Embed Size (px)

Citation preview

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Chapter 6

The search for evidence explained

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Learning objectives

• Explain why the audit evidence search is a central concept of auditing.

• Identify the stages of the audit process and show that evidence has to be collected in different ways at each stage.

• Explain the relationship between audit evidence and audit risk.

• Show there are different grades of audit evidence and that evidence may be upgraded or downgraded.

• Explain the relationship between audit evidence and the application of audit judgement.

• Show to what extent the evidence-gathering process might be affected by a decision by the auditor to rely on the directors and the control environment they have introduced.

• Form conclusions on the basis of evidence available in selected scenarios.

• Explain the difference between an audit, a limited assurance engagement, a compilation engagement and an engagement involving agreed upon procedures, and suggest how the evidence-gathering process may differ between them.

2

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Audit is a search for evidence to enable an opinion to be formed

• Evidence search is to enable conclusions to be formed on: – Accuracy and dependability of accounting records – Truth and fairness of financial statements – Compliance with legislation, accounting, reporting standards

• Audit evidence collected from audited entity and independent sources.

• Auditors collect audit evidence using inquiry, inspection, observation, confirmation, recalculation, re-performance, analytical procedures

3

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Audit is a search for evidence to enable an opinion to be formed

• Sufficient appropriate audit evidence – ‘Sufficient’: enough evidence is obtained to meet audit objectives.

Persuasiveness of audit evidence and quantity linked. – ‘Appropriate’ has two elements: Relevance: evidence must be pertinent to matter in hand. Reliability: many grades of reliability.

• Sufficiency and appropriateness related – the higher the quality the less may be required.

4

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

5

Audit is a search for evidence to enable an opinion to be formed

5

Figure 6.1

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

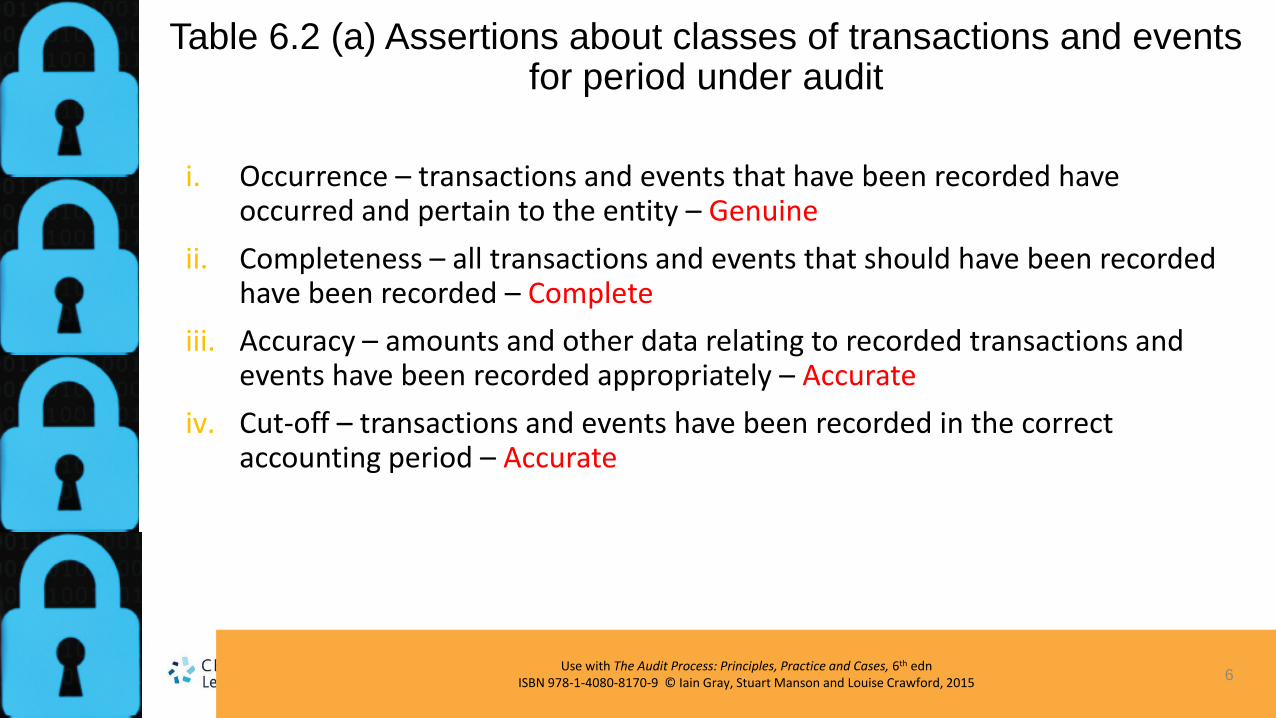

Table 6.2 (a) Assertions about classes of transactions and events for period under audit

i. Occurrence – transactions and events that have been recorded have occurred and pertain to the entity – Genuine

ii. Completeness – all transactions and events that should have been recorded have been recorded – Complete

iii. Accuracy – amounts and other data relating to recorded transactions and events have been recorded appropriately – Accurate

iv. Cut-off – transactions and events have been recorded in the correct accounting period – Accurate

6

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

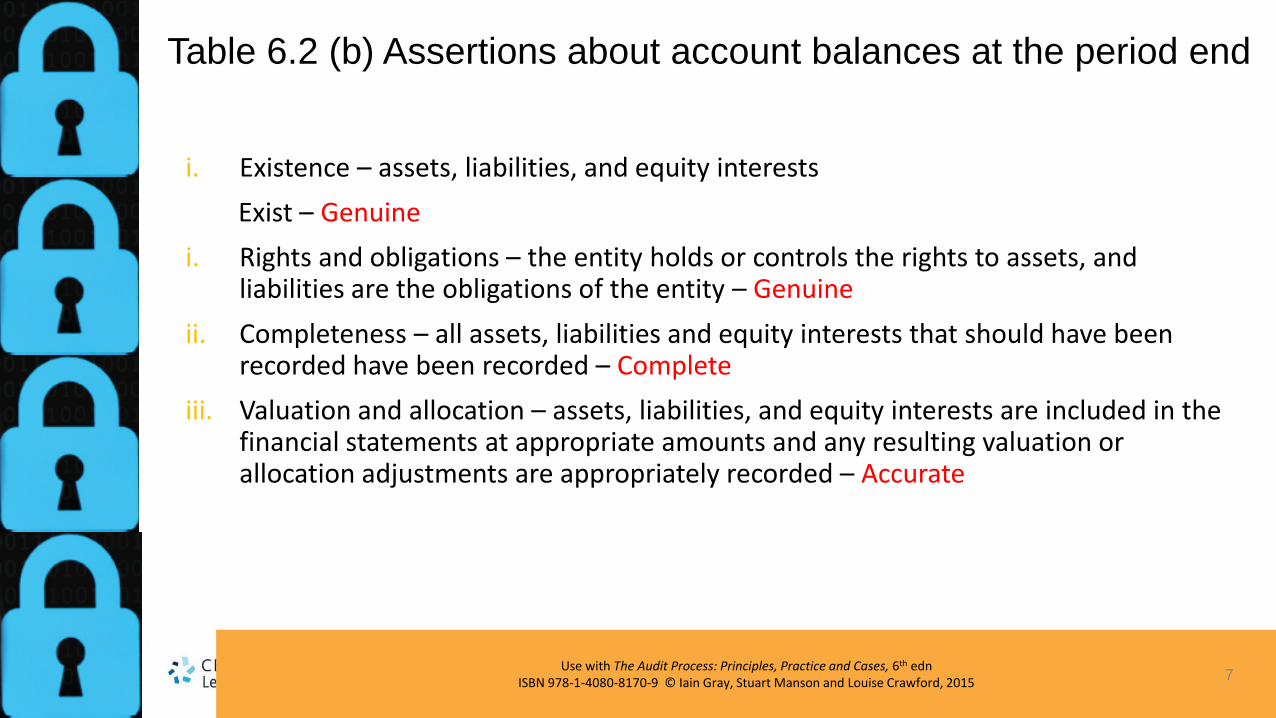

Table 6.2 (b) Assertions about account balances at the period end

i. Existence – assets, liabilities, and equity interests

Exist – Genuine

i. Rights and obligations – the entity holds or controls the rights to assets, and liabilities are the obligations of the entity – Genuine

ii. Completeness – all assets, liabilities and equity interests that should have been recorded have been recorded – Complete

iii. Valuation and allocation – assets, liabilities, and equity interests are included in the financial statements at appropriate amounts and any resulting valuation or allocation adjustments are appropriately recorded – Accurate

7

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Table 6.2 (c) Assertions about presentation and disclosure

i. Occurrence and rights and obligations – Disclosed events, transactions, and other matters have occurred and pertain to the entity – Genuine

ii. Completeness – all disclosures that should have been included in the financial statements have been included – Complete

iii. Classification and understandability – financial information is appropriately presented and described, and disclosures are clearly expressed – Accurate

iv. Accuracy and valuation – financial and other information are disclosed fairly and at appropriate amounts – Accurate

8

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Role of management assertions in the audit process

• The importance of management assertions is that (reframed) they form audit objectives

• Assertion: All trade receivables shown in the financial statements are collectable

• Audit objective: To prove within reason that all trade receivables shown in the financial statements are collectable

• Suggested audit step to prove collectability: Test amounts received from credit customers after the year-end

9

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Reliability of audit evidence (grades of audit evidence)

• Reliability of audit evidence increases when from independent sources outside the entity (particularly from professional persons).

• Reliability of audit evidence generated internally increases when related controls on preparation and maintenance are effective.

• Audit evidence obtained directly by the auditor more reliable than evidence obtained indirectly or by inference.

• Audit evidence in documentary form more reliable than oral evidence.

• Audit evidence provided by original documents is more reliable than copies, reliability of which depends on controls over preparation and maintenance.

• Evidence created in normal course of business is better than evidence specially created to satisfy the auditor.

• Best-informed source of evidence normally management of the company but lack of independence reduces its value.

• Evidence about future particularly difficult to obtain and less reliable than evidence about past events.

• Evidence may be upgraded by skilful use of corroborative evidence.

10

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Forming conclusions on the basis of evidence: the exercise of judgement

Figure 6.2

11

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The business risk approach to gathering audit evidence

• If auditors form good impression of management, evidence from them may be relied on by

auditor to greater extent.

• As auditors get to know individual members of management well, engagement partners may feel they can judge integrity.

• Close involvement of audit team with management may reveal lack of integrity – reason for withdrawing from engagement.

• Trust in integrity and competence of management could lead to reducing level of substantive tests of detail.

• A basic idea of agency theory is principals cannot trust managers to use resources properly. But, auditors cannot start with presumption that managements lack integrity.

• A major issue is that business risk approach brings auditor close to management and independence may be threatened

• Protagonists of business risk approach suggest audit failures are not because auditors fail to perform tests of detail, but because they missed clear indicators of impending catastrophe.

12

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The stages of the audit process and evidential requirements at

each stage (1) (Table 1.1)

• See Gilsland Electronics Limited – auditors’ year

13

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

14

The stages of the audit process and the evidential requirements at

each stage (2)

14

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The stages of the audit process and the evidential requirements at each stage (3)

15

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The stages of the audit process and the evidential requirements at each stage (4)

16

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The stages of the audit process and the evidential requirements at each stage (5)

17

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The stages of the audit process and the evidential requirements at each stage (6)

18

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The stages of the audit process and the evidential requirements at each stage (7)

19

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The stages of the audit process and the evidential requirements at each stage (8)

Figure 6.3 below shows the audit process, its audit stages, and evidence-gathering process in more detail.

20

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

21

The stages of the audit process and evidential requirements at each stage (9) Figure 6.3

21

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

22

The stages of the audit process and evidential requirements at each stage (10) (Figure 6.3 continued)

22

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

23

The stages of the audit process and evidential requirements at each stage (11) (Figure 6.3 continued)

23

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

24

The stages of the audit process and evidential requirements at each stage (12) (Figure 6.3 continued)

24

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Compilation engagements

• Professional accountants prepare financial statements on basis of data and information provided by management – not an audit. Normally carry out following procedures: – Find out what accounting principles and practices are common in entity’s industry. – Get general understanding of business, the risks facing it, nature of the

transactions, accounting principles used, and the presentation and content of the financial statements.

– Generally review the financial statements using limited analytical procedures and discuss critically with management.

– Obtain letter from management saying they have been given all the books and records and other information pertinent to the preparation of the financial statements.

25

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Limited assurance engagement

• Not full audit; accountant aims to obtain limited assurance financial statements

comply with legislation and accounting standards. Evidence-gathering procedures include: – Determine accounting principles and practices in industry. – Get good understanding of business, how organized, operating characteristics, risks facing it

and related controls, nature of transactions, assets and liabilities – goes further than compilation engagement work but very few detailed tests.

– Analytical procedures to identify relationships between figures appearing unusual and discuss with management. May advise management on appropriate adjustments to financial statements.

– Letter of representation from management confirming significant oral representations by management during review.

– At completion of review read financial statements to ascertain appear to conform to requirements of Companies Act and accounting standards.

26

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Agreed upon procedures engagement

• Similar to limited assurance engagement except certain detailed procedures would be performed – as agreed with management.

• Report would indicate detailed procedures carried out but would disclaim a full audit opinion.

• Agreed procedures would require the accountant to seek evidence the items subject to the agreed procedures have been stated appropriately.

27

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Figure 6.1 Audit evidence supporting reasonable

conclusions

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Figure 6.2 Evidence corroboration and upgrading in a sales system

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Figure 6.3 The audit process: audit stages, evidence-gathering

process and main audit objectives

![[PPT]Six Types of Audit Evidence - Jacksonville State · Web viewChapter 7 Audit Planning and Analytical Procedures Presentation Outline Defining Audit Evidence Types of Audit Evidence](https://img.dokumen.tips/doc/110x75/5ab7b3757f8b9ad13d8ba778/pptsix-types-of-audit-evidence-jacksonville-state-viewchapter-7-audit-planning.jpg)