Embed Size (px)

Citation preview

CEE Meeting 2015 - LjubljanaThe Hungarian Experience

Andras TemmelSecretary General

www.bamosz.hu

I. Political-economical background1. Elections in 2014: 2/3 majority again for Fidesz

government» Economical consolidation, moderate growth (2-3%)» Stabilized budget deficit (constantly below 3%) and debt

(around 78-80%/GDP)» No big changes in taxation system – extraordinary taxes

seem to remain (bank tax, telecom tax etc.)» High VAT (27%), low tax rate on personal income (16%) and

on company profits (10% til 1,5 mEur and 19% above), massive tax benefits after children (e.g. 3 children, til 2 th Eur/month – 0% tax)

» Supported groups: upper-middle class with children, pensioners

2. Controversial political steps» New tobacco distribution system – „trafics/shops for friends”» Privatization of big state owned agricultural fields» Unexpected split in the Fidesz party – braking with the oldest

friend and oligarch » Clear signs of corruption – no steps against it» The radical right party (Jobbik) is coming up – 2 interval

elections won – 2/3 majority gone» Socialist party: no recovery» New era: migration problem –vast majority of the society is

supporting Orban

www.bamosz.hu

2

2

II. Economic overviewBasic indicators:» GDP: moderate growth» Unemployment rate is decreasing, but mainly thanks to

social work programs.» Slight growth in consumption, still industry and export

driven economic growth» Huge surplus in the foreign trade in past 4 years (6-7% of

the GDP) and in foreign fiscal balance (1-2%)» All time high currency reserves enabled the termination of

households foreign currency loans – very lucky timing» Budget deficit below 3% - but gov. bonds still rated under

investment grade – revision is expected

www.bamosz.hu

3

3

2014 2015 Q1 2015 Q2

GDP 3,6% 3,5% 2,7%

Investment 15,8% -3,9% 5,7%

Households consuption 1,5% 2,6% 2,6%

Budget deficit -2,6% -2,0% na

Unemployment rate 7,8% 6,9% 6,8%

Employment rate 61,8% 63,8% 64,1%

Industrial production 7,7% 11,0% 3,4%

Trade surplus / GDP 6,3%

Consumer prices -0,2% 0,6% 0,4%

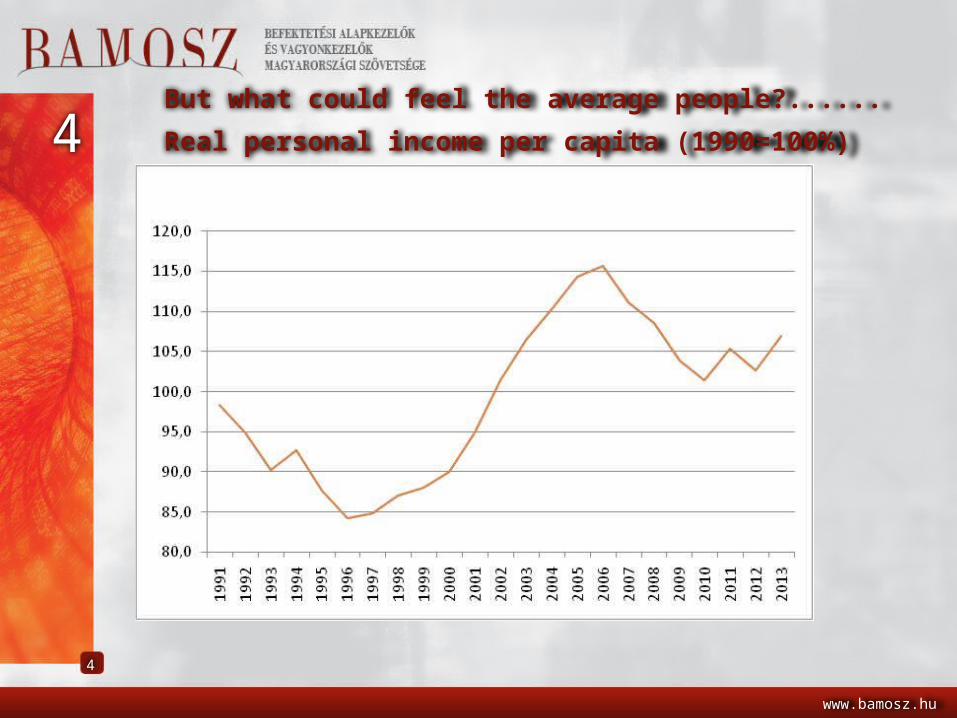

But what could feel the average people?......

Real personal income per capita (1990=100%)

www.bamosz.hu

4

4

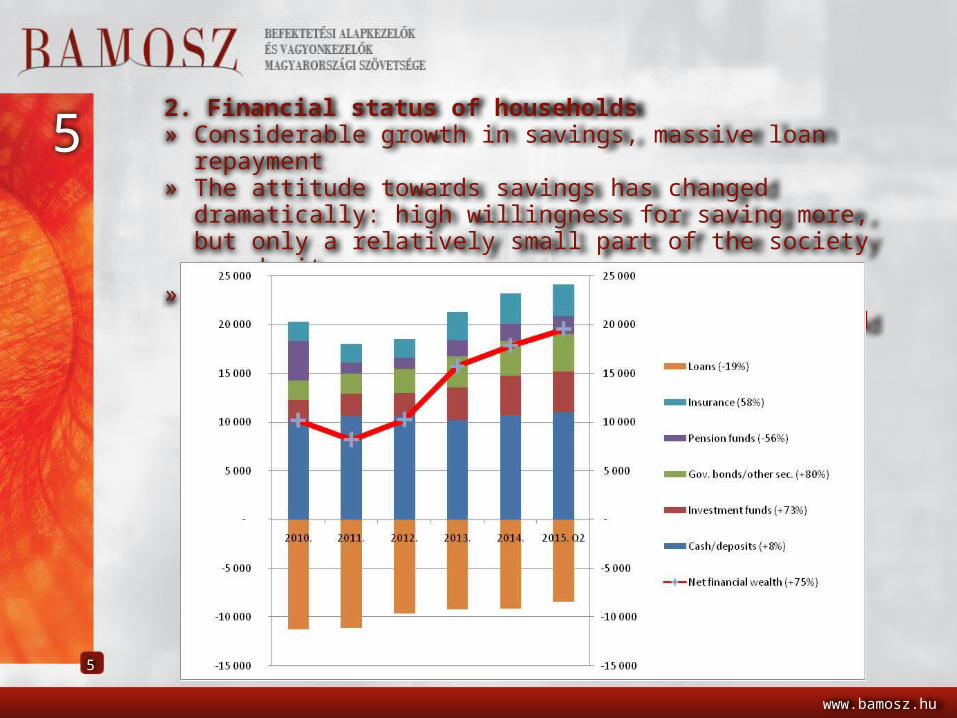

2. Financial status of households» Considerable growth in savings, massive loan repayment» The attitude towards savings has changed dramatically:

high willingness for saving more, but only a relatively small part of the society can do it.

» Fundamental changes on the savings market – winners: government bonds, investment funds and recently pension savings insurances

www.bamosz.hu

5

5

www.bamosz.hu

6

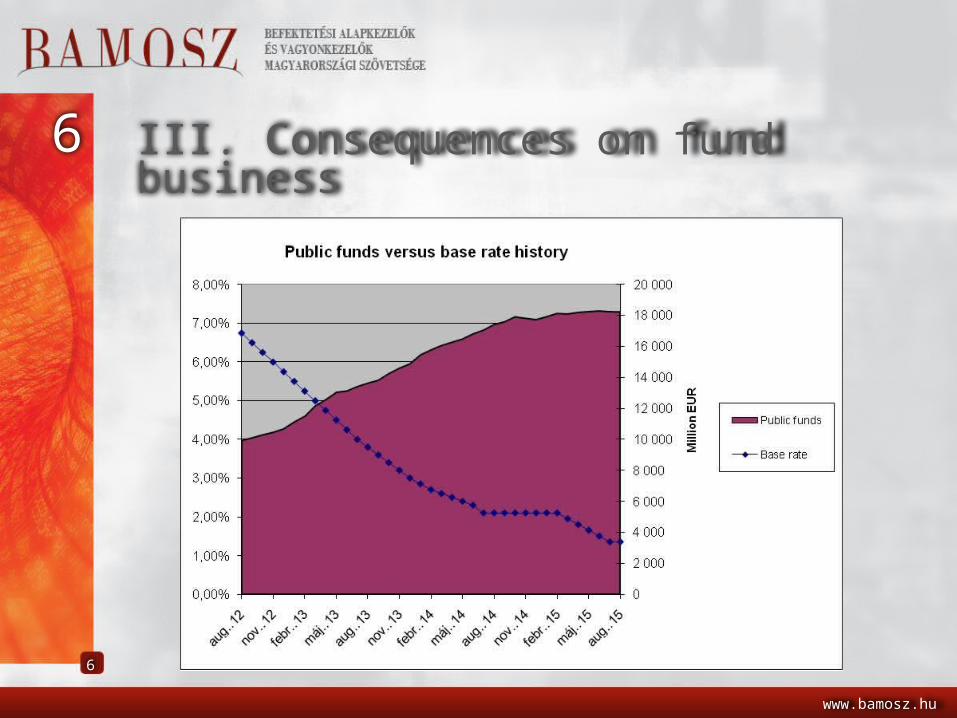

6 III. Consequences on fund business

www.bamosz.hu

7

7

0500

1 0001 5002 0002 5003 0003 5004 0004 5005 0005 5006 000

1994

. dec

.19

95. d

ec.

1996

. dec

.19

97. d

ec.

1998

. dec

.19

99. d

ec.

2000

. dec

.20

01. d

ec.

2002

. dec

.20

03. d

ec.

2004

. dec

.20

05. d

ec.

2006

. dec

.20

07. d

ec.

2008

. dec

.20

09. d

ec.

2010

. dec

.20

11. d

ec.

2012

. dec

.20

13. d

ec.

2014

. dec

.

bn

HU

F

From the beginning…

www.bamosz.hu

8

8 Big changes in the market share of different categories

Thank you!

www.bamosz.hu

9

9