Embed Size (px)

DESCRIPTION

Chapter 22. Long-Term Bonds. LO1. Bond Selling Price. Bond Certificate at Par Value. Learning Objective 1 Compare bond financing with stock financing. Bond Issuing Procedures. - PowerPoint PPT Presentation

Citation preview

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Chapter 22

Long-Term Bonds

22-22-22

Bond Certificateat Par Value

Bond Certificateat Par Value

Bond Selling Price

Corporation Investors

Learning Objective 1 Compare bond financing with stock financing.Bond Issuing Procedures

Bonds are securities that can be readily bought and sold. A large number of bonds are traded on the New York Exchange and the American Exchange. Since bonds are bought and sold in the market, they have a market value, or price. For convenience, bond market values are expressed as a percent of their par value.

At regularly scheduled dates during the life of the bond, the company pays the bondholders interest. Interest is calculated as Bond Par Value times the Stated Interest Rate on the bond times the length of time the bond has been outstanding during the year. Just like all interest rates, the stated interest rate is expressed on an annual basis.

LO1

22-22-33

Bond Issue Date

Bond Maturity Date

Bond Par Value

at Maturity Date

Corporation Investors

Bond Issuing Procedures

At the maturity date, the company pays the bondholders the bond’s par value.

LO1

22-22-44

King Co. issues the following bonds on January 1, 2010King Co. issues the following bonds on January 1, 2010Par Value = $1,000,000Par Value = $1,000,000Stated Interest Rate = 10%Stated Interest Rate = 10%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2010Bond Date = Jan. 1, 2010Maturity Date = Dec. 31, 2029 (20 years)Maturity Date = Dec. 31, 2029 (20 years)

DR CRJan. 1 Cash 1,000,000

Bonds payable 1,000,000 Issued bonds at par

Learning Objective 2Prepare entries to record bond issuance and bond interest expense.

Issuing Bonds at Par

$1,000,000 $1,000,000 × 10% × ½ year = × 10% × ½ year = $50,000$50,000

This entry is made every six months until the bonds mature.

$1,000,000 $1,000,000 × 10% × ½ year = × 10% × ½ year = $50,000$50,000

This entry is made every six months until the bonds mature.

The entry on June 30, 2010, to record the first The entry on June 30, 2010, to record the first semiannual interest payment is . . .semiannual interest payment is . . .

The entry on June 30, 2010, to record the first The entry on June 30, 2010, to record the first semiannual interest payment is . . .semiannual interest payment is . . .

LO2

22-22-55

Prepare the entry for Jan. 1, 2010, to record the Prepare the entry for Jan. 1, 2010, to record the following bond issue by Rose Co. following bond issue by Rose Co. Par Value = $1,000,000Par Value = $1,000,000Issue Price = 92.6405% of par valueIssue Price = 92.6405% of par valueStated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 12%Market Interest Rate = 12%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2010 Bond Date = Jan. 1, 2010

Maturity Date = Dec. 31, 2014 (5 years)Maturity Date = Dec. 31, 2014 (5 years)

Prepare the entry for Jan. 1, 2010, to record the Prepare the entry for Jan. 1, 2010, to record the following bond issue by Rose Co. following bond issue by Rose Co. Par Value = $1,000,000Par Value = $1,000,000Issue Price = 92.6405% of par valueIssue Price = 92.6405% of par valueStated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 12%Market Interest Rate = 12%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2010 Bond Date = Jan. 1, 2010

Maturity Date = Dec. 31, 2014 (5 years)Maturity Date = Dec. 31, 2014 (5 years)

Learning Objective 3Compute and record amortization of bond discount.

} Bond will sell at a discount.Bond will sell at a discount.

LO3

22-22-66

Par Value

Cash Proceeds Discount

1,000,000$ - 926,405$ = 73,595$

Par Value

Cash Proceeds Discount

1,000,000$ - 926,405$ = 73,595$

Amortizing the discount increases Interest Expense over the Amortizing the discount increases Interest Expense over the outstanding life of the bond.outstanding life of the bond.

Amortizing the discount increases Interest Expense over the Amortizing the discount increases Interest Expense over the outstanding life of the bond.outstanding life of the bond.

$1,000,000$1,000,000 92.6405%92.6405%$1,000,000$1,000,000 92.6405%92.6405%

Issuing Bonds at a Discount

On Jan. 1, 2010, Rose Co. records the bond issue as follows. On Jan. 1, 2010, Rose Co. records the bond issue as follows.

DR CR Jan. 1 Cash 926,405

Discount on bonds payable 73,595 Bonds payable 1,000,000

Sold bonds at a discount on issue date

Contra-LiabilityContra-LiabilityAccountAccount

Contra-LiabilityContra-LiabilityAccountAccount

LO3

22-22-77

Partial Balance Sheet as of January 1, 2010

Long-term Liabilities: Bonds Payable 1,000,000$ Less: Discount on Bonds Payable 73,595 926,405$

Partial Balance Sheet as of January 1, 2010

Long-term Liabilities: Bonds Payable 1,000,000$ Less: Discount on Bonds Payable 73,595 926,405$

Issuing Bonds at a DiscountUsing the straight-line Using the straight-line method, the discount method, the discount amortization is $7,360 amortization is $7,360

every six months. every six months.

$73,595 ÷ 10 periods = $73,595 ÷ 10 periods = $7,360* *(rounded)$7,360* *(rounded)

Using the straight-line Using the straight-line method, the discount method, the discount amortization is $7,360 amortization is $7,360

every six months. every six months.

$73,595 ÷ 10 periods = $73,595 ÷ 10 periods = $7,360* *(rounded)$7,360* *(rounded)

DR CR June 30 Bond interest expense 57,360

Discount on bonds payable 7,360 Cash 50,000

Paid semi-annual interest and amortized discount

$73,595 ÷ 10 periods = $7,360 (rounded)

$1,000,000 × 10% × ½ = $50,000

$73,595 ÷ 10 periods = $7,360 (rounded)

$1,000,000 × 10% × ½ = $50,000

Make the following entry every six months to record the payment of interest and Make the following entry every six months to record the payment of interest and the amortization of the discount.the amortization of the discount.

Make the following entry every six months to record the payment of interest and Make the following entry every six months to record the payment of interest and the amortization of the discount.the amortization of the discount.

LO3

22-22-88

Learning Objective 4Compute and record amortization of bond premium.

Prepare the entry for Jan. 1, 2010, to record the following bond issue by Rose Co.Prepare the entry for Jan. 1, 2010, to record the following bond issue by Rose Co. Par Value = $1,000,000Par Value = $1,000,000Issue Price = 108.1145% of par valueIssue Price = 108.1145% of par valueStated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 8%Market Interest Rate = 8%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2010Bond Date = Jan. 1, 2010

Maturity Date = Dec. 31, 2014 (5 years)Maturity Date = Dec. 31, 2014 (5 years)

Prepare the entry for Jan. 1, 2010, to record the following bond issue by Rose Co.Prepare the entry for Jan. 1, 2010, to record the following bond issue by Rose Co. Par Value = $1,000,000Par Value = $1,000,000Issue Price = 108.1145% of par valueIssue Price = 108.1145% of par valueStated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 8%Market Interest Rate = 8%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2010Bond Date = Jan. 1, 2010

Maturity Date = Dec. 31, 2014 (5 years)Maturity Date = Dec. 31, 2014 (5 years)

Bond will sell at a premium.

DR CRJan. 1 Cash 1,081,145

Premium on bonds payable 81,145 Bonds payable 1,000,000

Issued bonds at a premium on issue date

Adjunct-LiabilityAdjunct-LiabilityAccountAccount

Adjunct-LiabilityAdjunct-LiabilityAccountAccount

LO4

22-22-99

Using the straight-line Using the straight-line method, the premium method, the premium amortization is $8,115 amortization is $8,115

every six months. every six months.

$81,145 ÷ 10 periods = $81,145 ÷ 10 periods = $8,115 (rounded)$8,115 (rounded)

Using the straight-line Using the straight-line method, the premium method, the premium amortization is $8,115 amortization is $8,115

every six months. every six months.

$81,145 ÷ 10 periods = $81,145 ÷ 10 periods = $8,115 (rounded)$8,115 (rounded)

Partial Balance Sheet as of January 1, 2010

Long-term Liabilities: Bonds Payable 1,000,000$ Add: Premium on Bonds Payable 81,145 1,081,145$

Partial Balance Sheet as of January 1, 2010

Long-term Liabilities: Bonds Payable 1,000,000$ Add: Premium on Bonds Payable 81,145 1,081,145$

Issuing Bonds at a Premium

DR CR June 30 Bond interest expense 41,885

Premium on bonds payable 8,115 Cash 50,000

Paid semi-annual interest and

amortized premium

$81,145 ÷ 10 periods = $8,115 (rounded)

$1,000,000 × 10% × ½ = $50,000

$81,145 ÷ 10 periods = $8,115 (rounded)

$1,000,000 × 10% × ½ = $50,000

This entry is made every six months to record the payment of interest and This entry is made every six months to record the payment of interest and the amortization of the premium.the amortization of the premium.

This entry is made every six months to record the payment of interest and This entry is made every six months to record the payment of interest and the amortization of the premium.the amortization of the premium.

LO4

22-22-1010

Learning Objective 5Record the retirement of bonds.

When bonds are paid off at maturity, the carrying value of the bond will equal the par value; the journal entry to record the transaction simply includes a debit to Bonds Payable and a credit to Cash.

Assume that Rose Co. permits its bondholders to convert their bond certificates for 100,000 shares of the company’s $5 par value common

stock. At the time of conversion, the carrying value of the bonds is $1,024,340. The following entry is required.

DR CR Bonds payable 1,000,000 Premium on bonds payable 24,340

Common stock 500,000 Paid-in capital in excess of par 524,340

To record retirement of bonds by conversion

LO5

22-22-1111

Learning Objective 6Prepare entries to account for bond sinking funds.

DR CR Jan. 1 Bond sinking fund 180,975

Cash 180,975 Initial contribution to sinking fund

On January 1, 2010, Ross makes the On January 1, 2010, Ross makes the first contribution to the sinking fund first contribution to the sinking fund and prepares the following entries.and prepares the following entries.

On January 1, 2010, Ross makes the On January 1, 2010, Ross makes the first contribution to the sinking fund first contribution to the sinking fund and prepares the following entries.and prepares the following entries.

On December 31, 2010, the On December 31, 2010, the sinking fund manager reported sinking fund manager reported

interest earned. Ross makes this interest earned. Ross makes this entry . . .entry . . .

On December 31, 2010, the On December 31, 2010, the sinking fund manager reported sinking fund manager reported

interest earned. Ross makes this interest earned. Ross makes this entry . . .entry . . .

DR CR Dec. 31 Bond sinking fund 9,049

Bond sinking fund income 9,049 Interest earned during 2010

On January 1, 2010, Rose Co. issues $1,000,000 par value On January 1, 2010, Rose Co. issues $1,000,000 par value bonds due in 5 years. The company is required to make 5 bonds due in 5 years. The company is required to make 5 contributions of $180,975 into a sinking fund that will earn contributions of $180,975 into a sinking fund that will earn

5% interest on all contributions.5% interest on all contributions.

On January 1, 2010, Rose Co. issues $1,000,000 par value On January 1, 2010, Rose Co. issues $1,000,000 par value bonds due in 5 years. The company is required to make 5 bonds due in 5 years. The company is required to make 5 contributions of $180,975 into a sinking fund that will earn contributions of $180,975 into a sinking fund that will earn

5% interest on all contributions.5% interest on all contributions.

LO6

22-22-1212

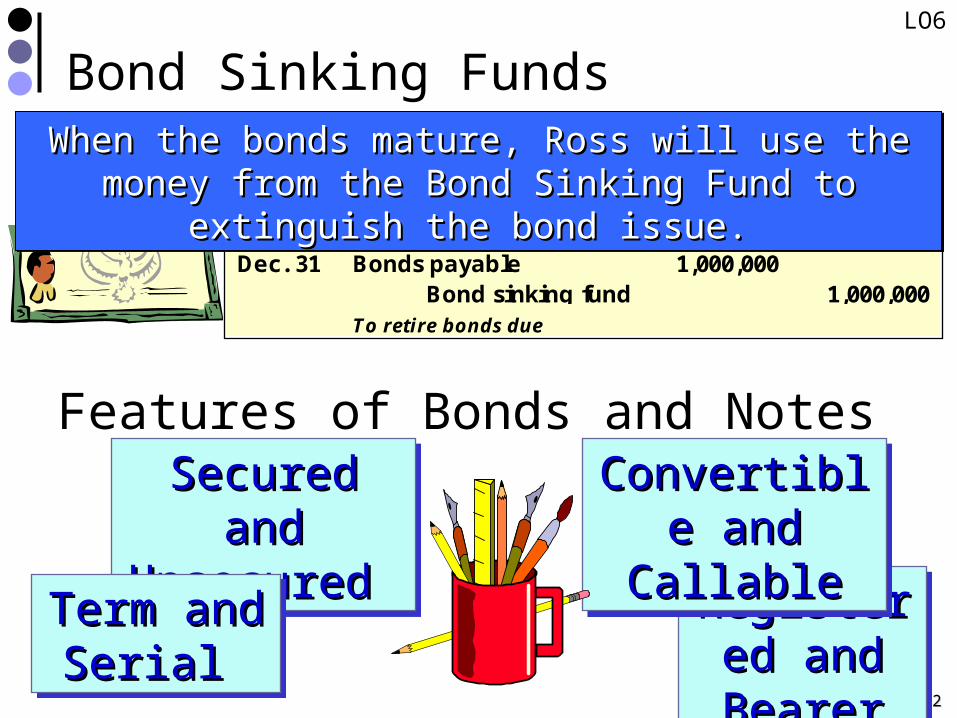

Bond Sinking Funds

DR CR Dec. 31 Bonds payable 1,000,000

Bond sinking fund 1,000,000 To retire bonds due

When the bonds mature, Ross will use the money from When the bonds mature, Ross will use the money from the Bond Sinking Fund to extinguish the bond issue. the Bond Sinking Fund to extinguish the bond issue.

When the bonds mature, Ross will use the money from When the bonds mature, Ross will use the money from the Bond Sinking Fund to extinguish the bond issue. the Bond Sinking Fund to extinguish the bond issue.

Features of Bonds and NotesSecured and Secured and Unsecured Unsecured

Secured and Secured and Unsecured Unsecured

Term and Term and Serial Serial

Term and Term and Serial Serial

Registered Registered and Bearerand BearerRegistered Registered and Bearerand Bearer

Convertible Convertible and Callableand CallableConvertible Convertible and Callableand Callable

LO6

22-22-1313

Learning Objective 7Assess debt features and their implications.

Notes are typically between a company and a single lender, such as a bank.When the note payable is issued, the lender provides the cash to the company and the company signs a note payable contract agreeing to repay the principal plus interest. For some notes, the note principal and interest are paid in a single payment at the end of the note term.

Other notes require regular payments during the note term. In some cases, the regular payments consist of equal principal payments plus interest. In other cases, the regular payments consist of equal payments that include both principal payments and interest payments.

Other notes require regular payments during the note term. In some cases, the regular payments consist of equal principal payments plus interest. In other cases, the regular payments consist of equal payments that include both principal payments and interest payments.

In cases where the payments include equal principal payments, the payment amounts decrease over time as interest expense decreases.

In cases where the payments are equal, the amount of the principal payment increases each year as the interest expense decreases.

In cases where the payments include equal principal payments, the payment amounts decrease over time as interest expense decreases.

In cases where the payments are equal, the amount of the principal payment increases each year as the interest expense decreases.

LO7

22-22-1414

Mortgage Notes and Bonds A legal agreement that helps protect the lender if the borrower fails to make A legal agreement that helps protect the lender if the borrower fails to make

the required payments.the required payments.

Gives the lender the right to be paid out of the cash proceeds from the sale of Gives the lender the right to be paid out of the cash proceeds from the sale of the borrower’s assets specifically identified in the mortgage contract. the borrower’s assets specifically identified in the mortgage contract.

A legal agreement that helps protect the lender if the borrower fails to make A legal agreement that helps protect the lender if the borrower fails to make the required payments.the required payments.

Gives the lender the right to be paid out of the cash proceeds from the sale of Gives the lender the right to be paid out of the cash proceeds from the sale of the borrower’s assets specifically identified in the mortgage contract. the borrower’s assets specifically identified in the mortgage contract.

Operating LeasesA lease is a contractual agreement between a lessor (asset owner) and a lessee A lease is a contractual agreement between a lessor (asset owner) and a lessee (asset renter or tenant). The lessee has the right to use the asset for a period of (asset renter or tenant). The lessee has the right to use the asset for a period of

time in exchange for cash payments to the lessor.time in exchange for cash payments to the lessor.

A lease is a contractual agreement between a lessor (asset owner) and a lessee A lease is a contractual agreement between a lessor (asset owner) and a lessee (asset renter or tenant). The lessee has the right to use the asset for a period of (asset renter or tenant). The lessee has the right to use the asset for a period of

time in exchange for cash payments to the lessor.time in exchange for cash payments to the lessor.

Learning Objective 8Compute the debt-to-equity ratio and explain its use.

Debt-to-Equity Ratio

Total Liabilities

Total Equity=

This ratio helps investors determine the risk of investing in a

company by dividing its total liabilities by its total equity. The lower the number, the safer the

investment will be.

This ratio helps investors determine the risk of investing in a

company by dividing its total liabilities by its total equity. The lower the number, the safer the

investment will be.

LO7

LO8

22-22-1515

Learning Objective 9Describe the accrual of bond interest when bond payments do not align with accounting periods.OnOn 2/1/092/1/09, , Matrix, Inc. issues 1,000 bonds at face value plus accrued Matrix, Inc. issues 1,000 bonds at face value plus accrued

interest to Webster, Inc. The market interest rate is 10%.interest to Webster, Inc. The market interest rate is 10%.

Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/11 (5 years) Maturity Date = 12/31/11 (5 years)

Stated Interest Rate = 10%Stated Interest Rate = 10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = Bond Date = 1/1/091/1/09

OnOn 2/1/092/1/09, , Matrix, Inc. issues 1,000 bonds at face value plus accrued Matrix, Inc. issues 1,000 bonds at face value plus accrued interest to Webster, Inc. The market interest rate is 10%.interest to Webster, Inc. The market interest rate is 10%.

Face Value = $1,000Face Value = $1,000

Maturity Date = 12/31/11 (5 years) Maturity Date = 12/31/11 (5 years)

Stated Interest Rate = 10%Stated Interest Rate = 10%

Interest Dates = 6/30 & 12/31Interest Dates = 6/30 & 12/31

Bond Date = Bond Date = 1/1/091/1/09

DR CR Feb. 1 Cash 1,008,333

Interest Payable 8,333 Bonds Payable 1,000,000 To record issuance of bonds

DR CR June 1 Bond Interest Expense 41,667

Interest Payable 8,333 Cash 50,000 To record interest payment

LO9

22-22-1616

End of Chapter 22