Embed Size (px)

Citation preview

1

Latin American Scenario July 2018

Challenging environment for Latin America Constantin Jancsó

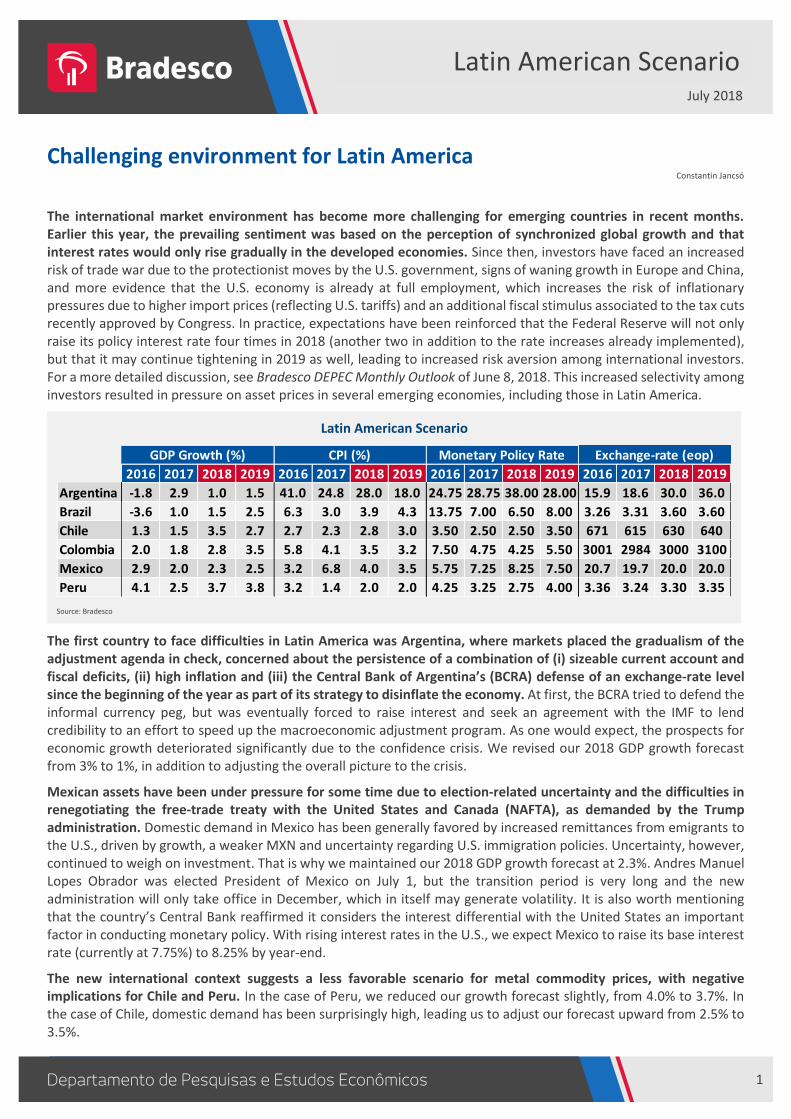

The international market environment has become more challenging for emerging countries in recent months. Earlier this year, the prevailing sentiment was based on the perception of synchronized global growth and that interest rates would only rise gradually in the developed economies. Since then, investors have faced an increased risk of trade war due to the protectionist moves by the U.S. government, signs of waning growth in Europe and China, and more evidence that the U.S. economy is already at full employment, which increases the risk of inflationary pressures due to higher import prices (reflecting U.S. tariffs) and an additional fiscal stimulus associated to the tax cuts recently approved by Congress. In practice, expectations have been reinforced that the Federal Reserve will not only raise its policy interest rate four times in 2018 (another two in addition to the rate increases already implemented), but that it may continue tightening in 2019 as well, leading to increased risk aversion among international investors. For a more detailed discussion, see Bradesco DEPEC Monthly Outlook of June 8, 2018. This increased selectivity among investors resulted in pressure on asset prices in several emerging economies, including those in Latin America.

The first country to face difficulties in Latin America was Argentina, where markets placed the gradualism of the adjustment agenda in check, concerned about the persistence of a combination of (i) sizeable current account and fiscal deficits, (ii) high inflation and (iii) the Central Bank of Argentina’s (BCRA) defense of an exchange-rate level since the beginning of the year as part of its strategy to disinflate the economy. At first, the BCRA tried to defend the informal currency peg, but was eventually forced to raise interest and seek an agreement with the IMF to lend credibility to an effort to speed up the macroeconomic adjustment program. As one would expect, the prospects for economic growth deteriorated significantly due to the confidence crisis. We revised our 2018 GDP growth forecast from 3% to 1%, in addition to adjusting the overall picture to the crisis.

Mexican assets have been under pressure for some time due to election-related uncertainty and the difficulties in renegotiating the free-trade treaty with the United States and Canada (NAFTA), as demanded by the Trump administration. Domestic demand in Mexico has been generally favored by increased remittances from emigrants to the U.S., driven by growth, a weaker MXN and uncertainty regarding U.S. immigration policies. Uncertainty, however, continued to weigh on investment. That is why we maintained our 2018 GDP growth forecast at 2.3%. Andres Manuel Lopes Obrador was elected President of Mexico on July 1, but the transition period is very long and the new administration will only take office in December, which in itself may generate volatility. It is also worth mentioning that the country’s Central Bank reaffirmed it considers the interest differential with the United States an important factor in conducting monetary policy. With rising interest rates in the U.S., we expect Mexico to raise its base interest rate (currently at 7.75%) to 8.25% by year-end.

The new international context suggests a less favorable scenario for metal commodity prices, with negative implications for Chile and Peru. In the case of Peru, we reduced our growth forecast slightly, from 4.0% to 3.7%. In the case of Chile, domestic demand has been surprisingly high, leading us to adjust our forecast upward from 2.5% to 3.5%.

Latin American Scenario

Source: Bradesco

2016 2017 2018 2019 2016 2017 2018 2019 2016 2017 2018 2019 2016 2017 2018 2019

Argentina -1.8 2.9 1.0 1.5 41.0 24.8 28.0 18.0 24.75 28.75 38.00 28.00 15.9 18.6 30.0 36.0

Brazil -3.6 1.0 1.5 2.5 6.3 3.0 3.9 4.3 13.75 7.00 6.50 8.00 3.26 3.31 3.60 3.60

Chile 1.3 1.5 3.5 2.7 2.7 2.3 2.8 3.0 3.50 2.50 2.50 3.50 671 615 630 640

Colombia 2.0 1.8 2.8 3.5 5.8 4.1 3.5 3.2 7.50 4.75 4.25 5.50 3001 2984 3000 3100

Mexico 2.9 2.0 2.3 2.5 3.2 6.8 4.0 3.5 5.75 7.25 8.25 7.50 20.7 19.7 20.0 20.0

Peru 4.1 2.5 3.7 3.8 3.2 1.4 2.0 2.0 4.25 3.25 2.75 4.00 3.36 3.24 3.30 3.35

GDP Growth (%) CPI (%) Monetary Policy Rate Exchange-rate (eop)

2

Latin American Scenario – July 2018

So far, Colombia has faced the more challenging external environment with certain ease. It was favored by high oil prices and positive expectations regarding the electoral victory of a presidential candidate committed to economic policy continuity. Our GDP growth forecast stands at 2.8% in 2018 and 3.5% in 2019. However, the persistence of a high current account deficit remains a major vulnerability in the new international context.

Exchange Rates (1/1/2018 = 100)

Source: Bloomberg and Bradesco

80

90

100

110

120

130

140

150

160

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18

ARS BRL CLP COP MXN PEN

Consumer inflation (Y/Y – %)

Source: Central Bank of Chile, DANE, Bank of Mexico, BCRP, IBGE, INDEC and Bradesco

2.0%

3.2%

4.5%

0.9%

2.9%

27.2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0%

2%

4%

6%

8%

10%

12%

13 14 15 16 17 18

Chile Colombia Mexico Peru Brazil Argentina (RHA)

3

Latin American Scenario – July 2018

Monetary policy Interest Rate – %

Source: BCB, Central Bank of Chile, Central Bank of Colombia, Bank of México, BCRP and Bradesco

6.50

2,50

4.25

7.75

2.75

0

2

4

6

8

10

12

14

16

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17 Jul-17 Dec-17 May-18

Brazil Chile Colombia Mexico Peru

GDP Growth (accumulated over 4 quarters – %)

Source: INDEC, IBGE, INE, DANE, INEGI, BCRP and Bradesco

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

06 07 08 09 10 11 12 13 14 15 16 17 18

Argentina Brazil Chile Colombia Mexico Peru

4

Latin American Scenario – July 2018

Current Account Balance (accumulated over 4 quarters – % GDP)

Source: INDEC, BCB, Central Bank of Chile, Central Bank of Colombia, Bank of Mexico, BCRP and Bradesco

-8

-6

-4

-2

0

2

4

6

8

06 07 08 09 10 11 12 13 14 15 16 17 18

Argentina Brazil Chile Colombia Mexico Peru

Structural Fiscal Balance of the General Government (IMF concept) – % GDP

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Argentina 2.8 1.4 1.5 0.2 -0.2 -0.7 -1.1 -2.7 -4.2 -3.8 -3.0

Brazil 3.4 1.9 3.6 4.2 3.7 3.0 0.7 0.2 -1.0 -1.1 -0.4

Chile 5.2 -3.8 0.2 2.0 1.1 0.0 -1.0 -1.5 -2.0 -2.0 -1.3

Colombia 2.9 0.5 -0.5 0.7 3.0 1.3 0.3 -0.9 0.6 0.7 1.0

Mexico 1.7 -0.1 -0.9 -0.6 -0.6 -0.4 -1.1 -1.2 -0.1 1.4 0.2

Peru 4.2 0.0 1.0 3.3 3.4 2.0 0.7 -1.0 -1.5 -1.9 -2.2 The structural fiscal balance corresponds to the nominal fiscal balance, adjusted for the economic cycle, changes in asset prices, and by certain non-recurrent revenues and expenditures.

Source: IMF, Bradesco

5

Latin American Scenario – July 2018

Argentina

The Argentine economy sustained a strong growth rate in the first quarter: +3.6% year over year and +1.1% compared to 4Q17 (seasonally adjusted). The second quarter, however, was far more challenging.

Argentina was one of the first emergent countries to be affected by increased risk aversion in the international market, making it difficult for it to purse a gradualist macroeconomic adjustment strategy. The persistence of twin fiscal and current account deficits triggered a loss of confidence that resulted in significant pressure on the exchange-rate.

The BCRA (Central Bank of Argentina) had adopted an informal exchange-rate peg at ARS/USD 20-21 throughout the first quarter as part of its effort to disinflate the economy. Between April 23 and May 2, the institution sold USD 4.9 billion (almost 10% of the international reserve stock at that time) to defend this peg. Unsuccessful, the monetary authority ended up hiking the policy rate from 27.5% to 40% at the beginning of May. The BCRA also lowered the limit on long foreign currency positions for local banks from 30% to 10% of their capital (this limit was later lowered again, to 5%, in June), while the Ministry of Finance announced fiscal policy tightening, reducing the target for the primary deficit in 2018 from 3.2% to 2.7% of the GDP.

The federal government of Argentina has a reasonable level of gross public debt at 57.1% of the GDP at the end of 2017. Additionally, almost half of this debt is in the hands of other entities of the public sector (especially the Central Bank). The portion held by the private sector was 29.6% of the GDP. But 80% of that debt in the hands of the private sector is denominated in or indexed to the U.S. dollar, which results in the country having little tolerance for exchange-rate volatility.

In addition to the more ambitious fiscal target, Argentina sought to reinforce the credibility of its economic policy by seeking IMF assistance. For a total of USD 50 billion, this program ratified the new fiscal target for 2018 and

After a strong performance in the first quarter, the economy will have likely slowed down in the second quarter due to the currency crisis.

Argentina will cease to pursue a gradualist reform agenda and with the IMF agreement, will now adopt adjustment measures more quickly.

We lowered our GDP growth forecast for 2018 to 1%. We expect second quarter retraction of 1-1.5% with respect to the first quarter.

Argentine Peso/USD

Source: Bloomberg, Bradesco

15

17

19

21

23

25

27

29

Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18

Primary Result of the Central Government (% GDP)

Note: Values for 2018 and 2019 correspond to the new fiscal targets set in the IMF agreement.

Source: Ministry of Finance, Bradesco

-0.7-1.1

-2.3

-3.4

-4.0-4.3

-3.9

-2.7

-1.3

-5

-4

-3

-2

-1

0

2011 2012 2013 2014 2015 2016 20172018

(T)2019

(T)

6

Latin American Scenario – July 2018

established a faster adjustment trend for the coming years, with the target of zero primary deficit by 2020.

The agreement with the Fund implies less intervention in the foreign exchange market: in the Economic and Financial Policy Memorandum, Argentina agrees “[it is] fully committed to a flexible and market-determined exchange rate”, “to limit the sales of foreign currency reserves to periods when there is clear market dysfunction” and “Even then… to absorb such external pressures through a flexible exchange rate and very limited foreign currency sales”. There will be a program to accumulate reserves in the medium term and all sales of foreign currency will be made at auction.

Another important aspect of the agreement with the IMF is the end of the Central Bank’s financing of the Treasury deficit. The government is committed to redeeming non-negotiable bonds previously issued to the BCRA’s portfolio, and to appropriately capitalize the Central Bank.

Half of the initial USD 15 billion disbursement will be allocated to finance the Treasury’s budget deficit. These resources will be converted into ARS in daily auctions of USD 100 million conducted by the BCRA, and also comprises the bulk of FX intervention planned for the coming months. There is also a plan for the Central Bank not to sterilize the monetary impact of these FX sales. The monetary contraction caused by the auctions will be offset by the net redemption of Central Bank bills (LEBACs) in the market, whose rolling-over has been a source of volatility.

Finally, the IMF agreement also lays out new inflation targets for 2018 and 2019 and a mechanism for consultations between Argentina and the Fund if inflation falls outside the tolerance bands, and prior to the BCRA beginning to reduce interest rates.

A good news for Argentina was its promotion from frontier market to emerging market in the MSCI indexes. Despite all the current uncertainty, this change in classification of Argentine assets will likely lead to increased foreign portfolio investment.

After solid growth in the first quarter, GDP growth was most likely negative in the second quarter. Agricultural output was affected by a drought and the currency crisis was a significant negative confidence shock. We estimate a 1%-1.5% Q/Q contraction of GDP in 2Q18, led by lower investment, and growth of 1% for 2018 as a whole.

Consumer inflation (%)

Note: The agreement with the IMF sets two tolerance bands for inflation. If inflation moves outside the internal band, the agreement requires Argentina to enter consultations with IMF staff. Inflation moving outside the external band triggers full consultations with the IMF board, including a discussion of remedial actions, as needed.

Source: Indec, IMF, Bradesco

10

15

20

25

30

35

40

45

50

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

Jan

-17

May

-17

Sep

-17

Jan

-18

May

-18

Sep

-18

Jan

-19

May

-19

Sep

-19

New Targets(IMF agreement)

Current Account Balance

(Accumulated over 4 quarters – USD billion)

Source: INDEC, Bradesco

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

4T0

6

3T0

7

2T0

8

1T0

9

4T0

9

3T1

0

2T1

1

1T1

2

4T1

2

3T1

3

2T1

4

1T1

5

4T1

5

3T1

6

2T1

7

7

Latin American Scenario – July 2018

Chile

Improved confidence after the election of President Sebastian Piñera, in December of last year, helped fuel a sustained economic recovery. GDP grew 4.2% in the first quarter year over year and 1.2% at the margin (seasonally adjusted).

First quarter year over year growth was widespread, led by the mining sector and, to a lesser extent, by trade. From the side of demand, GDP was driven by household consumption and investment in machinery and equipment. Note that the comparison base is particularly weak due to the effects of the strike that paralyzed the Escondida mine (the largest copper mine in the world) for almost a month and a half early last year. As a result, mining GDP expanded by 19.3% y/y.

In general, the high frequency economic indicators have surprised to the upside over the past few months. Along with the strong GDP performance in the first quarter, this led to a significant improvement in growth expectations. According to the Economic Expectations Survey of the Central Bank of Chile (BCCh), the median 2018 growth forecast rose from 3.0% late last year to 3.8% in June. Expectations for growth in 2019 accelerated from 3.3% to 3.8% over the same period. The median estimate for the IMACEC index (an estimate of monthly GDP) 12 months out expanded from 2.3% to 4.2% over the first half.

At the end of the first quarter, the BCCh communication suggested concern regarding the decline of inflation, from 2.3% y/y late last year to 1.8% y/y in March – below the floor of the tolerance interval around the inflation target of 3%. The decline in inflation surprised markets and occurred in the context of CLP appreciation, leading us to forecast an interest rate cut at the May monetary policy meeting, which did not materialize (see Inflation surprises in 2018 pave the way for interest cuts in Latin America – Bradesco Depec Highlight of April 25, 2018).

Chilean peso (CLP/USD) and Copper (USD/ton-LME)

(Price of copper in inverted axis)

Price of Copper is the 3rd future of the LME.

Source: Bloomberg, Bradesco

4.000

4.500

5.000

5.500

6.000

6.500

7.000

7.500400

450

500

550

600

650

700

750

Dec-15 Jul-16 Feb-17 Sep-17 Apr-18

CLP (LHA) Copper (RHA - inverted

Market expectations for growth in 2018 accelerated from 3% at the end of last year to 3.8% in June.

With inflation back at 2% and economic recovery, the Central Bank may raise interest rates in 2019.

Disruptions in international trade and commodities prices are major risks for Chile.

GDP (YoY – %)

Source: Central Bank of Chile, Bradesco

1T17 2T17 3T17 4T17 1T18

GDP -0.4 0.5 2.5 3.3 4.2

Mining -17.4 -5.5 8.3 6.8 19.3

X-mining 1.1 1.1 2,0 2.9 3.1

Domestic demand 2.5 3.6 2.2 4,0 3.8

Consumption 2.4 2.8 2.5 3.1 3.6

Household 2,0 2.5 2.2 3,0 3.9

Government 5,0 4.3 3.7 3.4 2.7

Investment -2.3 -4.6 -0.9 2.7 3.6

Construct. -4.7 -6.7 -5.9 -1.7 2,0

Equipment 1.8 -0.8 8.1 10.8 6.5

Exports -4.4 -4.4 2.7 2.5 7.2

Imports 5.6 6.3 2,0 5.2 6.1

Ch. Inventories -0.4 0.2 0.3 0.5 0.6

8

Latin American Scenario – July 2018

Consumer inflation returned to 2% in May. Similarly, inflation expectations for 2018 (BCCh Economic Expectations Survey) recovered from 2.5% in April to 2.8% in June.

With inflation returning to the target and solid growth, we believe that policy rate (currently 2.5%) normalization is back on the radar. We expect the Central Bank to cautiously raise interest, but only in 2019.

As for President Piñera’s reform agenda, the government will likely continue working to simplify the tax reform passed in 2014 by President Bachelet, even if it has given up on the promise of reversing the increase in the corporate income tax rate to 27% (arguing that the government needs the resources to handle fiscal problems inherited from the previous administration).

Another important topic on the agenda is the adjustments of the Chilean social security system. The government abandoned the reform proposal prepared by the previous administration, but promises changes to strengthen retirement for the poor (a proposal has not yet been formalized). The problem faced by the system (and cause for protests in 2017) is that, for many people, the system’s individual capitalization accounts have not accumulated sufficient assets (partly because lower interest rates caused the return rate to fall below expectations), forcing workers to postpone retirement or to retire with less than expected.

The U.S. protectionist agenda and trade tensions around the world are a significant risk for Chile, not only due to commodities prices (especially copper), but also because the country’s economy is open and exposed to disturbances in international trade.

On the other hand, the CLP performed better than other Latin currencies since risk aversion increased in the international market, reflecting the good fundamentals of the Chilean economy.

We revised our 2018 growth forecast to 3.5% (from 2.5% early in the year), slightly below the consensus.

Consumer inflation (% y/y)

Note: Core inflation excludes fresh fruit, vegetables and fuel

Source: INE, Bradesco

1,0

2,0

3,0

4,0

5,0

6,0

Jan-14 Aug-14 Mar-15 Oct-15 May-16 Dec-16 Jul-17 Feb-18

CPI Core Target

Fiscal Result and Public Debt (% GDP)

Source: OECD, Bradeco

-6

-4

-2

0

2

4

6

8

10

0

5

10

15

20

25

30

35

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

General Govt. Debt (LHA)

General Govt. Fiscal Bal. (RHA)

9

Latin American Scenario – July 2018

Colombia

Ivan Duque was elected President of Colombia on June 17, receiving 54% of the vote, compared to 41.8% of his second round opponent, Gustavo Petro. Duque, who will take office on August 7, will have a majority in Congress.

There was uncertainty early in the campaign regarding the electoral outcome and the outlook on continuity for the current reformist economic policy, but as polls began to show favoritism for Duque, the election was no longer a determining factor for investor confidence.

Oil prices play a key role in Colombia’s economy –for fiscal accounts, terms of trade and the external accounts. Climbing oil prices after the global financial crisis of 2009 allowed the country to finance the strong increase in domestic demand without significantly pressuring the deficit in current transactions. Despite the current account deficit having remained stable at around 3% of the GDP between 2009 and 2012, we estimate that the deficit adjusted by the change in terms of trade for the period increased to 8% of the GDP (see Bradesco DEPEC Highlight: Latin America to benefit from rising commodities, of March 14, 2018). Consequently, the decline in oil prices required Colombia to make strong external account adjustments as of 2013, with depreciation of the peso and slower growth.

In the opposite direction, higher oil prices in recent years facilitated the adjustment of the external accounts. The Colombian peso is among the best performing EM currencies in 2018 due to the combination of higher oil prices, favorable expectations regarding the election and early signs of an economic recovery.

As in other countries in the region, inflation was surprisingly low at the end of the first quarter, closing March at 3.14%, compared to 4.09% at the end of 2017, mainly driven by low food inflation. This downward surprise led the Central Bank of Colombia (Banrep) to reduce the base interest rate from 4.50% to 4.25% during its meeting in late April, even after having signaled it expected to keep the policy rate stable after the preceding meeting.

Ivan Duque was elected as president of Colombia and should rely on a Congressional majority when he takes office on August 7, which should be positive for investor confidence.

We expect inflation to stabilize at around 3% and growth to gradually expand (from 2.8% in 2018 to 3.5% in 2019), with no significant increase in the trade deficit.

The Colombian peso has performed better than its peers, despite the external accounts deficit. Thus, the increase in risk aversion on the international market is an important factor.

Colombian Peso (COP/USD) and Brent-type Oil Price (USD/barrel)

Source: Bloomberg, Bradesco

20

30

40

50

60

70

80

902000

2200

2400

2600

2800

3000

3200

3400

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

COP (LHA) Oil (Brent) - inverted (RHA)

GDP (%)

Source: DANE, Bradesco

4,6 4,73,0

2,0 1,8

-6

-4

-2

0

2

4

6

8

10

12

14

2013 2014 2015 2016 2017

Consumption Investment Exports

Imports GDP

10

Latin American Scenario – July 2018

Banrep justified its decision by explaining that in a context of COP appreciation and low food inflation, its estimate for 2018 GDP growth (2.7%) implied in a wider output gap and, therefore, an increased risk of inflation remaining below target at the end of the year.

In fact, although the 1Q18 GDP grew by 2.8% y/y and 0.7% at the margin (after having expanded 0.5% in the fourth quarter and 0.4% in the third quarter), the average unemployment rate in the first 4 months of 2018 was 10.4%, compared to the 10.2% during the same period last year, and unemployment rose from 8.9% in April 2017 to 9.5% in the same month of 2018.

Inflation seems to have stabilized at around 3%, after effects of currency depreciation in 2015 (the COP fell by about 50%) and the tax reform of early 2017 (that increased the VAT from 16% to 19%, among other measures) dissipated.

The expectation for 2019 is that the current level of oil prices, monetary stimulus and increased confidence after the election are positive for investment, which expanded only 0.9% in 2017, with a year over year drop of 5.6% in 1Q18 after contracting 0.9% in 2016. Consumption, on the other hand, should continue to be an important factor in sustaining the economy, with growth of 4.9% in 2016 and 3.7% in 2017 (3.3% in 1Q18). As a result, we forecast slightly faster growth in 2018 and 2019 (2.8% in 2018 and 3.5% in 2019).

Although the current account deficit fell from 6.3%/GDP in 2015 to 3.3% in 2017 on the back of COP depreciation and weaker growth, it remains relatively high compared to Latin American peers. As a result, greater risk aversion in the international market is an important challenge for the country, especially in the case of any downward corrections to the price of oil, where high levels have been a positive vector for Colombia’s currency until now.

Real Exchange Rate and Terms of Trade (Dec. 2009 = 100)

Real Exchange: basket of currencies weighted by the 22 major partners, deflated by CPI.

Source: Banrep, Bradesco

0

50

100

1500

25

50

75

100

125

150

Jan-95 Oct-98 Jul-02 Apr-06 Jan-10 Oct-13 Jul-17

Real exchange rate (LHA)

Terms of trade (inverted - RHA)

Consumer inflation (% y/y)

The most commonly used measure of core inflation in Colombia is Basic Inflation, which corresponds to the IPC x-food.

Source: DANE, Banrep, Bradesco

0

2

4

6

8

10

Jan-13 Nov-13 Sep-14 Jul-15 May-16 Mar-17 Jan-18

CPI Core Target

11

Latin American Scenario – July 2018

Mexico

The Mexican general elections were held on Sunday, July 1. Andrés Manuel Lopez Obrador (better known by his initials AMLO) won with 24.1 million votes (just under 53% of valid votes), well ahead of Ricardo Anaya, with 10.2mn (or 22.5% of valid votes), and Jose Antonio Meade, with 7.5mn (16.4% of valid votes). AMLO’s term in office will be of six years, without the possibility for reelection, and the transition period is particularly long: he will only take the oath of office in December. AMLO’s coalition also won a majority in both Houses of Congress.

Two factors caused volatility in Mexican asset prices throughout the first half of the year: uncertainty regarding the continuity of the economic policy and negotiations with the United States and Canada to reform the North American Free Trade Agreement (NAFTA), as required by President Trump.

As for the prospects of the AMLO administration, two topics drew investor attention during the campaign: the construction of a new airport in Mexico City and whether there will be changes to the energy sector reform, which opened the oil exploration segment to private and international companies.

The construction of the new airport and its administration have already been granted to private companies, but AMLO has been strongly critical of the project’s costs. Early in the campaign, he promised to cancel the entire project, but has adopted a more conciliatory tone in recent months, talking about project revisions. As for the oil sector, the candidate says that contracts already signed will be respected, but that there would be no new concessions to the private sector. The remainder of the candidate’s campaign has signaled that there will be no discrimination in other sectors to the private sector and that Mexico wants to continue attracting private and foreign investments. On other key economic issues, in his victory speech, AMLO promised to respect Central Bank autonomy, promote macroeconomic stability and fiscal equilibrium.

Andres Manuel Lopez Obrador was elected President of Mexico on July 1.

Although negotiations for the NAFTA reform have not been concluded, the risk of the U.S. abandoning the free-trade area did not materialize.

We estimate growth of 2.3% in 2018 and 2.5% in 2019. We believe that inflation should stabilize at around 4%, but the Bank of Mexico should continue to raise the base interest rate, maintaining the interest rate differential with the U.S. stable.

Mexican Peso (MXN/USD) and Brent-type Oil Price (USD/barrel)

Source: Bloomberg, Bradesco

20

30

40

50

60

70

80

9010

12

14

16

18

20

22

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

MXN (LHA) Oil - inverted (RHA)

Primary Balance and New Debt of the General Government (% of the GDP)

Note: The increase in the debt of over 10% of the GDP in 2009 is the result of recognizing pension liabilities due to the reform of the ISSSTE (social security institute for civil servants).

Source: Banco de México, Bradesco

0

10

20

30

40

50

-2

-1

0

1

2

3

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Net Public Debt (RHA) Primary Balance (LHA)

12

Latin American Scenario – July 2018

NAFTA negotiations were the other major cause for concern in the first half of the year. Several thematic rounds of negotiation were conducted since last year, but it became clear at the end of March that at that pace, the negotiations would not be completed in time for the new treaty to be ratified by the congresses of Mexico and the USA before elections in both countries. There was a concentrated effort by the countries, which conducted virtually continuous negotiations throughout April and most of May, but it was not enough to reach common ground on issues such as local automobile content, intellectual property, etc.

Despite the unsuccessful negotiations, the risk of the U.S. leaving NAFTA unilaterally (to do so, they would only need to give a 6-month notice) did not materialize and the agreement remains in effect. However, the risk is that, with the change in the Mexican government and the possibility that one of the houses of the U.S. Congress could pass to Democratic Party control, the negotiations could return to square one, even the President-elect indicated he generally agrees with the positions of the Mexican negotiating team.

The Mexican economy performed well in the first quarter. Private investments are still a bit retracted due to the uncertainties, but consumption has grown at a good pace – despite the tightening of monetary policy – spurred mainly by growth of savings remittances from Mexican emigrants to the U.S., driven by the strong U.S. economy, uncertainties regarding U.S. immigration policy and MXN weakness.

GDP growth reached 1.3% y/y in the first quarter (1.1% with respect to the fourth quarter of last year, seasonally adjusted). Private consumption expanded by 2.6% y/y (1.5% q/q, seasonally adjusted). We maintain our growth forecast of 2.3% for the year as a whole unchanged. For 2019, we forecast growth of 2019. Inflation is gradually converging back to the target after rising significantly in the last year, mainly due to the depreciation of the Mexican peso (MXN). Nevertheless, the Central Bank of Mexico (whose Board of Directors has a fixed mandate and autonomy with respect to the government) has remained cautious. In June, it raised the base interest rate to 7.75% and advised that it will maintain a prudent stance by closely monitoring the pass-through of exchange rate depreciation to inflation, the output gap and the interest-rate differential with the United States. We expect inflation to stabilize at around 4% and the Bank of Mexico to raise interest twice more in 2018, to 8.25 percent, maintaining the interest differential with the United States stable.

Supply and Aggregate Demand (annual %)

GDP on the expenditure side is usually presented in Mexico in the format above, separating aggregate demand from aggregate supply.

Source: Banco de México, Bradesco

2014 2015 2016 2017 1Q18

Aggregate Supply 3.6 3.9 2.9 3.2 2.4

GDP 2.8 3.3 2.9 2.0 1.3

Imports 5.9 5.9 2.9 6.5 5.7

Aggregate Demand 3.6 3.9 2.9 3.2 2.4

Consumption 2.2 2.6 3.6 2.6 2.3

Private 2.1 2.7 3.8 3.0 2.6

Government 2.6 1.9 2.4 0.1 1.1

Investment 3.1 5.0 1.1 -1.5 1.5

Private 4.5 8.9 2.0 -0.5 0.8

Public -2.3 -10.7 -3.4 -6.6 6.4

Exports 7.0 8.4 3.5 3.8 1.6

Inventories -20.9 -11.1 6.6 -4.7 17.0

Consumer inflation (% y/y)

Core inflation excludes fresh agricultural products, energy and utility prices regulated by the government.

Source: INEGI, Bradesco

0

1

2

3

4

5

6

7

Jan-13 Oct-13 Jul-14 Apr-15 Jan-16 Oct-16 Jul-17 Apr-18

INPC Core Target

13

Latin American Scenario – July 2018

Peru

Former President Pedro Paulo Kuczynski resigned from office on March 21, hours before the Peruvian Congress was to resume the debate on his impeachment. Vice-President Martin Vizcarra assumed the office.

Political noise did not weigh on investor confidence. On the contrary: since President Kuczynski’s relationship with Congress had been very troubled for several months, Vizcarra is expected to be more effective as President.

The external backdrop was quite positive for Peru, at least until the recent turmoil. Like Chile, Peru is an open economy that is sensitive to metal commodities prices.

Consumer inflation fell sharply at the end of 2017, from 2.7% y/y in June of last year to 1.4% by the end of 2017 and 0.4% at the end of 1Q18, before returning to 0.9% in May. This deceleration was mainly a result of food inflation dynamics: inflation excluding food remained stable between 2.0% and 2.5% throughout the period, which is consistent with the inflation target of 2.0%.

Inflation expectations remain well-anchored (consensus stood at 2.1% in 2018 and 2.5% in 2019, according to a survey conducted by the Central Bank of Peru – BCRP).

The economy has shown signs of recovery in 2018, but the Central Bank assesses that the GDP remains below potential. The YoY rate of GDP growth in the period from January to April (Peru estimates GDP growth monthly) reached 4.4%, with significant contribution from domestic demand (+5.1%) and, in particular, from the formation of inventories.

For the year as a whole, we project growth of 3.7% and 2.0% consumer inflation. As for monetary policy, we believe that the BCRP will maintain the reference rate at 2.75% until the end of the year.

The political noise caused by the resignation of Pedro Paulo Kuczynski from the Presidency and First Vice-President Martin Vizcarra taking office did not weigh on investor confidence.

Consumer inflation dropped sharply in the second half of 2017 due to food inflation, to only 0.4% y/y in March, but is expected to return to the 2% target by the end of the year.

The economy has been recovering and we forecast growth of 3.7% in 2018 as a whole.

Peruvian Sol (PEN/USD) and Copper (USD/ton-LME)

(Price of copper in the inverted axis)

Note: Peru has a floating exchange rate regime, but the Sol (PEN) has very low volatility. Price of Copper refers to the 3rd future at the LME.

Source: Bloomberg, Bradesco

4000

4500

5000

5500

6000

6500

7000

7500

80002,00

2,20

2,40

2,60

2,80

3,00

3,20

3,40

3,60

3,80

4,00

Dec-15 Jul-16 Feb-17 Sep-17 Apr-18

PEN (LHA) Copper (RHA) - inverted

Consumer inflation (% y/y)

Core inflation excludes volatile foods or those subject to external shocks, fuel, regulated rates and public transportation.

Source: INEI, BCRP, Bradesco

0,0

1,0

2,0

3,0

4,0

5,0

Jan-13 Oct-13 Jul-14 Apr-15 Jan-16 Oct-16 Jul-17 Apr-18

CPI Core Target

14

Latin American Scenario – July 2018

Economics Team

Director of Economic Research and Studies Fernando Honorato Barbosa

Economists Andréa Bastos Damico / Constantin Jancsó / Daniela Cunha de Lima / Ellen Regina Steter / Estevão Augusto Oller Scripilliti / Fabiana D’Atri / Igor Velecico / Leandro Câmara Negrão / Mariana Silva de Freitas / Myriã Tatiany Neves Bast / Priscila Pacheco Trigo / Rafael Martins Murrer / Thomas Henrique Schreurs Pires

Interns Ana Beatriz Moreira dos Santos / Camila Medeiros Tanomaru / Felipe Yamamoto Ricardo da Silva / Isabel Cristina Oliveira / Lucas Maia Campos / Renan Bassoli Diniz / Thaís Rodrigues da Silva

DEPEC – BRADESCO may not be held liable for any acts/decisions taken on the basis of the information available through its publications and projections. All data or opinions contained in the information herein is carefully checked and prepared by fully qualified professionals, but should not be taken, under any circumstances, as a basis, support, guidance or standard for any document, assessment, judgment or decision-making, of a formal or informal nature. Therefore, the user hereby undertakes sole responsibility for all consequences arising from the use of the data or analyses hereof, hereby exempting BRADESCO from all claims thereof. Upon accessing the information hereof, users hereby accept these terms of use and responsibility. Total or partial reproduction of this publication is strictly prohibited, except upon due authorization from Banco BRADESCO or full citation of the source (including the authors, the publication, and Banco BRADESCO).