Embed Size (px)

Citation preview

CG-Unit 01-Introduction

•What Is Corporate Governance?

•Why Corporate Governance?

•Tools for Corporate Governance

•The Areas Covered

CG-Unit 01-Introduction

WHAT IS CORPORATE GOVERNANCE?

• Corporate governance refers to the structures and processes for the direction and control of companies.

• Corporate governance also is: – a relationship among stakeholders that is used to

determine and control the strategic direction and performance of organizations

– concerned with identifying ways to ensure that strategic decisions are made effectively

– used in corporations to establish order between the firm’s owners and its top-level managers

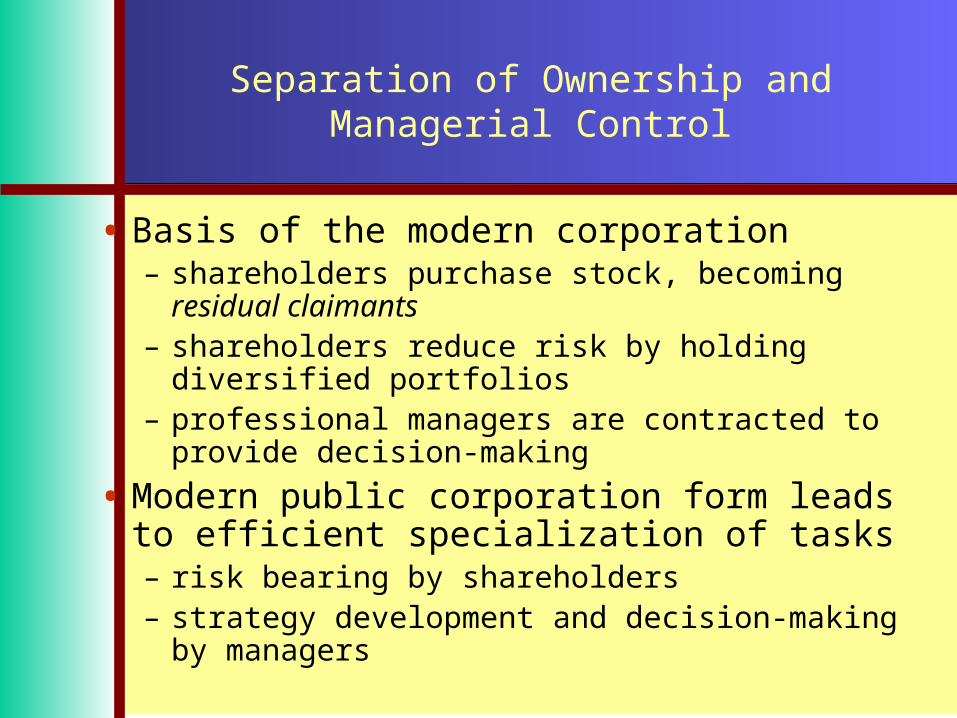

Separation of Ownership and Managerial Control

• Basis of the modern corporation– shareholders purchase stock, becoming residual

claimants– shareholders reduce risk by holding diversified portfolios– professional managers are contracted to provide decision-

making

• Modern public corporation form leads to efficient specialization of tasks– risk bearing by shareholders– strategy development and decision-making by managers

• Risk bearing specialist (principal) Risk bearing specialist (principal) pays compensation to a pays compensation to a managerial decision-making managerial decision-making specialist (agent)specialist (agent)

Agency Relationship: Owners and Managers

An AgencyAn AgencyRelationshipRelationship

ManagersManagers(Agents)(Agents)

ShareholdersShareholders(Principals)(Principals)

• Decision makersDecision makers

• Firm ownersFirm owners

CG-Unit 01-Introduction

• Corporate governance concerns the relationships among:

– The Management

– Board of Directors

– Controlling Shareholders

– Minority Shareholders and

– Other Stakeholders.

CG-Unit 01-Introduction

• Typically salaried professional managers have acquired substantial powers in respect of the affairs of the company they are paid to run on behalf of their shareholders.

CG-Unit 01-Introduction

• However, directors have not always had the best interests of shareholders in mind when performing their managerial functions and this has led to attempts to make directors more accountable for their policies and actions.

CG-Unit 01-Introduction

• The debate over how companies are best governed is at least as old as companies themselves.

• In this connection that a number of reports have been published since 1990s, prompted by the public’s concern at cases of gross mismanagement and “fat cat” pay increases secured by executive directors.

• Fat Cat is an impolite way of referring to someone who is very rich and powerful.

CG-Unit 01-Introduction

• Corporate governance is about the definition of property rights of shareholders and the mechanisms of exercising such rights.

• Equity rights are complex property rights.

• The right to participate in the profits of the company is conditional on the company generating a profit.

• If there is a profit, the next question is how the profit will be distributed.

CG-Unit 01-Introduction

• Corporate governance deals with the ways in which the rights of outside suppliers of equity finance to corporations are protected and receive a fair return if there is any.

• Good practices reduce the risk of expropriation of outsiders by insiders.

• Corporate governance deals with the market for corporate control

CG-Unit 01-Introduction

• Better corporate governance increases the likelihood that the enterprise will satisfy the legitimate claims of all stakeholders and fulfill its responsibilities.

• Accordingly, it contributes the long-term, sustainable growth of companies.

CG-Unit 01-Introduction

• A company that is well-governed is one that is accountable and transparent to:

– Its shareholders and

– Other stakeholders, such as:• Employees• Creditors• Customers and • The wider society.

CG-Unit 01-Introduction

• In consequence a company with good corporate governance is also likely to improve in other aspects of sustainable development such as the environment and social development.

• Corporate governance is not only a method firms use to discipline themselves while remaining profitable.

• It is also one of the principal ways they “make the society” in which they operate and which in turn “makes” them .

• Some relevant and interesting points are:

– Too many cooks will spoil the broth.

– Similarly, too many rules and regulations can stifle the entrepreneurial spirit.

– But too few rules and regulations could leave the investing public unprotected against unscrupulous business practices.

CG-Unit 01-Introduction

Why Corporate Governance?

• Good corporate governance contributes to sustainable economic development by:– Increasing their access to capital and– Enhancing the performance of companies

CG-Unit 01-Introduction

Access to Capital

• Empirical evidence suggests that good corporate governance:– Increases the efficiency of capital allocation within

and across firms– Reduces the cost of capital for issuers– Helps broaden access to capital– Reduces vulnerability to crises– Fosters savings provisions and– Renders corruption more difficult.

CG-Unit 01-Introduction

• Much attention to corporate governance issues, specially in emerging markets, among policymakers and academics has focused on the role governance can play in improving access for emerging market companies to global portfolio equity.

• An increasing volume of empirical evidence indicates that well-governed companies receive higher market valuations.

CG-Unit 01-Introduction

• However, improving corporate governance will also increase all other capital flows to companies in developing countries:

– From domestic and global capital

– Equity and debt and

– From public securities markets and private capital sources.

CG-Unit 01-Introduction

• Improving corporate governance contributes to the development of the public and private capital markets.

• Poor governance undermines the integrity of publicly traded securities and discourages the use of public markets as a means to intermediate savings.

CG-Unit 01-Introduction

• Poor standards of governance, particularly in the area of transparency and disclosure have been a major factor behind instability in the financial markets across the globe.

• This was seen in the case of the East Asian financial crisis of 1997, where so called "crony capitalism" combined with macroeconomic imbalances to interrupt decades of outstanding economic growth.

CG-Unit 01-Introduction

• Most recently, poor corporate governance contributed to the spread of corruption and fraud that led to the dramatic corporate failures in United States and Western Europe.

CG-Unit 01-Introduction

Improving Performance.

• Equally important and, irrespective of the need to access capital, good corporate governance brings better performance for the concerned companies.

CG-Unit 01-Introduction

• Improved governance structures and processes help insure:

– Quality decision making

– Encourage effective succession planning for senior management and

– Enhance the long-term prosperity of companies and its sources of finance.

• Experience has shown that failings in corporate governance practices have caused financial crisis to be blown up at the expense of lenders, investors, and customers.

• Poor corporate governance practices and also lack of transparency have provided an opportunity for companies to rob their financial stakeholders (shareholders and creditors) of their fair share of the company’s earnings and assets.

CG-Unit 01-Introduction

Tools for Corporate Governance

• While conducting any corporate governance review or study or inspection, various tools are used for this purpose.

• Such tools obviously will differ from case to case and situation to situation.

• Even then, certain well accepted tools have been identified.

CG-Unit 01-Introduction

• These are:

– Instruction Sheets

– Progression Matrices

– Information and Document Request List

– Explanatory Note

– Independent Director Definition

– Supervision Checklist

CG-Unit 01-Introduction

• Instruction Sheets – – These describe each of the key corporate

governance tools, how they should be used and who should be interviewed in the course of the corporate governance analysis.

CG-Unit 01-Introduction

• Progression Matrices – These relate the five areas of governance– Commitment to good corporate governance– the Board of Directors – Control Environment and Processes– Transparency and Disclosure, and – Shareholders Rights

to various levels of achievement.

CG-Unit 01-Introduction

• Information and Document Request List – – This list of questions and requests for

documentation forms the basis for the corporate governance analysis of a company. Each analyst will select the tools appropriate for particular project.

CG-Unit 01-Introduction

• Explanatory Note: – Each needs to understand regarding why this

exercise is being undertaken.

CG-Unit 01-Introduction

• Independent Director Definition – – This definition is often used during discussions

with the company to clarify the assessment of the current Board and its future needs.

CG-Unit 01-Introduction

• Supervision Checklist – – This is a list of key issues that should be

considered by supervisors while supervising companies, particularly, companies undertaking CG Improvement Programs.

CG-Unit 01-Introduction

The Areas Covered

• Corporate governance, in its wide connotation, covers a variety of aspects. They can be listed as:

1. Protection of shareholder’s rights

2. Enhancing shareholders’ value

3. Issues related with Board of Directors, including its composition and role

4. Disclosure requirements

5. The integrity of accounting practices

6. The internal control systems

7. The issue of insider trading

• For analytical purpose, these areas generally are grouped into following frameworks :

– Accounting

– Company boards

– Company bosses

– The rewards

CG-Unit 01-Introduction

• Accounting– To enable investors to find out what manager’s are doing with their

money

• Company boards– To understand its composition and its powers

• Company bosses– To know whether they are given a free rein to run things much as

they like or not

• The rewards– To understand whether senior managers are paid salary and bonus

only or share options also.