Embed Size (px)

Citation preview

1

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

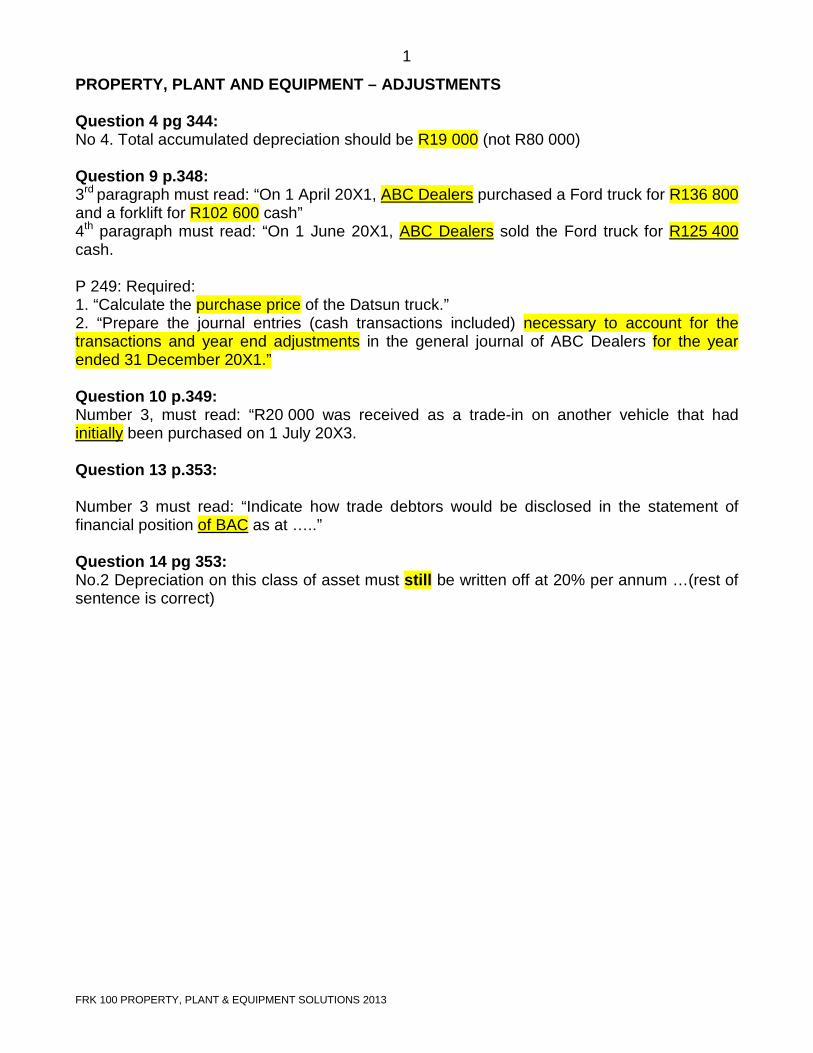

PROPERTY, PLANT AND EQUIPMENT – ADJUSTMENTS Question 4 pg 344: No 4. Total accumulated depreciation should be R19 000 (not R80 000) Question 9 p.348: 3rd paragraph must read: “On 1 April 20X1, ABC Dealers purchased a Ford truck for R136 800 and a forklift for R102 600 cash” 4th paragraph must read: “On 1 June 20X1, ABC Dealers sold the Ford truck for R125 400 cash. P 249: Required: 1. “Calculate the purchase price of the Datsun truck.” 2. “Prepare the journal entries (cash transactions included) necessary to account for the transactions and year end adjustments in the general journal of ABC Dealers for the year ended 31 December 20X1.” Question 10 p.349: Number 3, must read: “R20 000 was received as a trade-in on another vehicle that had initially been purchased on 1 July 20X3. Question 13 p.353: Number 3 must read: “Indicate how trade debtors would be disclosed in the statement of financial position of BAC as at …..” Question 14 pg 353: No.2 Depreciation on this class of asset must still be written off at 20% per annum …(rest of sentence is correct)

2

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

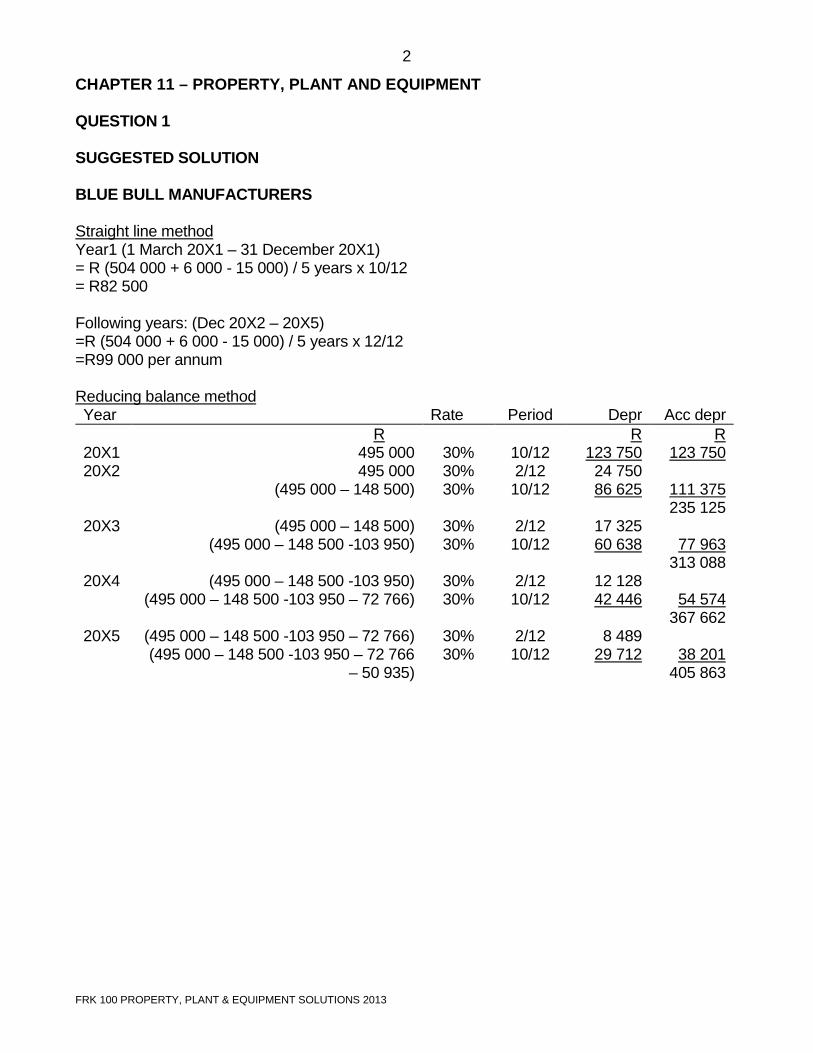

CHAPTER 11 – PROPERTY, PLANT AND EQUIPMENT QUESTION 1 SUGGESTED SOLUTION BLUE BULL MANUFACTURERS Straight line method Year1 (1 March 20X1 – 31 December 20X1) = R (504 000 + 6 000 - 15 000) / 5 years x 10/12 = R82 500 Following years: (Dec 20X2 – 20X5) =R (504 000 + 6 000 - 15 000) / 5 years x 12/12 =R99 000 per annum Reducing balance method Year Rate Period Depr Acc depr 20X1 20X2 20X3 20X4 20X5

R 495 000 495 000

(495 000 – 148 500)

(495 000 – 148 500) (495 000 – 148 500 -103 950)

(495 000 – 148 500 -103 950)

(495 000 – 148 500 -103 950 – 72 766)

(495 000 – 148 500 -103 950 – 72 766) (495 000 – 148 500 -103 950 – 72 766

– 50 935)

30% 30% 30%

30% 30%

30% 30%

30% 30%

10/12 2/12 10/12

2/12 10/12

2/12 10/12

2/12 10/12

R 123 750 24 750 86 625

17 325 60 638

12 128 42 446

8 489

29 712

R 123 750

111 375 235 125

77 963

313 088

54 574 367 662

38 201

405 863

3

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

Sum of digits method 5 + 4 + 3 + 2 + 1 = 15 parts Year Calculation Depreciation 20X1 20X2 20X3 20X4 20X5

5/15 x 495 000 x 10/12 5/15 x 495 000 x 2/12 4/15 x 495 000 x 10/12 4/15 x 495 000 x 2/12 3/15 x 495 000 x 10/12 3/15 x 495 000 x 2/12 2/15 x 495 000 x 10/12 2/15 x 495 000 x 2/12 1/15 x 495 000 x 10/12

R 137 500

27 500

110 000 137 500

22 000 82 500

104 500

16 500 55 000 71 500

11 000 27 500 38 500

Production unit method 495 000 / 900 000 = 55 cents per unit Period Units Depreciation Acc. depr.

20x1 20x2 20x3 20x4 20x5

190 000 240 000 220 000 200 000 50 000

55 cents

R 104 500 132 000 121 000 110 000 27 500

R 104 500 236 500 357 500 467 500 495 000

4

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

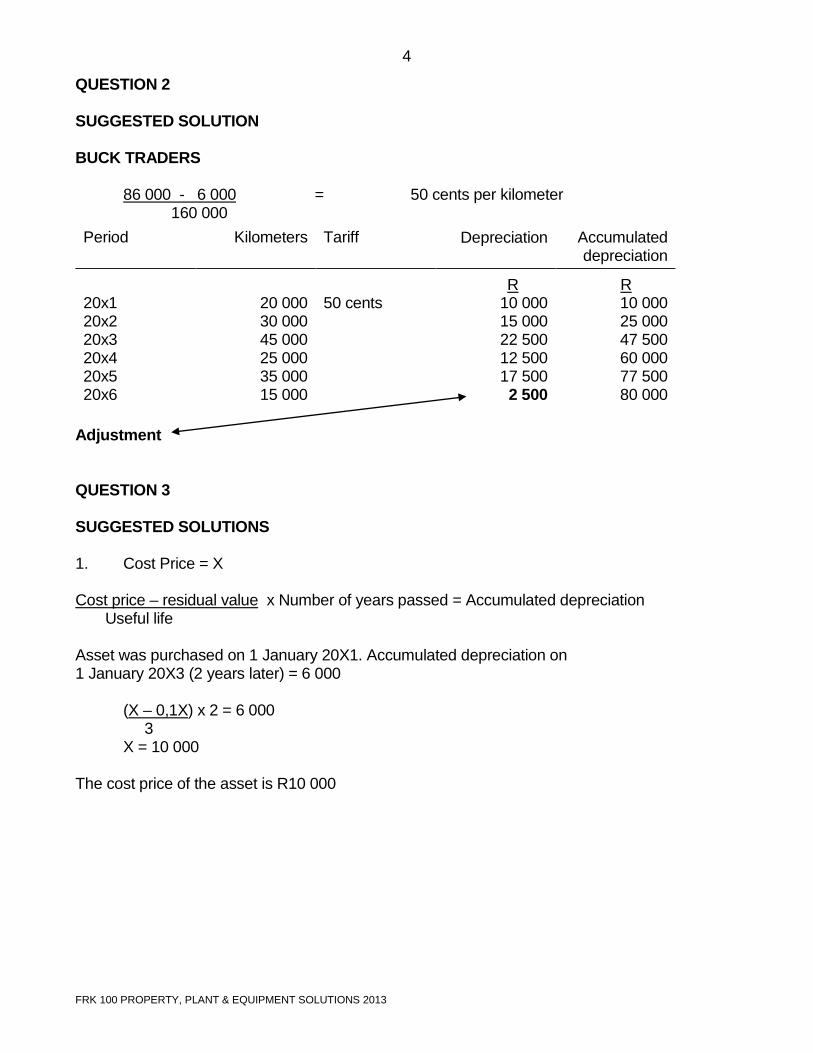

QUESTION 2 SUGGESTED SOLUTION BUCK TRADERS 86 000 - 6 000 = 50 cents per kilometer 160 000 Period Kilometers Tariff Depreciation Accumulated

depreciation

20x1 20x2 20x3 20x4 20x5 20x6

20 000 30 000 45 000 25 000 35 000 15 000

50 cents

R 10 000 15 000 22 500 12 500 17 500 2 500

R 10 000 25 000 47 500 60 000 77 500 80 000

Adjustment QUESTION 3 SUGGESTED SOLUTIONS 1. Cost Price = X Cost price – residual value x Number of years passed = Accumulated depreciation Useful life Asset was purchased on 1 January 20X1. Accumulated depreciation on 1 January 20X3 (2 years later) = 6 000 (X – 0,1X) x 2 = 6 000 3 X = 10 000 The cost price of the asset is R10 000

5

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

2. Cost price – Accumulated depreciation= Carrying amount Cost price = X Accumulated depreciation= Cost price – residual value x Years passed Useful life = X – 0,1X x 2 3 = 0,6X Thus: X – 0,6X = 4 000 0,4X = 4 000 X = 10 000 3. Depreciable amount = Cost price less residual value = 10 000 – 0,1(10 000) = 9 000 Fraction = 3 + 2 + 1 = 6 (product of estimated periods) Date Calculation Depreciation 1/1/20X1 – 28/2/20X1 9 000/6 x 3 x 2/12 = 750 1/3/20x1 – 28/2/20X2 9 000/6 x 3 x 10/12

9 000/6 x 2 x 2/12 3 750 500

= 4 250 1/3/20x2 – 28/2/20X3 9 000/6 x 2 x 10/12

9 000/6 x 1x 2/12 2 500 250

= 2 750 1/3/20x3 – 31/12/20X3 9 000/6 x 1 x 10/12 = 1 250 = 9 000 No depreciation 1/1/20X4 – 28/2/20X4 4. Residual value of machine sold: = 7 500 x 5 000 100 000 = R375 Accumulated depreciation: = 7 500 – 375 x 2 year 10 year 100 /10% = R1 425 Carrying amount of the asset: = R7 500 – R1 425 = R6 075 Sold for R3 000 (Loss with sale of asset: R6 075 – R3 000 = R3 075)

6

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

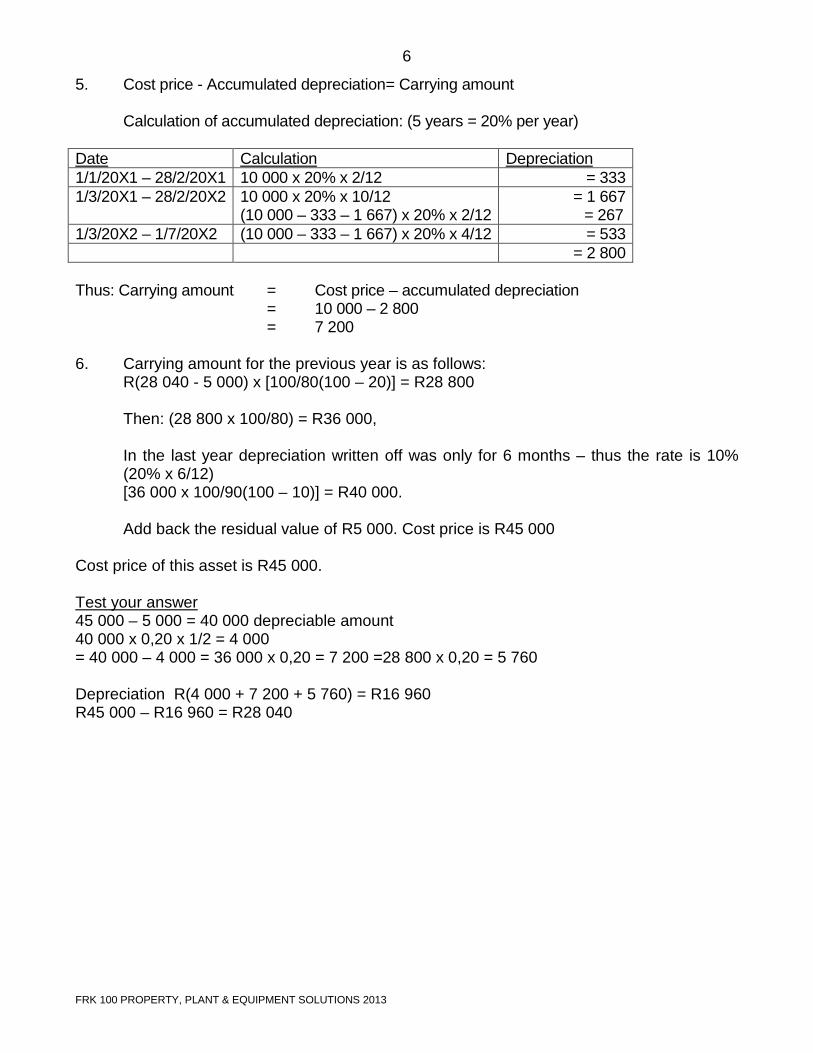

5. Cost price - Accumulated depreciation= Carrying amount Calculation of accumulated depreciation: (5 years = 20% per year) Date Calculation Depreciation 1/1/20X1 – 28/2/20X1 10 000 x 20% x 2/12 = 333 1/3/20X1 – 28/2/20X2 10 000 x 20% x 10/12

(10 000 – 333 – 1 667) x 20% x 2/12 = 1 667

= 267 1/3/20X2 – 1/7/20X2 (10 000 – 333 – 1 667) x 20% x 4/12 = 533 = 2 800 Thus: Carrying amount = Cost price – accumulated depreciation = 10 000 – 2 800 = 7 200 6. Carrying amount for the previous year is as follows:

R(28 040 - 5 000) x [100/80(100 – 20)] = R28 800

Then: (28 800 x 100/80) = R36 000,

In the last year depreciation written off was only for 6 months – thus the rate is 10% (20% x 6/12) [36 000 x 100/90(100 – 10)] = R40 000.

Add back the residual value of R5 000. Cost price is R45 000

Cost price of this asset is R45 000. Test your answer 45 000 – 5 000 = 40 000 depreciable amount 40 000 x 0,20 x 1/2 = 4 000 = 40 000 – 4 000 = 36 000 x 0,20 = 7 200 =28 800 x 0,20 = 5 760 Depreciation R(4 000 + 7 200 + 5 760) = R16 960 R45 000 – R16 960 = R28 040

7

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

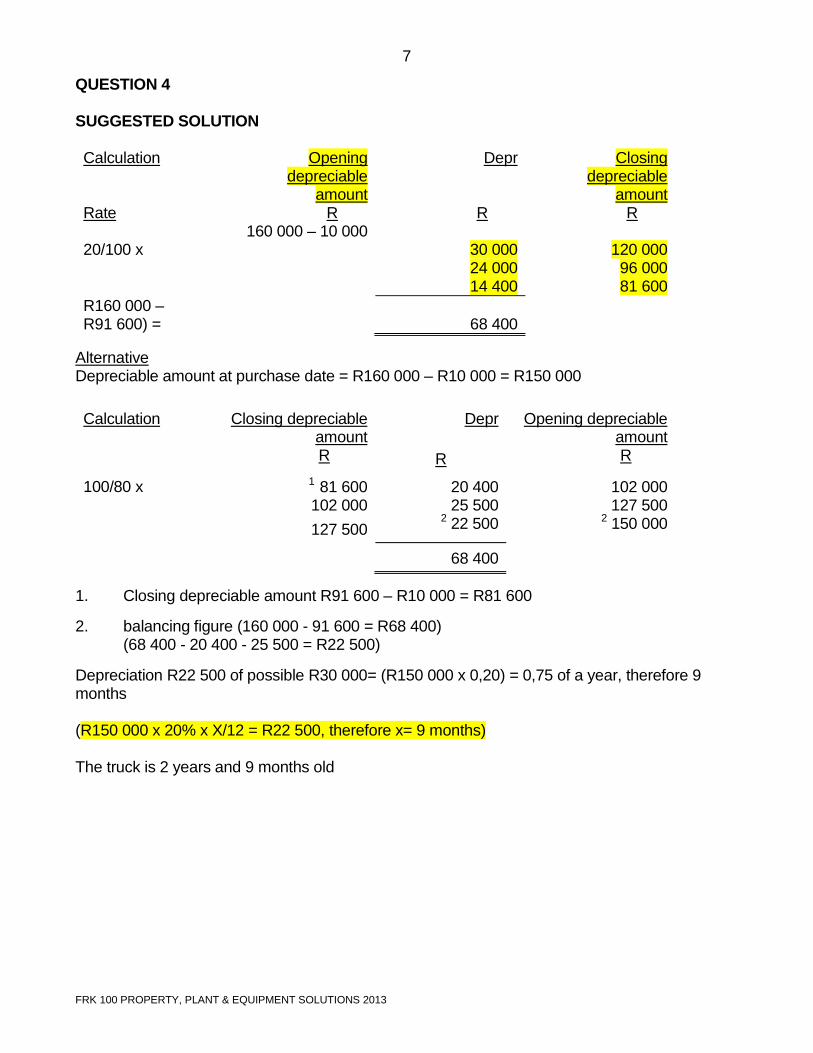

QUESTION 4 SUGGESTED SOLUTION Calculation Rate

Opening depreciable

amount R

Depr

R

Closing depreciable

amount R

20/100 x

160 000 – 10 000

30 000 24 000 14 400

120 000 96 000 81 600

R160 000 – R91 600) =

68 400

Alternative Depreciable amount at purchase date = R160 000 – R10 000 = R150 000 Calculation

Closing depreciable amount R

Depr

R

Opening depreciable amount R

100/80 x 1 81 600 102 000 127 500

20 400 25 500

2 22 500

102 000 127 500

2 150 000

68 400 1. Closing depreciable amount R91 600 – R10 000 = R81 600 2. balancing figure (160 000 - 91 600 = R68 400) (68 400 - 20 400 - 25 500 = R22 500) Depreciation R22 500 of possible R30 000= (R150 000 x 0,20) = 0,75 of a year, therefore 9 months (R150 000 x 20% x X/12 = R22 500, therefore x= 9 months) The truck is 2 years and 9 months old

8

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

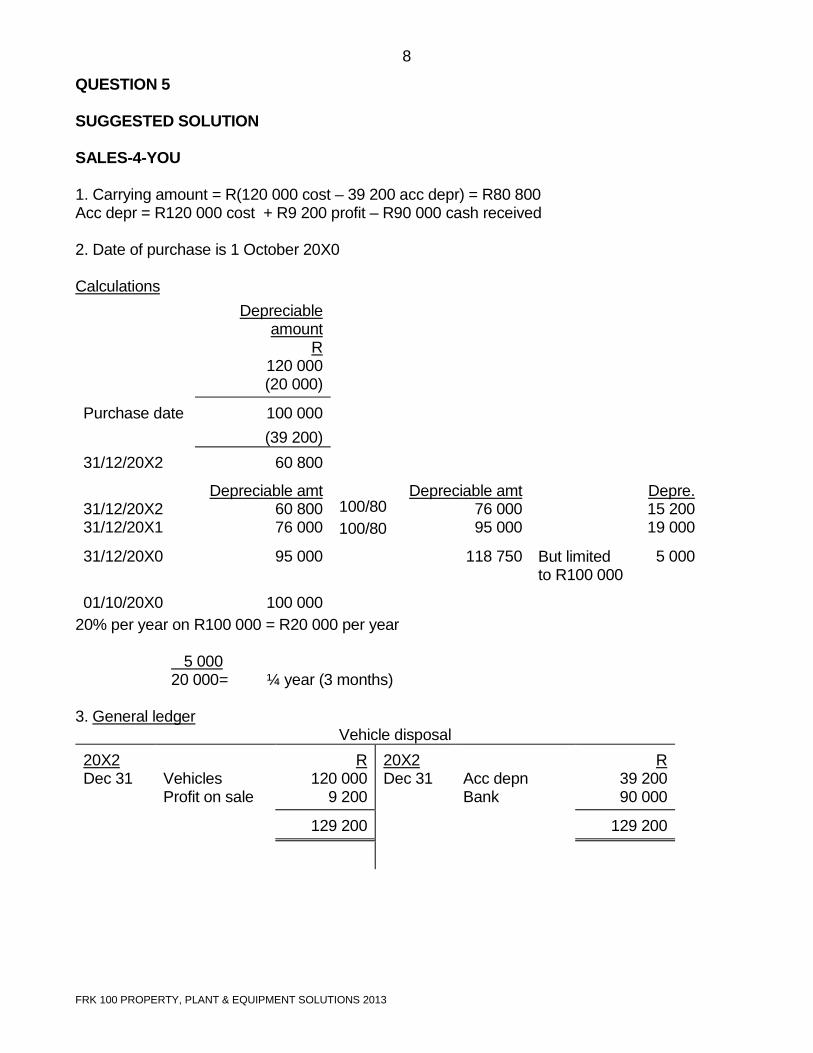

QUESTION 5 SUGGESTED SOLUTION SALES-4-YOU 1. Carrying amount = R(120 000 cost – 39 200 acc depr) = R80 800 Acc depr = R120 000 cost + R9 200 profit – R90 000 cash received 2. Date of purchase is 1 October 20X0 Calculations

Depreciable amount

R 120 000 (20 000)

Purchase date 100 000 (39 200)

31/12/20X2 60 800

31/12/20X2 31/12/20X1

Depreciable amt 60 800 76 000

100/80 100/80

Depreciable amt 76 000 95 000

Depre. 15 200 19 000

31/12/20X0 95 000 118 750 But limited to R100 000

5 000

01/10/20X0 100 000 20% per year on R100 000 = R20 000 per year 5 000 20 000 = ¼ year (3 months) 3. General ledger Vehicle disposal 20X2 Dec 31

Vehicles Profit on sale

R 120 000

9 200

20X2 Dec 31

Acc depn Bank

R 39 200 90 000

129 200 129 200

9

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

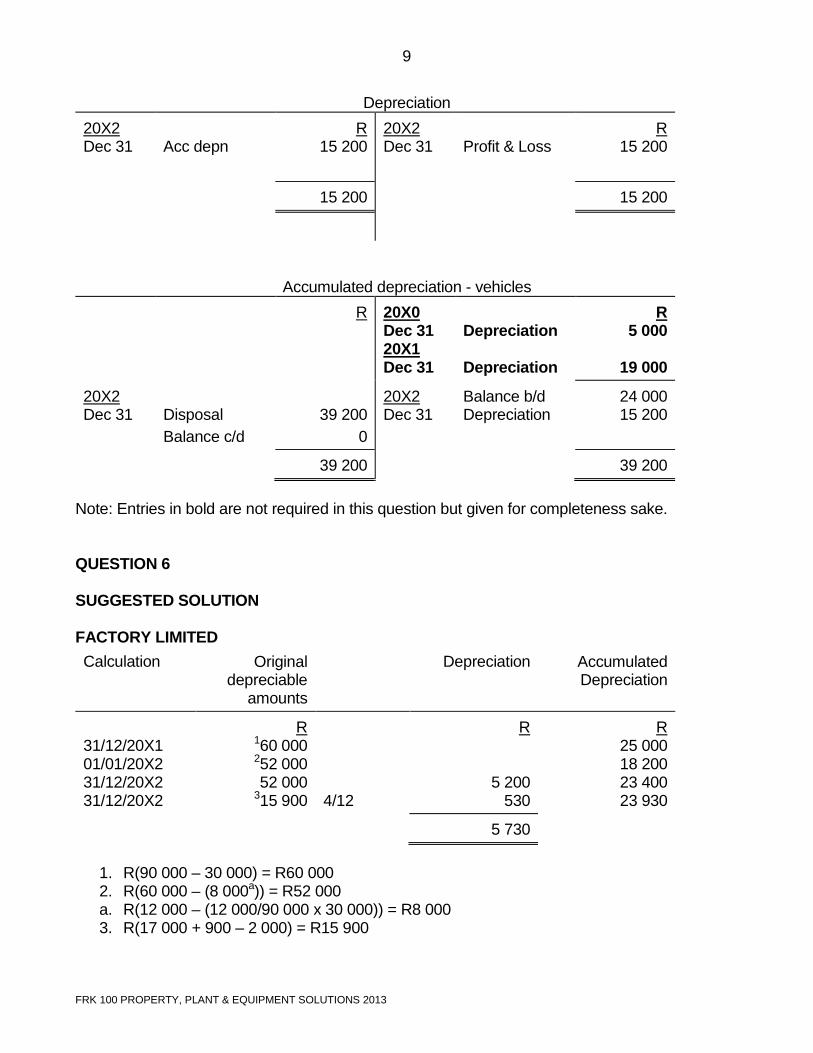

Depreciation

20X2 Dec 31

Acc depn

R 15 200

20X2 Dec 31

Profit & Loss

R 15 200

15 200 15 200

Accumulated depreciation - vehicles R

20X0 Dec 31 20X1 Dec 31

Depreciation Depreciation

R 5 000

19 000

20X2 Dec 31

Disposal Balance c/d

39 200

0

20X2 Dec 31

Balance b/d Depreciation

24 000 15 200

39 200 39 200 Note: Entries in bold are not required in this question but given for completeness sake. QUESTION 6 SUGGESTED SOLUTION FACTORY LIMITED Calculation Original

depreciable amounts

Depreciation Accumulated Depreciation

31/12/20X1 01/01/20X2 31/12/20X2 31/12/20X2

R 160 000 252 000 52 000

315 900

4/12

R

5 200 530

R 25 000 18 200 23 400 23 930

5 730

1. R(90 000 – 30 000) = R60 000 2. R(60 000 – (8 000a)) = R52 000 a. R(12 000 – (12 000/90 000 x 30 000)) = R8 000 3. R(17 000 + 900 – 2 000) = R15 900

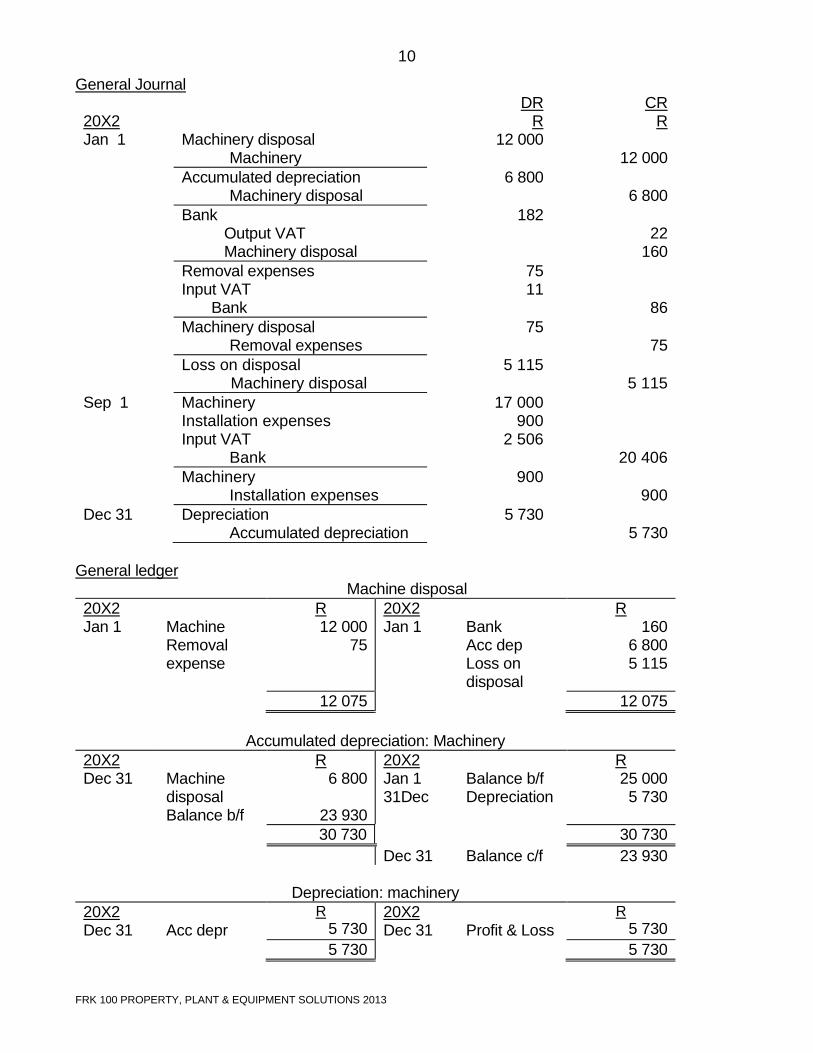

10

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

General Journal 20X2 Jan 1

Machinery disposal Machinery

DR R

12 000

CR R

12 000

Accumulated depreciation Machinery disposal

6 800 6 800

Bank Output VAT Machinery disposal

182 22

160 Removal expenses

Input VAT Bank

75 11

86 Machinery disposal

Removal expenses 75

75 Loss on disposal

Machinery disposal 5 115

5 115 Sep 1 Machinery

Installation expenses Input VAT Bank

17 000 900

2 506

20 406 Machinery

Installation expenses 900

900 Dec 31 Depreciation

Accumulated depreciation 5 730

5 730 General ledger

Machine disposal 20X2 Jan 1

Machine Removal expense

R 12 000

75

20X2 Jan 1

Bank Acc dep Loss on disposal

R 160

6 800 5 115

12 075 12 075 Accumulated depreciation: Machinery 20X2 Dec 31

Machine disposal Balance b/f

R 6 800

23 930

20X2 Jan 1 31Dec

Balance b/f Depreciation

R 25 000 5 730

30 730 30 730 Dec 31 Balance c/f 23 930

Depreciation: machinery 20X2 Dec 31

Acc depr

R 5 730

20X2 Dec 31

Profit & Loss

R 5 730

5 730 5 730

11

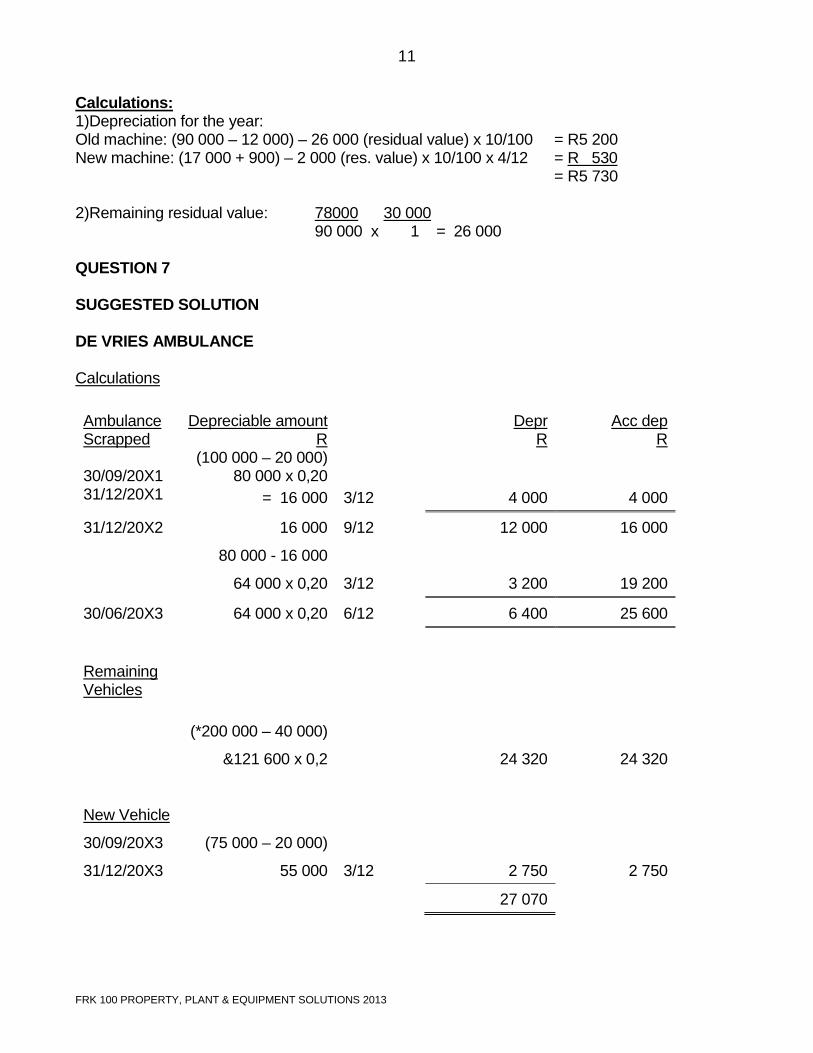

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

Calculations: 1)Depreciation for the year: Old machine: (90 000 – 12 000) – 26 000 (residual value) x 10/100 = R5 200 New machine: (17 000 + 900) – 2 000 (res. value) x 10/100 x 4/12 = R 530 = R5 730 2)Remaining residual value: 78000 30 000 90 000 x 1 = 26 000 QUESTION 7 SUGGESTED SOLUTION DE VRIES AMBULANCE Calculations Ambulance Scrapped 30/09/20X1 31/12/20X1

Depreciable amount R

(100 000 – 20 000) 80 000 x 0,20

= 16 000

3/12

Depr R

4 000

Acc dep R

4 000

31/12/20X2 16 000 9/12 12 000 16 000

80 000 - 16 000

64 000 x 0,20 3/12 3 200 19 200

30/06/20X3 64 000 x 0,20 6/12 6 400 25 600

Remaining Vehicles

(*200 000 – 40 000)

&121 600 x 0,2 24 320 24 320

New Vehicle

30/09/20X3 (75 000 – 20 000)

31/12/20X3 55 000 3/12 2 750 2 750

27 070

12

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

* (300 000 – 100 000) = 200 000 & (160 000 – #38 400) = 121 600 # R57 600 – R19 200 = R38 400 Motor vehicles 20X2 Dec 31 20X3 Sept 30

Bal b/f Bank

R 300 000

75 000

20X3 Jun 30 Dec 31

Disposal Bal c/f

R 100 000 275 000

375 000 375 000

20X3 Dec 31

Bal b/f

275 000

Accumulated depreciation 20X3 Dec 31

Disposal Bal c/f

R 25 600 65 470

20X2 Dec 31 20X3 Jun 30 Dec 31

Bal b/f Depreciation Depreciation

R 57 600

6 400

27 070

91 070 91 070

20X3 Dec 31

Bal b/f

65 470

Motor vehicles disposal 20X3 Jun 30

Motor vehicles

R 100 000

20X3 Jun 30

Acc depn Bank Loss on scrapping

R 25 600 60 000

14 400

100 000 100 000

Depreciation 20X3 Jun 30 Dec 31

Acc depn Acc depn

R 6 400

27 070

20X3 Dec 31

Profit & loss

R

33 470

33 470 33 470

13

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

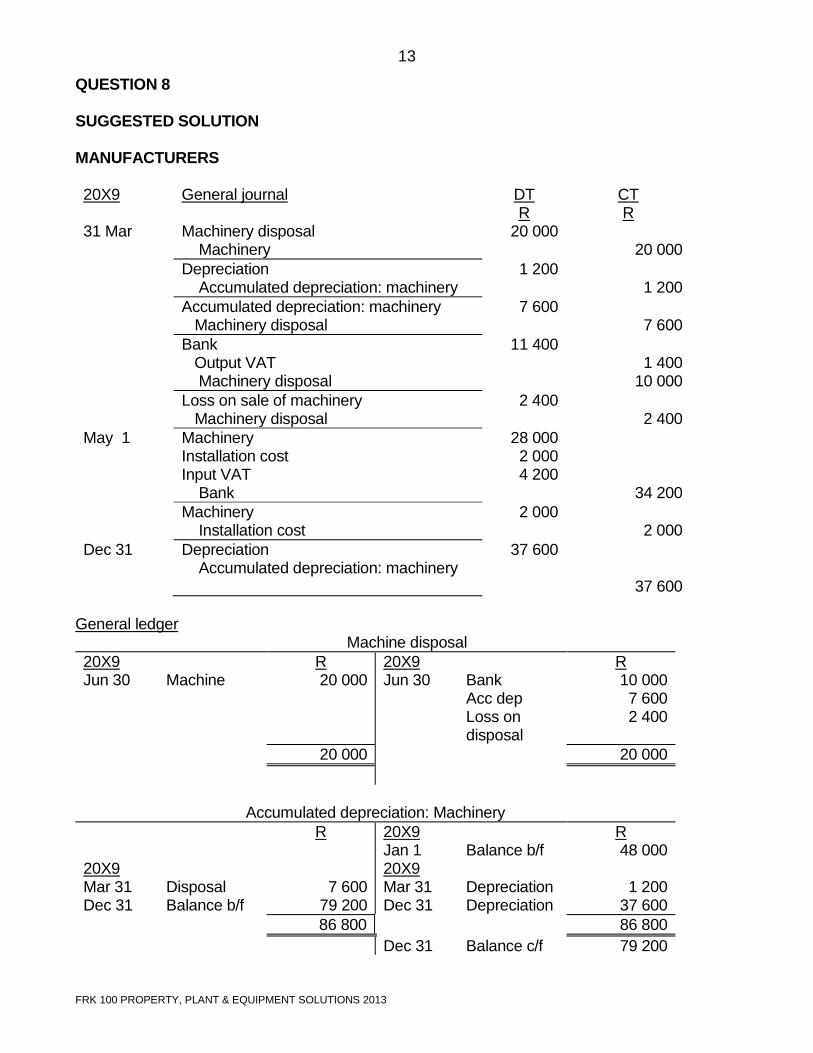

QUESTION 8 SUGGESTED SOLUTION MANUFACTURERS 20X9 31 Mar

General journal Machinery disposal Machinery

DT R

20 000

CT R

20 000

Depreciation Accumulated depreciation: machinery

1 200 1 200

Accumulated depreciation: machinery Machinery disposal

7 600 7 600

Bank Output VAT Machinery disposal

11 400 1 400

10 000 Loss on sale of machinery

Machinery disposal 2 400

2 400 May 1 Machinery

Installation cost Input VAT Bank

28 000 2 000 4 200

34 200 Machinery

Installation cost 2 000

2 000 Dec 31 Depreciation

Accumulated depreciation: machinery 37 600

37 600

General ledger

Machine disposal 20X9 Jun 30

Machine

R 20 000

20X9 Jun 30

Bank Acc dep Loss on disposal

R 10 000 7 600 2 400

20 000 20 000

Accumulated depreciation: Machinery 20X9 Mar 31 Dec 31

Disposal Balance b/f

R

7 600 79 200

20X9 Jan 1 20X9 Mar 31 Dec 31

Balance b/f Depreciation Depreciation

R 48 000

1 200

37 600 86 800 86 800 Dec 31 Balance c/f 79 200

14

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

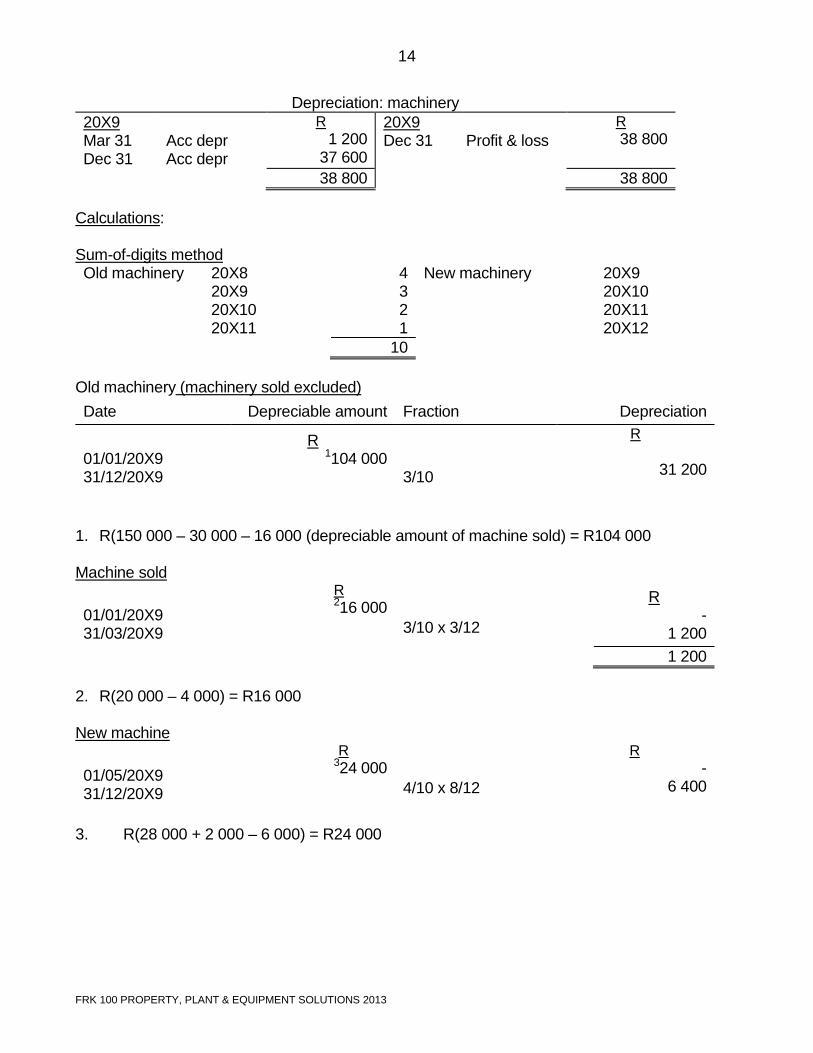

Depreciation: machinery 20X9 Mar 31 Dec 31

Acc depr Acc depr

R 1 200 37 600

20X9 Dec 31

Profit & loss

R 38 800

38 800 38 800 Calculations: Sum-of-digits method Old machinery 20X8

20X9 20X10 20X11

4 3 2 1

New machinery 20X9 20X10 20X11 20X12

10 Old machinery (machinery sold excluded) Date Depreciable amount Fraction Depreciation

01/01/20X9 31/12/20X9

R 1104 000

3/10

R

31 200

1. R(150 000 – 30 000 – 16 000 (depreciable amount of machine sold) = R104 000

Machine sold 01/01/20X9 31/03/20X9

R 216 000

3/10 x 3/12

R -

1 200 1 200

2. R(20 000 – 4 000) = R16 000 New machine 01/05/20X9 31/12/20X9

R 324 000

4/10 x 8/12

R -

6 400

3. R(28 000 + 2 000 – 6 000) = R24 000

15

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

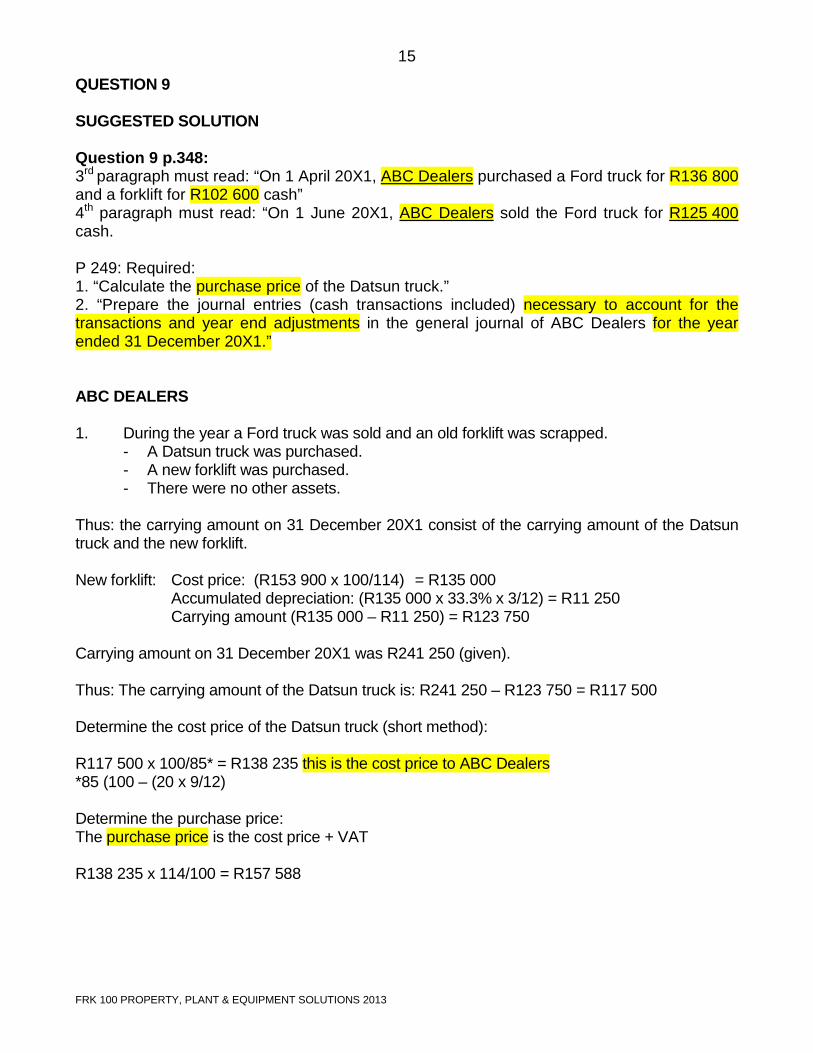

QUESTION 9 SUGGESTED SOLUTION Question 9 p.348: 3rd paragraph must read: “On 1 April 20X1, ABC Dealers purchased a Ford truck for R136 800 and a forklift for R102 600 cash” 4th paragraph must read: “On 1 June 20X1, ABC Dealers sold the Ford truck for R125 400 cash. P 249: Required: 1. “Calculate the purchase price of the Datsun truck.” 2. “Prepare the journal entries (cash transactions included) necessary to account for the transactions and year end adjustments in the general journal of ABC Dealers for the year ended 31 December 20X1.” ABC DEALERS 1. During the year a Ford truck was sold and an old forklift was scrapped.

- A Datsun truck was purchased. - A new forklift was purchased. - There were no other assets.

Thus: the carrying amount on 31 December 20X1 consist of the carrying amount of the Datsun truck and the new forklift. New forklift: Cost price: (R153 900 x 100/114) = R135 000 Accumulated depreciation: (R135 000 x 33.3% x 3/12) = R11 250 Carrying amount (R135 000 – R11 250) = R123 750 Carrying amount on 31 December 20X1 was R241 250 (given). Thus: The carrying amount of the Datsun truck is: R241 250 – R123 750 = R117 500 Determine the cost price of the Datsun truck (short method): R117 500 x 100/85* = R138 235 this is the cost price to ABC Dealers *85 (100 – (20 x 9/12) Determine the purchase price: The purchase price is the cost price + VAT R138 235 x 114/100 = R157 588

16

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

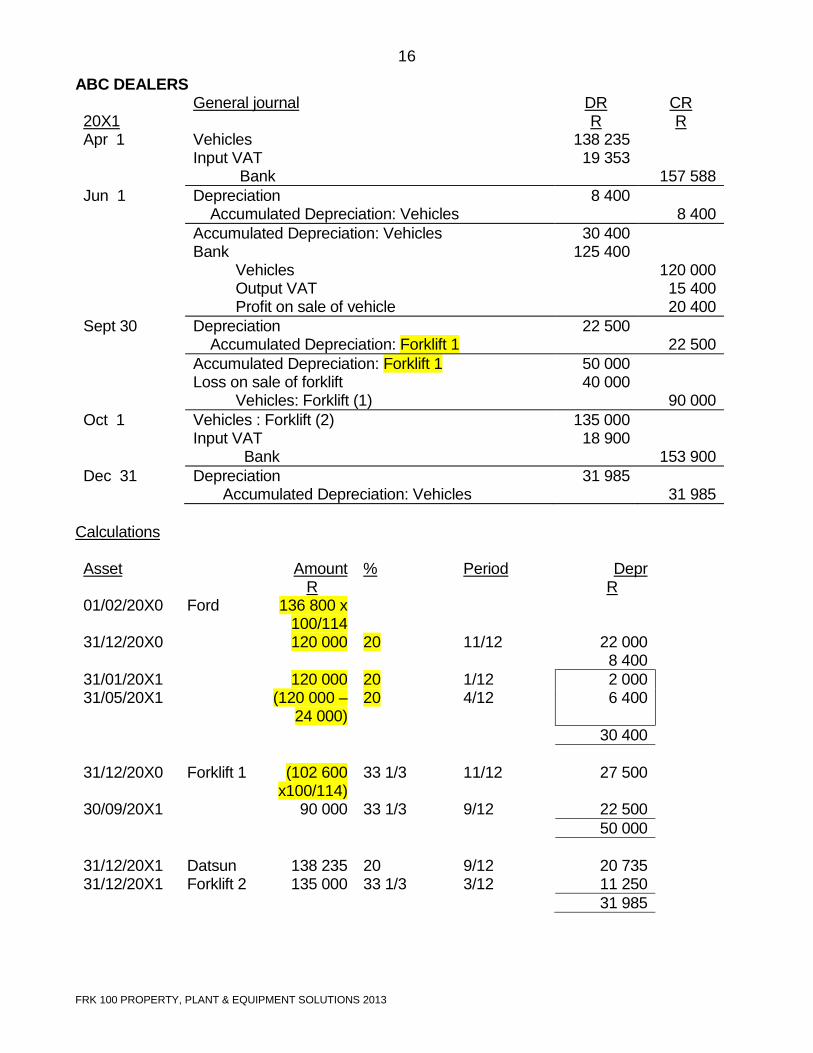

ABC DEALERS 20X1 Apr 1

General journal Vehicles Input VAT Bank

DR R

138 235 19 353

CR R

157 588 Jun 1 Depreciation

Accumulated Depreciation: Vehicles 8 400

8 400 Accumulated Depreciation: Vehicles

Bank Vehicles Output VAT Profit on sale of vehicle

30 400 125 400

120 000 15 400 20 400

Sept 30 Depreciation Accumulated Depreciation: Forklift 1

22 500 22 500

Accumulated Depreciation: Forklift 1 Loss on sale of forklift Vehicles: Forklift (1)

50 000 40 000

90 000 Oct 1 Vehicles : Forklift (2)

Input VAT Bank

135 000 18 900

153 900 Dec 31 Depreciation

Accumulated Depreciation: Vehicles 31 985

31 985 Calculations Asset 01/02/20X0

Ford

Amount R

136 800 x 100/114

%

Period

Depr R

31/12/20X0 120 000 20 11/12 22 000 8 400 31/01/20X1 120 000 20 1/12 2 000 31/05/20X1 (120 000 –

24 000) 20 4/12 6 400

30 400 31/12/20X0 Forklift 1 (102 600

x100/114) 33 1/3 11/12 27 500

30/09/20X1 90 000 33 1/3 9/12 22 500 50 000 31/12/20X1 Datsun 138 235 20 9/12 20 735 31/12/20X1 Forklift 2 135 000 33 1/3 3/12 11 250 31 985

17

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

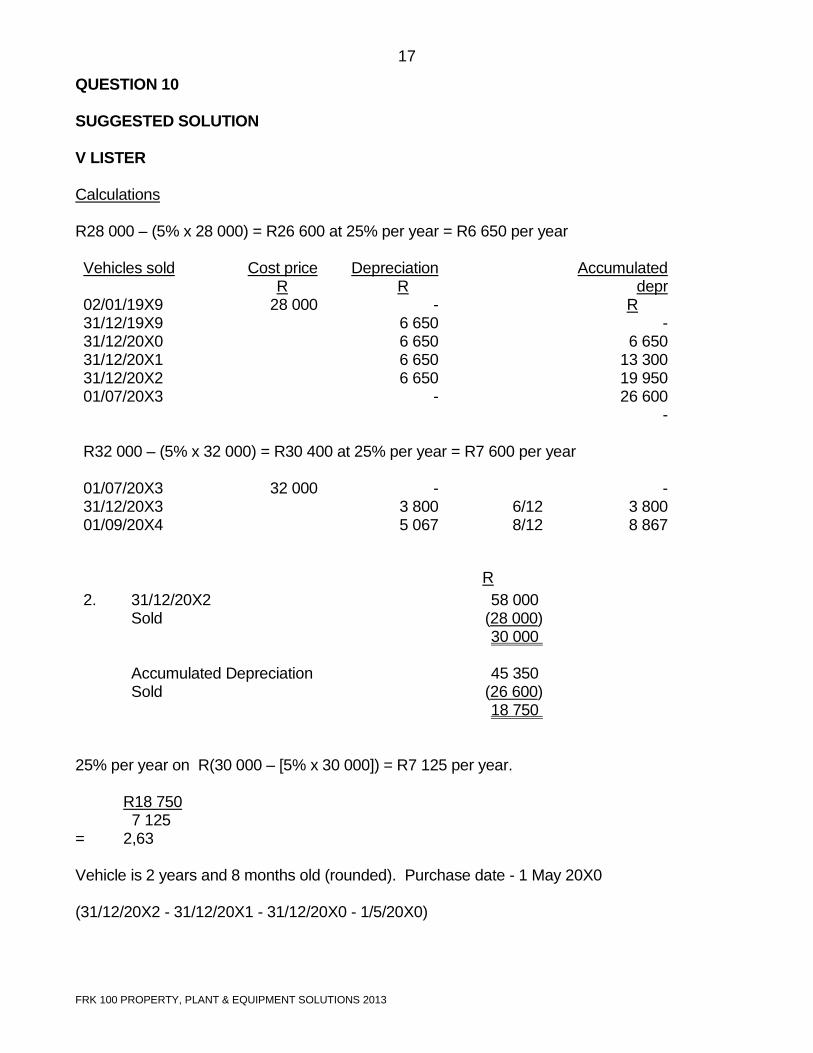

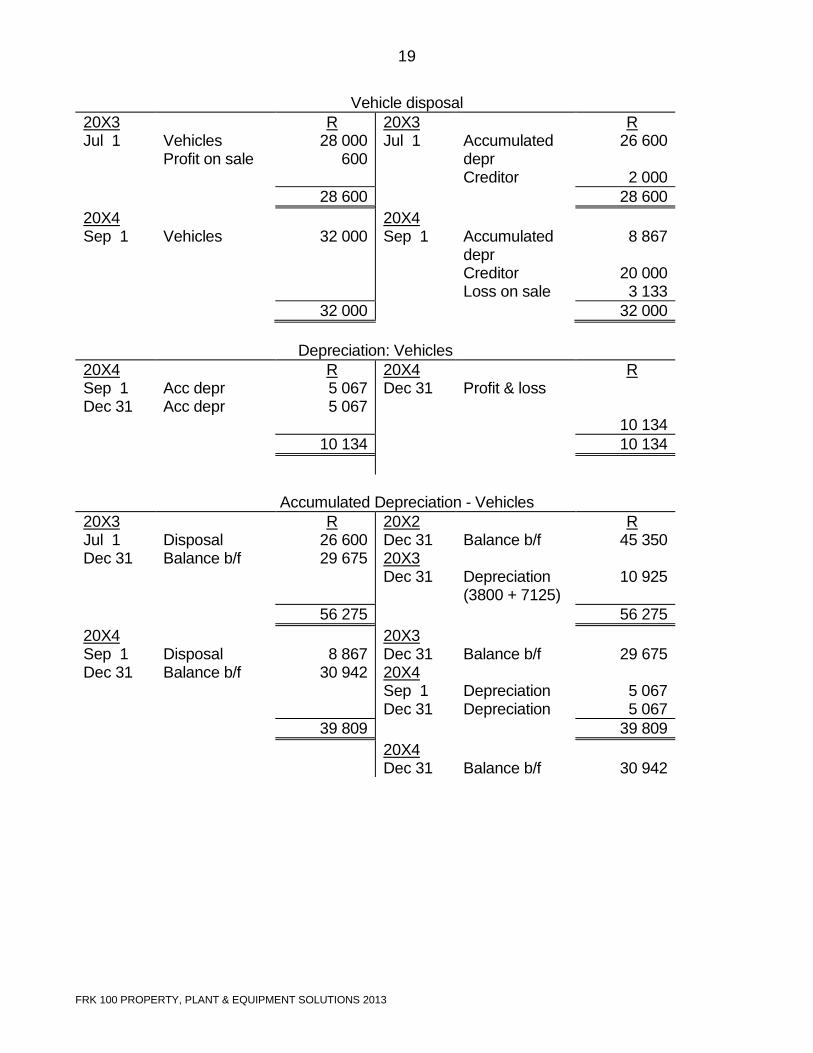

QUESTION 10 SUGGESTED SOLUTION V LISTER Calculations R28 000 – (5% x 28 000) = R26 600 at 25% per year = R6 650 per year Vehicles sold 02/01/19X9 31/12/19X9 31/12/20X0 31/12/20X1 31/12/20X2 01/07/20X3

Cost price R

28 000

Depreciation R

- 6 650 6 650 6 650 6 650

-

Accumulated depr

R -

6 650 13 300 19 950 26 600

- R32 000 – (5% x 32 000) = R30 400 at 25% per year = R7 600 per year 01/07/20X3 31/12/20X3

32 000

-

3 800

6/12

-

3 800 01/09/20X4 5 067 8/12 8 867

R

2. 31/12/20X2 Sold

58 000 (28 000) 30 000

Accumulated Depreciation Sold

45 350 (26 600) 18 750

25% per year on R(30 000 – [5% x 30 000]) = R7 125 per year. R18 750 7 125 = 2,63 Vehicle is 2 years and 8 months old (rounded). Purchase date - 1 May 20X0 (31/12/20X2 - 31/12/20X1 - 31/12/20X0 - 1/5/20X0)

18

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

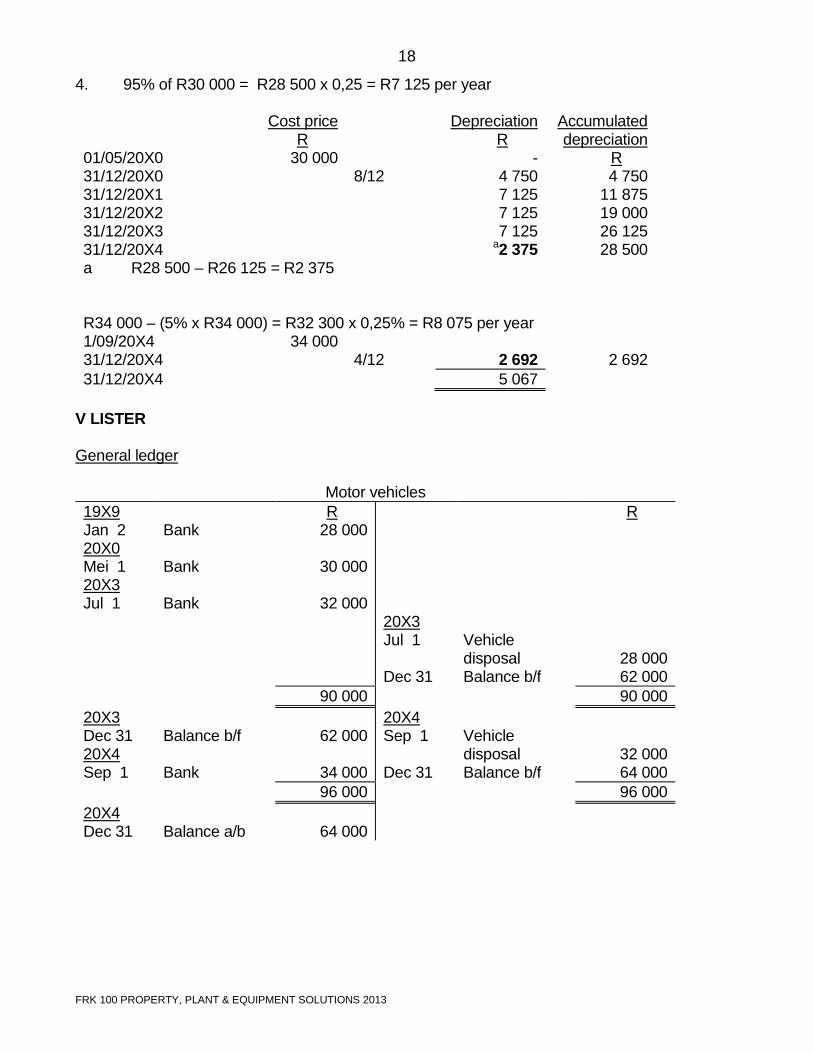

4. 95% of R30 000 = R28 500 x 0,25 = R7 125 per year 01/05/20X0 31/12/20X0 31/12/20X1 31/12/20X2 31/12/20X3 31/12/20X4

Cost price R

30 000

8/12

Depreciation R

- 4 750 7 125 7 125 7 125

a2 375

Accumulated depreciation

R 4 750

11 875 19 000 26 125 28 500

a R28 500 – R26 125 = R2 375

R34 000 – (5% x R34 000) = R32 300 x 0,25% = R8 075 per year 1/09/20X4 31/12/20X4

34 000 4/12

2 692

2 692

31/12/20X4 5 067 V LISTER General ledger Motor vehicles 19X9 Jan 2 20X0 Mei 1 20X3 Jul 1

Bank Bank Bank

R 28 000

30 000

32 000

R

20X3 Jul 1 Dec 31

Vehicle disposal Balance b/f

28 000 62 000

90 000 90 000 20X3 Dec 31 20X4 Sep 1

Balance b/f Bank

62 000

34 000

20X4 Sep 1 Dec 31

Vehicle disposal Balance b/f

32 000 64 000

96 000 96 000 20X4 Dec 31

Balance a/b

64 000

19

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

Vehicle disposal

20X3 Jul 1

Vehicles Profit on sale

R 28 000

600

20X3 Jul 1

Accumulated depr Creditor

R 26 600

2 000

28 600 28 600 20X4 Sep 1

Vehicles

32 000

20X4 Sep 1

Accumulated depr Creditor Loss on sale

8 867

20 000 3 133

32 000 32 000 Depreciation: Vehicles 20X4 Sep 1 Dec 31

Acc depr Acc depr

R 5 067 5 067

20X4 Dec 31

Profit & loss

R

10 134 10 134 10 134

Accumulated Depreciation - Vehicles

20X3 Jul 1 Dec 31

Disposal Balance b/f

R 26 600 29 675

20X2 Dec 31 20X3 Dec 31

Balance b/f Depreciation (3800 + 7125)

R 45 350

10 925

56 275 56 275 20X4 Sep 1 Dec 31

Disposal Balance b/f

8 867

30 942

20X3 Dec 31 20X4 Sep 1 Dec 31

Balance b/f Depreciation Depreciation

29 675

5 067 5 067

39 809 39 809 20X4

Dec 31 Balance b/f

30 942

20

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

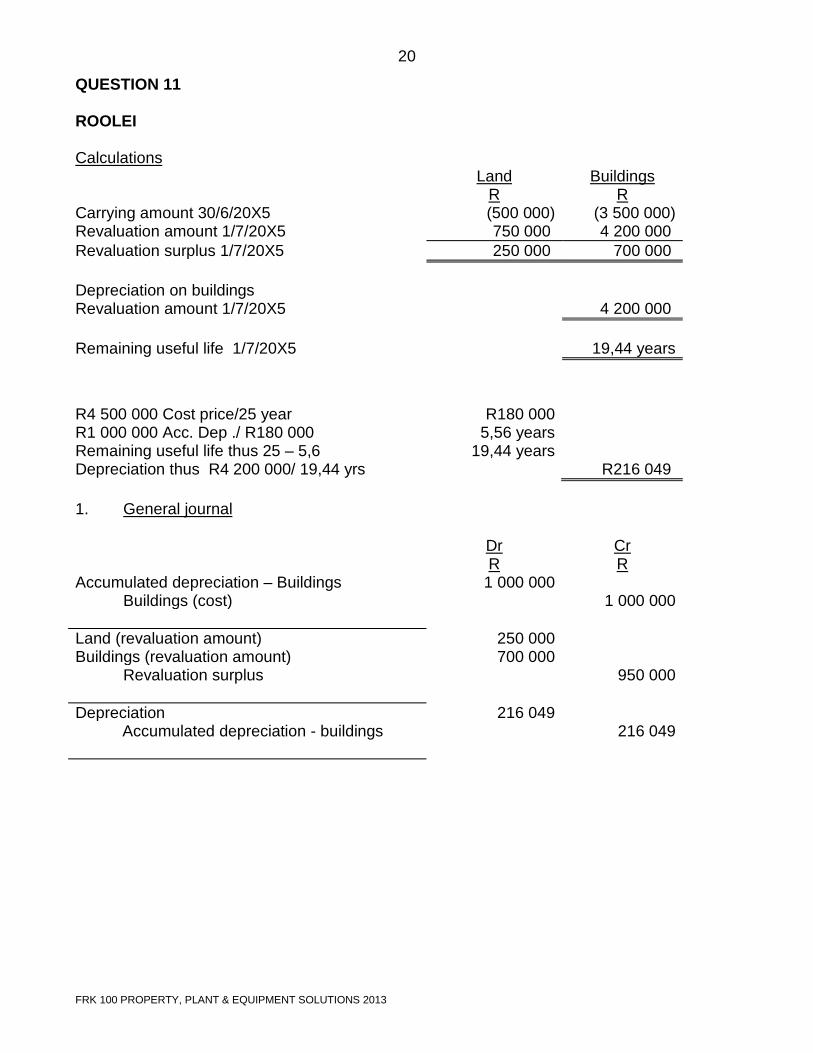

QUESTION 11 ROOLEI Calculations Land Buildings R R Carrying amount 30/6/20X5 (500 000) (3 500 000) Revaluation amount 1/7/20X5 750 000 4 200 000 Revaluation surplus 1/7/20X5 250 000 700 000 Depreciation on buildings Revaluation amount 1/7/20X5 4 200 000 Remaining useful life 1/7/20X5

19,44 years

R4 500 000 Cost price/25 year R180 000 R1 000 000 Acc. Dep ./ R180 000 5,56 years Remaining useful life thus 25 – 5,6 19,44 years Depreciation thus R4 200 000/ 19,44 yrs R216 049 1. General journal Dr Cr R R Accumulated depreciation – Buildings Buildings (cost)

1 000 000 1 000 000

Land (revaluation amount) 250 000 Buildings (revaluation amount) 700 000 Revaluation surplus 950 000 Depreciation 216 049 Accumulated depreciation - buildings 216 049

21

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

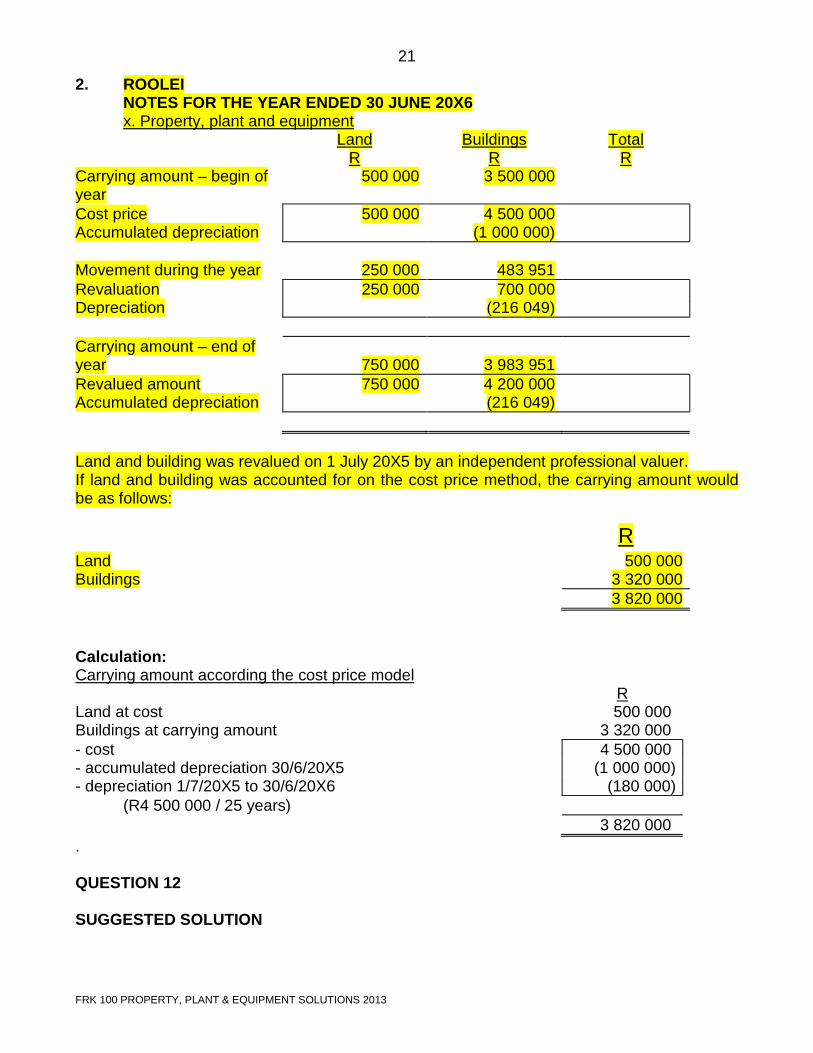

2. ROOLEI NOTES FOR THE YEAR ENDED 30 JUNE 20X6 x. Property, plant and equipment

Land Buildings Total R R R Carrying amount – begin of year

500 000 3 500 000

Cost price 500 000 4 500 000 Accumulated depreciation (1 000 000) Movement during the year

250 000

483 951

Revaluation 250 000 700 000 Depreciation (216 049) Carrying amount – end of year

750 000

3 983 951

Revalued amount 750 000 4 200 000 Accumulated depreciation (216 049) Land and building was revalued on 1 July 20X5 by an independent professional valuer. If land and building was accounted for on the cost price method, the carrying amount would be as follows:

R Land 500 000 Buildings 3 320 000 3 820 000 Calculation: Carrying amount according the cost price model R Land at cost 500 000 Buildings at carrying amount 3 320 000 - cost 4 500 000 - accumulated depreciation 30/6/20X5 (1 000 000) - depreciation 1/7/20X5 to 30/6/20X6 (180 000) (R4 500 000 / 25 years) 3 820 000 . QUESTION 12 SUGGESTED SOLUTION

22

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

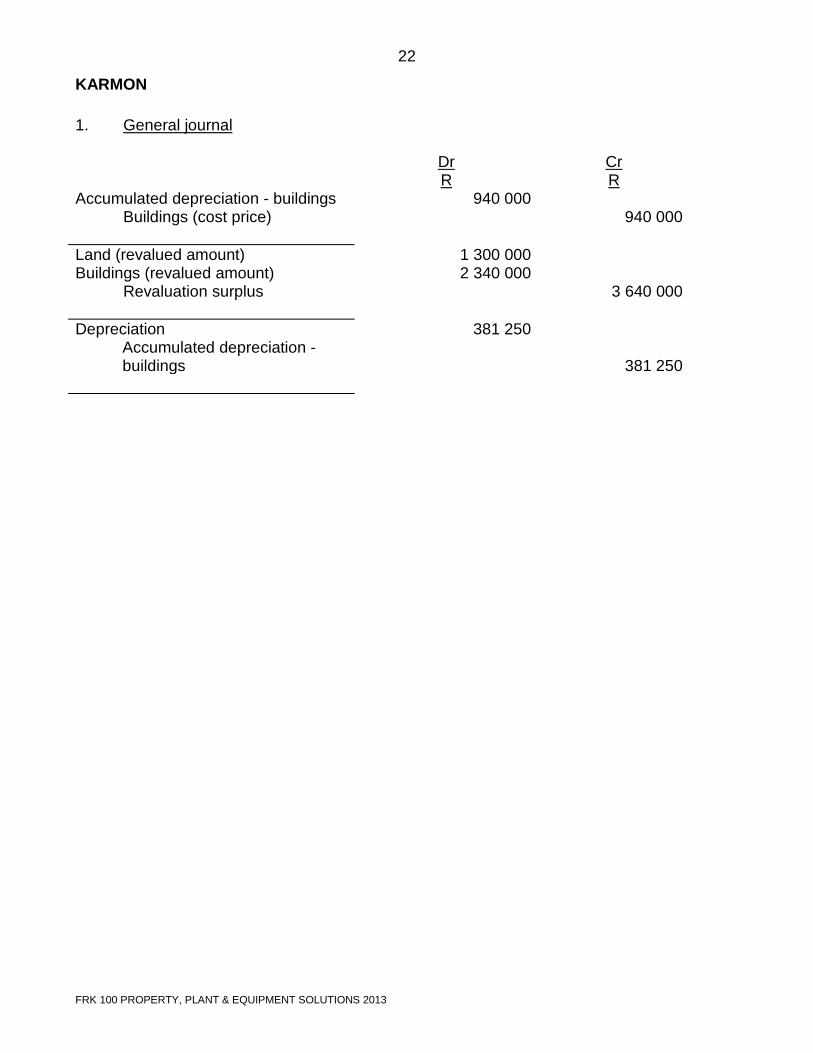

KARMON 1. General journal Dr Cr R R Accumulated depreciation - buildings Buildings (cost price)

940 000 940 000

Land (revalued amount) 1 300 000 Buildings (revalued amount) 2 340 000 Revaluation surplus 3 640 000 Depreciation 381 250 Accumulated depreciation -

buildings

381 250

23

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

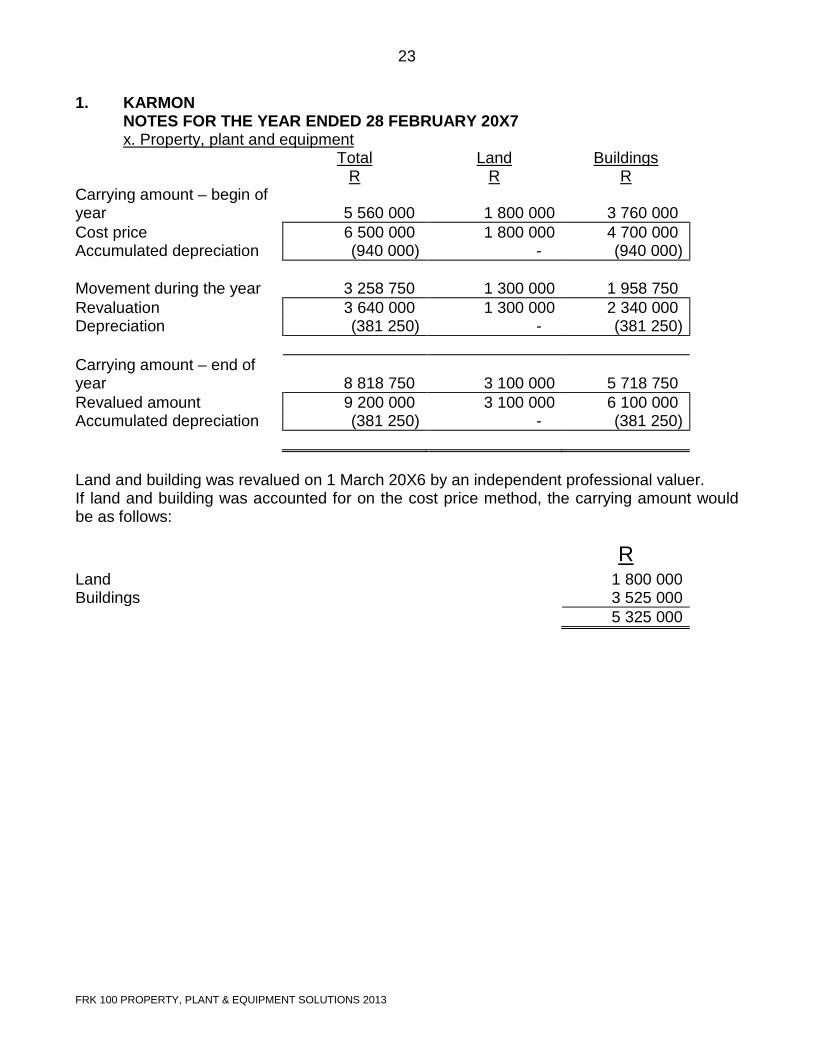

1. KARMON

NOTES FOR THE YEAR ENDED 28 FEBRUARY 20X7 x. Property, plant and equipment

Total Land Buildings R R R Carrying amount – begin of year

5 560 000

1 800 000

3 760 000

Cost price 6 500 000 1 800 000 4 700 000 Accumulated depreciation (940 000) - (940 000) Movement during the year

3 258 750

1 300 000

1 958 750

Revaluation 3 640 000 1 300 000 2 340 000 Depreciation (381 250) - (381 250) Carrying amount – end of year

8 818 750

3 100 000

5 718 750

Revalued amount 9 200 000 3 100 000 6 100 000 Accumulated depreciation (381 250) - (381 250) Land and building was revalued on 1 March 20X6 by an independent professional valuer. If land and building was accounted for on the cost price method, the carrying amount would be as follows:

R Land 1 800 000 Buildings 3 525 000 5 325 000

24

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

Calculations 1. Revaluation surplus and depreciation Land Buildings Accumulated Cost price/

Revalued amount Depreciation

R R R Purchases 1/3/20X2 1 800 000 4 700 000 Depreciation - 940 000 1/3/20X2 – 28/3/20x6 R4 700 000/20 years x 4 years

Accumulated depreciation set off against gross carrying amount on date of valuation

(940 000)

(940 000) Carrying amount 1/3/20X6 1 800 000 3 760 000 - Revalued amount 3 100 000 6 100 000 Revaluation surplus 1 300 000 2 340 000 Revalued amount 3 100 000 6 100 000 R6100000/(20 – 4 years) (381 250) 381 250 Carrying amount 28/2/20X7 3 100 000 5 718 750 381 250 2. Carrying amount – cost model R Land at cost 1 800 000 Buildings 3 525 000 Carrying amount on 1/3/20X6 3 760 000 Depreciation – 28/2/20X7 (235 000) (4 700 000/20 years) 5 325 000

25

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

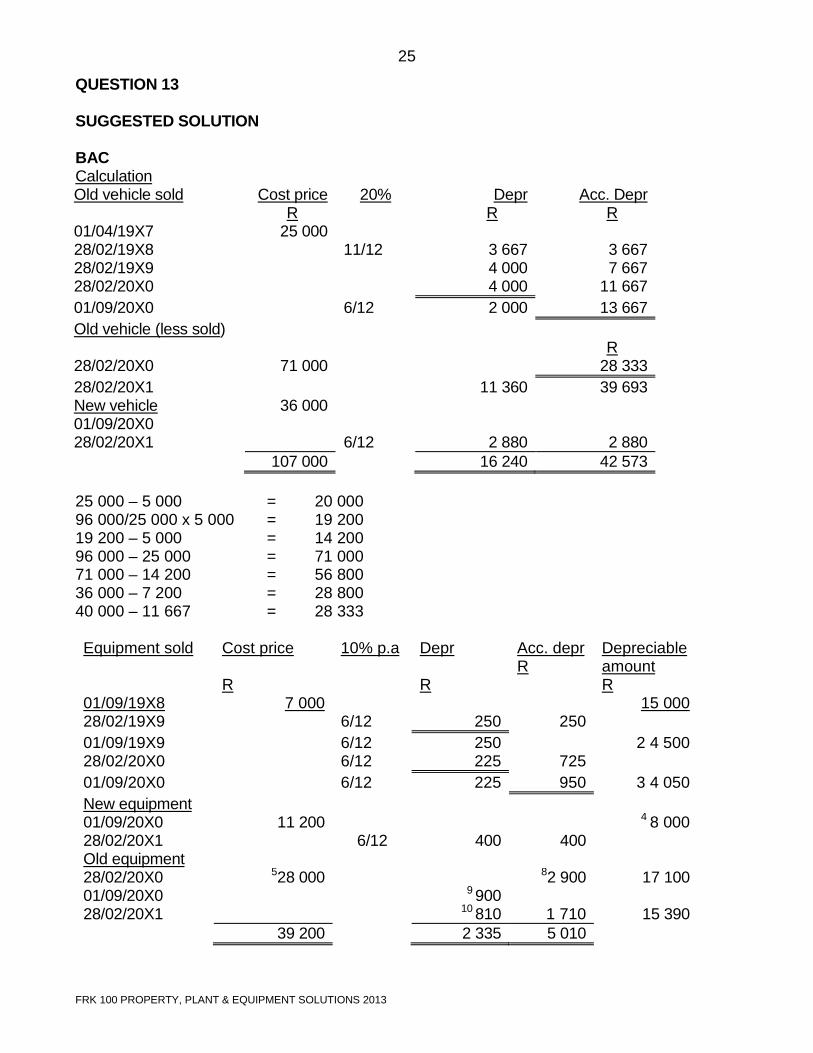

QUESTION 13 SUGGESTED SOLUTION BAC Calculation Old vehicle sold 01/04/19X7 28/02/19X8 28/02/19X9 28/02/20X0

Cost price R

25 000

20% 11/12

Depr R

3 667 4 000 4 000

Acc. Depr R

3 667 7 667

11 667 01/09/20X0 6/12 2 000 13 667 Old vehicle (less sold) 28/02/20X0

71 000

R

28 333 28/02/20X1 11 360 39 693 New vehicle 01/09/20X0 28/02/20X1

36 000 6/12

2 880

2 880 107 000 16 240 42 573 25 000 – 5 000 = 20 000 96 000/25 000 x 5 000 = 19 200 19 200 – 5 000 = 14 200 96 000 – 25 000 = 71 000 71 000 – 14 200 = 56 800 36 000 – 7 200 = 28 800 40 000 – 11 667 = 28 333 Equipment sold 01/09/19X8

Cost price R

7 000

10% p.a

Depr R

Acc. depr R

Depreciable amount R

15 000 28/02/19X9 6/12 250 250 01/09/19X9 6/12 250 2 4 500 28/02/20X0 6/12 225 725 01/09/20X0 6/12 225 950 3 4 050 New equipment 01/09/20X0 11 200 4 8 000 28/02/20X1 6/12 400 400

Old equipment 28/02/20X0 528 000 82 900 17 100 01/09/20X0 9 900

28/02/20X1 10 810 1 710 15 390 39 200 2 335 5 010

26

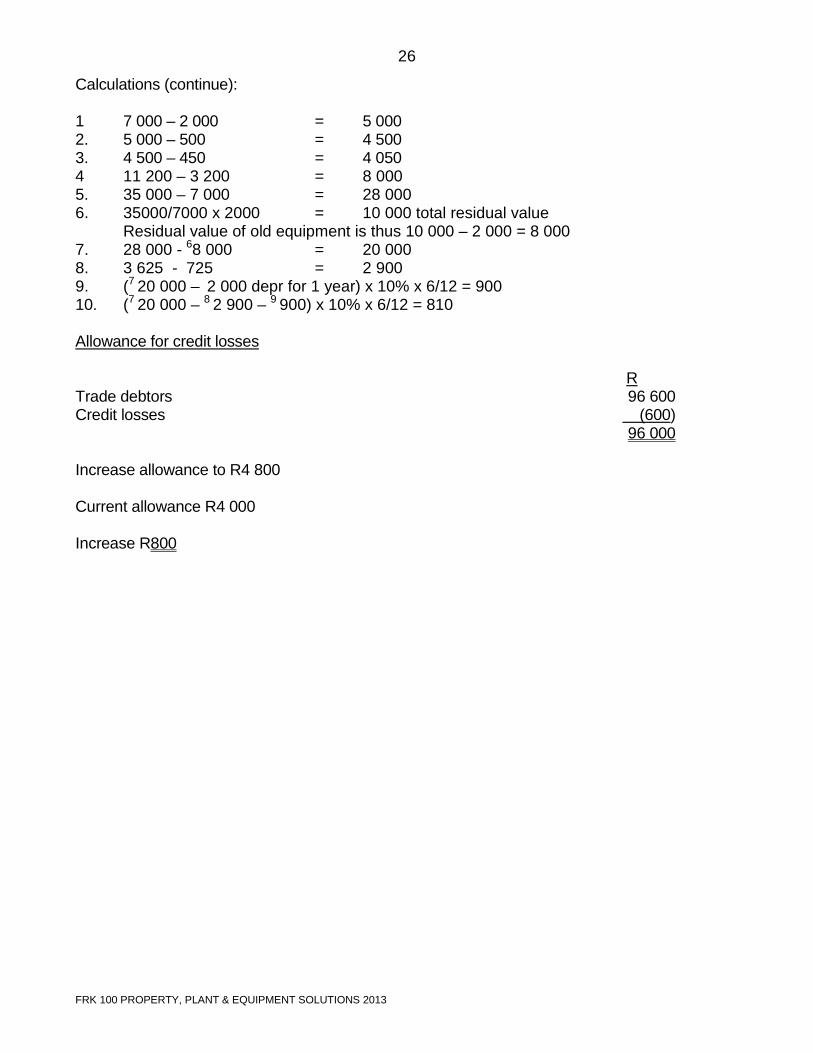

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

Calculations (continue): 1 7 000 – 2 000 = 5 000 2. 5 000 – 500 = 4 500 3. 4 500 – 450 = 4 050 4 11 200 – 3 200 = 8 000 5. 35 000 – 7 000 = 28 000 6. 35000/7000 x 2000 = 10 000 total residual value Residual value of old equipment is thus 10 000 – 2 000 = 8 000 7. 28 000 - 68 000 = 20 000 8. 3 625 - 725 = 2 900 9. (7 20 000 – 2 000 depr for 1 year) x 10% x 6/12 = 900 10. (7 20 000 – 8 2 900 – 9 900) x 10% x 6/12 = 810 Allowance for credit losses R Trade debtors 96 600 Credit losses (600) 96 000 Increase allowance to R4 800 Current allowance R4 000 Increase R800

27

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

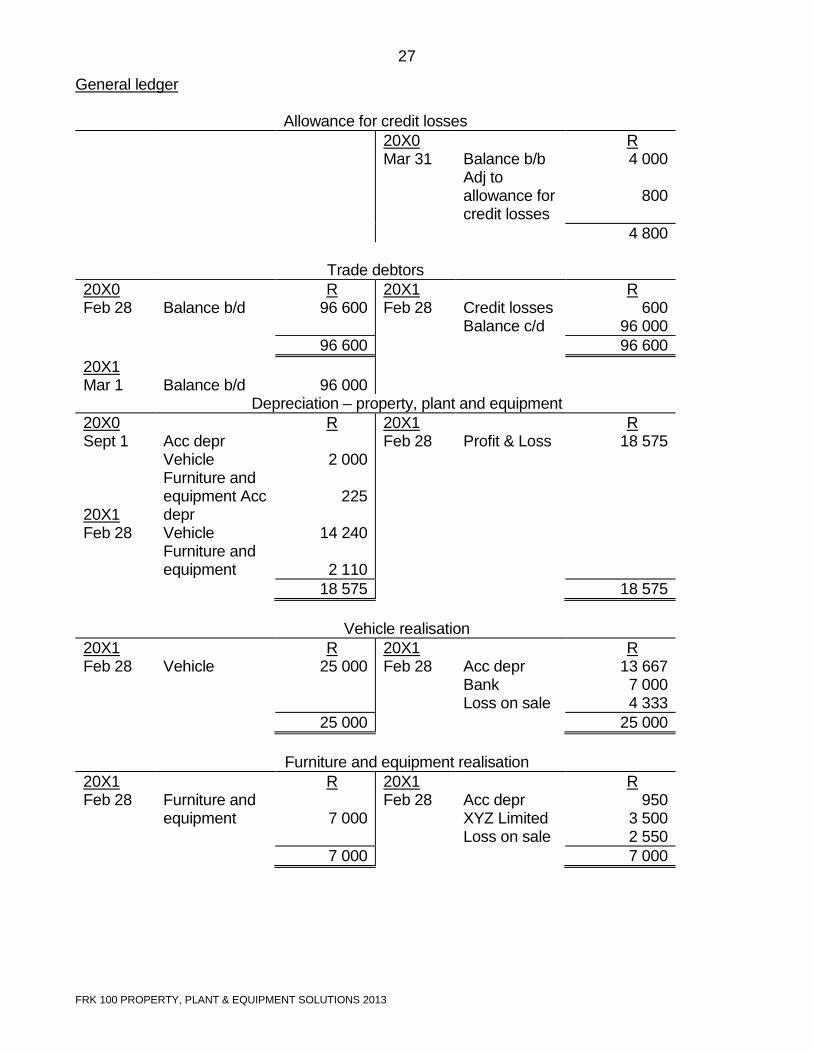

General ledger Allowance for credit losses

20X0 Mar 31

Balance b/b Adj to allowance for credit losses

R 4 000

800

4 800 Trade debtors 20X0 Feb 28

Balance b/d

R 96 600

20X1 Feb 28

Credit losses Balance c/d

R 600

96 000 96 600 96 600 20X1 Mar 1

Balance b/d

96 000

Depreciation – property, plant and equipment 20X0 Sept 1 20X1 Feb 28

Acc depr Vehicle Furniture and equipment Acc depr Vehicle Furniture and equipment

R

2 000

225

14 240

2 110

20X1 Feb 28

Profit & Loss

R 18 575

18 575 18 575

Vehicle realisation 20X1 Feb 28

Vehicle

R 25 000

20X1 Feb 28

Acc depr Bank Loss on sale

R 13 667 7 000 4 333

25 000 25 000

Furniture and equipment realisation 20X1 Feb 28

Furniture and equipment

R

7 000

20X1 Feb 28

Acc depr XYZ Limited Loss on sale

R 950

3 500 2 550

7 000 7 000

28

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

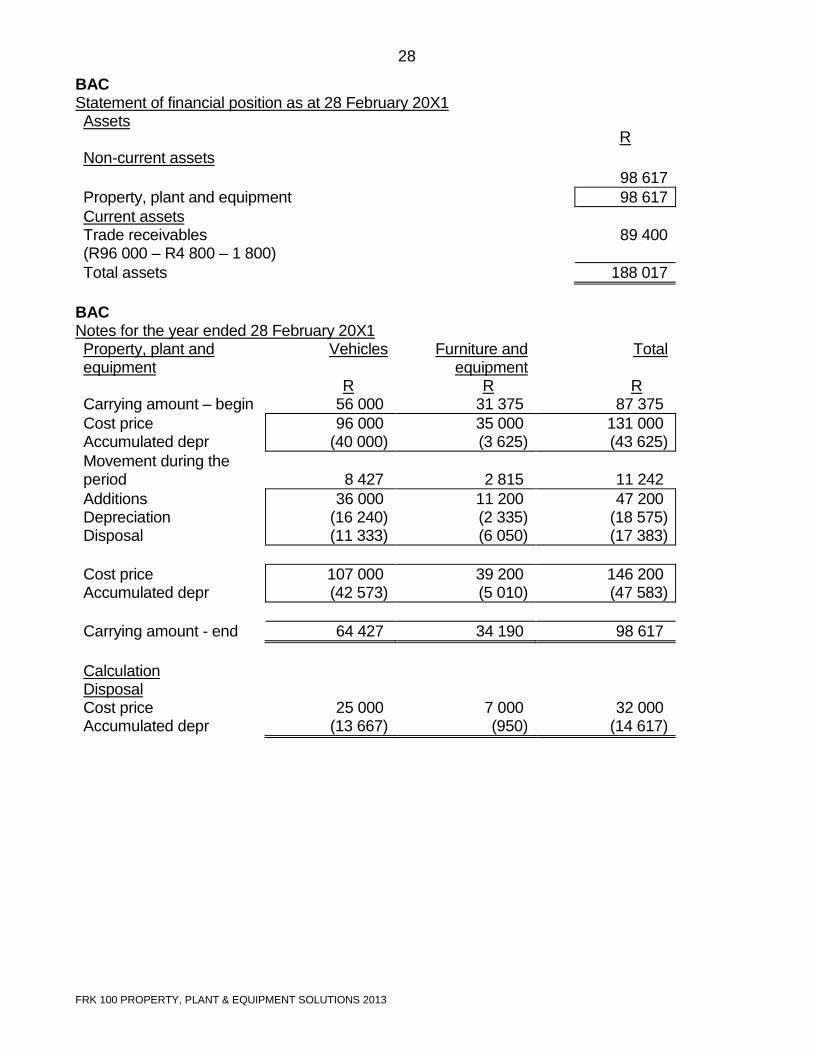

BAC Statement of financial position as at 28 February 20X1 Assets Non-current assets

R

98 617 Property, plant and equipment 98 617 Current assets Trade receivables (R96 000 – R4 800 – 1 800)

89 400

Total assets 188 017 BAC Notes for the year ended 28 February 20X1 Property, plant and equipment Carrying amount – begin

Vehicles

R 56 000

Furniture and equipment

R 31 375

Total

R 87 375

Cost price Accumulated depr

96 000 (40 000)

35 000 (3 625)

131 000 (43 625)

Movement during the period

8 427

2 815

11 242

Additions Depreciation Disposal

36 000 (16 240) (11 333)

11 200 (2 335) (6 050)

47 200 (18 575) (17 383)

Cost price Accumulated depr

107 000 (42 573)

39 200 (5 010)

146 200 (47 583)

Carrying amount - end 64 427 34 190 98 617

Calculation Disposal Cost price Accumulated depr

25 000 (13 667)

7 000 (950)

32 000 (14 617)

29

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

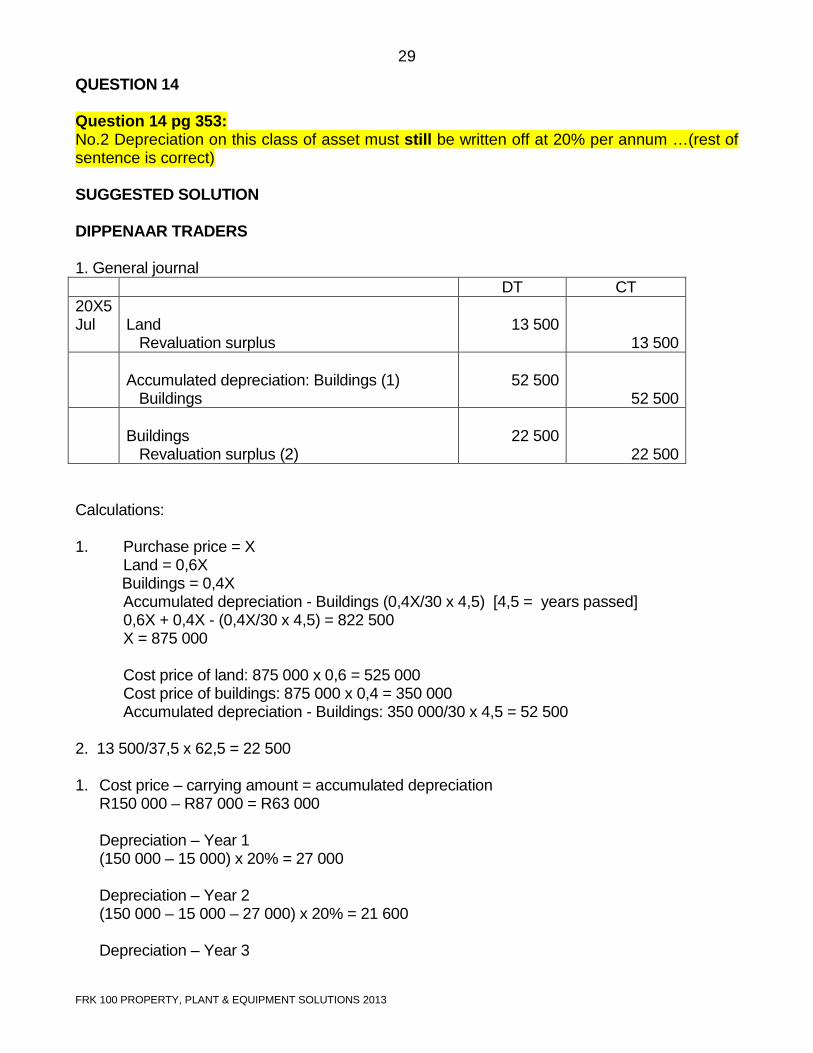

QUESTION 14 Question 14 pg 353: No.2 Depreciation on this class of asset must still be written off at 20% per annum …(rest of sentence is correct) SUGGESTED SOLUTION DIPPENAAR TRADERS 1. General journal DT CT 20X5 Jul

Land Revaluation surplus

13 500

13 500

Accumulated depreciation: Buildings (1) Buildings

52 500

52 500

Buildings Revaluation surplus (2)

22 500

22 500 Calculations: 1. Purchase price = X Land = 0,6X Buildings = 0,4X Accumulated depreciation - Buildings (0,4X/30 x 4,5) [4,5 = years passed] 0,6X + 0,4X - (0,4X/30 x 4,5) = 822 500 X = 875 000 Cost price of land: 875 000 x 0,6 = 525 000 Cost price of buildings: 875 000 x 0,4 = 350 000 Accumulated depreciation - Buildings: 350 000/30 x 4,5 = 52 500 2. 13 500/37,5 x 62,5 = 22 500 1. Cost price – carrying amount = accumulated depreciation

R150 000 – R87 000 = R63 000 Depreciation – Year 1 (150 000 – 15 000) x 20% = 27 000 Depreciation – Year 2 (150 000 – 15 000 – 27 000) x 20% = 21 600 Depreciation – Year 3

30

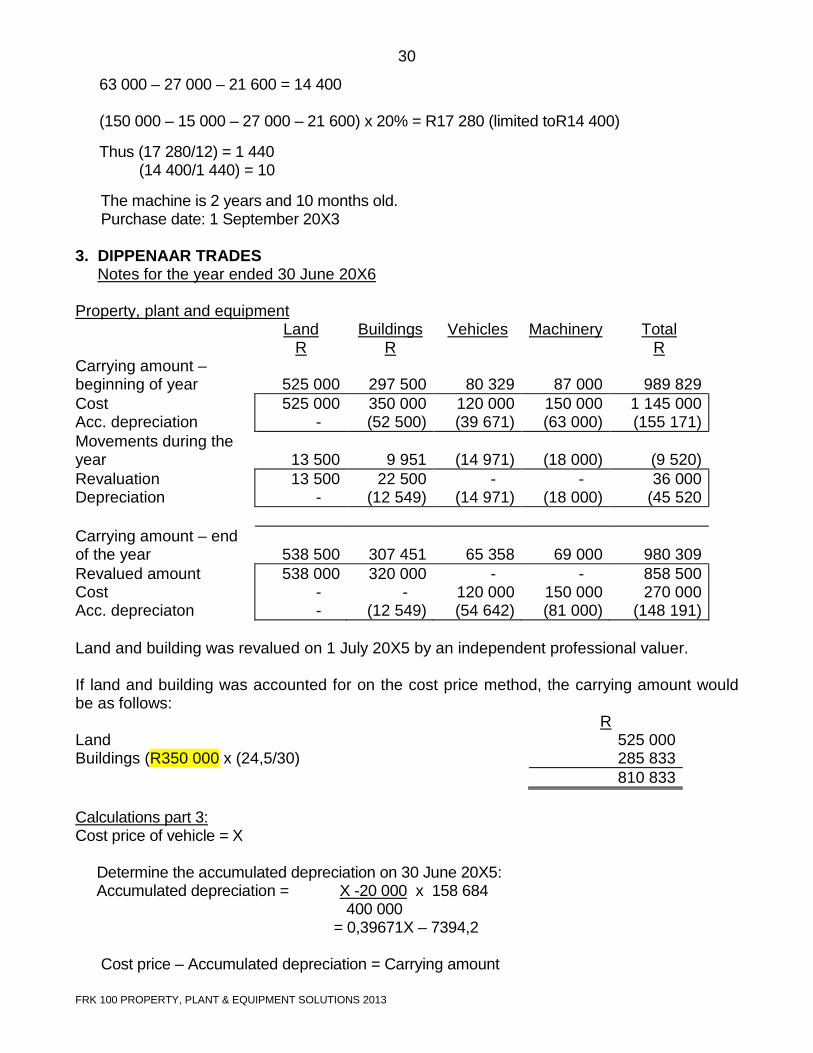

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

63 000 – 27 000 – 21 600 = 14 400 (150 000 – 15 000 – 27 000 – 21 600) x 20% = R17 280 (limited toR14 400) Thus (17 280/12) = 1 440

(14 400/1 440) = 10 The machine is 2 years and 10 months old. Purchase date: 1 September 20X3 3. DIPPENAAR TRADES Notes for the year ended 30 June 20X6 Property, plant and equipment Land Buildings Vehicles Machinery Total R R R Carrying amount – beginning of year

525 000

297 500

80 329

87 000

989 829

Cost 525 000 350 000 120 000 150 000 1 145 000 Acc. depreciation - (52 500) (39 671) (63 000) (155 171) Movements during the year

13 500

9 951

(14 971)

(18 000)

(9 520)

Revaluation 13 500 22 500 - - 36 000 Depreciation - (12 549) (14 971) (18 000) (45 520 Carrying amount – end of the year

538 500

307 451

65 358

69 000

980 309

Revalued amount 538 000 320 000 - - 858 500 Cost - - 120 000 150 000 270 000 Acc. depreciaton - (12 549) (54 642) (81 000) (148 191) Land and building was revalued on 1 July 20X5 by an independent professional valuer. If land and building was accounted for on the cost price method, the carrying amount would be as follows:

R Land 525 000 Buildings (R350 000 x (24,5/30) 285 833

810 833 Calculations part 3: Cost price of vehicle = X Determine the accumulated depreciation on 30 June 20X5: Accumulated depreciation = X -20 000 x 158 684 400 000 = 0,39671X – 7394,2 Cost price – Accumulated depreciation = Carrying amount

31

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

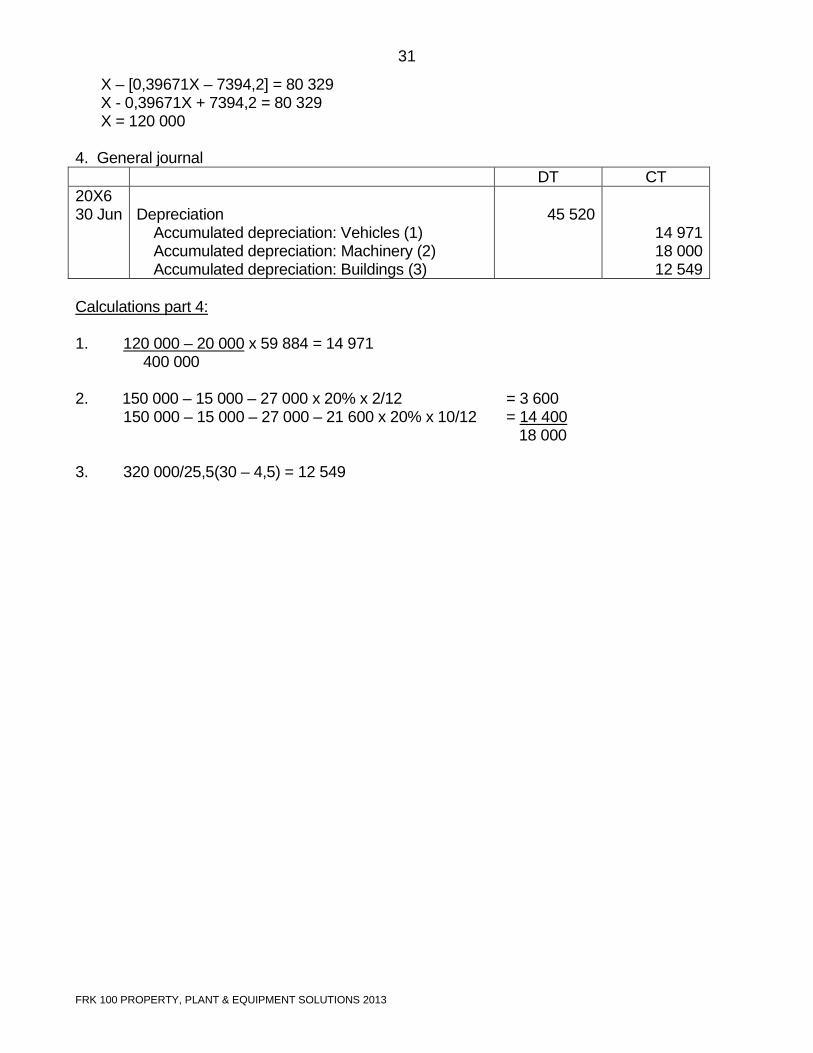

X – [0,39671X – 7394,2] = 80 329 X - 0,39671X + 7394,2 = 80 329 X = 120 000 4. General journal DT CT 20X6 30 Jun

Depreciation Accumulated depreciation: Vehicles (1) Accumulated depreciation: Machinery (2) Accumulated depreciation: Buildings (3)

45 520

14 971 18 000 12 549

Calculations part 4: 1. 120 000 – 20 000 x 59 884 = 14 971 400 000 2. 150 000 – 15 000 – 27 000 x 20% x 2/12 = 3 600 150 000 – 15 000 – 27 000 – 21 600 x 20% x 10/12 = 14 400 18 000 3. 320 000/25,5(30 – 4,5) = 12 549

32

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

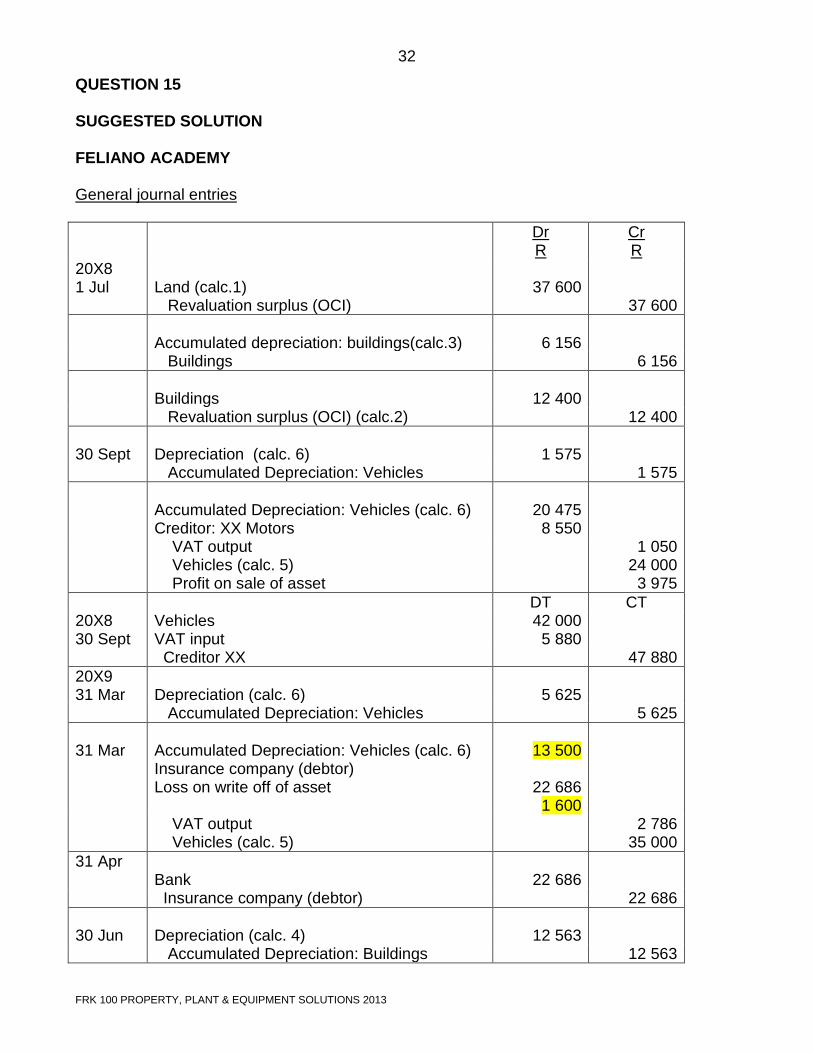

QUESTION 15 SUGGESTED SOLUTION FELIANO ACADEMY General journal entries Dr

R Cr R

20X8 1 Jul

Land (calc.1)

37 600

Revaluation surplus (OCI) 37 600

Accumulated depreciation: buildings(calc.3)

6 156

Buildings 6 156

Buildings

12 400

Revaluation surplus (OCI) (calc.2) 12 400 30 Sept

Depreciation (calc. 6)

1 575

Accumulated Depreciation: Vehicles 1 575

Accumulated Depreciation: Vehicles (calc. 6) Creditor: XX Motors

20 475

8 550

VAT output Vehicles (calc. 5) Profit on sale of asset

1 050 24 000

3 975 DT CT 20X8 30 Sept

Vehicles VAT input

42 000 5 880

Creditor XX 47 880 20X9 31 Mar

Depreciation (calc. 6)

5 625

Accumulated Depreciation: Vehicles 5 625 31 Mar

Accumulated Depreciation: Vehicles (calc. 6) Insurance company (debtor) Loss on write off of asset

13 500

22 686

1 600

VAT output Vehicles (calc. 5)

2 786 35 000

31 Apr Bank

22 686

Insurance company (debtor) 22 686 30 Jun

Depreciation (calc. 4)

12 563

Accumulated Depreciation: Buildings 12 563

33

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

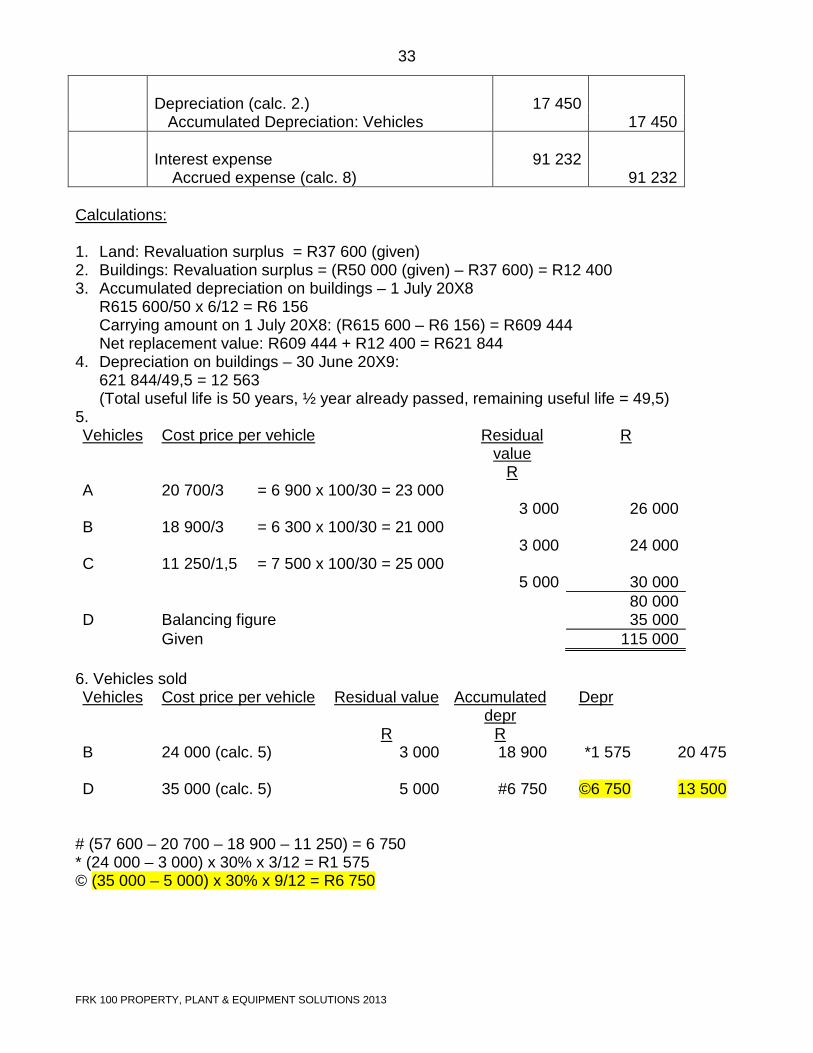

Depreciation (calc. 2.)

17 450

Accumulated Depreciation: Vehicles 17 450

Interest expense

91 232

Accrued expense (calc. 8) 91 232 Calculations: 1. Land: Revaluation surplus = R37 600 (given) 2. Buildings: Revaluation surplus = (R50 000 (given) – R37 600) = R12 400 3. Accumulated depreciation on buildings – 1 July 20X8

R615 600/50 x 6/12 = R6 156 Carrying amount on 1 July 20X8: (R615 600 – R6 156) = R609 444 Net replacement value: R609 444 + R12 400 = R621 844

4. Depreciation on buildings – 30 June 20X9: 621 844/49,5 = 12 563 (Total useful life is 50 years, ½ year already passed, remaining useful life = 49,5)

5. Vehicles Cost price per vehicle Residual

value R

R A 20 700/3 = 6 900 x 100/30 = 23 000

3 000

26 000 B 18 900/3 = 6 300 x 100/30 = 21 000

3 000

24 000 C 11 250/1,5 = 7 500 x 100/30 = 25 000

5 000

30 000 80 000 D Balancing figure 35 000 Given 115 000

6. Vehicles sold Vehicles Cost price per vehicle Residual value Accumulated

depr Depr

R R B 24 000 (calc. 5) 3 000 18 900 *1 575 20 475 D 35 000 (calc. 5) 5 000 #6 750 ©6 750 13 500

# (57 600 – 20 700 – 18 900 – 11 250) = 6 750 * (24 000 – 3 000) x 30% x 3/12 = R1 575 © (35 000 – 5 000) x 30% x 9/12 = R6 750

34

FRK 100 PROPERTY, PLANT & EQUIPMENT SOLUTIONS 2013

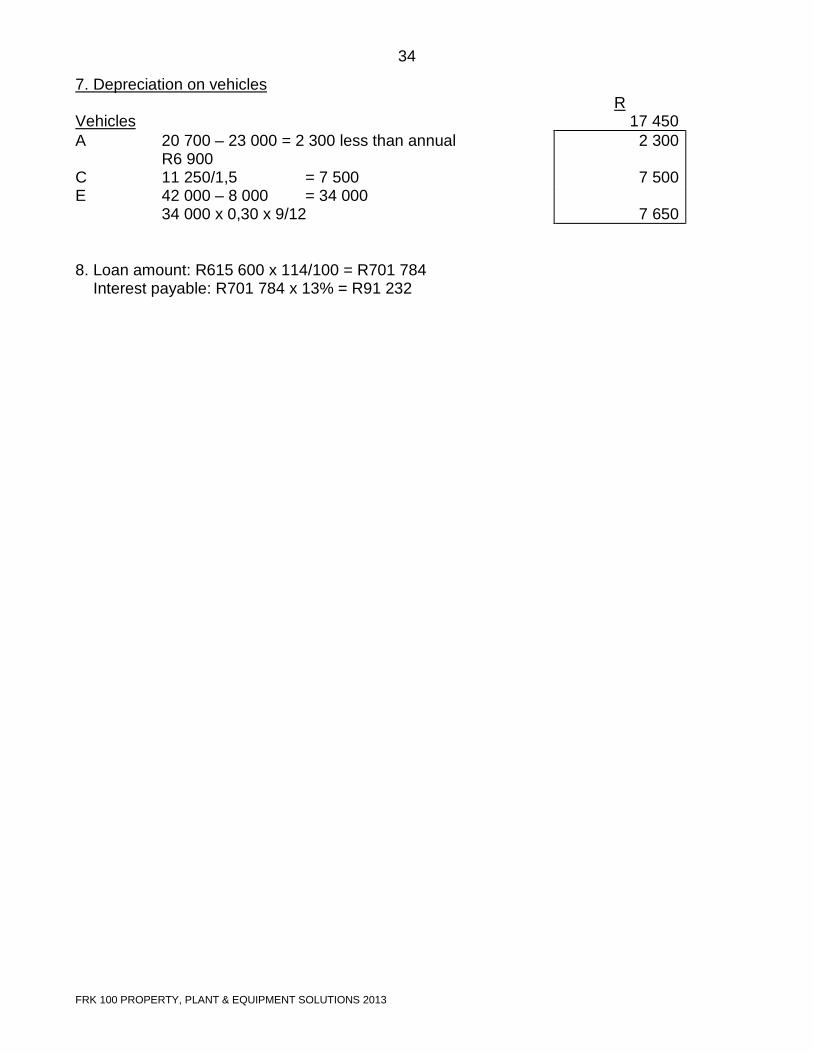

7. Depreciation on vehicles R Vehicles 17 450 A 20 700 – 23 000 = 2 300 less than annual

R6 900 2 300

C 11 250/1,5 = 7 500 7 500 E 42 000 – 8 000 = 34 000

34 000 x 0,30 x 9/12

7 650 8. Loan amount: R615 600 x 114/100 = R701 784 Interest payable: R701 784 x 13% = R91 232