Embed Size (px)

Citation preview

IE 5441 1

Chapter 12. Forwards, Futures, and Swaps

Shuzhong Zhang

IE 5441 2

Pricing Principles

Suppose that your uncle promises that he will give you an ounce of

gold 1 year from now, which is worth $1,000 today. How should you

evaluate this promised gift?

Pricing principles:

• Use the market. The gold market may be fluctuating, but one

can purchase the gold and give it to you next year. So using the

market, its value today is $1,000.

• Discounting certain cash at the current rate of interest.

Suppose your uncle promises to give you $1,000 next year, and the

interest rate is 10%. Then, the value of the cash is $909.

• If asset A has value VA, and B has value VB, then the value of a

units of A and b units of B is aVA + bVB .

Shuzhong Zhang

IE 5441 3

Forward Contracts

• A forward contract on a commodity is a contract to purchase or

sell a specific amount of the commodity at a specific price and at a

specific time in the future.

• Long position: buyer.

• Short position: seller.

• Spot market.

• Forward market.

Shuzhong Zhang

IE 5441 4

Forward interest rate

Example 12.1. Suppose that you wish to arrange to loan money for 6

months beginning 3 months from now. Suppose that the forward rate

for that period is 10%. A suitable contract that implements this loan

would be an agreement for a bank to deliver to you, 3 months from

now, a 6-month Treasury bill. The price would be agreed upon today

for this delivery, and the Treasury bill would pay its face value of, say

$1000, at maturity. The value of the T-bill would be

$1000/1.05=$952.38. This is the price you would agree to pay in 3

months when the T-bill is delivered to you. Six months later you

receive the $1000 face value.

Shuzhong Zhang

IE 5441 5

Forward prices

• Forward price F .

• Current value of a forward contract.

• Delivery time T .

• Spot market price S.

Forward price formula. Suppose an asset can be stored at no cost and

also sold short. The theoretical forward price is

F = S/d(0, T ).

Shuzhong Zhang

IE 5441 6

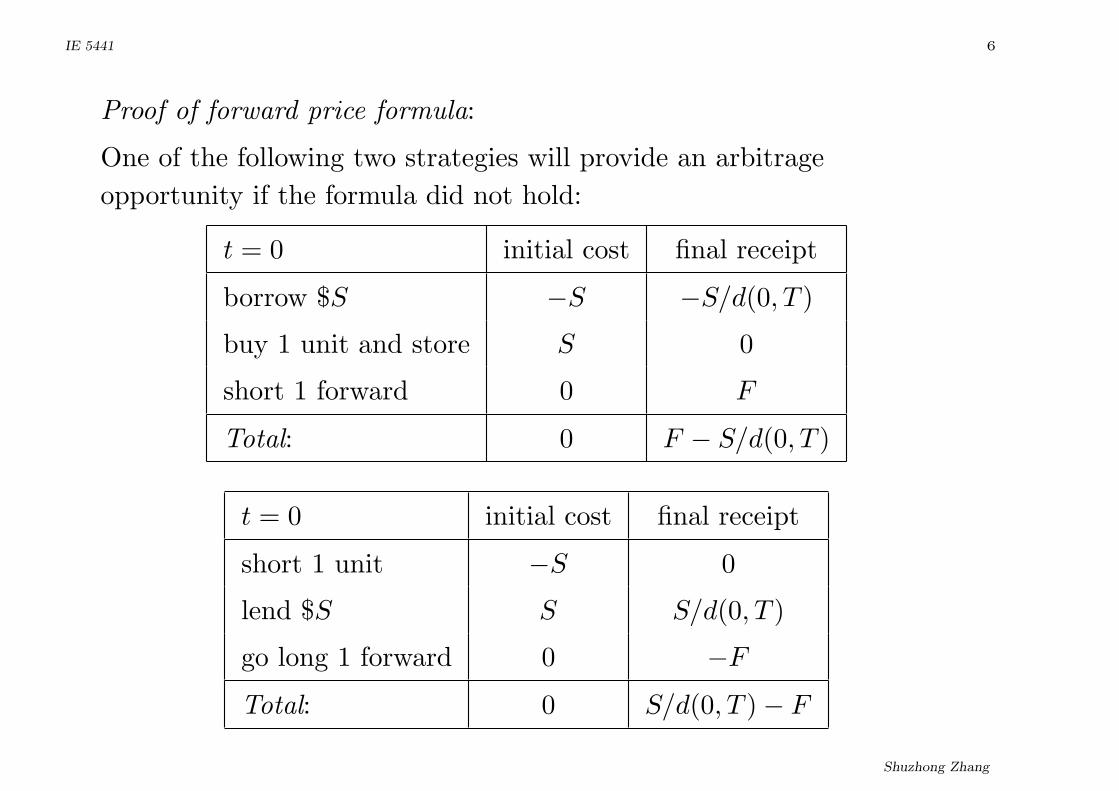

Proof of forward price formula:

One of the following two strategies will provide an arbitrage

opportunity if the formula did not hold:

t = 0 initial cost final receipt

borrow $S −S −S/d(0, T )

buy 1 unit and store S 0

short 1 forward 0 F

Total: 0 F − S/d(0, T )

t = 0 initial cost final receipt

short 1 unit −S 0

lend $S S S/d(0, T )

go long 1 forward 0 −F

Total: 0 S/d(0, T )− F

Shuzhong Zhang

IE 5441 7

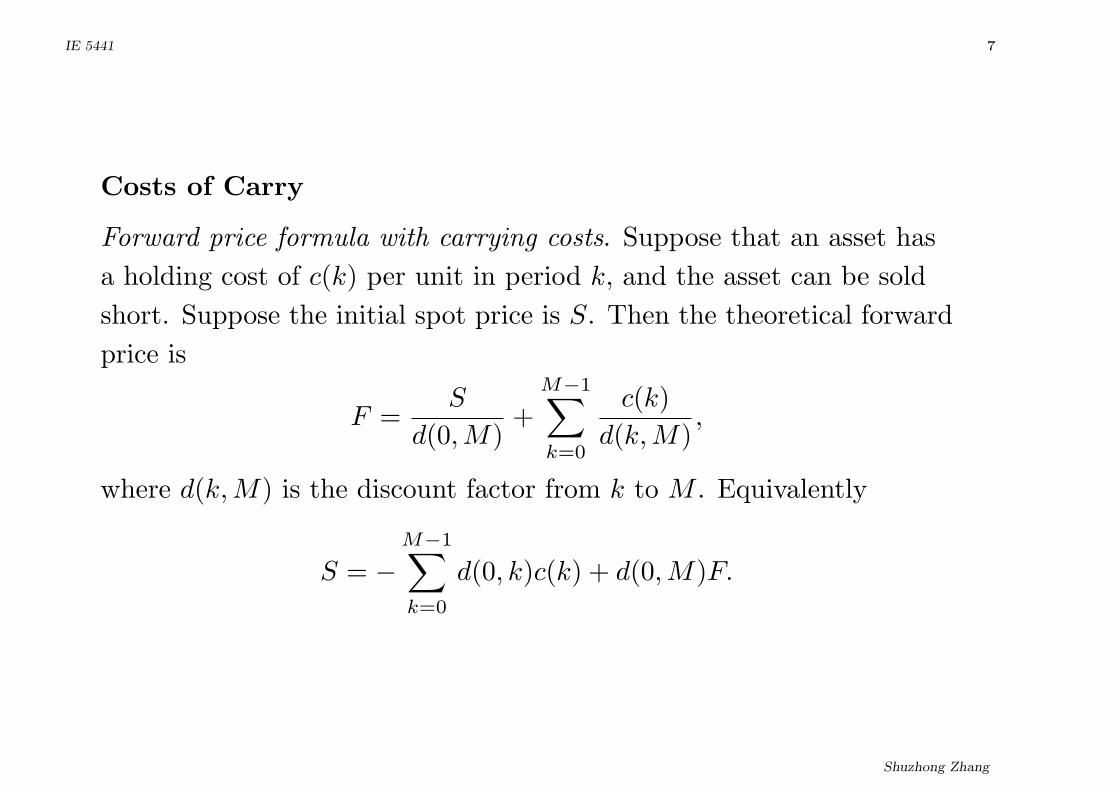

Costs of Carry

Forward price formula with carrying costs. Suppose that an asset has

a holding cost of c(k) per unit in period k, and the asset can be sold

short. Suppose the initial spot price is S. Then the theoretical forward

price is

F =S

d(0,M)+

M−1∑k=0

c(k)

d(k,M),

where d(k,M) is the discount factor from k to M . Equivalently

S = −M−1∑k=0

d(0, k)c(k) + d(0,M)F.

Shuzhong Zhang

IE 5441 8

t = 0 time 0 cost time k cost receipt at time M

short 1 unit 0 0 F

borrow $S −S 0 −S/d(0,M)

buy 1 unit spot S 0 0

borrow c(k)’s forward −c(0) −c(k) −∑M−1

k=0c(k)

d(k,M)

pay storage c(0) c(k) 0

Total: 0 0 F − Sd(0,M) −

∑M−1k=0

c(k)d(k,M)

Shuzhong Zhang

IE 5441 9

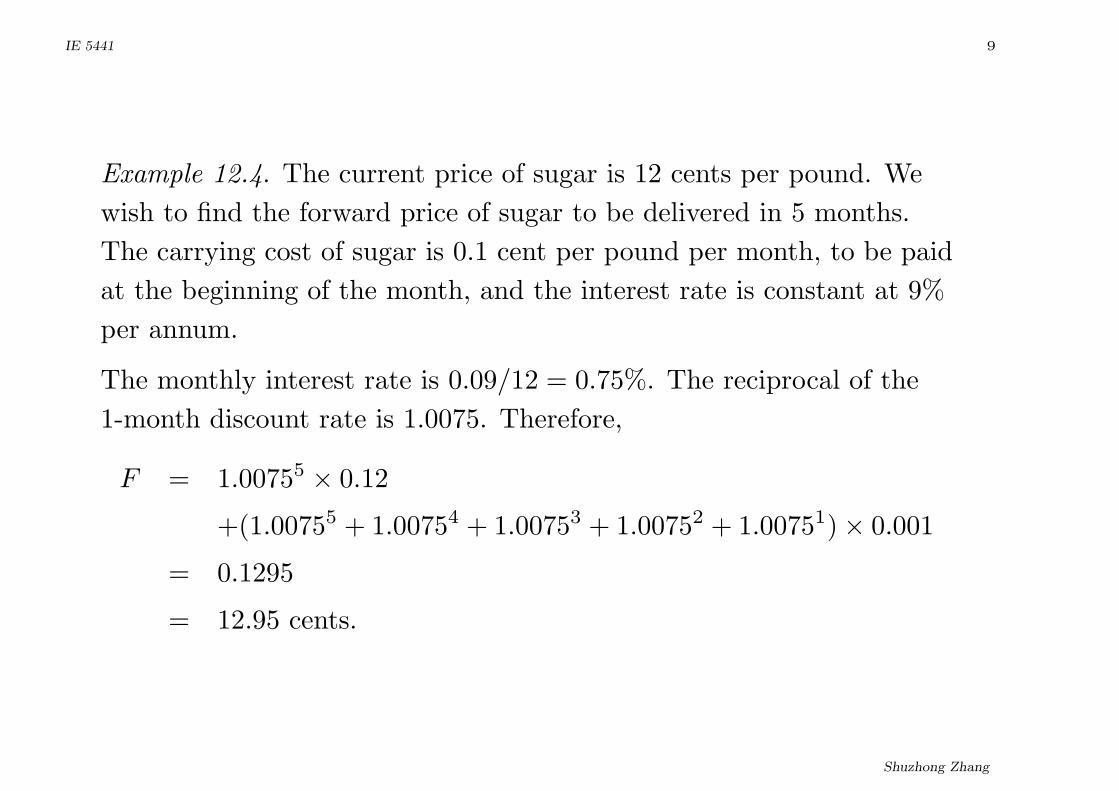

Example 12.4. The current price of sugar is 12 cents per pound. We

wish to find the forward price of sugar to be delivered in 5 months.

The carrying cost of sugar is 0.1 cent per pound per month, to be paid

at the beginning of the month, and the interest rate is constant at 9%

per annum.

The monthly interest rate is 0.09/12 = 0.75%. The reciprocal of the

1-month discount rate is 1.0075. Therefore,

F = 1.00755 × 0.12

+(1.00755 + 1.00754 + 1.00753 + 1.00752 + 1.00751)× 0.001

= 0.1295

= 12.95 cents.

Shuzhong Zhang

IE 5441 10

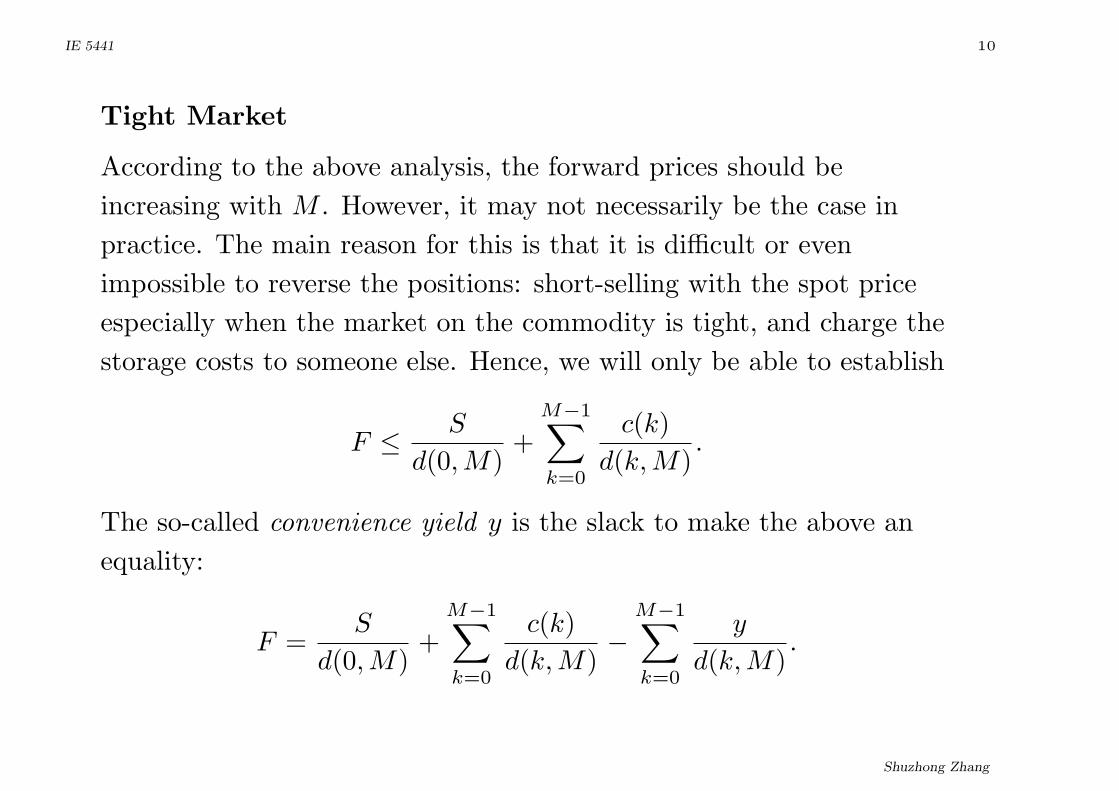

Tight Market

According to the above analysis, the forward prices should be

increasing with M . However, it may not necessarily be the case in

practice. The main reason for this is that it is difficult or even

impossible to reverse the positions: short-selling with the spot price

especially when the market on the commodity is tight, and charge the

storage costs to someone else. Hence, we will only be able to establish

F ≤ S

d(0,M)+

M−1∑k=0

c(k)

d(k,M).

The so-called convenience yield y is the slack to make the above an

equality:

F =S

d(0,M)+

M−1∑k=0

c(k)

d(k,M)−

M−1∑k=0

y

d(k,M).

Shuzhong Zhang

IE 5441 11

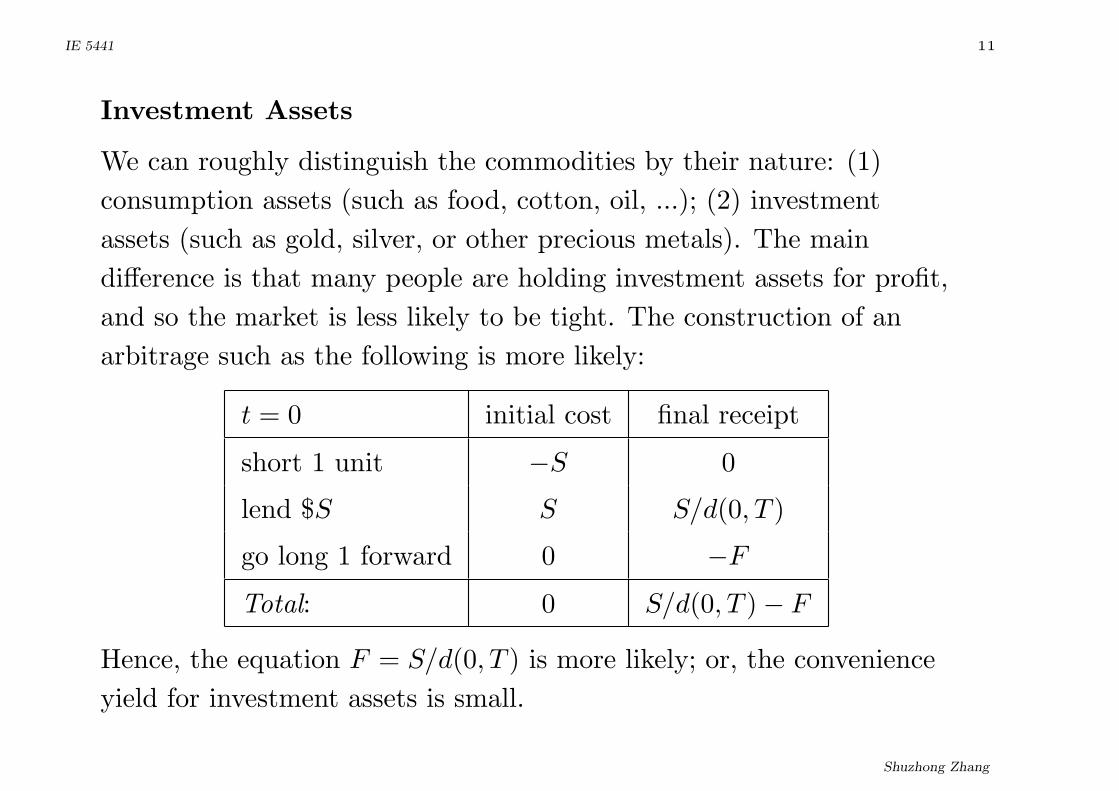

Investment Assets

We can roughly distinguish the commodities by their nature: (1)

consumption assets (such as food, cotton, oil, ...); (2) investment

assets (such as gold, silver, or other precious metals). The main

difference is that many people are holding investment assets for profit,

and so the market is less likely to be tight. The construction of an

arbitrage such as the following is more likely:

t = 0 initial cost final receipt

short 1 unit −S 0

lend $S S S/d(0, T )

go long 1 forward 0 −F

Total: 0 S/d(0, T )− F

Hence, the equation F = S/d(0, T ) is more likely; or, the convenience

yield for investment assets is small.

Shuzhong Zhang

IE 5441 12

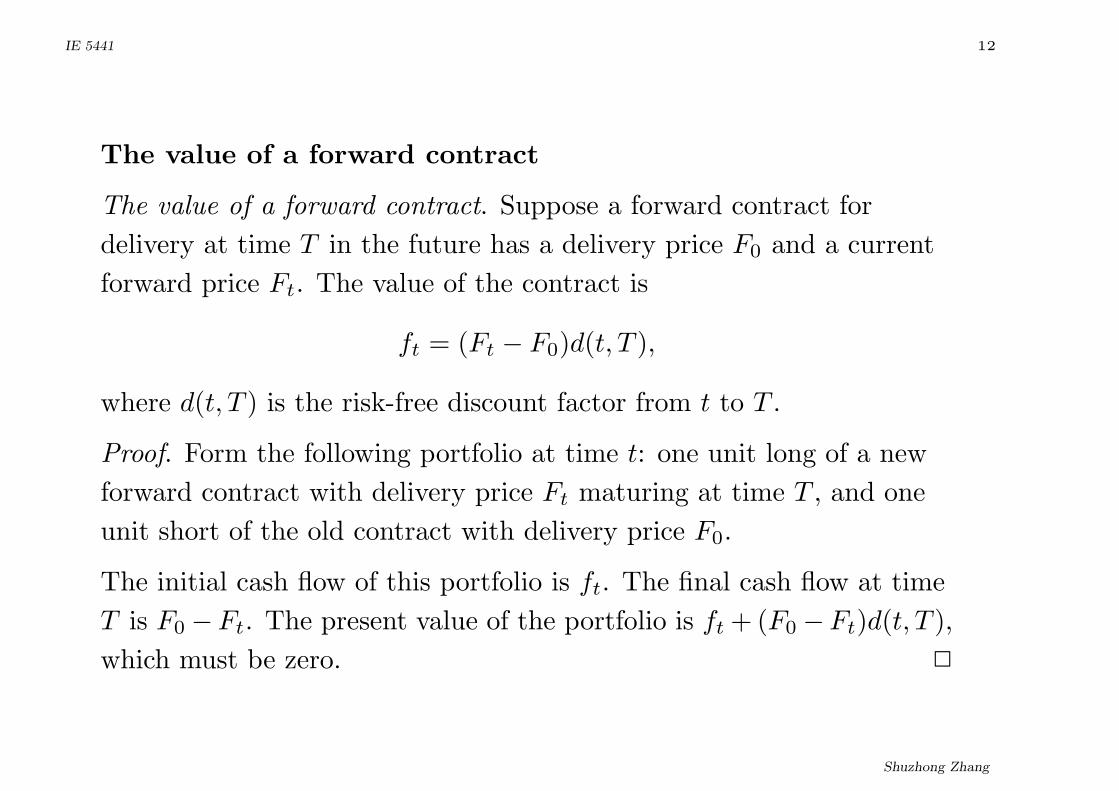

The value of a forward contract

The value of a forward contract. Suppose a forward contract for

delivery at time T in the future has a delivery price F0 and a current

forward price Ft. The value of the contract is

ft = (Ft − F0)d(t, T ),

where d(t, T ) is the risk-free discount factor from t to T .

Proof. Form the following portfolio at time t: one unit long of a new

forward contract with delivery price Ft maturing at time T , and one

unit short of the old contract with delivery price F0.

The initial cash flow of this portfolio is ft. The final cash flow at time

T is F0 −Ft. The present value of the portfolio is ft + (F0 −Ft)d(t, T ),

which must be zero. 2

Shuzhong Zhang

IE 5441 13

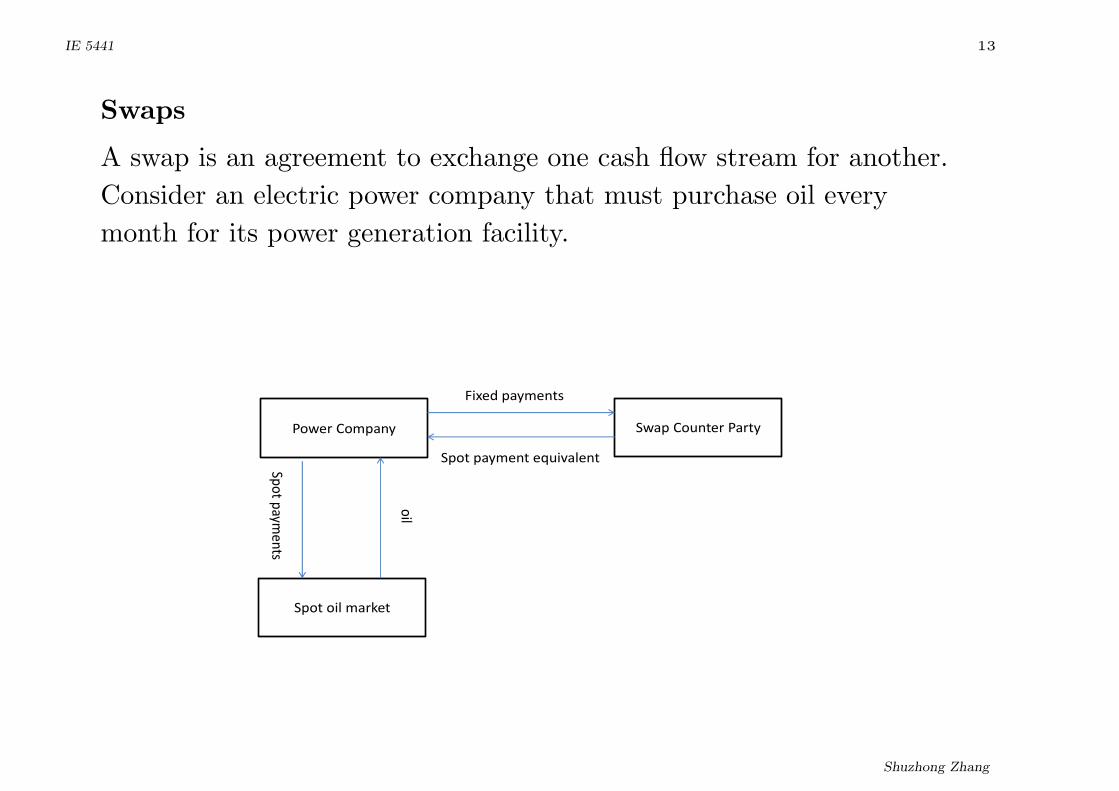

Swaps

A swap is an agreement to exchange one cash flow stream for another.

Consider an electric power company that must purchase oil every

month for its power generation facility.

�����������

������������

��������������

������������

������������������

���

������

����

Shuzhong Zhang

IE 5441 14

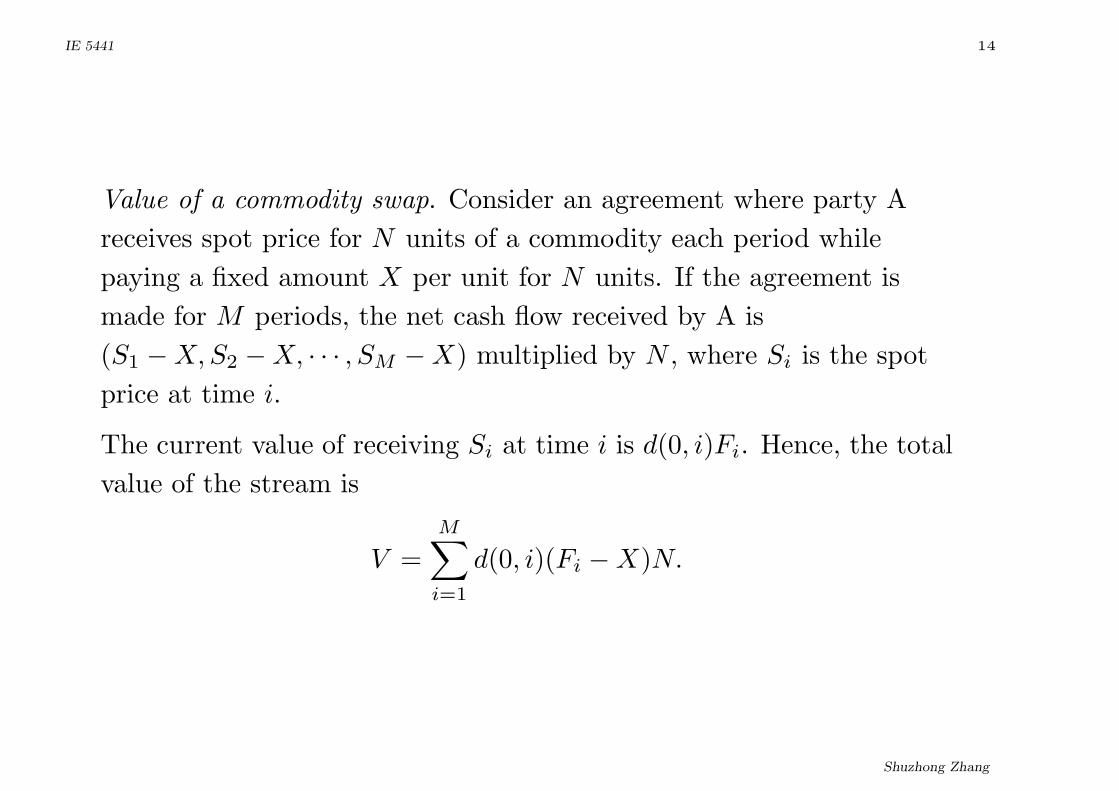

Value of a commodity swap. Consider an agreement where party A

receives spot price for N units of a commodity each period while

paying a fixed amount X per unit for N units. If the agreement is

made for M periods, the net cash flow received by A is

(S1 −X,S2 −X, · · · , SM −X) multiplied by N , where Si is the spot

price at time i.

The current value of receiving Si at time i is d(0, i)Fi. Hence, the total

value of the stream is

V =M∑i=1

d(0, i)(Fi −X)N.

Shuzhong Zhang

IE 5441 15

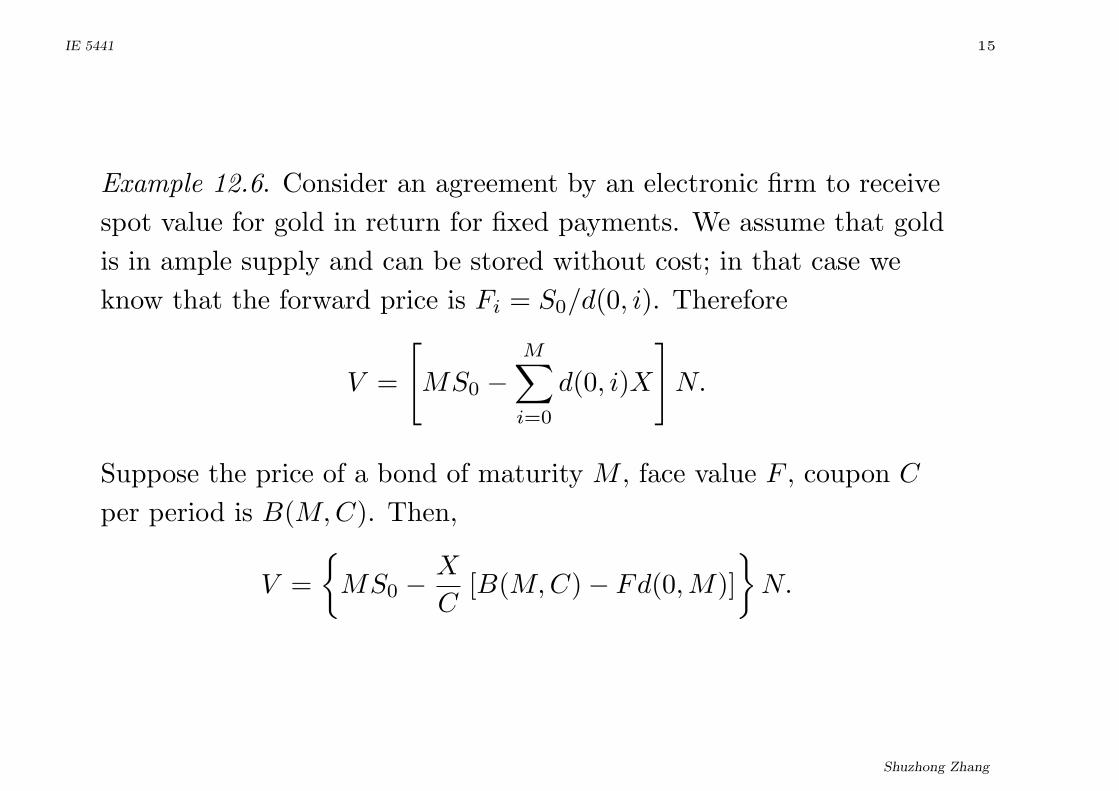

Example 12.6. Consider an agreement by an electronic firm to receive

spot value for gold in return for fixed payments. We assume that gold

is in ample supply and can be stored without cost; in that case we

know that the forward price is Fi = S0/d(0, i). Therefore

V =

[MS0 −

M∑i=0

d(0, i)X

]N.

Suppose the price of a bond of maturity M , face value F , coupon C

per period is B(M,C). Then,

V =

{MS0 −

X

C[B(M,C)− Fd(0,M)]

}N.

Shuzhong Zhang

IE 5441 16

Value of an interest rate swap. Party A agrees to make payments of a

fixed rate r of interest on principal N while receiving floating rate

payments on the same notional principal for M periods. The cash flow

stream received by A is (c0 − r, c1 − r, · · · , cM − r)×N where ci is the

floating rate in period i.

The initial value of a floating rate bond is par. The value of the

floating rate portion of the swap is par minus the present value of the

principal received at M . Hence, the value of the floating rate portion

of the swap is N − d(0,M)N .

The overall value of the swap is

V =

[1− d(0,M)− r

M∑i=1

d(0, i)

]N.

Shuzhong Zhang

IE 5441 17

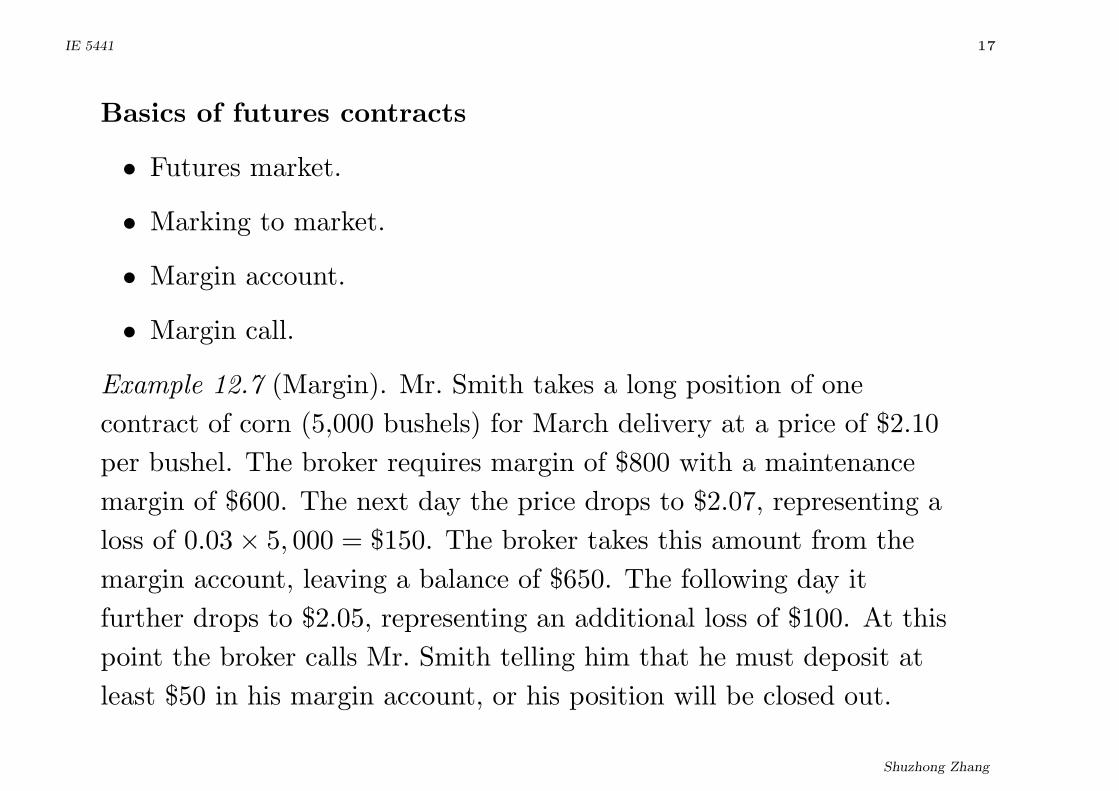

Basics of futures contracts

• Futures market.

• Marking to market.

• Margin account.

• Margin call.

Example 12.7 (Margin). Mr. Smith takes a long position of one

contract of corn (5,000 bushels) for March delivery at a price of $2.10

per bushel. The broker requires margin of $800 with a maintenance

margin of $600. The next day the price drops to $2.07, representing a

loss of 0.03× 5, 000 = $150. The broker takes this amount from the

margin account, leaving a balance of $650. The following day it

further drops to $2.05, representing an additional loss of $100. At this

point the broker calls Mr. Smith telling him that he must deposit at

least $50 in his margin account, or his position will be closed out.

Shuzhong Zhang

IE 5441 18

Futures prices

Futures-forward equivalence. Suppose that the interest rates are known

to follow expectation dynamics. Then the theoretical futures and

forward prices of corresponding contracts are identical.

�

����

�����

����

� �

Shuzhong Zhang

IE 5441 19

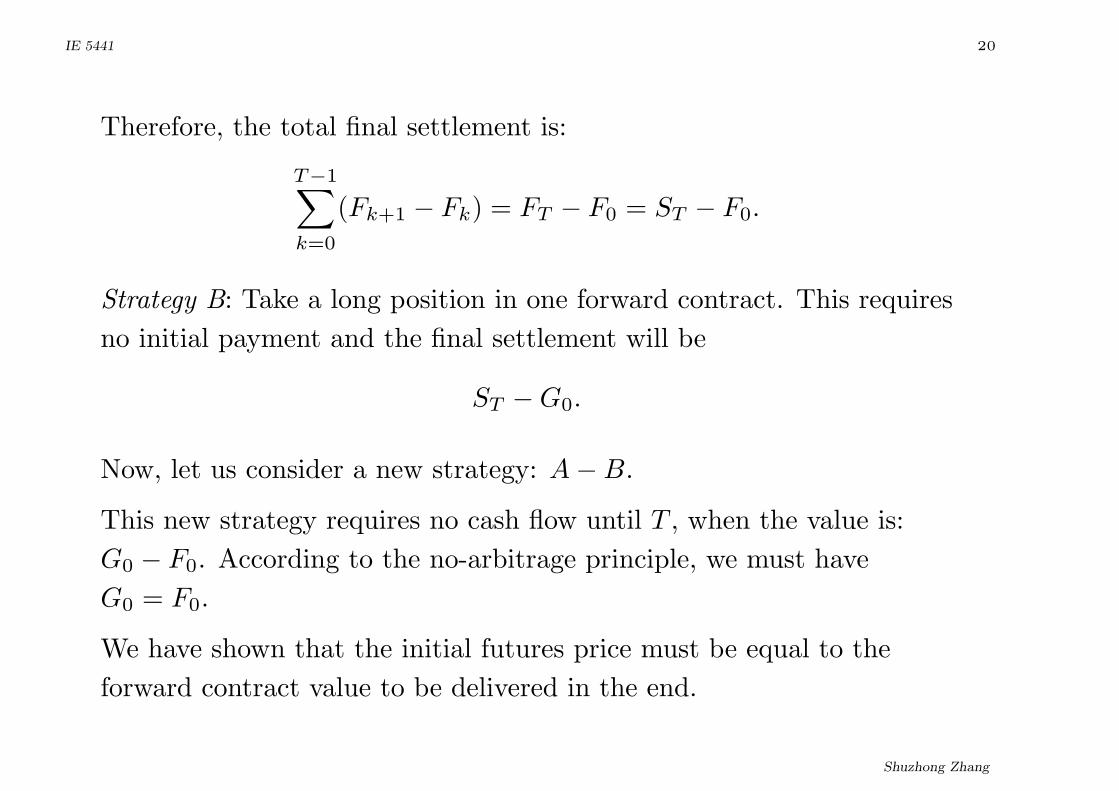

Let F0 be the initial futures price. Let G0 be the forward price (to be

paid at delivery). Consider the following two strategies:

Strategy A:

• Time 0: Go long d(1, T ) futures.

• Time 1: Increase position to d(2, T ).

• · · ·

• Time k: Increase position to d(k + 1, T ).

• · · ·

• Time T − 1: Increase position to 1.

The profit at time k + 1 from the previous period is

(Fk+1 − Fk)d(k + 1, T ). This amounts to the final payment

(Fk+1 − Fk)d(k + 1, T )

d(k + 1, T )= Fk+1 − Fk.

Shuzhong Zhang

IE 5441 20

Therefore, the total final settlement is:

T−1∑k=0

(Fk+1 − Fk) = FT − F0 = ST − F0.

Strategy B: Take a long position in one forward contract. This requires

no initial payment and the final settlement will be

ST −G0.

Now, let us consider a new strategy: A−B.

This new strategy requires no cash flow until T , when the value is:

G0 − F0. According to the no-arbitrage principle, we must have

G0 = F0.

We have shown that the initial futures price must be equal to the

forward contract value to be delivered in the end.

Shuzhong Zhang

IE 5441 21

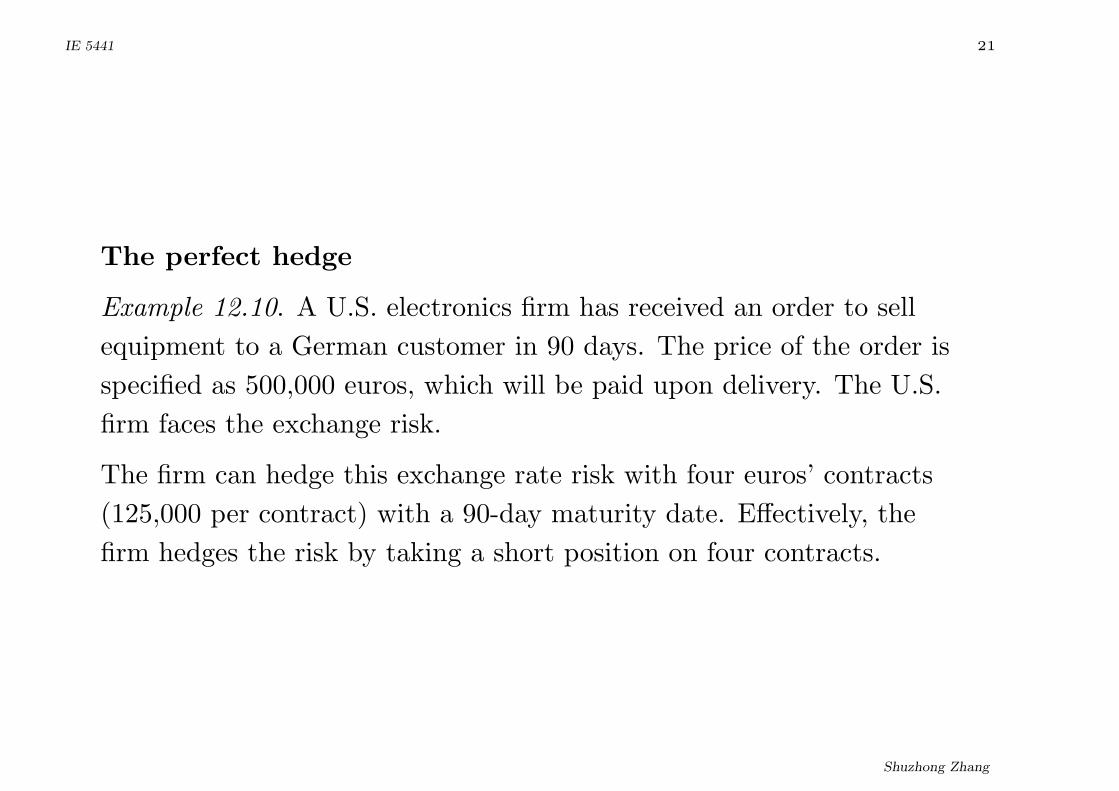

The perfect hedge

Example 12.10. A U.S. electronics firm has received an order to sell

equipment to a German customer in 90 days. The price of the order is

specified as 500,000 euros, which will be paid upon delivery. The U.S.

firm faces the exchange risk.

The firm can hedge this exchange rate risk with four euros’ contracts

(125,000 per contract) with a 90-day maturity date. Effectively, the

firm hedges the risk by taking a short position on four contracts.

Shuzhong Zhang

IE 5441 22

The minimum-variance hedge

Sometimes it is not possible to hedge the risk perfectly. The lack of

hedging perfection can be measured by the so-called basis:

basis = spot price of asset to be hedged - futures price of contract used.

Suppose x to be the cash to occur at T , h to be the futures position

taken. Then, the cash flow at T is

y = x+ (FT − F0)h,

with var (y) = var (x) + 2cov (x, FT )h+ var (FT )h2. The

minimum-variance hedging formula:

h = −cov (x, FT )

var (FT )

var (y) = var (x)− cov (x, FT )2

var (FT ).

Shuzhong Zhang

IE 5441 23

Optimal Hedging

If a utility function U is available, then it is appropriate to solve

maxh

E[U(x+ h(FT − F0))].

Suppose the utility function is a quadratic function. Then, the

objective becomes E[x+ h(FT − F0)]− rvar (x+ hFT ). The optimal

solution is

h =E[FT ]− F0

2rvar (FT )− cov (x, FT )

var (FT ).

Shuzhong Zhang

IE 5441 24

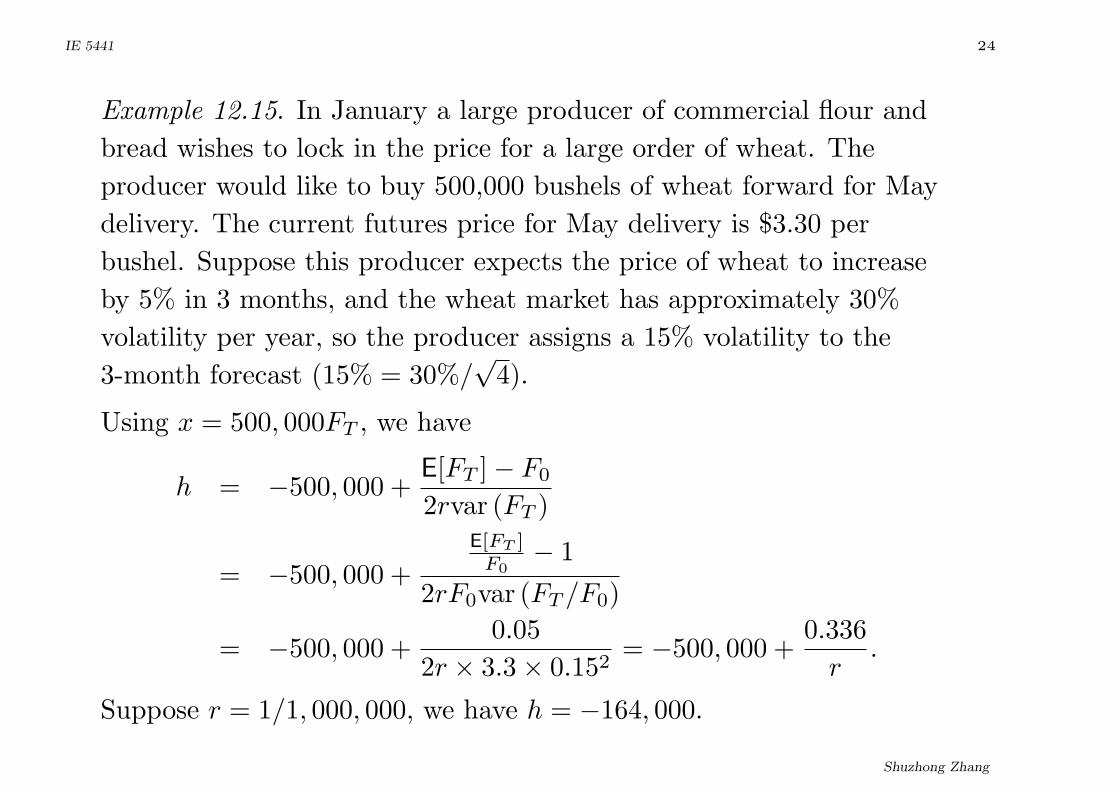

Example 12.15. In January a large producer of commercial flour and

bread wishes to lock in the price for a large order of wheat. The

producer would like to buy 500,000 bushels of wheat forward for May

delivery. The current futures price for May delivery is $3.30 per

bushel. Suppose this producer expects the price of wheat to increase

by 5% in 3 months, and the wheat market has approximately 30%

volatility per year, so the producer assigns a 15% volatility to the

3-month forecast (15% = 30%/√4).

Using x = 500, 000FT , we have

h = −500, 000 +E[FT ]− F0

2rvar (FT )

= −500, 000 +

E[FT ]F0

− 1

2rF0var (FT /F0)

= −500, 000 +0.05

2r × 3.3× 0.152= −500, 000 +

0.336

r.

Suppose r = 1/1, 000, 000, we have h = −164, 000.

Shuzhong Zhang

IE 5441 25

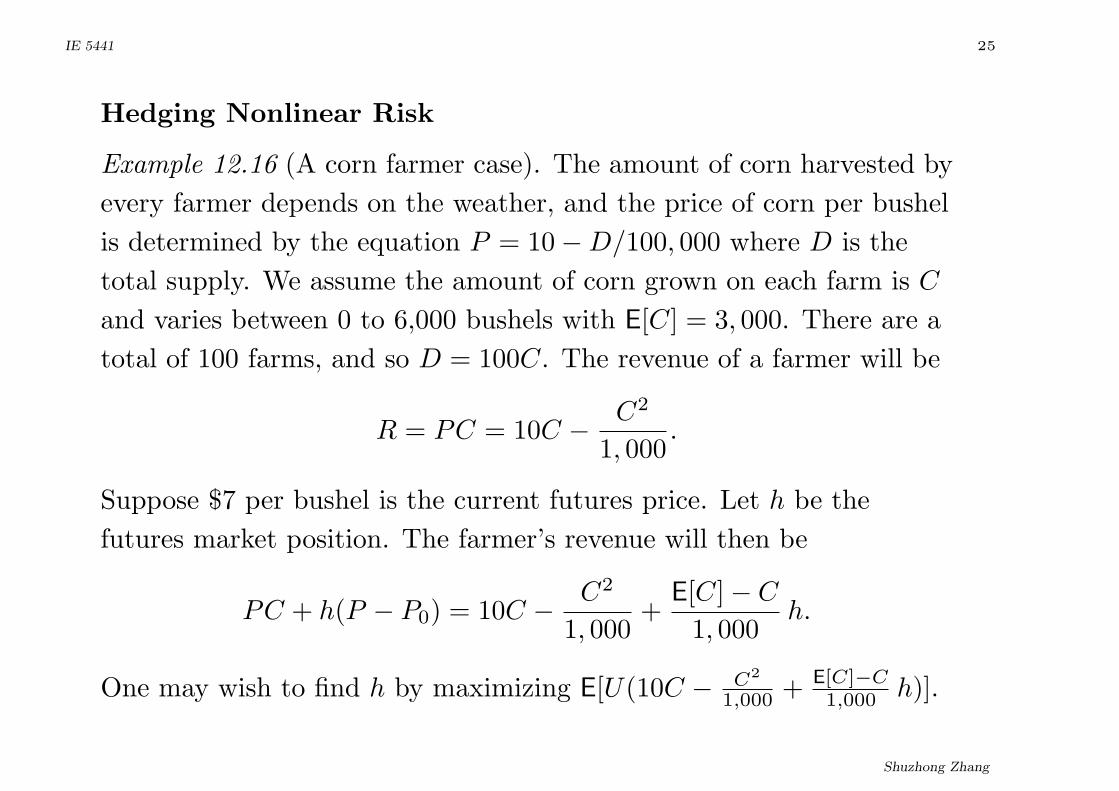

Hedging Nonlinear Risk

Example 12.16 (A corn farmer case). The amount of corn harvested by

every farmer depends on the weather, and the price of corn per bushel

is determined by the equation P = 10−D/100, 000 where D is the

total supply. We assume the amount of corn grown on each farm is C

and varies between 0 to 6,000 bushels with E[C] = 3, 000. There are a

total of 100 farms, and so D = 100C. The revenue of a farmer will be

R = PC = 10C − C2

1, 000.

Suppose $7 per bushel is the current futures price. Let h be the

futures market position. The farmer’s revenue will then be

PC + h(P − P0) = 10C − C2

1, 000+

E[C]− C

1, 000h.

One may wish to find h by maximizing E[U(10C − C2

1,000 + E[C]−C1,000 h)].

Shuzhong Zhang