Embed Size (px)

Citation preview

Chapter 17

Activity-Based Costing and Analysis

17-2

Conceptual Learning Objectives

C1: Distinguish between the plantwide overhead rate method, the departmental overhead rate method, and activity-based costing method.

C2: Explain cost flows for the plant wide overhead rate method.

C3: Explain cost flows for the departmental overhead rate method.

C4: Explain cost flows for activity-based costing.

17-3

A1: Identify and assess advantages and disadvantages of the plantwide overhead rate method.

A2: Identify and assess advantages and disadvantages of the departmental overhead rate method.

A3: Identify and assess advantages and disadvantages of activity-based costing.

Analytical Learning Objectives

17-4

P1: Allocate overhead costs to products using the plantwide overhead rate method.

P2: Allocate overhead costs to products using departmental overhead rate method.

P3: Allocate overhead costs to products using activity-based costing.

Procedural Learning Objectives

17-5

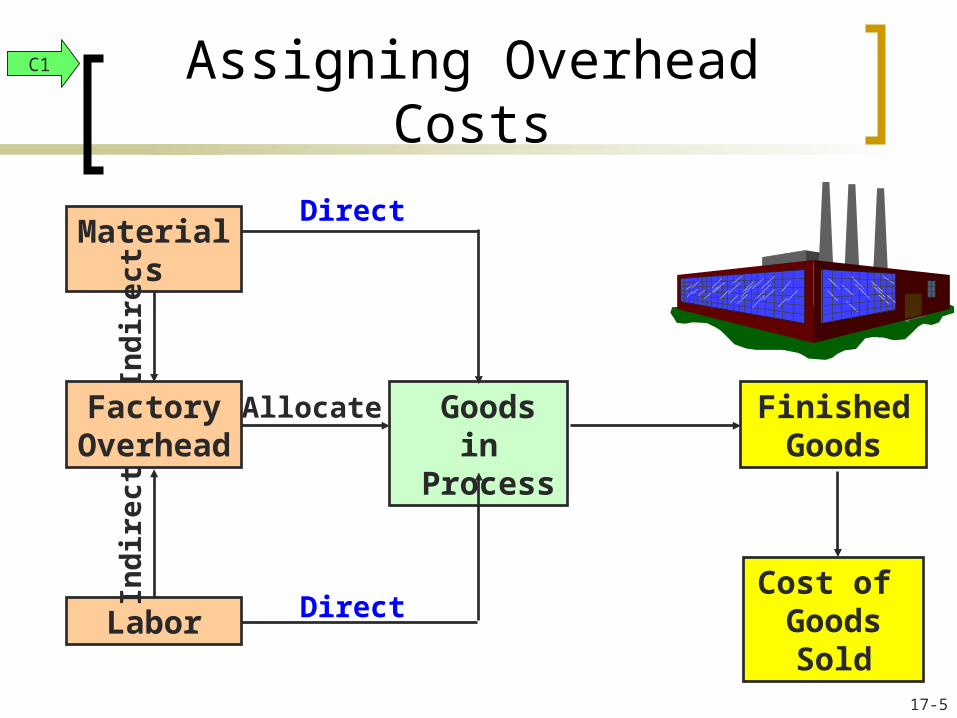

Assigning Overhead CostsC1

Goods in Process

Cost of GoodsSold

Labor

Materials

Ind

irec

tIn

dir

ect

FinishedGoods

FactoryOverhead

Direct

Direct

Allocate

17-6

Assigning Overhead Costs

Overhead costs are not directly related to production volume, and therefore cannot be traced to units of product in the same way as direct materials and direct labor. Consequently, we must assign overhead costs using an allocation system.

This chapter identifies three methods of overhead allocation.

17-7

Assigning Overhead CostsC1

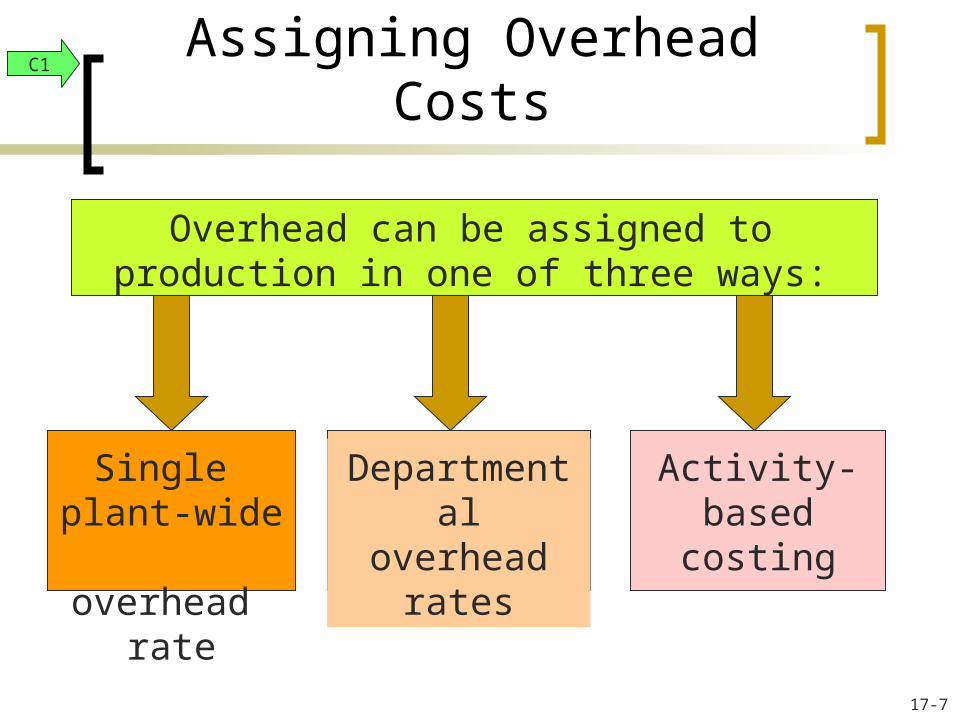

Overhead can be assigned to production in one of three ways:

Single plant-wide overhead

rate

Departmental overhead

rates

Activity-based costing

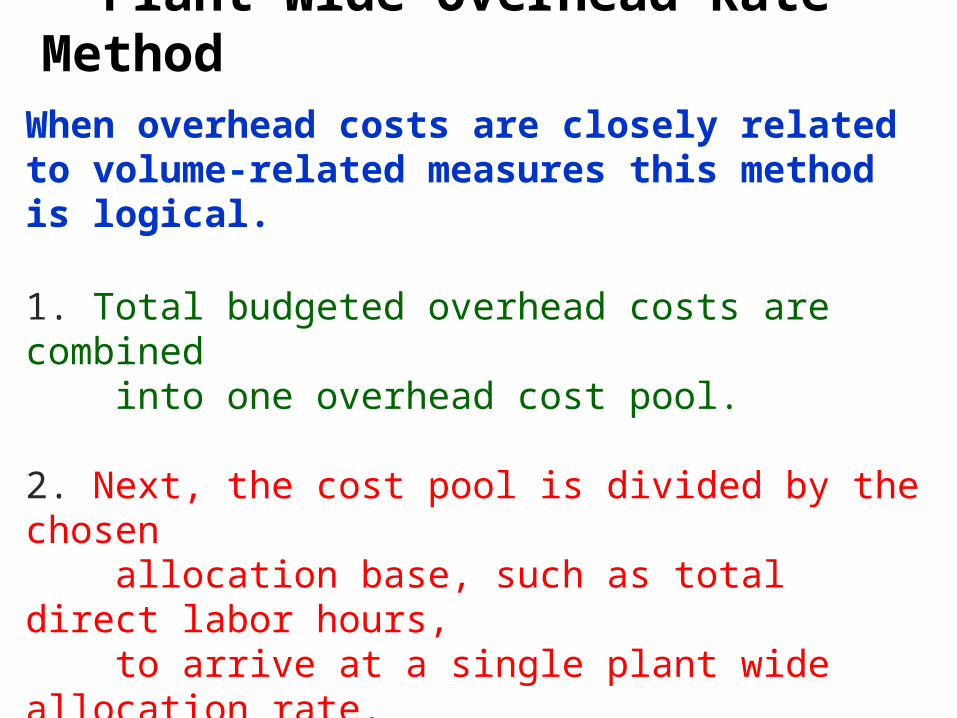

Plant Wide Overhead Rate MethodWhen overhead costs are closely related to volume-related measures this method is logical.

1. Total budgeted overhead costs are combined into one overhead cost pool.

2. Next, the cost pool is divided by the chosen allocation base, such as total direct labor hours, to arrive at a single plant wide allocation rate.

3. Finally, this rate is applied to assign costs to all products.

4. The target of the cost assignment or Cost Object is the unit of product.

17-9

Plant Wide Overhead Rate Method

Overhead CostIndirect Costs

Cost Allocation

Base

Single Plant-Wide Overhead Rate

Cost Objects Product 1 Product 2 Product 3

C2

17-10

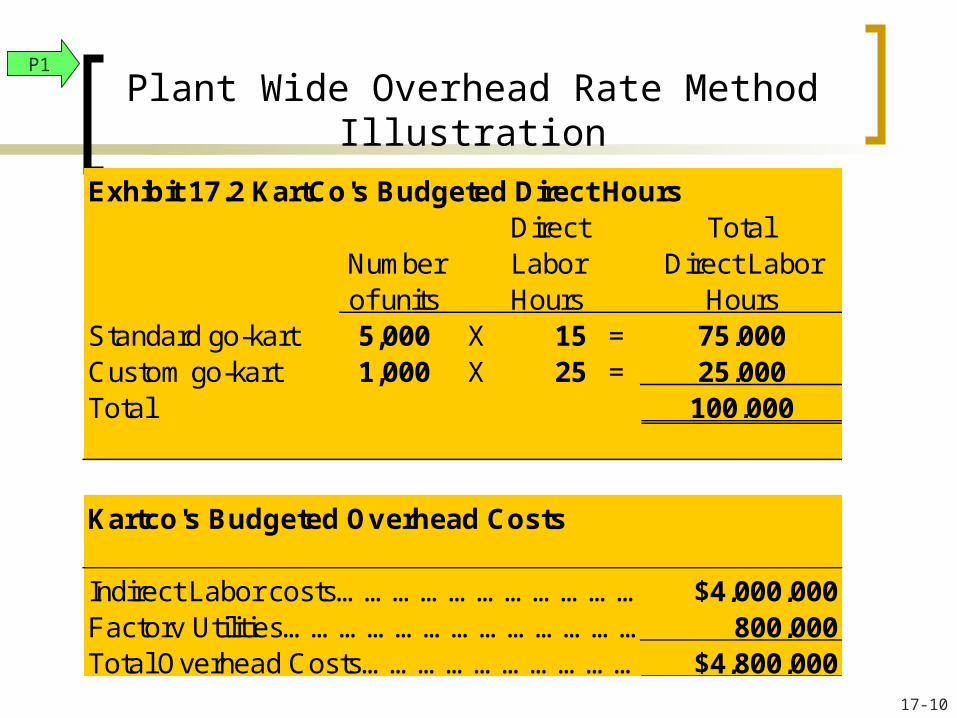

Plant Wide Overhead Rate Method Illustration

Exhibit 17.2 KartCo's Budgeted Direct HoursDirect Total

Number Labor Direct Laborof units Hours Hours

Standard go-kart 5,000 X 15 =Custom go-kart 1,000 X 25 =Total

Kartco's Budgeted Overhead Costs

100,000

75,00025,000

$4,800,000

Indirect Labor costs………………………………………………………………………………………………………………………………..Factory Utilities………………………………………………………………………………………………………………………………………..Total Overhead Costs……………………………………………………………………………………………………………………………

$4,000,000800,000

P1

17-11

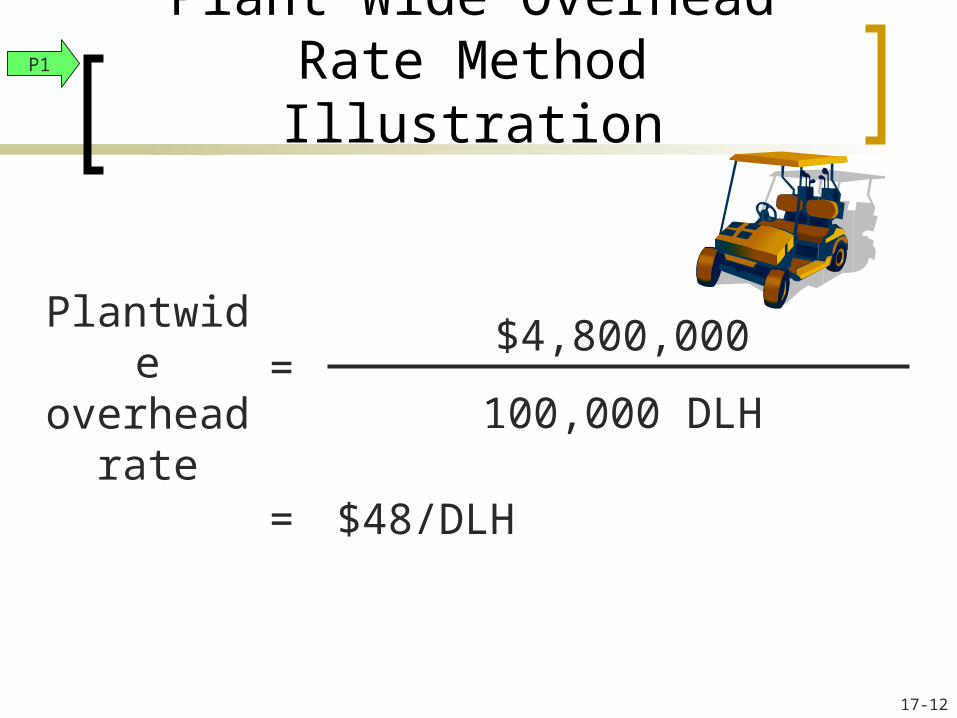

Plant Wide Overhead Rate Method Illustration

P1

Plantwide overhead

rate=

Total budgeted overhead costs

Total budgeted DLH

17-12

Plant Wide Overhead Rate Method Illustration

P1

Plantwide overhead

rate=

$4,800,000

100,000 DLH

= $48/DLH

17-13

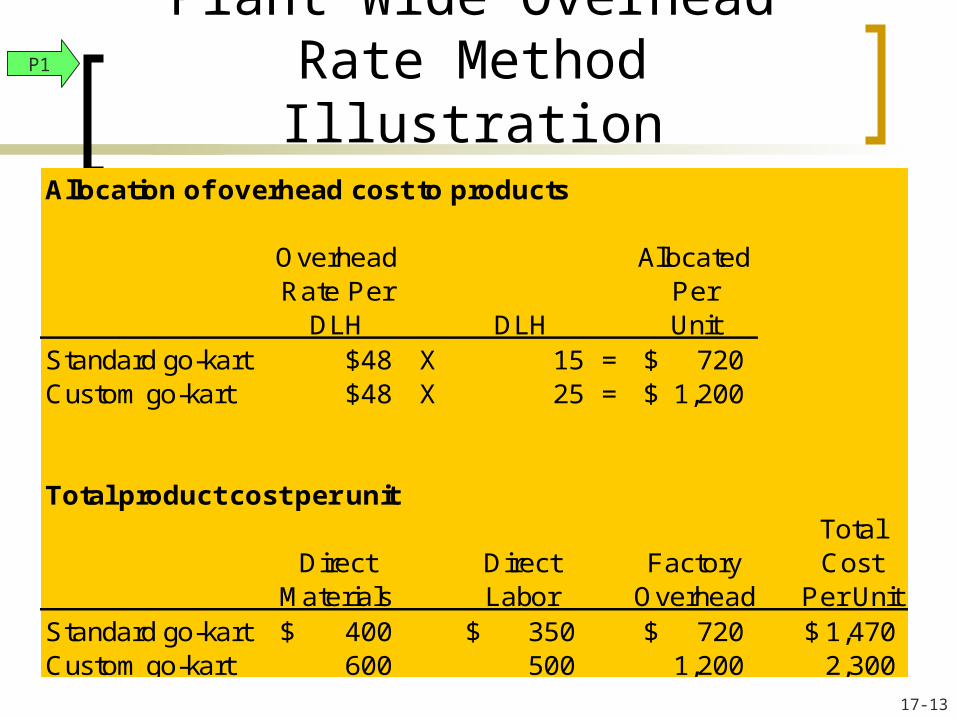

Plant Wide Overhead Rate Method Illustration

P1

Allocation of overhead cost to products

Overhead AllocatedRate Per Per

DLH DLH UnitStandard go-kart $48 X 15 = 720$ Custom go-kart $48 X 25 = 1,200$

Total product cost per unitTotal

Direct Direct Factory CostMaterials Labor Overhead Per Unit

Standard go-kart 400$ 350$ 720$ 1,470$ Custom go-kart 600 500 1,200 2,300

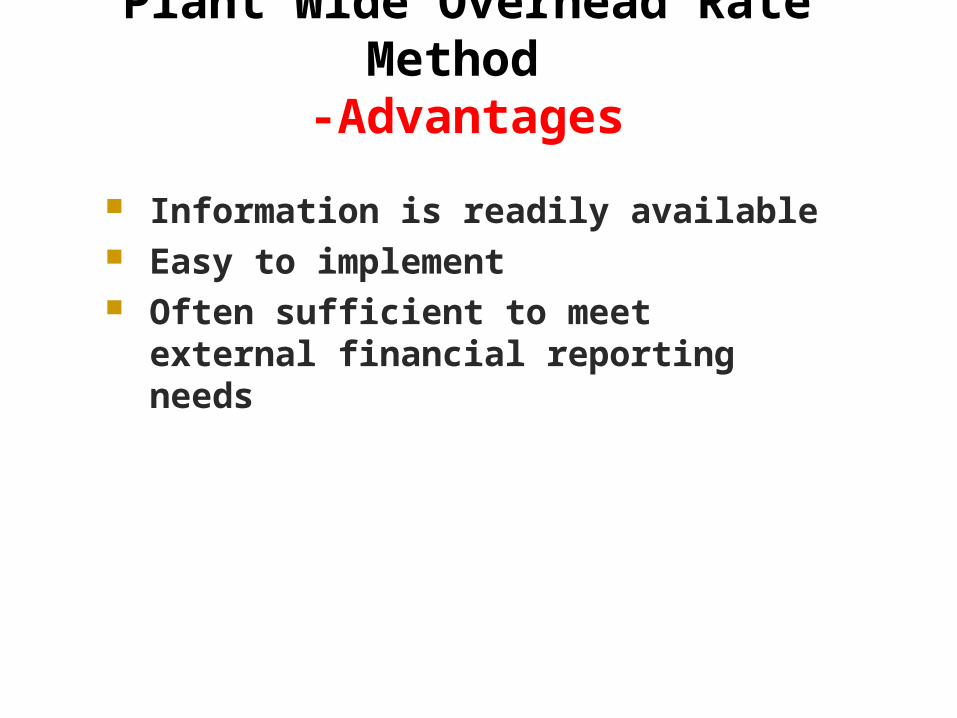

Plant Wide Overhead Rate Method -Advantages

Information is readily available Easy to implement Often sufficient to meet external

financial reporting needs

Plant Wide Overhead Rate Method -Disadvantages

Overhead costs may not bear any relationship with direct labor hours.

Example: Technology Intensive vs. Labor Intensive production stages.

Various types of products within the same company may not use overhead costs in the same proportion.

Departmental Overhead Rate Method

Many companies have several departments that produce various products and consumes overhead resources in a substantially different way.

Example:Machining Dept => Machine HoursAssembly Dept => Labor Hours

Departmental OH Rate is a better method to allocate of costs to departments when overhead resources are consumed in substantially different ways.

Departmental Overhead Rate Method

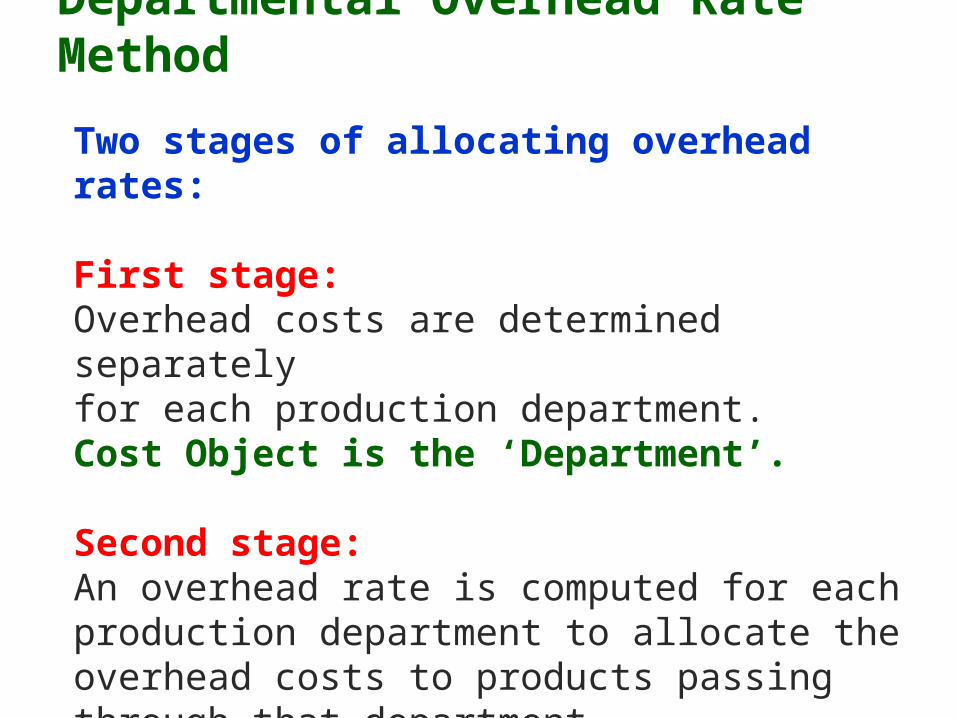

Two stages of allocating overhead rates:

First stage: Overhead costs are determined separately for each production department.Cost Object is the ‘Department’.

Second stage:An overhead rate is computed for each production department to allocate the overhead costs to products passing through that department. Cost Object is the ‘Product’.

17-18

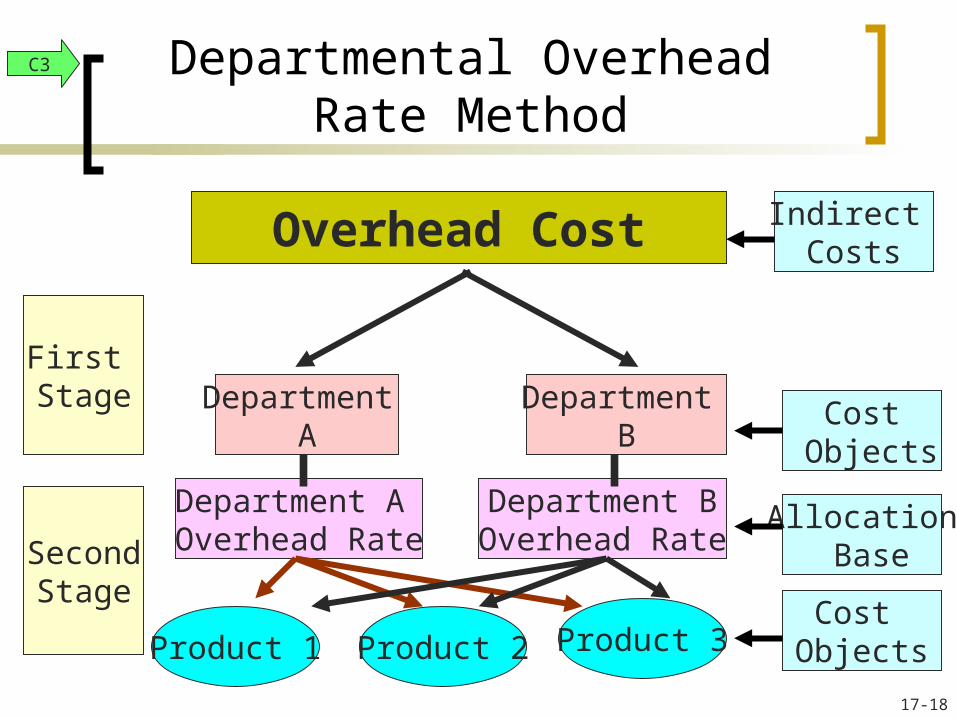

Departmental Overhead Rate Method

Overhead Cost

First Stage

SecondStage

Department A

Indirect Costs

Cost Objects

Allocation Base

Cost Objects

Department A Overhead Rate

Department B

Department BOverhead Rate

Product 1 Product 2 Product 3

C3

17-19

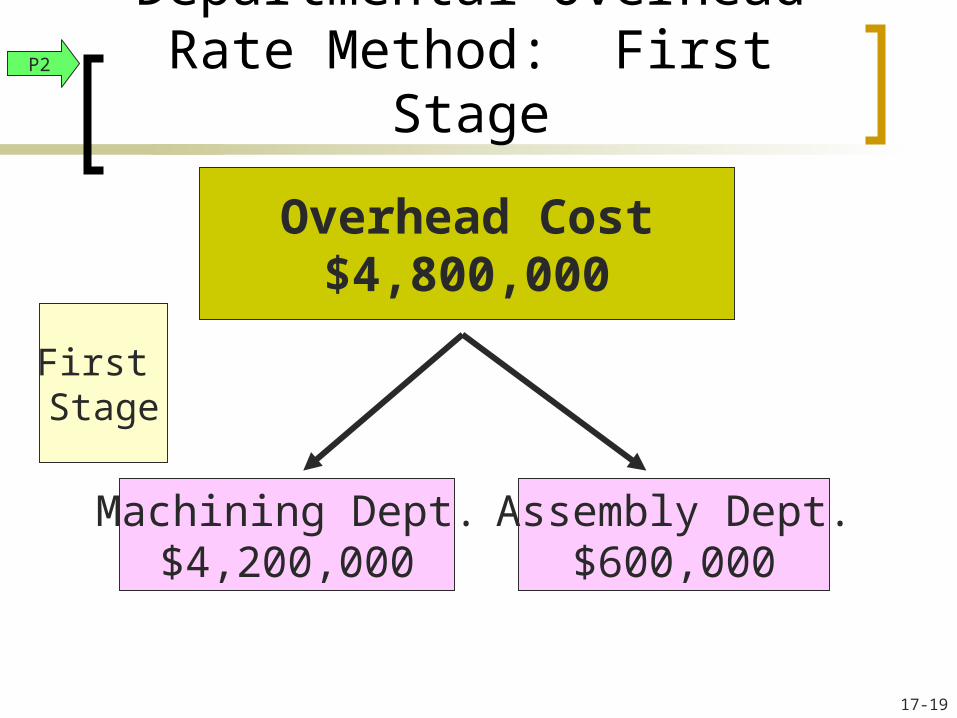

Departmental Overhead Rate Method: First Stage

Overhead Cost$4,800,000

First Stage

Machining Dept.$4,200,000

Assembly Dept.$600,000

P2

17-20

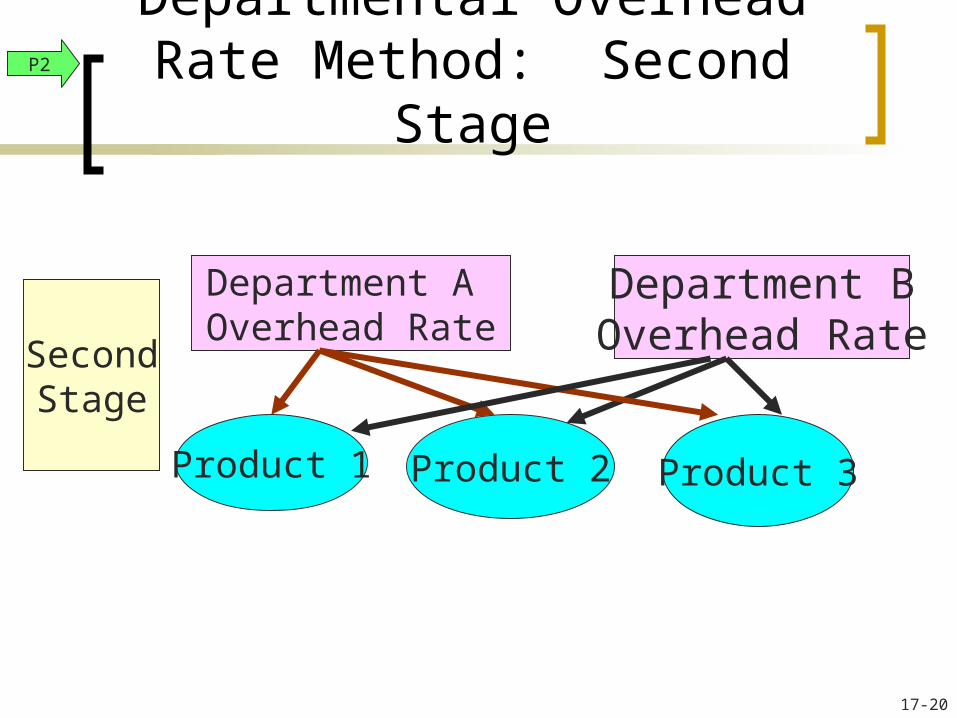

Departmental Overhead Rate Method: Second Stage

SecondStage

Department A Overhead Rate

Department BOverhead Rate

Product 1 Product 2 Product 3

P2

17-21

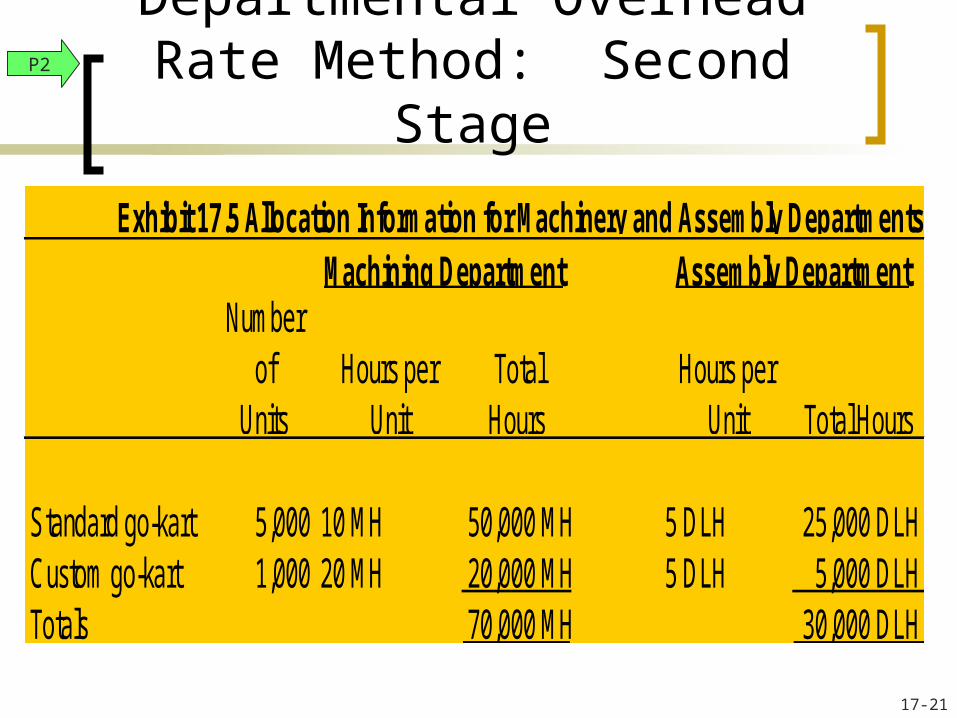

Departmental Overhead Rate Method: Second Stage

Number of

UnitsHours per

UnitTotal Hours

Hours per Unit Total Hours

Standard go-kart 5,000 10 MH 50,000 MH 5 DLH 25,000 DLHCustom go-kart 1,000 20 MH 20,000 MH 5 DLH 5,000 DLHTotals 70,000 MH 30,000 DLH

Exhibit 17.5 Allocation Information for Machinery and Assembly DepartmentsMachining Department Assembly Department

P2

17-22

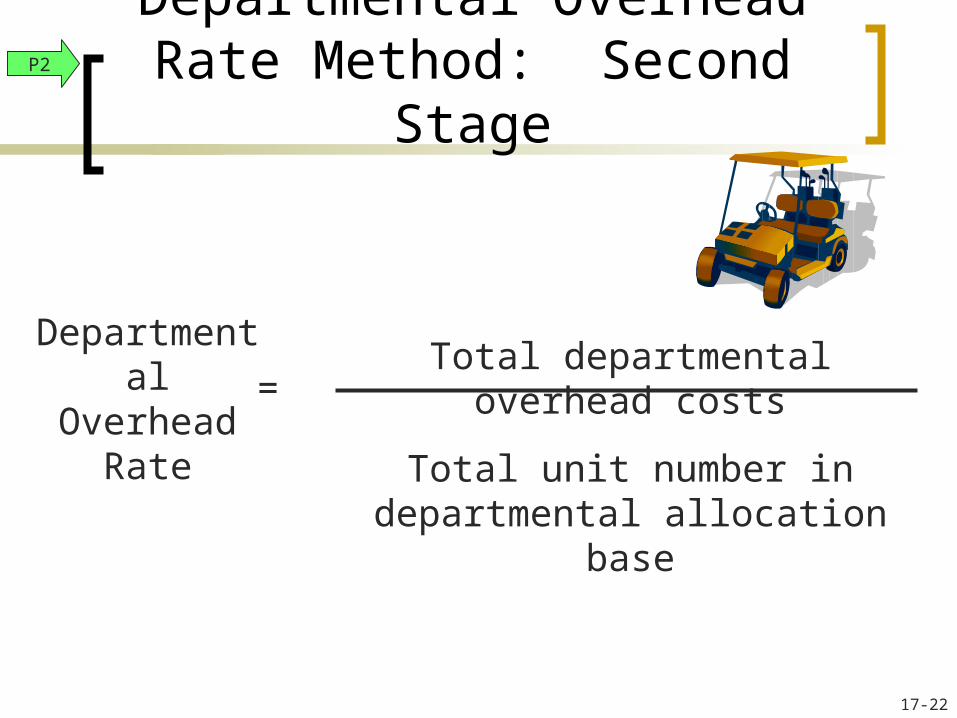

Departmental Overhead Rate Method: Second Stage

P2

Departmental Overhead

Rate=

Total departmental overhead costs

Total unit number in departmental allocation base

17-23

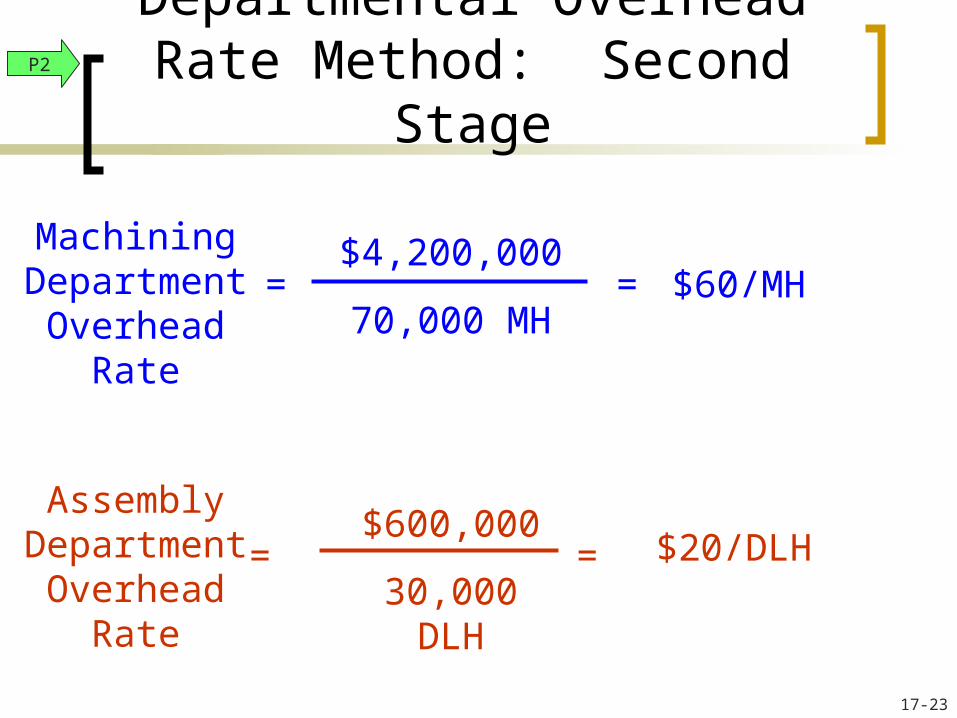

Departmental Overhead Rate Method: Second Stage

P2

Machining Department Overhead

Rate

=$4,200,000

70,000 MH= $60/MH

Assembly Department Overhead

Rate

=$600,000

30,000 DLH= $20/DLH

17-24

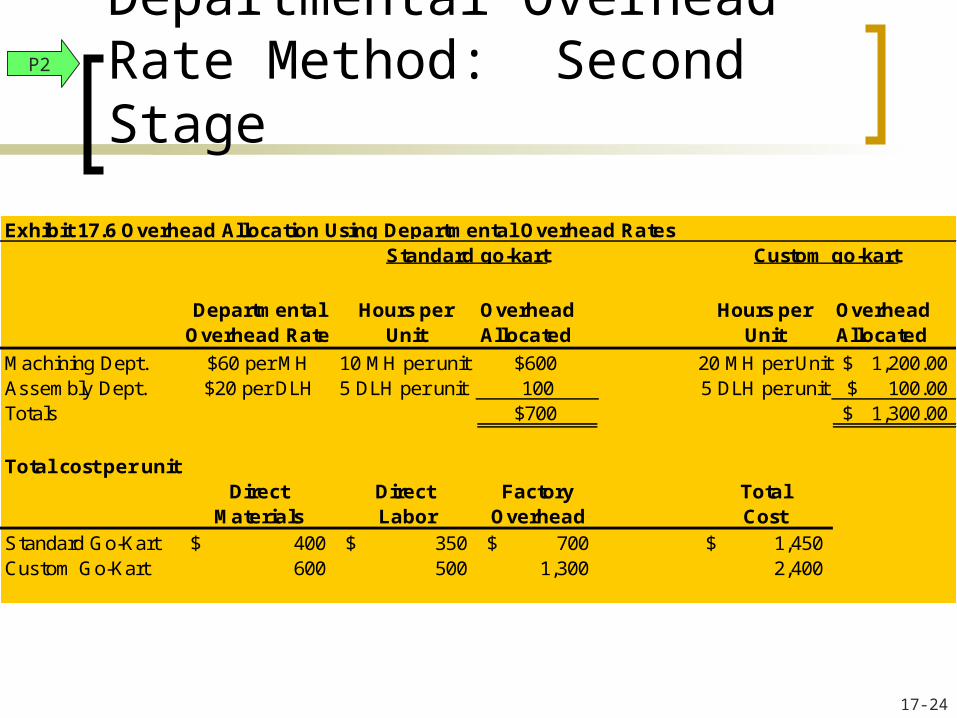

Departmental Overhead Rate Method: Second Stage

Departmental Overhead Rate

Hours per Unit

Overhead Allocated

Hours per Unit

Overhead Allocated

Machining Dept. $60 per MH 10 MH per unit $600 20 MH per Unit 1,200.00$ Assembly Dept. $20 per DLH 5 DLH per unit 100 5 DLH per unit 100.00$ Totals $700 1,300.00$

Total cost per unitDirect Direct Factory Total

Materials Labor Overhead CostStandard Go-Kart 400$ 350$ 700$ 1,450$ Custom Go-Kart 600 500 1,300 2,400

Exhibit 17.6 Overhead Allocation Using Departmental Overhead RatesStandard go-kart Custom go-kart

P2

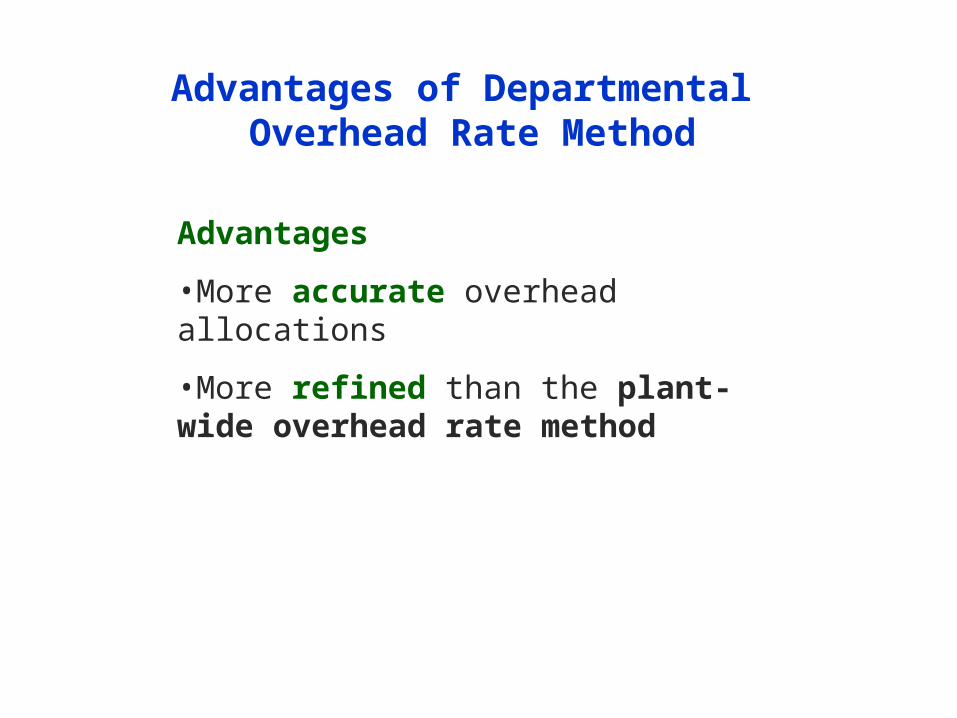

Advantages of Departmental Overhead Rate Method

Advantages

•More accurate overhead allocations

•More refined than the plant-wide overhead rate method

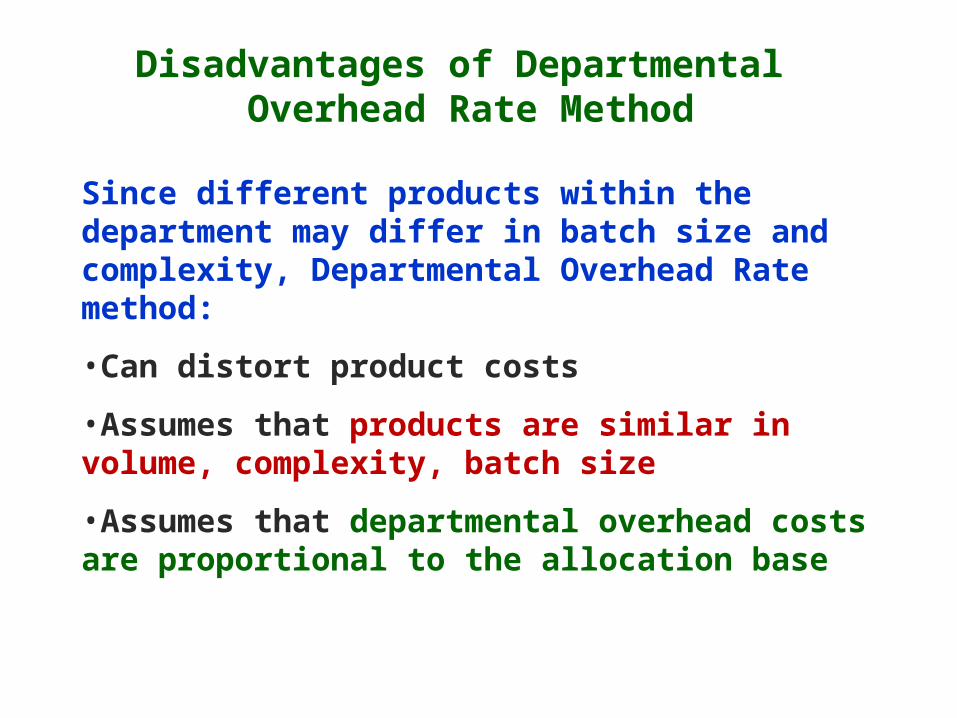

Disadvantages of Departmental Overhead Rate Method

Since different products within the department may differ in batch size and complexity, Departmental Overhead Rate method:

•Can distort product costs

•Assumes that products are similar in volume, complexity, batch size

•Assumes that departmental overhead costs are proportional to the allocation base

Activity-Based Costing (ABC) MethodActivity-Based Costing (ABC) Rates and method attempts to more accurately assign overhead costs by focusing on activities.

The premise of ABC is that it takes activities to make products and provide services.

These activities drive cost. For example, costs are incurred and resources are used when we perform activities:

-Cutting Raw Materials;-Inspecting parts;-Processing Invoices

Activity-Based Costing (ABC) Method

Activity is the basic principle underlying ABC method.Activity is a TASK, OPERATION, or PROCEDURE which causes costs to be incurred => Cost Driver.

Example: Warehousing Products consumes resources (drives costs) such as:

-Employee time for driving forklift;-Electricity to power forklift;-Wear & tear (depreciation) on a forklift.

Training employees consumes resources (drives costs) such as:

-Trainers’ salaries;-Training supplies

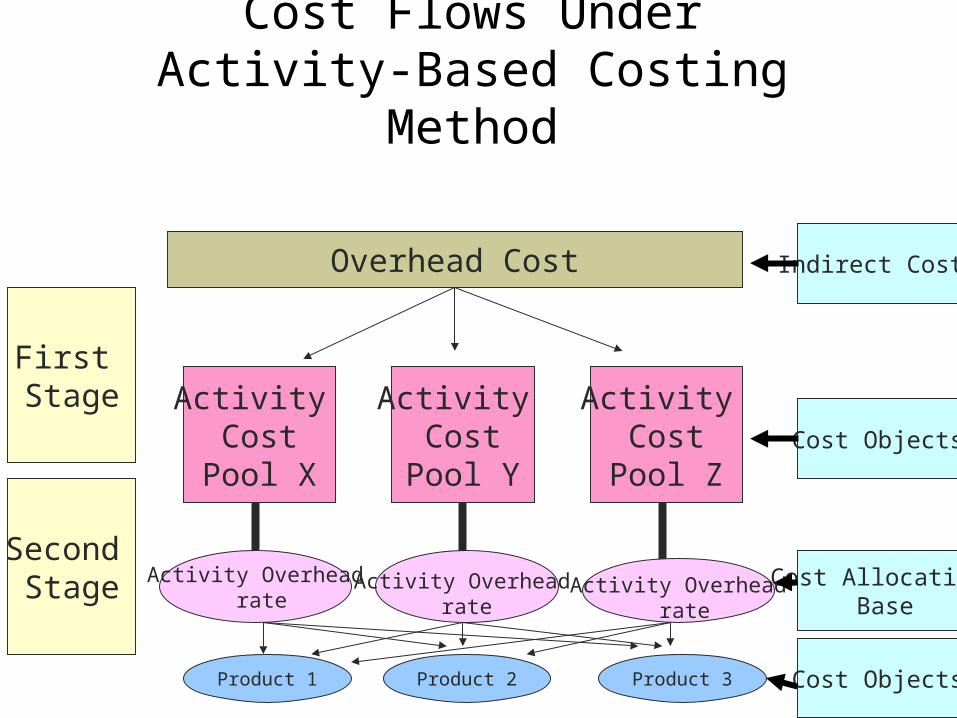

Activity-Based Costing (ABC) MethodThere are two basic stages to ABC:

The first stage of ABC cost assignment is to Identify the activities (cost objects) involved in manufacturing products and match those activities with the costs that they cause (cost driver).

To reduce the total number of activities that must be assigned costs, the homogeneous activities (those caused by the same factors such as cutting metal) are grouped into activity cost pool.

The second stage of ABC is to compute an activity rate for each cost pool and use this rate to allocate overhead costs to products (cost objects).

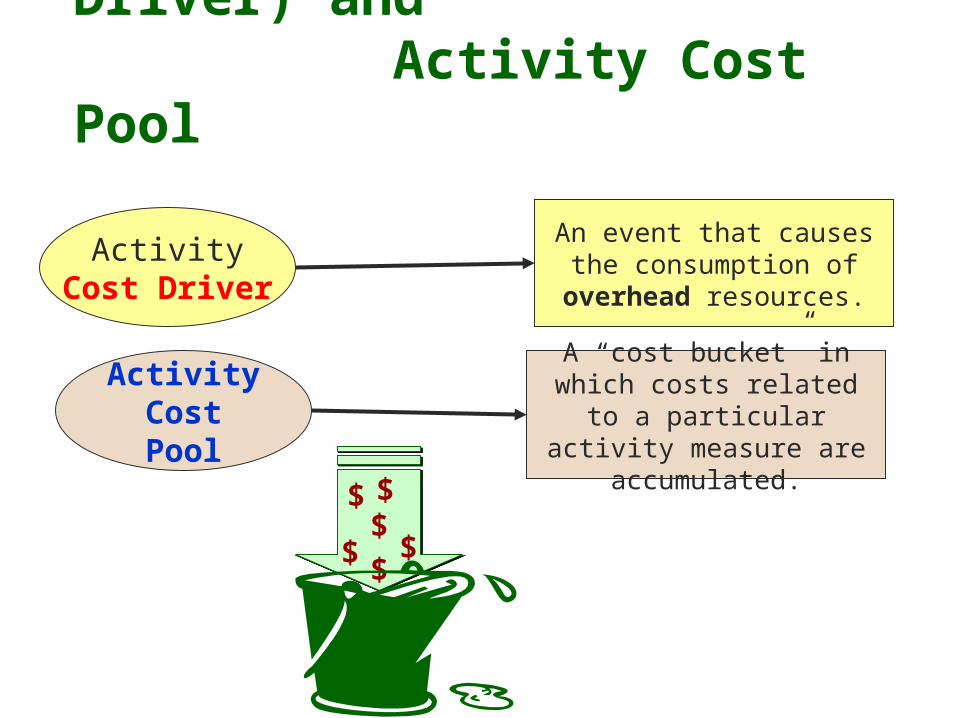

ActivityCost Driver

An event that causes the consumption of overhead

resources.

Activity Cost Pool

A “cost bucket” in which costs related to a particular

activity measure are accumulated.

$

$

$ $

$$

ABC: Activity (Cost Driver) and Activity Cost Pool

Cost Flows Under Activity-Based Costing Method

Overhead Cost

Activity Cost

Pool X

Activity Cost

Pool Y

Activity Cost

Pool Z

First Stage

Second Stage Activity Overhead

rateActivity Overhead

rateActivity Overhead

rate

Product 1 Product 2 Product 3

Indirect Costs

Cost Objects

Cost Objects

Cost Allocation Base

17-32

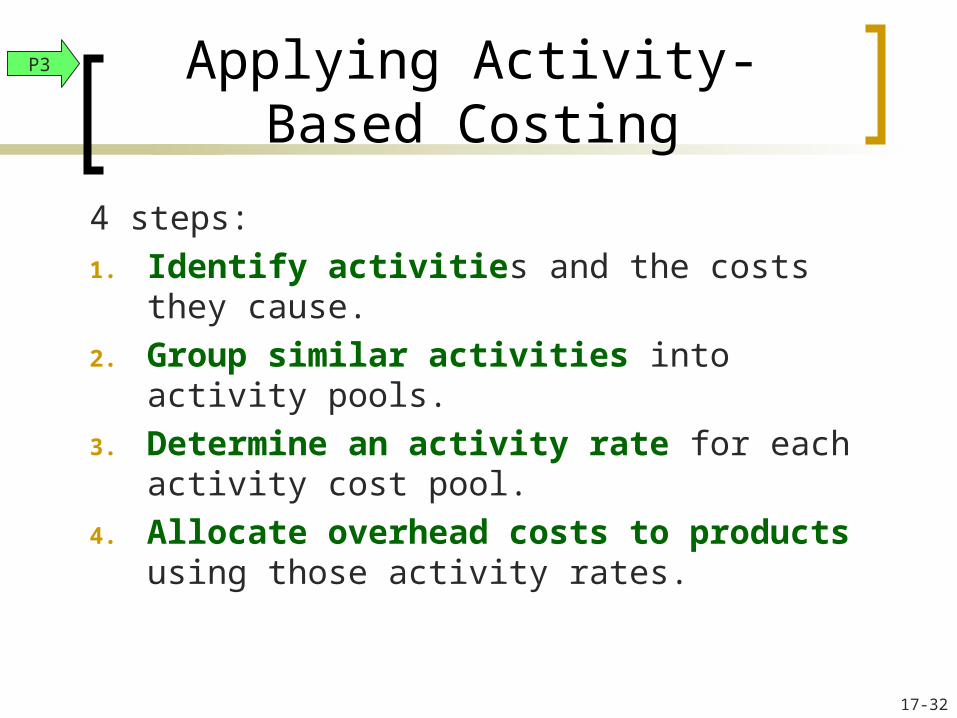

Applying Activity-Based Costing

4 steps:

1. Identify activities and the costs they cause.

2. Group similar activities into activity pools.

3. Determine an activity rate for each activity cost pool.

4. Allocate overhead costs to products using those activity rates.

P3

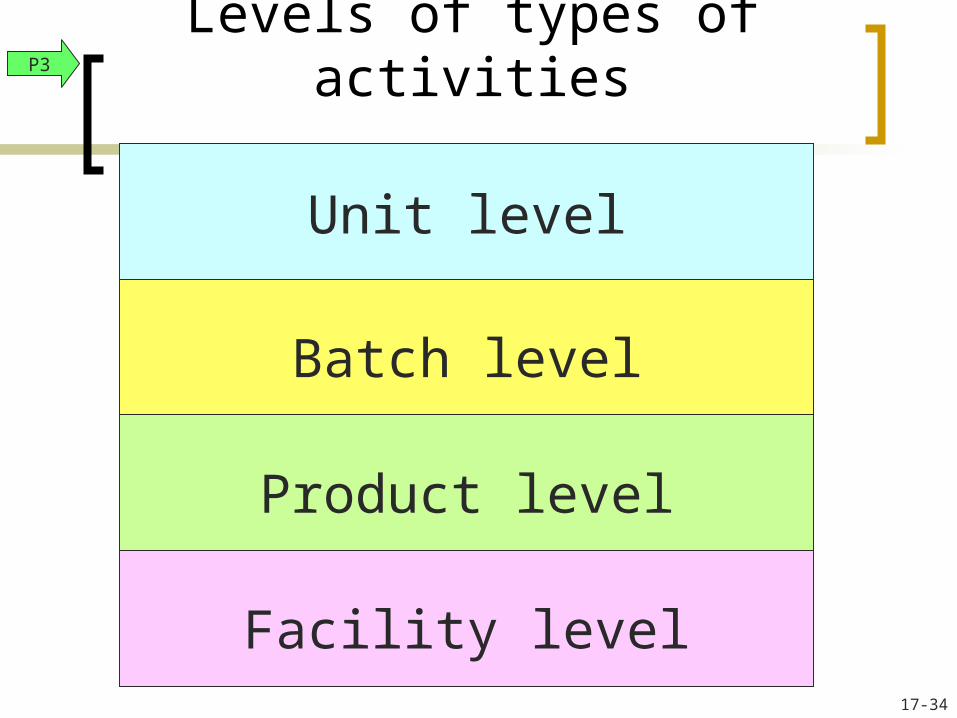

Step one: Identify activities and cost pools.

Activities causing overhead cost are typically separated into four levels reflecting control:

(1) Unit level activities are performed on each product unit,

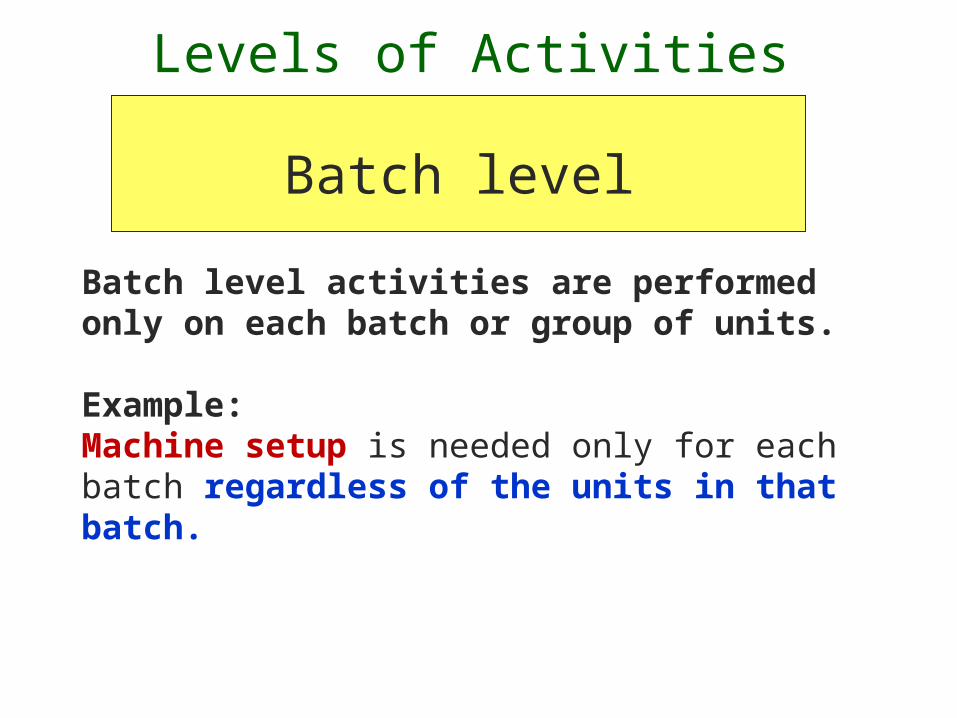

(2) Batch level activities are performed only on each batch or group of units,

(3) Product level activities are performed on each product line independent of the number of units or batches, and

(4) Facility level activities are performed to sustain facility capacity as a whole.

17-34

Levels of types of activitiesP3

Unit level

Batch level

Product level

Facility level

17-35

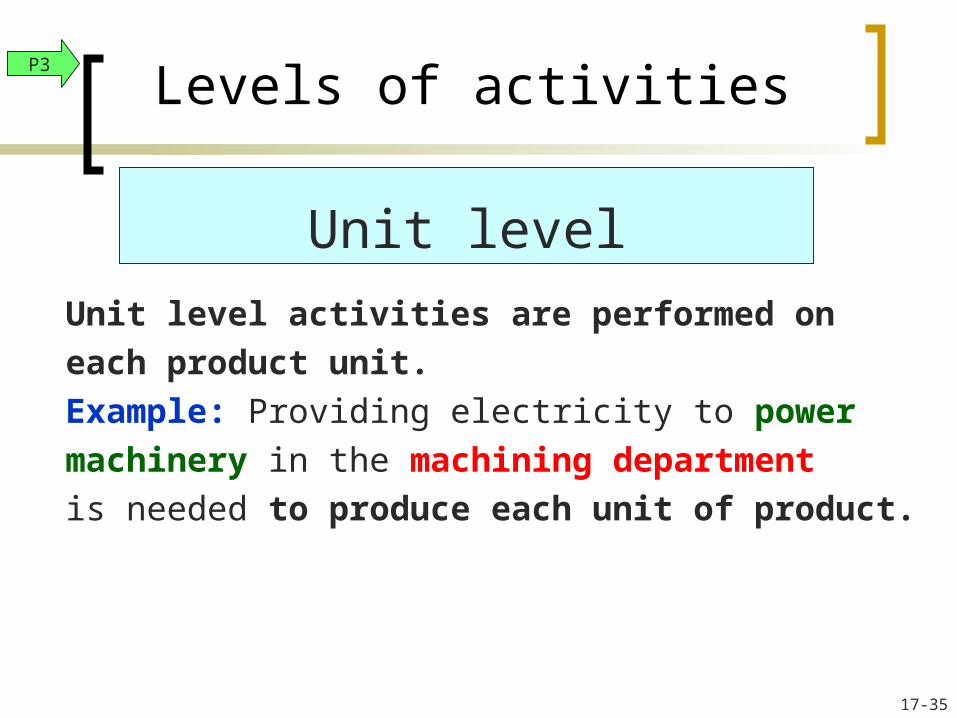

Levels of activities

Unit level activities are performed on

each product unit.

Example: Providing electricity to power

machinery in the machining department

is needed to produce each unit of product.

P3

Unit level

Levels of Activities

Batch level activities are performedonly on each batch or group of units.

Example: Machine setup is needed only for eachbatch regardless of the units in thatbatch.

Batch level

Levels of Activities

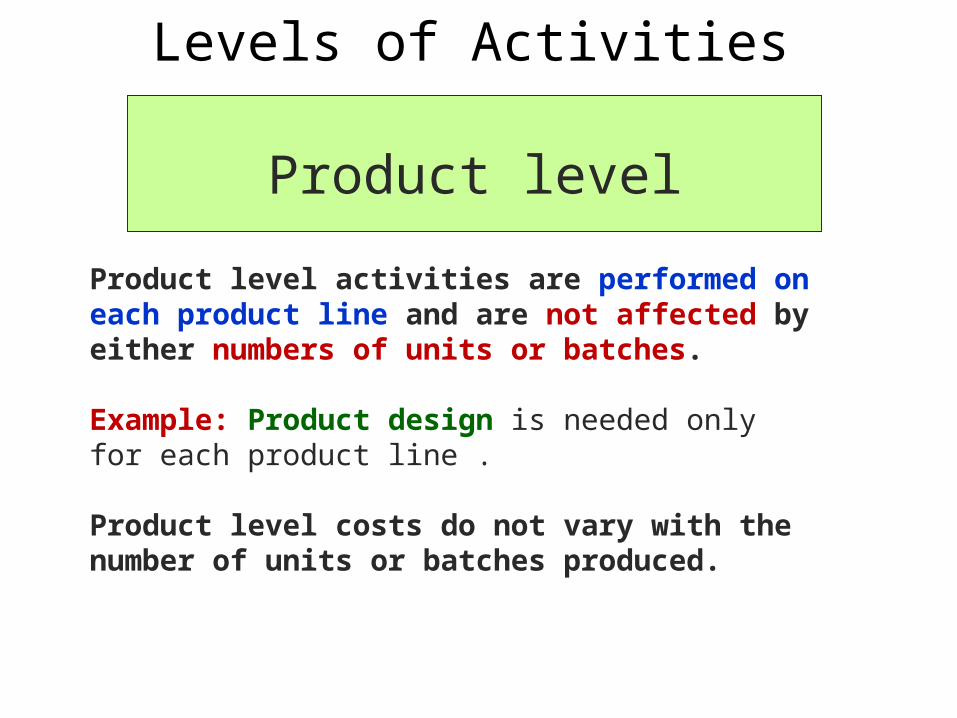

Product level activities are performed on each product line and are not affected by either numbers of units or batches.

Example: Product design is needed onlyfor each product line .

Product level costs do not vary with thenumber of units or batches produced.

Product level

Facility Level Activities

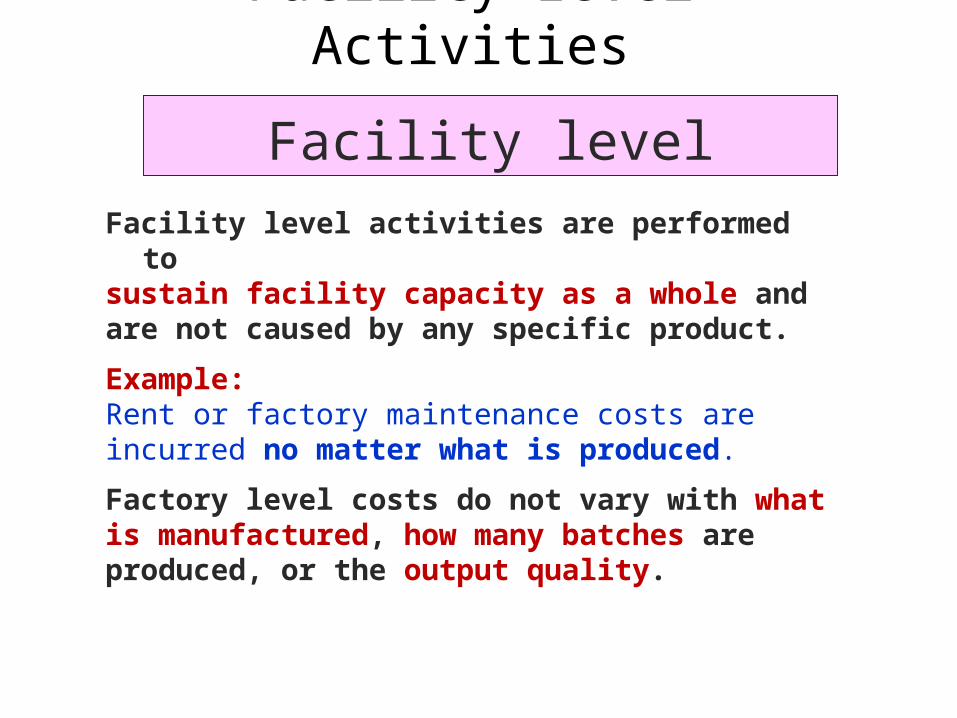

Facility level activities are performed to sustain facility capacity as a whole and are not caused by any specific product.

Example: Rent or factory maintenance costs are incurred no matter what is produced.

Factory level costs do not vary with what is manufactured, how many batches areproduced, or the output quality.

Facility level

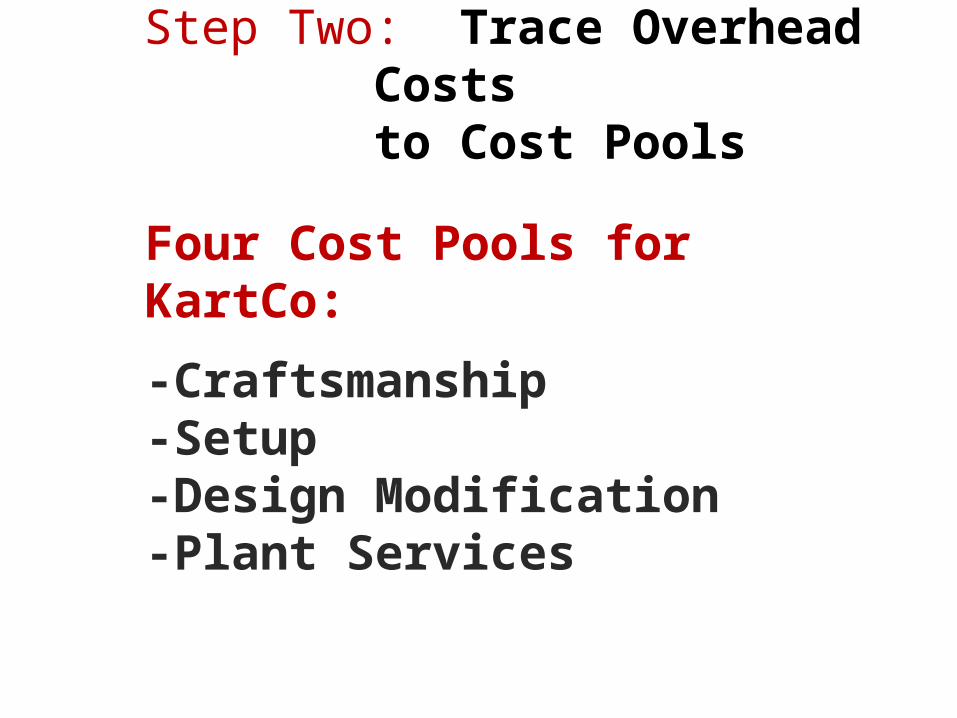

Step Two: Trace Overhead Costs to Cost Pools

Overhead Cost

Activity Cost

Pool X

Activity Cost

Pool Y

Activity Cost

Pool Z

Four Cost Pools for KartCo:

-Craftsmanship -Setup

-Design Modification-Plant Services

Step Two: Trace Overhead Costs

to Cost Pools

17-41

Step Two: Trace Overhead Costs to Cost Pools

ActivityIndirect

LaborFactory Utilities

Total Overhead

Replacing Tools $700,000 $700,000Machine Repair 1,300,000$ 1,300,000Factory Maintenance 800,000$ 800,000Engineer Salaries 1,200,000$ 1,200,000Assembly Line Power $600,000 600,000Heating and Lighting 200,000 200,000Totals $4,000,000 $800,000 $4,800,000

Exhibit 17.9 Kartco Overhead Cost Details

P3

17-42

Step Two: Assigning Overhead to Activity Cost Pools

Activity Pools Activity Cost Pooled Cost Activity DriverCraftsmanship 30,000 direct labor hours Assembly line power $600,000 $600,000Set-up 200 batches Replacing tools 700,000 Machine repair 1,300,000 2,000,000Design modification 10 designs Engineer salaries 1,200,000 1,200,000Plant services Factory maintenance 800,000 20,000 square feet Heating and lighting 200,000 1,000,000Total overhead cost $4,800,000

Exhibit 17.10 Assigning Overhead Costs to Activity Pools

P3

17-43

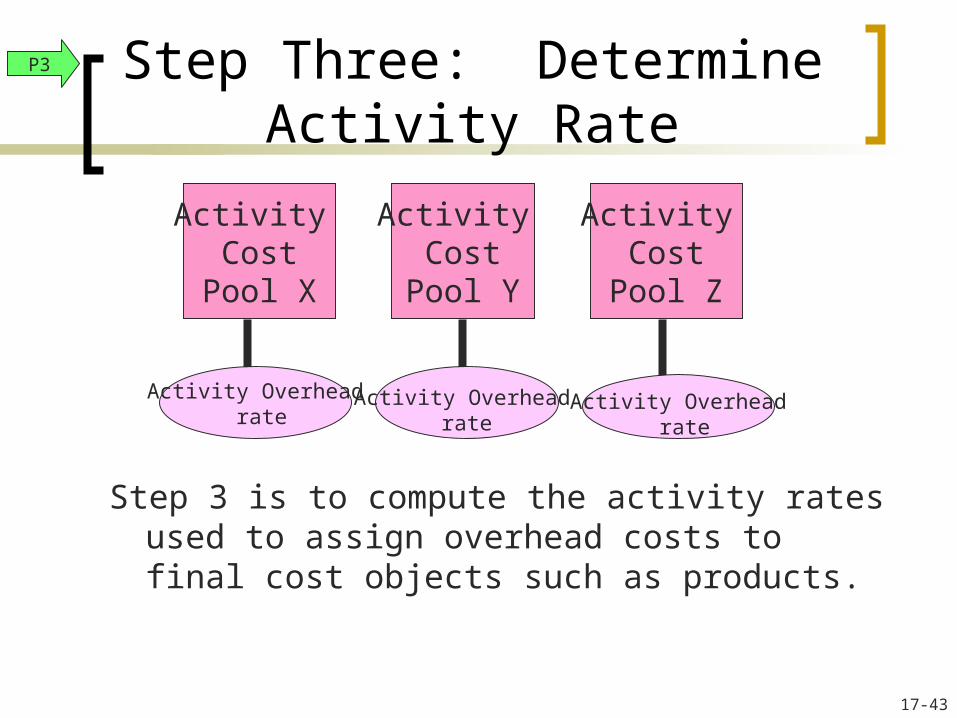

Step Three: Determine Activity Rate

Step 3 is to compute the activity rates used to assign overhead costs to final cost objects such as products.

P3

Activity Cost

Pool X

Activity Cost

Pool Y

Activity Cost

Pool Z

Activity Overhead rate

Activity Overhead

rateActivity Overhead

rate

17-44

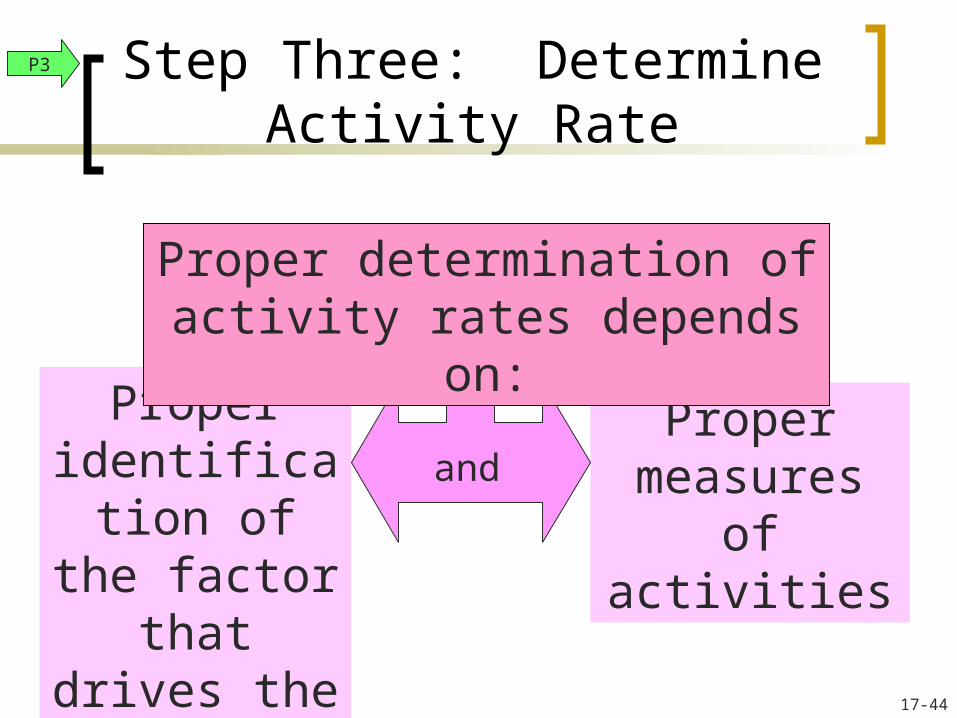

Step Three: Determine Activity Rate

P3

Proper identification of the factor that drives

the cost

Proper measures of

activities

Proper determination of activity rates depends on:

and

17-45

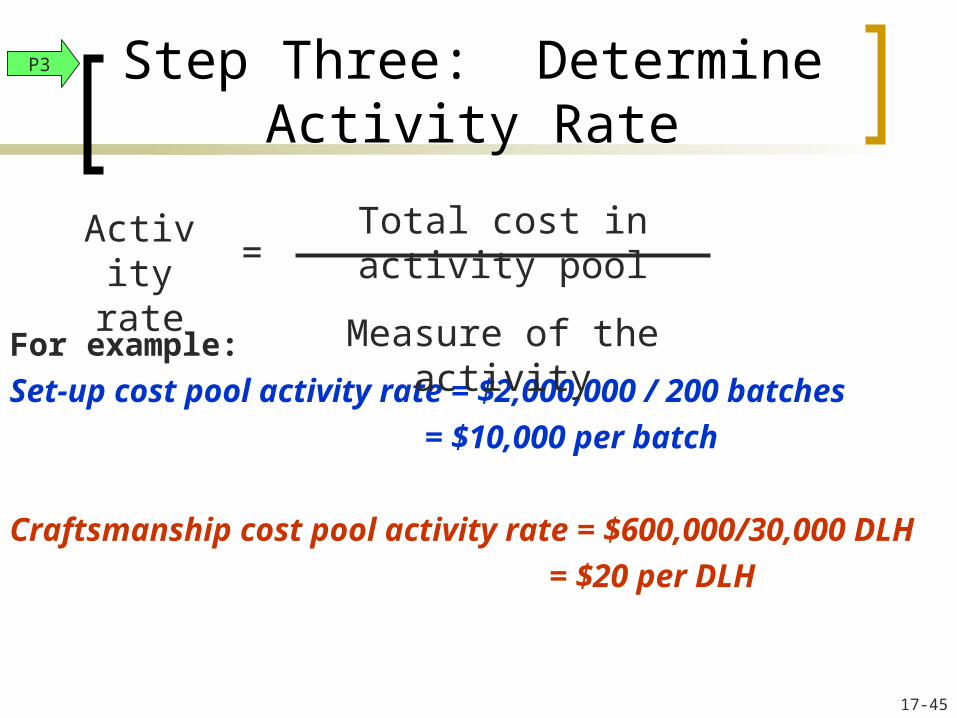

Step Three: Determine Activity Rate

For example:

Set-up cost pool activity rate = $2,000,000 / 200 batches

= $10,000 per batch

Craftsmanship cost pool activity rate = $600,000/30,000 DLH

= $20 per DLH

P3

Activity rate =

Total cost in activity pool

Measure of the activity

17-46

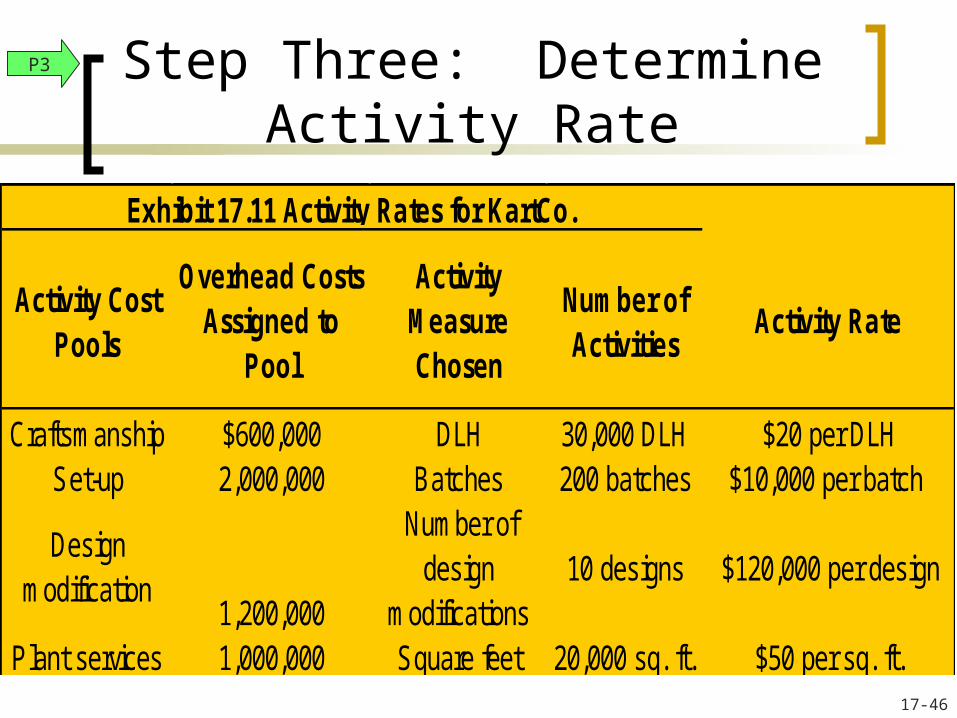

Step Three: Determine Activity Rate

Activity CostPools

Overhead CostsAssigned to

Pool

Activity MeasureChosen

Number of Activities

Activity Rate

Craftsmanship $600,000 DLH 30,000 DLH $20 per DLHSet-up 2,000,000 Batches 200 batches $10,000 per batch

Designmodification

1,200,000

Number of design

modifications10 designs $120,000 per design

Plant services 1,000,000 Square feet 20,000 sq. ft. $50 per sq. ft.

Exhibit 17.11 Activity Rates for KartCo.

P3

17-47

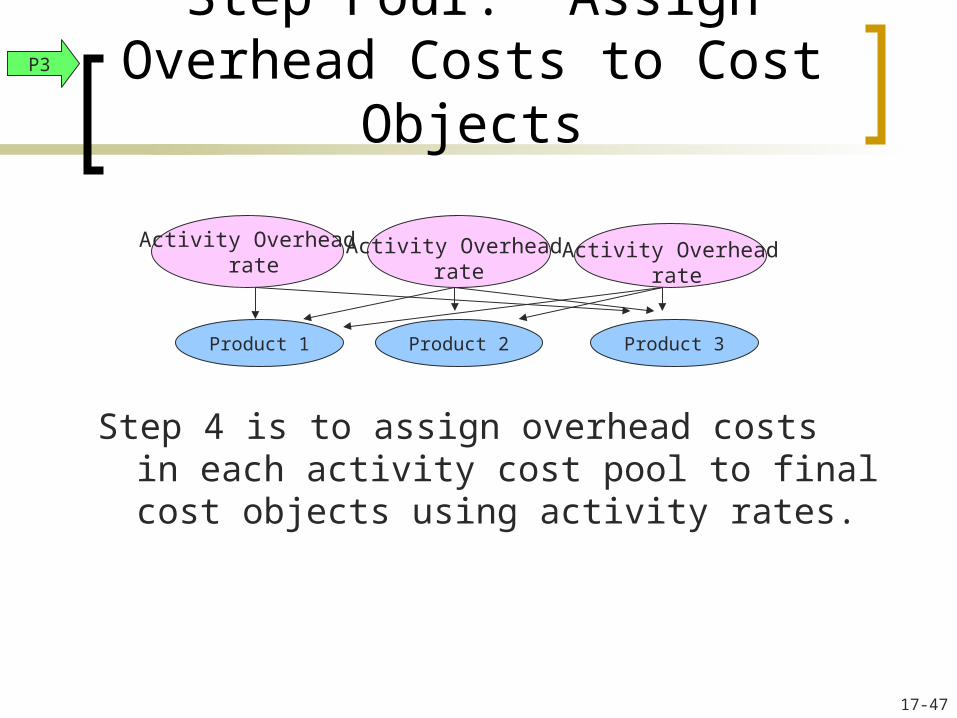

Step Four: Assign Overhead Costs to Cost Objects

Step 4 is to assign overhead costs in each activity cost pool to final cost objects using activity rates.

P3

Activity Overhead rate

Activity Overhead

rateActivity Overhead

rate

Product 1 Product 2 Product 3

17-48

Step Four: Assign Overhead Costs to Cost Objects

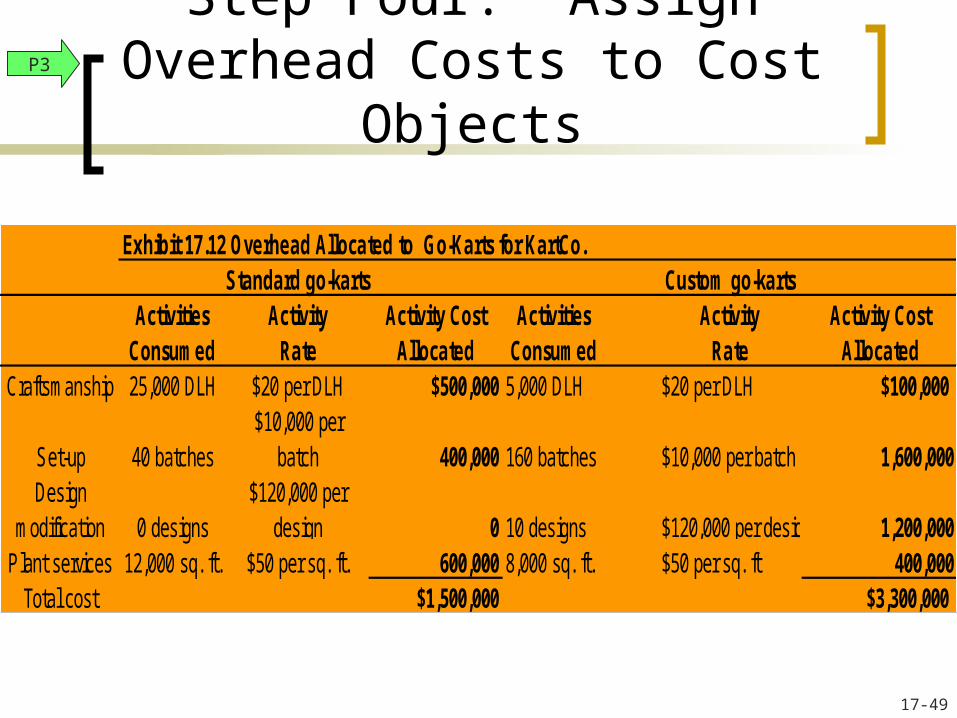

To illustrate, the overhead costs in the craftsmanship pool are allocated to standard go-karts as follows:

Overhead allocated to standard go-kart = Activities consumed X Activity rate =

25,000 DLH x $20 / DLH = $500,000

P3

17-49

Step Four: Assign Overhead Costs to Cost Objects

Standard go-karts Custom go-kartsActivities

ConsumedActivity

RateActivity Cost

AllocatedActivities

ConsumedActivity

RateActivity Cost

AllocatedCraftsmanship 25,000 DLH $20 per DLH $500,000 5,000 DLH $20 per DLH $100,000

Set-up 40 batches$10,000 per

batch 400,000 160 batches $10,000 per batch 1,600,000Design

modification 0 designs$120,000 per

design 0 10 designs $120,000 per design 1,200,000Plant services 12,000 sq. ft. $50 per sq. ft. 600,000 8,000 sq. ft. $50 per sq. ft 400,000

Total cost $1,500,000 $3,300,000

Exhibit 17.12 Overhead Allocated to Go-Karts for KartCo.

P3

17-50

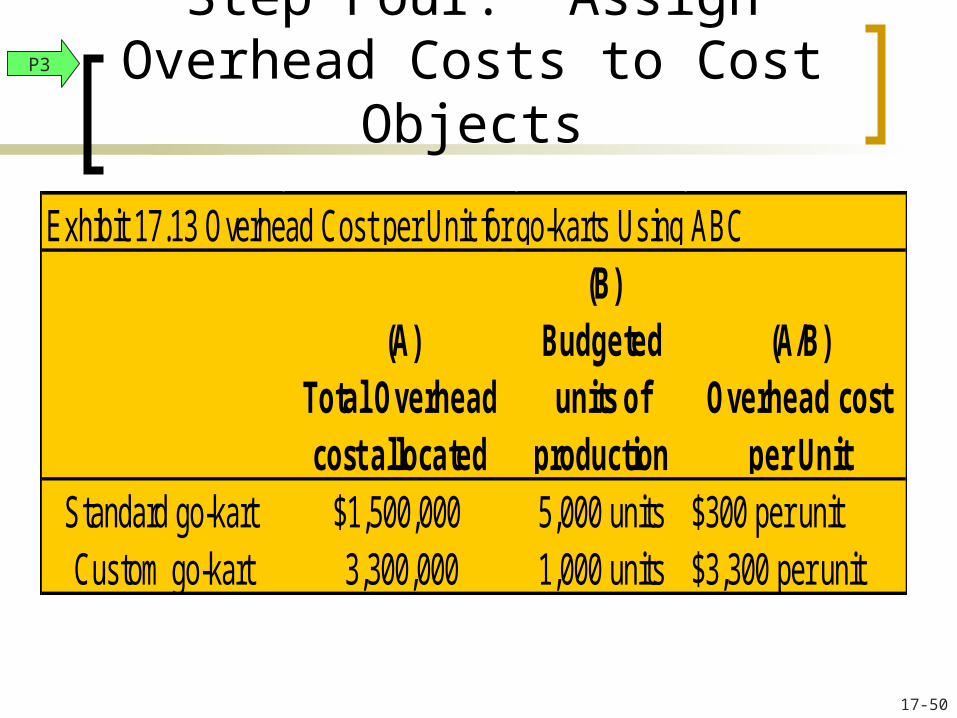

Step Four: Assign Overhead Costs to Cost Objects

(A)Total Overheadcost allocated

(B) Budgeted units of

production

(A/B)Overhead cost

per UnitStandard go-kart $1,500,000 5,000 units $300 per unitCustom go-kart 3,300,000 1,000 units $3,300 per unit

Exhibit 17.13 Overhead Cost per Unit for go-karts Using ABC

P3

17-51

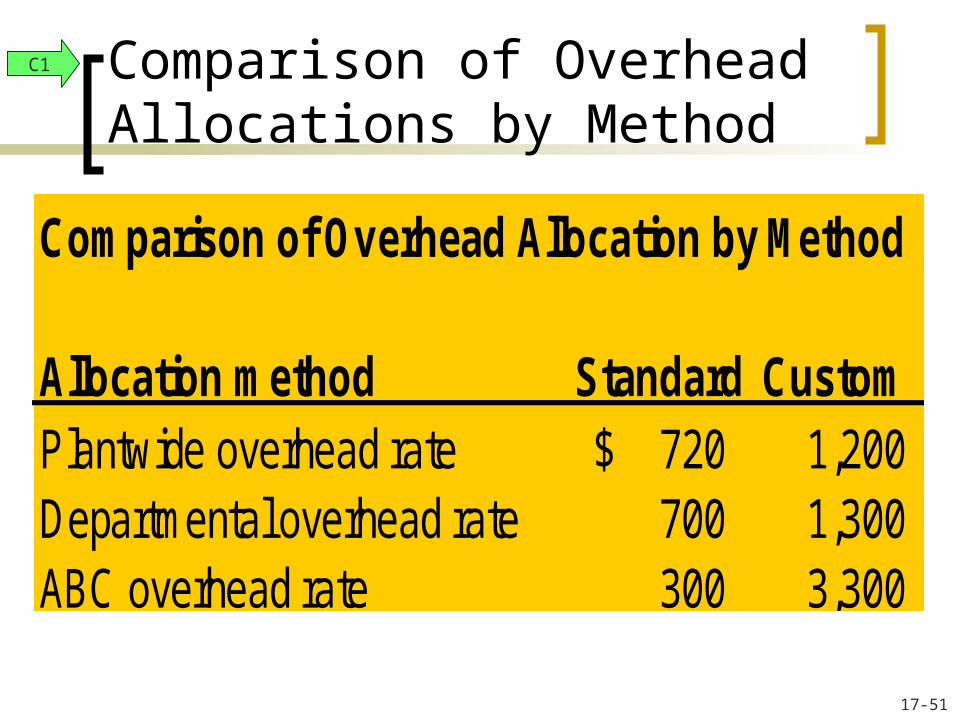

Comparison of Overhead Allocations by Method

C1

Comparison of Overhead Allocation by Method

Allocation method Standard CustomPlantwide overhead rate 720$ 1,200 Departmental overhead rate 700 1,300 ABC overhead rate 300 3,300

17-52

Advantages and Disadvantages of Activity-Based Costing

A3

Advantages:

•More accurate overhead cost allocation

•More effective overhead cost control

•Focus on relevant factors

•Better management of activities

Disadvantages:

•Costs to implement and maintain

•Uncertainty with decisions still remains

17-53

End of Chapter 17