Embed Size (px)

Citation preview

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-1

Chapter 8

Reporting and Analyzing Long-Term Operating Assets

Learning Objectives – coverage by question

Mini-exercises

Exercises Problems Cases

LO1 – Describe and distinguish between tangible and intangible assets.

17 31 38, 39

LO2 – Determine which costs to capitalize and report as assets and which costs to expense.

11,17 22 38, 39

LO3 – Apply different depreciation methods to allocate the cost of assets over time.

12, 13, 16, 18 22, 23, 24,

25, 26, 27, 28

LO4 – Determine the effects of asset sales and impairments on financial statements.

14, 15 22, 24, 26, 35 36, 38, 39 40 42

LO5 – Describe the accounting and reporting for intangible assets.

17, 21 31, 34 37, 38 42

LO6 – Analyze the effects of tangible and intangible assets on key performance measures.

20, 21 29, 30, 33 41 42

LO7 – Explain the accounting for acquisition and depletion of natural resources.

19 32

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-2

QUESTIONS Q8-1. Routine maintenance costs that are necessary to realize the full benefits of

ownership of the asset should be expensed. However, betterment or improvement costs should be capitalized if the outlay enhances the usefulness of the asset or extends the asset’s useful life beyond original expectations. As would be the case with any cost, an immaterial amount should be expensed as incurred.

Q8-2. Capitalizing interest costs as part of the cost of constructing an asset reduces interest expense, and increases net income during the construction period. In subsequent periods, the interest costs that were capitalized as part of the cost of the asset will increase the periodic depreciation expense and reduce net income.

Q8-3. As any asset is used up, its cost is removed from the balance sheet and transferred into the income statement as an expense. Capitalization of costs onto the balance sheet and subsequent removal as expense is the essence of accrual accounting. If the cost of a depreciable asset is recognized in full upon purchase, profit would be inaccurately measured: it would be too low in the year of purchase when the asset is expensed and too high in later years as revenues earned by the asset are not matched with a corresponding cost. The proper matching of costs (expenses) and revenues is essential for the proper recognition of profit.

Q8-4. The primary benefit of accelerated depreciation for tax reporting is that the higher depreciation deductions in early periods reduce taxable income and income taxes. Cash flow is, therefore, increased, and this additional cash can be invested to yield additional cash inflows (e.g., an "interest-free loan" that can be used to generate additional income). We would generally prefer to receive cash inflows sooner rather than later in order to maximize this investment potential.

Q8-5. When a change occurs in the estimate of an asset's useful life or its salvage value, the revision of depreciation expense is handled by depreciating the current undepreciated cost of the asset (original cost – accumulated depreciation) using the revised assumptions of remaining useful life and salvage value.

Present and future periods are affected by such revisions. Depreciation expense calculated and reported in past periods is not revised.

Q8-6. The gain or loss on the sale of a PPE asset is determined by the difference between the asset's book value and the sale proceeds. Sales proceeds in excess of book values create gains; sales proceeds less than book values cause losses. The relevant factors, then, are the depreciation rate and salvage values used to compute depreciation expense, accumulated depreciation and the net book value of the asset, as well as the selling price of the asset.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-3

Q8-7. A PPE asset is considered to be impaired when the sum of the undiscounted expected cash flows to be derived from the asset is less than its current book value.

An impairment loss is calculated as the difference between the asset's book value and its current fair market value.

Q8-8. Research and development costs must be expensed under GAAP unless they have alternative future uses. Equipment relating to a specific research project with no alternative use would, therefore, be expensed rather than capitalized and subsequently depreciated.

Accounting standard-setters have justified this ‘expense as incurred’ treatment for R&D costs since the outputs from research and development activities are uncertain and there are, therefore, no expected cash flows against which to match any future depreciation expense.

Q8-9. The difficulty with amortizing intangible assets is estimating the useful life. For some intangibles, the useful life is limited and can be easily estimated. However, some intangibles have an indefinite life. This means that the useful life of the intangible is long and cannot be determined with any reasonable degree of accuracy. Under these circumstances, it is not appropriate to amortize the asset until the useful life can be determined.

Q8-10. Goodwill arises whenever a company acquires another company and the purchase price is greater than the fair value of the identifiable assets acquired. The amount of goodwill is the difference between the purchase price and the value assigned to the net assets of the acquired company. It is recorded as a long-term asset in the balance sheet.

Since goodwill is assumed to have an indefinite life, it is not amortized. The only time that goodwill might affect the income statement is if it is determined that its value is impaired. In that case, an impairment loss is recorded in the income statement and the value of the goodwill asset on the balance sheet is reduced.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-4

MINI EXERCISES M8-11 (10 minutes) a. expense b. capitalize c. capitalize (the new equipment enhances the assembly line) d. expense – this is routine maintenance of the building, unless it extends the

building’s useful life e. capitalize – the useful life is extended f. capitalize – this is a purchased intangible asset M8-12 (15 minutes) a. Straight-line: ($18,000 - $1,500)/ 5 years = $3,300 for both 2008 and 2009. b. Double-declining-balance: Twice straight-line rate = 2 x 1/5 = 40% 2010: $18,000 x 0.40 = $7,200 2011: ($18,000 - $7,200) x 0.40 = $4,320

Notice that, over the first two years, the company reports $6,600 of depreciation expense under the straight-line method and $11,520 of depreciation expense under the double-declining-balance method.

M8-13 (15 minutes) a. Straight-line: ($130,000 - $10,000)/ 6 years = $20,000 for both 2010 and 2011. b. Double-declining-balance: Twice straight-line rate = 2 x 1/6 = 1/3 2010: $130,000 x 1/3 = $43,333 2011: ($130,000 - $43,333) x 1/3 = $28,889 c. Units of production: ($130,000 - $10,000) / 1,000,000 = $0.12 per unit 2010: 180,000 units x $0.12 = $21,600 2011: 140,000 units x $0.12 = $16,800 M8-14 (15 minutes) Straight-line depreciation: $40,000/10 = $4,000; 8 years x $4,000 = $32,000. a. Cash (+A) ........................................................................................ 3,500 Accumulated depreciation (-XA, +A) ........................................... 32,000 Loss on sale of furniture and fixtures (+E, -SE) .......................... 4,500 Furniture and fixtures (-A) ............................................................. 40,000

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-5

M8-14—continued. b.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabi-lities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

Sold furniture and fixtures for cash.

+3,500 Cash

-40,000 Furniture

and Fixtures

-

-32,000 Accumulated Depreciation

-4,500 Retained Earnings

-

+4,500 Loss on Sale of

Furniture and

Fixtures

=

-4,500

M8-15 (15 minutes) Twice the straight-line rate = 1/5 x 2 = 40%

Year 1: $75,000 x .4 = $30,000 Year 2: ($75,000 - $30,000) x .4 = 18,000 Year 3: ($75,000 - $30,000 - $18,000) x .4 = 10,800 Total accumulated depreciation $58,800 a. Cash (+A) ........................................................................................ 25,000 Accumulated depreciation (-XA, +A) ............................................ 58,800 Machinery (-A) ................................................................................ 75,000 Gain on sale of machinery (+R, +SE) ............................................ 8,800 b.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabi-lities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

Sold machinery for cash.

+25,000 Cash

-75,000 Machinery

-

-58,800 Accumulated Depreciation

+8,800 Retained Earnings

+8,800 Gain on Sale of Machinery

-

= +8,800

M8-16 (15 minutes) a. Straight-line depreciation

2010: ($145,800 - $5,400)/3 = $46,800; (8/12) x $46,800 = $31,200

2011: $46,800 b. Double-declining-balance depreciation Preliminary computation: Twice straight-line rate = 2 x 100%/3 = 66⅔% ($145,800 x 66⅔%) = $97,200

2010: (8/12) x $97,200 = $64,800

2011: ($145,800 - $64,800) x 66⅔% = $54,000

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-6

M8-17 (20 minutes) a. Under U.S. GAAP, capitalization of development costs is not allowed and all R&D

costs must be expensed. Under IFRS, development costs are capitalized if there is the intention, feasibility and resources to bring the asset to completion, there exists the ability to use or sell the asset to generate an economic benefit. Otherwise the costs must be expensed.

b. Direct R&D personnel costs. Legal fees and registering costs. Overhead that cannot be allocated on a consistent basis including depreciation on equipment and amortization of patents and licenses related to the generation of the intangible. Administration, related promotion, and training expenses.

c. Yes, impairment should be tested for annually. M8-18 (20 minutes) a. Year Book value Depreciation rate Depreciation expense

1 $50,000 2 x ¼ = 0.5 $25,000 2 25,000 2 x ¼ = 0.5 12,500 3 12,500 4,500 4 8,000 0*

* No depreciation is recorded in Year 4 because the asset is depreciated to its residual value of $8,000.

b. Year Book value Depreciation rate Depreciation expense

1 $50,000 2 x 1/5 = 0.4 $20,000 2 30,000 2 x 1/5 = 0.4 12,000 3 18,000 2 x 1/5 = 0.4 7,200 4 10,800 2 x 1/5 = 0.4 4,320 5 6,480 3,480*

* $3,480 of depreciation is required in Year 5 to depreciate the asset to its residual value of $3,000.

c. Year Book value Depreciation rate Depreciation expense

1 $50,000 2 x 1/10 = 0.2 $10,000 2 40,000 2 x 1/10 = 0.2 8,000 3 32,000 2 x 1/10 = 0.2 6,400 4 25,600 2 x 1/10 = 0.2 5,120 5 20,480 2 x 1/10 = 0.2 4,096 6 16,384 2 x 1/10 = 0.2 3,277 7 13,107 2 x 1/10 = 0.2 2,621 8 10,486 2 x 1/10 = 0.2 2,097 9 8,389 2 x 1/10 = 0.2 1,678 10 6,711 5,711*

* $5,711 of depreciation is required in Year 10 to depreciate the remaining value of the asset. Alternatively, DeFond could switch to straight-line depreciation in Year 7, recording $3,027 of depreciation in Years 7 through 10.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-7

M8-19 (15 minutes) a. Year Barrels extracted Depletion per barrel Depletion 2010 300,000 $32,000,000 / 4,000,000 = $8 $2,400,000 2011 500,000 $32,000,000 / 4,000,000 = $8 $4,000,000 2012 600,000 $32,000,000 / 4,000,000 = $8 $4,800,000 b. i. Oil reserve (+A) ............................................................................... 32,000,000 Cash (-A) ......................................................................................... 32,000,000 ii. Oil inventory (+A) ............................................................................ 2,400,000 Oil reserve (-A) ................................................................................ 2,400,000 c.

+ Oil Reserve (A) - + Oil Inventory (A) -

i. 32,000,000 i. 2,400,000 2,400,000 ii.

Balance 29,600,000 Balance 2,400,000

M8-20 (15 minutes) a.

PPE turnover rates for 2007

Texas Instruments $12,501 / [($3,609 + $3,304) / 2] = 3.62

Intel Corp. $37,586 / [($16,918 + $17,544) / 2] = 2.18

Texas Instruments turns its PPE more quickly than does Intel.

b. PPE turnover rates increase with increases in sales volume relative to the dollar

amount of PPE on the balance sheet. The PPE turnover rate is often a very difficult turnover rate to change, and typically requires creative thinking. Many companies are outsourcing the manufacturing process in whole or in part to others in the supply chain. This is beneficial so long as the benefits realized by the reduction of manufacturing assets more than offset the higher cost of the goods as these are now purchased rather than manufactured. Another approach is to utilize long-term operating assets in partnership with another firm, say in a joint venture.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-8

M8-21 (15 minutes) a. $2,786,067 / $29,527,552 = 9.4%. Abbott’s R&D expenditure level could be compared to the R&D expenditure

level for its competitors to gain a sense of the appropriateness of its R&D expenditures.

b. R&D costs must be expensed when incurred unless acquired depreciable

assets have alternative future uses. As a result, the balance sheet does not reflect the costs incurred for long-term R&D assets. In addition, operating expenses are increased, thus reducing retained earnings.

($000) Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabi-lities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income R&D expenditures -2,786,067

Cash

=

-2,786,067

Retained Earnings

- +2,786,067 R&D Expense =

-2,786,067

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-9

EXERCISES E8-22 (15 minutes) a. Machine (+A) ................................................................................... 89,500 Cash (-A) ($85,000 + $2,000 + $2,500) ........................................... 89,500 b. ($89,500 - $7,000) / 5 = $16,500 per year.

Depreciation expense (+E, -SE) .................................................... 16,500 Accumulated depreciation (+XA, -A) ............................................. 16,500 c. Cash (+A) ......................................................................................... 12,000 Accumulated depreciation (-XA, +A) ($16,500 x 4) ...................... 66,000 Loss on sale of machine (+E, -SE) ................................................ 11,500 Machine (-A) .................................................................................... 89,500 E8-23 (20 minutes) a. Straight line: ($80,000 - $5,000)/5 years = $15,000 per year b. Double declining balance: Twice straight-line rate = 2 x 100%/5 = 40%

Year Book Value x Rate Depreciation Expense

1 $80,000 x 0.40 = $32,000

2 ($80,000 - $32,000) x 0.40 = 19,200

3 ($80,000 - $51,200) x 0.40 = 11,520

4 ($80,000 - $62,720) x 0.40 = 6,912

5 5,368 (plug)

Total $75,000

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-10

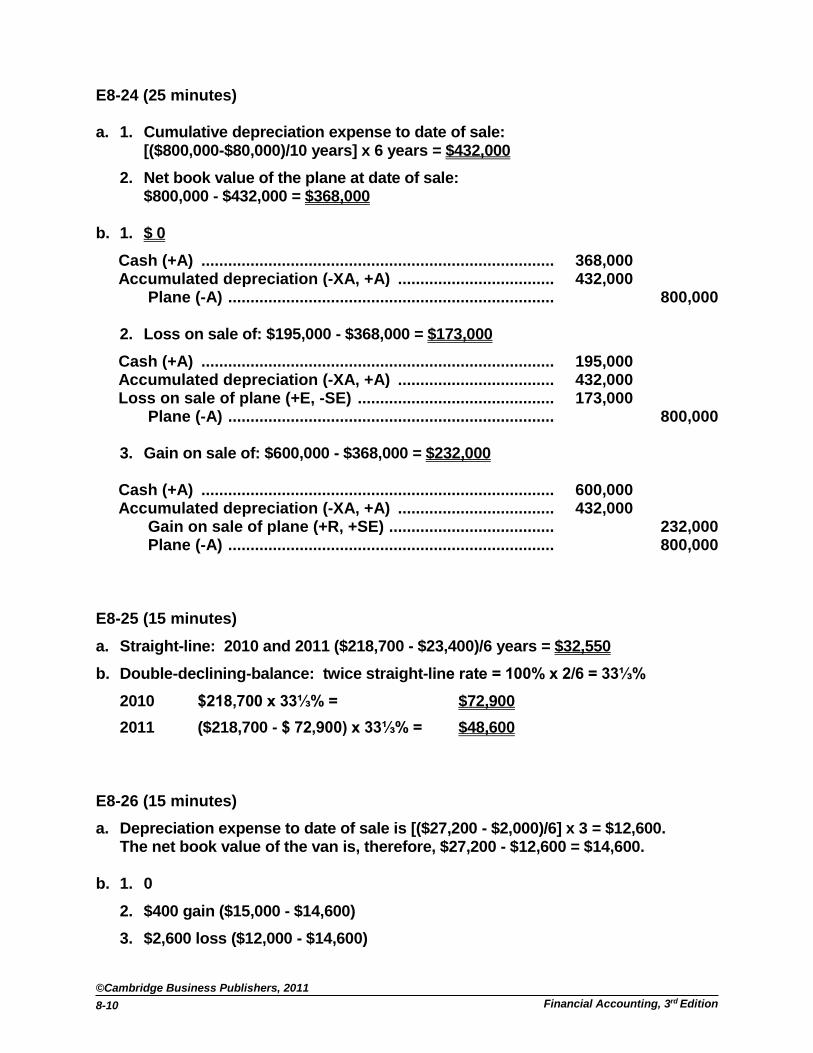

E8-24 (25 minutes) a. 1. Cumulative depreciation expense to date of sale: [($800,000-$80,000)/10 years] x 6 years = $432,000

2. Net book value of the plane at date of sale: $800,000 - $432,000 = $368,000 b. 1. $ 0

Cash (+A) ........................................................................................ 368,000 Accumulated depreciation (-XA, +A) ............................................ 432,000 Plane (-A) ......................................................................................... 800,000

2. Loss on sale of: $195,000 - $368,000 = $173,000

Cash (+A) ........................................................................................ 195,000 Accumulated depreciation (-XA, +A) ............................................ 432,000 Loss on sale of plane (+E, -SE) ..................................................... 173,000 Plane (-A) ......................................................................................... 800,000

3. Gain on sale of: $600,000 - $368,000 = $232,000

Cash (+A) ........................................................................................ 600,000 Accumulated depreciation (-XA, +A) ............................................ 432,000 Gain on sale of plane (+R, +SE) ..................................................... 232,000 Plane (-A) ......................................................................................... 800,000 E8-25 (15 minutes)

a. Straight-line: 2010 and 2011 ($218,700 - $23,400)/6 years = $32,550

b. Double-declining-balance: twice straight-line rate = 100% x 2/6 = 33⅓%

2010 $218,700 x 33⅓% = $72,900

2011 ($218,700 - $ 72,900) x 33⅓% = $48,600 E8-26 (15 minutes)

a. Depreciation expense to date of sale is [($27,200 - $2,000)/6] x 3 = $12,600. The net book value of the van is, therefore, $27,200 - $12,600 = $14,600. b. 1. 0

2. $400 gain ($15,000 - $14,600)

3. $2,600 loss ($12,000 - $14,600)

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-11

E8-27 (20 minutes)

a. Straight line: ($110,000 - $15,000) / 6 = $15,833 each year. b. Double-declining-balance: rate = 2 x 1/6 = 1/3.

2010: $110,000 x 1/3 = $36,667

2011: ($110,000 – $36,667) x 1/3 = $24,444

2012: ($110,000 – $36,667 – $24,444) x 1/3 = $16,296 c. Straight line: ($110,000 – $15,833x2 – $10,000) / 5 = $13,667 each year.

Double-declining balance: rate = 2 x 1/7 = 2/7.

($110,000 – $36,667 – $24,444) x 2/7 = $13,968 in 2012 E8-28 (20 minutes)

a. Straight-line: $6,000,000 / 30 = $200,000 per year each year. b. Double-declining balance: rate = 2 x 1/30 = 1/15.

2010: $6,000,000 x 1/15 = $400,000

2011: ($6,000,000 – $400,000) x 1/15 = $373,333 c. The revised depreciation rate = 2 x 1/25 = 8%

2012: ($6,000,000 – $400,000 – $373,333) x 8% = $418,133 E8-29 (10 minutes)

Percent depreciated = Accumulated depreciation / Asset cost

= $4,411 million / ($8,539 - $95 - $833) million = 58%

Note: We eliminate land and construction in progress from the computation because these assets are not depreciated.

Assuming that assets are replaced evenly as they are used up, we would expect assets to be 50% depreciated, on average. Deere’s 58% is higher than this level. Our concern is that it will require higher capital expenditures in the near future to replace aging assets.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-12

E8-30 (25 minute)

a. Receivable turnover rate Inventory turnover rate PPE turnover rate

2007 57.72

102,3$362,3$

462,24$

67.42

601,2$852,2$

735,12$ 92.3

2

907,5$582,6$

462,24$

2008 71.72

362,3$195,3$

269,25$ 56.4

2

852,2$013,3$

379,13$ 75.3

2

582,6$886,6$

269,25$

b. 3M’s Inventory and PPE turnover ratios have declined slightly while its

receivable turnover rates improved slightly. The latter could be due to monitoring more closely the quality of customers to which credit is granted, implementing better collection procedures, and offering discounts as an incentive for early payment. Inventory turnover rates can be improved by weeding out slowly moving product lines, by reducing the depth and breadth of products carried, and by implementing just-in-time deliveries. PPE turns can be improved by off-loading manufacturing to other companies in the supply chain and acquiring long-term operating assets in partnership with other companies, for example, in a joint venture.

E8-31 (10 minutes) a. Fair Value

(capitalized) Useful life

b. Amortization expense for 2009

Patent $200,000 3 years $66,667

Trademark $500,000 Indefinite

Noncompetition agreement

$300,000 5 years 60,000

$126,667

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-13

E8-32 (15 minutes) a. Cost of reserve: $7,200,000 + $420,000 + $50,000 = $7,670,000 Residual value: $1,200,000 – $800,000 = $400,000 Depletion base: $7,670,000 – $400,000 = $7,270,000 Depletion rate: $7,270,000 / 500,000 tons = $14.54 per ton

2010: 60,000 x $14.54 = $872,400

2011: 85,000 x $14.54 = $1,235,900 b. 2010: Inventory (+A) ................................................................................. 872,400 Resource reserve (-A) ..................................................................... 872,400 2011: Inventory (+A) ................................................................................. 1,235,900 Resource reserve (-A) .................................................................... 1,235,900 E8-33 (15 minutes) a. Percent depreciated – 2008: $10,070 / $11,280 = 89.3%

2007: $10,132 / $11,178 = 90.6% b. PPET: $91,451 / [(1,210 + 1,046)/2] = 81.1 times c. Adams’ assets are almost completely depreciated. This results in an

extremely high percent depreciated ratio and also a very high PPE turnover ratio (PPET). Adding inventories and receivables to get all the firm’s net operating asset turnover (NOAT) is more reasonable devisor. Adams outsources most of its manufacturing and, recognizing concerns that these numbers might produce, reports in its 10K that its current facilities (PPE assets) are adequate for the foreseeable future. Thus, although the ratios might suggest otherwise, the company does not anticipate large capital expenditures in the near future. Indeed this has been the case for the last several years as well.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-14

E8-34 (15 minutes) a. The list illustrates the wide range in expenditures for R&D (as a percent of

sales) across firms. Note the large amount spent by pharmaceutical companies Pfizer (16.45%) and Merck (20.15%), compared to the amount spent by Dell (1.09%). The companies in the list are paired by industry. It is interesting to see how similar some firms in the same industry are. For example, Callaway Golf and Adams Golf spend almost the same percentage of sales on R&D despite the fact that Callaway is several times larger than Adams. Similarly, Baxter International and Advanced Medical Optics, both in the medical/surgical instruments industry, are very similar. Also noteworthy is the significant difference between some firms in the same industry (e.g., Apple and Dell).

b. Beside industry affiliation, the differences in R&D expenditures as a percent of

sales is due to differences in markets, product mix, and other strategic considerations. Apple, for example, has established itself as a technological innovator and has spent millions of dollars developing unique products such as the Ipod. Dell, on the other hand, is best known for its operating efficiencies. Rather than developing new, innovative products, the company sells mainstream computers and peripherals using state-of-the-art inventory management and distribution methods. Because of its strategy, Apple relies on R&D to a much greater extent than does Dell.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-15

E8-35 (20 minutes) a. Yes, the equipment is impaired at July 1, 2010. This is because its book value is

not recoverable through future cash flows. Specifically, on July 1, 2010, its book value is $145,000 ($225,000 initial cost less $80,000 accumulated depreciation*) and the estimated future (undiscounted) cash flows are only $125,000.

*4 years of [($225,000-$25,000)/10 years]. b. The impairment loss in a is computed as the equipment's book value minus its

current fair value: $145,000 $90,000 = $55,000 Impairment loss (+E, -SE) .............................................................. 55,000 Equipment* (-A) .............................................................................. 55,000

* Accumulated depreciation is sometimes credited for the loss. c. Assuming that the salvage value remains the same after the impairment (this is

not likely given the decline in market value of the asset), the annual depreciation expense would be ($90,000 - $25,000) / 6 = $10,833 per year.

Depreciation expense (+E, -SE) ..................................................... 10,833 Accumulated depreciation (+XA, -A) ............................................ 10,833

d.

($000) Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabi-lities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

b. Impairment charge.

-55,000

Equipment -

-55,000 Retained Earnings

- +55,000

Impairment Loss

=

-55,000

c. Depreciation expense.

- +10,833

Accumulated Depreciation

-10,833 Retained Earnings

- +10,833

Depreciation Expense

=

-10,833

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-16

PROBLEMS P8-36 (20 minutes) (i) Land, buildings and equipment (+A) ............................................ 246,851 Cash (-A) ......................................................................................... 246,851 (ii) Depreciation expense (+E, -SE) ..................................................... 264,769 Accumulated depreciation (+XA, -A) ............................................ 264,769 (iii) Cash (+A) ......................................................................................... 5,473 Loss on sale of land, buildings and equipment (+E) ................... 4,021 Accumulated depreciation (-XA, +A) ............................................ 75,320 Land, buildings and equipment (-A) ............................................. 84,814

+ Land, Buildings and Equipment (A) - - Accumulated Depreciation (XA) +

Balance 3,928,936 2,121,158 Balance (i) 246,851 264,769 (ii) 84,814 (iii) (iii) 75,320

Balance 4,090,973 2,310,607 Balance

P8-37 (20 minutes)

a. $704 million / $5,774 million = 12.2%

b. R&D costs are expensed in the income statement except for the portion relating to depreciable assets that have alternate uses. Expensing (rather than capitalizing and depreciating) reduces assets, and the additional expense reduces profit and equity (via the reduction in retained earnings). In addition, expensing R&D as incurred means that potentially valuable intangible assets are omitted from the balance sheet.

c. Agilent has reduced its R&D spending as a percent of revenues in recent years and, as a result, increased its earnings. This has turned operating losses into an operating profit for the company. However, Agilent is dependent upon technology in order to maintain its market position, and R&D is critical to its very existence. The market is generally not very forgiving of technology-related companies that improve operating results via the reduction of R&D spending.

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-17

P8-38 (20 minutes)

($ millions)

a. Depreciation expense (+E, -SE) .................................................... 1,804 Accumulated depreciation (+XA, -A) ............................................. 1,804

b. Amortization expense (+E, -SE) ($1,826 - $1,804) ........................ 22 Accumulated amortization (+XA, -A) ............................................. 22

c. Property and equipment (+A) ........................................................ 3,547 Cash (-A) ......................................................................................... 3,547

d. Cash (+A) ........................................................................................ 49 Loss on sale of property and equipment (+E, -SE) ..................... 33 Accumulated depreciation (-XA, +A) (see T-account) ................. 631 Property and equipment (-A) (see T-account) .............................. 713

e. Repair and maintenance expense (+E, -SE) ................................. 609 Cash (-A) ......................................................................................... 609

+ Property and Equipment (A) - - Accumulated Depreciation (XA) +

Balance 31,982 7,887 Balance (c) 3,547 1,804 (a) 713 (d) (d) 631

Balance 34,816 9,060 Balance

P8-39 (20 minutes)

($ thousands)

a. Depreciation expense (+E, -SE) .................................................... 148,083 Accumulated depreciation (+XA, -A) ............................................. 148,083

b. Property and equipment (+A) ........................................................ 191,789 Cash (-A) .......................................................................................... 191,789

c. Loss on impairment of property and equipment (+E) ................. 33,995 Property and equipment (-A) ......................................................... 33,995

d. Cash (+A) ........................................................................................ 9,250 Loss on sale of property and equipment (+E, -SE) ...................... 39,317 Accumulated depreciation (-XA, +A) (see T-account) ................. 60,798 Property and equipment (-A) (see T-account) .............................. 109,365

+ Property and Equipment (A) - - Accumulated Depreciation (XA) +

Balance 1,843,101 862,026 Balance (b) 191,789 148,083 (a)

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-18

33,995 (c) 109,365 (d) (d) 60,798

Balance 1,891,530 949,311 Balance

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-19

CASES C8-40 (90 min)

a. PPE Turnover: $9,575/[($2,853 + $2,871)/2] = 3.35

Inventory Turnover: $7,165/[($1,099 + $1,024)/2] = 6.75 The firm does not appear to be as capital intensive as others in the industry based on a lower than average PPE turnover ratio than that in the industry. Further, their inventory turnover appears high given the firm’s business.

b. Accumulated depreciation / Depreciable asset cost $6,040/ ($8,893 - $154*- $231*- $367*) = 0.7419 or 74%

*Note: We eliminate land from the computation because land is never depreciated. We

eliminate construction in progress and capitalized interest because these represent assets that the company is building (and the interest paid on the construction loans). These assets are not yet in service and are consequently not yet depreciable. This elimination is also used in part c.

If plant assets are replaced at a constant rate, we would expect those assets to be about 50% “used up,” on average. A substantially higher percentage “used up” indicates that the assets are closer to the end of their useful lives and will require replacement (and usually higher maintenance costs near the end of their useful lives). Such a situation would negatively impact future cash flows. Rohm & Haas’s depreciable assets appear to be substantially “used up” based on this analysis.

c. Depreciable asset cost / Depreciation expense ($8,893 - $154*- $231* - $367*) / $467 = 17.4 years

d. Depreciation expense (+E, -SE) .................................................... 467 PPE accumulated depreciation (+XA, -A) .................................... 467

PPE (+A) .......................................................................................... 520 Cash (-A) ......................................................................................... 520

Impairment loss (+E, -SE) .............................................................. 42 PPE (-A) ........................................................................................... 42

e. The recognition of the impairment loss reduces operating income and this in turn reduces cash flow from operations. However, the loss is added back in the operating cash flow adjustments and so there is no impact on the company’s cash flow. In addition, the impairment charge is not deductible for tax purposes until the asset is disposed of, that is, until the loss is realized. Asset impairment

©Cambridge Business Publishers, 2011

Financial Accounting, 3rd Edition 8-20

charges are nonrecurring. Analysts would be justified in treating them as transitory (nonrecurring operating) items for analysis purposes.

C8-41 (40 minutes)

Reducing operating assets is an important means of increasing performance measures including the return on net operating assets. Most companies focus first on reducing receivables and inventories. This is the so-called low-hanging fruit that can lead to quick results. Some possible actions include those listed. Students will think of additional possibilities.

a. Reducing receivables through: 1. Better underwriting of credit quality 2. Better controls to identify delinquencies, automated over-due

notices, and better collection procedures 3. Increased attention to accuracy in invoicing 4. Offering early payment incentives

b. Reducing inventories and inventory costs through essentially

eliminating nonproductive activities including inspection, moving activities, waiting setup time, : 1. Use of less costly components (of equal quality) and production with

lower wage rates 2. Elimination of product features not valued by customers 3. Outsourcing to reduce product cost 4. Just-in-time deliveries of raw materials 5. Elimination of manufacturing bottlenecks to reduce work-in-process

inventories 6. Producing to order rather than to estimated demand to reduce

finished goods inventories 7. Eliminating defects

c. Reducing PPE assets is much more difficult. The benefits, however, can

be substantial. Some suggestions are the following: 1. Sale of unused and unnecessary assets 2. Acquisition of production and administrative assets in partnership

with other companies for greater throughput 3. Acquisition of finished or semi finished goods (sub-components)

from suppliers to reduce manufacturing assets

d. Reducing unnecessary intangible assets that are reported on the balance sheet is the most difficult.

1.Sale of assets no longer relevant to company plans 2.License intangibles to other companies

©Cambridge Business Publishers, 2011

Solutions Manual, Chapter 8 8-21

C8-42 (30 minutes)

a. Take-Two (TT) spent $166,020 in 2007 and in 2008 $145,623 on software development. TT’s amortization and write-downs were $106,675 in 2007 and $146,102 in 2008. Using EA’s method, the money spent on additions would be expensed, and the amortization and write-downs would disappear. The result is that if TT’s used EA’s approach, the COGS would increase by $59,345 = $166,020 - $106,675 and net income decrease by $38,574 = $59,345(1-0.35) in 2007. But in 2008, TT’s COGS would decrease by $479 = $146,102 - $145,623 and net income would increase by $311.35 = $479(1-0.35).

b. A variety of answers are possible here. Amortization (including write-

downs) as a percentage of “amortizable cost” (beginning balance plus additions) rose from 0.37% in 2007 to 45% in 2006. The increase indicates a possible increase in the rate of amortization. However, because write- downs are included in the denominator, the increase could be partly due to an increase in write-downs in 2008. Write downs of $27,136 would lead to 0.37 rate for 2008 (about 18.6% of the total charge of $146,102).