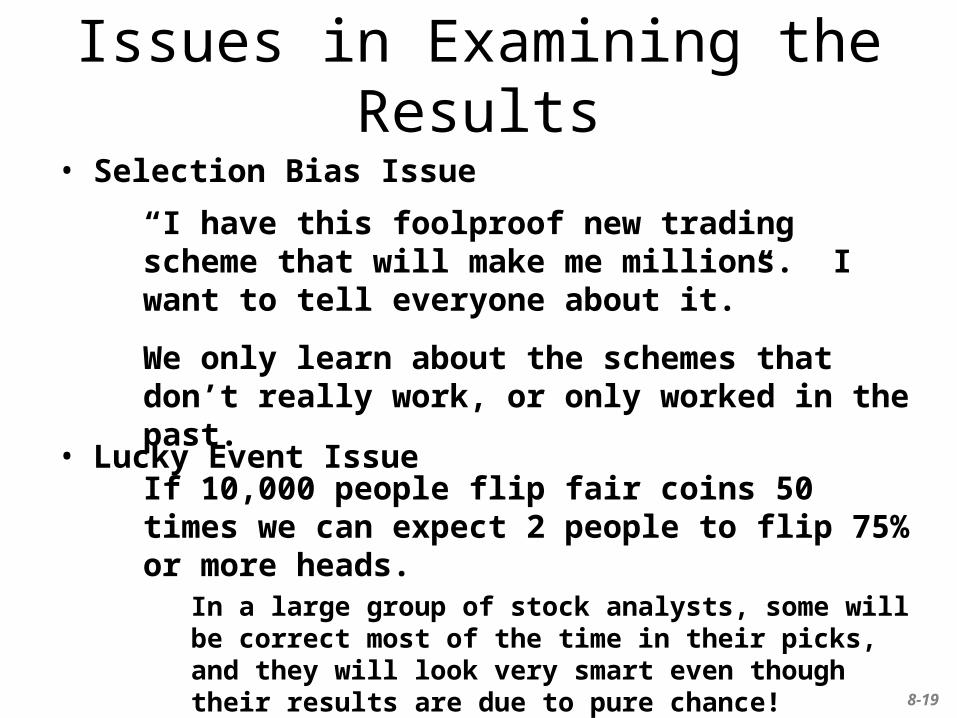

• Selection Bias Issue

• Lucky Event Issue

Issues in Examining the Results

“I have this foolproof new trading scheme that will make me millions. I want to tell everyone about it.”

We only learn about the schemes that don’t really work, or only worked in the past.

If 10,000 people flip fair coins 50 times we can expect 2 people to flip 75% or more heads.

In a large group of stock analysts, some will be correct most of the time in their picks, and they will look very smart even though their results are due to pure chance!

8-19

Counter Evidence: Some Apparent Predictors of Broad Market Returns

• Fama and French–

• Campbell and Shiller–

• Keim and Stambaugh–

Aggregate returns tend to be higher for firms with higher dividend yields

Aggregate returns tend to be higher for firms with higher earnings yields

Changes in bond credit spreads can predict market returns

Each of these may also be consistent with changing risk premiums and may have nothing to say about market efficiency.

8-20

Bubbles and Market Efficiency

Periodically stock prices appear to undergo a ‘speculative bubble.’

A speculative bubble is said to occur if prices do not equal the intrinsic value of the security.

Does this imply that markets are not efficient?

– Very difficult to predict if you are in a bubble and when the bubble will burst.

– Stock prices are estimates of future economic performance of the firm and these estimates can change rapidly.

– Risk premiums can change rapidly and dramatically.

8-21

Bubbles and Market Efficiency

With hindsight there appear to be times when stock prices decouple from intrinsic or fundamental value, sometimes for years.

• Prices eventually conform to intrinsic value.

• Brings into question the allocational efficiency of the markets more than the informational efficiency.

• What capital allocation mechanism is likely to perform better than the market based system?

8-22

Mutual Fund and Professional Manager Performance

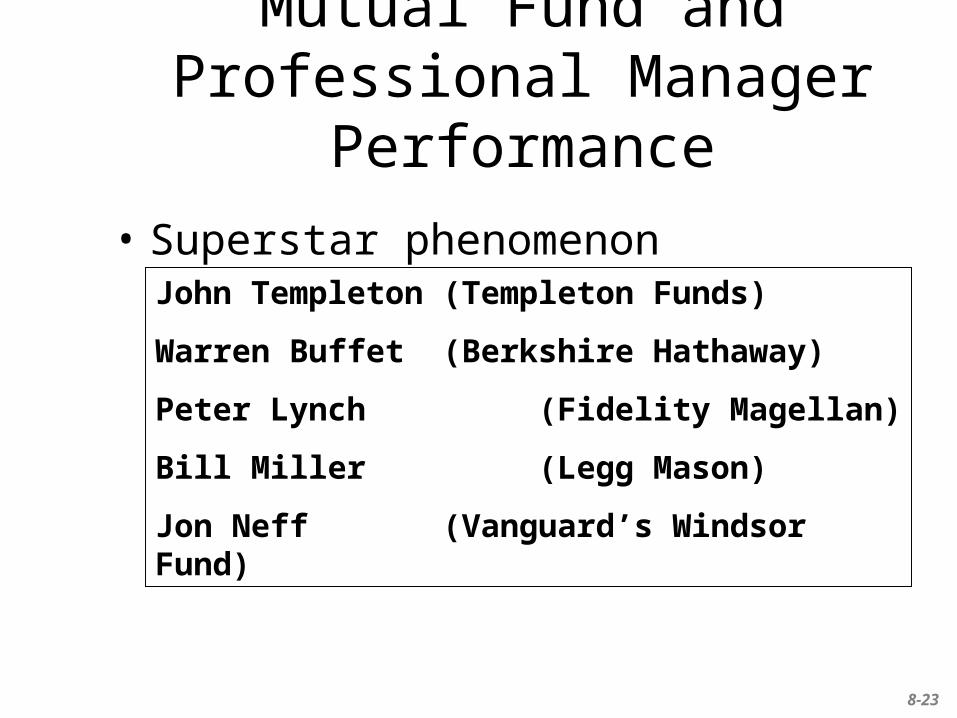

• Superstar phenomenon John Templeton (Templeton Funds)

Warren Buffet (Berkshire Hathaway)

Peter Lynch (Fidelity Magellan)

Bill Miller (Legg Mason)

Jon Neff (Vanguard’s Windsor Fund)

8-23

• Technical Analysis (TA)

Summary: What Does the Evidence

Show?

Stocks do not follow a pure random walk, so there is hope for technical trading strategies.

Most TA rules utilize short term trading strategies that generate excessive transaction costs and are not profitable.

There appears to be some long term trend reversals.

8-24

• Fundamental Analysis

Summary: What Does the Evidence

Show?

Appears to be difficult to consistently generate abnormal returns using fundamental analysis.

This is because the analysis/investment industry is so competitive and volatility is high.

May help you avoid seriously overvalued investments.

8-25

• Fundamental Analysis

Summary: What Does the Evidence

Show?

The Conundrum:

Without fundamental analysis the markets would surely be inefficient, &

Abnormal profit opportunities would exist,

Leading to profitable fundamental analysis

Grossman & Stiglitz AER, 1980

8-26

• Anomalies Exist– – – –

Summary: What Does the Evidence

Show?

Small Firm in January Effect

Book to Market Ratios

Long Term Reversals

Post-Earnings Announcement Drift (Momentum)

8-27

Behavioralism bias

• MotivationStock prices in the 1990s did not appear to match “fundamentals,” e.g., high price earnings ratios

Evidence of refusal to sell losers

Economics discipline is exploring behavioral aspects of decision making

8-28

What does it all mean?

• Technical Analysis:

• Your choices–

• –

• •

–

It may be an item in your toolkit but be careful relying on it too much.

Pick stocks yourself, based on fundamental analysis, but diversify

Beat and/or avoid the competition.

Pick one or more mutual fundsUnlikely to consistently earn + abnormal returns

Pros paying attention to market and firm conditions

Index or otherwise passively diversify.8-29

Problem 1

• Zero, otherwise returns from the prior period could be used to predict returns in the subsequent period.

8-30

Problem 2

• No. Why?

• One would have to show that Intel investors earned a higher rate of return than they should have for the risk taken. – Many investors bought Intel only after its

success was evident.– By chance some stocks will perform extremely

well.

8-31

Problem 3

• No, Why?

• It does not indicate investors are failing to consider current information in the price, nor does it present an abnormal return opportunity.

• It could indicate information leakage or it could indicate that splits occur during price runups.

8-32

Problem 4

• No, Why?

• You won’t get + abnormal returns if the economic cycle is predictable, the news will already be incorporated in the stock’s price.

8-33

Problem 5

• Buy it

• This is a “Value Investment” where you believe the stock will perform better than the market and if you are correct you will earn a positive abnormal return.

8-34

Problem 7

a. Consistent, expect about half to outperform the market by chance

b. Violation, earn + AR by investing with last year’s winners• Probably consistent, but it depends. I might be able to use an

option strategy to take advantage of this.• Violation, you have exploitable price momentum persisting into

February• Violation, the reversal offers an exploitable opportunity, namely buy

last week’s losers

8-35

Problem 8

i. Implicit in the dollar-cost averaging strategy is the notion that stock prices fluctuate around a “normal” level. Otherwise, there is no meaning to statements such as: “when the price is high.”

ii. How do we know, for example, whether a price of $25 today will be viewed as high or low compared to the stock price six months from now?

8-36

Problem 9

The market expected earnings to increase by more than they actually did.

8-37