Embed Size (px)

DESCRIPTION

w

Citation preview

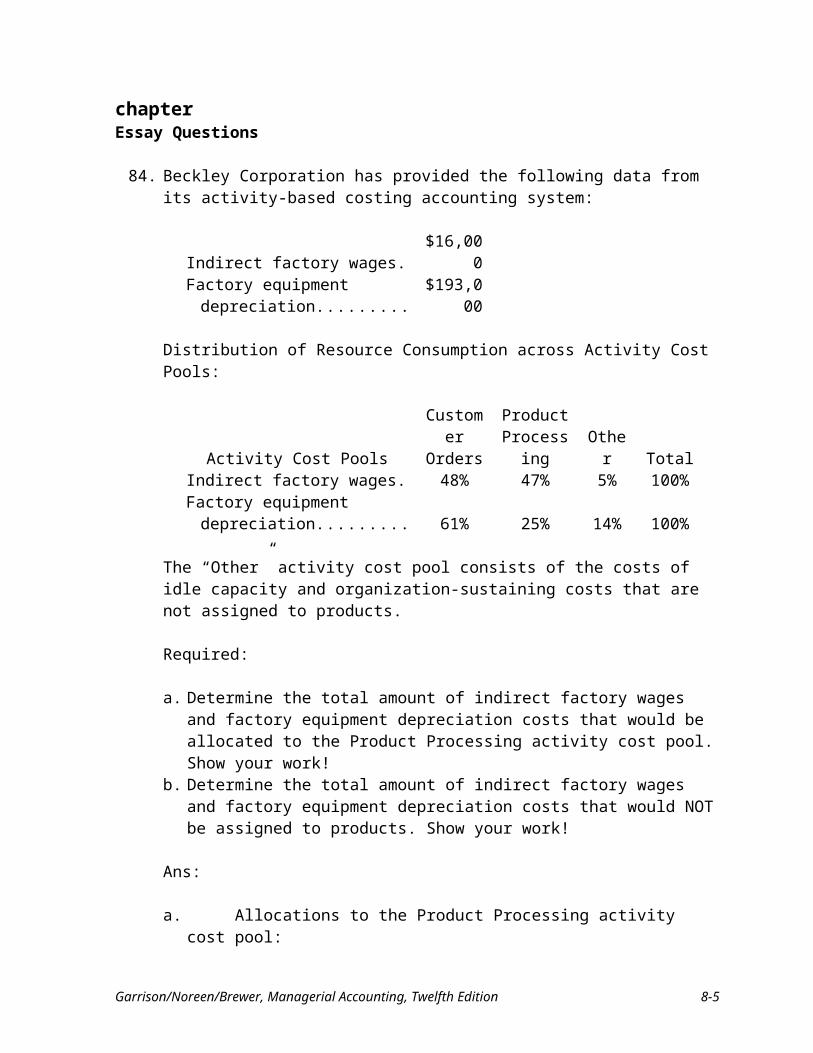

chapterEssay Questions

84. Beckley Corporation has provided the following data from its activity-based costing accounting system:

Indirect factory wages.................... $16,000Factory equipment depreciation..... $193,000

Distribution of Resource Consumption across Activity Cost Pools:

Activity Cost PoolsCustomer

OrdersProduct

Processing Other TotalIndirect factory wages.................... 48% 47% 5% 100%Factory equipment depreciation..... 61% 25% 14% 100%

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs that are not assigned to products.

Required:

a. Determine the total amount of indirect factory wages and factory equipment depreciation costs that would be allocated to the Product Processing activity cost pool. Show your work!

b. Determine the total amount of indirect factory wages and factory equipment depreciation costs that would NOT be assigned to products. Show your work!

Ans:

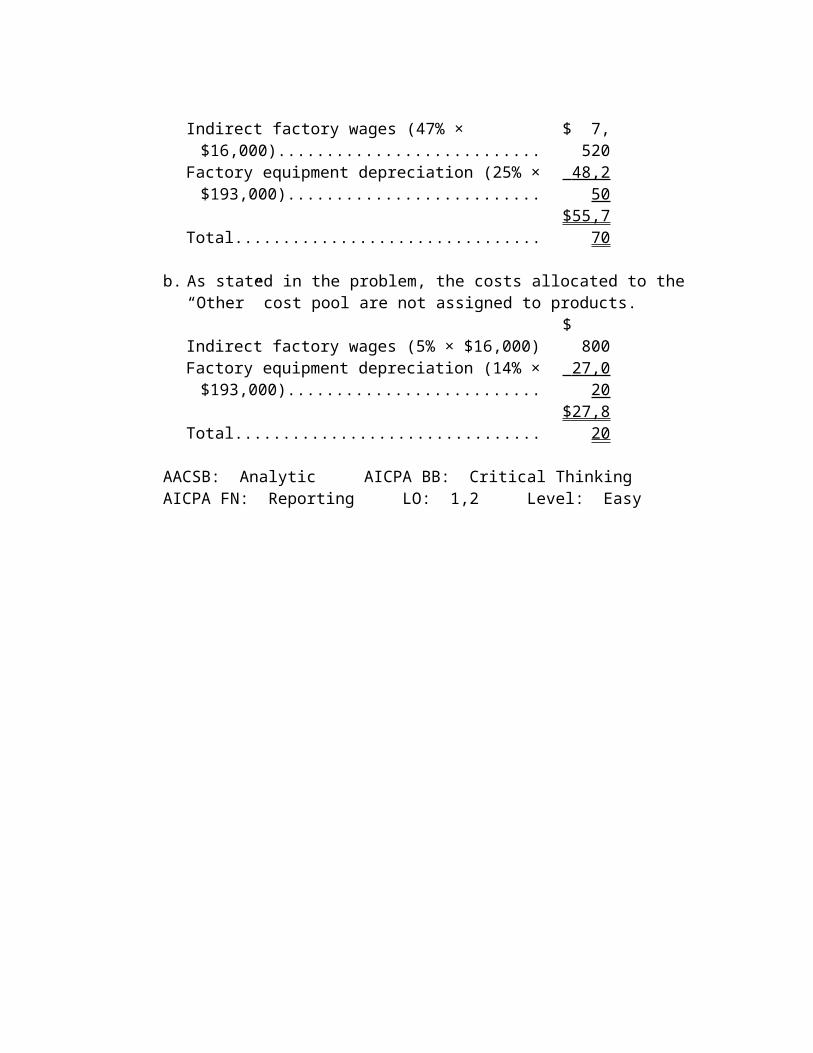

a. Allocations to the Product Processing activity cost pool:Indirect factory wages (47% × $16,000)......................... $ 7,520Factory equipment depreciation (25% × $193,000)....... 48,250 Total................................................................................ $55,770

b. As stated in the problem, the costs allocated to the “Other” cost pool are not assigned to products.Indirect factory wages (5% × $16,000)........................... $ 800Factory equipment depreciation (14% × $193,000)....... 27,020 Total................................................................................ $27,820

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1,2 Level: Easy

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-5

85. Desilets Corporation has provided the following data from its activity-based costing accounting system:

Supervisory wages............. $94,000Factory utilities.................. $128,000

Distribution of Resource Consumption across Activity Cost Pools:

Activity Cost PoolsBatch

Set-UpsUnit

Processing Other TotalSupervisory wages....... 34% 64% 2% 100%Factory utilities............ 49% 35% 16% 100%

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs that are not assigned to products.

Required:

a. Determine the total amount of supervisory wages and factory utilities costs that would be allocated to the Unit Processing activity cost pool. Show your work!

b. Determine the total amount of supervisory wages and factory utilities costs that would NOT be assigned to products. Show your work!

Ans:

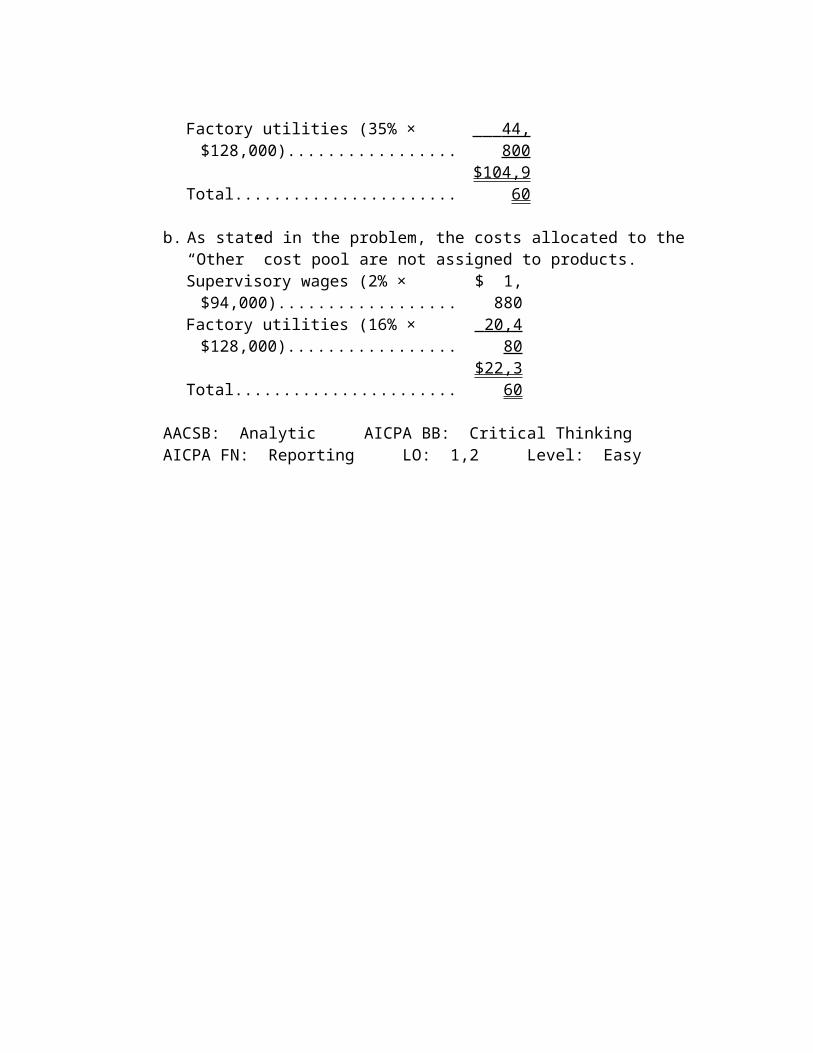

a. Allocations to the Unit Processing activity cost pool:Supervisory wages (64% × $94,000)......... $ 60,160Factory utilities (35% × $128,000)............ 44,800 Total........................................................... $104,960

b. As stated in the problem, the costs allocated to the “Other” cost pool are not assigned to products.Supervisory wages (2% × $94,000)........... $ 1,880Factory utilities (16% × $128,000)............ 20,480 Total........................................................... $22,360

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1,2 Level: Easy

chapter

86. The following data have been provided by Hooey Corporation from its activity-based costing accounting system:

Supervisory wages............. $46,000Factory utilities.................. $199,000

Distribution of Resource Consumption across Activity Cost Pools:

Activity Cost Pools Product

Change-Overs Machining Other TotalSupervisory wages....... 59% 33% 8% 100%Factory utilities............ 18% 69% 13% 100%

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs that are not assigned to products.

Required:

a. Determine the total amount of supervisory wages and factory utilities costs that would be allocated to the Machining activity cost pool. Show your work!

b. Determine the total amount of supervisory wages and factory utilities costs that would NOT be assigned to products. Show your work!

Ans:

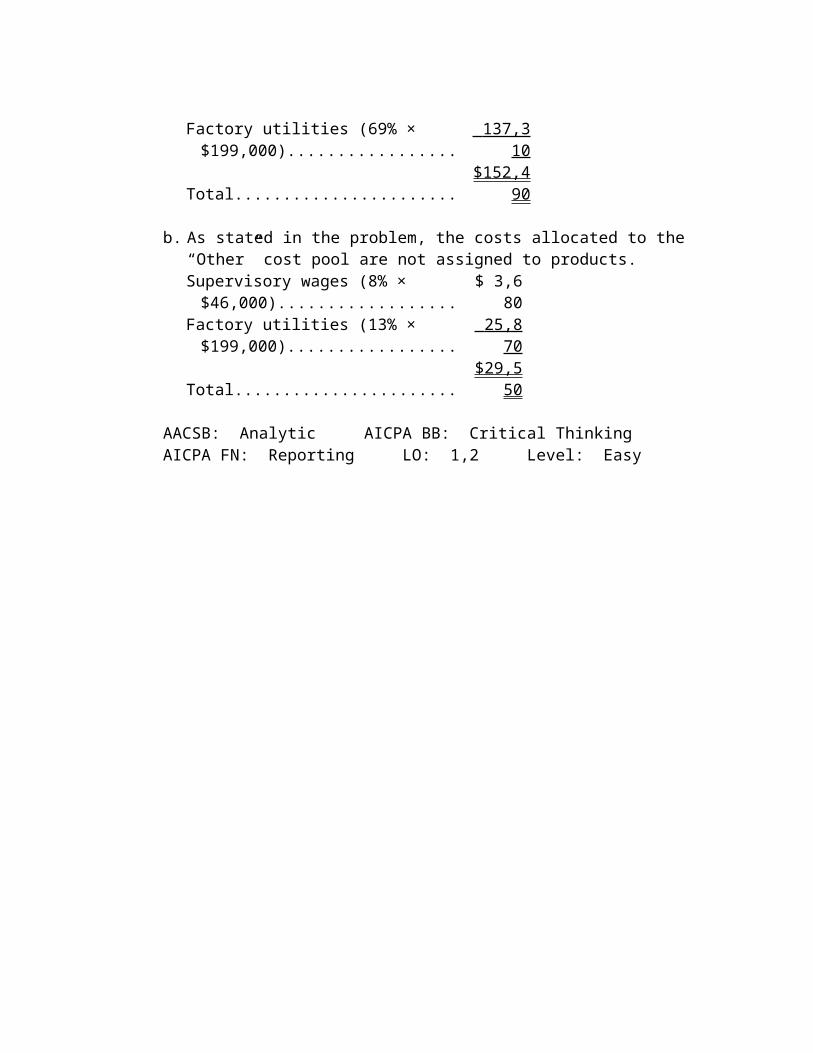

a. Allocations to the Machining activity cost pool:Supervisory wages (33% × $46,000)......... $ 15,180Factory utilities (69% × $199,000)............ 137,310 Total........................................................... $152,490

b. As stated in the problem, the costs allocated to the “Other” cost pool are not assigned to products.Supervisory wages (8% × $46,000)........... $ 3,680Factory utilities (13% × $199,000)............ 25,870 Total........................................................... $29,550

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1,2 Level: Easy

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-7

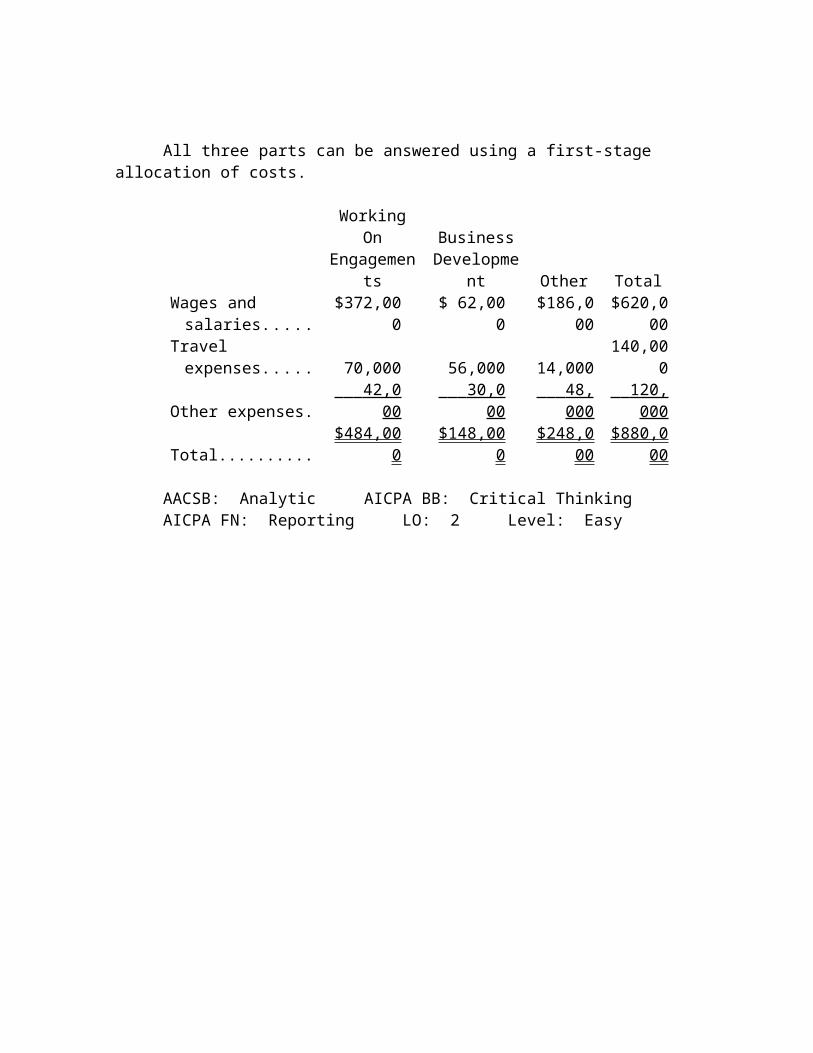

87. Fidler & Jenkins PLC, a consulting firm, uses an activity-based costing in which there are three activity cost pools. The company has provided the following data concerning its costs and its activity based costing system:

Costs:Wages and salaries............. $620,000Travel expenses.................. 140,000Other expenses................... 120,000 Total................................... $880,000

Distribution of resource consumption:

Activity Cost PoolsWorking On Engagements

Business Development Other Total

Wages and salaries....... 60% 10% 30% 100%Travel expenses............ 50% 40% 10% 100%Other expenses............. 35% 25% 40% 100%

Required:

a. How much cost, in total, would be allocated to the Working On Engagements activity cost pool?

b. How much cost, in total, would be allocated to the Business Development activity cost pool?

c. How much cost, in total, would be allocated to the Other activity cost pool?

Ans:

All three parts can be answered using a first-stage allocation of costs.

Working On Engagements

Business Development Other Total

Wages and salaries..... $372,000 $ 62,000 $186,000 $620,000Travel expenses.......... 70,000 56,000 14,000 140,000Other expenses........... 42,000 30,000 48,000 120,000 Total........................... $484,000 $148,000 $248,000 $880,000

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Easy

chapter

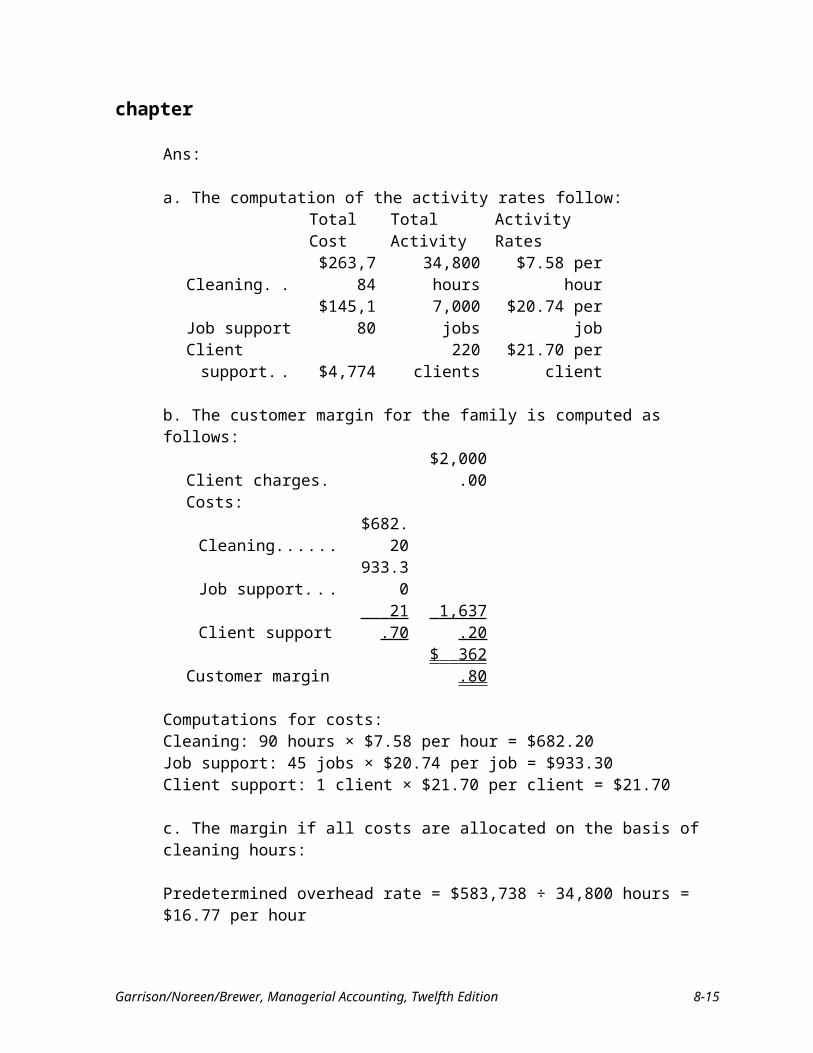

88. Dane Housecleaning provides housecleaning services to its clients. The company uses an activity-based costing system for its overhead costs. The company has provided the following data from its activity-based costing system.

Activity Cost Pool Total Cost Total ActivityCleaning.................... $263,784 34,800 hoursJob support................ 145,180 7,000 jobsClient support............ 4,774 220 clientsOther......................... 170,000 Not applicableTotal.......................... $583,738

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs.

One particular client, the Hoium family, requested 45 jobs during the year that required a total of 90 hours of housecleaning. For this service, the client was charged $2,000.

Required:

a. Compute the activity rates (i.e., cost per unit of activity) for the activity cost pools. Round off all calculations to the nearest whole cent.

b. Using the activity-based costing system, compute the customer margin for the Hoium family. Round off all calculations to the nearest whole cent.

c. Assume the company decides instead to use a traditional costing system in which ALL costs are allocated to customers on the basis of cleaning hours. Compute the margin for the Hoium family. Round off all calculations to the nearest whole cent.

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-9

Ans:

a. The computation of the activity rates follow:Total Cost Total Activity Activity Rates

Cleaning........... $263,784 34,800 hours $7.58 per hourJob support....... $145,180 7,000 jobs $20.74 per jobClient support... $4,774 220 clients $21.70 per client

b. The customer margin for the family is computed as follows:Client charges............... $2,000.00Costs:

Cleaning.................... $682.20Job support................ 933.30Client support............ 21.70 1,637.20

Customer margin.......... $ 362.80

Computations for costs:Cleaning: 90 hours × $7.58 per hour = $682.20Job support: 45 jobs × $20.74 per job = $933.30Client support: 1 client × $21.70 per client = $21.70

c. The margin if all costs are allocated on the basis of cleaning hours:

Predetermined overhead rate = $583,738 ÷ 34,800 hours = $16.77 per hour

Client charges..................... $2,000.00Allocated costs*................. 1,509.30 Customer margin................ $ 490.70

* 90 hours × $16.77 per hour = $1,509.30

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3,4,5 Level: Medium

chapter

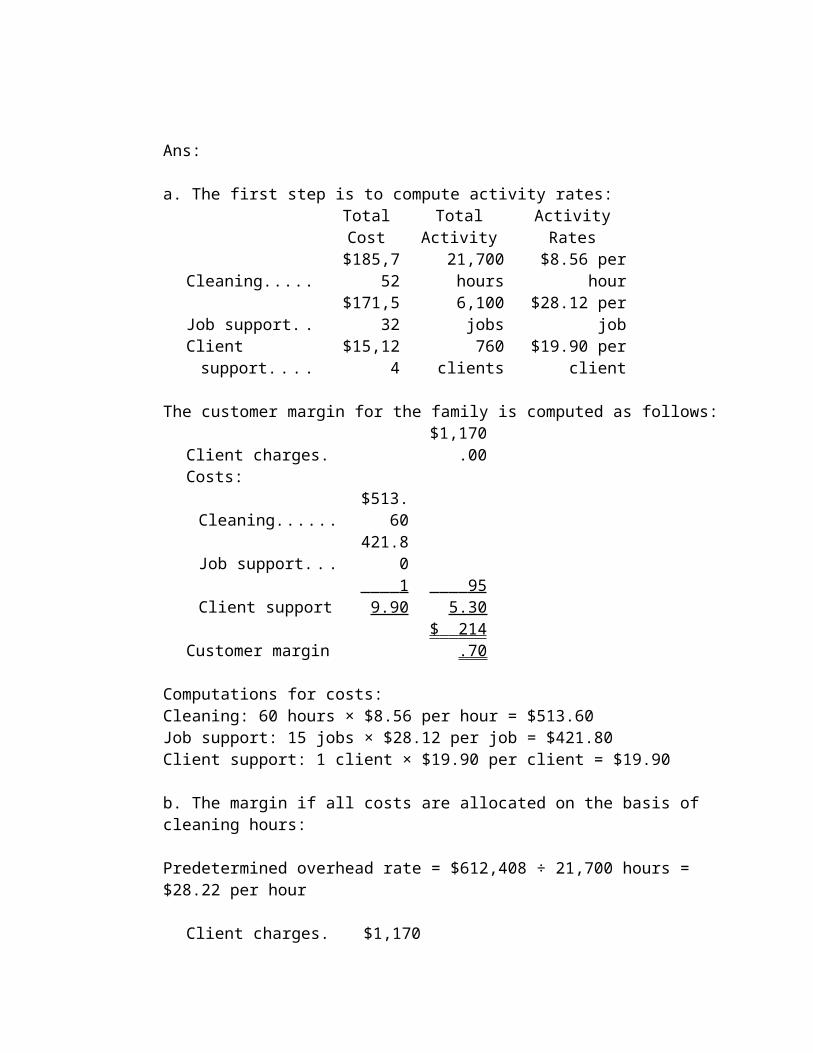

89. The Kamienski Cleaning Brigade Company provides housecleaning services to its clients. The company uses an activity-based costing system for its overhead costs. The company has provided the following data from its activity-based costing system.

Activity Cost Pool Total Cost Total ActivityCleaning................. $185,752 21,700 hoursJob support............. 171,532 6,100 jobsClient support......... 15,124 760 clientsOther...................... 240,000 Not applicableTotal....................... $612,408

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs.One particular client, the Whiddon family, requested 15 jobs during the year that required a total of 60 hours of housecleaning. For this service, the client was charged $1,170.

Required:

a. Using the activity-based costing system, compute the customer margin for the Whiddon family. Round off all calculations to the nearest whole cent.

b. Assume the company decides instead to use a traditional costing system in which ALL costs are allocated to customers on the basis of cleaning hours. Compute the margin for the Whiddon family. Round off all calculations to the nearest whole cent.

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-11

Ans:

a. The first step is to compute activity rates:Total Cost Total Activity Activity Rates

Cleaning................. $185,752 21,700 hours $8.56 per hourJob support............. $171,532 6,100 jobs $28.12 per jobClient support......... $15,124 760 clients $19.90 per client

The customer margin for the family is computed as follows:Client charges............... $1,170.00Costs:

Cleaning.................... $513.60Job support................ 421.80Client support............ 19.90 955.30

Customer margin.......... $ 214.70

Computations for costs:Cleaning: 60 hours × $8.56 per hour = $513.60Job support: 15 jobs × $28.12 per job = $421.80Client support: 1 client × $19.90 per client = $19.90

b. The margin if all costs are allocated on the basis of cleaning hours:

Predetermined overhead rate = $612,408 ÷ 21,700 hours = $28.22 per hour

Client charges............... $1,170.00Allocated costs*........... 1,693.20 Customer margin.......... ($523.20)

* 60 hours × $28.22 per hour = $1,693.20

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3,4,5 Level: Medium

chapter

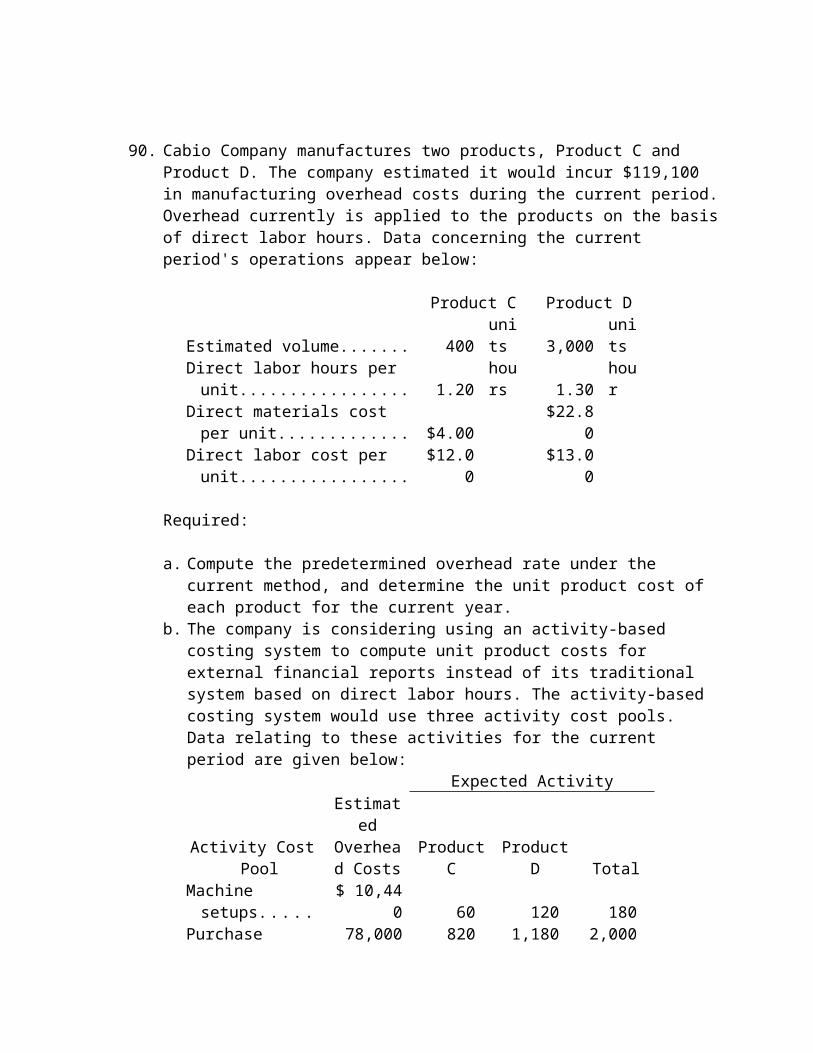

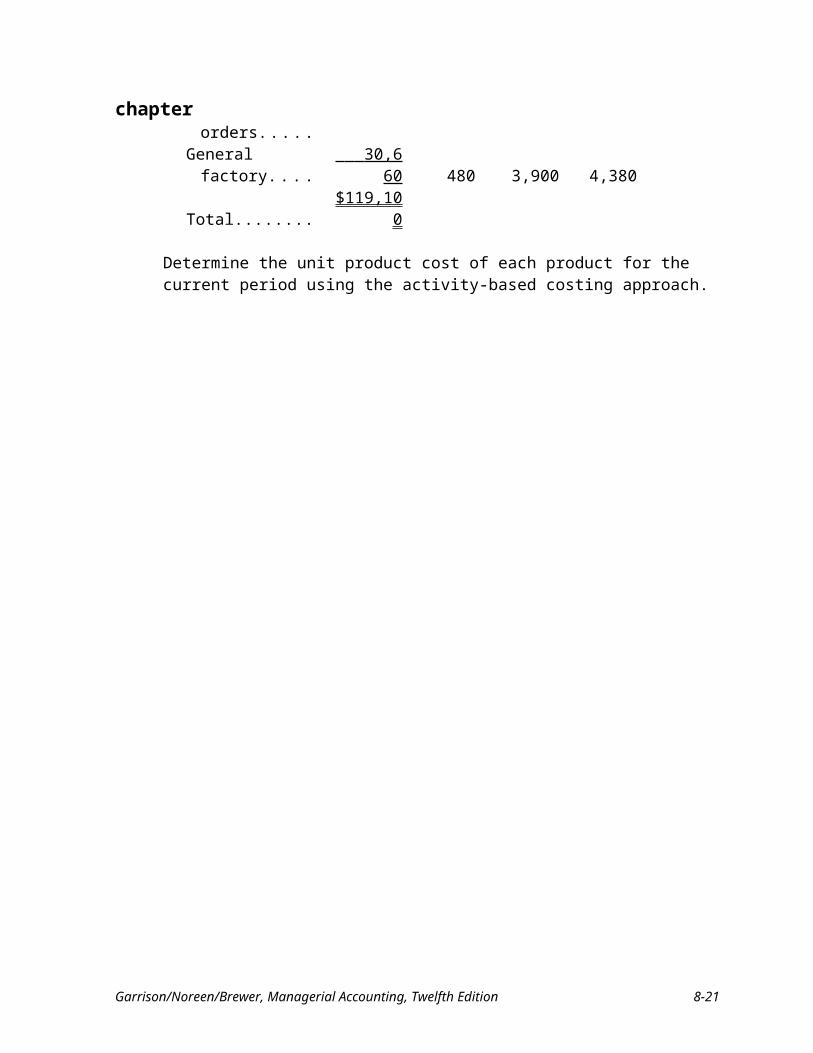

90. Cabio Company manufactures two products, Product C and Product D. The company estimated it would incur $119,100 in manufacturing overhead costs during the current period. Overhead currently is applied to the products on the basis of direct labor hours. Data concerning the current period's operations appear below:

Product C Product DEstimated volume........................... 400 units 3,000 unitsDirect labor hours per unit............. 1.20 hours 1.30 hourDirect materials cost per unit......... $4.00 $22.80Direct labor cost per unit................ $12.00 $13.00

Required:

a. Compute the predetermined overhead rate under the current method, and determine the unit product cost of each product for the current year.

b. The company is considering using an activity-based costing system to compute unit product costs for external financial reports instead of its traditional system based on direct labor hours. The activity-based costing system would use three activity cost pools. Data relating to these activities for the current period are given below:

Expected Activity

Activity Cost Pool

Estimated Overhead

Costs Product C Product D TotalMachine setups....... $ 10,440 60 120 180Purchase orders...... 78,000 820 1,180 2,000General factory....... 30,660 480 3,900 4,380Total....................... $119,100

Determine the unit product cost of each product for the current period using the activity-based costing approach.

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-13

Ans:

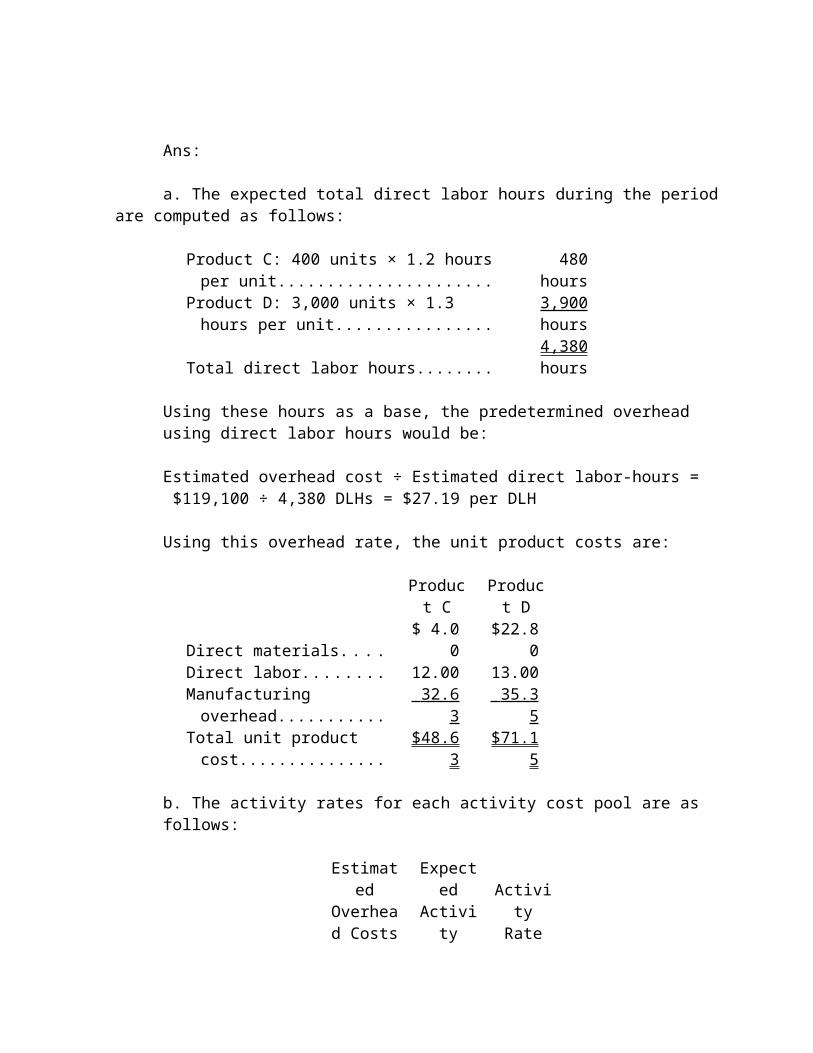

a. The expected total direct labor hours during the period are computed as follows:

Product C: 400 units × 1.2 hours per unit........... 480 hoursProduct D: 3,000 units × 1.3 hours per unit........ 3,900 hoursTotal direct labor hours....................................... 4,380 hours

Using these hours as a base, the predetermined overhead using direct labor hours would be:

Estimated overhead cost ÷ Estimated direct labor-hours = $119,100 ÷ 4,380 DLHs = $27.19 per DLH

Using this overhead rate, the unit product costs are:

Product C Product DDirect materials........................ $ 4.00 $22.80Direct labor.............................. 12.00 13.00Manufacturing overhead.......... 32.63 35.35 Total unit product cost............. $48.63 $71.15

b. The activity rates for each activity cost pool are as follows:

Estimated Overhead

CostsExpected Activity

Activity Rate

Machine setups....... $10,440 180 $58.00Purchase orders...... $78,000 2,000 $39.00General factory....... $30,660 4,380 $7.00

The overhead cost charged to each product is:

Product C Product DActivity Amount Activity Amount

Machine setups.......... 60 $ 3,480 120 $ 6,960Purchase orders......... 820 31,980 1,180 46,020General factory.......... 480 3,360 3,900 27,300 Total overhead cost... $38,820 $80,280

chapter

Overhead cost per unit:Product C: $38,820 ÷ 400 units = $97.05 per unitProduct D: $80,280 ÷ 3,000 units = $26.76 per unit

Using activity based costing, the unit product cost of each product would be:

Product C Product DDirect materials.............................. $ 4.00 $22.80Direct labor.................................... 12.00 13.00Manufacturing overhead................ 97.05 26.76 Total unit product cost................... $113.05 $62.56

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 7 Level: Hard

91. Danton Company manufactures two products, Product F and Product G. The company expects to produce and sell 600 units of Product F and 3,000 units of Product G during the current year. The company uses activity-based costing to compute unit product costs for external reports. Data relating to the company's three activity cost pools are given below for the current year:

Expected Activity

Activity Cost Pool

Estimated Overhead

Costs Product F Product G TotalMachine setups....... $13,720 140 140 280Purchase orders...... $74,730 630 960 1,590General factory....... $15,000 600 2,400 3,000

Required:

Using the activity-based costing approach, determine the overhead cost per unit for each product.

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-15

Ans:

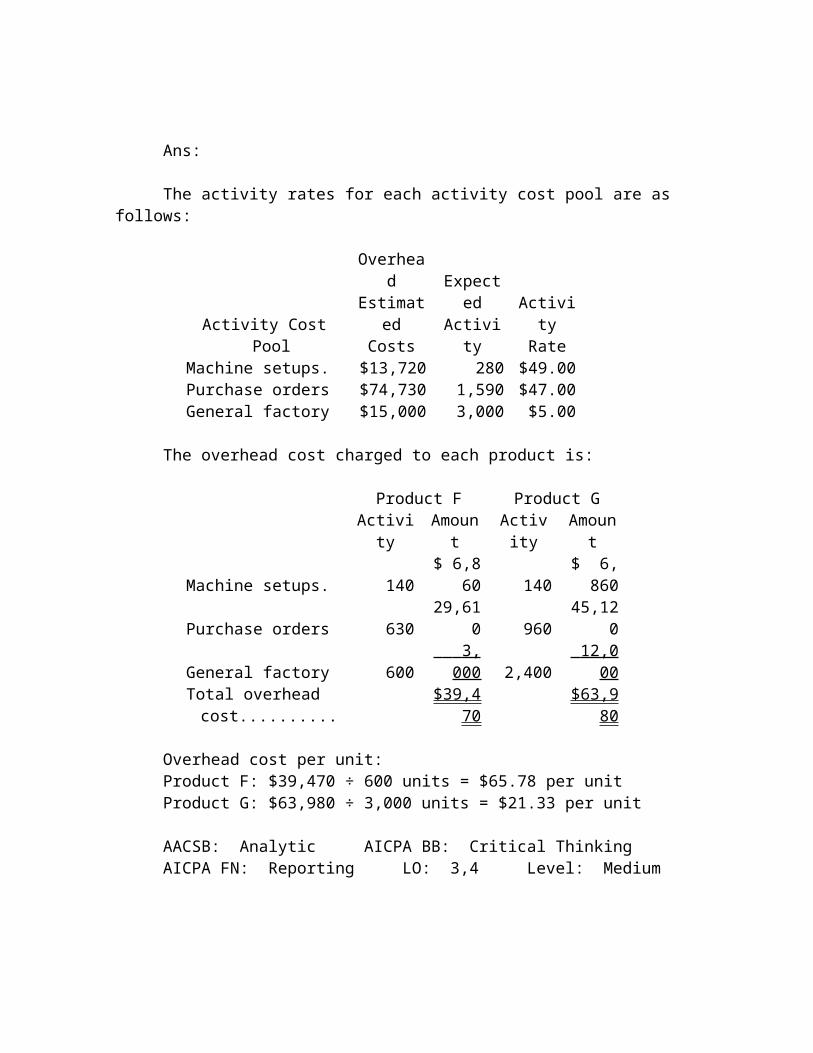

The activity rates for each activity cost pool are as follows:

Activity Cost Pool

Overhead Estimated

CostsExpected Activity

Activity Rate

Machine setups............. $13,720 280 $49.00Purchase orders............ $74,730 1,590 $47.00General factory............. $15,000 3,000 $5.00

The overhead cost charged to each product is:

Product F Product GActivity Amount Activity Amount

Machine setups............. 140 $ 6,860 140 $ 6,860Purchase orders............ 630 29,610 960 45,120General factory............. 600 3,000 2,400 12,000 Total overhead cost...... $39,470 $63,980

Overhead cost per unit:Product F: $39,470 ÷ 600 units = $65.78 per unitProduct G: $63,980 ÷ 3,000 units = $21.33 per unit

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3,4 Level: Medium

chapter

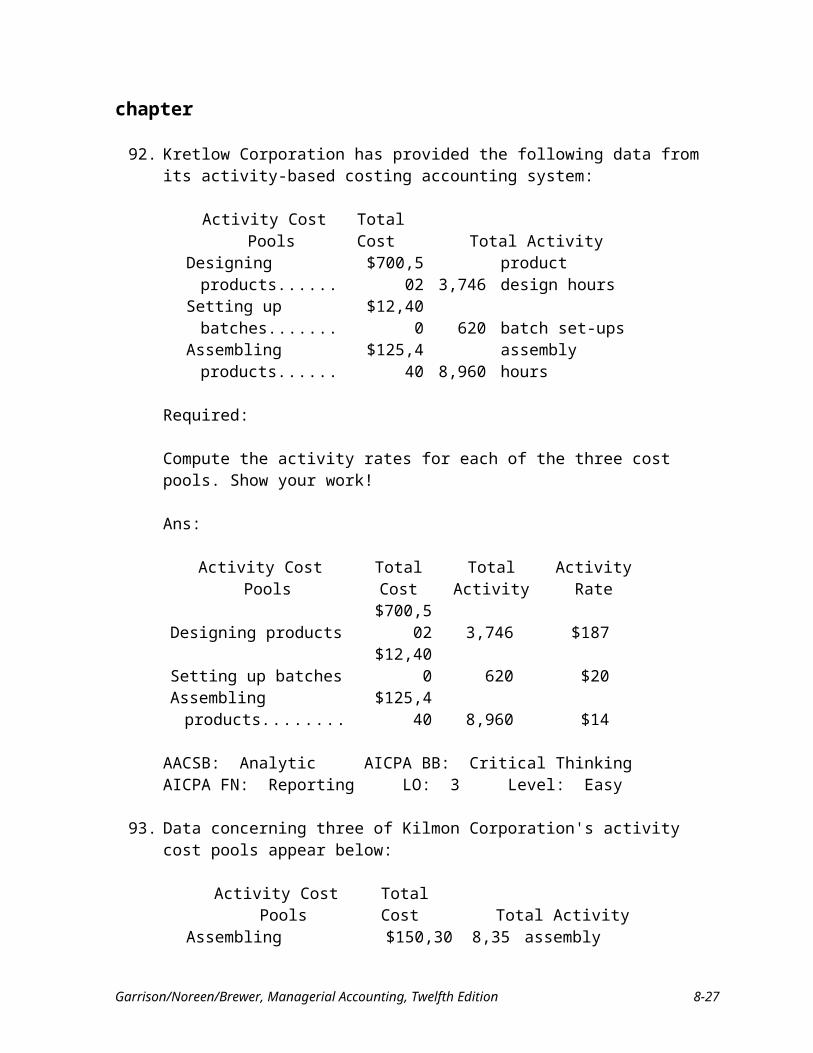

92. Kretlow Corporation has provided the following data from its activity-based costing accounting system:

Activity Cost Pools Total Cost Total ActivityDesigning products...... $700,502 3,746 product design hoursSetting up batches........ $12,400 620 batch set-upsAssembling products.... $125,440 8,960 assembly hours

Required:

Compute the activity rates for each of the three cost pools. Show your work!

Ans:

Activity Cost Pools Total Cost Total Activity Activity RateDesigning products............ $700,502 3,746 $187Setting up batches.............. $12,400 620 $20Assembling products.......... $125,440 8,960 $14

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3 Level: Easy

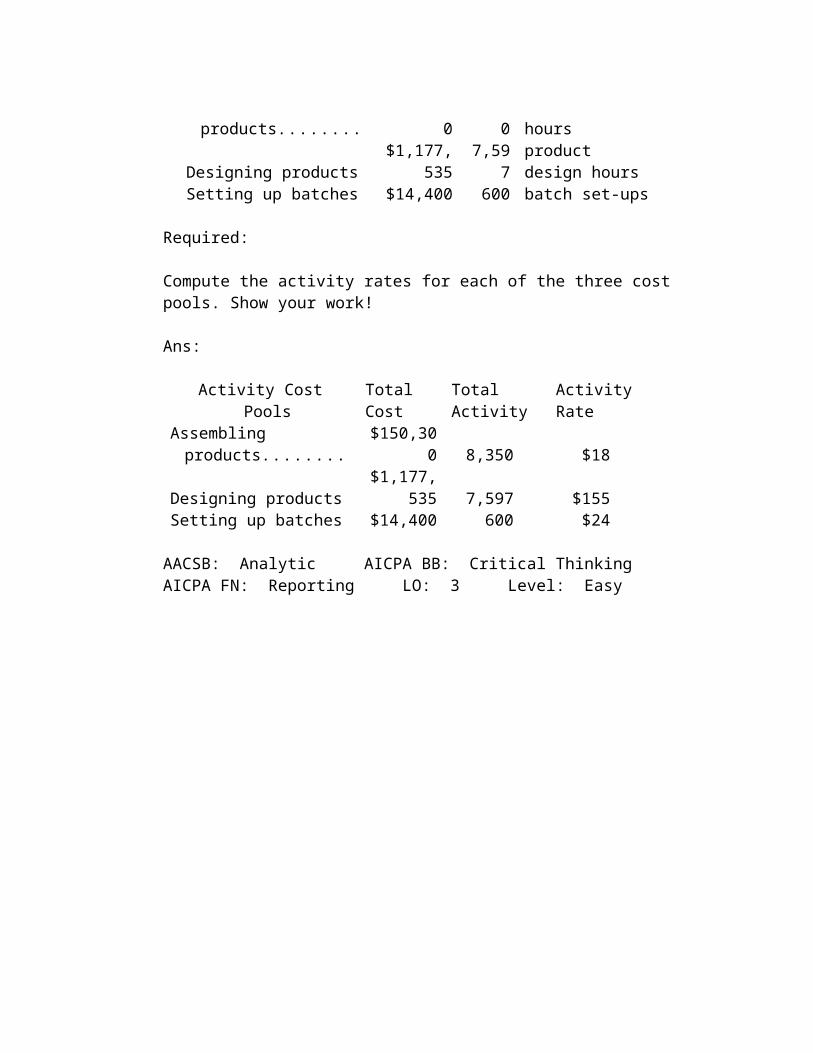

93. Data concerning three of Kilmon Corporation's activity cost pools appear below:

Activity Cost Pools Total Cost Total ActivityAssembling products.......... $150,300 8,350 assembly hoursDesigning products............ $1,177,535 7,597 product design hoursSetting up batches.............. $14,400 600 batch set-ups

Required:

Compute the activity rates for each of the three cost pools. Show your work!

Ans:

Activity Cost Pools Total Cost Total Activity Activity RateAssembling products.......... $150,300 8,350 $18Designing products............ $1,177,535 7,597 $155Setting up batches.............. $14,400 600 $24

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3 Level: Easy

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-17

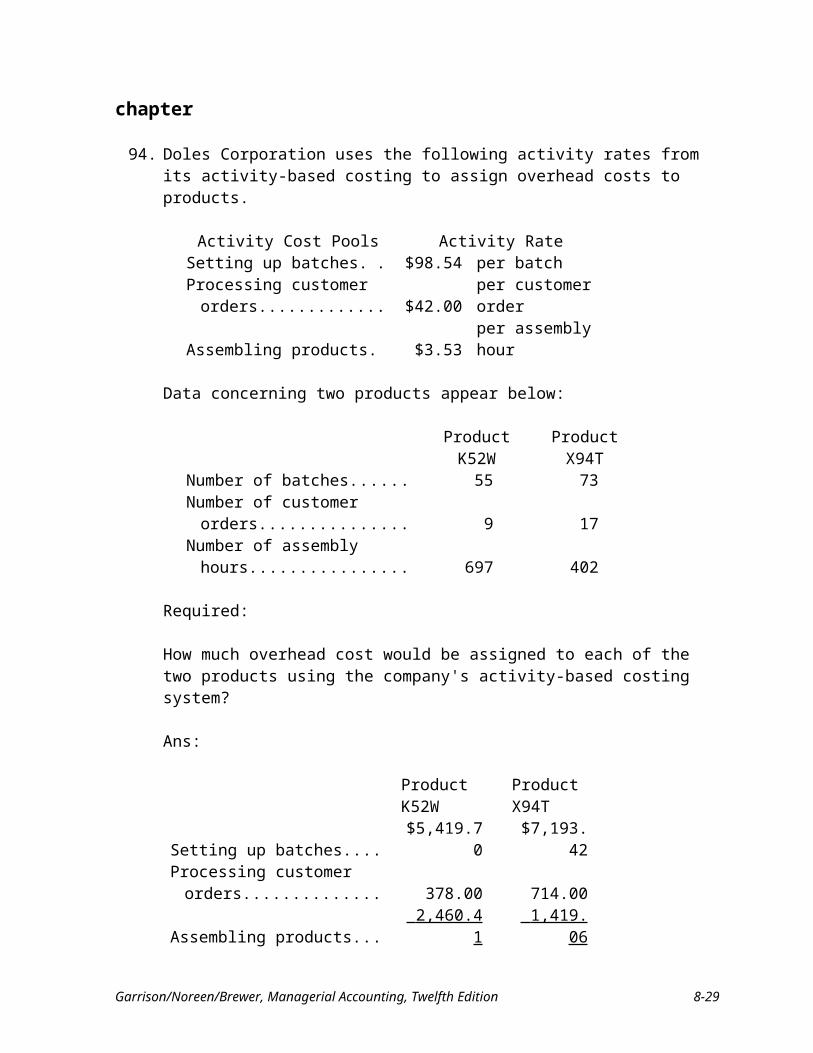

94. Doles Corporation uses the following activity rates from its activity-based costing to assign overhead costs to products.

Activity Cost Pools Activity RateSetting up batches.................... $98.54 per batchProcessing customer orders...... $42.00 per customer orderAssembling products................ $3.53 per assembly hour

Data concerning two products appear below:

Product K52W Product X94TNumber of batches......................... 55 73Number of customer orders........... 9 17Number of assembly hours............ 697 402

Required:

How much overhead cost would be assigned to each of the two products using the company's activity-based costing system?

Ans:

Product K52W Product X94TSetting up batches....................... $5,419.70 $7,193.42Processing customer orders......... 378.00 714.00Assembling products................... 2,460.41 1,419.06 Total overhead cost..................... $8,258.11 $9,326.48

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Easy

chapter

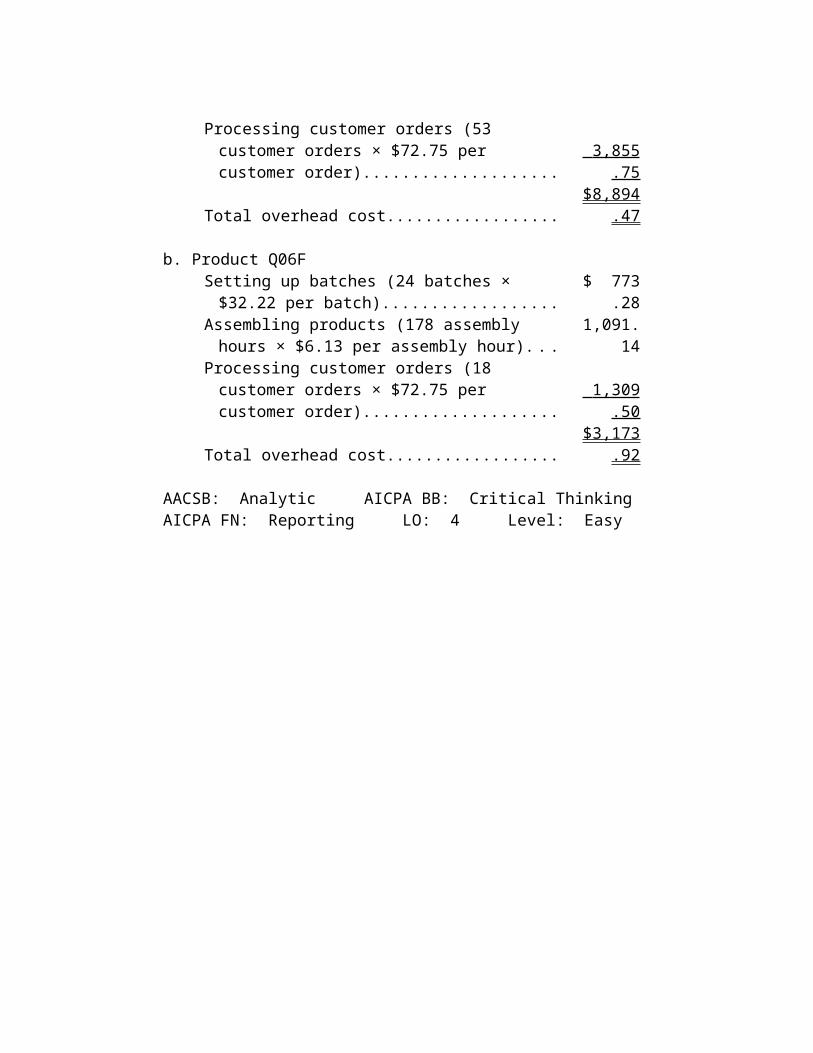

95. Desjarlais Corporation uses the following activity rates from its activity-based costing to assign overhead costs to products.

Activity Cost Pools Activity RateSetting up batches.......................... $32.22 per batchAssembling products...................... $6.13 per assembly hourProcessing customer orders............ $72.75 per customer order

Data concerning two products appear below:

Product S96U Product Q06FNumber of batches......................... 78 24Number of assembly hours............ 412 178Number of customer orders........... 53 18

Required:

a. How much overhead cost would be assigned to Product S96U using the company's activity-based costing system? Show your work!

b. How much overhead cost would be assigned to Product Q06F using the company's activity-based costing system? Show your work!

Ans:

a. Product S96USetting up batches (78 batches × $32.22 per batch)........ $2,513.16Assembling products (412 assembly hours × $6.13 per

assembly hour)............................................................ 2,525.56Processing customer orders (53 customer orders ×

$72.75 per customer order)......................................... 3,855.75 Total overhead cost......................................................... $8,894.47

b. Product Q06FSetting up batches (24 batches × $32.22 per batch)........ $ 773.28Assembling products (178 assembly hours × $6.13 per

assembly hour)............................................................ 1,091.14Processing customer orders (18 customer orders ×

$72.75 per customer order)......................................... 1,309.50 Total overhead cost......................................................... $3,173.92

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Easy

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-19

96. Archie Corporation uses the following activity rates from its activity-based costing to assign overhead costs to products.

Activity Cost Pools Activity RateSetting up batches.................... $16.68 per batchProcessing customer orders...... $98.60 per customer orderAssembling products................ $7.89 per assembly hour

Last year, Product X26X involved 18 batches, 4 customer orders, and 103 assembly hours.

Required:

How much overhead cost would be assigned to Product X26X using the company's activity-based costing system? Show your work!

Ans:

Setting up batches (18 batches × $16.68 per batch)........ $ 300.24Processing customer orders (4 customer orders ×

$98.60 per customer order)......................................... 394.40Assembling products (103 assembly hours × $7.89 per

assembly hour)............................................................ 812.67 Total overhead cost......................................................... $1,507.31

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Easy

chapter

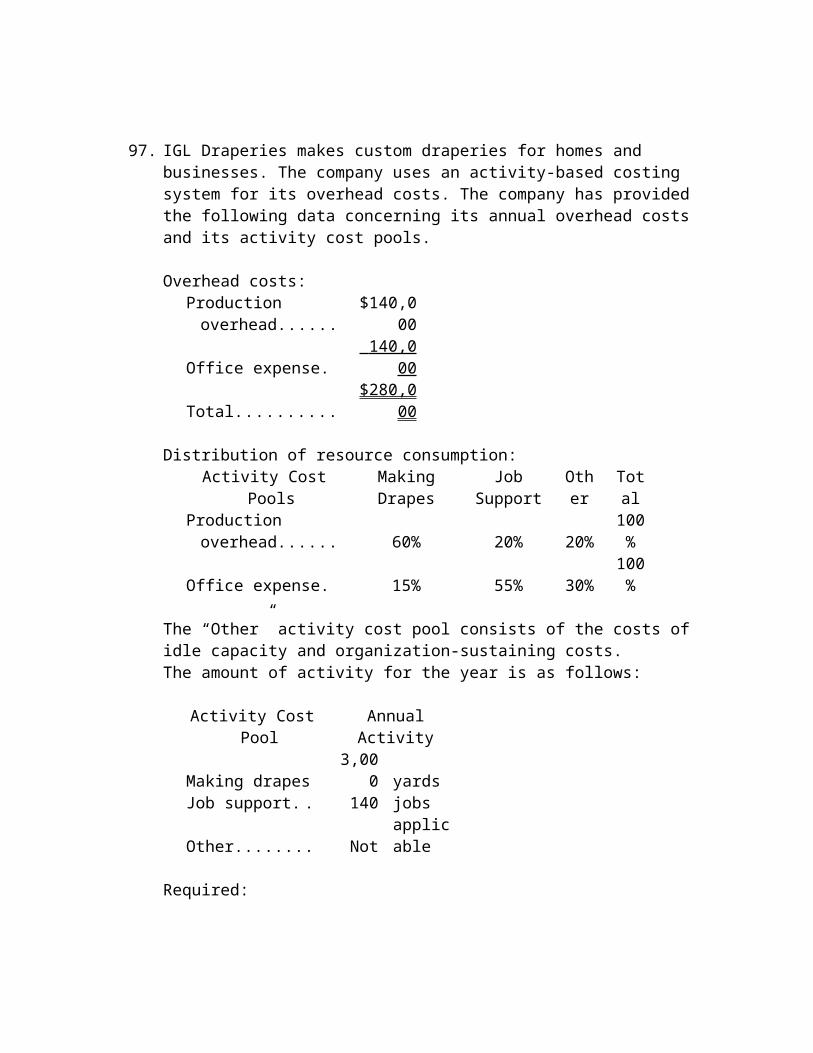

97. IGL Draperies makes custom draperies for homes and businesses. The company uses an activity-based costing system for its overhead costs. The company has provided the following data concerning its annual overhead costs and its activity cost pools.

Overhead costs:Production overhead.... $140,000Office expense............. 140,000 Total............................. $280,000

Distribution of resource consumption:Activity Cost Pools Making Drapes Job Support Other Total

Production overhead.... 60% 20% 20% 100%Office expense............. 15% 55% 30% 100%

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs.The amount of activity for the year is as follows:

Activity Cost Pool Annual ActivityMaking drapes........ 3,000 yardsJob support............. 140 jobsOther...................... Not applicable

Required:

a. Prepare the first-stage allocation of overhead costs to the activity cost pools by filling in the table below:

Making Drapes

Job Support Other Total

Production overhead....Office expense.............Total.............................

b. Compute the activity rates (i.e., cost per unit of activity) for the Making Drapes and Job Support activity cost pools by filling in the table below:

Making Drapes Job SupportProduction overhead....Office expense.............Total.............................

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-21

c. Prepare an action analysis report in good form of a job that involves making 85 yards of drapes and has direct materials and direct labor cost of $2,990. The sales revenue from this job is $6,000. For purposes of this action analysis report, direct materials and direct labor should be classified as a Green cost; production overhead as a Red cost; and office expense as a Yellow cost.

Ans:

a. First-stage allocationMaking Drapes Job Support Other Total

Production overhead.... $84,000 $28,000 $28,000 $140,000Office expense............. 21,000 77,000 42,000 140,000Total............................. $105,000 $105,000 $70,000 $280,000Activity........................ 3,000 yards 140 jobs

b. Activity rates (costs divided by activity)Making JobDrapes Support

Activity........................ 3,000 yards 140 jobs

Production overhead.... $28.00 $200.00Office expense............. 7.00 550.00 Total............................. $35.00 $750.00

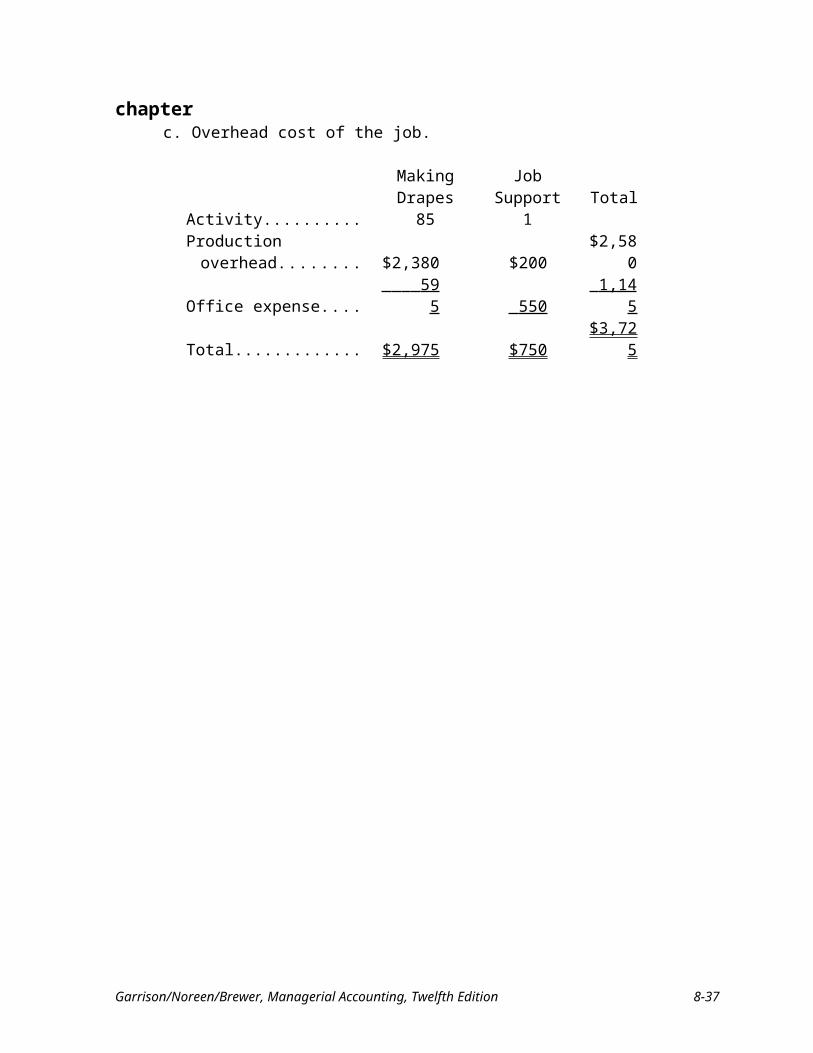

c. Overhead cost of the job.

Making Drapes Job Support TotalActivity.............................. 85 1Production overhead.......... $2,380 $200 $2,580Office expense................... 595 550 1,145 Total................................... $2,975 $750 $3,725

chapter

Sales............................................... $6,000Green costs:

Direct materials and labor........... 2,990 Green margin................................. 3,010Yellow costs:

Office expense............................ 1,145 Yellow margin............................... 1,865Red costs:

Production overhead................... 2,580Red margin..................................... ($ 715 )

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 8A LO: 6 Level: Hard

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-23

98. Haskell Hardwood Floors installs oak and other hardwood floors in homes and businesses. The company uses an activity-based costing system for its overhead costs. The company has provided the following data concerning its annual overhead costs and its activity based costing system:

Overhead costs:Production overhead.......... $120,000Office expense................... 140,000 Total................................... $260,000

Distribution of resource consumption:

Installing JobActivity Cost Pools Floors Support Other Total

Production overhead.......... 55% 25% 20% 100%Office expense................... 20% 50% 30% 100%

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs.

The amount of activity for the year is as follows:

Activity Cost Pool Annual ActivityInstalling floors...... 800 squaresJob support............. 100 jobsOther...................... Not applicable

A “square” is a measure of area that is roughly equivalent to 1,000 square feet.

Required:

a. Prepare the first-stage allocation of overhead costs to the activity cost pools by filling in the table below:

Installing JobFloors Support Other Total

Production overhead..........Office expense...................Total...................................

chapter

b. Compute the activity rates (i.e., cost per unit of activity) for the Installing Floors and Job Support activity cost pools by filling in the table below:

Installing JobFloors Support

Production overhead..........Office expense...................Total...................................

c. Compute the overhead cost, according to the activity-based costing system, of a job that involves installing 3.2 squares.

Ans:

a. First-stage allocationInstalling Job

Floors Support Other TotalProduction overhead.... $66,000 $ 30,000 $24,000 $120,000Office expense............. 28,000 70,000 42,000 140,000 Total............................. $94,000 $100,000 $66,000 $260,000

b. Activity rates (costs divided by activity)

Installing JobFloors Support

Activity.............................. 800 squares 100 jobs

Production overhead.......... $ 82.50 $ 300.00Office expense................... 35.00 700.00 Total................................... $117.50 $1,000.00

c. Overhead cost of the job.Installing Job

Floors Support TotalActivity........................ 3.2 1

Production overhead.... $264.00 $ 300.00 $ 564.00Office expense............. 112.00 700.00 812.00 Total............................. $376.00 $1,000.00 $1,376.00

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 8A LO: 6 Level: Medium

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-25

99. Golden Company, a wholesale distributor, uses activity-based costing for its overhead costs. The company has provided the following data concerning its annual overhead costs and its activity based costing system:

Overhead costs:Wages and salaries....... $680,000Nonwage expenses....... 120,000 Total............................. $800,000

Distribution of resource consumption:

Filling ProductActivity Cost Pools Orders Support Other Total

Wages and salaries............. 15% 75% 10% 100%Nonwage expenses............. 25% 55% 20% 100%

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs.The amount of activity for the year is as follows:

Activity Cost Pool Annual ActivityFilling orders............. 4,000 ordersProduct support......... 40 productsOther......................... Not applicable

Required:

Compute the activity rates (i.e., cost per unit of activity) for the Filling Orders and Product Support activity cost pools by filling in the table below:

Filling ProductOrders Support Other Total

Wages and salaries.............Nonwage expenses.............

chapter

Ans:

First-stage allocationFilling ProductOrders Support Other Total

Wages and salaries....... $102,000 $510,000 $68,000 $680,000Nonwage expenses....... 30,000 66,000 24,000 120,000 Total............................. $132,000 $576,000 $92,000 $800,000

Filling ProductOrders Support

Activity....................................... 4,000 orders 40 products

Wages and salaries...................... $25.50 $12,750Nonwage expenses...................... 7.50 1,650 Total............................................ $33.00 $14,400

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 8A LO: 6 Level: Medium

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-27

100. Jared Painting paints the interiors and exteriors of homes and commercial buildings. The company uses an activity-based costing system for its overhead costs. The company has provided the following data concerning its activity-based costing system.

Activity Cost Pool Activity Measure Annual ActivityPainting overhead............... Square meters 10,000 square metersJob support......................... Jobs 200 jobsOther.................................. None Not applicable

The “Other” activity cost pool consists of the costs of idle capacity and organization-sustaining costs.

The company has already finished the first stage of the allocation process in which costs were allocated to the activity cost centers. The results are listed below:

JobPainting Support Other Total

Painting overhead...... $ 99,000 $ 45,000 $36,000 $180,000Office expense.......... 6,000 78,000 36,000 120,000 Total.......................... $105,000 $123,000 $72,000 $300,000

Required:

a. Compute the activity rates (i.e., cost per unit of activity) for the Painting and Job Support activity cost pools by filling in the table below. Round off all calculations to the nearest whole cent.

JobPainting Support

Painting overhead......Office expense..........Total..........................

b. Prepare an action analysis report in good form of a job that involves painting 71 square meters and has direct materials and direct labor cost of $2,410. The sales revenue from this job is $3,800.

For purposes of this action analysis report, direct materials and direct labor should be classified as a Green cost; painting overhead as a Red cost; and office expense as a Yellow cost.

chapterAns:

a. Activity rates (costs divided by activity)Job

Painting SupportPainting overhead...... $ 9.90 $225.00Office expense.......... 0.60 390.00 Total.......................... $10.50 $615.00

b. Overhead cost of the job.Job

Painting Support TotalActivity........................ 71 1

Painting overhead......... $702.90 $225.00 $ 927.90Office expense............. 42.60 390.00 432.60 Total............................. $745.50 $615.00 $1,360.50

Sales............................................... $3,800.00Green costs:

Direct materials and labor........... 2,410.00 Green margin................................. 1,390.00Yellow costs:

Office expense............................ 432.60 Yellow margin............................... 957.40Red costs:

Painting overhead....................... 927.90 Red margin..................................... $ 29.50

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 8A LO: 6 Level: Medium

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-29

101. Werger Manufacturing Corporation has a traditional costing system in which it applies manufacturing overhead to its products using a predetermined overhead rate based on direct labor-hours (DLHs). The company has two products, W82R and L48S, about which it has provided the following data:

W82R L48SDirect materials per unit................. $11.50 $62.90Direct labor per unit....................... $2.00 $13.00Direct labor-hours per unit............. 0.20 1.30Annual production......................... 45,000 10,000

The company’s estimated total manufacturing overhead for the year is $1,521,960 and the company’s estimated total direct labor-hours for the year is 22,000.

The company is considering using a variation of activity-based costing to determine its unit product costs for external reports. Data for this proposed activity-based costing system appear below:

Activities and Activity Measures Estimated Overhead CostSupporting direct labor (DLHs)........... $ 352,000Setting up machines (setups)............... 201,960Parts administration (part types).......... 968,000 Total..................................................... $1,521,960

Activities W82R L48S TotalSupporting direct labor...... 9,000 13,000 22,000Setting up machines........... 814 374 1,188Parts administration........... 924 1,012 1,936

Required:

a. Determine the unit product cost of each of the company's two products under the traditional costing system.

b. Determine the unit product cost of each of the company's two products under activity-based costing system.

chapter

Ans:

a. Traditional Unit Product CostsPredetermined overhead rate = $1,521,960 ÷ 22,000 DLHs = $69.18 per DLH

W82R L48SDirect materials............................................................... $11.50 $ 62.90Direct labor..................................................................... 2.00 13.00Manufacturing overhead (0.2 DLHs × $69.18 per DLH;

1.3 DLHs × $69.18 per DLH)..................................... 13.84 89.93 Unit product cost............................................................. $27.34 $165.83

b. ABC Unit Product CostsEstimated Overhead

CostTotal Expected

Activity Activity RateSupporting direct labor. . . $352,000 22,000 DLHs $16 per DLHSetting up machines........ $201,960 1,188 setups $170 per setupParts administration........ $968,000 1,936 part types $500 per part type

Overhead cost for W82R

Activity Rate ActivityABC Cost

Supporting direct labor. . . $16 per DLH 9,000 DLHs $144,000Setting up machines........ $170 per setup 814 setups 138,380Parts administration........ $500 per part type 924 part types 462,000 Total................................ $744,380

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-31

Overhead cost for L48S

Activity Rate ActivityABC Cost

Supporting direct labor. . . $16 per DLH 13,000 DLHs $208,000Setting up machines........ $170 per setup 374 setups 63,580Parts administration........ $500 per part type 1,012 part types 506,000 Total................................ $777,580

W82R L48SDirect materials............................................................... $11.50 $62.90Direct labor..................................................................... 2.00 13.00Manufacturing overhead ($744,400 ÷ 45,000 units;

$777,600 ÷ 10,000 units)............................................. 16.54 77.76 Unit product cost............................................................. $30.04 $153.66

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 8B LO: 7 Level: Medium

chapter

102. Torri Manufacturing Corporation has a traditional costing system in which it applies manufacturing overhead to its products using a predetermined overhead rate based on direct labor-hours (DLHs). The company has two products, B40W and C63J, about which it has provided the following data:

B40W C63JDirect materials per unit........... $34.90 $63.70Direct labor per unit................. $20.80 $62.40Direct labor-hours per unit....... 0.80 2.40Annual production................... 35,000 15,000

The company’s estimated total manufacturing overhead for the year is $2,656,000 and the company’s estimated total direct labor-hours for the year is 64,000.

The company is considering using a variation of activity-based costing to determine its unit product costs for external reports. Data for this proposed activity-based costing system appear below:

Activities and Activity Measures Estimated Overhead CostAssembling products (DLHs).............. $1,216,000Preparing batches (batches)................. 480,000Milling (MHs)...................................... 960,000 Total..................................................... $2,656,000

Activities B40W C63J TotalAssembling products.......... 28,000 36,000 64,000Preparing batches............... 2,304 2,496 4,800Milling................................ 1,088 2,112 3,200

Required:

a. Determine the unit product cost of each of the company's two products under the traditional costing system.

b. Determine the unit product cost of each of the company's two products under activity-based costing system.

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-33

Ans:

a. Traditional Unit Product CostsPredetermined overhead rate = $2,656,000 ÷ 64,000 DLHs = $41.50 per DLH

B40W C63JDirect materials............................................................... $34.90 $ 63.70Direct labor..................................................................... 20.80 62.40Manufacturing overhead (0.8 DLHs × $41.50 per DLH;

2.4 DLHs × $41.50 per DLH)..................................... 33.20 99.60 Unit product cost............................................................. $88.90 $225.70

b. ABC Unit Product CostsEstimated Overhead

CostTotal Expected

Activity Activity RateAssembling products.... $1,216,000 64,000 DLHs $19 per DLHPreparing batches......... $480,000 4,800 batches $100 per setupMilling.......................... $960,000 3,200 MHs $300 per MH

Overhead cost for B40WActivity Rate Activity ABC Cost

Assembling products.... $19 per DLH 28,000 DLHs $ 532,000Preparing batches......... $100 per setup 2,304 batches 230,400Milling.......................... $300 per MH 1,088 MHs 326,400 Total............................. $1,088,800

Overhead cost for C63JActivity Rate Activity ABC Cost

Assembling products.... $19 per DLH 36,000 DLHs $ 684,000Preparing batches......... $100 per setup 2,496 batches 249,600Milling.......................... $300 per MH 2,112 MHs 633,600 Total............................. $1,567,200

B40W C63JDirect materials............................................................... $34.90 $ 63.70Direct labor..................................................................... 20.80 62.40Manufacturing overhead ($1,088,800 ÷ 35,000 units;

$1,567,200 ÷ 15,000 units).......................................... 31.11 104.48 Unit product cost............................................................. $86.81 $230.58

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 8B LO: 7 Level: Medium

chapter

103. Welk Manufacturing Corporation has a traditional costing system in which it applies manufacturing overhead to its products using a predetermined overhead rate based on direct labor-hours (DLHs). The company has two products, H16Z and P25P, about which it has provided the following data:

H16Z P25PDirect materials per unit................. $10.20 $50.50Direct labor per unit....................... $8.40 $25.20Direct labor-hours per unit............. 0.40 1.20Annual production......................... 30,000 10,000

The company’s estimated total manufacturing overhead for the year is $1,464,480 and the company’s estimated total direct labor-hours for the year is 24,000.

The company is considering using a variation of activity-based costing to determine its unit product costs for external reports. Data for this proposed activity-based costing system appear below:

Activities and Activity Measures Estimated Overhead CostSupporting direct labor (DLHs)................. $ 552,000Setting up machines (setups)..................... 132,480Parts administration (part types)................ 780,000 Total........................................................... $1,464,480

H16Z P25P TotalSupporting direct labor...... 12,000 12,000 24,000Setting up machines........... 864 240 1,104Parts administration........... 600 960 1,560

Required:

a. Determine the manufacturing overhead cost per unit of each of the company's two products under the traditional costing system.

b. Determine the manufacturing overhead cost per unit of each of the company's two products under activity-based costing system.

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-35

Ans:

a. Traditional Manufacturing Overhead CostsPredetermined overhead rate = $1,464,480 ÷ 24,000 DLHs = $61.02 per DLH

H16Z P25PDirect labor-hours...................................... 0.40 1.20Predetermined overhead rate per DLH...... $61.02 $61.02Manufacturing overhead cost per unit....... $24.41 $73.22

b. ABC Manufacturing Overhead Costs

Estimated Overhead

CostTotal Expected

Activity Activity RateSupporting direct labor. . . $552,000 24,000 DLHs $23 per DLHSetting up machines........ $132,480 1,104 setups $120 per setupParts administration........ $780,000 1,560 part types $500 per part type

Overhead cost for H16Z

Activity Rate ActivityABC Cost

Supporting direct labor. . . $23 per DLH 12,000 DLHs $276,000Setting up machines........ $120 per setup 864 setups 103,680Parts administration........ $500 per part type 600 part types 300,000 Total................................ $679,680Annual production.......... 30,000Manufacturing overhead

cost per unit................. $22.66

Overhead cost for P25P

Activity Rate ActivityABC Cost

Supporting direct labor. . . $23 per DLH 12,000 DLHs $276,000Setting up machines........ $120 per setup 240 setups 28,800Parts administration........ $500 per part type 960 part types 480,000 Total................................ $784,800Annual production.......... 10,000Manufacturing overhead

cost per unit................. $78.48

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 8B LO: 7 Level: Medium

chapter

104. Bullie Manufacturing Corporation has a traditional costing system in which it applies manufacturing overhead to its products using a predetermined overhead rate based on direct labor-hours (DLHs). The company has two products, D31X and U75X, about which it has provided the following data:

D31X U75XDirect materials per unit........... $29.20 $47.40Direct labor per unit................. $1.10 $23.10Direct labor-hours per unit....... 0.10 2.10Annual production................... 35,000 15,000

The company’s estimated total manufacturing overhead for the year is $1,147,650 and the company’s estimated total direct labor-hours for the year is 35,000.

The company is considering using a variation of activity-based costing to determine its unit product costs for external reports. Data for this proposed activity-based costing system appear below:

Activities and Activity Measures Estimated Overhead CostAssembling products (DLHs)........ $ 140,000Preparing batches (batches)........... 241,150Axial milling (MHs)...................... 766,500 Total............................................... $1,147,650

D31X U75X TotalAssembling products.......... 3,500 31,500 35,000Preparing batches............... 560 1,295 1,855Axial milling...................... 1,540 1,015 2,555

Required:

a. Determine the manufacturing overhead cost per unit of each of the company's two products under the traditional costing system.

b. Determine the manufacturing overhead cost per unit of each of the company's two products under activity-based costing system.

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 8-37

Ans:

a. Traditional Manufacturing Overhead CostsPredetermined overhead rate = $1,147,650 ÷ 35,000 DLHs = $32.79 per DLH

D31X U75XDirect labor-hours...................................... 0.10 2.10Predetermined overhead rate per DLH...... $32.79 $32.79Manufacturing overhead cost per unit....... $3.28 $68.86

b. ABC Manufacturing Overhead Costs

Estimated Overhead

CostTotal Expected

Activity Activity RateAssembling products.... $140,000 35,000 DLHs $4 per DLHPreparing batches......... $241,150 1,855 batches $130 per batchAxial milling................ $766,500 2,555 MHs $300 per MH

Overhead cost for D31X

Activity Rate ActivityABC Cost

Assembling products........ $4 per DLH 3,500 DLHs $ 14,000Preparing batches.............. $130 per batch 560 batches 72,800Axial milling..................... $300 per MH 1,540 MHs 462,000 Total.................................. $548,800Annual production............ 35,000Manufacturing overhead

cost per unit................... $15.68

Overhead cost for U75X

Activity Rate ActivityABC Cost

Assembling products........ $4 per DLH 31,500 DLHs $126,000Preparing batches.............. $130 per batch 1,295 batches 168,350Axial milling..................... $300 per MH 1,015 MHs 304,500 Total.................................. $598,850Annual production............ 15,000Manufacturing overhead

cost per unit................... $39.92

AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 8B LO: 7 Level: Medium