Embed Size (px)

DESCRIPTION

Chapter 16. Notes Receivable and Notes Payable. LO1. Term. Payee. Principal. Interest Rate. Maker. Due Date. Learning Objective 1 Describe a promissory note. - PowerPoint PPT Presentation

Citation preview

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Chapter 16

NotesReceivable andNotes Payable

16-16-22

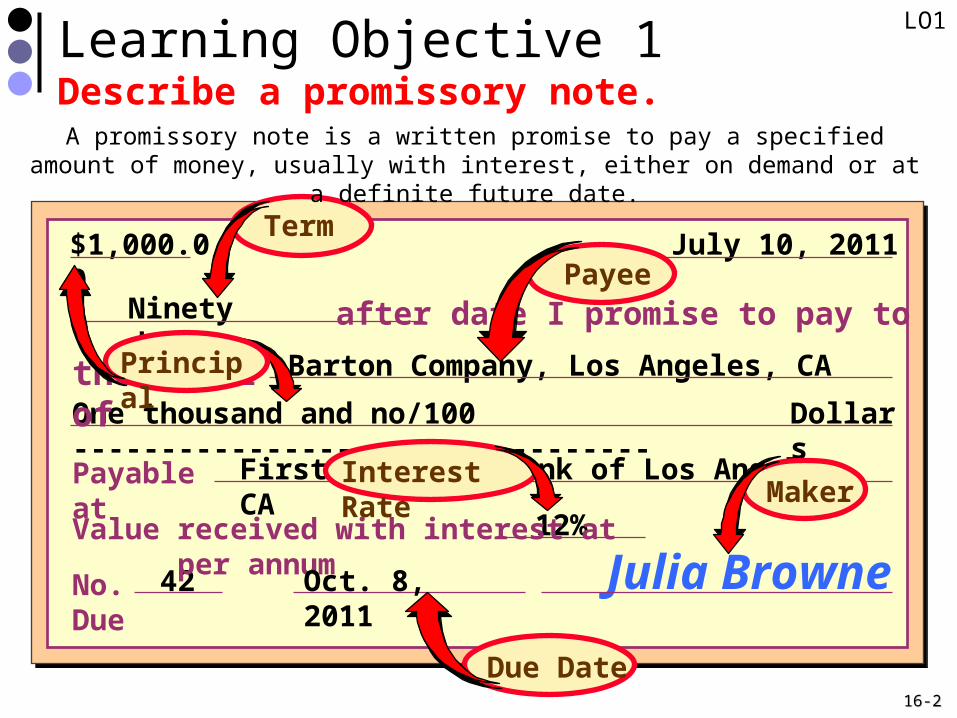

$1,000.00 July 10, 2011

Ninety days

Barton Company, Los Angeles, CA

One thousand and no/100 --------------------------------- Dollars

First National Bank of Los Angeles, CA

42

12%

Julia Browne

after date I promise to pay to

the order of

Payable atValue received with interest at per annumNo. Due Oct. 8, 2011

Term

Payee

Maker

Learning Objective 1Describe a promissory note.

Principal

Interest Rate

Due Date

A promissory note is a written promise to pay a specified amount of money, usually with interest, either on demand or at a definite future date.

LO1

16-16-33

Learning Objective 2Compute the maturity date and interest due on a promissory note.

Days in March 31 Minus the date of the note 1 Days remaining in March 30 Days in April 30 Days in May to maturity 30 Period of the note in days 90

The note is due and payable on May 30, 2010.The note is due and payable on May 30, 2010.The note is due and payable on May 30, 2010.The note is due and payable on May 30, 2010.

How much interest will Matrix pay to Office Supplies, Inc. on this note?How much interest will Matrix pay to Office Supplies, Inc. on this note?

On March 1, 2010, Matrix, Inc.On March 1, 2010, Matrix, Inc.purchases a copier for $12,000 from Office Supplies, Inc. Matrix gave purchases a copier for $12,000 from Office Supplies, Inc. Matrix gave Office Supplies a 9% note due in 90 days in payment for the copier. Office Supplies a 9% note due in 90 days in payment for the copier.

What is the maturity date of the note?What is the maturity date of the note?

On March 1, 2010, Matrix, Inc.On March 1, 2010, Matrix, Inc.purchases a copier for $12,000 from Office Supplies, Inc. Matrix gave purchases a copier for $12,000 from Office Supplies, Inc. Matrix gave Office Supplies a 9% note due in 90 days in payment for the copier. Office Supplies a 9% note due in 90 days in payment for the copier.

What is the maturity date of the note?What is the maturity date of the note?

In this example, we add 30 days in

March, 30 days in April, and 30 days in May to add up to the note term of 90 days.

LO2

16-16-44

Learning Objective 3Record the receipt of a note receivable.

Here are the entry on March 1, 2006, to record Here are the entry on March 1, 2006, to record the sale and note receivable. the sale and note receivable.

Here are the entry on March 1, 2006, to record Here are the entry on March 1, 2006, to record the sale and note receivable. the sale and note receivable.

DR CRMar. 1 Notes Receivable 12,000

Sales 12,000 Sold goods in exchange for note

DR CRMay 30 Cash 12,270

Interest Revenue 270 Notes Receivable 12,000

Collected note and interest due

On May 30, 2010, Office Supplies, Inc. receives On May 30, 2010, Office Supplies, Inc. receives the principal amount of the note plus interest. the principal amount of the note plus interest.

On May 30, 2010, Office Supplies, Inc. receives On May 30, 2010, Office Supplies, Inc. receives the principal amount of the note plus interest. the principal amount of the note plus interest.

LO3

16-16-55

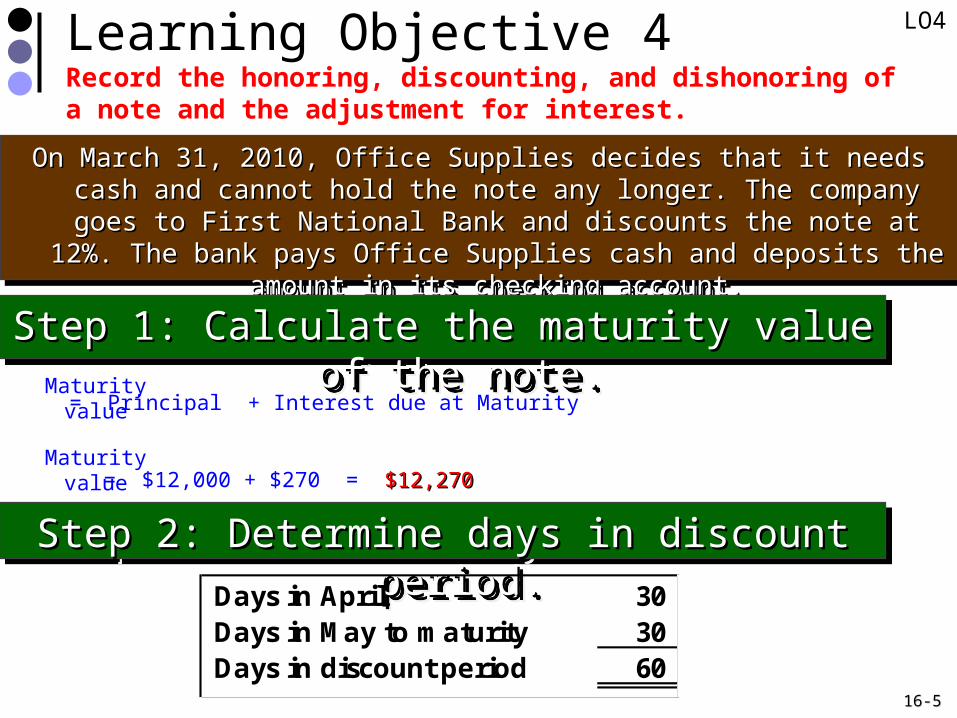

Learning Objective 4Record the honoring, discounting, and dishonoring of a note and the adjustment for interest.

On March 31, 2010, Office Supplies decides that it needs cash and cannot hold On March 31, 2010, Office Supplies decides that it needs cash and cannot hold the note any longer. The company goes to First National Bank and the note any longer. The company goes to First National Bank and

discounts the note at 12%. The bank pays Office Supplies cash and discounts the note at 12%. The bank pays Office Supplies cash and deposits the amount in its checking account.deposits the amount in its checking account.

On March 31, 2010, Office Supplies decides that it needs cash and cannot hold On March 31, 2010, Office Supplies decides that it needs cash and cannot hold the note any longer. The company goes to First National Bank and the note any longer. The company goes to First National Bank and

discounts the note at 12%. The bank pays Office Supplies cash and discounts the note at 12%. The bank pays Office Supplies cash and deposits the amount in its checking account.deposits the amount in its checking account.

Step 1: Calculate the maturity value of the note.Step 1: Calculate the maturity value of the note.Step 1: Calculate the maturity value of the note.Step 1: Calculate the maturity value of the note.Maturity

value = Principal + Interest due at Maturity

Maturityvalue = $12,000 + $270 = $12,270$12,270

Step 2: Determine days in discount period.Step 2: Determine days in discount period.Step 2: Determine days in discount period.Step 2: Determine days in discount period.Days in April 30 Days in May to maturity 30 Days in discount period 60

LO4

16-16-66

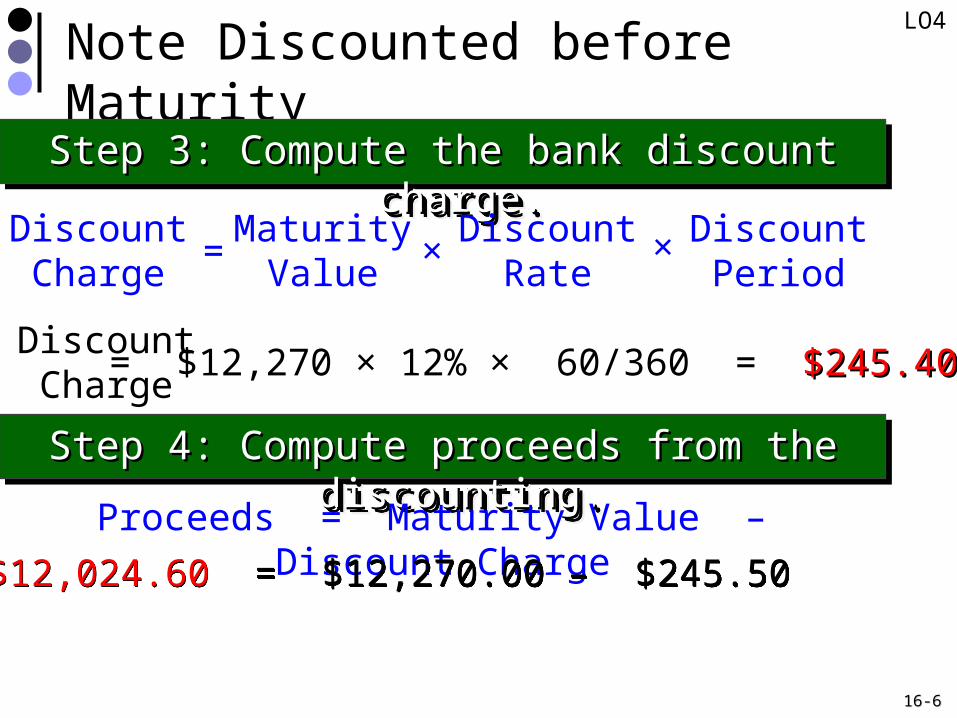

Note Discounted before Maturity

Step 3: Compute the bank discount charge.Step 3: Compute the bank discount charge.Step 3: Compute the bank discount charge.Step 3: Compute the bank discount charge.

DiscountCharge

=MaturityValue

DiscountRate

DiscountPeriod

×

×

DiscountCharge

= $12,270 × 12% × 60/360 = $245.40$245.40

Step 4: Compute proceeds from the discounting.Step 4: Compute proceeds from the discounting.Step 4: Compute proceeds from the discounting.Step 4: Compute proceeds from the discounting.

Proceeds = Maturity Value – Discount Charge

$12,024.60 = $12,270.00 – $245.50 $12,024.60 = $12,270.00 – $245.50

LO4

16-16-77

Note Discounted before Maturity

Cash 12,024.60 Interest revenue 24.60 Notes Receivable 12,000.00

To record discounting of note receivable

Let’s look at the journal entry to record the discounting of the note receivable.

Now let’s assume that Office Supplies held the note to maturity. At maturity, Matrix informs Office Supplies that it is unable to pay the note or interest. The note has

matured and is no longer valid.

Accounts Receivable - Matrix 12,270 Interest revenue 270 Notes Receivable 12,000

To charge accounts receivable for dishonored

note

LO4

16-16-88

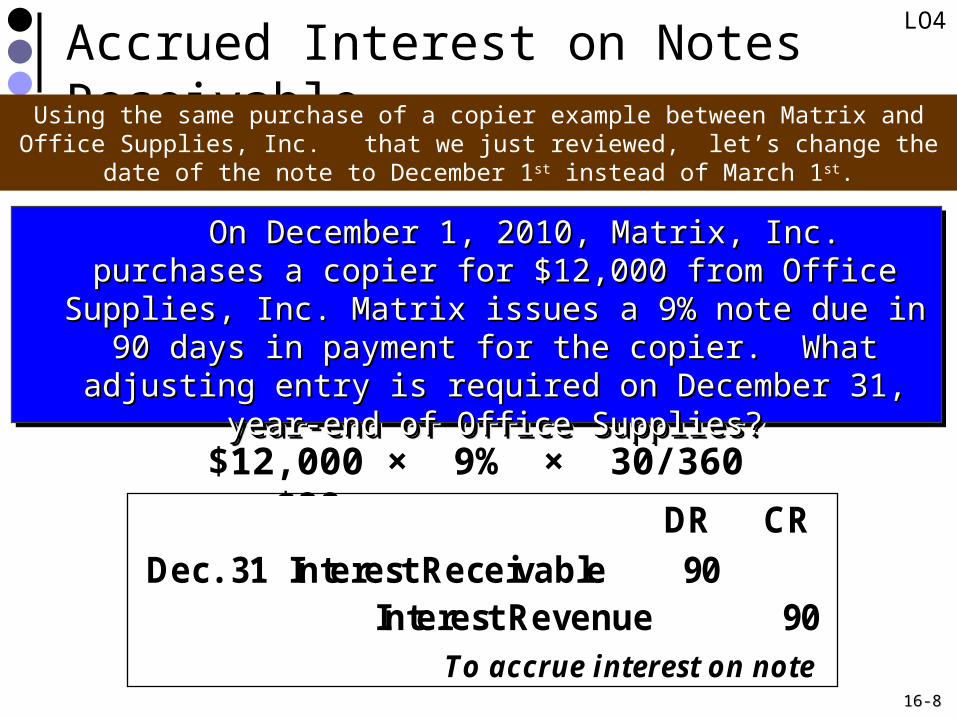

Accrued Interest on Notes Receivable

On December 1, 2010, Matrix, Inc. purchases a copier for On December 1, 2010, Matrix, Inc. purchases a copier for $12,000 from Office Supplies, Inc. Matrix issues a 9% note $12,000 from Office Supplies, Inc. Matrix issues a 9% note due in 90 days in payment for the copier. What adjusting due in 90 days in payment for the copier. What adjusting

entry is required on December 31, year-end of Office entry is required on December 31, year-end of Office Supplies?Supplies?

On December 1, 2010, Matrix, Inc. purchases a copier for On December 1, 2010, Matrix, Inc. purchases a copier for $12,000 from Office Supplies, Inc. Matrix issues a 9% note $12,000 from Office Supplies, Inc. Matrix issues a 9% note due in 90 days in payment for the copier. What adjusting due in 90 days in payment for the copier. What adjusting

entry is required on December 31, year-end of Office entry is required on December 31, year-end of Office Supplies?Supplies?

$12,000 × 9% × 30/360 = $90

DR CRDec. 31 Interest Receivable 90

Interest Revenue 90 To accrue interest on note

Using the same purchase of a copier example between Matrix and Office Supplies, Inc. that we just reviewed, let’s change the date of the note to December 1st instead of

March 1st.

LO4

16-16-99

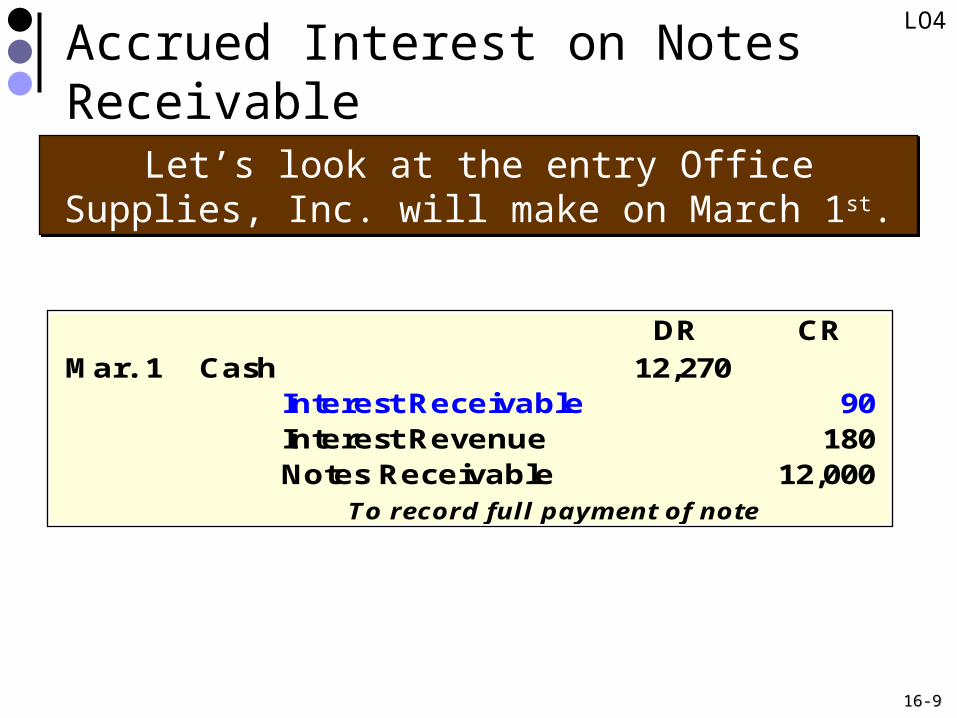

Accrued Interest on Notes Receivable

DR CRMar. 1 Cash 12,270

Interest Receivable 90 Interest Revenue 180 Notes Receivable 12,000

To record full payment of note

Let’s look at the entry Office Supplies, Inc. will make on March 1st.

Let’s look at the entry Office Supplies, Inc. will make on March 1st.

LO4

16-16-1010

On March 15, 2010, Western, Inc. issues a $10,000, 12%, 90-day note to On March 15, 2010, Western, Inc. issues a $10,000, 12%, 90-day note to First Bank for cash. Let’s make the journal entry. First Bank for cash. Let’s make the journal entry.

Learning Objective 5Prepare entries to account for notes payable.

Let’s calculate interest to maturity.

$10,000 $10,000 × 12% × 12% × 90/360 = $300× 90/360 = $300$10,000 $10,000 × 12% × 12% × 90/360 = $300× 90/360 = $300

LO5

16-16-1111

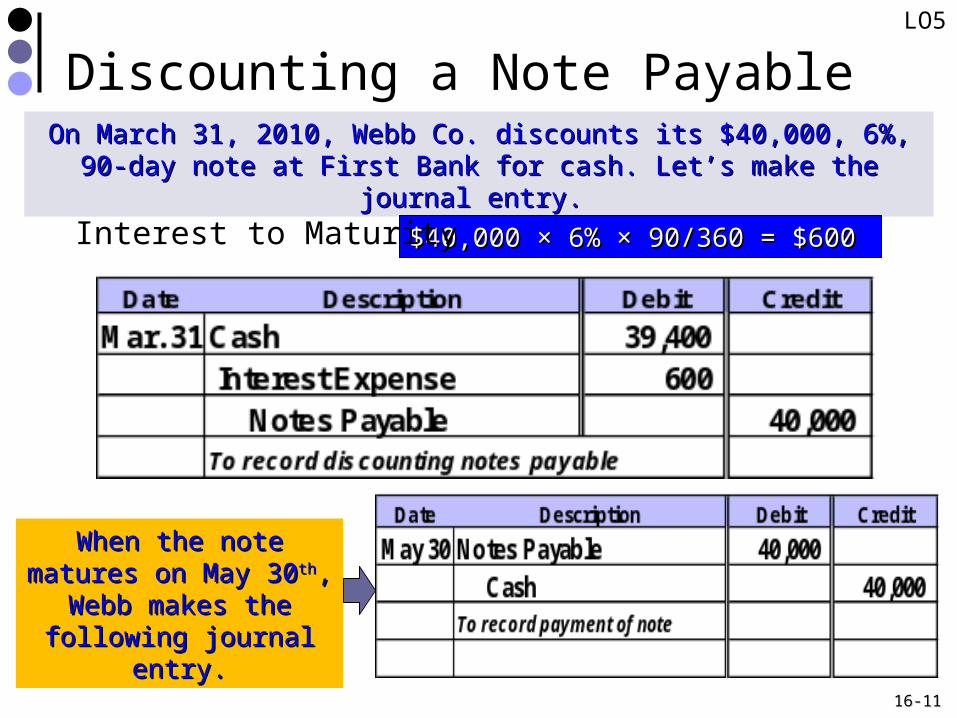

Discounting a Note PayableOn March 31, 2010, Webb Co. discounts its $40,000, 6%, 90-day note at On March 31, 2010, Webb Co. discounts its $40,000, 6%, 90-day note at

First Bank for cash. Let’s make the journal entry. First Bank for cash. Let’s make the journal entry.

$40,000 $40,000 × 6% × 6% × 90/360 = $600× 90/360 = $600 Interest to Maturity

When the note matures When the note matures on May 30on May 30thth, Webb makes , Webb makes

the following journal the following journal entry.entry.

LO5

16-16-1212

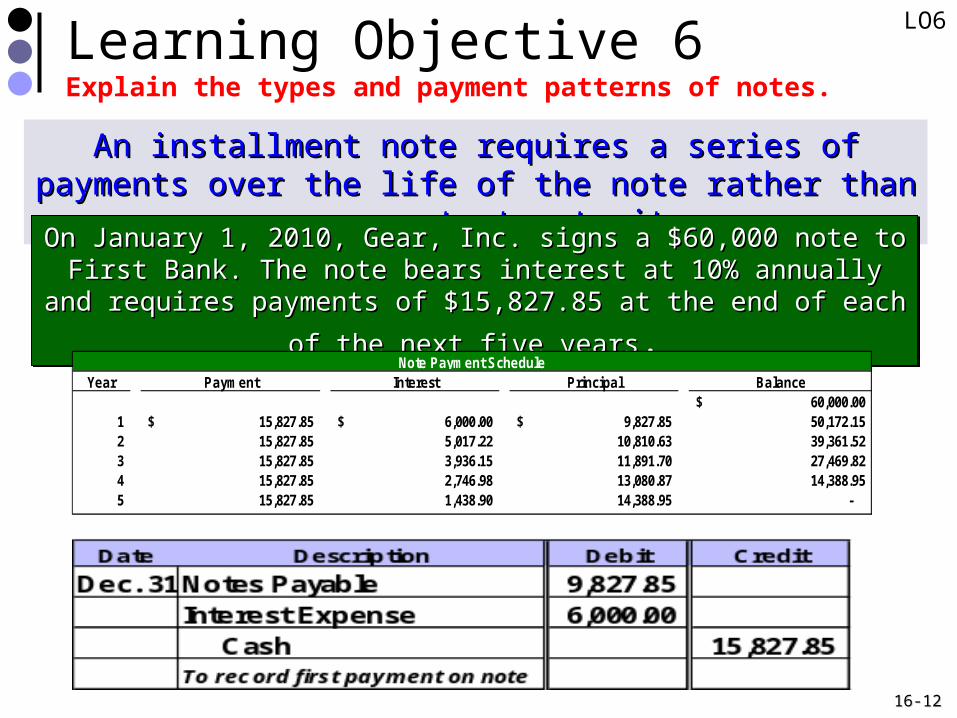

Learning Objective 6Explain the types and payment patterns of notes.

An installment note requires a series of payments over the life An installment note requires a series of payments over the life of the note rather than one payment at maturity.of the note rather than one payment at maturity.

On January 1, 2010, Gear, Inc. signs a $60,000 note to First Bank. The On January 1, 2010, Gear, Inc. signs a $60,000 note to First Bank. The note bears interest at 10% annually and requires payments of $15,827.85 note bears interest at 10% annually and requires payments of $15,827.85

at the end of each of the next five yearsat the end of each of the next five years..

On January 1, 2010, Gear, Inc. signs a $60,000 note to First Bank. The On January 1, 2010, Gear, Inc. signs a $60,000 note to First Bank. The note bears interest at 10% annually and requires payments of $15,827.85 note bears interest at 10% annually and requires payments of $15,827.85

at the end of each of the next five yearsat the end of each of the next five years..

Year Payment Interest Principal Balance60,000.00$

1 15,827.85$ 6,000.00$ 9,827.85$ 50,172.15 2 15,827.85 5,017.22 10,810.63 39,361.52 3 15,827.85 3,936.15 11,891.70 27,469.82 4 15,827.85 2,746.98 13,080.87 14,388.95 5 15,827.85 1,438.90 14,388.95 -

Note Payment Schedule

LO6

16-16-1313

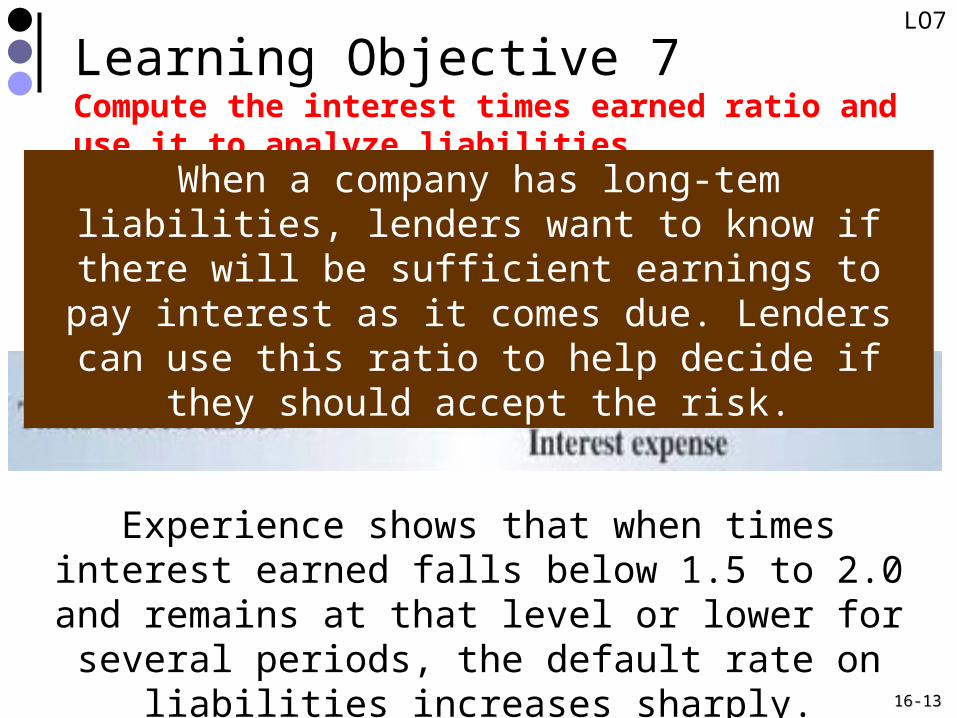

Learning Objective 7Compute the interest times earned ratio and use it to analyze liabilities.

Experience shows that when times interest earned falls below 1.5 to 2.0 and remains at that level or

lower for several periods, the default rate on liabilities increases sharply.

When a company has long-tem liabilities, lenders want to know if there will be sufficient earnings to pay interest as it comes due. Lenders can use this ratio to

help decide if they should accept the risk.

LO7

16-16-1414

End of Chapter 16