Embed Size (px)

Citation preview

1

CHAPTER - 1

INTRODUCTION AND DESIGN OF THE THESIS

"A brand for a company is like a reputation for a person. You earn reputation by

trying to do hard things well."

Kenneth Blanchard

Introduction to Brand equity

A basic premise of brand equity is that the power of a brand lies in the minds of

consumers and what they have experienced and learned about the brand over time. Brand

equity can be thought of as the "added value" endowed to a product in the thoughts,

words, and actions of consumers. There are many different ways that this added value

can be created for a brand.

Similarly, there are also many different ways the value of a brand can be

manifested or exploited to benefit the firm (i.e., in terms of greater revenue and/or lower

costs). For brand equity to provide a useful strategic function and guide marketing

decisions, it is important for marketers to fully understand the sources of brand equity,

how they affect outcomes of interest (e.g., sales), and how these sources and outcomes

change, if at all, over time. Understanding the sources and outcomes of brand equity

provides a common denominator for interpreting marketing strategies and assessing the

value of a brand: The sources of brand equity help managers understand and focus on

what drives their brand equity; the outcomes of brand equity help managers understand

exactly how and where brands add value.

2

Hoeffler& Keller1, indicates that as a consequence of creating knowledge

structures about a brand, consumers should respond more favorably to the marketing

activity for a brand than if the brand had not been identified to consumers. Specifically, a

product with positive brand equity can potentially enjoy the following seven important

customer-related benefits:

� Be perceived differently and produce different interpretations of product

performance;

� Enjoy greater loyalty and be less vulnerable to competitive marketing actions;

� Command larger margins and have more inelastic responses to price increases

and elastic responses to price decreases;

� Receive greater trade cooperation and support;

� Increase marketing communication effectiveness;

� Yield licensing opportunities;

� Support brand extensions.

These benefits, and thus the ultimate value of a brand, depends on the underlying

components of brand knowledge and sources of brand equity. Via the indirect approach,

individual components can be measured, but to provide more direct estimates, their

resulting value still must be estimated in some way. The direct approach to measuring

customer-based brand equity attempts to more explicitly assess the impact of brand

knowledge on consumer response to different aspects of the marketing program for the

firm. The direct approach is useful in approximating the possible outcomes and benefits

that arise from differential response to marketing activity due to the brand, either

individually or in aggregate.

1 The marketing advantages of strong brands S Hoeffler, KL Keller - The Journal of Brand Management, 2003

3

Retail Brand Equity

Extant Research provides different conceptualizations of retailer brand equity ,

based on the consumer – perspective. Hartman and spiro2( 2005) have used the term ‘

customer based store equity’ drawing mainly from Keller’s conceptualization of

customer based brand equity. According to Pappu and Quester’s3 , Retail Brand Equity is

defined as “ the value associated by the consumer with the name of a retailer, as reflected

in the dimensions of retailer awareness, retailer associations, retailer perceived quality

and retailer loyalty”

Retail Industry

Retailing is the largest private sector industry in the world economy with the

global industry size exceeding $6.6 trillion and a latest survey has projected India as the

top destination for retail investors. And the further upsurge is anticipated in the retail

sector as the Government of opened up 51% FDI in single brand retail outlets.

Industry experts are sensitive to the point that local markets have an edge over the retail

investors in India as they have unique advantages such as an understanding of local

needs and extended service like home delivery. As the FDI influence on the Indian retail

sector sets in, the total size of the retail trade is expected to grow extensively in the

coming years and the consumer segments patronizing the big malls will create frenzy for

organized retailing predicting a growth of 25-30 per cent per annum over the next

decade.

2 K.B. Hartman, R.L. Spiro Recapturing store image in customer-based store equity: a

construct conceptualization/ Journal of Business Research 58 (2005) 1112–1120 3 Ravi Pappu, Pascale G. Quester, Ray W. Cooksey, (2005) "Consumer-based brand

equity: improving the measurement – empirical evidence", Journal of Product & Brand Management, Vol. 14 Iss: 3, pp.143 - 154

4

The Indian retail industry is divided into organised and unorganised sectors.

Organised sectors are licensed retailers and unorganised relates to traditional or low cost

retailing. India’s retail sector with a compounded growth rate of 46.64% is the fastest

growing sector in Indian economy. Traditional markets are making way for new formats

like departmental stores, hypermarkets and speciality stores. So in such a competition in

order to maintain good recall it is essential for a retail outlet to be to a great extent

visible.

Also the particular factors focused by the outlets is important with regards to the

footfalls and sales as, if those factors meet with the expectations of the customers and is

targeted in satisfying their needs and demands then a brand bond is created between the

outlet and the customer. It is an everyday challenge for a retailer to satisfy the diversified

demands of discerning customers. The further challenges are to reel in more customers,

assure their loyalty, and drive in more footfalls and to ensure the conversion rate. In

order to gain more profits, retailers try to lure the customers with in-store signage’s,

advertisements and customer-loyalty programmes. No matter how unique these strategies

may be, they do not guarantee a success rate. Thus, to ensure a minimum return on

investment, the retailers need to ascertain that the format, product assortment and the

location of their store assures profits.

The bottom line in any business is profit and retail is certainly no exception to

this rule. In order to make sales you need to first attract people into your shop and then

get them to stay long enough to look around and make that all important purchase. The

number of people coming into the shop is known as the footfall and, like many other

businesses, it is all about the numbers. The more people who come into the shop then

generally the more you will sell. This is always provided that you are selling what the

customers want to buy.

5

The word 'retail' is extracted from the French word 'retaillier' meaning 'to cut a

piece off' or 'to break bulk'. In simple terms it involves activities whereby products or

services are sold to final consumers in smaller consumption quantities. Although

retailing in its various formats has been around in India for many years, it has been

confined for a long time to family owned corner shops or mom and pop shops popularly

known as kirana shop.

The term “retailing “refers to any activity that involves a sale to a customer who

consumes or uses the product or service. Retailing is the sale interface between the

producer and the individual consumer buying for personal consumption. The term

includes direct interface between the manufacturer and institutional buyers such as

government and other bulk customers. The retail industry is of late often being hailed as

one of the sunrise sectors in the economy. AT Kearny4, the well known international

management consultancy, recently identified India as the “Second most attractive

destination” globally from among thirty emergent markets. In India, the unorganized

retailing sector comprises of 96.5% while that of organized sector is just 3.5% that is

mainly in major metropolitan and urban areas. Indian retailing has been traditionally

dominated by a small family run “Kirana store”.

Retailing in India is the second largest untapped market after China. Professional

management and strong customer focus characterize organized retailing. Despite the

huge size of the industry, only 8% of the country’s population is engaged in retailing

while on a comparative the United States of America, it is 20%. The positive factor such

as increased purchasing power, rise in number of double income families and demanding

customers, due to change in life style and paucity of time, customers are increasingly

looking for convenience in shopping.

4 http://www.atkearney.com/consumer-products-retail/global-retail-development-index

6

To woo the customers to the store, retailers are providing a wide product range,

quality and value for money, apart from creating a pleasant shopping experience.

India has one of the largest numbers of the retail outlets (organized and

unorganized) in the world. Of the 12 million retail outlets present in the country, nearly 5

million sell food and related products. Thought of the market has been dominated by

unorganized players, the rapid entry of domestic and international organized players is

set to change the scenario.

Organized retail segment has been growing at a blistering pace, exceeding all

previous estimates.

According to a study by TSMG5 projects that in the next 10 years, the overall

retail market in India is likely to grow at a CAGR of 5.5% (at constant prices) to

1,677,000 Cr in 2015. The organized retail market is expected to grow much faster at a

CAGR of 21.8% (at constant prices) to Rs. 246,000 Cr by 2015 thereby constituting

~15% of the overall retail sales. Based on our projections, the top 5 organized retail

categories by 2015 would be food, grocery & general merchandise, apparel, durables,

food service and home improvement.

Indian retail industry is the largest industry in India, with an employment of

around 8% of work force and contributing to over 10% of the country’s GDP. Retail

industry in India is expected to rise 25% yearly being driven by strong income growth,

changing lifestyles, and favorable demographic patterns. It is expected that by 2016

modern retail industry in India will be worth US$ 175-200 billion. India retail industry is

one of the fastest growing industries with revenue expected in 2007 to amount US$ 320

billion and is increasing at a rate of 5% yearly.

5 Tata Strategic Management Group Analysis.

7

A further increase of 7%-8% is expected in the industry of retail in India by

growth in consumerism in urban areas, rising incomes and a steep rise in rural

consumption. It has further been predicted that the retailing industry in India will amount

to US$ 21.5 billion by 2010 from the current size of US$7.5 billion.

Shopping in India has witnessed a revolution with the change in the consumer

buying behavior and the wholesale format of shopping also altering. Industry of retail in

India which has become modern can be seen from the fact that there are multi-stored

malls, huge shopping centres, sprawling complexes which offer food, shopping and

entertainment all under the same roof. Indian retail industry is expanding itself most

aggressively; as a result a great demand for real estate is being created. Indian retailers

preferred means of expansion to expand to other regions and to increase the number of

their outlets in a city. It is expected that by 2010, India may have 600 new shopping

centres. Indian retail industry is progressing well and for this to continue retailers as well

as the Indian government will have to make a combined effort.

Organized Retail Vs Unorganized Retail

Global Retail Development Index-2011

As per Global Retail Development Index (GRDI) 2011 ( Table 1. 1 ) high saving

and investment rates; fast labor force growth; and increased consumer spending—make

India for a very favorable retail environment and the 4th spot in the GRD.

8

TABLE - 1.1

THE 2011 GLOBAL RETAIL DEVELOPMENT INDEX™

Source: Population Reference Bureau International Monetary Fund World Bank; World

Economic Forum; Economist Intelligence Unl; Planer Retail; A. T. Kearney analysis

2011 Rank Country Region

Market Attractive

ness ( 25%)

Country Risk (25%)

Market Saturation (25%)

Time Pressure (25%)

GRDI Score

Change in Rank

compared to 2010

1 Brazil Latin America 100.0 79.4 42.9 63.9 71.5 +4

2 Uruguay Latin America 85.0 73.8 63.6 39.6 65.5 +6

3 Chile Latin America 84.3 100.0 30.3 44.3 64.7 +3

4 India Asia 28.9 59.9 63.1 100.0 63.0 -1

5 Kuwait MENA 80.4 80.6 57.3 27.1 61.3 -3

6 China Asia 49.5 76.5 31.0 87.7 61.2 -5

7 Saudi Arabia MENA 70.9 80.7 50.6 35.7 59.5 -3

8 Peru Latin America 39.8 61.5 72.0 59.5 58.2 + 1

9 United Arab Emirates

MENA 87.6 88.9 12.6 42.9 58.0 -2

10 Turkey MENA 83.8 65.5 45.0 37.0 57.8 +8

11 Lebanon MENA 56.3 43.0 57.5 53.8 52.6 N/A

12 Egypt MENA 22.1 49.5 855 52.7 52.5 +1

13 Albania Eastern Europe 19.9 48.3 79.6 60.5 52.1 -1

14 Russia Eastern Europe 76.2 49.1 308 51.0 51.8 -4

15 Kazakhstan Asia 29.2 30.1 87.5 60.1 51.7 N/A

16 Indonesia Asia 38.2 53.0 54.5 58.8 51.1 0

17 Morocco MENA 22.6 72.9 528 54.8 50.8 -2

18 Philippines Asia 26.2 548 66.1 51.0 49.4 +4

19 Tunisia MENA 37.5 75.2 63.0 21.3 49.3 -7

20 Sri Lanka Asia 8.4 52.6 865 42.4 47.5 N/A

21 Malaysia Asia 53.9 64.0 18.0 52.7 47.2 -4

22 Mexico Latin America 74.6 67.5 16.3 23.8 45.6 +3

23 Vietnam Asia 8.4 35.0 48.8 85.1 44.3 -9

24 Colombia Latin America 45.7 54.0 35.8 36.9 43.1 +2

25 Argentina Latin America 60.4 26.6 44.2 38.4 42.4 N/A

26 South Africa Sub-Saharan Africa

46.9 898 15.2 17.2 42.2 -2

27 Panama Latin America 44.3 47.3 44.5 27.6 40.9 N/A

28 Dominican Republic

Latin America 39.5 0.0 74.2 49.0 40.7 -5

29 Iran MENA 33.5 3.4 89.2 31.0 39.3 N/A

30 Bulgaria Eastern Europe 45.1 56.2 4.9 50.2 39.1 -11

9

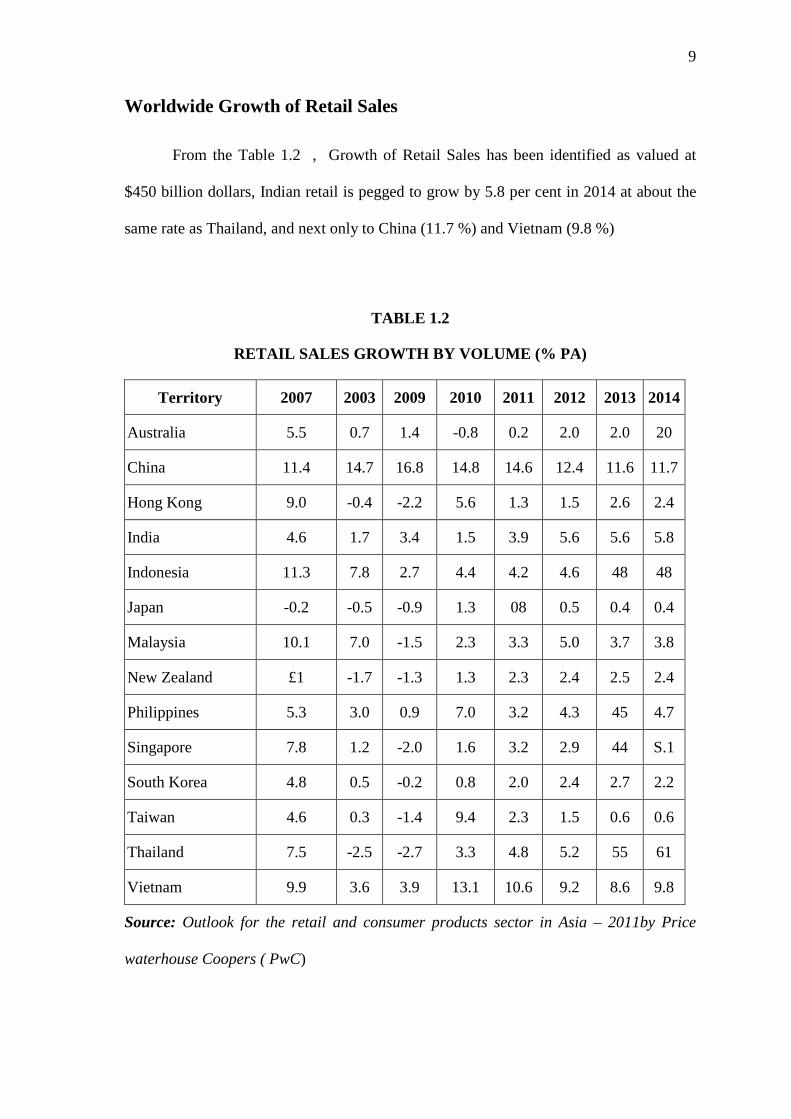

Worldwide Growth of Retail Sales

From the Table 1.2 , Growth of Retail Sales has been identified as valued at

$450 billion dollars, Indian retail is pegged to grow by 5.8 per cent in 2014 at about the

same rate as Thailand, and next only to China (11.7 %) and Vietnam (9.8 %)

TABLE 1.2

RETAIL SALES GROWTH BY VOLUME (% PA)

Territory 2007 2003 2009 2010 2011 2012 2013 2014

Australia 5.5 0.7 1.4 -0.8 0.2 2.0 2.0 20

China 11.4 14.7 16.8 14.8 14.6 12.4 11.6 11.7

Hong Kong 9.0 -0.4 -2.2 5.6 1.3 1.5 2.6 2.4

India 4.6 1.7 3.4 1.5 3.9 5.6 5.6 5.8

Indonesia 11.3 7.8 2.7 4.4 4.2 4.6 48 48

Japan -0.2 -0.5 -0.9 1.3 08 0.5 0.4 0.4

Malaysia 10.1 7.0 -1.5 2.3 3.3 5.0 3.7 3.8

New Zealand £1 -1.7 -1.3 1.3 2.3 2.4 2.5 2.4

Philippines 5.3 3.0 0.9 7.0 3.2 4.3 45 4.7

Singapore 7.8 1.2 -2.0 1.6 3.2 2.9 44 S.1

South Korea 4.8 0.5 -0.2 0.8 2.0 2.4 2.7 2.2

Taiwan 4.6 0.3 -1.4 9.4 2.3 1.5 0.6 0.6

Thailand 7.5 -2.5 -2.7 3.3 4.8 5.2 55 61

Vietnam 9.9 3.6 3.9 13.1 10.6 9.2 8.6 9.8

Source: Outlook for the retail and consumer products sector in Asia – 2011by Price

waterhouse Coopers ( PwC)

10

Country wise share of organized retail Organized versus unorganized debate

India's share of organized retail has just hovered around about 4 per cent despite

advent of big corporate in retail sector.

TABLE 1. 3

SHARE OF ORGANIZED RETAIL IN SELECTED COUNTRIES, 20 06

S

Source: Planet Retail and Technopak Advisers Pvt. Ltd – www.technopak.com

Country Total Retail Sales (US$ bn)

Share of Organized Retail (%)

USA 2,983 85

Japan 1,182 66

China 785 20

United Kingdom 475 80

France 436 80

Germany 421 80

India 322 A

Brazil 284 12

Russia 276 33

Korea, South 201 15

Indonesia 150 30

Poland 120 20

Thailand 68 40

Pakistan 67 1

Argentina 53 40

Philippines 51 35

Malaysia 34 55

Czech Republic 34 30

Vietnam 26 22

Hungary 24 30

11

Difference between Organised and Unorganised Retail

The Organised retailing refers to the trading activities undertaken by licensed

retailers that is those who registered themselves for sales tax ,income tax ,etc. These

include the corporate –backed hypermarkets and retail chains and also the privately

owned large businesses. The various forms of organized retail are

� Hypermarket: They store products of multiple brands comprising food items and

non-food items. Eg: HyperCity

� Supermarkets: These are self service stores selling food and personal care

products. E.g. Reliance Fresh

� Departmental Stores: Retails branded goods in non-food categories. E.g.

Shoppers stop.

� Specialty Chains: These focus on branded product or product category. E.g. Bata

Convenience Stores., EZone,etc

Organized retailing is based on the principle of unity and unorganized retailing is

based on the principle of singularity. Both organized and unorganized retailing is found

in most countries throughout the world. India and China are strong examples of countries

in which unorganized retailing is dominating the markets. Today these countries have a

growing economy today because of the influx of organized retailers into these markets.

12

The demand for giant malls with large department stores, cinemaplexes,

supermarkets, and pharmacy chains is the result of higher incomes and urban customers

looking for convenience in shopping. Large chains such as WalMart, McDonald's,

Vodefone, Dell and other organized retailers have reached across the world sharing their

retailing expertise.

The unorganized mom and pop retailers and independent retailers also continue

to fulfill the local needs. The organized retailing giants are trading their organizational

expertise for a share of the markets across the world.

Indian retail is dominated by a large number of small retailers consisting of the

local kirana shops, owner-manned general stores, chemists, footwear shops, apparel

shops, paan and beedi shops, hand-cart hawkers, pavement vendors, etc. which together

make up the so-called “unorganized retail” or traditional retail. Organized retailing is

based on the principle of unity and unorganized retailing is based on the principle of

singularity. Both organized and unorganized retailing is found in most of the countries

throughout the world. India and China are strong examples of countries in which

unorganized retailing dominated their markets. Today these countries have a growing

economy because of the influx of organized retailers into their markets. The last 3-4

years have witnessed the entry of a number of organized retailers, opening stores in

various modern formats in metros and other important cities. The growth in organized

retailing in recent years can also be gauged by the rise of shopping malls as well as the

rising number of modern retail formats.

13

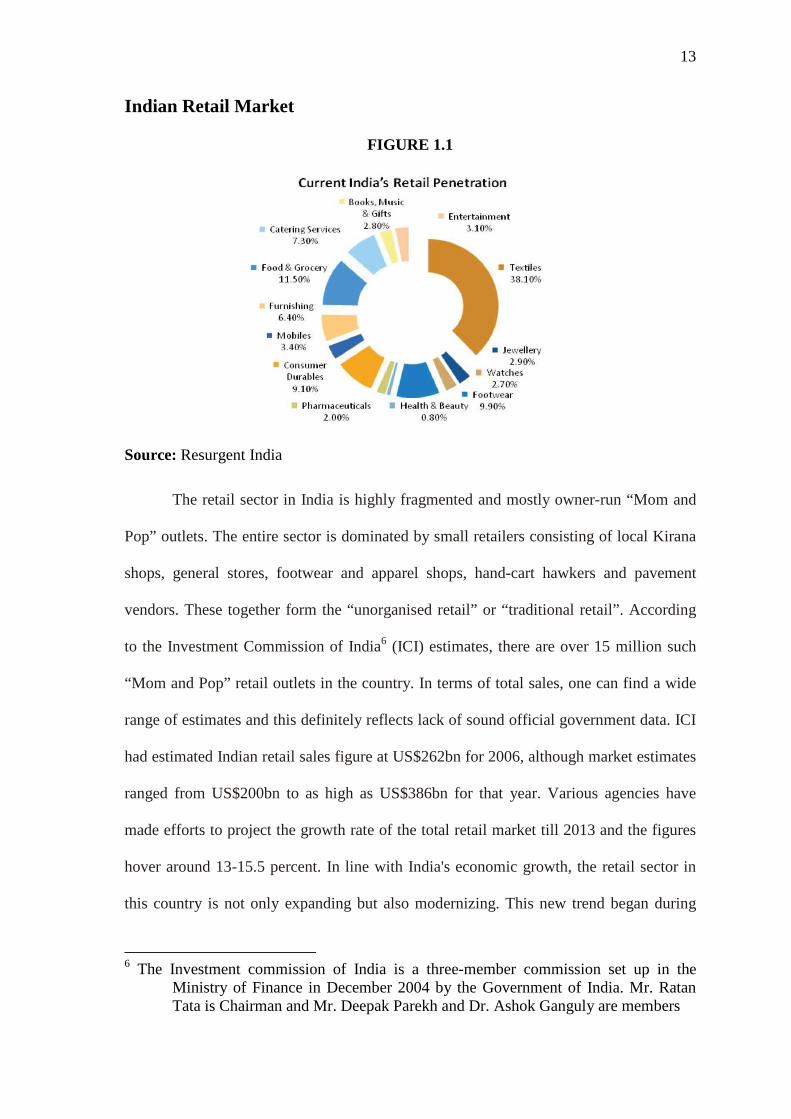

Indian Retail Market

FIGURE 1.1

Source: Resurgent India

The retail sector in India is highly fragmented and mostly owner-run “Mom and

Pop” outlets. The entire sector is dominated by small retailers consisting of local Kirana

shops, general stores, footwear and apparel shops, hand-cart hawkers and pavement

vendors. These together form the “unorganised retail” or “traditional retail”. According

to the Investment Commission of India6 (ICI) estimates, there are over 15 million such

“Mom and Pop” retail outlets in the country. In terms of total sales, one can find a wide

range of estimates and this definitely reflects lack of sound official government data. ICI

had estimated Indian retail sales figure at US$262bn for 2006, although market estimates

ranged from US$200bn to as high as US$386bn for that year. Various agencies have

made efforts to project the growth rate of the total retail market till 2013 and the figures

hover around 13-15.5 percent. In line with India's economic growth, the retail sector in

this country is not only expanding but also modernizing. This new trend began during

6 The Investment commission of India is a three-member commission set up in the

Ministry of Finance in December 2004 by the Government of India. Mr. Ratan Tata is Chairman and Mr. Deepak Parekh and Dr. Ashok Ganguly are members

14

late 1990s and early 2000s. In the midst of the unorganised retail sector's strong

dominance, some of the major industrial houses have entered into this sector and have

announced ambitious future expansion plans. Transnational corporations have also

joined hands with big Indian companies to set up retail chains. India's Bharti group

joined hands with Wal-Mart, the world's largest retailer and Tata group tied up with the

UK based Tesco, the world's third largest retail group. A perceptible structural change

towards an organized format is foreseeable in the retail sector. These organized and

modern retail formats generally consist of supermarkets/convenience stores,

hypermarkets, discount stores, specialty stores and departmental stores. These outlets are

usually chain stores, all owned or franchised by a central entity or a single store large

enough to form a part of the modern retail segment. The existence of these modern retail

outlets are generally found in malls and prominent high streets across various cities. As

discussed earlier, the retail market in India is primarily unorganized and the penetration

of modern retail is very minimal. This is in contrast to the trend in developed economies

of USA, UK, France and Germany where organized retail is in the range of 75-80 per

cent. As per the data released by ICI, organized retail market size was to the tune of

US$12.1bn in 2006, accounting for 4.6 per cent of the total retail segment. The late

diffusion and low share of modern retail is mainly attributable to the severe restrictions

on foreign direct investment (FDI) for retailing in our country till end of 2005. The

demand side characteristics such as moderately high economic growth, ever expanding

middle and upper class consumer base, high urbanization rate, increasing share of

women in workforce and greater availability of personal credit were definitely favorable

for a greater penetration of modern retail in the economy. In January 2006, India allowed

foreign companies to own up to 51 per cent in single-brand retail joint ventures (JVs) and

as a result the organized retail in India got a boost. Though multiple-brand foreign firms

15

are still barred in retail, they can set up wholesale operations. The growth in organized

retailing in the present decade may be gauged by the rise in number of shopping malls. In

1999, India had just 3 shopping malls measuring around 1 mn.sq.ft. and by the end of

2006, the total mall space rose up to 28 mn.sq.ft. with an average annual addition of 3.9

mn.sq.ft. Post 2006, on an average 8 mn.sq.ft. of retail space has been added annually

pan India taking the mall space to over 52 mn.sq.ft by the end of 2009. With partial

relaxation of FDI norms pertaining to retail, the modern retail market is expected to grow

at a healthy rate. There has been a creeping internationalization of retailing in the recent

past. As home markets are becoming crowded, modern retailers from developed

countries are turning to new emerging markets like India. The projected annual growth

rate of this segment of the retail market till 2013 is slated to be over 30 per cent. As a

result, its share in total retail market is expected to be around 11 per cent by 2013. On the

flip side, concerns have been raised that the growth of modern retail will have an adverse

impact on retailers in the unorganized sector. However, a recent study (2008) undertaken

by the Indian Council for Research on International Economic Relations7 (ICRIER) and

commissioned by Department of Industrial Promotion and Policy8 (DIPP), Ministry of

Commerce & Industry, Government of India has shown that there would be a positive

sum game in the retail sector in India where both organized and unorganized retail

segments not only coexist but also grow substantially in size. As a result, it is expected

that a positive environment is likely to be prevalent in the economy which would take the

organized retail on a high growth trajectory.

7 Established in August 1981, ICRIER is an autonomous, policy-oriented, not-for-profit,

economic policy think tank. 88 The Department of Industrial Policy & Promotion was established in 1995 and has

been reconstituted in the year 2000 with the merger of the Department of Industrial Development. Earlier separate Ministries for Small Scale Industries & Agro and Rural Industries (SSI&A&RI) and Heavy Industries and Public Enterprises (HI&PE) were created in October, 1999.

16

Dynamics of Organized Retailing

The economic meltdown of 2008 and 2009 has brought in some important

alterations in the organized retail market in India. During the boom period, prior to the

downturn, the outlook for this sector exuded confidence. Lots of developers announced

their forays into mall development and the penetration of modern retail was expected to

grow at a phenomenal rate. However, as a result of the economic slowdown in the last

couple of years, bullish sentiments have given way to the much needed cautious and

consolidative approach among developers and retailers. Lease rentals have been

renegotiated and a substantial correction in the rental rates has taken place. Mumbai

witnessed an average rental correction of 15-20 per cent during Q1 2008 to Q4 2009

while the average correction in Bangalore and NCR was more than 25 per cent during

the same period. Apart from rental corrections, various lease rental models have evolved

as a corollary to coping strategies adopted by the stakeholders of organised retailing

during 2008 and 2009. Zero rental schemes and revenue sharing models are options that

are proving increasingly attractive to retailers looking to trim costs and to property

owners seeking to maintain occupancies. Revenue sharing models are based on the

premise that rent paid is linked to store performance. Some retailers are also attempting

to negotiate a combination of zero rentals and revenue sharing agreements, whereby a

period of zero rentals will be followed by revenue sharing for a duration until sales

volumes begin to rise again. Another variant that is increasingly gaining importance is

revenue sharing with a minimum guarantee from the retailer's side. In addition to the

short-term measure of renegotiating rent, retailers are also looking at long-term

initiatives in order to trim costs and diversify risk. Certain national brands have started

exploring relatively untapped or growing segments in order to diversify their range of

products. Consolidation of operations by reducing number of outlets is also another

17

strategy adopted by several retailers to beat the adverse consequence of oversupply

created during the boom time. Once the phase of control and consolidation is over,

significant new trends could well begin to emerge across the board. Retailers are

expected to shift focus to food and related items, rather than lifestyle goods. In addition

to this, Tier I and Tier II cities could become more attractive propositions for developers

and retailers due to lower rentals and operating costs and high growth in population.

Market Review

Mumbai bears the tag of being the financial capital of the country and contributes

around 5% of the country's GDP. The city is home to important financial institutions like

the Reserve Bank of India, the Bombay Stock Exchange and the National Stock

Exchange. Besides being the entertainment capital of the country, the city has rich

cosmopolitan demographics. These factors also ensure that the city remains foremost in

terms of the real estate development. The region referred to as Mumbai Metropolitan

Region (MMR), covers the city of Thane and Navi Mumbai along with Mumbai city.

Mumbai, which houses the first Mall in the country, has a total organised retail stock of

8.72 mn.sq.ft. and will witness 11.26 mn.sq.ft. of new retail development over the next 3

years. The city is home to some of the most prominent and successful malls in the

country and the retail rentals are amongst the most expensive in the world. While the size

of the consumer market in the city is particularly large, the pace of retail real estate

development has outgrown the organised retail business over the last 4-5 years. This

situation, coupled with the global financial crisis in 2008, forced retailers to curtail their

expansion plans and put some large retailers on the brink of bankruptcy. While the

confidence of the retailers was shaken, the mall projects in the city were stalled due to

poor liquidity. Retail and commercial projects of the city were on a negative list of the

institutional lenders which made situation worse for commercial real estate segment.

18

According to Knight Frank Research 9While the situation has improved since mid 2009,

the retail space vacancy across the city still remains high. Many mall projects have been

marred because of poor design and also high concentration of malls in particular

catchment area. Taking cognizance of the poor demand situation, some malls with high

vacancy have started leasing space to office occupiers instead of waiting for retailers

Mumbai currently has 8.72 mn. sq.ft. of major operational mall space in the city. These

malls are spread all over the city, stretching from Nariman Point in South Mumbai to

Bhayander in the Western Suburbs and Kalyan in the Central Suburbs. The city of

Mumbai is divided into 4 zones: Island City, Western Suburbs, Central Suburbs and Navi

Mumbai. The malls in these zones have been analyzed and their characteristics have been

studied in order to provide a thorough examination of mall space in Mumbai.

Zone Locations

Island City : Nariman Point, Haji Ali, Worli, Lower Parel, Dadar, Mahim

Western Suburbs : Bandra, Santacruz, Andheri, Goregaon, Malad, Borivali,

Dahisar, Mira Road- Bhayander stretch

Central Suburbs : Matunga, Chembur, Ghatkopar, Mulund, Thane,

Kalyan, Bhandup

Navi Mumbai Airoli, Vashi, Kharghar

Source: Knight Frank Research

9 http://www.knightfrank.co.in/en

19

As mentioned above, the Island City zone of Mumbai encompasses all of South

Mumbai, Worli to Nariman Point, as well as Prabhadevi, Dadar and Mahim. The major

micro-markets covered in the Island City are Nariman Point, Worli-Prabhadevi, Lower

Parel and Haji Ali-Kemps Corner. Some of the major malls in the zone include High

Street Phoenix located at Lower Parel and Atria Mall located at Worli. Since the Island

City is considered to be a fairly up market residential area, there are a large number of

national and international brands present here. Two out of the three major high streets

that were covered in this study are present in this zone, further enhancing this zone's

exclusive status. Crossroads, the first mall in the country, located at Haji Ali was shut

down and bought by the Future Group in 2006 to convert it into office space with some

amount of retail space as well. The initially unorganised retail space has now been

organised and is referred to as SoBo (South Bombay) Central Mall, having a built up

area of 0.1 mn. sq.ft. This name of the retail space was given as recently as 2009.

Currently, there is just a fraction of the space that is used commercially, with the

majority comprising retail space.

This zone saw the development of a new mall called Palladium, which is the

newest part of the High Street Phoenix Mall at Lower Parel. It is referred to as Phase 3,

came into operation in 2009 and has a built up area of approximately 0.2 mn. sq.ft. The

Island City only accounts for 15% of the major operational malls in Mumbai with a total

built up area of 1.3 mn. sq.ft. As mentioned earlier, owing to the large volume of

organised retail in this zone, there is a lack of dependence on mall space. Furthermore,

the average mall vacancy is only 4% since there are only 5 major malls in the Island

City. With a smaller number of malls in the zone, it is unlikely that any of them would

operate without full capacity.

20

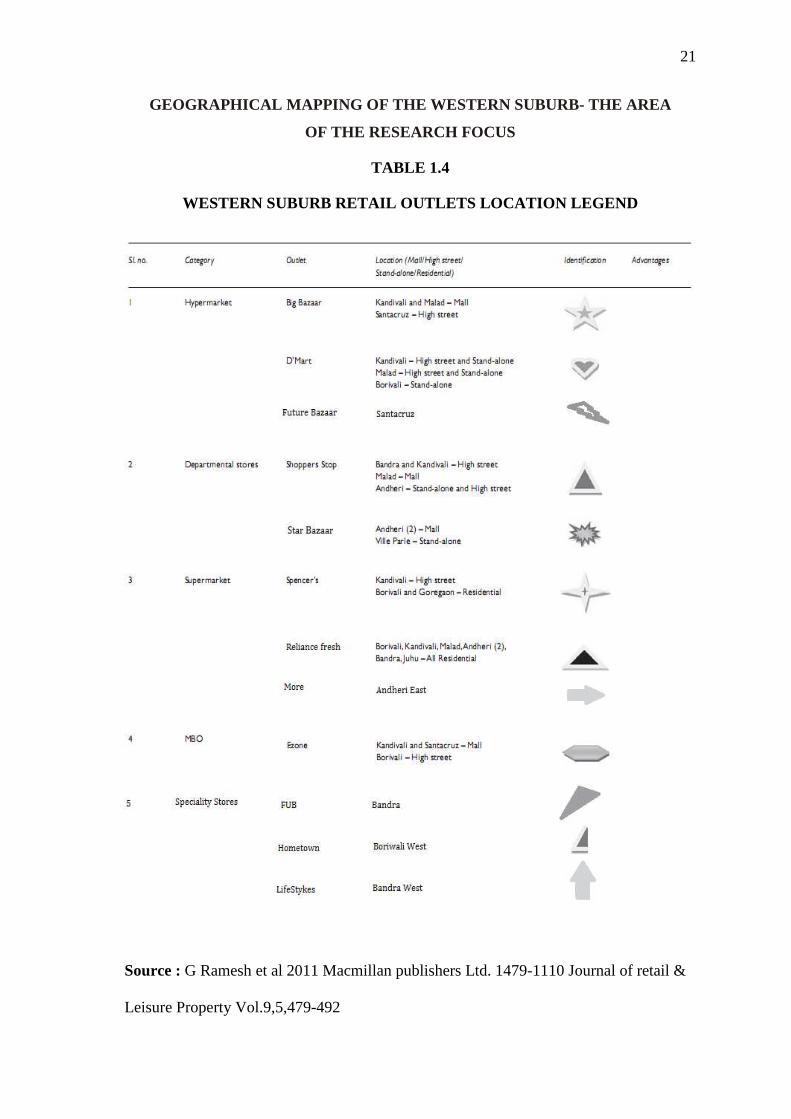

Western Suburbs

Our scope of research is the Western Suburb of Mumbai covering Bandra to

Borivali and some of the major micro-markets falling under the Western Suburbs include

Santacruz, Linking Road in Bandra, Andheri, Malad, Goregaon , Kandivali and Borivali.

A geographical mapping of the area is placed as figure 1.1 with the different formats of

retail outlets and some of the prominent retail brands with location using semiotics. The

legend with the outlets and its identified semiotics are put up as Table 1.4 for easy

reference.

21

GEOGRAPHICAL MAPPING OF THE WESTERN SUBURB- THE ARE A

OF THE RESEARCH FOCUS

TABLE 1.4

WESTERN SUBURB RETAIL OUTLETS LOCATION LEGEND

Source : G Ramesh et al 2011 Macmillan publishers Ltd. 1479-1110 Journal of retail &

Leisure Property Vol.9,5,479-492

22

FIGURE 1.2

RETAIL LOCATION WESTERN SUBURB OF MUMBAI

Source : G Ramesh et al 2011 Macmillan publishers Ltd. 1479-1110 Journal of retail &

Leisure Property Vol.9,5,479-492

23

Statement of the Problem

Brand Equity of a product has been in prominence across the globe and its

measure is of another importance cutting across all the products be it fast moving or the

durables. However, from the service point of view, this equity concept has not taken

wings among the managers and marketers especially in the business of Retail sector.

This shows clearly that both the Management and the Marketers are neither much

worried about nor concentrate on the places where the different products are available.

The issue of Organized Retail although has a nominal growth of about 4 to 5 % in the

entire retail industry in India, it is indeed gaining momentum considering the fact that the

government has provided the much needed and expected fillip to the issue of Foreign

Direct Investment in the Single Brand business and also in the Multi brand Business.

Keeping this as the strong background as the problem identified, this research was

initiated and the statement of the problem is appended below

“Measurement of Brand Equity for a product is in prevalence but the same

is not so in the case of Service aspect especially with respect to Retail outlets as a

service provider. Hence there is a strong felt need in research attempts on the issues

related to Brand Equity on Retail outlets and its Measurement”.

Need for the study

Many Researchers have carried out extensive studies on the brand equity issues

in relevance to Products. However, very few studies are found even globally on the

Brand Equity study of Services especially in reference to Organized Retail Outlets.

Hence a need was felt to pursue a study to understand the concept of Brand Equity with

reference to Organized Retail outlets and to formulate an equation which will necessitate

measuring the brand equity of a particular Organized Retail outlet/store. The scope of

24

the research is limited to the area covered under the Western Suburb of Mumbai region

only ( From Bandra to Borivali ).

Various studies and extensive research have been undertaken to study the concept

of Brand Equity and its application with respect to Products. However, not many have

been done as on date in order to study the concept of Brand Equity with respect to

Services and in particular the organized Retail Brands. Hence the motivation to develop

into a research area will enable to bring out a better understanding on the concept of

Retail Brand Equity and its application. Although the organized retail has just touched

upon the 5 % mark as its share over the entire Retail Sector, we have taken a sizeable

strength of Organized Retail brands under various Formats in the catchment area of

Mumbai suburbs. The challenges faced by undertaking this research is the fact that the

equity measure is based on the customer patronizing the store/outlet and the concerned

outlet per se may not be convinced with these projections. Unfortunately, we are bound

to go by the projections as given by the customers who are the real judge anyways.

However, vital information have been duly cross checked with the experts at the time of

in depth interview that we have conducted.

Significance of the study

In the light of the fact that very few studies have been reported or rather

identified across the globe in the field of Brand Equity of Organized Retail Outlet, it is

indeed significant to undertake the study not only to understand the concept of Brand

Equity but also to formulate an equation to measure the brand equity of an organized

Retail Outlet.

25

Scope of the study

The Scope of the research includes the Organized Retail outlets in Mumbai. Data

for this study were collected from about 3000 shoppers by intercept method intercepting

them immediately after they finish their shopping from a particular organized Retail

outlet. In addition to this, supplementary information were also used from the sources of

Retailers Association of India ( rai) which is head quartered at Mumbai.

Research Methodology

Theory Building Up

In order to understand more on the problem recognized, numerous articles from

various journals were reviewed. These articles are referred in the review of literature

chapter. Also theory building up helped us to establish the specific indicators and

constructs which are in turn used to develop a structured questionnaire.

Establishing the constructs

As indicated in the previous paragraph, based on the theory build up, specific

indicators say about 45 were identified covering different attributes such as product

assortment, Service quality rendered, ambience ( both internal and external), pricing

issues, facilities provided etc. These indicators were then grouped into four constructs as

per Aaker model. They are Brand Awareness, Brand Association, Perceived Quality and

Customer Loyalty. For the sake of ease in reference, these constructs were written in an

acronym form such as Brand Awareness as BAW, Brand Association as BAS, Perceived

Quality as PQ and Customer Loyalty as CL.

26

Developing Research Questions, Hypotheses and Research Objectives

Research Questions

The following questions were developed on the basis of the theory building up.

1. Does the concept of Brand Equity in the Organized Retail outlet has an

significance on the Brand Image of the Outlet?

2. Does Strong Brand Awareness for a brand helps to create strong Brand Equity?

3. Does Strong Brand Association for a brand helps to create strong Brand Equity?

4. Does Strong perceived quality for a brand is positively related to Brand Equity?

5. Does Superior customer Loyalty of a brand helps to create strong Brand Equity?

TABLE 1.5

LIST OF ABBREVIATION

Abbreviation Expansion

SB Star Bazaar

SS Shopper’s Stop

FUB Furniture Bazaar

SP Spencer

EZ EZone

BB Big Bazaar

HT Home Town

DM D Mart

RF Reliance Fresh

LS LifeStyle

MO More

FB Future Bazaar

BAW Brand Awareness

BAS Brand Association

PQ Customer Perceived Quality

CL Customer Brand Loyalty

27

Categorization of Retail Brands under specific Organized Retail

Outlets Formats

The Current Research is specifically on the Organized Retail sector which is

categorized into various formats. For the Study, specific Retail brand of Outlets falling

under specific formats have been chosen as per availability under the scope of the

research ( From Bandra to Borivali) and on the basis of certain evaluation. A Sample List

of the Retail Formats with example is placed in Table 1.6

TABLE 1.6

CATEGORIZATION OF RETAIL BRANDS UNDER SPECIFIC ORGA NIZED

RETAIL OUTLETS FORMATS

Sl No Organized Retail Formats Brands

1 Hypermarket HyperCity

2 Supermarket Reliance Fresh, Star Bazaar,etc

3 Departmental Store Shopper’s Stop, Big Bazaar,etc

4 Discount Store D Mart, Spencers

5 Specialty Store Croma, Crossword, Bodyshop etc

6 Multi Brand Outlets (MBO) Vijay Sales, Next etc

Source : Prepared for the Study based on discussion with experts

Research Hypotheses

Following are the specific Hypotheses (H) developed as a declaration to the

Research questions.

HSB: Retail Brand Equity positively influences the retail brand image of the

Brand SB in terms of the four constructs BAW, BAS, PQ and CL

HSS: Retail Brand Equity positively influences the retail brand image of the

Brand SS in terms of the four constructs BAW, BAS, PQ and CL

28

HFUB: Retail Brand Equity positively influences the retail brand image of the

Brand FUB in terms of the four constructs BAW, BAS, PQ and CL

HSP: Retail Brand Equity positively influences the retail brand image of the

Brand SP in terms of the four constructs BAW, BAS, PQ and CL

HEZ: Retail Brand Equity positively influences the retail brand image of the

Brand EZ in terms of the four constructs BAW, BAS, PQ and CL

HBB: Retail Brand Equity positively influences the retail brand image of the

Brand BB in terms of the four constructs BAW, BAS, PQ and CL

HHT: Retail Brand Equity positively influences the retail brand image of the

Brand HT in terms of the four constructs BAW, BAS, PQ and CL

HDM: Retail Brand Equity positively influences the retail brand image of the

Brand DM in terms of the four constructs BAW, BAS, PQ and CL

HRF: Retail Brand Equity positively influences the retail brand image of the

Brand RF in terms of the four constructs BAW, BAS, PQ and CL

HLS: Retail Brand Equity positively influences the retail brand image of the

Brand LS in terms of the four constructs BAW, BAS, PQ and CL

HMO: Retail Brand Equity positively influences the retail brand image of the

Brand MO in terms of the four constructs BAW, BAS, PQ and CL

HFB: Retail Brand Equity positively influences the retail brand image of the

Brand FB in terms of the four constructs BAW, BAS, PQ and CL

H1 : Strong brand awareness for a brand helps to create strong brand equity

H2 : Strong brand association for a brand helps to create strong brand equity

H3 : Strong perceived quality of a brand is positively related to brand equity.

H4 : Superior customer loyalty regarding a brand helps to create strong brand equity.

29

Objectives of the study

The Primary Objective of the research would identify the effect that both the

brand image of the store and the perceived value as realized by the customers in shaping

the brand loyalty and in turn deriving good brand equity.

The following are the Sub objectives of the current study on the brand equity

study on Organized Retail Outlets.

� To establish the factors which influences the Brand Equity of an Organized Retail

Outlet and helps decision making by the consumers selecting a particular retail

outlet for patronizing

� To analyze and identify those established factors which are dependent and

independent on the Brand Equity of the outlet using the data collected on Twelve

(12) brands of Organized Retail outlets in Mumbai covering Three Thousand

(3000) Shoppers.

� To carry out inferential analysis on the chosen brands of organized retail outlets

and to formulate a mathematical equation using the multiple regression analysis

that can be used to measure the brand equity of a particular retail outlet.

� To Construct a Brand Equity Equation and Brand Equity Index that could capture

the full domain of Brand Equity using specific models and Statistical tools and

analysis with respect to Organized Retail Outlets/Stores.

Research Design

A Research Design is the arrangement of conditions for collection and analysis of

data in a manner that fits the requirement of the research purpose keeping in view the

expenditure aspects also so as to have an effective and comprehensive procedure. The

arrangement of conditions suitable for collection and analysis of data depends on the

subject and purpose of the research study.

30

To study the brand equity of organized retail outlets, the descriptive research

design has been adopted. The descriptive research involves collection of data with the

help of a designed questionnaire by using an appropriate sampling procedure and

analyzing of the same using inferential statistical techniques to find out the measure of

the retail brand equity of the organized retail outlets in Mumbai.

Tools for data collection

Structured questionnaires were distributed to find out the data of the

consumer/shopper experience in the organized retail brands categorized under various

formats in the geographical area of Mumbai. Data were collected on the basis of

qualitative study such as in depth interview with senior management personnel of

various brands of organized retail and focus groups conducted across different ranks of

specialist in the retail and other field. There are primarily two ways of collecting data

with regard to understanding the brand equity aspect as advocated by prominent authors

and experts of the subject. One is using the method called residual wherein the data

related to the opening and closing stock of all the Stock Keeping Units ( SKU’s) of

different products is needed. The second method is consumer oriented and requires

understanding the experience of their shopping in a particular organized retail

outlet/store. Application of the first method was found to be difficult as on the basis of

in depth interviews with senior management people indicated the non readiness towards

the divulging of internal data. Hence the second method focusing on consumer/shopper

orientation was chosen. The data related to the consumers/shopper’s experience were

collected based on the catchment area where the outlet/store was located and on the basis

a set of common attributes associated with the Organized retail outlets/stores. Also as the

study is related to measuring the brand equity of the outlets, a minimum of 12 brands of

the organized retail brands in Mumbai was felt as a bare necessity.

31

Type of Data Used

The primary data, which is the back bone of the study in terms of its effectiveness

and requirement, is collected for the purpose of analysis from the various organized retail

outlets and also the secondary data were collected as appropriate for interpretive and

corroborative purpose.

Framework of Analysis

As part of descriptive analysis, mean, Standard Deviation, Percentages,

Distribution, Bar Charts, etc., are used. As a part of inferential analysis, of test, Analysis

of Variance (one way correlated and two-way without replication), Multiple Regression

Analysis, Factor Analysis using Structural Equation Modeling and the respective follow

up tests have been used to analyze the data. Different Organized Retail Brands

representing specific formats of Organized Retail Outlets in Mumbai are chosen so to

have an appropriate mix of units for the purpose of the study. The choice of the units is

based primarily on the catchments areas followed by the availability of Retail brands in

the area identified. While the object of evaluation was the Organized Retail brands, the

subject of evaluation was the regular consumers/shoppers who are visiting the various

Organized Brands of Retail Outlets/stores. In order to bring in a substantial result, the

respondents were identified as those who finish their shopping and their respective

opinions were captured at the exit level. Although this exercise was subjected to lot of

inconvenience to the shopper, maximum care was taken to get the most unbiased

responses from them.

32

Sampling Size and Sampling procedure

While the population of Organized Retail outlets across is more than 100 and the

shoppers are countless, from the Subject of evaluation point of view ( vide Table 1.6 &

vide Objective b), and the scope of the research restricted to the western suburb covering

Bandra to Borivali, a sample of Twelve (12) Organized Retail brands representing

different format were taken and from the object of evaluation point of view, a sample of

3000 consumers/shoppers were taken on the convenience of the researcher on the

purposes selected for the study.

Data Collection

The data was collected from among the object respondents through a structured

questionnaire (vide Appendix A – page No.273 ) which was subjected to its validity and

reliability using various test such as Cronbach Alpha Test etc. The responses were

collected through specially trained students by incentivizing them appropriately.