Embed Size (px)

Citation preview

Changes in Families’ Ability & Willingness to Pay for College: How Should This Affect

a College’s Strategy?

Dan Lundquist Matt ScottyThe Stockade Consulting Group National Education Servicing

Moodys Offers Vote of Support

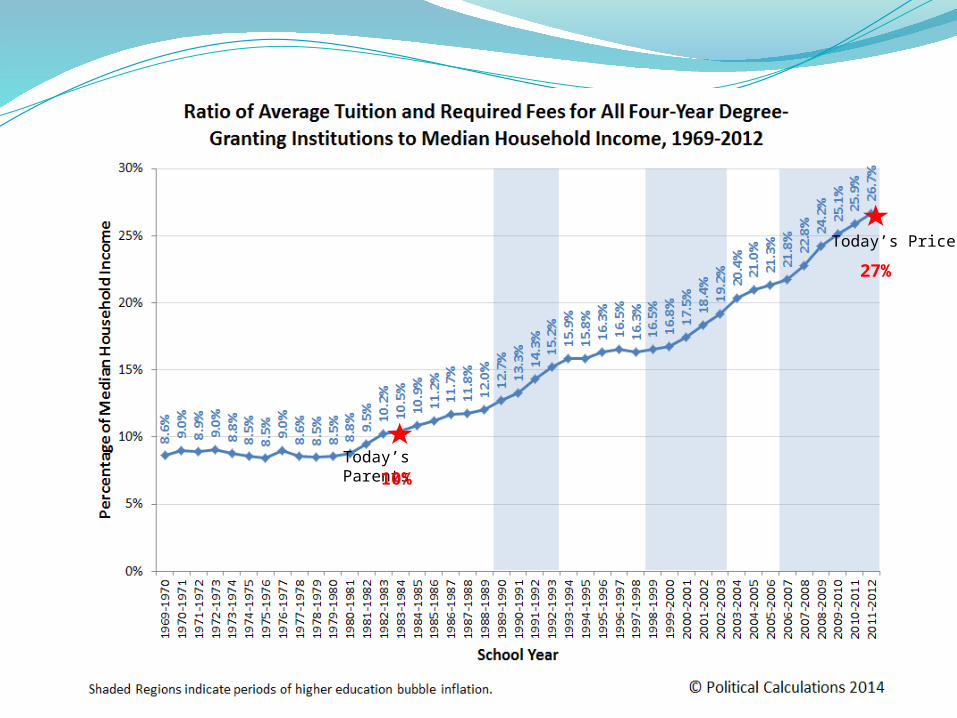

Situation Analysis 2014 Ability/Willingness to Pay

Price tags continue to increase, fueling anxiety

But there are fewer college-ready students from families who are able or willing to pay

Though they see the value of a college education, families hedge more (negotiate and borrow) and will “settle” for a second-choice college if it saves them money (up front in tuition or longer-term in loans)

Today’s Parents

Today’s Price

10%

27%

$0 AGI

Revenue from Families Declining

Situation Analysis 2014 61 percent of colleges didn’t meet goals by May 1

(up from 60 percent a year ago) 71 percent of private bachelor’s institutions didn’t

meet goals by May 1 (up from 59 percent a year ago). 32 percent of all institutions – in violation of

NACAC’s principles of good practice – reported recruiting students after May 1 who committed to other institutions (up from 29 percent last year).

SO expenditure/revenue tensions rise…for colleges and for families

Situation Analysis 2014 Education (and credentialing) is “evergreen” and can't be

killed. Its importance and value are inherent parts of society; and given

structure in the form of highered institutions BUT… the past two decades of increasing demand and price elasticity have led to some purposefully inefficient practices most can no longer afford

If allowed to continue with what are viewed as outmoded policies and practices the structure be driven to change by market forces (consumer choice) and regulation (government policy)

Kodak presumably had more business savvy than highered and look what happened to them.

To be fair, MOOCS won't do to highered what digital did to Kodak… but there is no reason for us to pass our leadership obligation

Reality Check: You Say…

The 2014 CFO Surveys conducted by Gallup and Inside Higher Ed

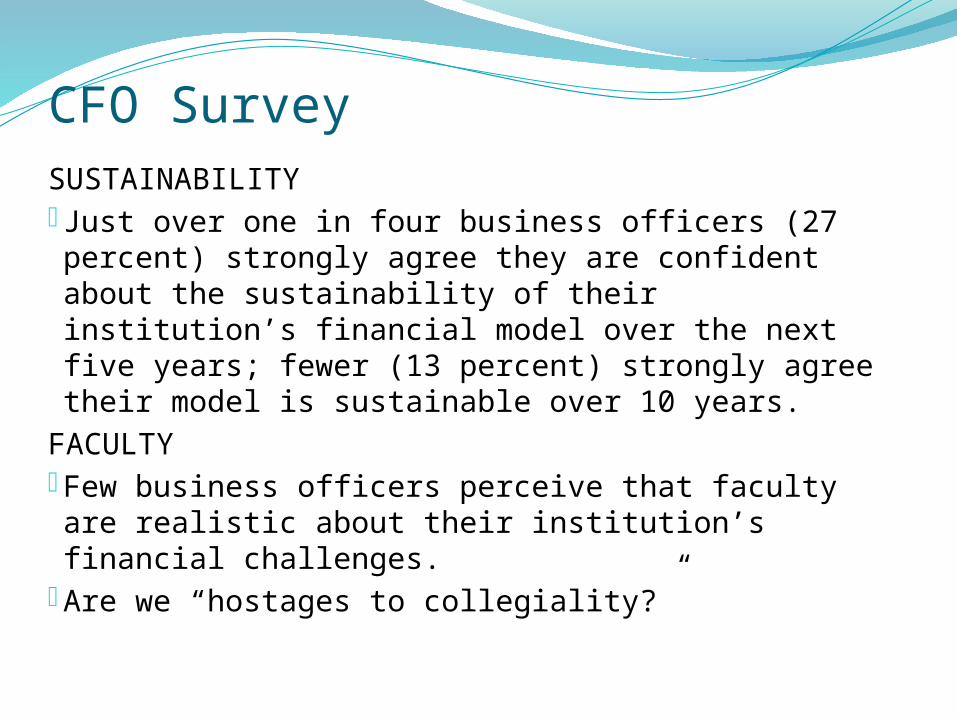

CFO SurveySUSTAINABILITY Just over one in four business officers (27 percent) strongly agree they are confident about the sustainability of their institution’s financial model over the next five years; fewer (13 percent) strongly agree their model is sustainable over 10 years.

FACULTYFew business officers perceive that faculty are realistic about their institution’s financial challenges.

Are we “hostages to collegiality?”

CFO SurveyBUSINESS MODEL and OPERATIONS Just 4 percent of business officers responding strongly agree that the

business model of for-profit universities is sustainable; over half (51 percent) say the same about elite private universities.

Health care costs: Nearly half of business officers (49 percent) strongly agree they have experienced increases in health care premiums for employees; nearly as many (46 percent) say the same regarding student premiums. Four in 10 business officers strongly agree their institution is more focused on the cost of providing health care and benefits than it was five years ago.

Enrollment: Most business officers (92 percent) say retaining current students is a very important strategy to increase revenue in the near future.

CFO Survey Efficiency: Many business officers (45 percent) say that using

technology tools, such as business analytics technology, to evaluate programs and identify problems/potential improvements is a very important strategy for reducing operating expenses at their institution.

But fewer than half say their institution has the program and performance data and information it needs to make informed decisions.

Collaboration: About six in 10 (59 percent) agree or strongly agree they were well-informed about campus issues, including budget, prior to accepting the job at the institution.

Debt: Only 3 percent strongly agree their institution should take on significantly more debt than it has now; seven times as many (21 percent) strongly agree their institution has increased the use of debt to finance projects.

Un-Reality Check? They Say…

2014 Colleges & University Presidents’ Surveyconducted by Gallup and Inside Higher Ed

Presidents’ Survey Seven in 10 presidents said their institutions would

face budget shortfalls and increased competition for students this year, in a climate of cutbacks of state and federal aid. But fewer than a third said they expected to take the sort of

strong actions – cutting administrative positions, freezing salaries, changing faculty roles or teaching loads – that would suggest deep concern, let alone panic, about their institutions' financial futures.

Nearly two-thirds of presidents are confident about the sustainability of their institution’s financial model over the next five years -- but that proportion falls to half over 10 years. (These numbers were 27% & 13% in CFO Survey.)

2013-14: Most Colleges Missed Goals

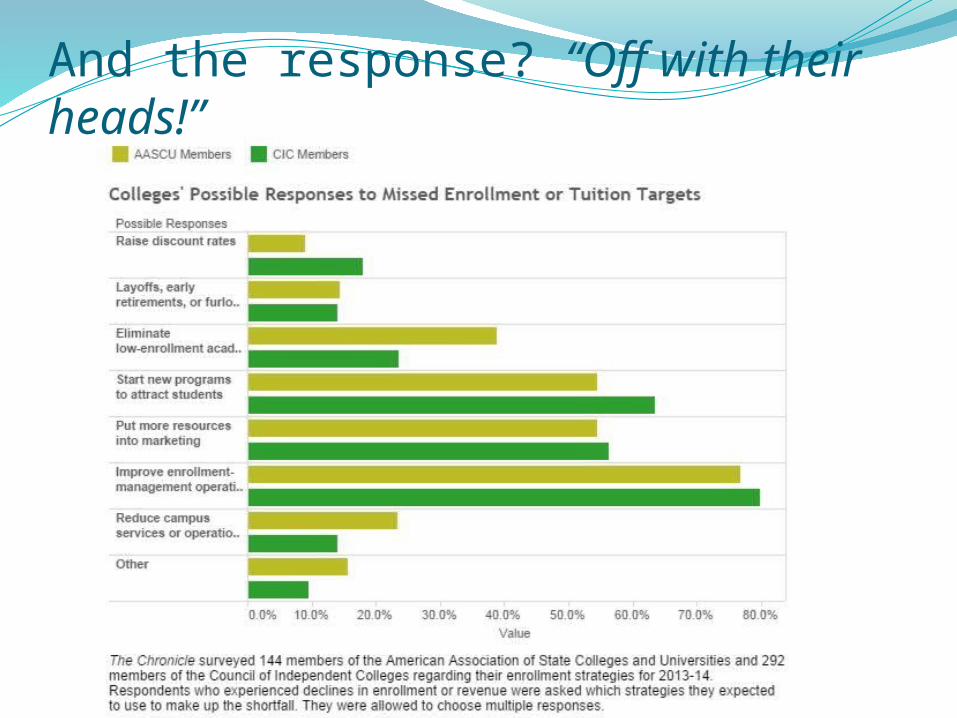

And the response? “Off with their heads!”

Where Solutions Will Be Found: DISTINCTIVENESS: not only having special value but having

your value KNOWN and APPRECIATED OPERATIONS: 85% see serious sustainability challenges yet

fewer than a third are doing anything about this (per KPMG). EXAMINE, AFFIRM or CHANGE your business models (cost

overhead, mergers, etc.) prioritize what's important, cost it out, match against realistic revenue, draw a line and eliminate below-the-line.

Sacred Cows (tenure, course loads, health care, TIAA, B&G, academic and extracurricular programs, etc.) will kill us. Highered may be “evergreen” but very few individual

institutions are! COLLABORATION: call it getting rid of silos or creating

synergy, no institution is optimized… demand on-going efforts and culture change.

How Solutions Will Be Driven: Survey after survey shows there are two sources of viable, reliable

intelligence on today’s campus The revenue producers The financial gatekeepers There are no universal Silver Bullets Each campus culture and college market position is unique, requiring

custom intel garnered from our experience Who better than vested “owner-operators” to bring data and insist

that acknowledging reality is not a lowering of ambitions? There will be winners and losers in the years ahead, and the

“winners” will be those who proactively adapted – not panicked or capitulated – early.

Let’s go home feeling empowered. Highered deserves no less.

Highered deserves no less