Embed Size (px)

DESCRIPTION

Chapter 11. Merchandise Sales and Accounts Receivable. LO1. Learning Objective 1 Analyze and record transactions for merchandise sales. Merchandising companies sell products , also called goods. They can be either wholesalers or retailers. Manufacturer. Wholesaler. Retailer. - PowerPoint PPT Presentation

Citation preview

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Chapter 11

Merchandise

Sales and Accounts

Receivable

11-11-22

Manufacturer Wholesaler Retailer Customer

Learning Objective 1Analyze and record transactions for merchandise sales.

Merchandising companies sell Merchandising companies sell productsproducts,, also called also called goods. They can be either wholesalers or retailers.goods. They can be either wholesalers or retailers.

Merchandising companies sell Merchandising companies sell productsproducts,, also called also called goods. They can be either wholesalers or retailers.goods. They can be either wholesalers or retailers.

Sales Revenue– Cost of Goods SoldGross Profit– Selling and Administrative ExpensesIncome

Sales Revenue– Cost of Goods SoldGross Profit– Selling and Administrative ExpensesIncome

LO1

11-11-33

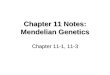

Merchandising Sales

On November 3, Z-Mart sold $5,400 On November 3, Z-Mart sold $5,400 of merchandise on account.of merchandise on account.

We record the sale entry as follows:We record the sale entry as follows:

On November 3, Z-Mart sold $5,400 On November 3, Z-Mart sold $5,400 of merchandise on account.of merchandise on account.

We record the sale entry as follows:We record the sale entry as follows:

LO1

11-11-44

2/10,n/302/10,n/30Discount Percent

Discount Percent

Number of Days

Discount Is Available

Number of Days

Discount Is Available

Otherwise, Net (or All) Is Due in 30

Days

Otherwise, Net (or All) Is Due in 30

Days

CreditPeriod

CreditPeriod

Learning Objective 2Describe how to compute and record sales discounts.

This is what a typical sales discount will look like.

LO2

11-11-55

Nov. 12 Accounts Receivable 1,000 Sales 1,000

Sales of merchandise on credit

Sales DiscountsOn November 12, Z-Mart On November 12, Z-Mart

sold $1,000 sold $1,000 of merchandise on account of merchandise on account

with termswith termsof 2/10,n/60.of 2/10,n/60.

We record the sale entry We record the sale entry as follows:as follows:

On November 12, Z-Mart On November 12, Z-Mart sold $1,000 sold $1,000

of merchandise on account of merchandise on account with termswith terms

of 2/10,n/60.of 2/10,n/60.

We record the sale entry We record the sale entry as follows:as follows:

On January 11, Z-Mart On January 11, Z-Mart received a check from the received a check from the

customer for $1,000, the full customer for $1,000, the full amount of the sale made on amount of the sale made on

November 12.November 12.

We record the cash receipt We record the cash receipt as follows:as follows:

On January 11, Z-Mart On January 11, Z-Mart received a check from the received a check from the

customer for $1,000, the full customer for $1,000, the full amount of the sale made on amount of the sale made on

November 12.November 12.

We record the cash receipt We record the cash receipt as follows:as follows:

Jan. 11 Cash 1,000 Accounts Receivable 1,000

Received payment in full for Nov. 12 sale

LO2

11-11-66

Nov. 22 Cash 980 Sales Discount 20

Accounts Receivable 1,000 Received payment less discount for Nov. 12 sale

Instead of waiting 60 days, if the customer Instead of waiting 60 days, if the customer had paid within the 10-day discount period had paid within the 10-day discount period

(on or before November 22), we would record (on or before November 22), we would record the cash receipt as follows:the cash receipt as follows:

Instead of waiting 60 days, if the customer Instead of waiting 60 days, if the customer had paid within the 10-day discount period had paid within the 10-day discount period

(on or before November 22), we would record (on or before November 22), we would record the cash receipt as follows:the cash receipt as follows:

Sales DiscountsLO2

11-11-77

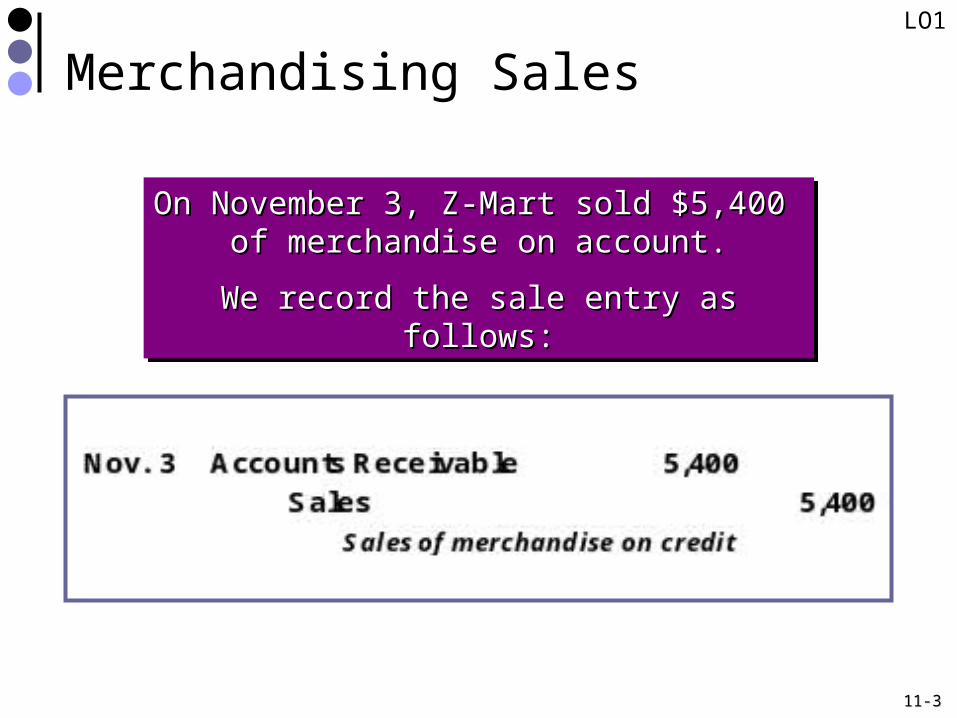

Learning Objective 3Explain how to record sales returns and allowances.

On November 3, Z-Mart sold On November 3, Z-Mart sold $2,400 $2,400

of merchandise on account. of merchandise on account. On November 6, the customer On November 6, the customer

returned $800 of this returned $800 of this merchandise.merchandise.

We record the return as We record the return as follows:follows:

On November 3, Z-Mart sold On November 3, Z-Mart sold $2,400 $2,400

of merchandise on account. of merchandise on account. On November 6, the customer On November 6, the customer

returned $800 of this returned $800 of this merchandise.merchandise.

We record the return as We record the return as follows:follows:

Nov. 6 Sales Returns and Allowances 800 Accounts Receivable 800

Customer returned merchandise

Now assume that the Now assume that the customer agreed to keep the customer agreed to keep the

$800 of defective merchandise $800 of defective merchandise because Z-Mart offers a $100 because Z-Mart offers a $100

price reduction.price reduction.

This is a sales allowance and This is a sales allowance and is recorded as follows:is recorded as follows:

Now assume that the Now assume that the customer agreed to keep the customer agreed to keep the

$800 of defective merchandise $800 of defective merchandise because Z-Mart offers a $100 because Z-Mart offers a $100

price reduction.price reduction.

This is a sales allowance and This is a sales allowance and is recorded as follows:is recorded as follows:

Nov. 6 Sales Returns and Allowances 100 Accounts Receivable 100

Customer returned merchandise

LO3

11-11-88

Recording and PostingMerchandise Sales

Nov. 3 Sold merchandise on credit to Bradford Inc.: Sales Invoice No. 145 for $2,400 plus $144 sales tax

5 Sold merchandise on credit to Smith Inc.:Sales Invoice No. 146 for $1,050 plus $63 sales tax

8 Sold merchandise on credit to Cluff Inc.: Sales Invoice No. 147 for $250 plus $15 sales tax

11 Sold merchandise on credit to Dobson Inc.: Sales Invoice No. 148 for $550 plus $33 sales tax

Nov. 3 Sold merchandise on credit to Bradford Inc.: Sales Invoice No. 145 for $2,400 plus $144 sales tax

5 Sold merchandise on credit to Smith Inc.:Sales Invoice No. 146 for $1,050 plus $63 sales tax

8 Sold merchandise on credit to Cluff Inc.: Sales Invoice No. 147 for $250 plus $15 sales tax

11 Sold merchandise on credit to Dobson Inc.: Sales Invoice No. 148 for $550 plus $33 sales tax

Z-Mart had the following transactions in early November:

Z-Mart had the following transactions in early November:

Nov. 3 Accounts Receivable 2,544 Sales Tax Payable 144 Sales 2,400

Nov. 5 Accounts Receivable 1,113 Sales Tax Payable 63 Sales 1,050

Nov. 8 Accounts Receivable 265 Sales Tax Payable 15 Sales 250

Nov. 11 Accounts Receivable 583 Sales Tax Payable 33 Sales 550

LO3

11-11-99

Learning Objective 4Describe the use of special journals and subsidiary ledgers.

GeneralGeneralJournalJournalGeneralGeneralJournalJournal

For transactionsFor transactionsnot in specialnot in special

journalsjournals

For transactionsFor transactionsnot in specialnot in special

journalsjournals

CashCashDisbursementsDisbursements

JournalJournal

CashCashDisbursementsDisbursements

JournalJournal

For recordingFor recordingcash paymentscash paymentsFor recordingFor recording

cash paymentscash payments

PurchasesPurchasesJournalJournal

PurchasesPurchasesJournalJournal

For recordingFor recordingcredit purchasescredit purchases

For recordingFor recordingcredit purchasescredit purchases

Cash ReceiptsCash ReceiptsJournalJournal

Cash ReceiptsCash ReceiptsJournalJournal

For recordingFor recordingcash receiptscash receiptsFor recordingFor recordingcash receiptscash receipts

Sales JournalSales JournalSales JournalSales Journal

For recordingFor recordingcredit salescredit sales

For recordingFor recordingcredit salescredit sales

LO4

11-11-1010

Page 3

Date Account DebitedInvoice Number PR

Accounts Receivable

Debit

Sales Tax Payable Credit

Sales Credit

Nov 3 Bradford Inc. 145 2,544 144 2,400

5 Smith Inc. 146 1,113 63 1,050

8 Cluff Inc. 147 265 15 250

11 Dobson Inc. 148 583 33 550

12 Taylor Inc. 149 1,431 81 1,350

15 Burns Inc. 150 636 36 600

17 Smith Inc. 151 1,484 84 1,400

23 Dobson Inc. 152 1,272 72 1,200

27 Taylor Inc. 153 318 18 300

SALES JOURNAL

Notice only sales on credit are recorded in the Sales Journal. Notice only sales on credit are recorded in the Sales Journal.

Learning Objective 5Journalize and post transactions using a sales journal.

LO5

11-11-1111

Accounts Receivable Subsidiary

Cluff Inc.

Date PR Debit Credit Balance

Nov. 8 S3 265 265

Accounts Receivable Subsidiary

Bradford Inc.

Date PR Debit Credit Balance

Nov. 3 S3 2,544 2,544

Accounts Receivable Subsidiary

Smith Inc.

Date PR Debit Credit Balance

Nov. 5 S3 1,113 1,113

17 S3 1,484 2,597

Learning Objective 6Prepare and prove the accuracy of the accounts receivable subsidiary ledger.

Page 3

Date Account DebitedInvoice Number PR

Accounts Receivable

Debit

Sales Tax Payable Credit

Sales Credit

Nov 3 Bradford Inc. 145 2,544 144 2,400

5 Smith Inc. 146 1,113 63 1,050

8 Cluff Inc. 147 265 15 250

11 Dobson Inc. 148 583 33 550

12 Taylor Inc. 149 1,431 81 1,350

15 Burns Inc. 150 636 36 600

17 Smith Inc. 151 1,484 84 1,400

23 Dobson Inc. 152 1,272 72 1,200

27 Taylor Inc. 153 318 18 300

30 Totals 9,646 546 9,100

SALES JOURNAL

After all items are posted, the balance in the Accounts Receivable general ledger must equal the sum of the balances of its customers’ accounts from the subsidiary ledgers.

LO6

11-11-1212

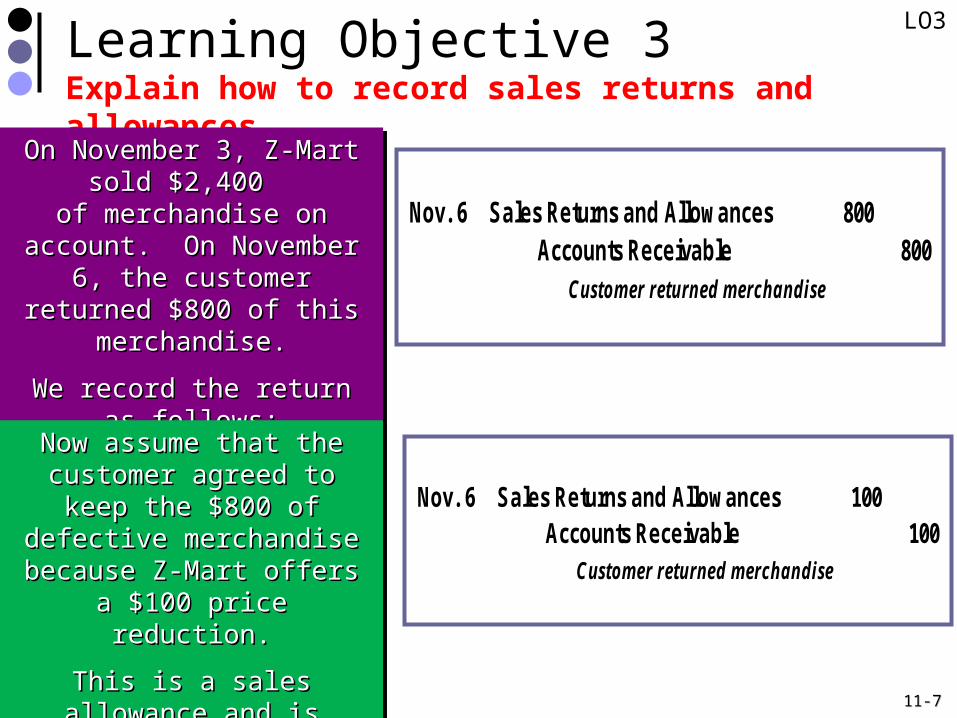

Page 3

Date Account DebitedInvoice Number PR

Accounts Receivable

Debit

Sales Tax Payable Credit

Sales Credit

Nov 3 Bradford Inc. 145 2,544 144 2,400

5 Smith Inc. 146 1,113 63 1,050

8 Cluff Inc. 147 265 15 250

11 Dobson Inc. 148 583 33 550

12 Taylor Inc. 149 1,431 81 1,350

15 Burns Inc. 150 636 36 600

17 Smith Inc. 151 1,484 84 1,400

23 Dobson Inc. 152 1,272 72 1,200

27 Taylor Inc. 153 318 18 300

30 Totals 9,646 546 9,100

(106) (232) (401)

SALES JOURNAL

Posting to General Ledger

The sales journal’s account columns are totaled at the end of each period and posted to the appropriate ledgers.

LO6

11-11-1313

Proving the LedgersSchedule of Accounts Receivable

November 30Bradford Inc. 2,544$ Smith Inc. 2,597 Cluff Inc. 265 Dobson Inc. 1,855 Taylor Inc. 1,749 Burns Inc. 636 Rytting Co. (pre November sales) 3,152 Total accounts receivable 12,798$

Schedule of Accounts ReceivableNovember 30

Bradford Inc. 2,544$ Smith Inc. 2,597 Cluff Inc. 265 Dobson Inc. 1,855 Taylor Inc. 1,749 Burns Inc. 636 Rytting Co. (pre November sales) 3,152 Total accounts receivable 12,798$

The Accounts Receivable controlling

account and the subsidiary ledger are in

balance.

LO6

11-11-1414

Cash Receipts Journal

Page 2

Date Account Credited Explanation PRCash Debit

Sales Discount

Debit

Accounts Receivable

CreditSales Credit

Other Accounts

CreditFeb 7 Sales Cash sales x 4,450 4,450

12 Jason Henry Invoice 307, 2/2 441 9 450 14 Sales Cash sales x 3,925 3,925 17 Albert Co. Invoice 308, 2/7 490 10 500 20 Notes Payable Note to bank 245 750 750 21 Sales Cash sales x 4,700 4,700 22 Interest Revenue Bank account 409 250 250 23 Kam Moore Invoice 309, 2/13 343 7 350 25 Paul Roth Invoice 310, 2/157 196 4 200 28 Sales Cash sales x 4,225 4,225 28 Totals 19,770 30 1,500 17,300 1,000

(101) (415) (106) (413) (X )

CASH RECEIPTS JOURNAL

Column totals postedCheck mark indicates immediateposting to accounts receivable

subsidiary ledger.

LO6

11-11-1515

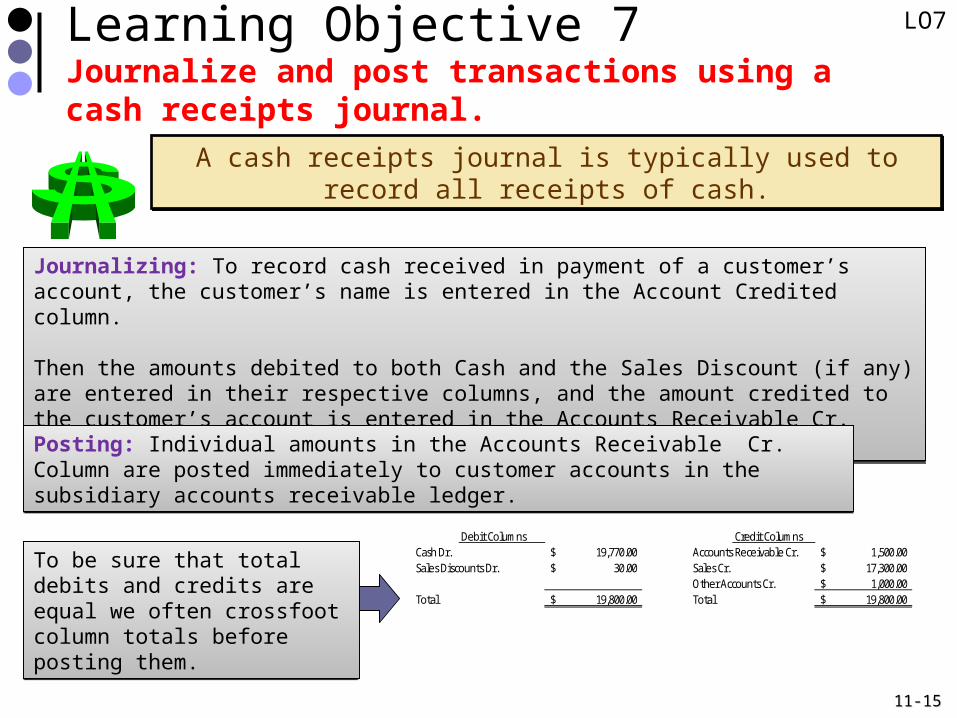

A cash receipts journal is typically used to record all receipts of cash.

A cash receipts journal is typically used to record all receipts of cash.

Learning Objective 7Journalize and post transactions using a cash receipts journal.

Journalizing: To record cash received in payment of a customer’s account, the customer’s name is entered in the Account Credited column.

Then the amounts debited to both Cash and the Sales Discount (if any) are entered in their respective columns, and the amount credited to the customer’s account is entered in the Accounts Receivable Cr. Column.

Journalizing: To record cash received in payment of a customer’s account, the customer’s name is entered in the Account Credited column.

Then the amounts debited to both Cash and the Sales Discount (if any) are entered in their respective columns, and the amount credited to the customer’s account is entered in the Accounts Receivable Cr. Column.

Posting: Individual amounts in the Accounts Receivable Cr. Column are posted immediately to customer accounts in the subsidiary accounts receivable ledger.Posting: Individual amounts in the Accounts Receivable Cr. Column are posted immediately to customer accounts in the subsidiary accounts receivable ledger.

To be sure that total debits and credits are equal we often crossfoot column totals before posting them.

To be sure that total debits and credits are equal we often crossfoot column totals before posting them.

Debit Columns Credit ColumnsCash Dr. 19,770.00$ Accounts Receivable Cr. 1,500.00$ Sales Discounts Dr. 30.00$ Sales Cr. 17,300.00$

Other Accounts Cr. 1,000.00$ Total 19,800.00$ Total 19,800.00$

LO7

11-11-1616

End of Chapter 11