Embed Size (px)

Citation preview

Chapter 6

Merchandising Activities• A merchandising company is an enterprise that buys

and sells goods to earn a profit.1. Wholesalers sell to retailers.2. Retailers sell to consumers.

• A merchandiser’s primary source of revenue is sales, whereas a service company’s primary source of revenue is service revenue.

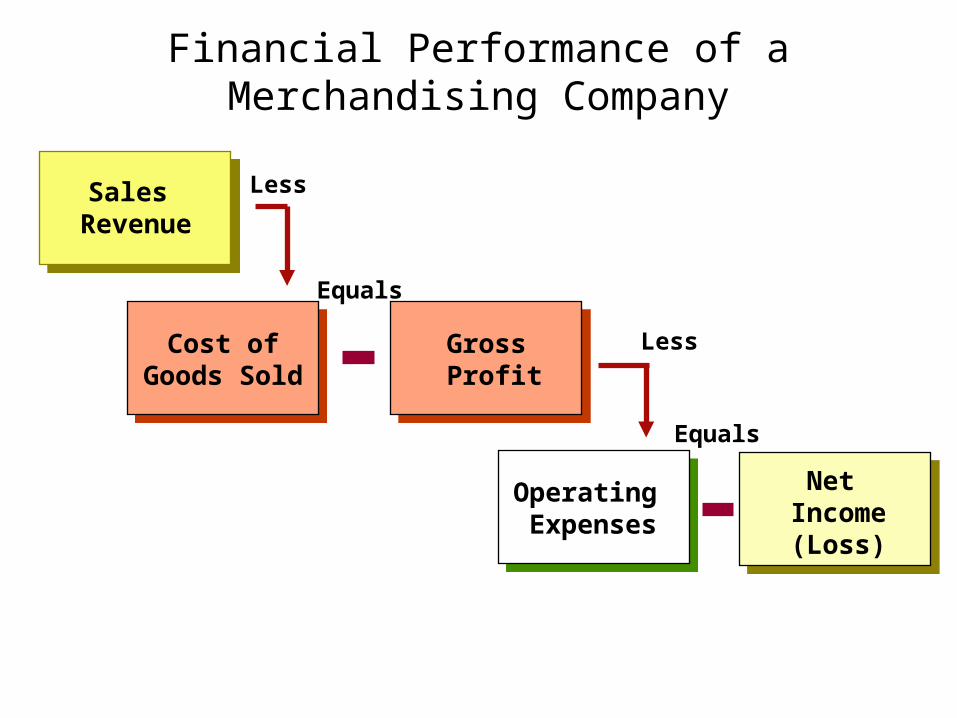

Financial Performance of a Merchandising Company

Sales Revenue

Cost ofGoods Sold

Cost ofGoods Sold

Less

Gross Profit

Gross Profit

Equals

Operating Expenses

Less

Net Income(Loss)

Equals

Merchandising Cash Flow

Beginning Inventory

Goods Purchased

during period

Cost of Goods Available for Sale

Ending Inventory

(Balance Sheet)

Cost of Goods Sold (Income

Statement)

Not Sold

Sold

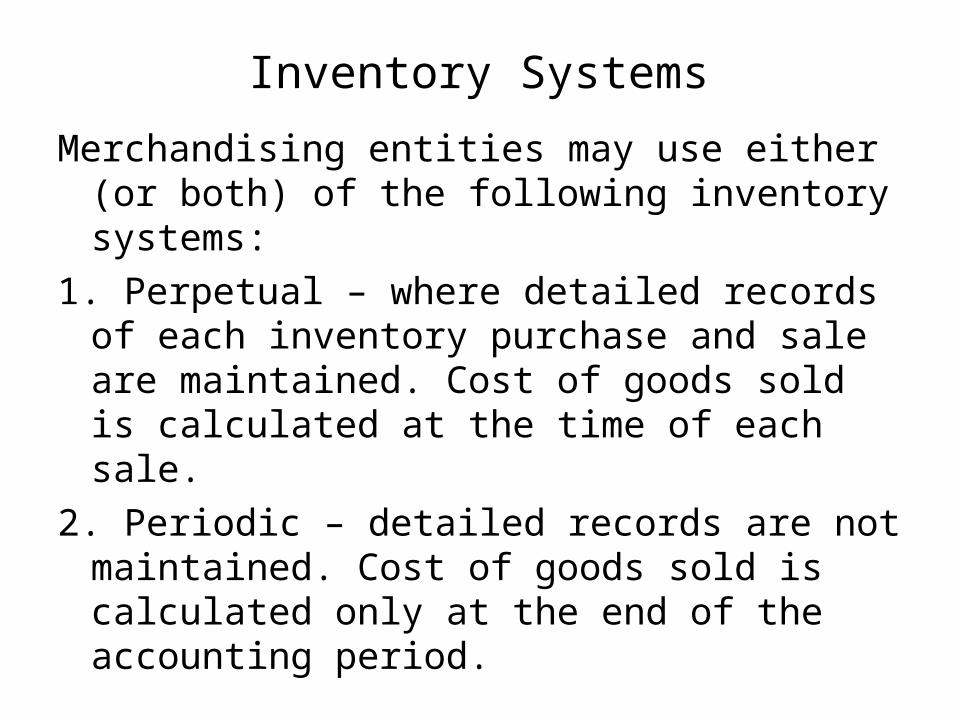

Inventory Systems

Merchandising entities may use either (or both) of the following inventory systems:

1. Perpetual – where detailed records of each inventory purchase and sale are maintained. Cost of goods sold is calculated at the time of each sale.

2. Periodic – detailed records are not maintained. Cost of goods sold is calculated only at the end of the accounting period.

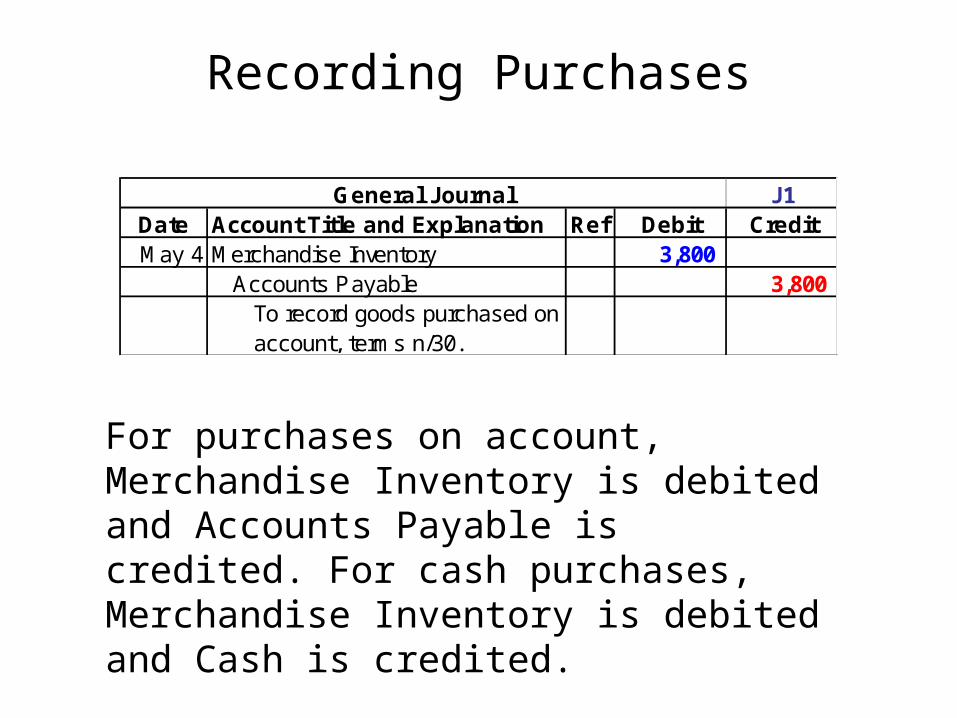

Recording Purchases

J1Date Account Title and Explanation Ref Debit CreditMay 4 Merchandise Inventory 3,800

Accounts Payable 3,800 To record goods purchased on account, terms n/30.

General Journal

For purchases on account, Merchandise Inventory is debited and Accounts Payable is credited. For cash purchases, Merchandise Inventory is debited and Cash is credited.

Accounting for Merchandise Purchases• To determine the inventory value, we must adjust

the invoice cost for:– Discounts given to a purchaser by a supplier.– Any returns and allowances for unsatisfactory items

received from a supplier.– Any required freight costs paid by a purchaser.

Trade Discounts vs. Purchase/Sales Discounts• Trade Discounts: Used by manufacturers and

wholesalers to change selling prices without republishing their catalogues. – Already deducted from the purchase price before the

transaction is recorded• Sales and Purchase Discounts: A deduction from

the invoice price granted to induce early payment of the amount due. Example – 2/10, n30 – Deducted after the initial journal entry that recorded the

purchase

Purchase Discounts

2/10,n/302/10,n/30Number of

Days Discount is Available

Number of Days

Discount is Available

Otherwise, Net (or All)

is Due

Otherwise, Net (or All)

is Due

Within CreditPeriod

Within CreditPeriod

Discount Percent

Discount Percent

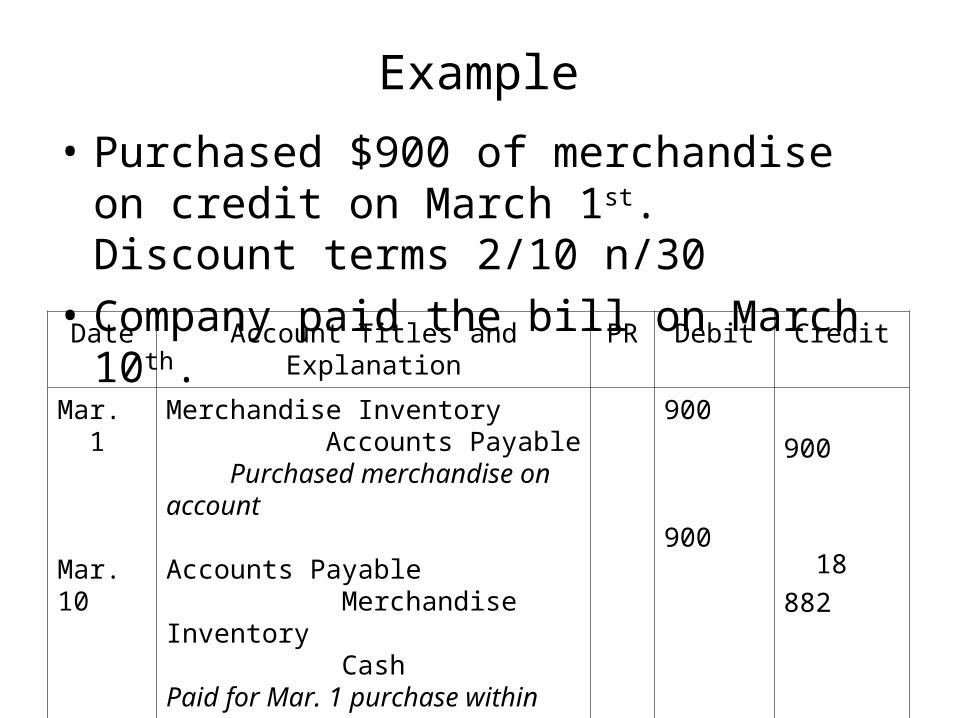

Example• Purchased $900 of merchandise on credit on March

1st. Discount terms 2/10 n/30• Company paid the bill on March 10th.

Date Account Titles and Explanation PR Debit Credit

Mar. 1

Mar. 10

Merchandise Inventory Accounts Payable Purchased merchandise on account

Accounts Payable Merchandise Inventory CashPaid for Mar. 1 purchase within the discount period

900

900

900

18882

Purchase Returns and Allowances• Purchase returns are merchandise received by a purchaser

but returned to the supplier.• A purchase allowance is a reduction in the cost of defective

merchandise received by a purchaser from a supplier.• A debit memorandum is a form issued by the purchaser to

inform the supplier of a debit made to the supplier's account, including the reason for a return or allowance. Memorandum gets its name from the issuer.

• Entry (On the books of the purchaser) Debit Accounts Payable or Cash (if refund given) and Credit Inventory

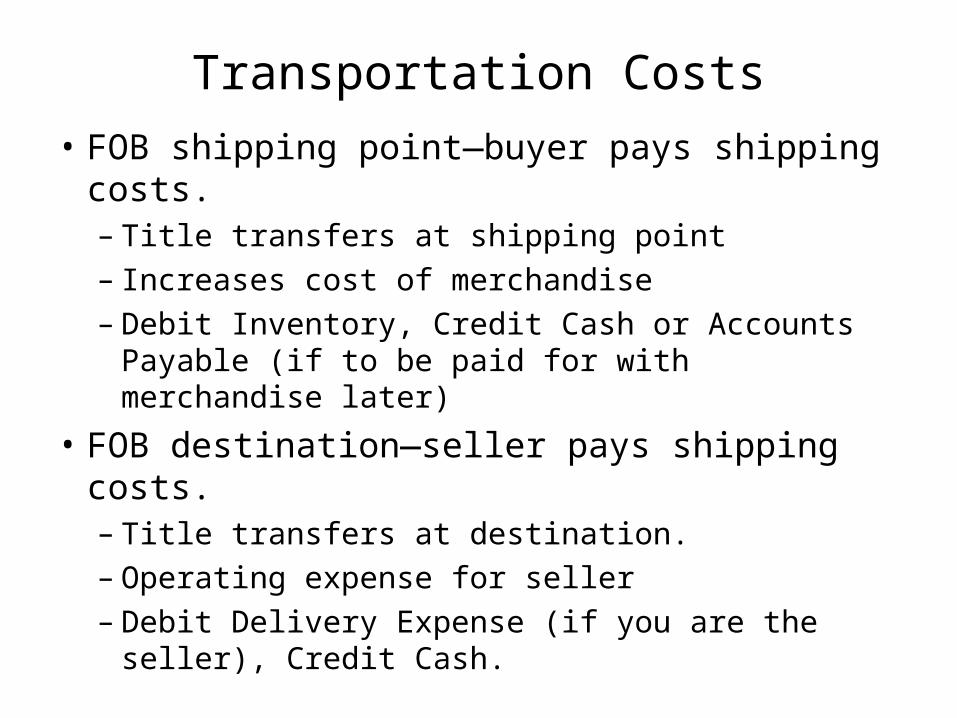

Transportation Costs• FOB shipping point—buyer pays shipping costs.

– Title transfers at shipping point – Increases cost of merchandise– Debit Inventory, Credit Cash or Accounts Payable (if to

be paid for with merchandise later)• FOB destination—seller pays shipping costs.

– Title transfers at destination. – Operating expense for seller– Debit Delivery Expense (if you are the seller), Credit

Cash.

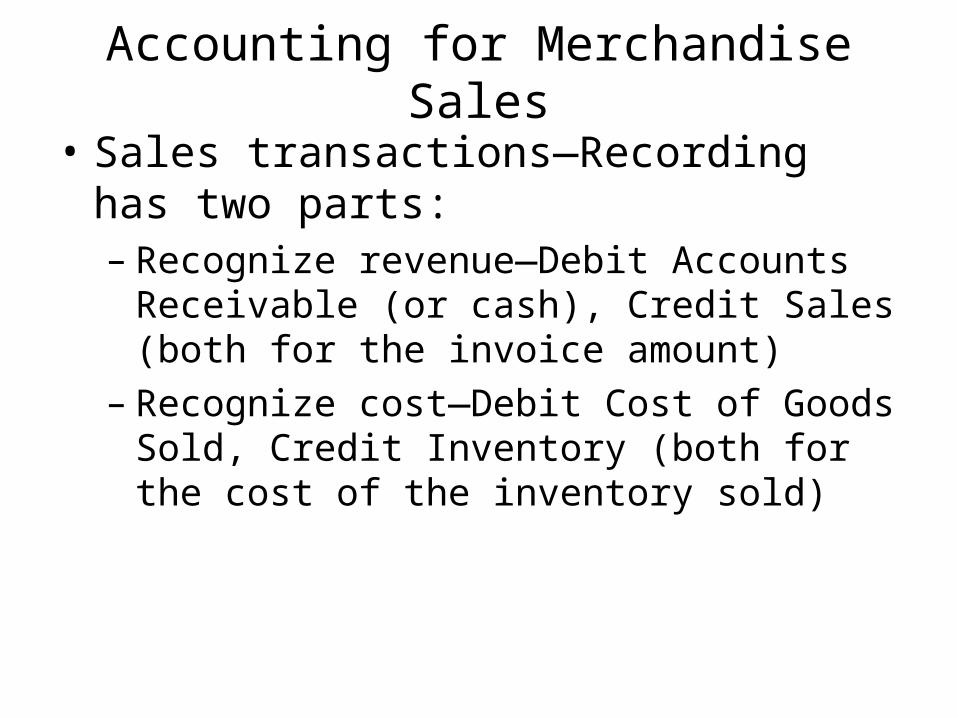

Accounting for Merchandise Sales• Sales transactions—Recording has two parts:

– Recognize revenue—Debit Accounts Receivable (or cash), Credit Sales (both for the invoice amount)

– Recognize cost—Debit Cost of Goods Sold, Credit Inventory (both for the cost of the inventory sold)

Example• A company sold $500 worth of merchandise for $800 on

credit on March 1st. Credit terms 3/10 n/EOM.

Date Account Titles and Explanation PR Debit Credit

Mar. 1 Accounts Receivable Revenue Sold merchandise on account

Cost of Goods Sold Merchandise Inventory To record the cost of merchandise

800

500

800

500

Sales Discounts• Discounts awarded to customers for payment within the

discount period. Recorded upon collection for sale. • Sales Discount is a contra-revenue account—subtraction

from Sales. • Collection after discount period—Debit Cash, Credit

Accounts Receivable (full invoice amount).• Collection within discount period—Debit Cash (invoice

amount less discount), Debit Sales Discount (discount amount), Credit Accounts Receivable (invoice amount).

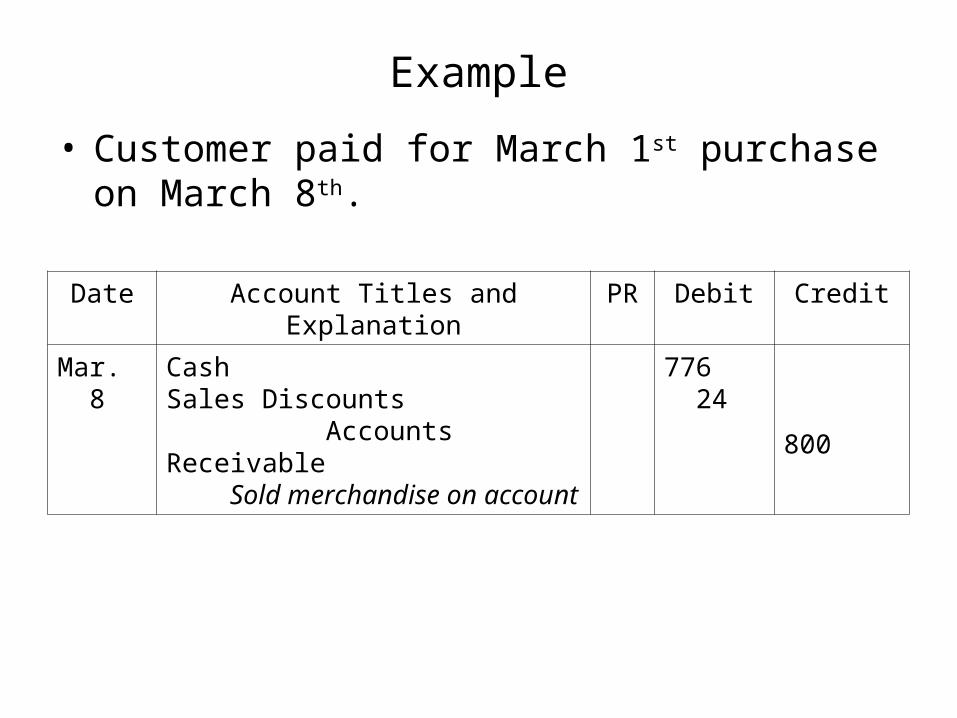

Example

• Customer paid for March 1st purchase on March 8th.

Date Account Titles and Explanation PR Debit Credit

Mar. 8 CashSales Discounts Accounts Receivable Sold merchandise on account

776 24

800

Sales Returns and Allowances• Sales returns—merchandise customers return to

the seller after a sale. • Sales allowances—reductions in the selling price of

merchandise sold to customers (usually for damaged merchandise that a customer is willing to keep at a reduced price).

• Sales Returns and Allowances is a contra-revenue account—subtraction from Sales

Sales Returns and Allowances• Entry: Debit Sales Returns and Allowances and a

Credit Accounts Receivable.Additional entry if returned merchandise is saleable:Debit Inventory, Credit Cost of Goods Sold

• Sales Returns and Allowances is a contra-revenue account—subtraction from Sales.

Example• March 15: Customer purchased 100 items for $12

per item. Each item has a cost of $5.• March 18: Customer returned 5 items that were

damaged. Items were destroyed.• March 20: Customer returned 3 items that were the

wrong colour. Items were returned to inventory.

Example ContinuedDate Account Titles and Explanation PR Debit Credit

Mar. 15

Mar. 18

Mar. 20

Accounts Receivable Revenue

Cost of Goods Sold Merchandise Inventory

Sales Returns and Allowances Accounts Receivable

Sales Returns and Allowances Accounts Receivable

Merchandise Inventory Cost of Goods Sold

1200

500

60

36

15

1200

500

60

36

15

Shrinkage• An adjusting entry is required to account for any

inventory loss.• Shrinkage is determined by comparing a physical

count of the inventory with recorded quantities.• Entry: Debit Cost of Goods Sold, Credit Inventory

Gross Margin Ratio• Shows the relation between sales and cost of goods sold by showing the percentage of net sales

available after deducting COGS.• The higher the value, the better.

Gross Margin =Gross Margin (Profit)

Net Sales