Embed Size (px)

Citation preview

Chapter 8Chapter 8

Taxation of IndividualsTaxation of Individuals

©2009 South-Western, a part of Cengage Learning©2009 South-Western, a part of Cengage Learning©2009 South-Western, a part of Cengage Learning©2009 South-Western, a part of Cengage Learning

Kevin MurphyKevin MurphyMark HigginsMark Higgins

Kevin MurphyKevin MurphyMark HigginsMark Higgins

8-28-22009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Taxation of IndividualsTaxation of Individuals

Individuals are the biggest single

group of taxpaying entities.

As taxpaying entities, they must adopt an annual accounting period

and method of accounting.

8-38-32009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Review of Tax FormulaReview of Tax Formula

The formula for calculating taxable income generally is gross income minus allowable deductions.

For individuals, deductions are split into two classesDeductions for adjusted gross incomeDeductions from adjusted gross income

8-48-42009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

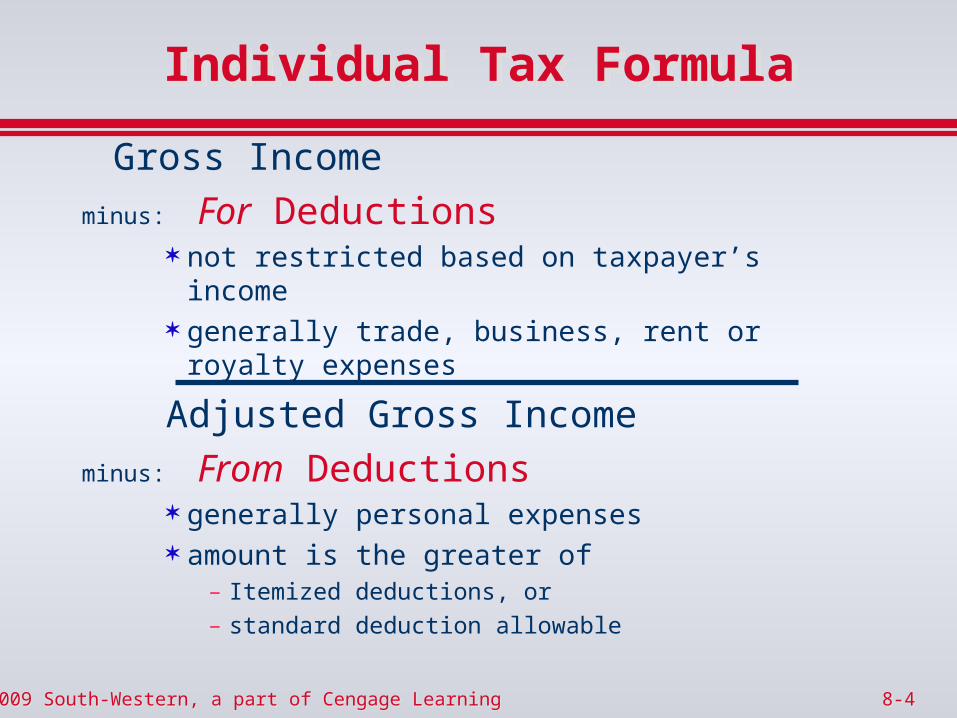

Individual Tax FormulaIndividual Tax Formula

Gross Income

minus: For Deductions not restricted based on taxpayer’s income generally trade, business, rent or royalty

expenses

Adjusted Gross Income

minus: From Deductions generally personal expenses amount is the greater of

– Itemized deductions, or

– standard deduction allowable

8-58-52009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Individual Tax FormulaContinued

Individual Tax FormulaContinued

Adjusted Gross Income [AGI]

minus: From Deductions

minus: Personal & Dependency Exemptions

• $3,500 per person

8-68-62009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Individual Tax FormulaTo Taxable Income

Individual Tax FormulaTo Taxable Income

Gross Income

minus: For Deductions

equals: Adjusted Gross Income [AGI]

minus: From Deductions

minus: Exemptions

equals: Taxable Income

8-78-72009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

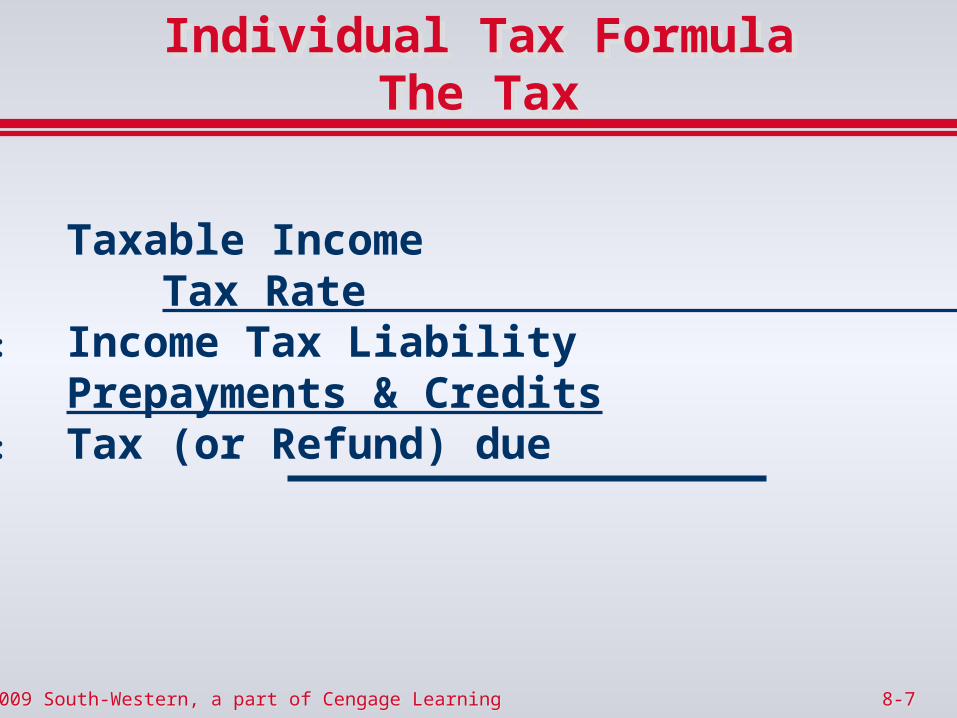

Individual Tax FormulaThe Tax

Individual Tax FormulaThe Tax

Taxable Incometimes: Tax Rate equals: Income Tax Liabilityminus: Prepayments & Creditsequals: Tax (or Refund) due

8-88-82009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

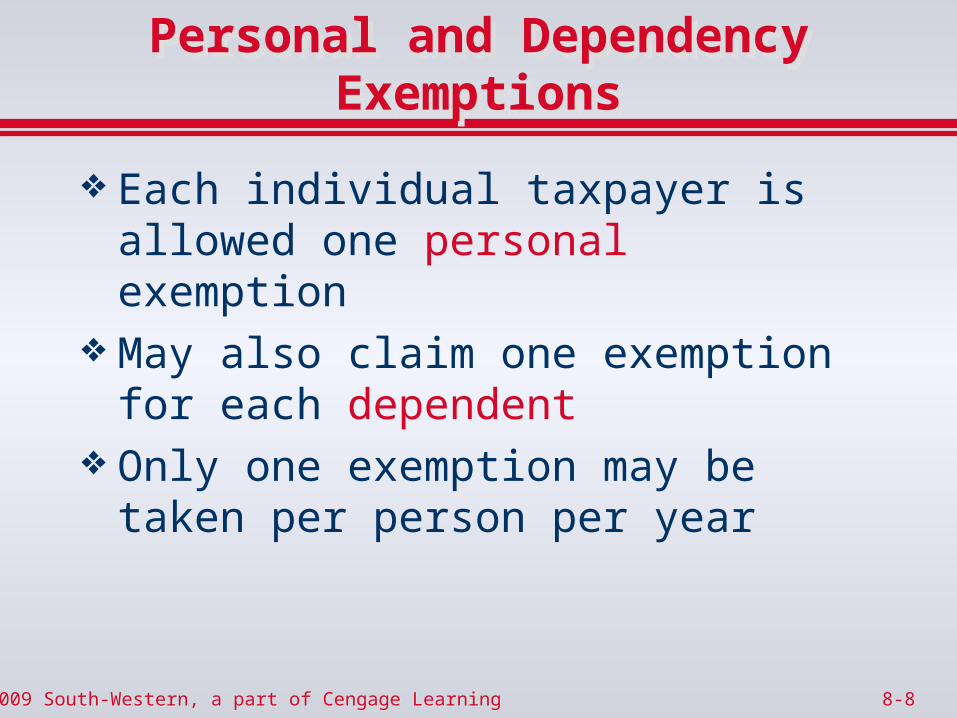

Personal and Dependency Exemptions

Personal and Dependency Exemptions

Each individual taxpayer is allowed one personal exemption

May also claim one exemption for each dependent

Only one exemption may be taken per person per year

8-98-92009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

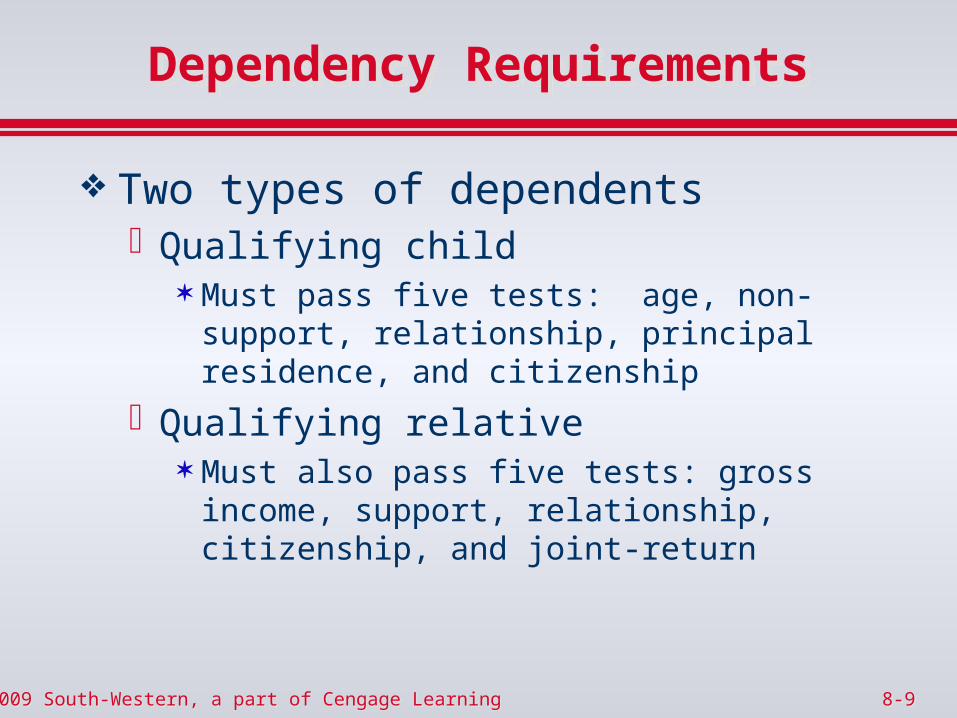

Dependency RequirementsDependency Requirements

Two types of dependentsQualifying child

Must pass five tests: age, non-support, relationship, principal residence, and citizenship

Qualifying relative Must also pass five tests: gross income,

support, relationship, citizenship, and joint-return

8-108-102009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Qualifying Child TestsQualifying Child Tests

Age Test – Must beyounger than 19, or a full-time student younger than 24, orPermanently and totally disabled

8-118-112009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

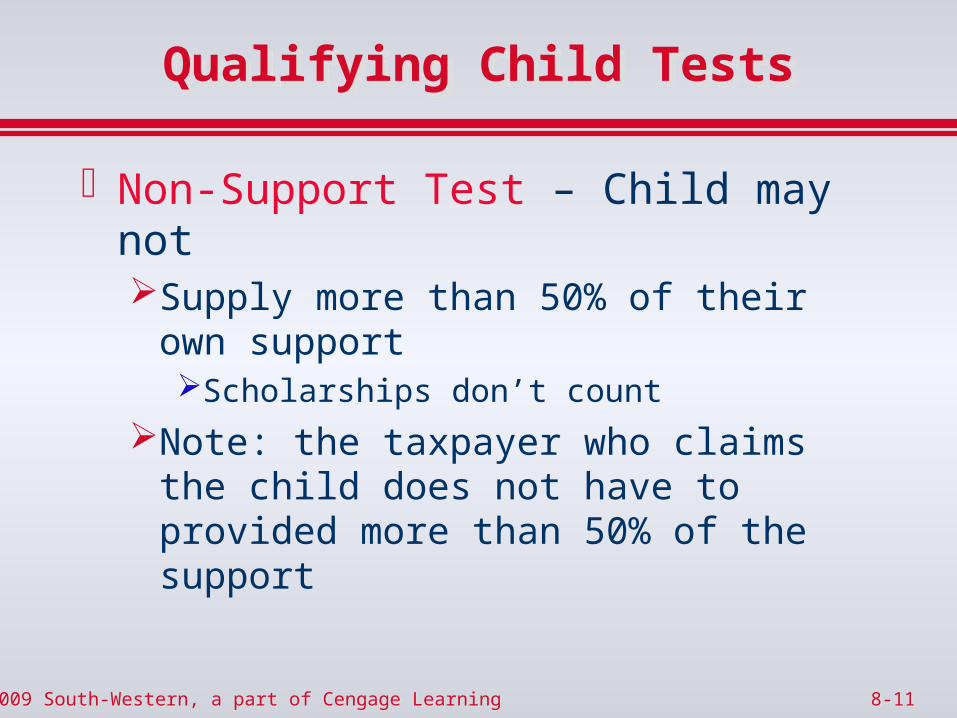

Qualifying Child TestsQualifying Child Tests

Non-Support Test – Child may notSupply more than 50% of their own support

Scholarships don’t count

Note: the taxpayer who claims the child does not have to provided more than 50% of the support

8-128-122009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

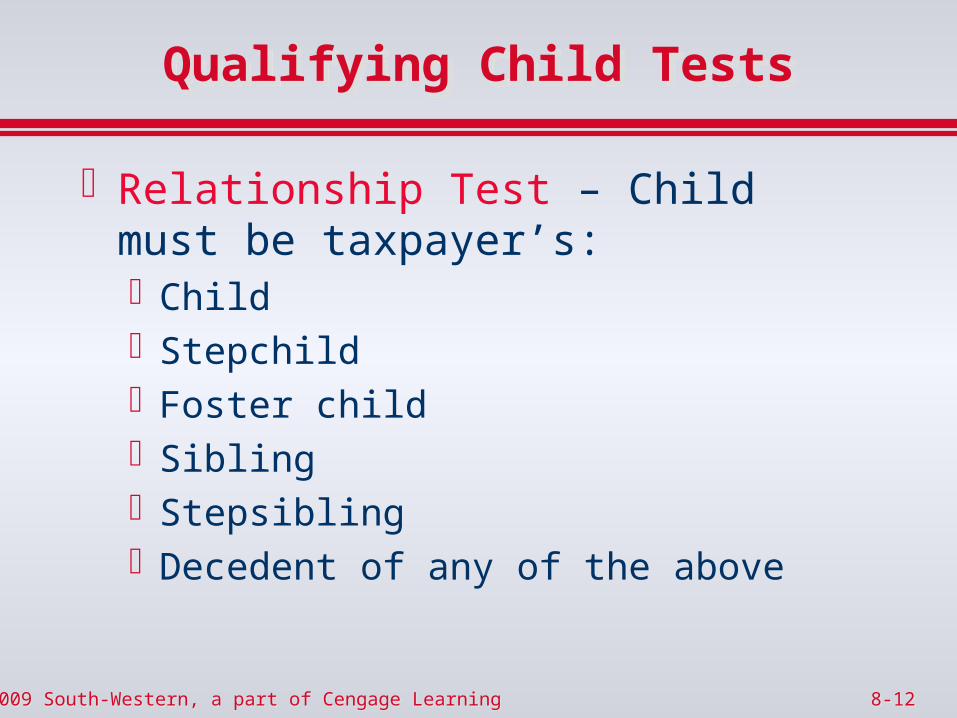

Relationship Test – Child must be taxpayer’s:ChildStepchildFoster childSiblingStepsibling Decedent of any of the above

Qualifying Child TestsQualifying Child Tests

8-138-132009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

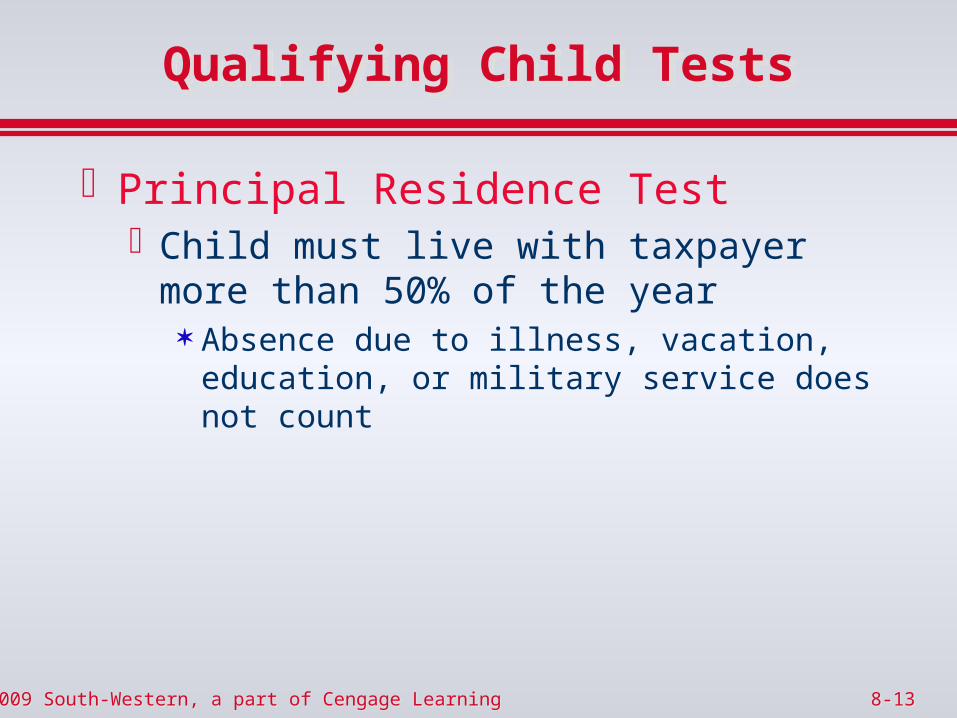

Qualifying Child TestsQualifying Child Tests

Principal Residence TestChild must live with taxpayer more than

50% of the year Absence due to illness, vacation, education, or

military service does not count

8-148-142009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Qualifying Child TestsQualifying Child Tests

Citizen or Resident TestChild must be a U.S. citizen, or Resident of the U.S., Canada, or Mexico

8-158-152009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

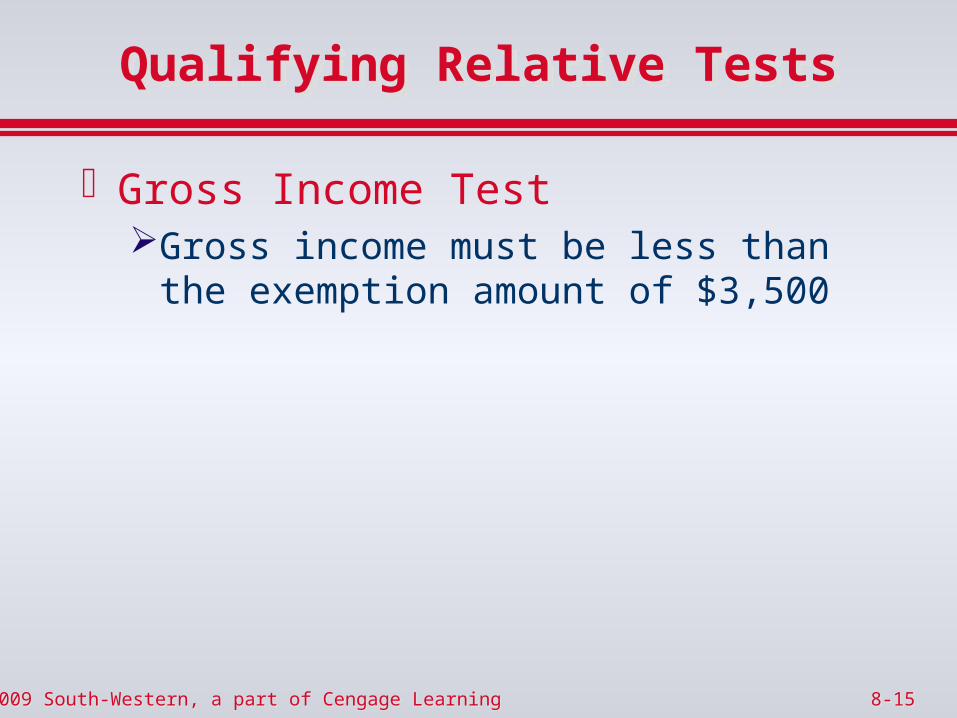

Qualifying Relative TestsQualifying Relative Tests

Gross Income Test Gross income must be less than the

exemption amount of $3,500

8-168-162009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Qualifying Relative TestsQualifying Relative Tests

Support TestThe taxpayer must provide more than 50%

of a dependent’s support for the year Two exceptions apply

Custodial parent may always claim a child

Multiple Support Agreement

8-178-172009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

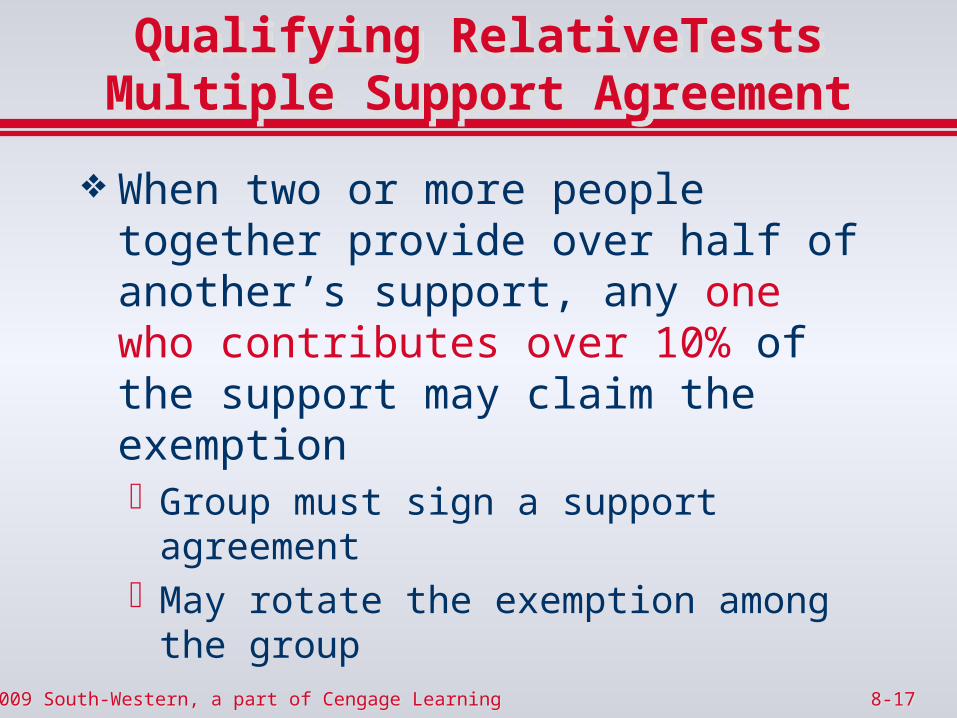

Qualifying RelativeTestsMultiple Support Agreement

Qualifying RelativeTestsMultiple Support Agreement

When two or more people together provide over half of another’s support, any one who contributes over 10% of the support may claim the exemptionGroup must sign a support agreementMay rotate the exemption among the group

8-188-182009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

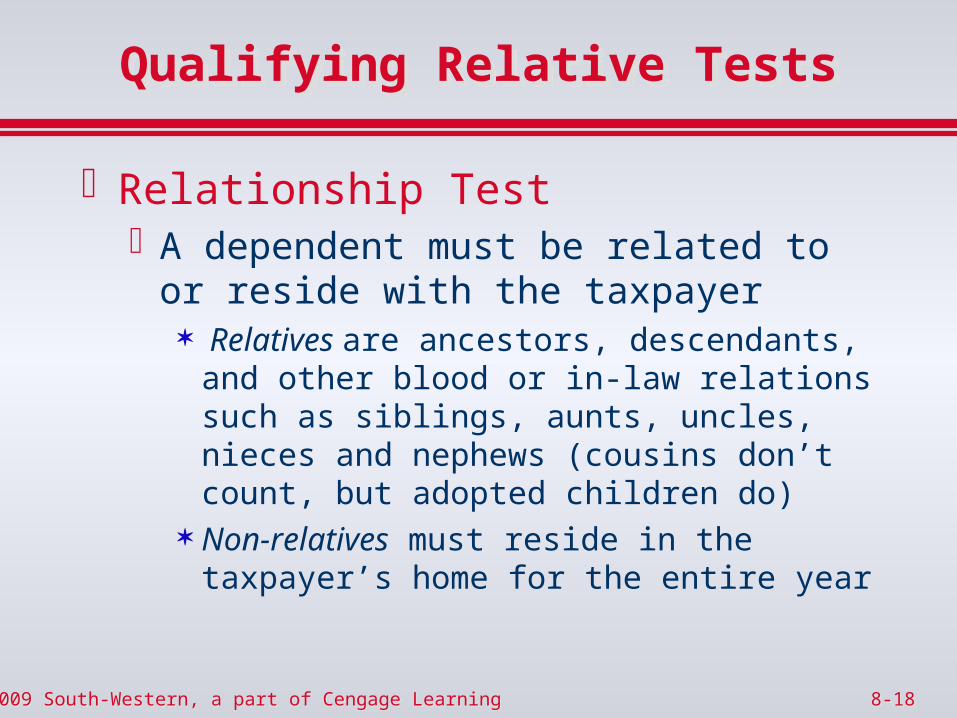

Qualifying Relative TestsQualifying Relative Tests

Relationship TestA dependent must be related to or reside

with the taxpayer Relatives are ancestors, descendants, and

other blood or in-law relations such as siblings, aunts, uncles, nieces and nephews (cousins don’t count, but adopted children do)

Non-relatives must reside in the taxpayer’s home for the entire year

8-198-192009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Dependency TestsDependency Tests

Citizenship or Residency Test A dependent must be a U.S. citizen or a

resident of a country adjacent to the U.S.

Joint Return Test A dependent must not file a joint returnA joint return may be filed simply to claim a

refund of all withheld tax

8-208-202009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

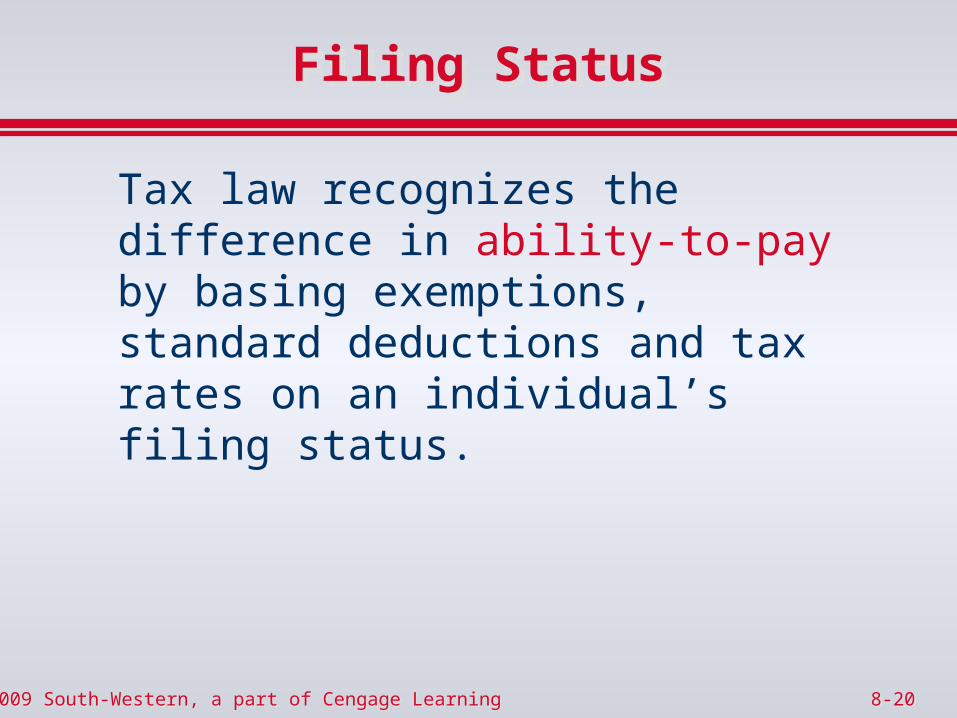

Filing StatusFiling Status

Tax law recognizes the difference in ability-to-pay by basing exemptions, standard deductions and tax rates on an individual’s filing status.

8-218-212009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

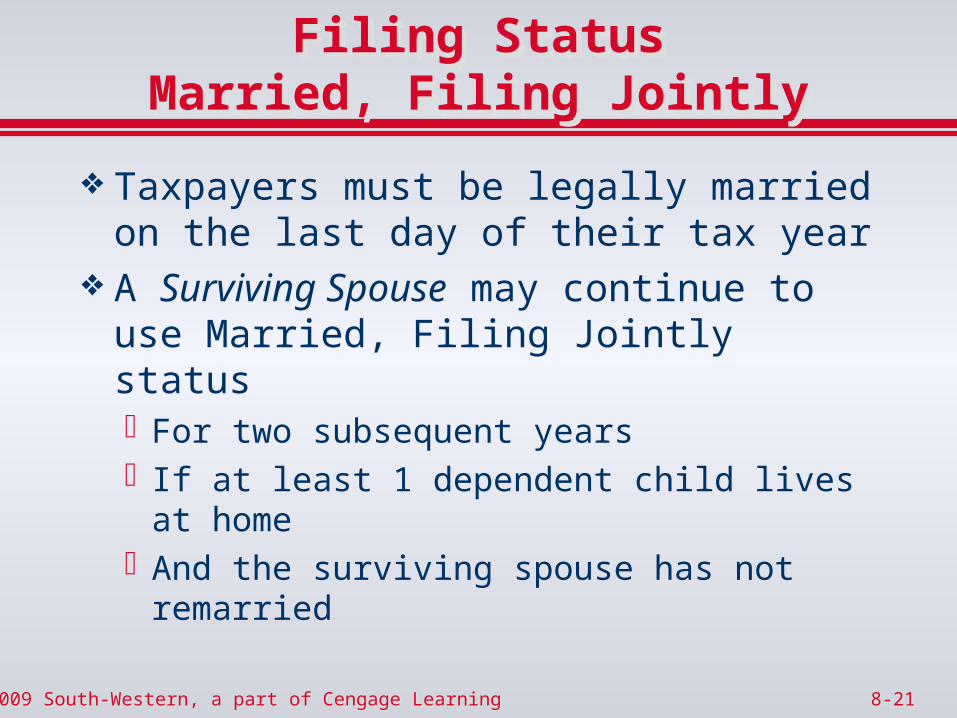

Filing StatusMarried, Filing Jointly

Filing StatusMarried, Filing Jointly

Taxpayers must be legally married on the last day of their tax year

A Surviving Spouse may continue to use Married, Filing Jointly status For two subsequent yearsIf at least 1 dependent child lives at homeAnd the surviving spouse has not

remarried

8-228-222009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Filing StatusMarried, Filing Separately

Filing StatusMarried, Filing Separately

Taxpayers married as of the last day of the year may choose to file separately

8-238-232009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

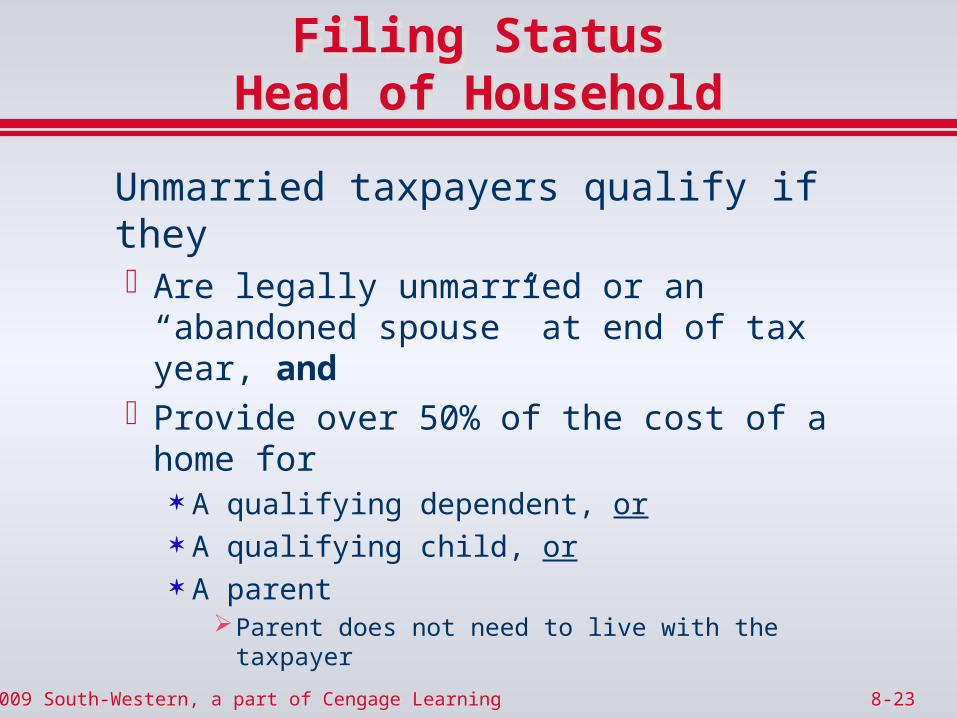

Filing StatusHead of Household

Filing StatusHead of Household

Unmarried taxpayers qualify if they Are legally unmarried or an “abandoned

spouse” at end of tax year, and Provide over 50% of the cost of a home for

A qualifying dependent, or A qualifying child, or A parent

Parent does not need to live with the taxpayer

8-248-242009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

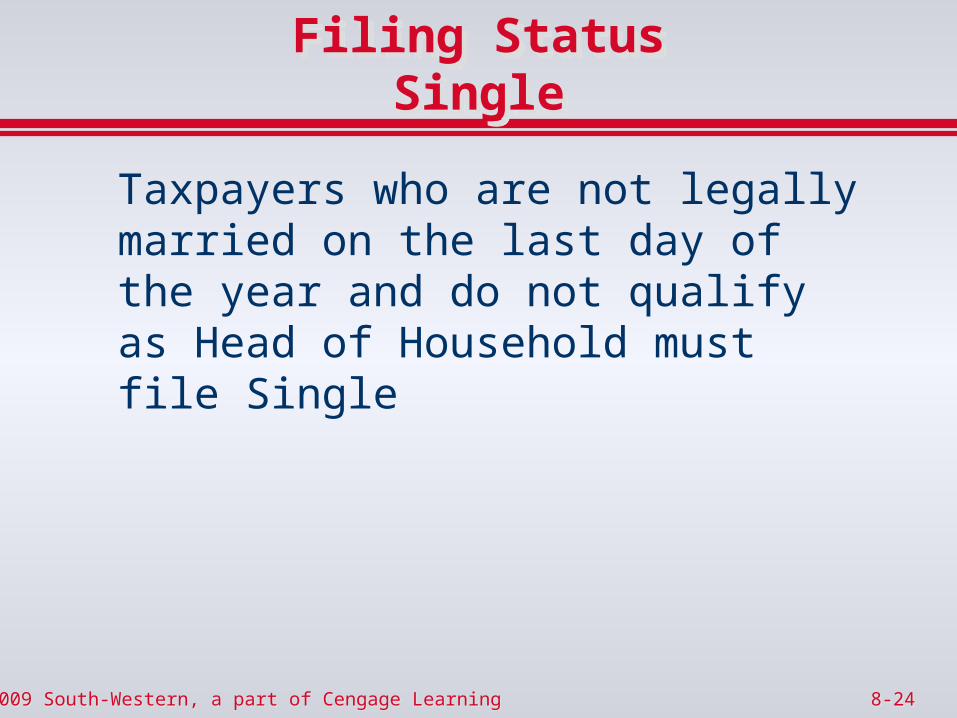

Filing StatusSingle

Filing StatusSingle

Taxpayers who are not legally married on the last day of the year and do not qualify as Head of Household must file Single

8-258-252009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

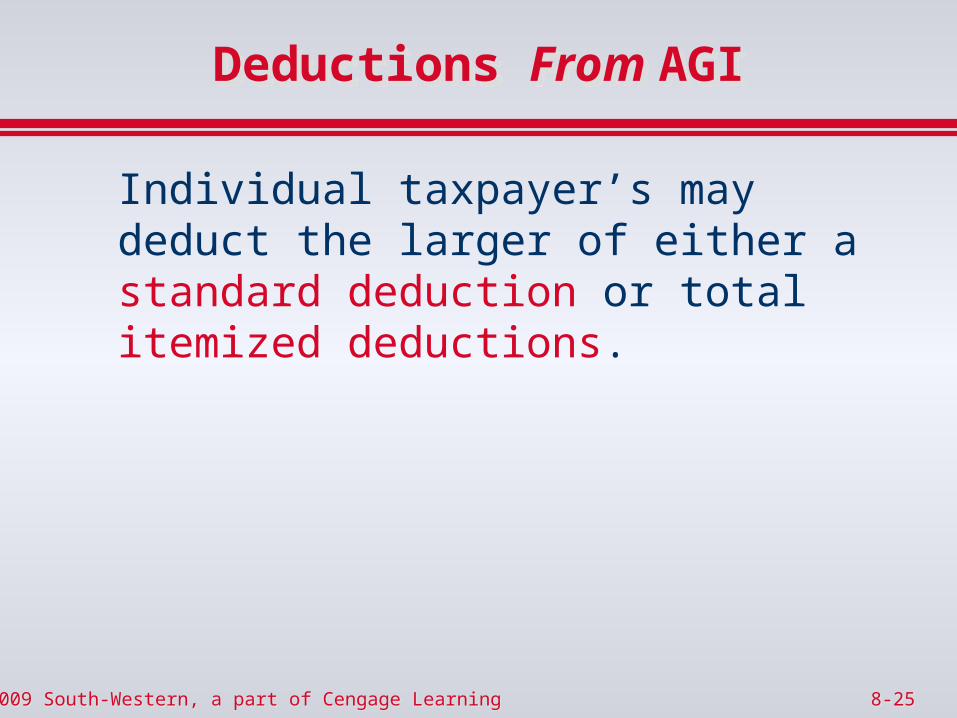

Deductions From AGIDeductions From AGI

Individual taxpayer’s may deduct the larger of either a standard deduction or total itemized deductions.

8-268-262009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

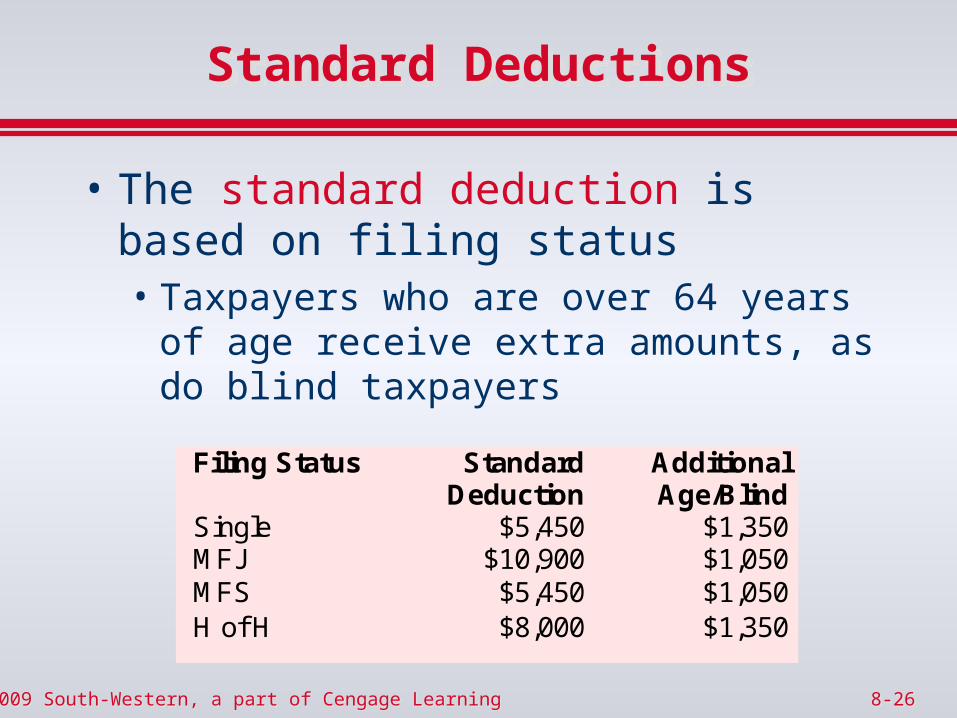

Standard DeductionsStandard Deductions

• The standard deduction is based on filing status• Taxpayers who are over 64 years of age

receive extra amounts, as do blind taxpayers

Filing Status Standard Deduction

Additional Age/Blind

Single $5,450 $1,350 MFJ $10,900 $1,050 MFS $5,450 $1,050 H of H $8,000 $1,350

8-278-272009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

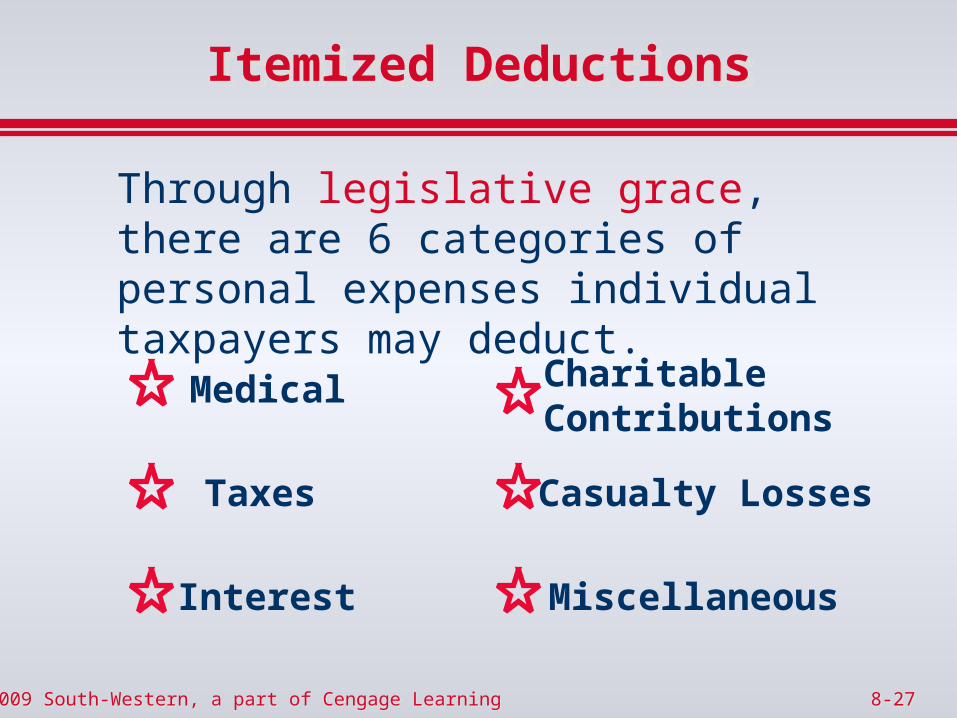

Itemized DeductionsItemized Deductions

Through legislative grace, there are 6 categories of personal expenses individual taxpayers may deduct.

Medical

Taxes

Interest

CharitableContributions

Casualty Losses

Miscellaneous

8-288-282009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

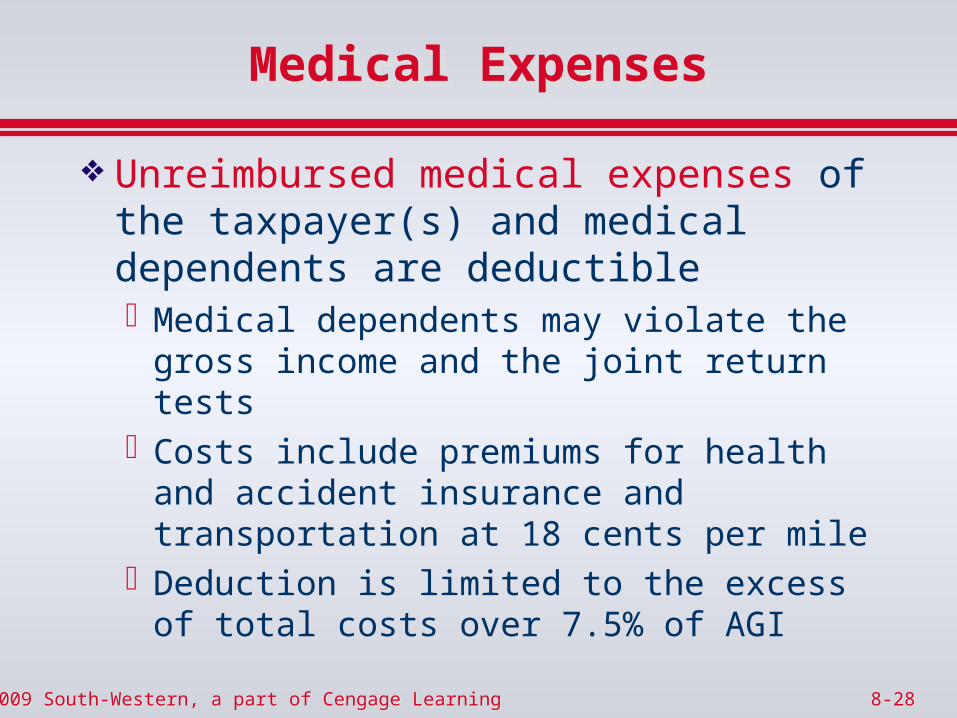

Medical ExpensesMedical Expenses

Unreimbursed medical expenses of the taxpayer(s) and medical dependents are deductibleMedical dependents may violate the gross

income and the joint return testsCosts include premiums for health and

accident insurance and transportation at 18 cents per mile

Deduction is limited to the excess of total costs over 7.5% of AGI

8-298-292009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

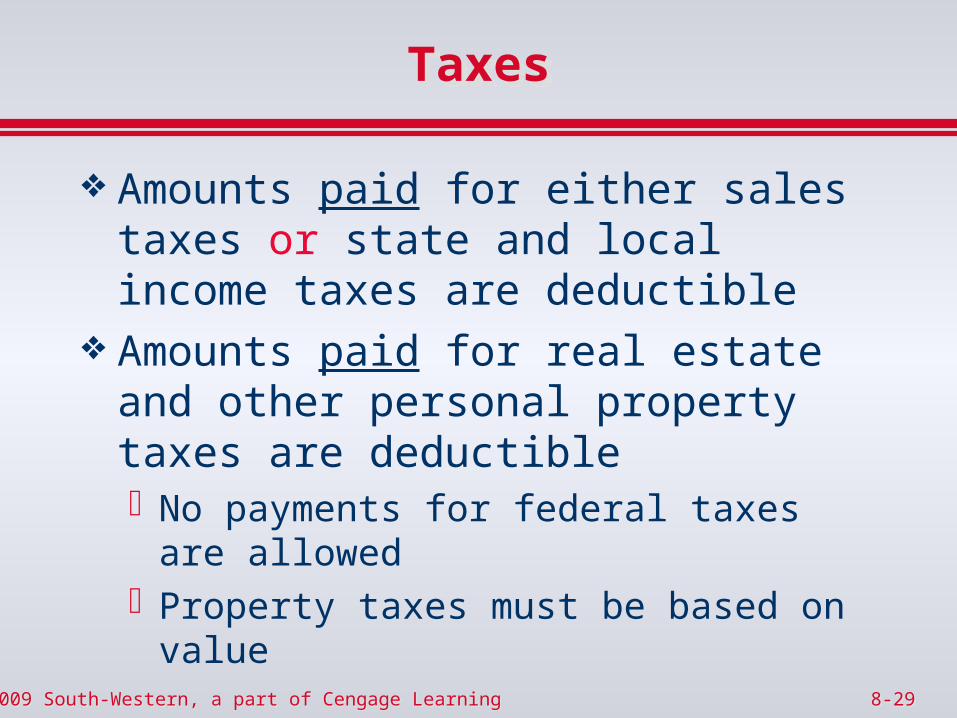

TaxesTaxes

Amounts paid for either sales taxes or state and local income taxes are deductible

Amounts paid for real estate and other personal property taxes are deductibleNo payments for federal taxes are allowedProperty taxes must be based on value

8-308-302009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

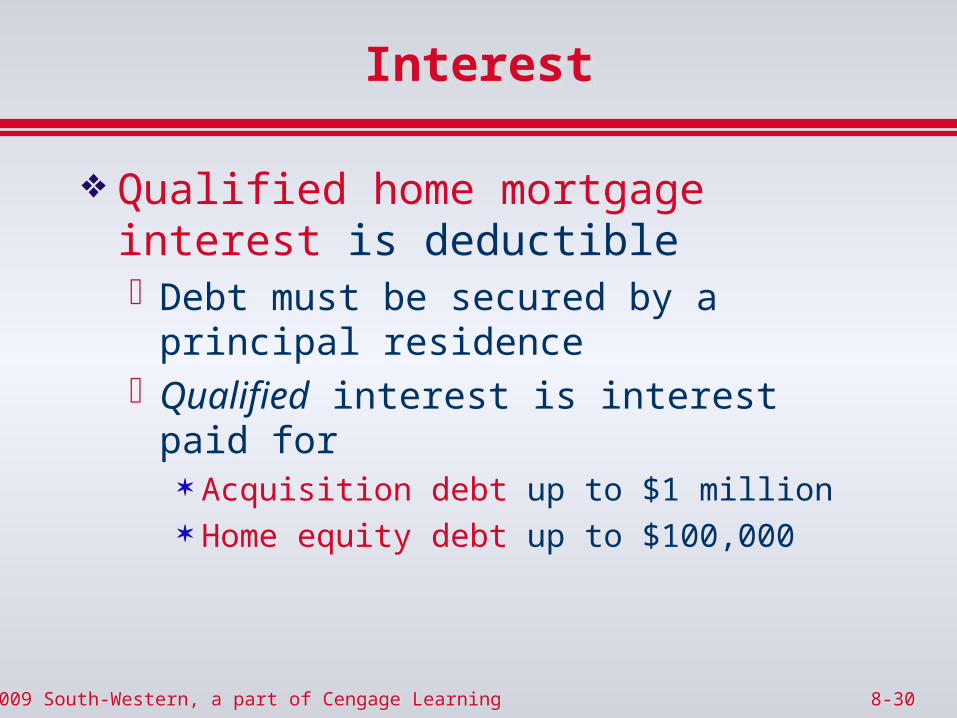

InterestInterest

Qualified home mortgage interest is deductibleDebt must be secured by a principal

residenceQualified interest is interest paid for

Acquisition debt up to $1 million Home equity debt up to $100,000

8-318-312009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

InterestInterest

Points on a qualified mortgage are deductible if paid to acquire financingMust be stated as a % of the loan valueDeductible currently if paid on acquisition

debt If for refinancing, amortize over the life of the

loan

8-328-322009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

InterestInterest

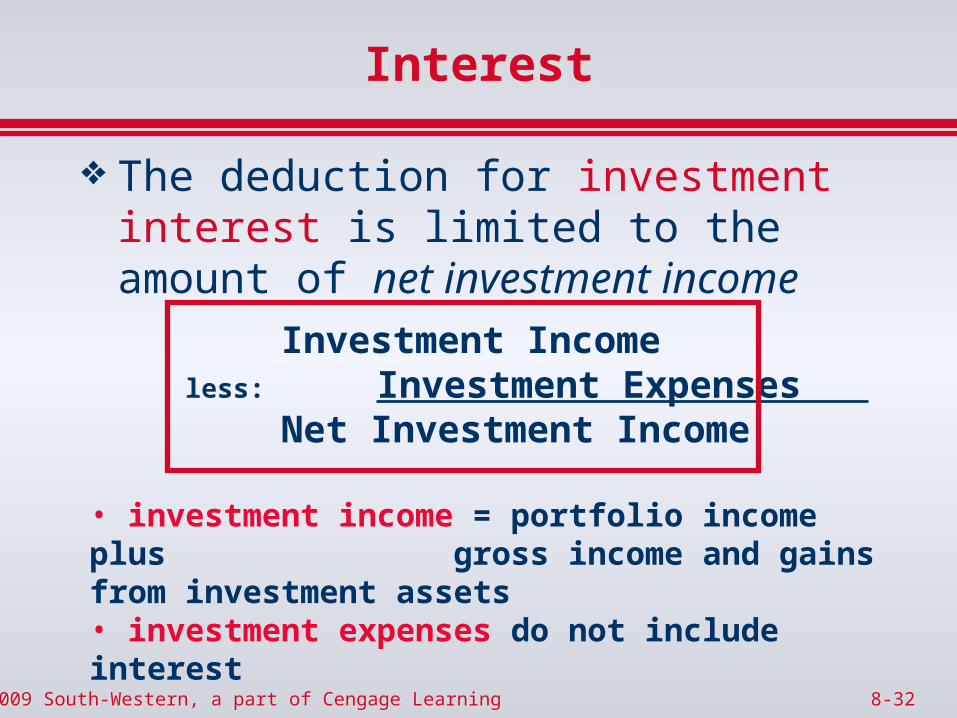

The deduction for investment interest is limited to the amount of net investment income

Investment Incomeless: Investment Expenses

Net Investment Income

• investment income = portfolio income plus gross income and gains from investment assets• investment expenses do not include interest

Charitable ContributionsCharitable Contributions

Contributions made to qualifying charitable organizations are deductibleOrganizations established for religious,

educational, charitable, scientific or literary purposes qualify

Deductible amount includes cash paid and the value of property given and $0.14 per mile driven

Three major limitations existContributions in excess of limitations may be

carried forward for five years

Transparency 8-33Transparency 8-33© 2004 South-Western College Publishing© 2004 South-Western College Publishing

8-348-342009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Charitable ContributionsCharitable Contributions

Deduction amount for property depends of the type of property givenOrdinary income property or short-term

capital gain property Deduction is the lesser of the property’s

FMV, oradjusted basis

Deduction amount for long-term capital gain property is FMV

8-358-352009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Charitable ContributionsLimitations

Charitable ContributionsLimitations

The overall deduction cannot exceed 50% of AGI

Deduction for long-term capital gain property cannot exceed 30% of AGI If the taxpayer elects to deduct the adjusted basis

rather than FMV, the 50% limit is used

Contributions to non-operating private foundations are subject to additional limits

8-368-362009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Casualty LossesCasualty Losses

These were discussed in Chapter 7. Loss is the lesser of

The property’s adjusted basis, orThe decline in the value of the property (repair

cost)

Loss is reduced by Insurance proceeds received,$100 per event (Administrative convenience), and10% of AGI per year

8-378-372009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Miscellaneous DeductionsMiscellaneous Deductions

Other various expenses are combined as miscellaneous itemized deductions and are either fully deductible or partially deductible

8-388-382009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

MiscellaneousFully DeductibleMiscellaneous

Fully Deductible

Fully Deductible expenses include: Gambling losses to the extent of

gambling winnings, Impairment-related-work expenses of

disabled taxpayers, and Unrecovered capital from a terminated

annuity

8-398-392009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

MiscellaneousPartially Deductible

MiscellaneousPartially Deductible

Other miscellaneous expenses are partially deductible to the extent their total exceeds 2% of AGIUnreimbursed employee expensesInvestment expenses other than interestHobby-related expenses

8-408-402009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Reductions for High-Income Taxpayers

Reductions for High-Income Taxpayers

Taxpayers whose AGI exceeds set threshold amounts must reduce their total itemized deductions and their total personal & dependency exemptions.

8-418-412009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Itemized Deduction Phase-Out

Itemized Deduction Phase-Out

Deductions for medical expenses, investment interest, casualty and theft losses and gambling losses are not subject to reduction

Calculated phase-out amount for taxpayers with AGI over $159,950 is the smaller of3% of (AGI - $159,950), or80% of the amount subject to reduction

8-428-422009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

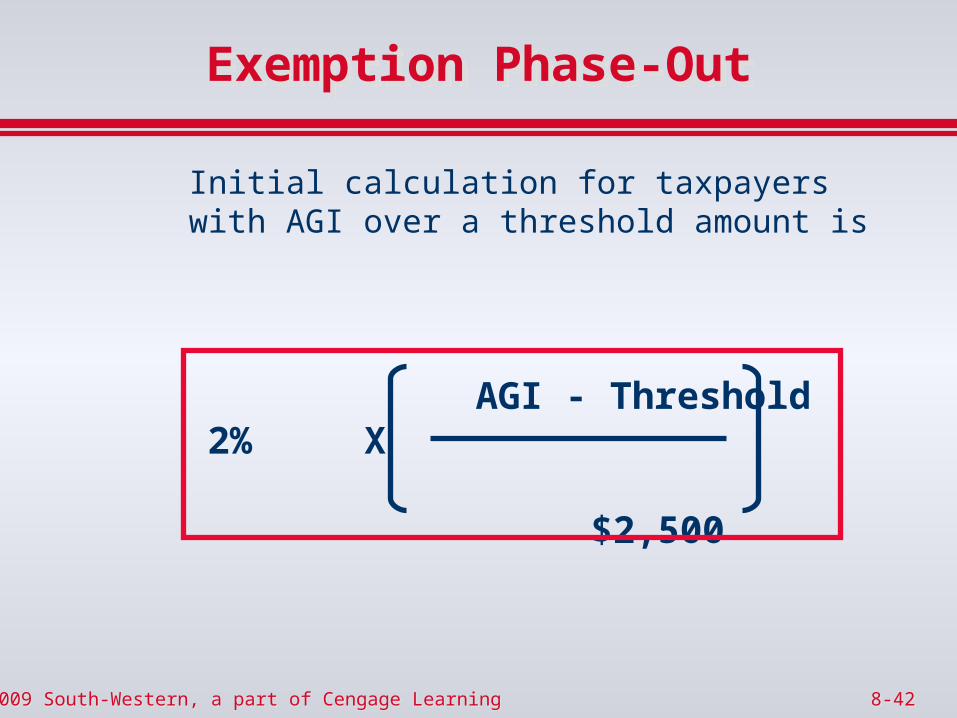

Exemption Phase-OutExemption Phase-Out

Initial calculation for taxpayers with AGI over a threshold amount is

AGI - Threshold2% X

$2,500

8-438-432009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

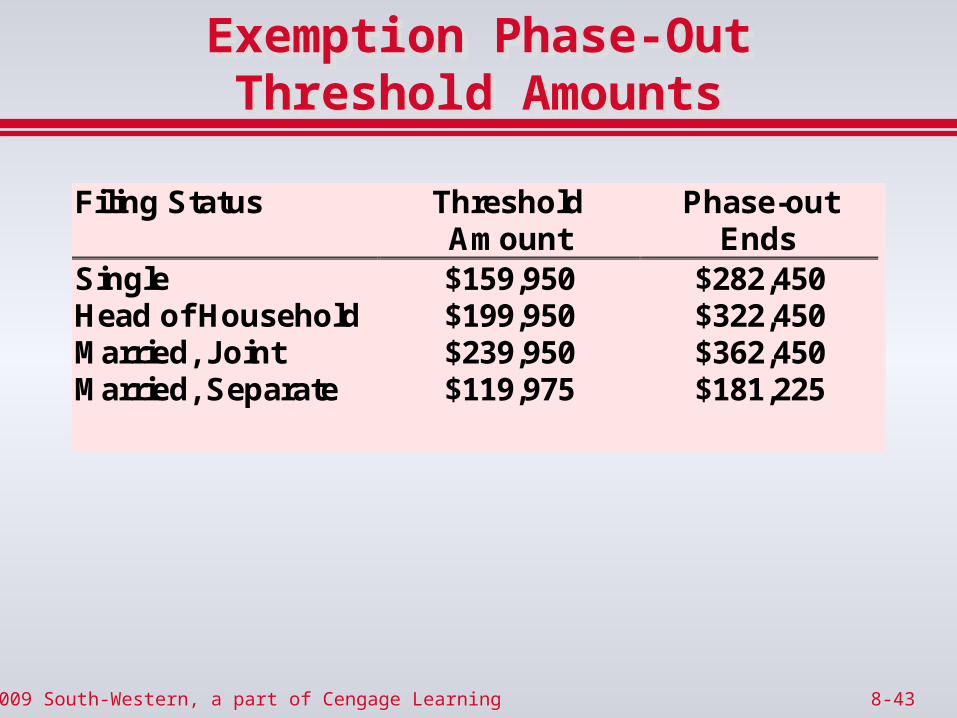

Exemption Phase-OutThreshold Amounts

Exemption Phase-OutThreshold Amounts

Filing Status Threshold Amount

Phase-out Ends

Single $159,950 $282,450 Head of Household $199,950 $322,450 Married, Joint $239,950 $362,450 Married, Separate $119,975 $181,225

8-448-442009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

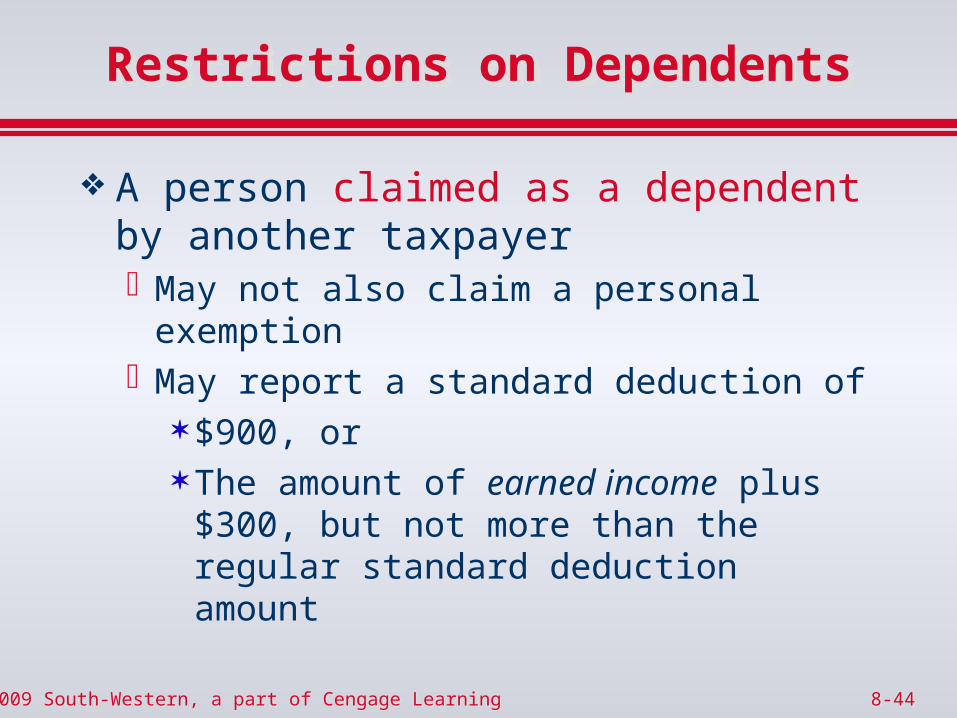

Restrictions on DependentsRestrictions on Dependents

A person claimed as a dependent by another taxpayer May not also claim a personal exemptionMay report a standard deduction of

$900, orThe amount of earned income plus

$300, but not more than the regular standard deduction amount

8-458-452009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

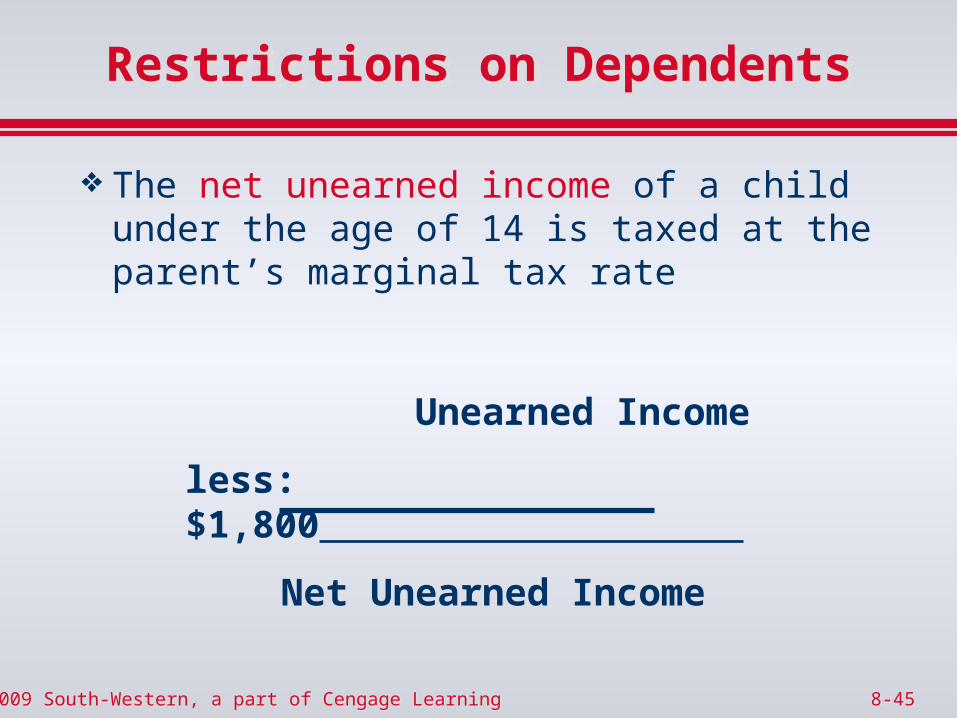

Restrictions on DependentsRestrictions on Dependents

The net unearned income of a child under the age of 14 is taxed at the parent’s marginal tax rate

Unearned Income

less: $1,800

Net Unearned Income

8-468-462009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

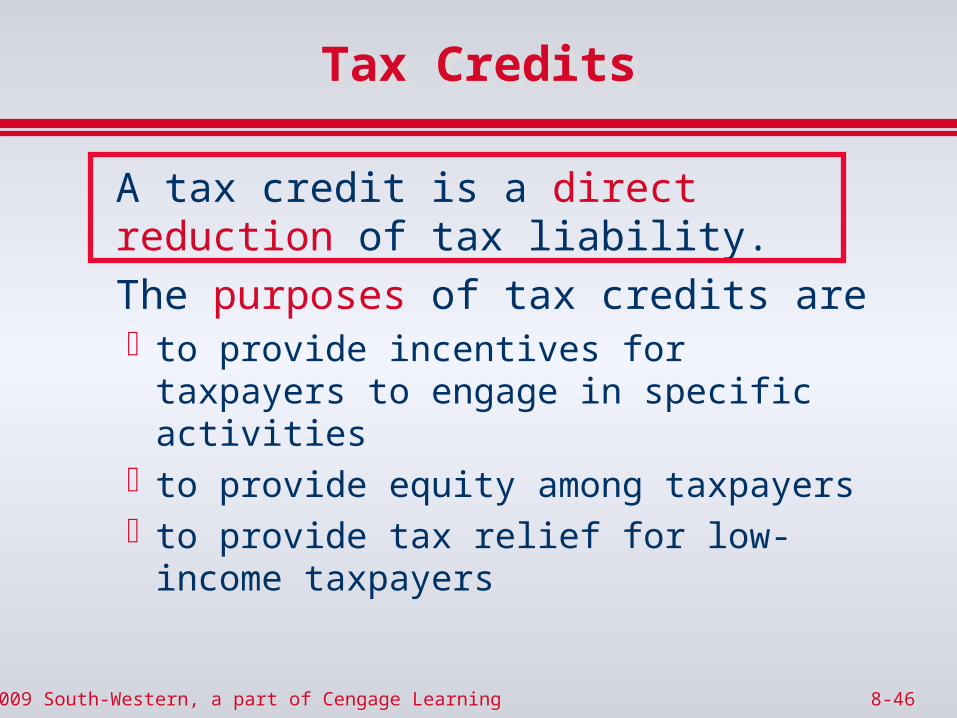

Tax CreditsTax Credits

A tax credit is a direct reduction of tax liability.

The purposes of tax credits areto provide incentives for taxpayers to

engage in specific activitiesto provide equity among taxpayersto provide tax relief for low-income

taxpayers

8-478-472009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

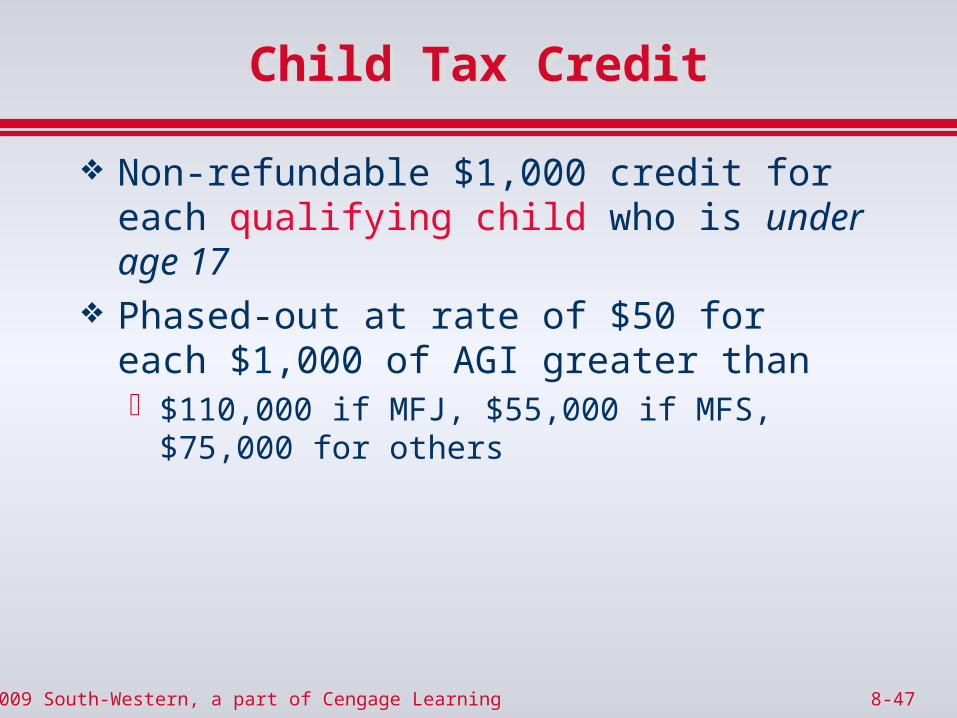

Child Tax CreditChild Tax Credit

Non-refundable $1,000 credit for each qualifying child who is under age 17

Phased-out at rate of $50 for each $1,000 of AGI greater than$110,000 if MFJ, $55,000 if MFS, $75,000 for

others

8-488-482009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

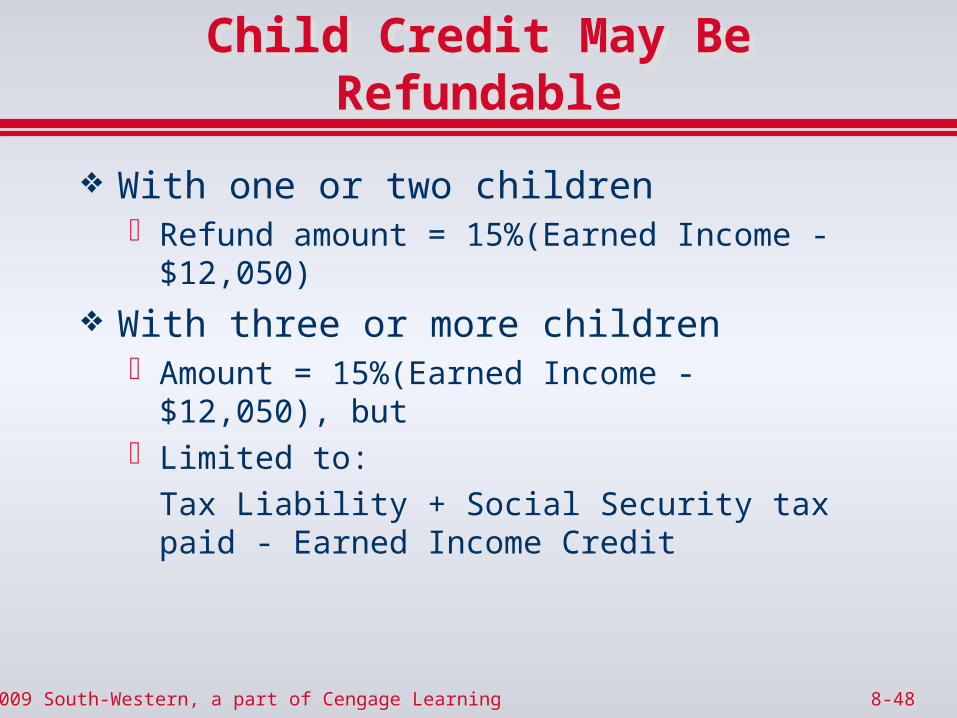

Child Credit May Be Refundable

Child Credit May Be Refundable

With one or two childrenRefund amount = 15%(Earned Income - $12,050)

With three or more childrenAmount = 15%(Earned Income - $12,050), butLimited to:

Tax Liability + Social Security tax paid - Earned Income Credit

8-498-492009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

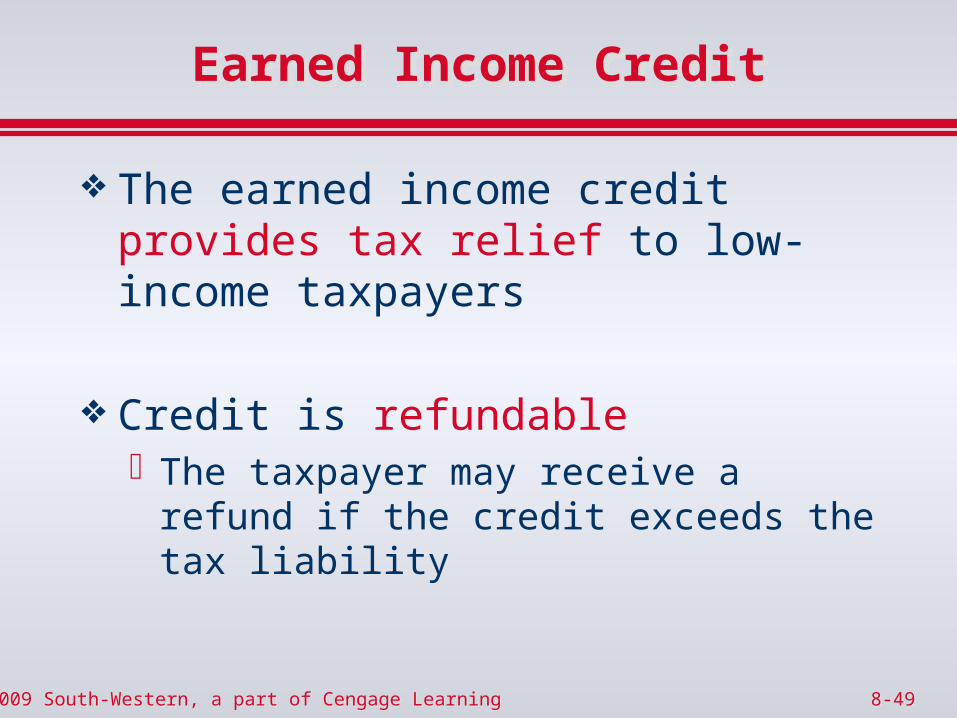

Earned Income CreditEarned Income Credit

The earned income credit provides tax relief to low-income taxpayers

Credit is refundableThe taxpayer may receive a refund if the

credit exceeds the tax liability

8-508-502009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

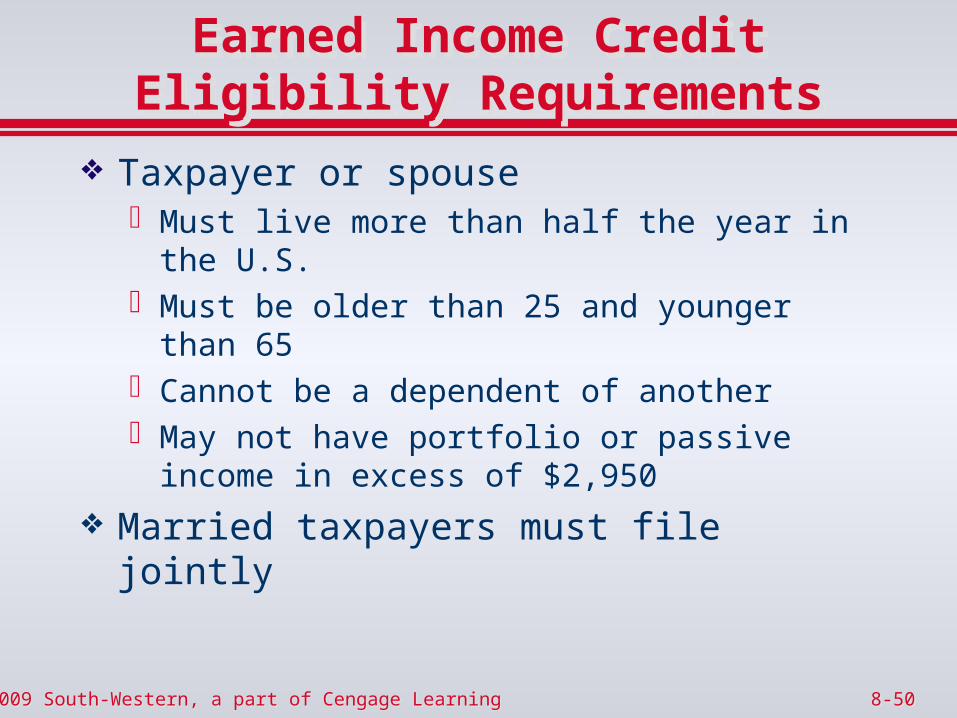

Earned Income CreditEligibility RequirementsEarned Income Credit

Eligibility Requirements

Taxpayer or spouseMust live more than half the year in the U.S.Must be older than 25 and younger than 65Cannot be a dependent of anotherMay not have portfolio or passive income in

excess of $2,950

Married taxpayers must file jointly

8-518-512009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

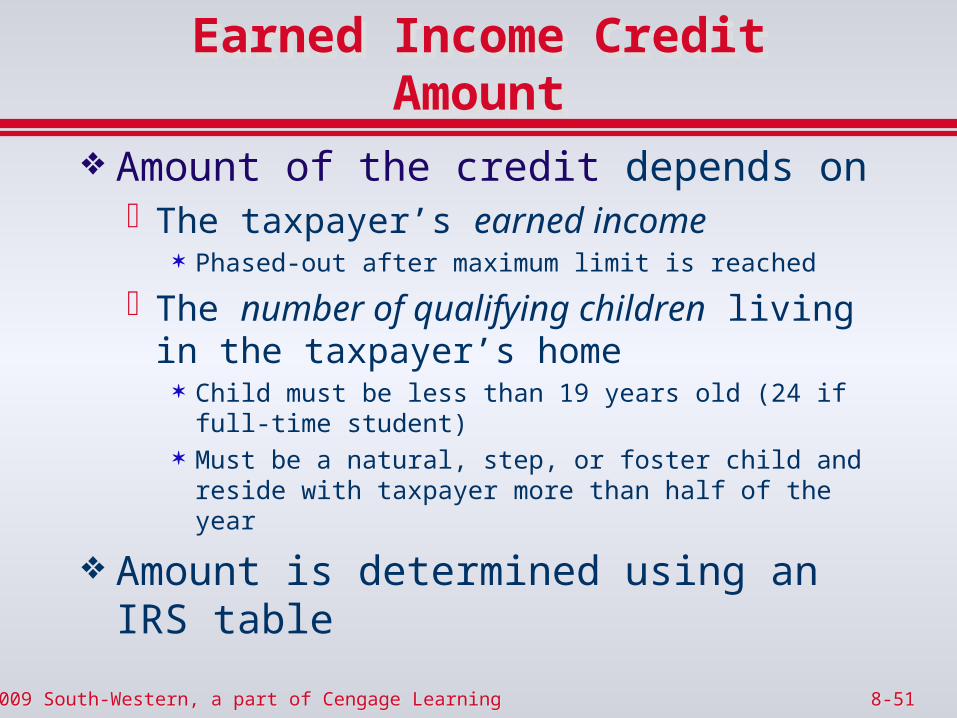

Earned Income CreditAmount

Earned Income CreditAmount

Amount of the credit depends on The taxpayer’s earned income

Phased-out after maximum limit is reached

The number of qualifying children living in the taxpayer’s home Child must be less than 19 years old (24 if full-time

student) Must be a natural, step, or foster child and reside with

taxpayer more than half of the year

Amount is determined using an IRS table

8-528-522009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Child and Dependent Care Credit

Child and Dependent Care Credit

The child and dependent care credit provides tax relief to taxpayers so that they can be employed

Two qualifying conditions must be metExpenses must be incurred so that

taxpayer can be employedExpenses must be for the care of qualified

individuals

8-538-532009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

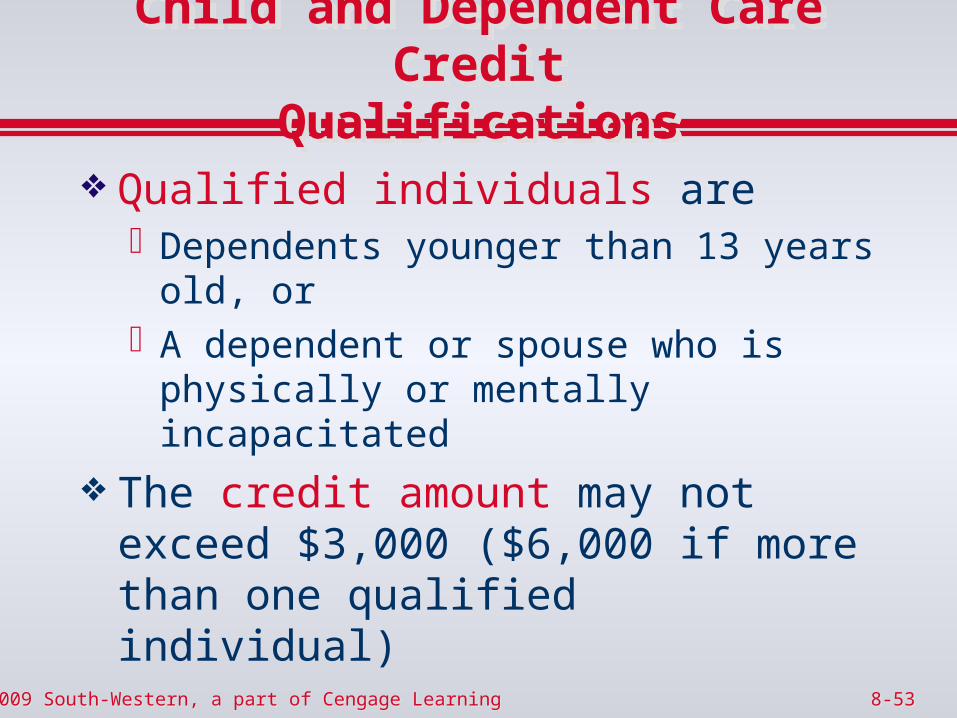

Child and Dependent Care Credit

Qualifications

Child and Dependent Care Credit

Qualifications Qualified individuals are

Dependents younger than 13 years old, orA dependent or spouse who is physically

or mentally incapacitated

The credit amount may not exceed $3,000 ($6,000 if more than one qualified individual)

8-548-542009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

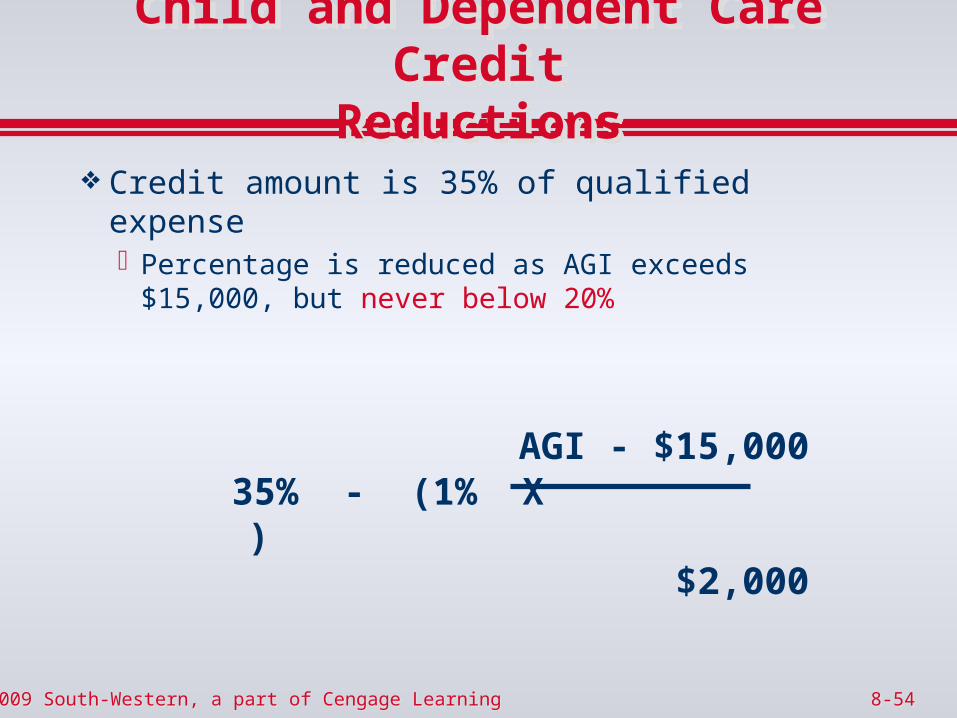

Child and Dependent Care Credit

Reductions

Child and Dependent Care Credit

Reductions Credit amount is 35% of qualified expense

Percentage is reduced as AGI exceeds $15,000, but never below 20%

AGI - $15,00035% - (1% X )

$2,000

8-558-552009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Higher Education CreditsHigher Education Credits

Two creditsHOPE Scholarship CreditLifetime Learning Credit

May claim only one per qualifying studentMust be enrolled at least one semesterMust be enrolled at least half-time

May not claim if deduction taken for Higher Education Expenses

8-568-562009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

Higher Education CreditQualifying Expenses

Higher Education CreditQualifying Expenses

Expenses must be for higher education of taxpayer, spouse, or dependent

Tuition and related fees are reduced by the amount of any scholarship or fellowship received

8-578-572009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

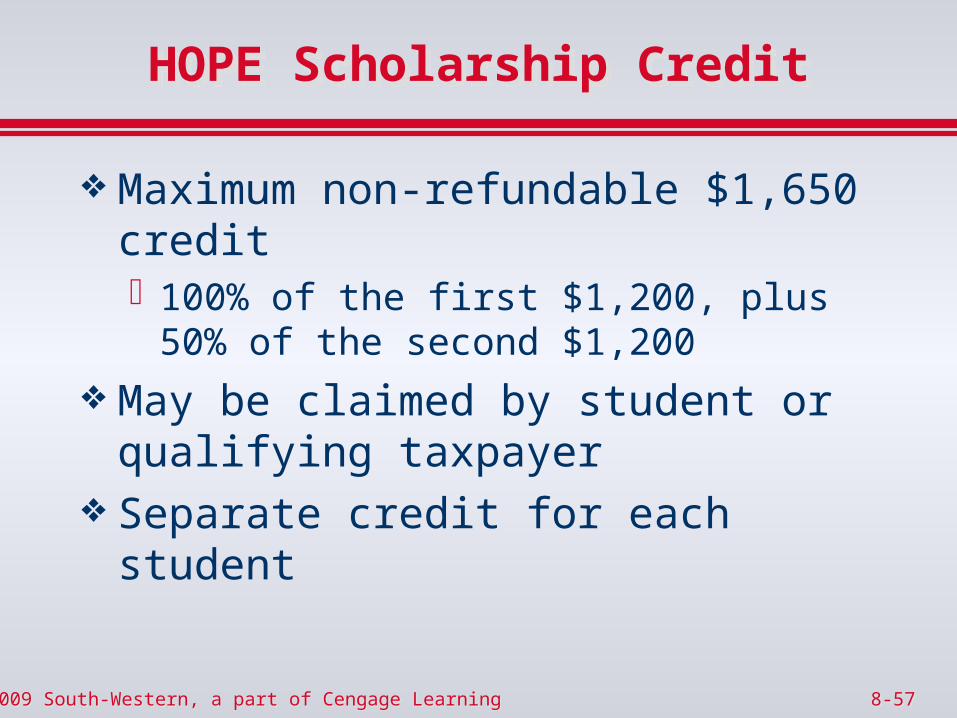

HOPE Scholarship CreditHOPE Scholarship Credit

Maximum non-refundable $1,650 credit100% of the first $1,200, plus 50% of the

second $1,200

May be claimed by student or qualifying taxpayer

Separate credit for each student

8-588-582009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

HOPE Scholarship CreditLimitations

HOPE Scholarship CreditLimitations

Available only for first two years of post-secondary education

Phased-out for AGI greater than$94,000 if MFJ$47,000 if other

Possible credit X [1 - {(AGI - phase-out) / 20,000}]

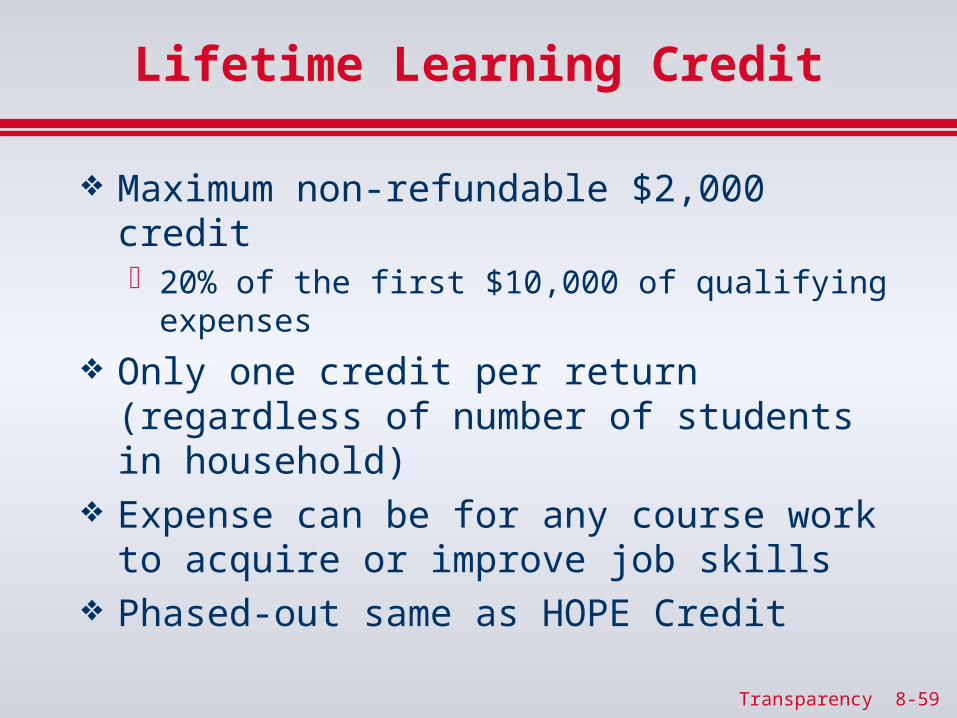

Lifetime Learning CreditLifetime Learning Credit

Maximum non-refundable $2,000 credit20% of the first $10,000 of qualifying expenses

Only one credit per return (regardless of number of students in household)

Expense can be for any course work to acquire or improve job skills

Phased-out same as HOPE Credit

Transparency 8-59Transparency 8-59

8-608-602009 South-Western, a part of Cengage Learning2009 South-Western, a part of Cengage Learning

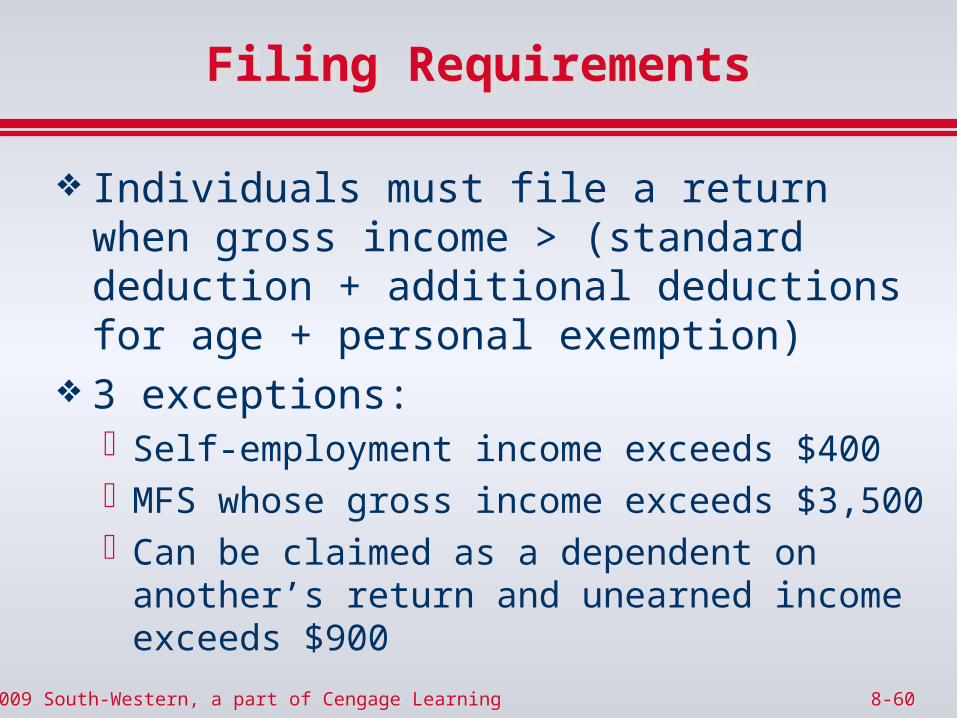

Filing RequirementsFiling Requirements

Individuals must file a return when gross income > (standard deduction + additional deductions for age + personal exemption)

3 exceptions:Self-employment income exceeds $400MFS whose gross income exceeds $3,500Can be claimed as a dependent on another’s

return and unearned income exceeds $900