Embed Size (px)

Citation preview

77

CHAPTER-4

MANAGEMENT ACCOUNTING INFORMATION SYSTEM IN

ORGANIZATIONS

4.1 Management Accounting Information System (MAIS)

4.1.1 What is management accounting information system?

4.1.2 Operational model and characteristics of MAIS

4.1.3 Factors influence data quality in MAIS

4.1.4 Traditional versus sophisticated MAIS

4.1.5 Usefulness of MAIS

4.2 Previous Studies

4.2.1 Studies related to cost accounting system and pricing

policy

4.2.2 Studies related to usage of management accounting

techniques

4.2.3 Studies related to information characteristics of MAIS

4.2.4 Studies related to the use of MAIS

4.3 Chapter Summary

78

The previous chapter has provided detailed discussion on management accounting and

decision making to support the role of MAIS on managerial decision making in

Ethiopian medium and large scale printing companies. Although it is a research area

in which not much research has been conducted and calls for further research as only

exists. It is the purpose of this chapter to review this literature.

This chapter reviews the literature on various issues related to management

accounting information system (MAIS) in organizations. The chapter begins by

reviewing the theoretical concept of MAIS. It includes the concept of MAIS,

operational model and characteristics of MAIS, factors influencing data quality in

MAIS, traditional versus sophisticated MAIS, and usefulness of MAIS. Then reviews

of various related studies conducted in this important field of research are presented.

It provides the researcher proper direction to carry out their research work and enables

them to arrive at meaningful conclusions. Therefore, the past studies were reviewed

and presented in this chapter.

Very few research studies have been carried out in the field of MAIS in general. The

available literature relevant to the objectives of the present study was reviewed and

presented under the following headings: cost accounting system and pricing policy,

usage of management accounting techniques, information characteristics of MAIS,

and the use of MAIS. Finally, the chapter ends with a summary.

4.1 Management Accounting Information System

4.1.1 What is management accounting information system?

Chenhall (2003) defined Management accounting information systems (MAIS) as a

formal system designed for providing information to facilitate decision making and

evaluation of managerial activity. Atkinson et al. (2001), defined as “information

79

system which is collecting operational data and financial, processing, keeping, and

reporting to user”. A definition by Bruggeman and Slagmulder (1995) describes

MAIS as: MAIS collect, classify, summarize, and report information to managers to

assist them in their control of production activities. It is an integral part of an

organization which is related to the structure and organization process, for products

control of organization including manager control.

The definitions supplied by all sources seem to be very much in synch. MAIS in this

thesis is defined as accounting system that records, processes and reports financial

information for internal use in accordance with the preferences of management. The

scope of this system is usually broader than that required by GAAP or IFRS.

4.1.2 Operational model and characteristics of MAIS

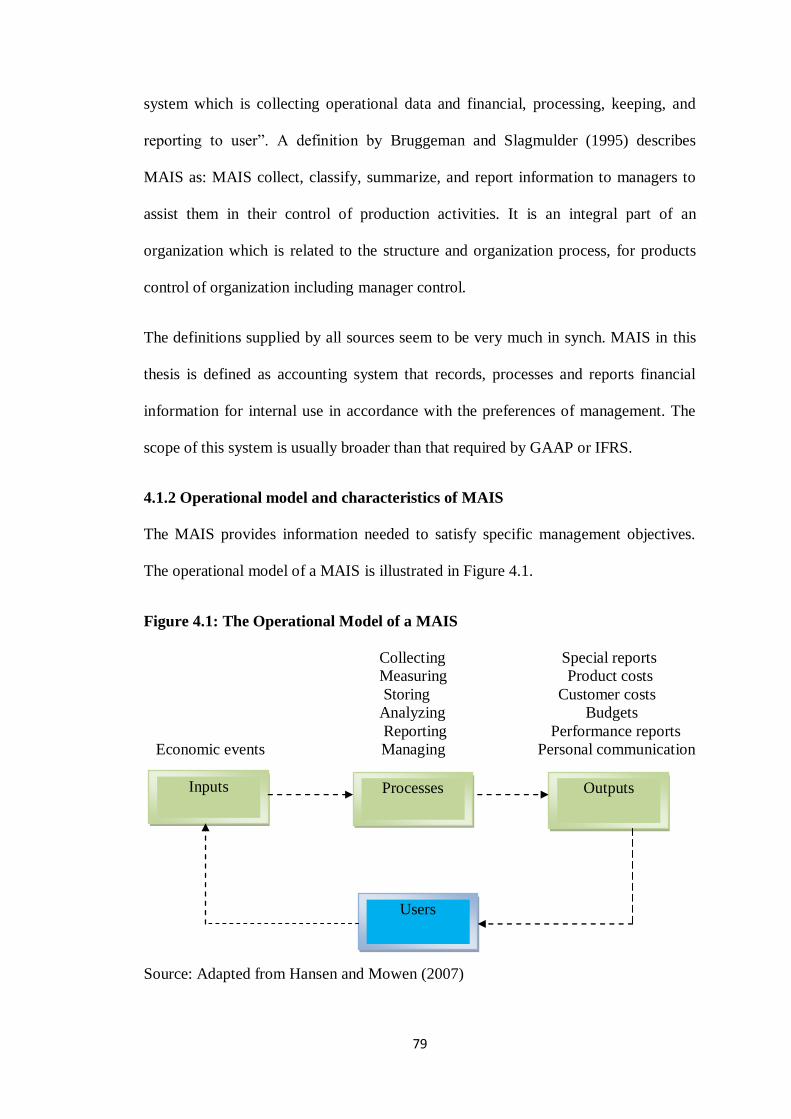

The MAIS provides information needed to satisfy specific management objectives.

The operational model of a MAIS is illustrated in Figure 4.1.

Figure 4.1: The Operational Model of a MAIS

Collecting Special reports

Measuring Product costs

Storing Customer costs

Analyzing Budgets

Reporting Performance reports

Economic events Managing Personal communication

Source: Adapted from Hansen and Mowen (2007)

Outputs Processes Inputs

Users

80

At the heart of a MAIS are processes; which transform the inputs into outputs and are

such things as collecting, measuring, storing, analyzing, reporting, and managing

information. Information on economic events is processed into outputs that satisfy the

system’s objectives. Out-puts include special reports, product costs, customer costs,

budgets, performance reports, and even personal communication (Hansen and

Mowen, 2007).

The MAIS is not bound by any formal criteria that define the nature of the processes,

inputs, or outputs. The criteria are flexible and based on management objectives.

Hansen and Mowen (2007) have identified three main objectives of a MAIS, these

are:

1. To provide information for costing out services, products, and other objectives

of interest to management.

2. To provide information for planning, controlling, evaluation, and continuous

improvement.

3. To provide information for decision making

These three objectives show that managers and other users need access to

management accounting information and need to know how to use it. Thus

management accounting information is needed and used in all phases of management,

including planning, controlling, and decision making. Management accounting

information has been characterized by breadth of scope, timeliness, levels of

aggregation and integrative nature (Chenhall and Morris, 1986). Table 4.1 gives an

overview of the information characteristics of MAIS considered important by these

managers nowadays.

81

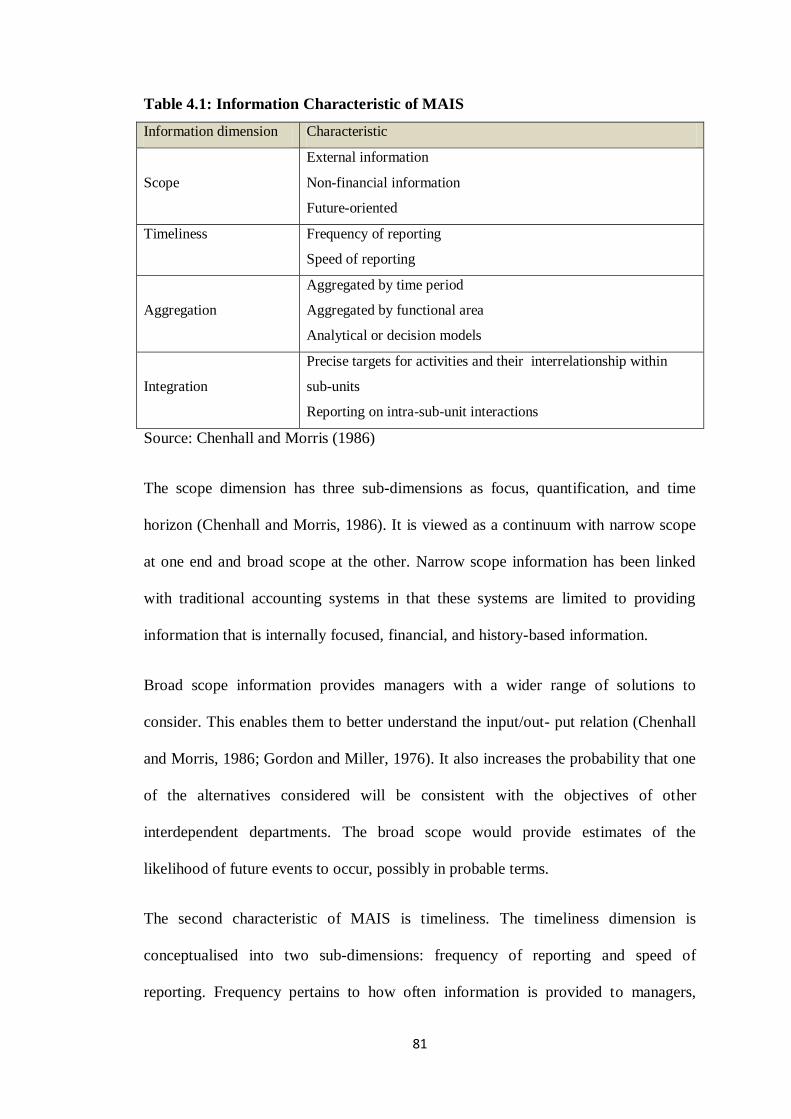

Table 4.1: Information Characteristic of MAIS

Information dimension Characteristic

Scope

External information

Non-financial information

Future-oriented

Timeliness Frequency of reporting

Speed of reporting

Aggregation

Aggregated by time period

Aggregated by functional area

Analytical or decision models

Integration

Precise targets for activities and their interrelationship within

sub-units

Reporting on intra-sub-unit interactions

Source: Chenhall and Morris (1986)

The scope dimension has three sub-dimensions as focus, quantification, and time

horizon (Chenhall and Morris, 1986). It is viewed as a continuum with narrow scope

at one end and broad scope at the other. Narrow scope information has been linked

with traditional accounting systems in that these systems are limited to providing

information that is internally focused, financial, and history-based information.

Broad scope information provides managers with a wider range of solutions to

consider. This enables them to better understand the input/out- put relation (Chenhall

and Morris, 1986; Gordon and Miller, 1976). It also increases the probability that one

of the alternatives considered will be consistent with the objectives of other

interdependent departments. The broad scope would provide estimates of the

likelihood of future events to occur, possibly in probable terms.

The second characteristic of MAIS is timeliness. The timeliness dimension is

conceptualised into two sub-dimensions: frequency of reporting and speed of

reporting. Frequency pertains to how often information is provided to managers,

82

while speed refers to the time lag between when a manager requests for information

and when the required information is provided to the manager (Bouwens and

Abernethy, 2000). Chenhall and Morris (1986) defined timeliness as a manager’s

ability to respond quickly to events regarding to provision of information on request

and the frequency of reporting systematically collected information. Timely

information also has the potential to reduce uncertainty. It enables managers to

continually adjust their activities in response to the changes demanded by

customization as well as the changes occurring in other interdependent departments.

Timely information enhances the facility of MAIS to report upon the most recent

events and to provide rapid feedback on management decisions (Chenhall and Morris,

1986). Furthermore, according to him a manager's ability to respond quickly to events

is likely to be influenced by the timeliness of the MAIS.

The third characteristic of MAIS is aggregation. The aggregation dimension provides

information in various forms of aggregation ranging from provision of basic raw,

unprocessed data to a variety of aggregations by functional area (i.e. summary reports

on activities of other business units, or other functions of the organization), by time

period (e.g. month, year) or through decision models, for example supporting

marginal analysis, inventory models, discounted cash flow analysis, what-if-analysis,

cost-volume-profit analysis (Chenhall and Morris, 1986).

Aggregated information enables managers to process larger quantities of information.

It condenses information into a format that can be processed quickly and, thus,

increases the overall amount of information that can be processed within a given time.

The potential for sub-optimal decision making owing to information overload is

thereby reduced. Aggregation of information enables managers to consider more

alternatives and develop a better understanding of input/output relations both at the

83

department and within departments. This increases the probability that solutions will

be found that are optimal for the overall firm.

Finally, Integration of information refers to how well the information flows within the

segments or sub-unit in organizations. Thus, allowing information sharing throughout

the sub-unit. The integration of information within sub-units will help the managers in

different departments seeking useful information from other department more easily.

Not only the flow of information is important, the coordination of the various

segments within a sub-unit is also an important aspect of organizational control

(Gordon and Miller, 1976). Integrated information reduces uncertainty relating to

cause and effect relations within departments as it encourages learning and the

generation of ideas. It enables departmental managers to `learn' how to adjust

products and production methods to be compatible with other departments. It also

enables managers to better understand the different objectives that exist within

separate decision units and to make trade-offs among alternative ways to operate

within the given set of objectives.

Among the characteristics of MAIS, the breadth of scope of the information has been

identified as potentially important in assisting managerial decision making (Hayes,

1977; Chenhall and Morris, 1986). Narrowly focused MAIS is derived from

conventional financial accounts, tends to be concerned with events within the

organization, and produces data that are financial and historic. Alternatively, broad

scope MAIS includes external, non-financial and future oriented information

(Chenhall and Morris, 1986). Support for the importance of broad scope MAIS draws

on the belief that managers are involved in a wide variety of tasks and processes

which entail dealing with events which are complex and uncertain. The quantification

of such events typically includes nonfinancial information, often related to the future.

84

4.1.3 Factors influencing data quality in MAIS

Today’s organizations are operating and competing in an information age.

Information has become a key resource of most organizations, economies, and

societies. Indeed, an organization’s basis for competition has changed from tangible

products to intangible information. More and more organizations believe that quality

information is critical to their success (Wang et al., 1998). However, not many of

them have turned this belief into effective action. Poor quality information can have

significant social and business impacts. There is strong evidence that data quality

problems are becoming increasingly prevalent in practice.

Most organizations have experienced the adverse effects of decisions based on

information of inferior quality (Huang, Lee and Wang, 1999). It is likely that some

data stakeholders are not satisfied with the quality of the information delivered in

their organizations. In brief, information quality issues have become important for

organizations that want to perform well, obtain competitive advantage, or even just

survive in the 21st century.

Traditionally, data quality has often been described from the perspective of accuracy.

Nowadays, research and practice indicates that data quality should be defined beyond

accuracy and is identified as encompassing multiple dimensions (Huang, Lee and

Wang, 1999). However, there is no single standard data quality definition that has

been accepted in the field. Information is an objective commodity carried by symbols

and relates to who produced it, why and how it was produced and its relationship to

what it signifies (Shanks and Darke, 1998). Although data and information are

different concepts, data quality is often treated as the same as information quality, in

some literature and real-world practice. Therefore, in this research, data quality and

information quality are synonymous.

85

The general definition of data quality is ‘data that is fit for use by data consumers’

(Huang, Lee and Wang, 1999). Many data quality dimensions have been identified.

Commonly identified data quality dimensions are:

Accuracy, which occurs when the recorded value is in conformity with the

actual value;

Timeliness, which occurs when the recorded value is not out of date;

Completeness, which occurs when all values for a certain variable are

recorded, and

Consistency, which occurs when the representation of the data values, is the

same in all cases (Ballou et al., 1993).

The dimensions that have been identified by Ballou et al. (1993) will be adopted in

this research because they cover the most important dimensions that have been

addressed in the MAIS literature and have been reasonably widely accepted in the

data quality field. Therefore, quality data in MAIS in this research means accurate,

timely, complete, and consistent data.

Following are the six attributes of successful information systems according to the

Petter, DeLone and McLean (2008):

1. System quality – the desirable characteristics of an information system such as

ease of use, system flexibility, system reliability, and ease of learning, as well

as system features of intuitiveness, sophistication, flexibility, and response

times.

2. Information quality – the desirable characteristics of the system outputs such

as relevance, understandability, accuracy, conciseness, completeness,

understandability, currency, timeliness, and usability.

86

3. Service quality – the quality of support users receive from the IS department

and IT support personnel such as responsiveness, accuracy, reliability,

technical competence, and empathy of the personnel staff.

4. System use – the degree and manner in which staff and customers utilize the

capabilities of the system such as amount of use, frequency of use, nature of

use, appropriateness of use, extent of use, and purpose of use.

5. User satisfaction – users’ level of satisfaction with reports, Web sites, and

support services such as the most widely used multi-attribute instrument for

measuring user information satisfaction can be found in Ives et al. (1983).

6. Net benefits – the extent to which the system is contributing to the success of

individuals, groups, organizations, industries, and nations such as improved

decision- making, improved productivity, increased sales, cost reductions,

improved profits, market efficiency, consumer welfare, creation of jobs, and

economic development.

4.1.4 Traditional versus sophisticated MAIS

Management accounting information systems (MAIS) have traditionally been

regarded as an important part of the management process, critical to the success of

organizations. Good strategies required to achieve competitive advantage need to be

supported with appropriate organizational factors, including effective MAIS

(Chenhall and Langfield, 1998; Jermias and Gani, 2000). The traditional MAIS using

techniques such as single volume-based, factory overhead rates for costing products

and basically financial performance measures for measuring performance have come

under criticisms. Critics have argued that these management accounting techniques

have been in place since 1925, when factories were highly labour intensive and low

product diversity and are therefore unlikely to provide useful information for

87

managing the modern company’s operation for competitive advantage (Johnson and

Kaplan, 1987; Cooper and Kaplan, 1988).

Some researchers have suggested that rather than assist the modern manufacturing

initiatives to succeed, the poor performance of these entities may be traceable to their

continued reliance on the traditional design of MAIS. They argued that these MAIS

fail to provide appropriate goals, performance measures, or reward systems (Kaplan,

1983; Johnson and Kaplan, 1987); provide distorted product cost information which,

can result in managers making decisions that may constitute bad competitive strategy

for the business (Cooper and Kaplan, 1988; Goldratt and Cox, 1992; Kennedy and

Affleck-Graves, 2001); or even diminish a plant’s total efficiency (Goldratt and Cox,

1992). As suggested by one of the most vehement critics, cost accounting information

provided by such systems is “the number one enemy of productivity” (Goldratt, 1983,

cited in Edward and Heard, 1984, p.44).

Following these arguments, more sophisticated designs of MAIS were offered as

improvements on the traditional MAIS design. These were meant to provide more

detailed and more frequent costing information with a broader focus including

financial as well as non-financial performance information. Such systems incorporate

management accounting (MA) techniques as: the activity based costing (ABC), which

uses multiple cost drivers, rather than the single factory/departmental overhead rates

for absorbing overhead; the balanced score card (BSC), which emphasizes

nonfinancial measures of performance in addition to the financial measures; the

theory of constraints (TOC) and its associated throughput accounting (TA) with its

focus on three measures of performance described as throughput (sales minus totally

variable costs), inventory and operating expense.

88

The prior researches gave empirical evidence that using sophisticated MAIS was

more when facing uncertainity high situation, for example intensity of market

competition (Chenhall and Morris, 1986). In high condition of the intensity of market

completion, managers need the sophisticated MAIS for decision making. The

traditional accountancy information and the less sophisticated MAIS were used more

precisely by managers for decision making in low conditions of the intensity of

market completion.

In sum, while more traditional management accounting information systems used to

focus on financial and historic information about events within the organization,

modern management accounting information systems also provide external, non-

financial and future-oriented information (Atkinson et al., 2001; Chenhall and Morris,

1986; Mia and Chenhall, 1994).

4.1.5 Usefulness of MAIS

The usefulness of management accounting for decision- making in the context of

management accounting information systems has been a point of study by many

researchers. Mia and Chenhall (1994) state that the role of the management

accounting information systems has evolved from a historic orientation incorporating

only internal and financial data to a system meant for attention-direction and problem

solving tasks. In that new, future oriented role these systems also need to incorporate

external and non-financial data focusing on marketing concerns, product innovation

and predictive information related to decision areas.

In the last two decades, management accounting studies have received considerable

attention. The findings of these studies highlight a significant role for management

accounting information systems in organizations in which management accounting

89

information is now used in planning, decision-making, control, performance

measurement and business strategy in most organizations (Akbar, 2010). Thus

Manager used the MAIS for decision making. It’s about product pricing, market

demand forecasting, market planning, purchasing of raw material, product planning

and improvement of organization infrastructure (Mia and Clarke, 1999).

Result of Mia and Clarke’s (1999) study expressing that usefulness of MAIS which

could assist the company for the implementation of their plans in response to the

competitive environment. Kaplan (1983) described MAIS as a part of the

management control system (MCS) whose function is to increase organizational

effectiveness by providing useful information for management planning and control.

MAIS are expected to add value to organizations, through ensuring the effective use

of resources to gain competitive advantage.

A fundamental purpose of managerial accounting is to enhance firm value by ensuring

the effective and efficient use of scarce resources. Thus, managerial accounting

information systems should provide information that improves employees’ abilities to

make organizationally desirable decisions, thereby enabling employees to achieve the

organization’s goals and objectives (Horngren, Foster and Datar, 2007).

Additionally, managerial accounting information systems should provide information

that helps align the interests of employees with owners by directing employee effort

and attention to activities that benefit the organization (Atkinson, Kaplan and Young,

2005). Viewed in this light, the information produced by a managerial accounting

information system serves two important roles in an organization: (1) to provide some

of the necessary information for planning and decision-making, and (2) to motivate

individuals (Zimmerman, 2003).

90

According to Banbury and Naphiet (1979), the management accounting information

system is useful to communicate within the organization to achieve financial goals. It

is also useful as a performance measurement tool in an organization. In the same vein,

Collin (1982) noted that the management accounting information system is useful in

communicating role expectations and organizational climate. It could also be used for

motivational purpose associated with role performance. Both attributes of MAIS,

which are usefulness and its availability to managers, are very important. In the aspect

of the availability, it is important because it could assist managers to make a wiser

decision based on the information provided. The information available must be very

precise and timely in nature. This will avoid miscommunication among managers

from different departments. Furthermore, it will allow information sharing among the

managers in each department and sub-unit.

Modern management accounting information system can serve as a two-way

communication system between senior management and subordinate managers.

Subordinate managers get information on the company′s objectives as soon as the

objectives are clear and senior managers receive regular information - which is not

only relevant for financial reports - on performance in the different parts of the

organization. So, the use of management accounting information by chief executive

officers (CEOs) is particularly important as they perceive and interpret information

for the entire company and take action based on this information. Due to their position

they have the greatest capacity to affect their company’s behavior and thus,

performance (Tripsas and Gavetti, 2000).

Having a good management accounting information system will ensure the

availability of necessary information in a timely manner, thus helping them make

better decisions for the companies, especially in time of crisis. It is very obvious that

91

the role of management accounting information system on managerial decisions

should be considered as an important subject to be studied.

4.2 Previous Studies

4.2.1 Studies related to cost accounting system and pricing policy

Ersoy et al. (2006) have conducted a study on 51 companies from largest 500

industrial enterprises in Turkey. Their study showed that (1) direct materials cost has

the largest portion in manufacturing costs, followed by manufacturing overhead and

direct labor costs, (2) the most widely used overhead allocation base is units produced

(30 percent), followed by direct labor hours (23 percent), direct machine hours (15

percent).

Ngu (1997) conducted a study on the topic of product cost and in it, he identified

importance of a product cost to the decision making process of the company. The data

used were got from primary and secondary sources and had been analysed using

quantitative and qualitative means. In the study, he made the point to differentiate the

various costing methods that can be used to come out with the product cost along with

job costing. The study revealed that companies making one of a kind or special order

products use job costing.

Uyar (2008) conducted a study in Denizli, Turkey. The study found that 30

companies out of 86 (35 percent) use process costing, 23 companies (27 percent) use

job costing, and 17 companies (20 percent) use both methods. The same study showed

that most widely used overhead allocation base is units produced (45 companies out

of 86), followed by direct material costs (14 companies out of 86), direct machine

hours (7 companies out of 86), and direct labor costs (7 companies out of 86).

92

Another important finding of this study is that the largest share in manufacturing costs

belongs to direct materials costs.

Gorpinpaitoon (1982) made a study on the use of job costing in the shipbuilding

industry in Thailand. His study was aimed at examining the costing method used by

shipbuilding firms in Thailand in order to ascertain the principle, the costing method

and its problems. This study was made through direct observation of the actual

operations and the interviews of the personnel involved in that industry. At the end of

the study, it was realised that the costs of direct materials and direct labour are

charged to the job, but factory overheads are accumulated and allocated to each job on

the basis of direct labour cost or as a percentage of work finished.

Dalci and Tanis (2008) argued that advancements in information technology (IT)

have enabled companies to use computers to carry out their activities that were

previously performed manually. Accounting systems that were previously performed

manually can now be performed with the help of computers. Therefore, improvements

in the information technology have facilitated the use of cost and management

accounting procedures.

Govindarajan and Anthony (1983) found in their survey of Fortune 1000 companies

that 82% of the respondents priced their products based on full costs. Only 17% of the

respondents indicated that they rely on variable costs for their product pricing

decisions.

Shim and Sudit (1995) found that about 70% of the companies used full cost-based

pricing, 12% used variable cost-based pricing, and 18% used market-based pricing.

93

4.2.2 Studies related to usage of management accounting techniques

Ghosh and Chan (1997) have conducted a study in Singapore companies. They

indicated that a general improvement was made in the management accounting

practice in Singapore, where more companies were employing various accounting

techniques in managing the business affairs. However, the new techniques such as

Total Quality Management (TQM) and Activity-Based Costing (ABC) were slowly

being accepted and used by the Singapore local companies, and these local companies

continue to lag behind the multinational companies.

Chan (2002) conducted a study in Singapore companies to investigate the

management accounting practices of companies in that country. The results of the

study showed that there was a little improvement in the practice of management

accounting since 1997. In addition, it was found that Singapore companies were

ineffective in the use of costing tools and that the local Singapore companies were

avoiding the use of advanced management accounting techniques. This is because the

advanced techniques would involve with high level of complexity and a high amount

of resources were needed for its implementation.

Triest and Elshabat (2007) have done a study on 40 industrial companies in Egypt.

This study indicated that cost accounting information in Egypt is available at a basic

level, and used more for external (pricing) purposes than for internal (performance)

purposes. They also found that the use of advanced cost accounting techniques such

as activity-based costing system seem absent.

Joshi (2001) has conducted a comparative study in manufacturing companies in India.

The results indicated that Indian manufacturing companies rely heavily on the

traditional management accounting techniques such as variable costing, budget for

94

day-to-day operations, capital budgeting tools, return on investment based

performance evaluation, and performance evaluation. However, the adoption rates of

recently developed practices such as shareholders’ value analysis, performance

evaluation (qualitative measures), product life cycle costing, back flush costing,

activity based budgeting, value chain analysis, benchmarking and balanced scorecard,

have been rather low and slow.

Hossain et al. (2006) have conducted a study on management accounting practices in

the listed manufacturing companies of Bangladesh. The results of this study have

revealed that all sectors fail to practice some newly developed techniques. They have

suggested improving and fastening the management accounting practices.

Wijewardena and Zoysa (1999) conducted a comparative analysis of management

accounting practices in Australia and Japan. They investigated the differences in the

adoption of management accounting techniques through a survey questionnaire which

was mailed to 1000 largest manufacturing companies in each country. The size of the

company was based on total assets. A total of 217 Japanese companies and 231

Australian companies responded to the 31 questions asked covering various aspects of

managerial accounting techniques.

The results of the comparative survey revealed that management accounting practices

of Australian companies placed emphasis on cost control tools (e.g. budgeting,

standard costing and variance analysis) at the manufacturing stage while Japanese

companies focused attention on cost planning and cost reduction tools such as target

costing at the product planning and design stage. This finding is in agreement with

another study of Howell and Sukarai (1992) that “Japanese companies seem to

understand better than their western counterparts that cost should be managed and

95

avoided during the product planning and product cycle stages rather than when

products have entered full scale production”. Another noteworthy difference that

emanated from the survey was that activity-based costing (ABC) appeared to be

popular among Australian companies while it was rarely used in Japanese companies.

Despite the decreased labor component in the manufacturing cost structure,

manufacturing companies in both countries seemed to allocate factory overhead

mainly on the basis of direct labor.

Adler, Everett and Waldron (2000) have conducted a survey that asked

management accountants, in New Zealand manufacturing businesses, to indicate the

techniques adopted in their business. While many studies have focused on particular

techniques such as ABC or target costing, Adler, Everett and Waldron provided a

questionnaire that included a vast array of management accounting techniques to

provide a fuller set of response options. Results indicated that traditional management

accounting techniques, such as full costing, direct costing and standard costing were

found to be used more often than advanced management accounting techniques, such

as strategic management accounting.

Chandra and Mazumder (2007) examined the status of use of management

accounting techniques in the manufacturing enterprises in Bangladesh. It has been

discovered that modern techniques like Activity-Based Costing, Target Costing, Just-

in-Time (JIT), Total Quality Management (TQM), Process Reengineering and The

Theory of Constraints (TOC) were not used in public and private sector

manufacturing enterprises but a few Multinational Corporations (MNC) are using

some of techniques like JIT and TQM. Also traditional techniques like ratio Analysis,

Standard Costing, Cash Flow Analysis were found widely used.

96

Chenhall and Langfield (1998) conducted a survey in Australian manufacturing

firms to identify the extent to which they have adopted certain traditional and recently

developed management accounting practices. The results of the study indicate that the

overall rates of adoption of traditional management accounting practices were higher

than recently developed techniques. However, newer techniques such as activity-

based costing were more widely adopted.

Drury et al. (1993) conducted a survey in U.K manufacturing firms. The study found

that allocation methods such as plant wide rates and labour based rates are being used

because of their simplicity. ABC was widely considered, but not used extensively.

Standard costing, payback analysis, and target profit and return on investment were

widely used. The survey by Drury et al. is consistent with a similar study in1990

found that target costing and ABC were widely used.

Farjana and Amran (2011) conducted a study to measure the significance of

management accounting techniques in decision making of the selected manufacturing

organizations in Bangladesh. The findings of the study reveal that cash flow statement

analysis, ratio analysis, budgetary control, CVP analysis, variance analysis and fund

flow analysis have been frequently used high-ranking techniques.

Farjana and Rehana (2010) have made a comparative analysis in the variability of

management accounting practice in manufacturing and service industries. The

findings reveal that ratio analysis, budgetary control, CVP analysis, variance analysis

and fund flow analysis are used frequently in managerial functions.

4.2.3 Studies related to information characteristics of MAIS

Chenhall and Morris (1986) studied managers' needs for their organizations' MAS

information. They identified four dimensions of information- scope, timeliness,

97

aggregation and integration. Using these four dimensions, they developed and tested

an instrument to measure perceived usefulness of MAS information. They argued that

managers would prefer strategically useful information which includes broad-scope,

timely, aggregated and integrated information. The findings of the study found that

the type of information perceived to be useful by managers was broad in scope and

timeliness. This study made an important contribution to management accounting

research by arguing that the broad characteristics of MAS would influence the design

of MAS. It concluded that such conceptualization can provide a common basis for

comparing MAS in different organizations and industries.

Chong (1996) has examined a study on the interactive effects of management

accounting systems design and task uncertainty of managerial performance. The

findings indicated that, under circumstances of high task uncertainty, the extent of

using broad-scope MAS information resulted in effective managerial decisions and

improved managerial performance. Whereas under a condition of low task

uncertainty, the extent of using broad-scope MAS information resulted in information

overload which was dysfunctional to managerial performance.

4.2.4 Studies related to the use of MAIS

Gaidiene and Skyrius (2006) have conducted a survey study on the usefulness of

management accounting information: users’ attitudes. The study investigates the role

and development of management accounting and the usefulness of its information

perceived by managers. The management accounting system is characterized in terms

of information. These characteristics are: scope, timeliness, the level of aggregation,

and information which assists integration. The results of the study showed that all

interviewed managers’ perceived management accounting (economic and non-

98

economic) information as useful. However, the level of their scores has been higher

than that of accountants.

Sajady et al. (2008) conducted a study on the effectiveness of accounting information

systems of finance managers of listed companies at Tehran Stock Exchange. The

findings of the study indicate that implementation of accounting information systems

at these companies caused the improvement of managers’ decision-making process,

internal controls, and the quality of the financial reports and facilitated the process of

the company’s transactions. The results did not show any indication that performance

evaluation process had been improved.

Subramaniam (1993) has examined the gap between the perceived usefulness of

MAS information by managers and the extent of availability of information. The

results of the study showed that there was a significant MAS adequacy gap in the

manufacturing industry.

Choe (1996) conducted a study on the importance of the relationships among

performance of accounting information systems, the result showed that the use of

information system a statistically significant influence on the performance for the

firms. The findings of the study concluded the following results: 1) There is a

significant relationship between the size of the firm and the AIS application 2) There

is a significant relationship between the ability of the employees and the AIS

applications.

Hayes (1977) has conducted a research on the role of managerial accounting in

business organizations which generally is perceived to be the provision of information

for decision making by various managerial levels of the organization's hierarchy. The

findings indicated that the management accounting information is perceived as an

99

important element to have, in helping the organization particularly the managers to

communicate with their colleagues in decision-making process.

4.3 Chapter Summary

In Chapter 4 the theoretical concepts and studies related to the role of management

accounting information system were reviewed. The review includes the theoretical

concept of MAIS such as the concept of MAIS, operational model and characteristics

of MAIS, factors influencing data quality in MAIS, traditional versus sophisticated

MAIS, and usefulness of MAIS; and various related studies conducted in this

important field of research under the headings of cost accounting system and pricing

policy, usage of management accounting techniques, information characteristics of

MAIS, and the use of MAIS.

The next chapter presents the research design and methodology associated with this

research.