Embed Size (px)

Citation preview

Deutsche Bank Markets Research

Global

Commodities

Date 13 October 2014

CFTC Commitment of Traders

Report for w/e 7 October 2014

________________________________________________________________________________________________________________

Deutsche Bank AG/London

DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 148/04/2014.

Michael Lewis

Strategist

(+44) 20 754-52166

Jayati Mukherjee

Strategist

(+91) 22 6181-2036

WTI: Net length lowest since June 2013

US NatGas : Net short highest since March 2011

Gold : Net length lowest since January 2014

Energy

With the exception of RBOB gasoline, the speculative community exhibited a bearish stance towards the energy complex during the latest reporting week. Net length in WTI decreased to the lowest level since June 2013 as prices moved lower. We believe that the weak economic data and ample supplies continue to pressure oil prices. We believe this bearishness to continue as we see no signs of possible cut back on supply from OPEC. A cut back in its official selling price from Saudi Arabia is a clear indication that they are focused on competing for market share. Hence in the short term we expect the speculator to cut back more on their net long positions.

Net shorts in heating oil continue to increase as prices fell during the latest reporting week. A drop in US distillate demand might be a possible factor for the decline in the prices. However, we expect this to change as we head into high demand winter season which will be supported further by low level of US inventories.

Meanwhile, net length in RBOB gasoline increased even as prices fell. Gasoline inventories in US continue to build despite lower imports and reduced crude runs. We expect this bearishness to continue in the short term as refineries in North America come out of maintenance.

Meanwhile net shorts in US natural gas increased to the highest level since March 2011 as prices advanced during the reporting week.

Metals

The speculative community exhibited a neutral to bullish stance towards the metals complex over the latest reporting week. Net length in gold decreased to its lowest level since January even though prices appreciated. In a scenario where the global economic growth remains passive the urge to hold length position in gold becomes attractive while benefitting the short term prices for gold. Once the adjustment in US rates, equities and the US dollar to the prospect of Fed tightening has occurred, we expect a more supportive flow story for gold may eventually emerge.

Net length in silver and palladium increased as prices advanced, while net length in platinum increased even as prices weakened over the reporting period.

The speculative community has increased its net shorts in copper even as prices strengthened during the latest reporting week. However, we expect China’s positive macro data to provide support to copper prices in the near term.

Agriculture With the exception of corn, the speculative community exhibited a bullish

stance towards the agricultural complex. Net shorts in soybeans decreased as prices gained during the reporting week. Meanwhile, net length in corn decreased even as prices strengthened.

Net shorts in sugar reversed to net length position as prices advanced during the latest reporting week. At the same time net shorts in wheat decreased as prices moved higher.

Comex Copper Open Interest vs Price

50

100

150

200

250

300

350

400

450

500

55

70

85

100

115

130

145

160

175

190

205

2007 2008 2009 2010 2011 2012 2013 2014

Open Interest (lhs)

Copper price (rhs)

K USc/lbK Open Interest

Source: CFTC, Deutsche Bank

Comex Gold Open Interest vs Price

250

450

650

850

1050

1250

1450

1650

1850

50

250

450

650

850

1050

1250

2007 2008 2009 2010 2011 2012 2013 2014

USD/oz

Open Interest (lhs)

Gold price (rhs)

KK Open Interest

Source: CFTC, Deutsche Bank

Nymex WTI Oil Open Interest vs Price

15

35

55

75

95

115

135

155

1000

1500

2000

2500

3000

3500

2007 2008 2009 2010 2011 2012 2013 2014

USD/bbl

Open Interest (lhs)

Crude Oil price (rhs)

K Open InterestK Open Interest

Source: Deutsche Bank

Net Non-Commercial Positions, 2 week summary

07-Oct-14 30-Sep-14 12M avg

Crude o il 299,755 303,079 383,675

Natural gas -193,119 -177,631 -112,474

RBOB Gasoline 42,709 34,183 54,478

Heating o il -14,172 -10,284 -9,378

Gold 66,968 67,083 107,977

Silver 2,987 2,836 18,270

Platinum 24,655 23,878 37,935

Palladium 22,944 21,443 23,108

Copper -25,201 -23,689 -9,509

Corn 140,687 157,258 116,492

Wheat -60,571 -61,431 -24,345

Soybean -24,227 -30,345 108,730

Sugar 13,166 -2,007 98,926 Source: Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Page 2 Deutsche Bank AG/London

Disaggregated COT report

In the past, COT reports have divided reportable traders into two broad categories: “commercial” and “non-commercial”. However, in 2009 significant improvements were made to the original CFTC report. These new reporting categories were an attempt to identify the significant increase in financial flows into commodities not just in ETFs but also OTC activities, particularly swaps as well as the increasing participation of pension and endowment funds into the commodities complex. With the publication of the new disaggregated COT report, the CFTC classifies traders into specific categories such as Producer/Merchant/Processor/User, Swap Dealers, Money Managers and Other Reportables. The characteristics of these various players are outlined below: Producer/Merchant/Processor/User represents commercial hedgers and predominantly engages in production and processing of a physical commodity and uses the futures markets to hedge risks. Swap Dealer deals primarily in swaps for a commodity and uses the futures markets to manage or hedge risks. The swap dealer’s counterparties may be speculative traders or commercial clients. Money Manager represents the large speculators and engages in managing futures trading on behalf of clients. They are typically registered commodity trading advisor (CTA), registered commodity pool operator (CPO) or hedge funds. Other Reportables are other non commercial traders.

Key Findings w/e October 7, 2014 WTI: Money Managers cut back on net long positions RBOB: Money Manager add long positions despite low prices Gold: Money Managers net long position lowest since Jan’14

As prices fell for WTI, large speculators or money managers were seen cutting back on their net long positions during the latest reporting week. We believe the recent US crude inventory buildup coupled with new infrastructure coming online (Pony Express pipeline) to deliver crude into Cushing will increasingly drive bearish sentiment among the speculators. We expect this bearish sentiment to continue in the short term as OPEC fails to cut back on supply. Additionally the crude arbitrage for West African crude and EU crudes to the USGC looks marginally open and we can expect to see US bound cargoes in the short term which will add to bearishness for US crude. Hence we expect this bias among money managers will be to continue to cut back on their net long positions. Commercial hedgers reinforced this bearishness as they increased their net short positions.

Despite a drop in prices for RBOB gasoline, money managers have become more bullish by increasing their net long positions. We believe this is due to ongoing refinery maintenance in North America. However, in our opinion this is likely to change as US inventories build in spite of lower imports and lower crude runs, indicating poor demand. We believe that the speculative community will cut back on their net long positions as refineries come out of maintenance in North America.

Meanwhile as prices continued to decline for heating oil we saw money managers increasing their net short positions for the seventh consecutive week. We expect this to reverse in the coming months as the US heads into what is likely to be a colder than normal winter and upcoming refinery maintenance. Commercial hedgers were also seen decreasing their net short position in heating oil.

As prices weakened for US natural gas we have seen money managers cut back on their bullish bets by reducing aggressively their net long positions, whereas commercial hedgers were seen adding contracts to their net long positions.

Money managers continue to cut their bullish bets on gold by decreasing their net long positions for the eighth consecutive week, even though prices have been relatively flat during. In silver even though prices appreciated we have seen money managers continue to increase their net short positions.

In copper, as prices appreciated during this reporting week, we have seen money managers cutting back on their net short positions indicating a bullish view on the industrial metal.

Net Money Managers Positions, 2 week summary

07-Oct-14 30-Sep-14 12M avg

Copper -21,249 -21,438 6,385

Gold 37,275 37,743 80,618

Silver -7,071 -6,073 10,477

Platinum 16,844 13,265 28,622

Palladium 19,091 18,318 20,463

Crude o il 192,208 201,863 272,730

Natural gas 6,288 26,166 69,012

RBOB Gasoline 20,363 10,321 43,679

Heating o il -30,604 -29,867 12,242

Corn 73,093 85,086 59,756

Wheat -67,970 -71,301 -27,929

Soybean -24,457 -15,214 154,351

Sugar -36,604 -51,789 57,273 Source: Deutsche Bank

Nymex crude oil net position vs Price

(Money Managers & PMPU)

20

40

60

80

100

120

140

160

-600

-400

-200

0

200

400

Jun-10 Feb-11 Oct-11 Jun-12 Feb-13 Oct-13 Jun-14

K Contracts

Producers / Merchants Money Managers WTI price

USD/bbl

Source: CFTC, Deutsche Bank

Comex gold net position vs Price

(Money Managers & PMPU)

500

1000

1500

2000

-300

-200

-100

0

100

200

300

Jun-10 Feb-11 Oct-11 Jun-12 Feb-13 Oct-13 Jun-14

K Contracts

Producers / Merchants Money Managers Gold price

USD/oz

Source: CFTC, Deutsche Bank

Comex copper net position vs Price (Money Managers & PMPU)

0

50

100

150

200

250

300

350

400

450

500

-80

-60

-40

-20

0

20

40

60

Jun-10 Feb-11 Oct-11 Jun-12 Feb-13 Oct-13 Jun-14

K Contracts

Producers / Merchants Money Managers Copper price

USc/lbK Contracts

Source: Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Deutsche Bank AG/London Page 3

Figure 1: Commitments of non-commercial traders energy data summary

Contracts NYMEX Crude oil ICE WTI Natural gas RBOB Heating oil

Long 427,007 82,332 255,510 91,207 56,417

Change 2,621 -5,750 -14,539 4,207 -2,433

Short 127,252 33,754 448,629 48,498 70,589

Change 5,945 2,174 949 -4,319 1,455

Net 299,755 48,578 -193,119 42,709 -14,172

Change contracts -3,324 -7,924 -15,488 8,526 -3,888

Price USD 88.85 88.85 3.96 2.37 2.61

Change -2.5% -2.5% -4.0% -2.8% -1.6%

Open Interest 2,146,776 646,132 955,101 299,805 418,748

Change 3.7% 5.89% -1.3% 2.5% 3.8%

Source: Deutsche Bank

Figure 2: Nymex Crude Oil (contract 1,000bbl) Figure 3: Natural Gas (contract 10,000mmBTU)

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

Figure 4: Nymex RBOB Gasoline* (contract 1,000bbl) Figure 5: Nymex Heating Oil (contract 1,000bbl)

Source: CFTC, Bloomberg Finance LP, Deutsche Bank *Historical data up to 12 December 2006 relates to the Nymex unleaded gasoline contract

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Page 4 Deutsche Bank AG/London

Figure 6: Commitments of non-commercial traders: metals data summary

Contracts Copper Gold Silver Platinum Palladium

Long 54,273 172,662 51,878 40,757 26,850

Change 2,513 456 -2,302 -524 782

Short 79,474 105,694 48,891 16,102 3,906

Change 4,025 571 -2,453 -1,301 -719

Net -25,201 66,968 2,987 24,655 22,944

Change contracts -1,512 -115 151 777 1,501

Price US$ 3.04 1,212.40 17.24 1,261.90 787.00

Change 1.0% 0.1% 1.1% -3.0% 1.5%

Open Interest 168,359 619,593 234,169 61,597 37,248

Change 4.5% 1.6% 0.0% 1.4% -1.1%

Source: Deutsche Bank

Figure 7: Comex Copper (contract 25,000lbs) Figure 8: Comex Gold (contract 100oz)

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

Figure 9: Comex Silver (contract 5,000oz) Figure 10: Nymex Platinum (contract 50oz)

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Deutsche Bank AG/London Page 5

Figure 11: Commitments of non-commercial traders: agricultural commodities data summary

Corn Wheat Soybean Sugar

Long 458,371 119,855 174,508 236,706

Change -6,544 -3,173 -5,519 -8,238

Short 317,684 180,426 198,735 223,540

Change 10,027 -4,033 -11,637 -23,411

Net 140,687 -60,571 -24,227 13,166

Change contracts -16,571 860 6,118 15,173

Price US$ 340.50 506.25 940.75 17.03

Change 6.2% 6.0% 3.0% 10.0%

Open Interest 1,893,351 548,921 1,232,537 919,609

Change -2.0% -0.4% -0.6% -2.2%

Source: Deutsche Bank

Figure 12: CBOT corn (contract 5,000 bushels) Figure 13: CBOT wheat (contract 5,000 bushels)

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

Figure 14: CBOT soybean (contract 5,000 bushels) Figure 15: COMEX sugar (contract 112,000 lbs)

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

Source: CFTC, Bloomberg Finance LP, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Page 6 Deutsche Bank AG/London

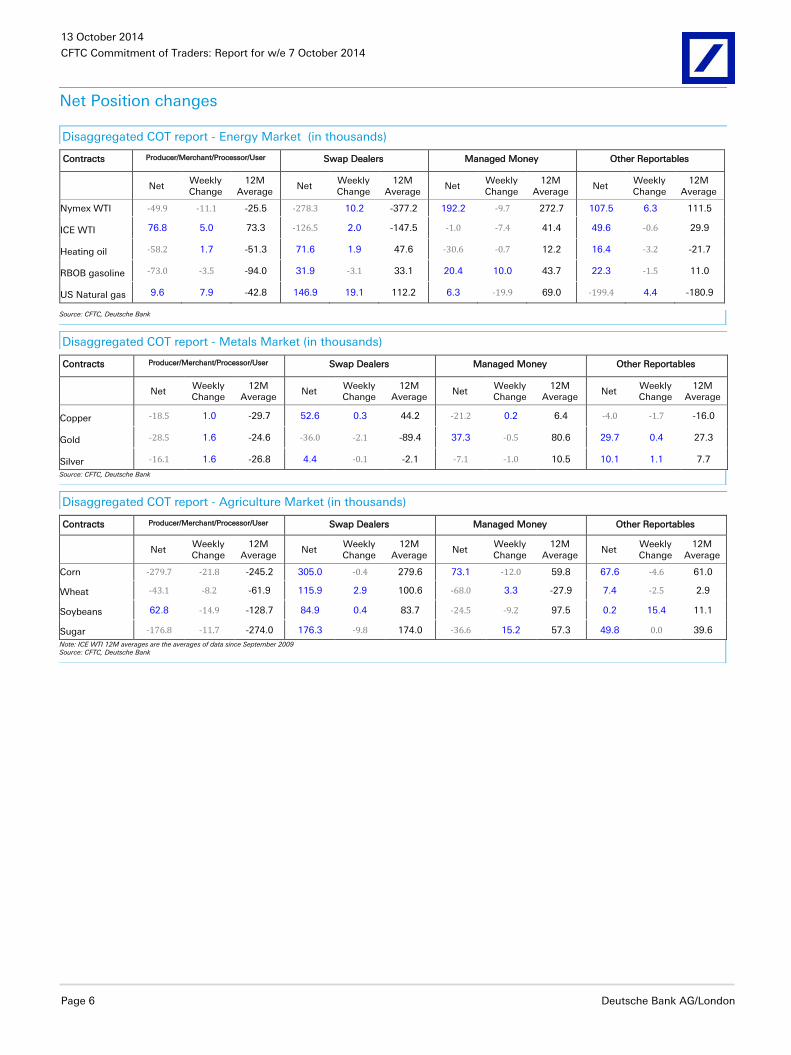

Net Position changes

Disaggregated COT report - Energy Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Net

Weekly Change

12M Average

Net Weekly Change

12M Average

Net Weekly Change

12M Average

Net Weekly Change

12M Average

Nymex WTI -49.9 -11.1 -25.5 -278.3 10.2 -377.2 192.2 -9.7 272.7 107.5 6.3 111.5

ICE WTI 76.8 5.0 73.3 -126.5 2.0 -147.5 -1.0 -7.4 41.4 49.6 -0.6 29.9

Heating oil -58.2 1.7 -51.3 71.6 1.9 47.6 -30.6 -0.7 12.2 16.4 -3.2 -21.7

RBOB gasoline -73.0 -3.5 -94.0 31.9 -3.1 33.1 20.4 10.0 43.7 22.3 -1.5 11.0

US Natural gas 9.6 7.9 -42.8 146.9 19.1 112.2 6.3 -19.9 69.0 -199.4 4.4 -180.9

Source: CFTC, Deutsche Bank

Disaggregated COT report - Metals Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Net

Weekly Change

12M Average

Net Weekly Change

12M Average

Net Weekly Change

12M Average

Net Weekly Change

12M Average

Copper -18.5 1.0 -29.7 52.6 0.3 44.2 -21.2 0.2 6.4 -4.0 -1.7 -16.0

Gold -28.5 1.6 -24.6 -36.0 -2.1 -89.4 37.3 -0.5 80.6 29.7 0.4 27.3

Silver -16.1 1.6 -26.8 4.4 -0.1 -2.1 -7.1 -1.0 10.5 10.1 1.1 7.7

Source: CFTC, Deutsche Bank

Disaggregated COT report - Agriculture Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Net

Weekly Change

12M Average

Net Weekly Change

12M Average

Net Weekly Change

12M Average

Net Weekly Change

12M Average

Corn -279.7 -21.8 -245.2 305.0 -0.4 279.6 73.1 -12.0 59.8 67.6 -4.6 61.0

Wheat -43.1 -8.2 -61.9 115.9 2.9 100.6 -68.0 3.3 -27.9 7.4 -2.5 2.9

Soybeans 62.8 -14.9 -128.7 84.9 0.4 83.7 -24.5 -9.2 97.5 0.2 15.4 11.1

Sugar -176.8 -11.7 -274.0 176.3 -9.8 174.0 -36.6 15.2 57.3 49.8 0.0 39.6

Note: ICE WTI 12M averages are the averages of data since September 2009 Source: CFTC, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Deutsche Bank AG/London Page 7

Chartbook of CFTC disaggregated COT report – Net position

Figure 16: Nymex crude oil position by trading category Figure 17: Nymex natural gas position by trading

category

20

40

60

80

100

120

140

160

-600

-400

-200

0

200

400

Jun-06 May-07 Apr-08 Mar-09 Feb-10 Jan-11 Dec-11 Nov-12 Oct-13 Sep-14

K Contracts

Producers / Merchants Swap Dealers

Money Managers Other Reportable

WTI price

USD/bbl

0

2

4

6

8

10

12

14

16

-340

-240

-140

-40

60

160

260

Jun-06 May-07 Apr-08 Mar-09 Feb-10 Jan-11 Dec-11 Nov-12 Oct-13 Sep-14

K Contracts

Producers / Merchants Swap Dealers Money Managers

Other Reportable US Natural gas Price

USD/mmBTU

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

Figure 18: Comex gold position by trading category Figure 19: Comex copper position by trading category

500

1000

1500

2000

-300

-200

-100

0

100

200

300

Jun-06 May-07 Apr-08 Mar-09 Feb-10 Jan-11 Dec-11 Nov-12 Oct-13 Sep-14

K Contracts

Producers / Merchants Swap Dealers

Money Managers Other Reportable

Gold price

USD/oz

0

50

100

150

200

250

300

350

400

450

500

-80

-60

-40

-20

0

20

40

60

Jun-06 May-07 Apr-08 Mar-09 Feb-10 Jan-11 Dec-11 Nov-12 Oct-13 Sep-14

K Contracts

Producers / Merchants Swap Dealers

Money Managers Other Reportable

Copper price

USc/lb

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

Figure 20: CBOT corn position by trading category Figure 21: CBOT soybean position by trading category

100

300

500

700

900

-900

-700

-500

-300

-100

100

300

500

Jun-06 May-07 Apr-08 Mar-09 Feb-10 Jan-11 Dec-11 Nov-12 Oct-13 Sep-14

K Contracts

Producers / Merchants Swap DealersMoney Managers Other ReportableCorn price

USc/bu

500

700

900

1100

1300

1500

1700

1900

-400

-300

-200

-100

0

100

200

300

Jun-06 May-07 Apr-08 Mar-09 Feb-10 Jan-11 Dec-11 Nov-12 Oct-13 Sep-14

K Contracts

Producers / Merchants Swap Dealers

Money Managers Other Reportable

Soybean price

USc/bu

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Page 8 Deutsche Bank AG/London

Long Position changes

Disaggregated COT report - Energy Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Long

Weekly Change

12M Average

Long Weekly Change

12M Average

Long Weekly Change

12M Average

Long Weekly Change

12M Average

Nymex WTI 254.8 19.1 312.7 122.7 2.5 128.6 266.2 -4.2 311.7 160.8 6.8 164.9

ICE WTI 202.2 14.7 230.3 10.2 2.0 12.1 26.8 -5.3 55.3 55.6 -0.4 37.5

Heating oil 115.1 3.7 95.2 72.0 1.3 53.4 24.4 -0.2 37.1 32.0 -2.2 17.0

RBOB gasoline 86.9 4.1 81.6 37.6 -0.6 36.9 56.9 4.6 64.1 34.3 -0.3 31.4

US Natural gas 127.7 4.8 139.8 163.8 13.8 144.5 233.6 -15.8 274.1 21.9 1.2 30.2

Source: CFTC, Deutsche Bank

Disaggregated COT report - Metals Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Long

Weekly Change

12M Average

Long Weekly Change

12M Average

Long Weekly Change

12M Average

Long Weekly Change

12M Average

Copper 29.0 3.4 19.0 57.2 -0.2 51.4 33.5 1.3 37.7 20.8 1.2 11.5

Gold 63.2 5.0 84.5 50.7 -7.4 40.2 118.3 -0.7 126.8 54.3 1.1 49.8

Silver 27.2 -0.5 21.0 41.9 0.5 35.4 36.6 -2.2 34.7 15.2 -0.1 11.9

Source: CFTC, Deutsche Bank

Disaggregated COT report - Agriculture Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Long

Weekly Change

12M Average

Long Weekly Change

12M Average

Long Weekly Change

12M Average

Long Weekly Change

12M Average

Corn 321.5 -1.0 382.5 308.6 -2.5 283.8 332.2 0.2 270.9 126.1 -6.8 120.7

Wheat 71.7 -4.5 73.3 118.1 2.0 109.1 80.7 -0.4 86.3 39.2 -2.8 29.5

Soybeans 358.9 -5.2 208.3 93.3 0.7 93.3 98.3 -5.7 159.5 76.2 0.2 57.6

Sugar 209.4 -14.5 224.1 210.0 -4.2 210.8 173.6 -3.9 185.5 63.1 -4.3 58.4

Note: ICE WTI 12M averages are the averages of data since September 2009 Source: CFTC, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Deutsche Bank AG/London Page 9

Chartbook of CFTC disaggregated COT report – Long Position

Figure 22: Nymex crude oil position by trading category Figure 23: Nymex natural gas position by trading

category

85

90

95

100

105

110

-80

-60

-40

-20

0

20

40

60

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables WTI price

K contracts

WTI

USD/bbl

3

4

5

6

-60

-40

-20

0

20

40

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables US natural gas price

K contracts

US natural gas

USD/mmBTU

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

Figure 24: Comex gold position by trading category Figure 25: Comex copper position by trading category

1100

1200

1300

1400

1500

-40

-20

0

20

40

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables Gold price

K contracts

Gold

USD/oz

250

300

350

400

-20

-15

-10

-5

0

5

10

15

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables Copper price

K contracts

Copper

USc/lb

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

Figure 26: CBOT corn position by trading category Figure 27: CBOT soybean position by trading category

300

400

500

600

700

-100

-80

-60

-40

-20

0

20

40

60

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables Corn price

K contracts

Corn

USc/bu

900

1000

1100

1200

1300

1400

1500

1600

-50

-30

-10

10

30

50

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables Soybean price

K contracts

Soybean

USc/bu

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Page 10 Deutsche Bank AG/London

Short Position changes

Disaggregated COT report - Energy Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Short

Weekly Change

12M Average

Short Weekly Change

12M Average

Short Weekly Change

12M Average

Short Weekly Change

12M Average

Nymex WTI 304.7 30.2 338.3 401.0 -7.7 505.8 74.0 5.5 39.0 53.2 0.5 53.4

ICE WTI 125.5 9.7 157.0 136.7 0.0 159.6 27.8 2.0 13.9 6.0 0.1 7.6

Heating oil 173.3 2.0 146.5 0.4 -0.6 5.8 55.0 0.5 24.8 15.6 1.0 38.7

RBOB gasoline 159.9 7.6 175.7 5.7 2.5 3.8 36.5 -5.5 20.4 12.0 1.2 20.4

US Natural gas 118.1 -3.1 182.6 16.9 -5.3 32.3 227.3 4.1 205.1 221.3 -3.1 211.1

Source: CFTC, Deutsche Bank

Disaggregated COT report - Metals Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Short

Weekly Change

12M Average

Short Weekly Change

12M Average

Short Weekly Change

12M Average

Short Weekly Change

12M Average

Copper 47.5 2.4 48.7 4.5 -0.5 7.2 54.7 1.1 31.4 24.8 2.9 27.5

Gold 91.7 3.5 109.0 86.7 -5.2 129.5 81.1 -0.2 46.1 24.6 0.8 22.5

Silver 43.3 -2.1 47.7 37.5 0.6 37.5 43.7 -1.2 24.2 5.2 -1.3 4.2

Source: CFTC, Deutsche Bank

Disaggregated COT report - Agriculture Market (in thousands)

Contracts Producer/Merchant/Processor/User Swap Dealers Managed Money Other Reportables

Short

Weekly Change

12M Average

Short Weekly Change

12M Average

Short Weekly Change

12M Average

Short Weekly Change

12M Average

Corn 601.1 20.8 627.7 3.6 -2.1 4.2 259.2 12.2 211.2 58.5 -2.2 59.7

Wheat 114.9 3.7 135.1 2.2 -0.9 8.5 148.6 -3.7 114.3 31.8 -0.3 26.6

Soybeans 296.1 9.8 337.0 8.3 0.3 9.6 122.8 3.6 62.0 75.9 -15.2 46.4

Sugar 386.2 -2.9 498.1 33.7 5.6 36.8 210.2 -19.1 128.3 13.4 -4.3 18.7

Note: ICE WTI 12M averages are the averages of data since September 2009 Source: CFTC, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Deutsche Bank AG/London Page 11

Chartbook of CFTC disaggregated COT report – Short Position

Figure 28: Nymex crude oil position by trading category Figure 29: Nymex natural gas position by trading

category

85

90

95

100

105

110

-70

-50

-30

-10

10

30

50

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables WTI price

K contracts

WTI

USD/bbl

3.0

3.5

4.0

4.5

5.0

5.5

6.0

-60

-40

-20

0

20

40

60

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables US natural gas price

K contracts

US natural gas

USD/mmBTU

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

Figure 30: Comex gold position by trading category Figure 31: Comex copper position by trading category

1100

1200

1300

1400

1500

-50

-25

0

25

50

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables Gold price

K contracts

Gold

USD/oz

250

300

350

400

-20

-15

-10

-5

0

5

10

15

20

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables Copper price

K contracts

Copper

USc/lb

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

Figure 32: CBOT corn position by trading category Figure 33: CBOT soybean position by trading category

300

400

500

600

700

-100

-80

-60

-40

-20

0

20

40

60

80

100

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables Corn price

K contracts

Corn

USc/bu

900

1000

1100

1200

1300

1400

1500

1600

-60

-40

-20

0

20

40

60

80

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Producer/Merchants Swap Dealers Money Managers

Other Reportables Soybean price

K contracts

Soybean

USc/bu

Source: CFTC, Deutsche Bank

Source: CFTC, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Page 12 Deutsche Bank AG/London

DB Commodity Positioning Index

The DB Commodity Positioning universe covers non-commercial future positions held on 13 different commodities across energy, precious metals, industrial metals and agriculture sectors as reported by the Commodities Futures Trading Commission (CFTC) every Friday. The index measures the magnitude of the current net speculative position relative to its long-term average on a scale of -10 to +10. A positive value indicates a net long position, while a negative value indicates a net short and the index level corresponds to its percentile rank.

For example, an index level of +8.7 indicates that the current net long position lies at the 87th percentile relative to the net long positions held historically (since January 03, 2006). Similarly, an index level of -4.3 suggests that the current net short position lies at the 43rd percentile of the net shorts distribution.

The DB Sector Positioning Index tracks the degree of speculative positioning in energy, metals and agriculture sectors. To avoid any offsetting effect, only absolute values of net positions are taken into account in calculating the index level. Thus, the DB Sector Positioning Index can only take positive values between 0 and 10. In essence, the DB Sector Positioning Index gives a sense of the scale of speculative positioning or liquidation risk in a particular sector.

Figure 37 shows the ratio between net positions (difference between total open long and open short) and open speculative interest (total number of open long and short contracts held by speculators). The standardized net speculative position reflects the speculative community’s directional view towards the underlying commodity.

DB Commodity Positioning Index

Net shorts in wheat and net length in palladium remain at aggressive levels.

Figure 34: DB Commodity Positioning Index (DB CPI)

0.09-0.11 -0.33

-1.40

0.63

0.04 -0.02

-0.644.38

0.22

1.20

-0.04

0.31

-10

-6

-2

2

6

10

Wheat Copper NatGas Heating oil

Soybean Silver Gold Sugar Corn RBOB Platinum WTI Palladium

Source: CFTC, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Deutsche Bank AG/London Page 13

Figure 35: DB Commodity Positioning Index

7-Oct-14 3mma Change (WoW)

WTI 8.01 8.45 -0.04

RBOB 3.39 3.60 1.20

Heating oil -6.88 -3.27 -1.40

NatGas -9.30 -8.62 -0.33

Copper -9.34 -2.72 -0.11

Gold 0.70 3.13 -0.02

Silver 0.11 3.82 0.04

Palladium 8.82 9.22 0.31

Platinum 7.17 8.80 0.22

Sugar 2.24 1.43 4.38

Soybean -5.21 -4.04 0.63

Corn 3.04 2.94 -0.64

Wheat -9.57 -8.61 0.09

Net long bigger Net short smaller

Net short bigger Net long smaller Source: CFTC, Deutsche Bank

Figure 36: DB Sector Positioning Index

0

2

4

6

Energy Metals Agriculture

Current week

Previous week

Source: Deutsche Bank

Figure 37: Net position as a percentage of open speculative interest

7-Oct-14 3mma 30-Sep-14 Change

WTI 54.1% 59.9% 55.5% -1.5%

RBOB 30.6% 32.2% 24.4% 6.1%

Heating oil -11.2% -5.3% -8.0% -3.1%

NatGas -27.4% -24.2% -24.7% -2.7%

Copper -18.8% -6.0% -18.6% -0.2%

Gold 24.1% 45.4% 24.2% -0.1%

Silver 3.0% 28.1% 2.7% 0.3%

Palladium 74.6% 71.6% 69.9% 4.7%

Platinum 43.4% 66.2% 40.7% 2.7%

Sugar 2.9% 4.1% -0.4% 3.3%

Soybean -6.5% -4.7% -7.8% 1.3%

Corn 18.1% 18.2% 20.4% -2.2%

Wheat -20.2% -18.7% -20.0% -0.2% Source: CFTC, Deutsche Bank

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Page 14 Deutsche Bank AG/London

Appendix 1

Important Disclosures

Additional information available upon request

For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr

Analyst Certification

The views expressed in this report accurately reflect the personal views of the undersigned lead analyst(s). In addition, the undersigned lead analyst(s) has not and will not receive any compensation for providing a specific recommendation or view in this report. Michael Lewis/Jayati Mukherjee

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Deutsche Bank AG/London Page 15

(a) Regulatory Disclosures

(b) 1. Country-Specific Disclosures

Australia and New Zealand: This research, and any access to it, is intended only for "wholesale clients" within the

meaning of the Australian Corporations Act and New Zealand Financial Advisors Act respectively.

Brazil: The views expressed above accurately reflect personal views of the authors about the subject company(ies) and

its(their) securities, including in relation to Deutsche Bank. The compensation of the equity research analyst(s) is

indirectly affected by revenues deriving from the business and financial transactions of Deutsche Bank. In cases where

at least one Brazil based analyst (identified by a phone number starting with +55 country code) has taken part in the

preparation of this research report, the Brazil based analyst whose name appears first assumes primary responsibility for

its content from a Brazilian regulatory perspective and for its compliance with CVM Instruction # 483.

EU countries: Disclosures relating to our obligations under MiFiD can be found at

http://www.globalmarkets.db.com/riskdisclosures.

Japan: Disclosures under the Financial Instruments and Exchange Law: Company name - Deutsche Securities Inc.

Registration number - Registered as a financial instruments dealer by the Head of the Kanto Local Finance Bureau

(Kinsho) No. 117. Member of associations: JSDA, Type II Financial Instruments Firms Association, The Financial Futures

Association of Japan, Japan Investment Advisers Association. This report is not meant to solicit the purchase of specific

financial instruments or related services. We may charge commissions and fees for certain categories of investment

advice, products and services. Recommended investment strategies, products and services carry the risk of losses to

principal and other losses as a result of changes in market and/or economic trends, and/or fluctuations in market value.

Before deciding on the purchase of financial products and/or services, customers should carefully read the relevant

disclosures, prospectuses and other documentation. "Moody's", "Standard & Poor's", and "Fitch" mentioned in this

report are not registered credit rating agencies in Japan unless "Japan" or "Nippon" is specifically designated in the

name of the entity.

Malaysia: Deutsche Bank AG and/or its affiliate(s) may maintain positions in the securities referred to herein and may

from time to time offer those securities for purchase or may have an interest to purchase such securities. Deutsche Bank

may engage in transactions in a manner inconsistent with the views discussed herein.

Qatar: Deutsche Bank AG in the Qatar Financial Centre (registered no. 00032) is regulated by the Qatar Financial Centre

Regulatory Authority. Deutsche Bank AG - QFC Branch may only undertake the financial services activities that fall

within the scope of its existing QFCRA license. Principal place of business in the QFC: Qatar Financial Centre, Tower,

West Bay, Level 5, PO Box 14928, Doha, Qatar. This information has been distributed by Deutsche Bank AG. Related

financial products or services are only available to Business Customers, as defined by the Qatar Financial Centre

Regulatory Authority.

Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute,

any appraisal or evaluation activity requiring a license in the Russian Federation.

Kingdom of Saudi Arabia: Deutsche Securities Saudi Arabia LLC Company, (registered no. 07073-37) is regulated by the

Capital Market Authority. Deutsche Securities Saudi Arabia may only undertake the financial services activities that fall

within the scope of its existing CMA license. Principal place of business in Saudi Arabia: King Fahad Road, Al Olaya

District, P.O. Box 301809, Faisaliah Tower - 17th Floor, 11372 Riyadh, Saudi Arabia.

United Arab Emirates: Deutsche Bank AG in the Dubai International Financial Centre (registered no. 00045) is regulated

by the Dubai Financial Services Authority. Deutsche Bank AG - DIFC Branch may only undertake the financial services

activities that fall within the scope of its existing DFSA license. Principal place of business in the DIFC: Dubai

International Financial Centre, The Gate Village, Building 5, PO Box 504902, Dubai, U.A.E. This information has been

distributed by Deutsche Bank AG. Related financial products or services are only available to Professional Clients, as

defined by the Dubai Financial Services Authority.

(c) Risks to Fixed Income Positions

Macroeconomic fluctuations often account for most of the risks associated with exposures to instruments that promise

to pay fixed or variable interest rates. For an investor that is long fixed rate instruments (thus receiving these cash

flows), increases in interest rates naturally lift the discount factors applied to the expected cash flows and thus cause a

loss. The longer the maturity of a certain cash flow and the higher the move in the discount factor, the higher will be the

loss. Upside surprises in inflation, fiscal funding needs, and FX depreciation rates are among the most common adverse

macroeconomic shocks to receivers. But counterparty exposure, issuer creditworthiness, client segmentation, regulation

(including changes in assets holding limits for different types of investors), changes in tax policies, currency

13 October 2014

CFTC Commitment of Traders: Report for w/e 7 October 2014

Page 16 Deutsche Bank AG/London

convertibility (which may constrain currency conversion, repatriation of profits and/or the liquidation of positions), and

settlement issues related to local clearing houses are also important risk factors to be considered. The sensitivity of fixed

income instruments to macroeconomic shocks may be mitigated by indexing the contracted cash flows to inflation, to

FX depreciation, or to specified interest rates - these are common in emerging markets. It is important to note that the

index fixings may -- by construction -- lag or mis-measure the actual move in the underlying variables they are intended

to track. The choice of the proper fixing (or metric) is particularly important in swaps markets, where floating coupon

rates (i.e., coupons indexed to a typically short-dated interest rate reference index) are exchanged for fixed coupons. It is

also important to acknowledge that funding in a currency that differs from the currency in which the coupons to be

received are denominated carries FX risk. Naturally, options on swaps (swaptions) also bear the risks typical to options

in addition to the risks related to rates movements.

David Folkerts-Landau Group Chief Economist

Member of the Group Executive Committee

Guy Ashton Global Chief Operating Officer

Research

Marcel Cassard Global Head

FICC Research & Global Macro Economics

Richard Smith and Steve Pollard Co-Global Heads Equity Research

Michael Spencer Regional Head

Asia Pacific Research

Ralf Hoffmann Regional Head

Deutsche Bank Research, Germany

Andreas Neubauer Regional Head

Equity Research, Germany

Steve Pollard Regional Head

Americas Research

International Locations

Deutsche Bank AG

Deutsche Bank Place

Level 16

Corner of Hunter & Phillip Streets

Sydney, NSW 2000

Australia

Tel: (61) 2 8258 1234

Deutsche Bank AG

Große Gallusstraße 10-14

60272 Frankfurt am Main

Germany

Tel: (49) 69 910 00

Deutsche Bank AG

Filiale Hongkong

International Commerce Centre,

1 Austin Road West,Kowloon,

Hong Kong

Tel: (852) 2203 8888

Deutsche Securities Inc.

2-11-1 Nagatacho

Sanno Park Tower

Chiyoda-ku, Tokyo 100-6171

Japan

Tel: (81) 3 5156 6770

Deutsche Bank AG London

1 Great Winchester Street

London EC2N 2EQ

United Kingdom

Tel: (44) 20 7545 8000

Deutsche Bank Securities Inc.

60 Wall Street

New York, NY 10005

United States of America

Tel: (1) 212 250 2500

Global Disclaimer

Investing in and/or trading commodities involves significant risk and may not be suitable for everyone. Participants in commodities transactions may incur risks from several factors, including changes in supply and demand of the commodity that can lead to large fluctuations in price. The use of leverage magnifies this risk. Readers must make their own investing and trading decisions using their own independent advisors as they believe necessary and based upon their specific objectives and financial situation. Past performance is not necessarily indicative of future results. Deutsche Bank may with respect to securities covered by this report, sell to or buy from customers on a principal basis, and consider this report in deciding to trade on a proprietary basis. Deutsche Bank makes no representation as to the accuracy or completeness of the information in this report. Target prices are inherently imprecise and a product of the analyst judgement. Deutsche Bank may buy or sell proprietary positions based on information contained in this report. Deutsche Bank may engage in securities transactions, on a proprietary basis or otherwise, in a manner inconsistent with the view taken in this research report. In addition, others within Deutsche Bank, including strategists and sales staff, may take a view that is inconsistent with that taken in this research report. Deutsche Bank has no obligation to update, modify or amend this report or to otherwise notify a reader thereof. This report is provided for information purposes only. It is not to be construed as an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Prices are current as of the end of the previous trading session unless otherwise indicated and are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the investor's home jurisdiction. In the U.S. this report is approved and/or distributed by Deutsche Bank Securities Inc., a member of the NYSE, the NASD, NFA and SIPC. In Germany this report is approved and/or communicated by Deutsche Bank AG Frankfurt authorized by the BaFin. In the United Kingdom this report is approved and/or communicated by Deutsche Bank AG London, a member of the London Stock Exchange and regulated by the Financial Conduct Authority for the conduct of investment business in the UK and authorized by the BaFin. This report is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in Korea by Deutsche Securities Korea Co. This report is distributed in Singapore by Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch (One Raffles Quay #18-00 South Tower Singapore 048583, +65 6423 8001), and recipients in Singapore of this report are to contact Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch in respect of any matters arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who is not an accredited investor, expert investor or institutional investor (as defined in the applicable Singapore laws and regulations), Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch accepts legal responsibility to such person for the contents of this report. In Japan this report is approved and/or distributed by Deutsche Securities Inc. The information contained in this report does not constitute the provision of investment advice. In Australia, retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any decision about whether to acquire the product. Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch Register Number in South Africa: 1998/003298/10). Additional information relative to securities, other financial products or issuers discussed in this report is available upon request. This report may not be reproduced, distributed or published by any person for any purpose without Deutsche Bank's prior written consent. Please cite source when quoting.

Copyright © 2014 Deutsche Bank AG