Embed Size (px)

Citation preview

13-1

Financial Statements

and Closing Procedures

Section 1: Preparing

the Financial Statements

Chapter

13

Section Objectives

1. Prepare a classified income statement

from the worksheet.

2. Prepare a statement of owner’s equity

from the worksheet.

3. Prepare a classified balance sheet from

the worksheet.

McGraw-Hill © 2009 The McGraw-Hill Companies, Inc. All rights reserved.

13-3

A classified income statement is sometimes

called a multiple-step income statement.

The Classified Income Statement

Objective 1 Prepare a classified income

statement from the worksheet

13-4

A single-step income statement is a

format in which only one computation

is needed to determine the net income.

ANSWER:

QUESTION:

What is a single-step income statement?

(Total Revenue – Total Expenses = Net Income)

13-5

Operating Revenue

Sales 561,650.00

Less Sales Returns and Allowances 12,500.00

Net Sales 549,150.00

Cost of Goods Sold

Income Statement

Year Ended December 31, 2010

Operating Revenue

Net sales for Simpson Antiques

13-6

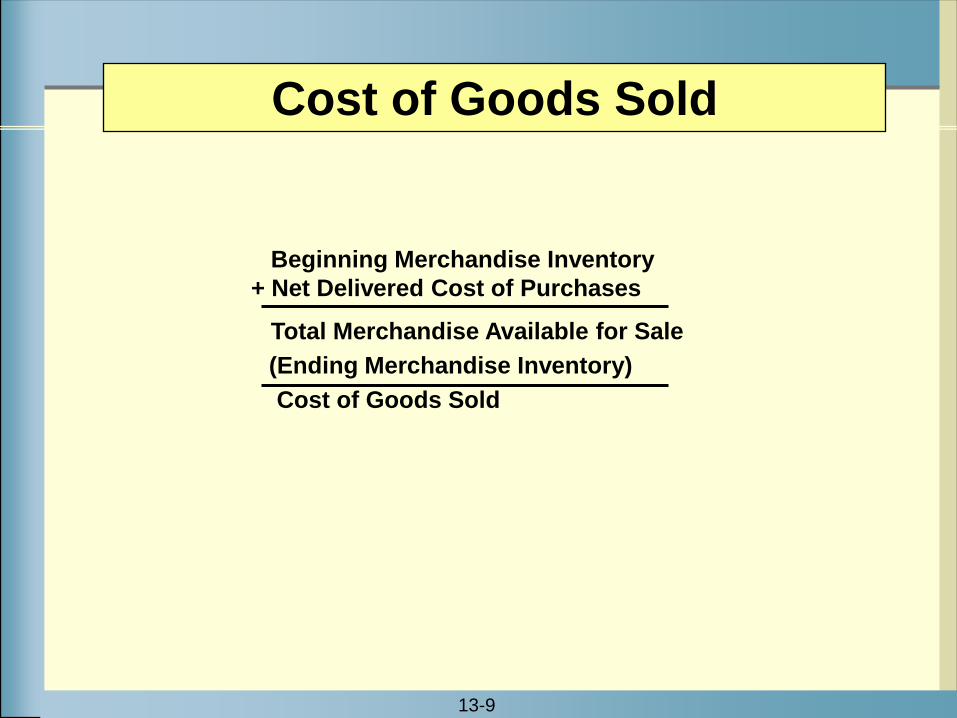

Three elements are needed to compute the cost of

goods sold:

The Cost of Goods Sold section contains information

about the cost of the merchandise that was sold during

the period.

Cost of Goods Sold

Beginning inventory

Net delivered cost of purchases

Ending inventory

13-7

Purchases

+ Freight In

(Purchases Returns and Allowances)

(Purchases Discounts)

Net Delivered Cost of Purchases

Net Delivered Cost of Purchases

13-8

Beginning Merchandise Inventory

+ Net Delivered Cost of Purchases

Total Merchandise Available for Sale

Total Merchandise Available for Sale

13-9

(Ending Merchandise Inventory)

Cost of Goods Sold

Cost of Goods Sold

Beginning Merchandise Inventory

+ Net Delivered Cost of Purchases

Total Merchandise Available for Sale

13-10

Merchandise Inventory is the one account that appears on both

the income statement and the balance sheet.

Beginning and ending merchandise inventory balances appear on

the income statement.

Ending merchandise inventory also appears on the balance sheet

in the Assets section.

13-11

Cost of Goods Sold

Merchandise Inventory, Jan. 1, 2010 52,000.00

Purchases 321,500.00

Freight In 9,800.00

Delivered Cost of Purchases 331,300.00

Less Purchases Returns and Allowances 3,050.00

Purchases Discounts 3,130.00 6,180.00

Net Delivered Cost of Purchases 325,120.00

Total Merchandise Available for Sale 377,120.00

Less Merchandise Inventory, Dec. 31, 2010 47,000.00

Cost of Goods Sold 330,120.00

Simpson Antiques

Income Statement

Year Ended December 31, 2010

Cost of Goods Sold

Merchandise available for sale

Cost of goods sold

13-12

Gross Profit on Sales

For Simpson Antiques net sales is the revenue earned from selling clothes.

Cost of goods sold is what Simpson Antiques paid for the clothes that were sold during the fiscal period.

Gross profit is what is left to cover operating expenses and provide a profit.

Gross profit is sales less the cost of goods sold.

13-13

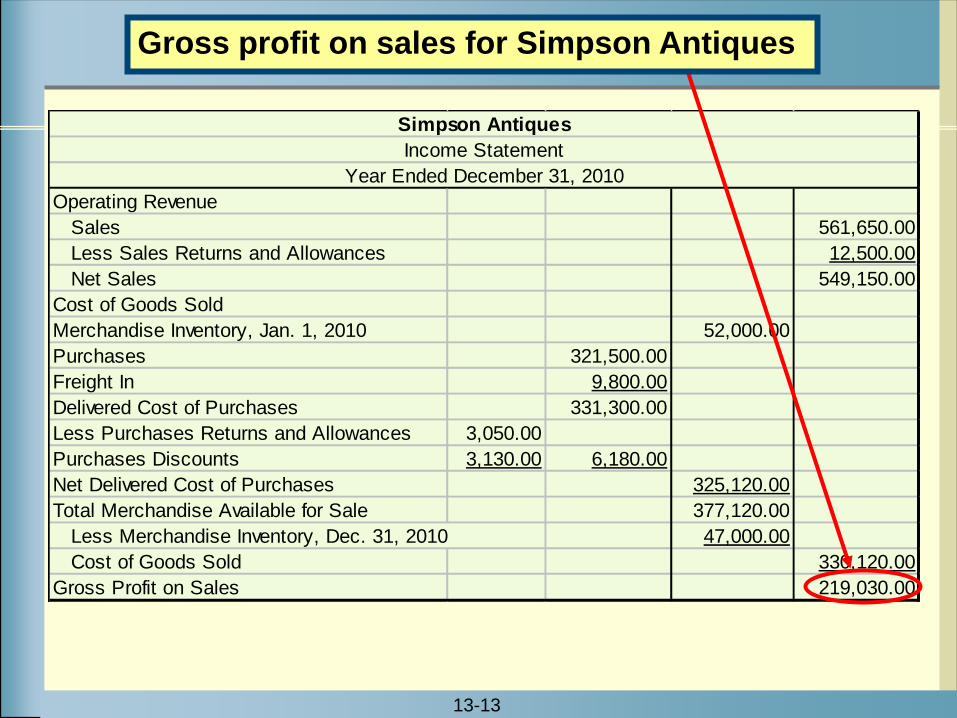

Operating Revenue

Sales 561,650.00

Less Sales Returns and Allowances 12,500.00

Net Sales 549,150.00

Cost of Goods Sold

Merchandise Inventory, Jan. 1, 2010 52,000.00

Purchases 321,500.00

Freight In 9,800.00

Delivered Cost of Purchases 331,300.00

Less Purchases Returns and Allowances 3,050.00

Purchases Discounts 3,130.00 6,180.00

Net Delivered Cost of Purchases 325,120.00

Total Merchandise Available for Sale 377,120.00

Less Merchandise Inventory, Dec. 31, 2010 47,000.00

Cost of Goods Sold 330,120.00

Gross Profit on Sales 219,030.00

Simpson Antiques

Income Statement

Year Ended December 31, 2010

Gross profit on sales for Simpson Antiques

13-14

Gross Profit on Sales 219,030.00

Operating Expenses

Selling Expenses

Salaries Expense - Sales 79,690.00

Advertising Expense 7,425.00

Cash Short or Over 125.00

Supplies Expense 4,975.00

Depreciation Expense - Store Equipment 2,400.00

Total Selling Expenses 94,615.00

General and Administrative Expenses

Rent Expense 27,600.00

Salaries Expense - Office 26,500.00

Insurance Expense 2,450.00

Payroll Taxes Expense 7,371.20

Telephone Expense 1,875.00

Uncollectible Accounts Expense 800.00

Utilities Expense 5,925.00

Depreciation Expense - Office Equipment 700.00

Total General and Administrative Expenses 73,221.20

Total Operating Expenses 167836.2

Simpson Antiques

Income Statement

Year Ended December 31, 2010

Salaries for salespersons and advertising

are examples of selling expenses.

Operating Expenses

13-15

Gross Profit on Sales 219,030.00

Operating Expenses

Selling Expenses

Salaries Expense - Sales 79,690.00

Advertising Expense 7,425.00

Cash Short or Over 125.00

Supplies Expense 4,975.00

Depreciation Expense - Store Equipment 2,400.00

Total Selling Expenses 94,615.00

General and Administrative Expenses

Rent Expense 27,600.00

Salaries Expense - Office 26,500.00

Insurance Expense 2,450.00

Payroll Taxes Expense 7,371.20

Telephone Expense 1,875.00

Uncollectible Accounts Expense 800.00

Utilities Expense 5,925.00

Depreciation Expense - Office Equipment 700.00

Total General and Administrative Expenses 73,221.20

Total Operating Expenses 167836.2

Simpson Antiques

Income Statement

Year Ended December 31, 2010

Operating Expenses

Rent, utilities, and salaries for office employees

are examples of general and administrative

expenses.

13-16

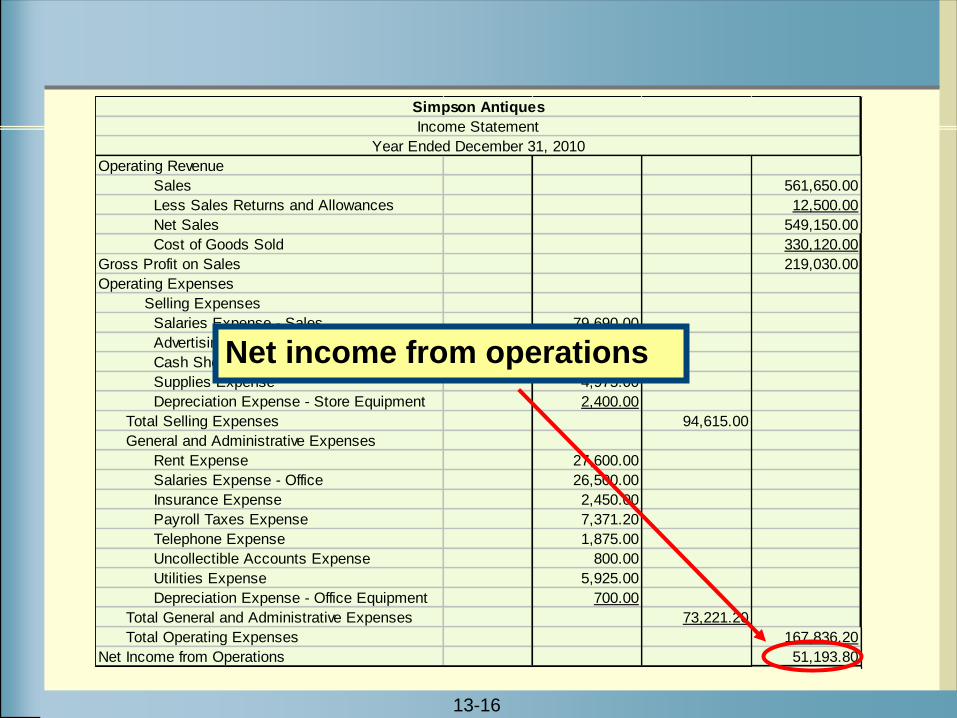

Operating Revenue

Sales 561,650.00

Less Sales Returns and Allowances 12,500.00

Net Sales 549,150.00

Cost of Goods Sold 330,120.00

Gross Profit on Sales 219,030.00

Operating Expenses

Selling Expenses

Salaries Expense - Sales 79,690.00

Advertising Expense 7,425.00

Cash Short or Over 125.00

Supplies Expense 4,975.00

Depreciation Expense - Store Equipment 2,400.00

Total Selling Expenses 94,615.00

General and Administrative Expenses

Rent Expense 27,600.00

Salaries Expense - Office 26,500.00

Insurance Expense 2,450.00

Payroll Taxes Expense 7,371.20

Telephone Expense 1,875.00

Uncollectible Accounts Expense 800.00

Utilities Expense 5,925.00

Depreciation Expense - Office Equipment 700.00

Total General and Administrative Expenses 73,221.20

Total Operating Expenses 167,836.20

Net Income from Operations 51,193.80

Simpson Antiques

Income Statement

Year Ended December 31, 2010

Net income from operations

13-17

Operating Expenses

Net Income from Operations 51,193.80

Other Income

Interest Income 166.00

Miscellaneous Income 582.00

Total Other Income 748.00

Other Expenses

Interest Expense 770.00

Net Nonoperating Expense 22.00

Simpson Antiques

Income Statement

Year Ended December 31, 2010

Other Income and Other Expenses

13-18

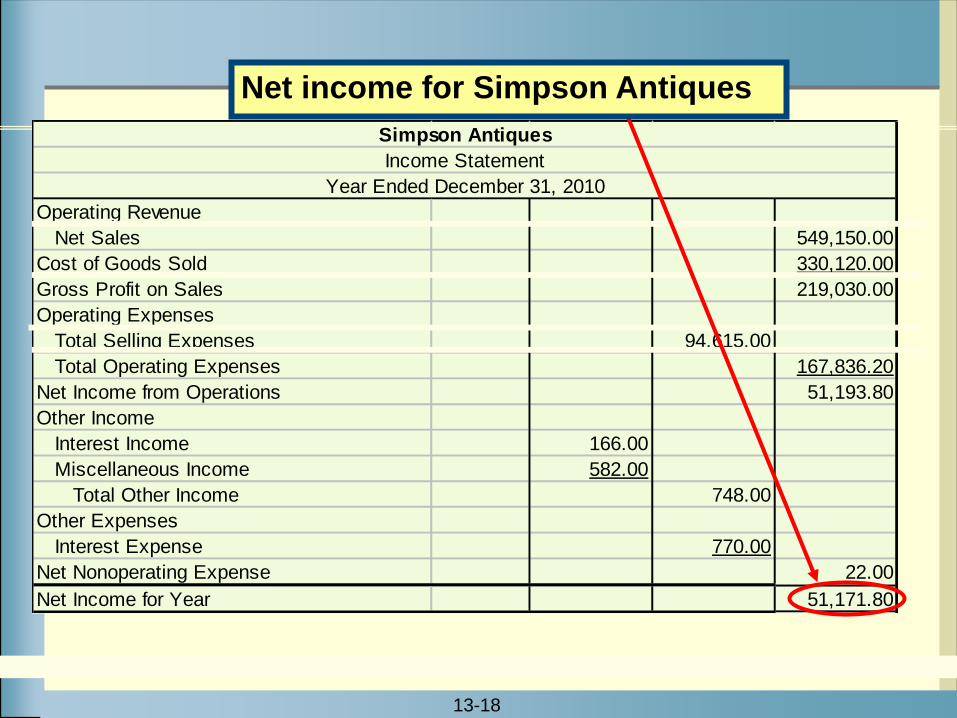

Operating Revenue

Net Sales 549,150.00

Cost of Goods Sold 330,120.00

Gross Profit on Sales 219,030.00

Operating Expenses

Total Selling Expenses 94,615.00

Total Operating Expenses 167,836.20

Net Income from Operations 51,193.80

Other Income

Interest Income 166.00

Miscellaneous Income 582.00

Total Other Income 748.00

Other Expenses

Interest Expense 770.00

Net Nonoperating Expense 22.00

Net Income for Year 51,171.80

Simpson Antiques

Income Statement

Year Ended December 31, 2010

Net income for Simpson Antiques

13-19

The statement of owner's equity reports the changes that occurred in the owner's financial interest during the period.

The ending capital balance for Patricia Simpson, $84,792.80, is used to prepare the balance sheet.

Patricia Simpson, Capital, January 1, 2010 61,221.00

Net Income for Year 51,171.80

Less Withdrawals for the Year 27,600.00

Increase in Capital 23,571.80

Patricia Simpson, Capital, December 31, 2010 84,792.80

Simpson Antiques

Statement of Owner's Equity

Year Ended December 31, 2010

Objective 2 Prepare a Statement of Owner’s

Equity from the worksheet

13-20

Current assets are assets consisting

of cash, items that normally will be

converted into cash within one year,

or items that will be used up within

one year.

ANSWER:

QUESTION:

What are current assets?

Objective 3 Prepare a classified balance

sheet from the worksheet

13-21

Current Assets

Assets

Current Assets

Cash 13,136.00

Petty Cash Fund 100.00

Notes Receivable 1,200.00

Accounts Receivable 32,000.00

Less Allow. for Doubtful Accounts 1,050.00 30,950.00

Interest Receivable 30.00

Merchandise Inventory 47,000.00

Prepaid Expenses

Supplies 1,325.00

Prepaid Insurance 4,900.00

Prepaid Interest 75.00 6,300.00

Total Current Assets 98,716.00

Simpson Antiques

Balance Sheet

Year Ended December 31, 2010

Current assets for Simpson Antiques

13-22

Plant and Equipment

Noncurrent assets are called long-term assets.

An important category of long-term assets is plant and equipment.

For many businesses plant and equipment represents a sizable

investment.

Assets

Prepaid Interest 75.00 6,300.00

Total Current Assets 98,716.00

Plant and Equipment

Store Equipment 30,000.00

Less Accumulated Depreciation 2,400.00 27,600.00

Office Equipment 5,000.00

Less Accumulated Depreciation 700.00 4,300.00

Total Plant and Equipment 31,900.00

Total Assets 130,616.00

Simpson Antiques

Balance Sheet

Year Ended December 31, 2010

13-23

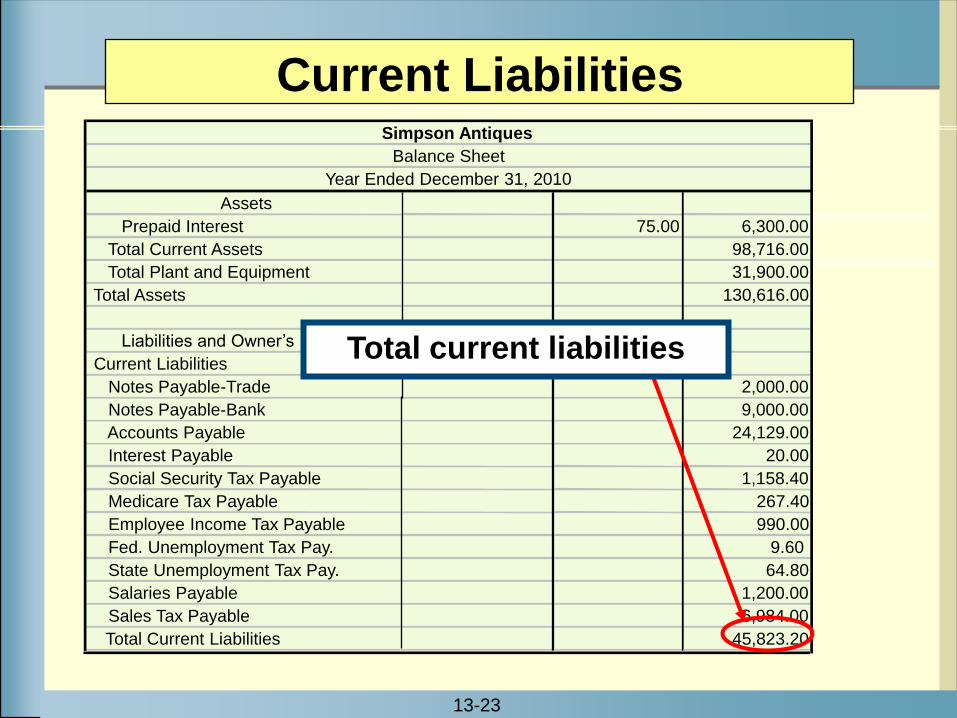

Current Liabilities

Assets

Prepaid Interest 75.00 6,300.00

Total Current Assets 98,716.00

Total Plant and Equipment 31,900.00

Total Assets 130,616.00

Liabilities and Owner’s Equity

Current Liabilities

Notes Payable-Trade 2,000.00

Notes Payable-Bank 9,000.00

Accounts Payable 24,129.00

Interest Payable 20.00

Social Security Tax Payable 1,158.40

Medicare Tax Payable 267.40

Employee Income Tax Payable 990.00

Fed. Unemployment Tax Pay. 9.60

State Unemployment Tax Pay. 64.80

Salaries Payable 1,200.00

Sales Tax Payable 6,984.00

Total Current Liabilities 45,823.20

Simpson Antiques

Balance Sheet

Year Ended December 31, 2010

Total current liabilities

13-24

Although repayment of long-term liabilities might not be due

for several years, management must make sure that periodic

interest is paid promptly.

Long-term liabilities include mortgages, notes payable, and

loans payable.

Long-Term Liabilities

13-25

Owner's Equity

The ending balance from the statement of owner’s equity is

transferred to the Owner's Equity section of the balance sheet.

61,221.00

51,171.80

27,600.00

23,571.80

84,792.80

Simpson Antiques

Statement of Owner's Equity

Year Ended December 31, 2010

Patricia Simpson, Capital, January 1, 2010

Net Income for Year

Less Withdrawals for the Year

Increase in Capital

Patricia Simpson, Capital, December 31, 2010

Assets

Owner’s Equity

Patricia Simpson, Capital 84,792.80

Total Liabilities and Owner's Equity 130,616.00

Simpson Antiques

Balance Sheet

Year Ended December 31, 2010

Financial Statements

and Closing Procedures

Section 2: Completing the

Accounting Cycle

Chapter

13

Section Objectives

4. Journalize and post the adjusting entries.

5. Journalize and post the closing entries.

6. Prepare a postclosing trial balance.

7. Journalize and post reversing entries.

McGraw-Hill © 2009 The McGraw-Hill Companies, Inc. All rights reserved.

13-27

All adjustments are shown on the worksheet.

After the financial statements have been prepared, the adjustments are made a permanent part of the accounting records.

They are recorded in the general journal as adjusting journal entries and are posted to the general ledger.

Objective 4 Journalize and post the

adjusting entries

13-28

Adjusting Entries

Type of

Adjustment

Worksheet

Reference

Purpose

Inventory (a – b) Removes beginning inventory and adds ending

inventory to the accounting records.

Expense (c – e) Matches expense to revenue for the period; the

credit is to a contra asset account.

Accrued Expense (f – i) Matches expense to revenue for the period; the

credit is to a liability account.

Prepaid Expense (j – l) Matches expense to revenue for the period; the

credit is to an asset account.

Accrued Income (m – n) Recognizes income earned in the period.

The debit is to an asset account (Interest

Receivable) or a liability account (Sales Tax

Payable).

13-29

At the end of the period, the temporary accounts are closed.

The temporary accounts are:

Revenue accounts

Cost of goods sold accounts

Expense accounts

Drawing account

Journalize and Post the

Closing EntriesObjective 5

13-30

1. Close revenue accounts and cost of goods sold accounts with credit balances to Income Summary.

2. Close expense accounts and cost of goods sold accounts with debit balances to Income Summary.

3. Close Income Summary, which now reflects the net income or loss for the period, to owner's capital.

4. Close the drawing account to owner's capital.

There are four steps in the closing process:

13-31

GENERAL JOURNAL PAGE 28

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

2010

Dec. 31

Closing Entries

Income Summary 568,578.00

Sales 561,650.00

Interest Income 166.00

Miscellaneous Income 582.00

Purchases Returns and Allowances 3,050.00

Purchases Discounts 3,130.00

Step 1: Closing the Revenue Accounts and the Cost of Goods Sold Accounts with

credit balances.

Debit each account, except Income Summary, for its balance. Credit Income Summary for the total.

13-32

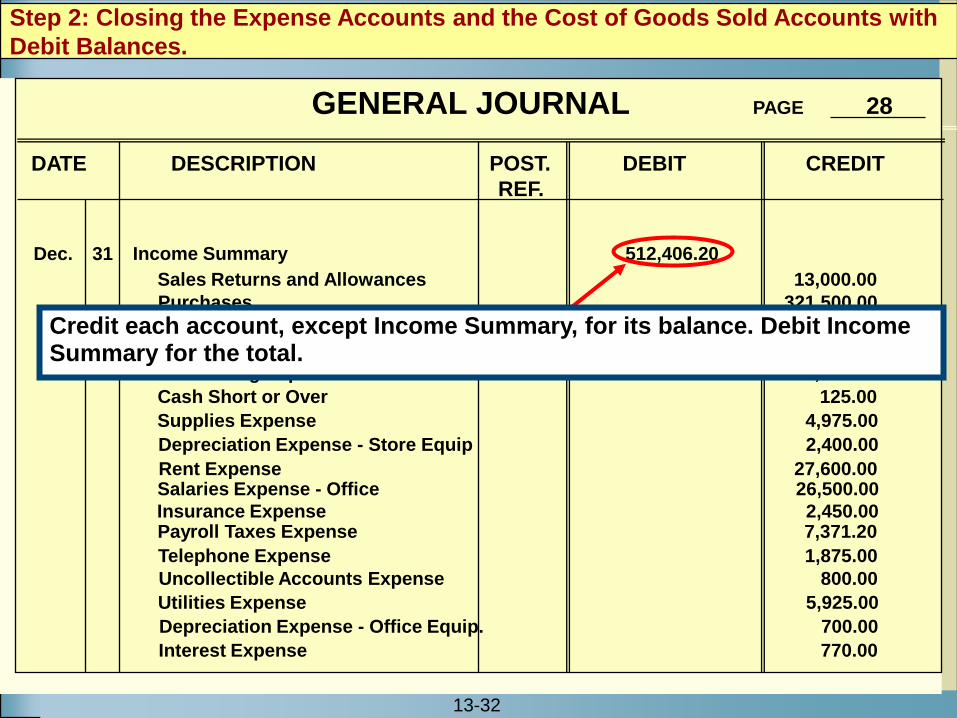

GENERAL JOURNAL PAGE 28

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31

Sales Returns and Allowances 13,000.00

Income Summary 512,406.20

Purchases 321,500.00

Salaries Expense – Sales 79,990.00

Advertising Expense 7,425.00

Cash Short or Over 125.00

Supplies Expense 4,975.00

Depreciation Expense - Store Equip 2,400.00

Rent Expense 27,600.00

Freight In 9,800.00

Salaries Expense - Office 26,500.00

Telephone Expense 1,875.00

Uncollectible Accounts Expense 800.00

Utilities Expense 5,925.00

Depreciation Expense - Office Equip. 700.00

Interest Expense 770.00

Payroll Taxes Expense 7,371.20Insurance Expense 2,450.00

Step 2: Closing the Expense Accounts and the Cost of Goods Sold Accounts with

Debit Balances.

Credit each account, except Income Summary, for its balance. Debit Income Summary for the total.

13-33

Income Summary

12/31 47,000.00

12/31 568,578.00

615,578.00

Bal. 51,171.80

Adjusting Entries (a-b) 12/31 52,000.00

Closing Entries 12/31 512,406.20564,406.20

GENERAL JOURNAL PAGE 28

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31 Income Summary 51,171.80

Patricia Simpson, Capital 51,171.80

The third closing entry transfers the Income Summary balance to the owner's capital account.

This closes the Income Summary account, which remains closed until it is used in the end-of-period process for the next year.

For Simpson Antiques, the third closing entry is as follows:

Step 3: Closing the Income Summary Account.

13-34

GENERAL JOURNAL PAGE 28

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31 Patricia Simpson, Capital 27,600.00

Patricia Simpson, Drawing 27,600.00

Step 4: Closing the Drawing account.

This entry closes the drawing account and updates the capital account.

13-35

Posting the Closing Entries

The closing entries are posted from the general journal to the general ledger.

This process brings the temporary account balances to zero.

The word Closing is entered in the Description column.

13-36

Preparing a Postclosing Trial

Balance

Prepare a postclosing trial balance to confirm that the general ledger is in balance.

Only the accounts that have balances – the asset, liability and owner's capital accounts – appear on the postclosing trial balance.

The postclosing trial balance matches the amounts reported on the balance sheet.

To verify this, compare the postclosing trial balance with the balance sheet.

Objective 6

13-37

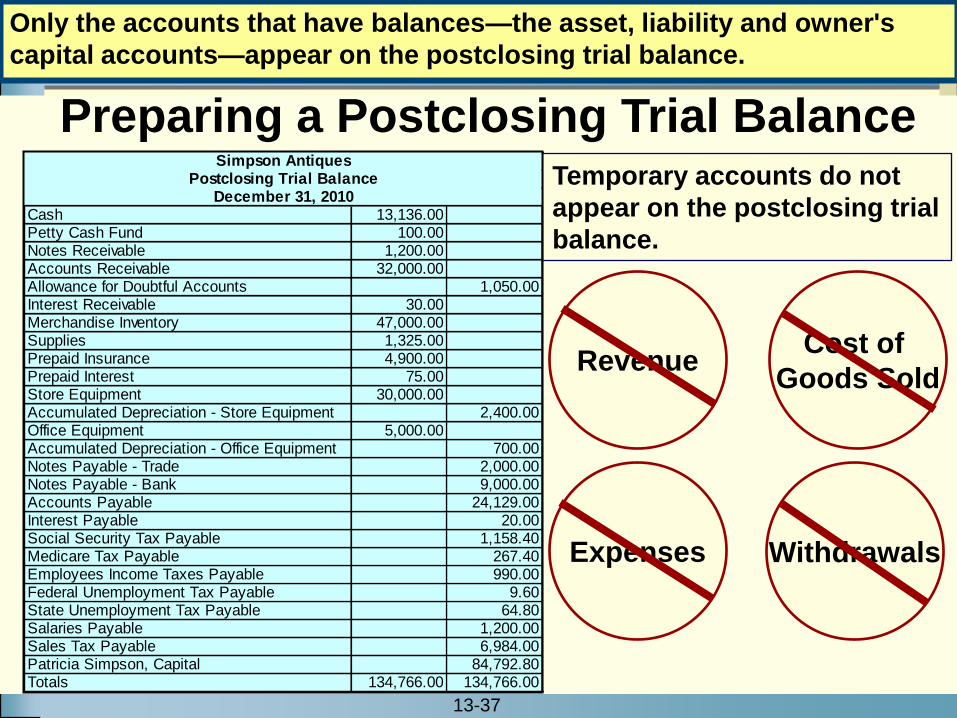

Revenue

Preparing a Postclosing Trial Balance

Cost of

Goods Sold

Expenses Withdrawals

Temporary accounts do not

appear on the postclosing trial

balance.Cash 13,136.00Petty Cash Fund 100.00Notes Receivable 1,200.00Accounts Receivable 32,000.00Allowance for Doubtful Accounts 1,050.00Interest Receivable 30.00Merchandise Inventory 47,000.00Supplies 1,325.00Prepaid Insurance 4,900.00Prepaid Interest 75.00Store Equipment 30,000.00Accumulated Depreciation - Store Equipment 2,400.00Office Equipment 5,000.00Accumulated Depreciation - Office Equipment 700.00Notes Payable - Trade 2,000.00Notes Payable - Bank 9,000.00Accounts Payable 24,129.00Interest Payable 20.00Social Security Tax Payable 1,158.40Medicare Tax Payable 267.40Employees Income Taxes Payable 990.00Federal Unemployment Tax Payable 9.60State Unemployment Tax Payable 64.80Salaries Payable 1,200.00Sales Tax Payable 6,984.00Patricia Simpson, Capital 84,792.80Totals 134,766.00 134,766.00

Simpson AntiquesPostclosing Trial Balance

December 31, 2010

Only the accounts that have balances—the asset, liability and owner's

capital accounts—appear on the postclosing trial balance.

13-38

Reversing entries are journal entries

made to reverse the effect of certain

adjusting entries involving accrued

income or accrued expenses.

ANSWER:

QUESTION:

What are reversing entries?

Objective 7 Journalize and post reversing entries

13-39

The Accounting Cycle

Step 1

Analyze

transactions

Step 2

Journalize the

data about

transactions

Step 3

Post the

data about

transactions

Step 4

Prepare

a

worksheet

Step 5

Prepare

financial

statements

Step 6

Journalize and

post adjusting

entriesStep 7

Journalize and

post closing

entries

Step 8

Prepare a

postclosing

trial balance

Step 9

Interpret

the financial

information

Step 9

Interpret

the financial

information Step 8

Prepare a

postclosing

trial balance

Step 5

Prepare

financial

statements

Step 4

Prepare

a

worksheet

Step 3

Post the

data about

transactions

Step 2

Journalize the

data about

transactionsStep 1

Analyze

transactions

Step 6

Journalize and

post adjusting

entriesStep 7

Journalize and

post closing

entries

13-40

Thank Youfor using

College Accounting, 12th Edition

Price • Haddock • Farina