Embed Size (px)

Citation preview

1 Copyright © 2017 Deloitte Development LLC. All rights reserved.

March 20, 2017

CBI - 13th Annual Life Sciences Accounting & Reporting Congress

Boot Camp - Accounting & Financial Reporting in Life Sciences Companies

Copyright © 2017 Deloitte Development LLC. All rights reserved. 2

Life Sciences

Focus StrategyPerformance

Transactions

ValueG

oals

Challenges

Controllership

Accounting

InnovationTeamwork

Reporting

Gro

wth

TechnologyDevelopment

Standards Regulation

Leadership

Transformations

Copyright © 2017 Deloitte Development LLC. All rights reserved. 3

Which presentation topic would you like to cover most?

a) Medicare Access & CHIP Reauthorization Act (MACRA) of 2015

b) Business combinations

c) Non-GAAP measures

d) Revenue: Collaboration and multiple element arrangements

e) SEC comment letter trends

f) Cost of goods sold and intercompany profit accounting

g) New Leasing Standard: ASC 842

Polling question #1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 4

Presentation topics

*Proposed durations (subject to audience feedback and participation)

Selection: Duration*

Overview & implications MACRA 30 minutes

Business combinations 30 minutes

Non GAAP measures 30 minutes

Revenue: Collaboration and multiple element arrangements 30 minutes

SEC comment letter trends 30 minutes

Cost of goods sold and intercompany profit accounting 30 minutes

New leasing standard: ASC 842 30 minutes

Copyright © 2017 Deloitte Development LLC. All rights reserved. 5

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

Disclaimer

As used in this document, “Deloitte” means Deloitte & Touche LLP, which is a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 6

Overview & implications of MACRA

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 7

MACRA is a bipartisan law that is poised to transform the future direction of health care

MACRA: Political context

“The passage of MACRA was a tremendous bipartisan achievement that addressed long-standing and reoccurring problems under Medicare. It was, I’ll note, one of the first of many significant bipartisan accomplishments we’ve seen in the 114th Congress.”

U.S. Senator Orrin Hatch (R-UT), Chairman Committee on Finance

“Now when it comes to replacing the SGR*, Medicare payment reform took the important step of engraving in stone the principle of rewarding medical care that provides quality over quantity... That’s the direction that health care is headed in across the country, and Medicare should be leading the way.”

U.S. Senator Ron Wyden(D-OR), Ranking Member Committee on Finance

*Sustainable Growth Rate (SGR)

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 8

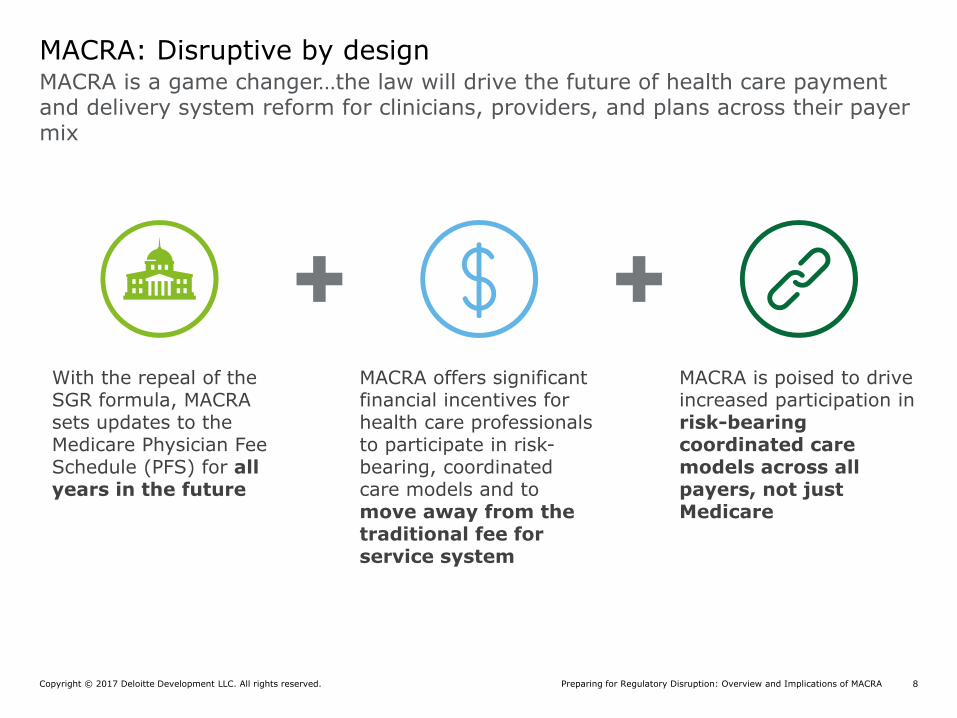

MACRA is a game changer…the law will drive the future of health care payment and delivery system reform for clinicians, providers, and plans across their payer mix

MACRA: Disruptive by design

MACRA offers significant financial incentives for health care professionals to participate in risk-bearing, coordinated care models and to move away from the traditional fee for service system

With the repeal of the SGR formula, MACRA sets updates to the Medicare Physician Fee Schedule (PFS) for all years in the future

MACRA is poised to drive increased participation in risk-bearing coordinated care models across all payers, not just Medicare

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 9

Advanced Alternative Payment Models

(APMs)

MACRA replaces the SGR formula for payments under the Medicare physician fee schedule (PFS) with fixed annual payment updates for all years in the future

Payment basics under MACRA

MACRA creates separate paths for payments under the Medicare physician fee schedule:

Merit-based Incentive Payment System

(MIPS)

Source: Public Law 114-10 (April 16, 2015)

APM25%

FFS75%

APM25%

• Bear financial risk for more than nominal monetary losses

• Base reimbursements for covered services on quality measures comparable to those used in MIPS, quality, resource use, clinical practice improvement

• Requires use of a Certified Electronic Health Record (CEHR)

• Eligible for a 5% lump sum incentive starting in 2019

• MIPS consolidates existing Physician Quality Reporting System (PQRS), Meaningful Use (MU) and Value Based Modifier (VBM) Programs

• Payment adjustments (both positive and negative) begin in 2019 based on performance in the following:

• Quality (PQRS)• Advancing Care Information

(Meaningful Use)• Cost (VBM)*• Improvement Activities (New)

• Note: Cost will not be used to determine payment adjustments until 2020

Beginning in 2019, clinician Medicare payment adjustments each year will depend on which

track the clinician’s medical group falls into.

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 10

Text

MACRA creates two separate paths for payments in addition to the Physician Fee Schedule

Payment updates, bonuses and adjustments under MACRA

2016:0.5%

2017: 0.5%

2018: 0.5%

2019: 0.5%

2020: 0%

2021: 0%

2022: 0%

2023: 0%

2024: 0%

2025: 0%

2026+: 0.75%

2026+: 0.25%PFS

Non QPs

APM QP

2019: +/-4%

2020: +/-5%

2021: +/-7%

2022 and subsequent years: +/-9%MIPS Performance

RangeMIPS

APM2019: 5%

2020: 5%

2021: 5%

2022: 5%

2023: 5%

2024: 5%

OR

Updates

Incentive Payments

Payment Adjustments

Source: Public Law 114-10 (April 16, 2015) *For 2019 through 2024, the highest performing MIPS eligible clinicians who receive a positive payment adjustment will be eligible to share up to $500 million each year for “exceptional performance” payments. This upside is limited by the statute to +10% of Medicare charges.

Physician Fee Schedule (PFS)

Alternative Payment Models (APMs)

Merit-Based Incentive Payment System (MIPS)

Preparing for Regulatory Disruption: Overview and Implications of MACRA]Copyright © 2017 Deloitte Development LLC. All rights reserved. 11

Overview of the quality payment program (QPP)

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 12

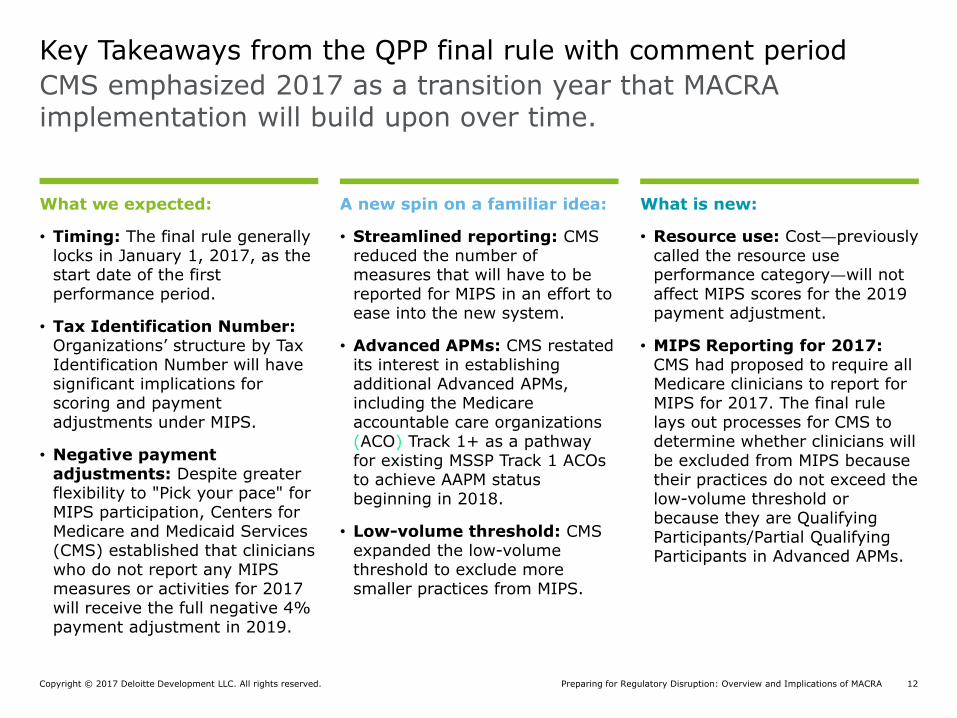

Key Takeaways from the QPP final rule with comment period

A new spin on a familiar idea:

• Streamlined reporting: CMS reduced the number of measures that will have to be reported for MIPS in an effort to ease into the new system.

• Advanced APMs: CMS restated its interest in establishing additional Advanced APMs, including the Medicare accountable care organizations (ACO) Track 1+ as a pathway for existing MSSP Track 1 ACOs to achieve AAPM status beginning in 2018.

• Low-volume threshold: CMS expanded the low-volume threshold to exclude more smaller practices from MIPS.

What we expected:

• Timing: The final rule generally locks in January 1, 2017, as the start date of the first performance period.

• Tax Identification Number: Organizations’ structure by Tax Identification Number will have significant implications for scoring and payment adjustments under MIPS.

• Negative payment adjustments: Despite greater flexibility to "Pick your pace" for MIPS participation, Centers for Medicare and Medicaid Services (CMS) established that clinicians who do not report any MIPS measures or activities for 2017 will receive the full negative 4% payment adjustment in 2019.

What is new:

• Resource use: Cost—previously called the resource use performance category—will not affect MIPS scores for the 2019 payment adjustment.

• MIPS Reporting for 2017: CMS had proposed to require all Medicare clinicians to report for MIPS for 2017. The final rule lays out processes for CMS to determine whether clinicians will be excluded from MIPS because their practices do not exceed the low-volume threshold or because they are Qualifying Participants/Partial Qualifying Participants in Advanced APMs.

CMS emphasized 2017 as a transition year that MACRA implementation will build upon over time.

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 13

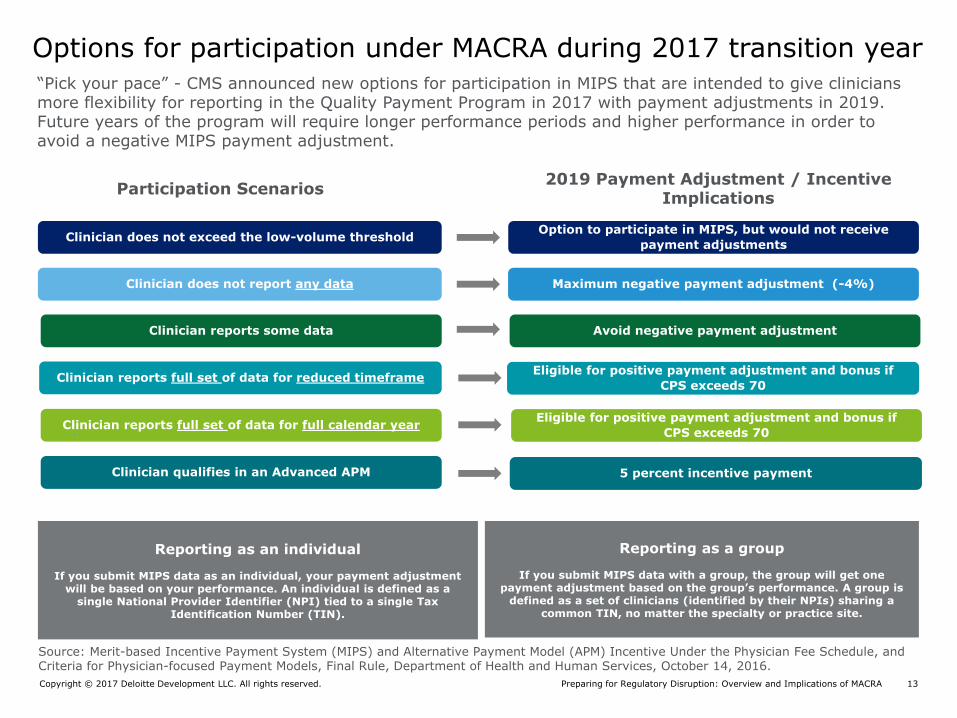

“Pick your pace” - CMS announced new options for participation in MIPS that are intended to give clinicians more flexibility for reporting in the Quality Payment Program in 2017 with payment adjustments in 2019. Future years of the program will require longer performance periods and higher performance in order to avoid a negative MIPS payment adjustment.

Participation Scenarios

Options for participation under MACRA during 2017 transition year

Reporting as an individual

If you submit MIPS data as an individual, your payment adjustment will be based on your performance. An individual is defined as a

single National Provider Identifier (NPI) tied to a single Tax Identification Number (TIN).

2019 Payment Adjustment / Incentive Implications

Source: Merit-based Incentive Payment System (MIPS) and Alternative Payment Model (APM) Incentive Under the Physician Fee Schedule, and Criteria for Physician-focused Payment Models, Final Rule, Department of Health and Human Services, October 14, 2016.

Maximum negative payment adjustment (-4%)Clinician does not report any data

Avoid negative payment adjustmentClinician reports some data

Eligible for positive payment adjustment and bonus if

CPS exceeds 70Clinician reports full set of data for reduced timeframe

Eligible for positive payment adjustment and bonus if

CPS exceeds 70Clinician reports full set of data for full calendar year

5 percent incentive payment Clinician qualifies in an Advanced APM

Option to participate in MIPS, but would not receive

payment adjustmentsClinician does not exceed the low-volume threshold

Reporting as a group

If you submit MIPS data with a group, the group will get one payment adjustment based on the group’s performance. A group is

defined as a set of clinicians (identified by their NPIs) sharing a common TIN, no matter the specialty or practice site.

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 14

The Final Rule weights Cost at 0% for the initial 2017 performance period. CMS reduced the number of required measures for ACI and Improvement Activities to be submitted in order to be eligible for the maximum positive adjustments. Quality reporting was also simplified for the transition year.

Overview of MIPS – including changes to the 2017 transition year

15% 15% 15%

25% 25% 25%

0%10%

30%

60%50%

30%

2017 2018 2019

Quality

Replaces the Physician Quality Reporting System (PQRS) Report up to six measures – including an outcome measure –

for a minimum of 90 days

Cost

Replaces Value-based Modifier Calculated from claims; no data submission required Counted in score beginning in 2018

Advancing Care Information

Replaces Medicare EHR Incentive Program for Providers (Meaningful Use)

Report four required measures for a minimum of 90 days Submit up to eleven measures for a minimum of 90 days for

additional credit

Improvement Activities

Attest to completion of up to four activities for a minimum of 90 days

Special consideration for smaller practices, patient-centered medical homes and certain APMs

Components of MIPS CPSPerformance Periods 2017-2019

Source: Merit-based Incentive Payment System (MIPS) and Alternative Payment Model (APM) Incentive Under the Physician Fee Schedule, and Criteria for Physician-focused Payment Models, Final Rule, Department of Health and Human Services, October 14, 2016.

Overview of General MIPS Reporting Requirements for 2017 Performance Year

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 15

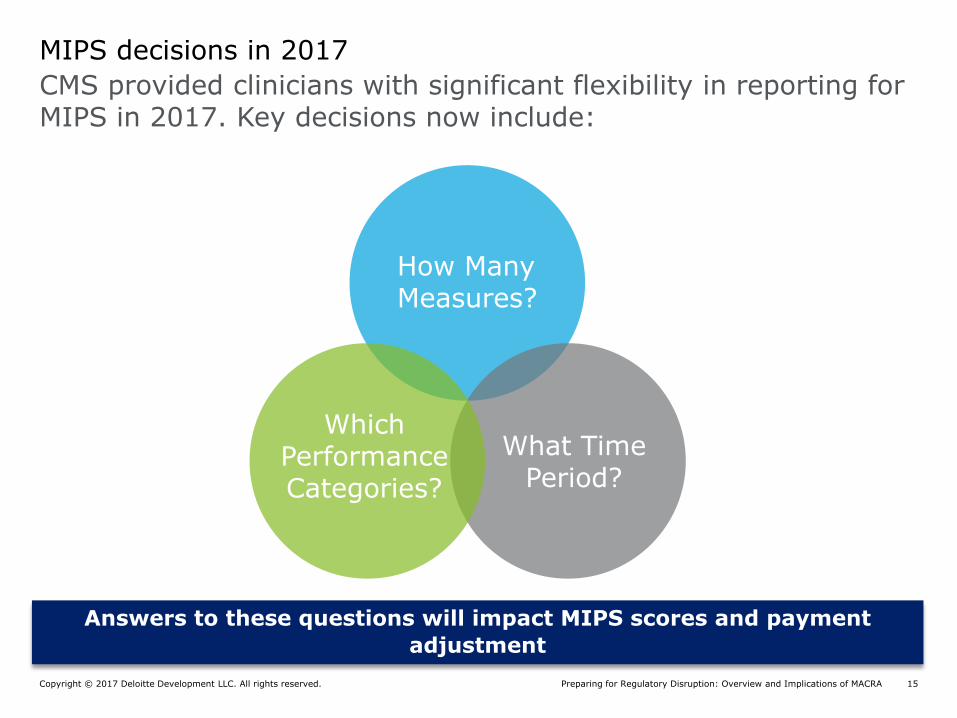

CMS provided clinicians with significant flexibility in reporting for MIPS in 2017. Key decisions now include:

MIPS decisions in 2017

How Many Measures?

What Time Period?

Which Performance Categories?

Answers to these questions will impact MIPS scores and payment

adjustment

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 16

CMS illustrative example: how the payment adjustment will work

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

0 10 20 30 40 50 60 70 80 90 100

Adju

stm

ent

Facto

rs

Final Score

MIPS Adjustment Factors Based on Final Scores

PerformanceThreshold = 3

Plus Additional Adjustment Factor

Adjustment Factor

The performance

threshold is akin to

the "pass/fail" score

for MIPS – clinicians

with lower scores

will get negative

adjustments, higher

scores get positive

adjustments

The additional

performance threshold

is the score MIPS

eligible clinicians need

to achieve to qualify for

additional payment

adjustment

factors for exceptional

performance

Source: Final Rule with Comment Period on Merit-based Incentive Payment System (MIPS) and Alternative Payment Model (APM) Incentive (November 4, 2016)

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 17

Key Highlights: advanced APMs

Key ConsiderationsKey Considerations

Enrollment: Application cycle for 2017 is closed

Timing: Next application cycle for MSSP will begin in April 2017 for 2018. Next Generation ACO Model and CPC+ Model will reopen and accept new applications for 2018.

Additional Options: The Physician-Focused Payment Technical Advisory Committee (PTAC) is accepting proposals from individuals and stakeholder-entities on new physician-focused payment models.

1. Next Generation ACO Model

2. Medicare Shared Savings Program (MSSP) ACOs — Track 2

3. MSSP ACOs — Track 3

4. Comprehensive Primary Care Plus (CPC+) Model

5. Oncology Care Model (OCM) two-sided risk arrangement

6. Comprehensive End-Stage Renal Disease (ESRD) Care (CEC) Model - Large Dialysis Organization (LDO) arrangement

7. Comprehensive ESRD Care Model (non-LDO two-sided risk arrangement

8. Vermont Medicare ACO Initiative (as part of the Vermont All-Payer ACO Model)

1. Medicare ACO Track 1+

2. Advancing Care Coordination through Episode Payment Models (EPMs) Track 1 Certified Electronic Health Record Technology (CEHRT)

3. Comprehensive Care for Joint Replacement (CJR) Payment Model (CEHRT)

Anticipated Available for 2017

Proposed / in Development to be Implemented in 2017 or 2018

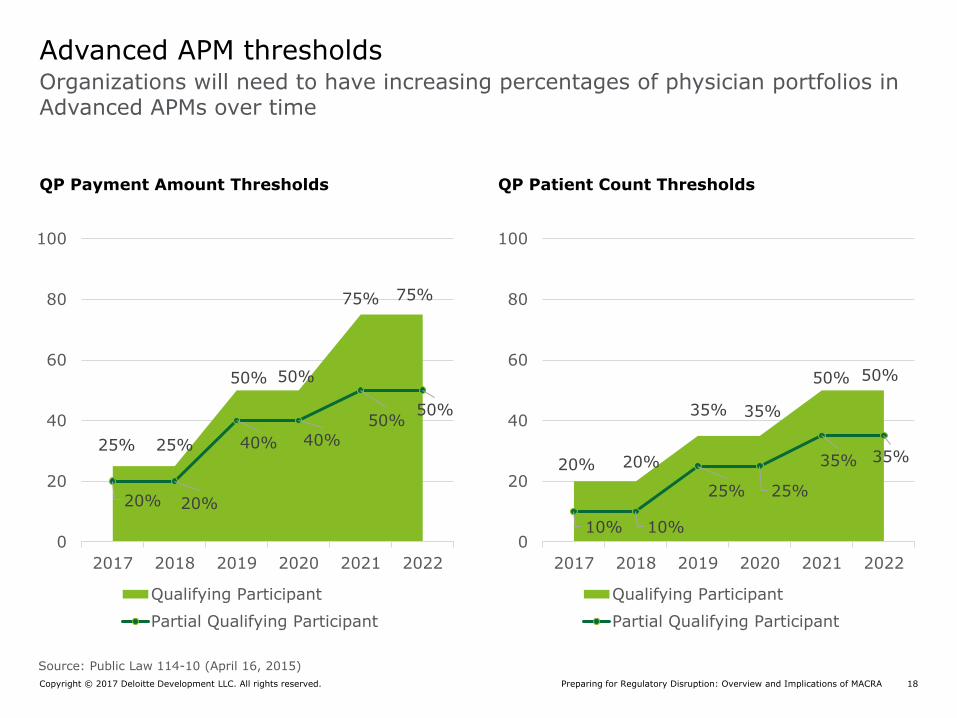

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 18

20% 20%

35% 35%

50% 50%

10% 10%

25% 25%

35% 35%

0

20

40

60

80

100

2017 2018 2019 2020 2021 2022

Qualifying Participant

Partial Qualifying Participant

QP Patient Count Thresholds

Organizations will need to have increasing percentages of physician portfolios in Advanced APMs over time

Advanced APM thresholds

25% 25%

50% 50%

75% 75%

20% 20%

40% 40%

50%50%

0

20

40

60

80

100

2017 2018 2019 2020 2021 2022

Qualifying Participant

Partial Qualifying Participant

QP Payment Amount Thresholds

Source: Public Law 114-10 (April 16, 2015)

Preparing for Regulatory Disruption: Overview and Implications of MACRA]Copyright © 2017 Deloitte Development LLC. All rights reserved. 19

Deloitte 2016 survey of US health care and life sciences executives

Taking a pulse on MACRA

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 20

CMS has announced $100 million in funding for small practice physicians to understand the Quality Payment Program.

Many physicians recognize they will need new capabilities in order to bear increased financial risk

Top needed supporting capabilities reported by surveyed physicians are related to reporting and include:

Source: Deloitte 2016 Survey of US Physicians.

Standardizedquality measures

42%

Analytics and othermonitoring tools to track

high-cost patients

29%

Standardized costmeasures

28%

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 21

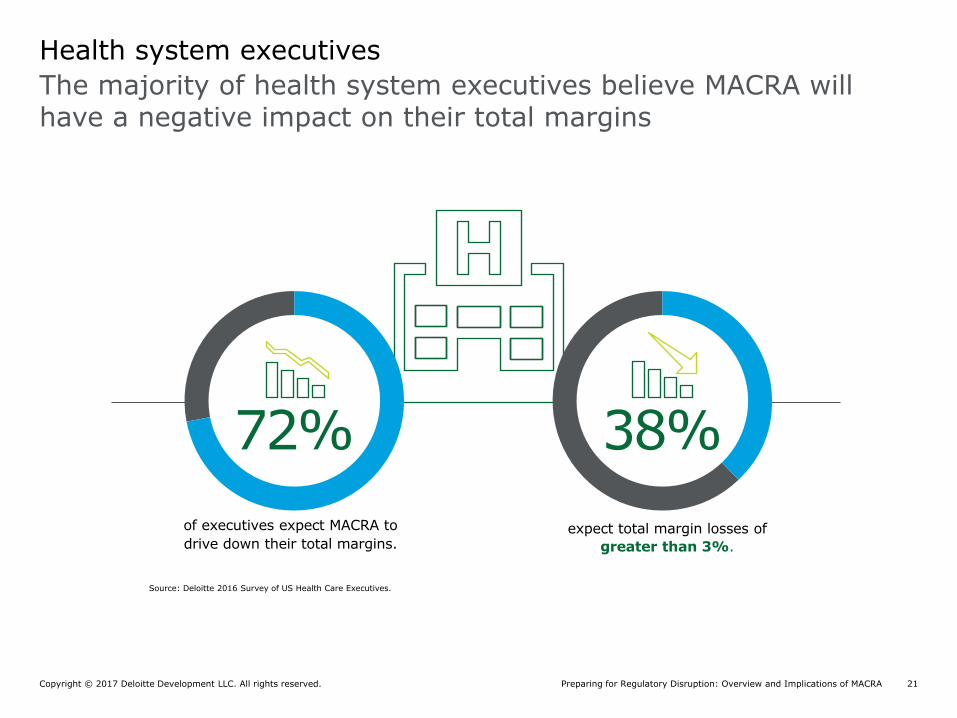

Health system executives

expect total margin losses of

greater than 3%.

of executives expect MACRA to

drive down their total margins.

72% 38%

Source: Deloitte 2016 Survey of US Health Care Executives.

The majority of health system executives believe MACRA will have a negative impact on their total margins

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 22

Most medtech and biopharma

executives believe

that MACRA will cause

hospital and health plandemand for

value- basedcontracting

arrangementsfrom their

company toincrease.

Some biopharma and medtech

executives believe that MACRA will have a negative impact on how

they do business with health systems;

independent clinicians; and health plans.

Most biopharma and

medtech executives believe that MACRA will

drive physicians to

join larger organizations

.

Most biopharma executives agree or

strongly agree that MACRA will make it

more difficult for patients

to access thecare,

services, orproducts

they need.

Source: Deloitte 2016 Survey of US Health Care Executives

Life sciences executives believe MACRA will lead to greater demand for value-based care but also disruption for their businesses

Life sciences executives

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 23

Most medtech

executives believe that

MACRA will have a

negative or neutral

impact on their total

margins.

Half of biopharma

executives believe that

MACRA will negatively

impact their total margins

while the other half believes

it will have no impact.

Many medtech executives believe their company’s margins will decrease under MACRA, while half of biopharma executives foresee no impact

Life sciences executives

Preparing for Regulatory Disruption: Overview and Implications of MACRACopyright © 2017 Deloitte Development LLC. All rights reserved. 24

Only 1 biopharma executiverespondent and no medtechexecutives say that MACRA hascaused them to pursue morevalue-based paymentarrangements in the future.

If Medicare were to create incentives

for hospitals and physicians to

consider the costs of drugs and

devices when making treatment

decisions, 13% of biopharma and

half of medtech executives would

explore risk-sharing agreements and

25% of biopharma

and half of medtech executives would invest in developingadditional evidence to demonstratecost-effectiveness.

Most (85%) medtech

executives already had

plans to implement

value-based payment

arrangements and

MACRA did not change

them.

Life sciences companies are interested in making investments to

generate additional evidence or exploring risk-sharing agreements in

response to MACRA, but many are not speeding up their value-based

care plans

Life sciences executives

Copyright © 2017 Deloitte Development LLC. All rights reserved. 25

Business combinations

Copyright © 2017 Deloitte Development LLC. All rights reserved. 26

The FASB added the project to the agenda for two primary reasons:

• Practice issues raised in the post-implementation review (PIR) of Statement 141(R), Business Combinations

• Issues raised within the new revenue standard:

− The scope of new revenue standard includes nonfinancial assets and transactions with

noncustomers (Subtopic 610-20, Other Income– Gains and Losses from the Derecognition of

Nonfinancial Assets). However, it excludes businesses (and not an in substance nonfinancial

asset).

− The standard supersedes the partial sales guidance in Subtopic 360-20, Sales of Real Estate

leaving no guidance on partial sales of real estate

The FASB decided to address the project in three phases:

• Phase 1: Clarify the definition of a business

• Phase 2: Address the accounting for partial sales and clarify the scope of Subtopic 610-20

• Phase 3: Address business versus asset accounting differences.

Project background: Clarifying the definition of a business

Copyright © 2017 Deloitte Development LLC. All rights reserved. 27

• Public business entities should apply the amendments by:

− Annual periods beginning after December 15, 2017, including interim periods within

those periods

• All other entities should apply the amendments by:

− Annual periods beginning after December 15, 2018 and interim periods with annual

periods beginning after December 15, 2019.

• The amendments should be applied prospectively as of the beginning of the period of adoption.

Effective amendment requirements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 28

Asset Business

ContingentConsideration

Typically not recognized until the contingency is resolved

Recognized at acquisition date fair value with changes in estimate recognized through earnings after the acquisition date

IPR&D Expensed as incurred unless it has an alternative future use

Measured at fair value and recognized as an indefinite-lived intangible asset until completion or abandonment of the project.

Transaction costs Capitalized Expensed

Initial measurement

Allocated on a relative fair value basis

Fair value

Goodwill/BargainPurchase

Goodwill/Bargain purchases are not recognized and allocated on a relative basis to assets and liabilities

Goodwill recognized as an asset; Bargain purchase recognized immediately in earnings

Why does it matter: Acquisition accounting differences

Copyright © 2017 Deloitte Development LLC. All rights reserved. 29

Asset (Subtopic 610-20) Business (Topic 810)

Control Control assessed pursuant to the new revenue standard

Consolidation guidance determines control

Variable Consideration

Included in transaction price subjectto the constraint on variable consideration in Topic 606

Policy election:1) Recognize at fair value; or2) Recognize as contingency is

resolved (FAS 5)

Existence of a Contract

Must evaluate Topic 606 guidance including collectibility

No such consideration

Goodwill allocation Disposals do not impact goodwill Goodwill is allocated to disposals

Measurement of Retained Interest in noncontrolling investment

Tentative FASB (“Board”) Decision on Phase 2: retained interest measured at carryover basis

Fair value

Why does it matter:derecognition differences

Copyright © 2017 Deloitte Development LLC. All rights reserved. 30

Excerpts from ASC 805-10-55-4 through 55-9:

• A business is an integrated set of activities and assets that is capable of being conducted and managed through the purpose of providing a return in the form of dividends, lower costs, or other economic benefits directly to investors or other owners, members, or participants.

• A business consists of inputs and processes applied to those inputs that have the ability to contribute to the creation of outputs. Although a business usually has outputs, outputs are not required to qualify as a business.

• A business need not include all of the inputs or processes that the seller used in operating that business if market participants are capable of acquiring the business and continuing to significantly contribute to produce outputs

Inputs

Processes

Ability to create

outputs

• In the absence of evidence to the contrary, a particular set of assets and activities in which goodwill is present shall be presumed to be a business. However, a business need not have goodwill.

Current definition of a business

Copyright © 2017 Deloitte Development LLC. All rights reserved. 31

Did you have a business combination or asset acquisition this year?

A. Yes

B. No

C. Not sure

Polling question #2

Copyright © 2017 Deloitte Development LLC. All rights reserved. 32

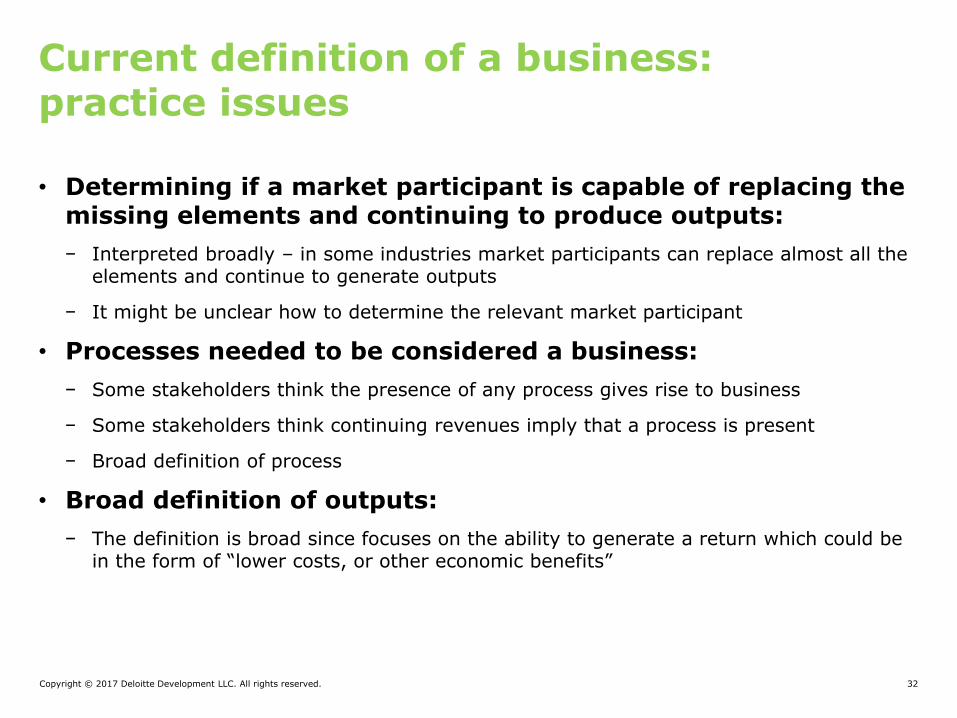

• Determining if a market participant is capable of replacing the missing elements and continuing to produce outputs:

− Interpreted broadly – in some industries market participants can replace almost all the elements and continue to generate outputs

− It might be unclear how to determine the relevant market participant

• Processes needed to be considered a business:

− Some stakeholders think the presence of any process gives rise to business

− Some stakeholders think continuing revenues imply that a process is present

− Broad definition of process

• Broad definition of outputs:

− The definition is broad since focuses on the ability to generate a return which could be in the form of “lower costs, or other economic benefits”

Current definition of a business:practice issues

Copyright © 2017 Deloitte Development LLC. All rights reserved. 33

• Single or Similar Asset Threshold:

− If substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or group of similar identifiable assets the set is not considered a business.

− Gross assets acquired should exclude cash and cash equivalents, deferred tax assets, and goodwill resulting from the effects of deferred tax liabilities.

− The Board intends for this to be a practical “screen”

• At a minimum, to be a business, a set must include and input and a substantive process:

− The Board also decided to provide a framework to assist in this determination

− The Board decided to remove the requirement that a market participant must be able to replace all the missing elements in order to be a business

• Outputs should be defined similar to goods or services provided to customers (i.e., focus on revenue)

Definition of a business:Major changes

Copyright © 2017 Deloitte Development LLC. All rights reserved. 34

• The Board decided on the threshold of “substantially all”.

• The comparison of the fair value is made between the single identifiable asset or group of similar assets compared to the gross assets acquired (including goodwill but excluding liabilities)

• A single asset is any asset that would be recognized and measured separately in a business combination:

− Some tangible assets that are attached can be considered a single asset. For example, land and buildings can be a single asset for this purpose.

• The Board did not provide guidance on what is considered similar but provided some guidelines for what cannot be considered similar:

− Tangible and intangible assets

− Different major classes of intangible assets

− Financial and nonfinancial

− Different major classes of financial assets

− Different major classes of tangible nonfinancial assets

− Identifiable assets with same major asset class with different risk characteristics

Single of similar asset threshold

Copyright © 2017 Deloitte Development LLC. All rights reserved. 35

Single of similar asset threshold example

Case B: Acquisition of a Drug Candidate

805-10-55-65 Pharma Co. purchases from Biotech a legal entity that contains the rights to a Phase 3 compound being developed to treat diabetes (the in-process research and development project). Included in the in-process research and development project is the historical know-how, formula protocols, designs, and procedures expected to be needed to complete the related phase of testing. The legal entity also holds an at-market clinical research organization contract and an at-market clinical manufacturing organization contract. No employees, other assets, or other activities are transferred.

805-10-55-66 Pharma Co. first considers the guidance in paragraph 805-10-55-5A through 55-5C. Pharma Co. concludes that the in-process research and development project is an identifiable intangible asset that would be accounted for as a single asset in a business combination. Pharma Co. also qualitatively concludes that there is no fair value associated with the clinical research organization contract and the clinical manufacturing organization contract because the services are being provided at market rates and could be provided by multiple vendors in the marketplace. Therefore, all of the consideration in the transaction would be allocated to the in-process research and development project. As such, Big Pharma concludes that substantially all of the fair value of the gross assets acquired is concentrated in the single in-process research and development asset and the set is not a business.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 36

• Case B Summary:

− Assets acquired are the in process research & development (IPR&D) project, contract research organization (CRO) contract and contract manufacturing organization (CMO) contract

− The CRO and CMO contracts are “at market” and do not have any fair value

− IPR&D asset is a single asset

− No employees are transferred

• Case B illustrates the application of the threshold:

− All of the fair value is concentrated in the single IPR&D asset

− The set is not a business

Single of similar asset threshold example

Copyright © 2017 Deloitte Development LLC. All rights reserved. 37

• The Board clarified that to be a business the set must include, at a minimum, an input and substantive process that together contribute the ability to create outputs.

• The Board proposed to remove the language that requires an assessment of whether the market participant can replace the missing elements:

− The removal is intended to refocus the analysis on what is acquired

− The Board thought this was no longer required if the minimum requirements were set

− Takes pressure off of identifying the market participant

• The Board decided to provide a framework to evaluate when the minimum requirements have been met:

− The Board decided on different criteria based on if the set includes outputs

Substantive processes

Copyright © 2017 Deloitte Development LLC. All rights reserved. 38

• When a set does not have outputs (for example, an early stage company that has not generated revenues) the set would have both an input and a substantive process if it includes:

− An organized workforce that has the necessary skills, knowledge, or experience necessary to perform an acquired process (or group of processes) that when applied to another acquired input(s) is critical to the ability to develop or convert that acquired input into outputs.

• When no outputs are present, the set must have both a workforce and input that works together to contribute to the ability to create outputs.

• The Board believes that the workforce must perform a critical process:

− The existence of any employee does not automatically indicate the set is a business

− A process is not critical if considered minor or ancillary. Judgment will be required to determine if the process is critical.

− The process has to contribute to developing or converting an acquired input

Substantive process: No outputs

Copyright © 2017 Deloitte Development LLC. All rights reserved. 39

Substantive process: No outputs example

Case C: Acquisition of Biotech

805-10-55-70 Pharma Co. buys all of the outstanding shares of Biotech. Biotech’s operations include research and development activities on several drug compounds that it is developing (in-process research and development projects). The in-process research and development projects are in different phases of the U.S. Food and Drug Administration approval process and would treat significantly different diseases. The set includes senior management and scientists that have the necessary skills, knowledge, or experience to perform research and development activities. In addition, Biotech has long-lived tangible assets such as a corporate headquarters, a research lab, and lab equipment. Biotech does not yet have a marketable product and, therefore, has not generated revenues. Assume that each research and development project has a significant amount of fair value.

(paragraph 805-10-55-71 omitted)

805-10-55-72 Because the set does not have outputs, Pharma Co. evaluates the criteria in paragraph 805-10-55-5D to determine whether the set has both an input and a substantive process that together significantly contribute to the ability to create outputs. Pharma Co. concludes that the criteria are met because the scientists make up an organized workforce that has the necessary skills, knowledge, or experience to perform processes that, when applied to the in-process research and development inputs, is critical to the ability to develop those inputs into a good that can be provided to a customer. Pharma Co. also determines that the is more-than-insignificant amount of goodwill (including the fair value associated with the workforce), which is another indicator that the workforce is performing a critical process. Thus, the set includes both inputs and substantive processes and is a business.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 40

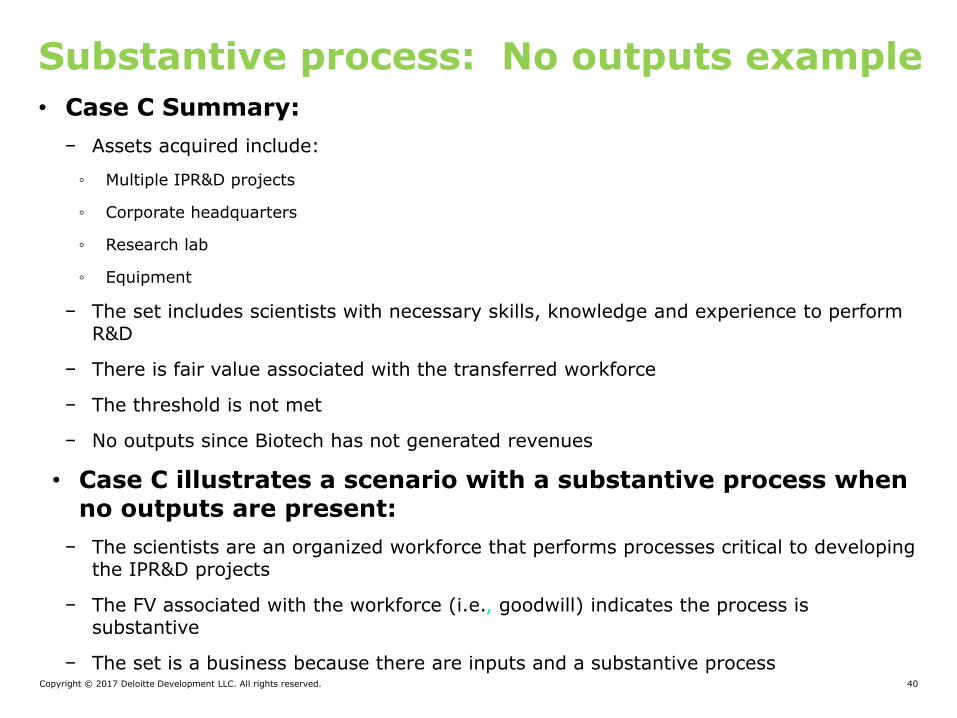

• Case C Summary:

− Assets acquired include:

◦ Multiple IPR&D projects

◦ Corporate headquarters

◦ Research lab

◦ Equipment

− The set includes scientists with necessary skills, knowledge and experience to perform R&D

− There is fair value associated with the transferred workforce

− The threshold is not met

− No outputs since Biotech has not generated revenues

• Case C illustrates a scenario with a substantive process when no outputs are present:

− The scientists are an organized workforce that performs processes critical to developing the IPR&D projects

− The FV associated with the workforce (i.e., goodwill) indicates the process is substantive

− The set is a business because there are inputs and a substantive process

Substantive process: No outputs example

Copyright © 2017 Deloitte Development LLC. All rights reserved. 41

• If the set has outputs (that is, there is a continuation of revenue before and after the transaction), the set would have a substantive process when any of the following are present:

− An organized workforce that has the skills, knowledge, or experience necessary to perform an acquired process that is critical to the ability to create outputs.

− An acquired contract that provides access to an organized workforce that has the necessary skills, knowledge, or experience to perform an acquired process (or group of processes) that when applied to an acquired input or inputs is critical to the ability to continue producing outputs

− The acquired process cannot be replaced without significant cost, effort or delay in the ability to continue producing outputs.

− The acquired process is considered unique or scarce

• When outputs are present, a workforce is not required. The last two criteria address when a process is substantive without a workforce.

Substantive process: Outputs are present

Copyright © 2017 Deloitte Development LLC. All rights reserved. 42

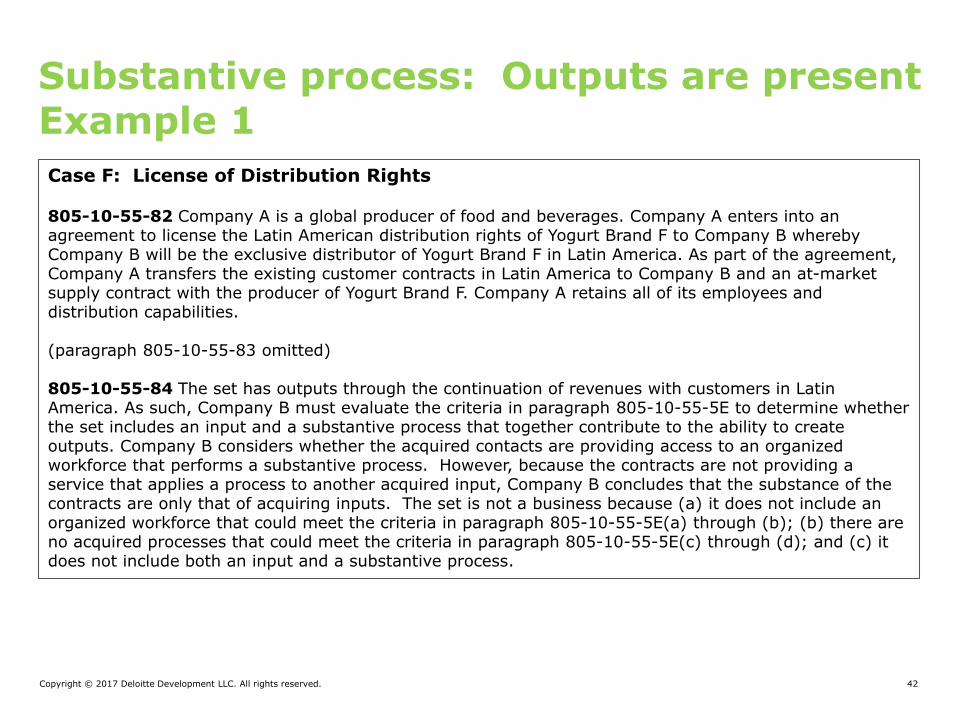

Substantive process: Outputs are present Example 1

Case F: License of Distribution Rights

805-10-55-82 Company A is a global producer of food and beverages. Company A enters into an agreement to license the Latin American distribution rights of Yogurt Brand F to Company B whereby Company B will be the exclusive distributor of Yogurt Brand F in Latin America. As part of the agreement, Company A transfers the existing customer contracts in Latin America to Company B and an at-market supply contract with the producer of Yogurt Brand F. Company A retains all of its employees and distribution capabilities.

(paragraph 805-10-55-83 omitted)

805-10-55-84 The set has outputs through the continuation of revenues with customers in Latin America. As such, Company B must evaluate the criteria in paragraph 805-10-55-5E to determine whether the set includes an input and a substantive process that together contribute to the ability to create outputs. Company B considers whether the acquired contacts are providing access to an organized workforce that performs a substantive process. However, because the contracts are not providing a service that applies a process to another acquired input, Company B concludes that the substance of the contracts are only that of acquiring inputs. The set is not a business because (a) it does not include an organized workforce that could meet the criteria in paragraph 805-10-55-5E(a) through (b); (b) there are no acquired processes that could meet the criteria in paragraph 805-10-55-5E(c) through (d); and (c) it does not include both an input and a substantive process.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 43

• Case F Summary

− Assets acquired include:

◦ License to distribute Brand F in Latin America

◦ Customer contracts

◦ Supply contract

− The set does not include a workforce

− The threshold is not met

− The set includes outputs (the continuing revenues through customer contracts)

• Case F illustrates a scenario with outputs and no substantive processes:

− The customer contracts cannot be considered a substantive process

− The supply contract is not a process that is being applied to acquired inputs

− Because there are no substantive processes the set is not a business

Substantive process: Outputs are present Example 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 44

Non-GAAP measures

Copyright © 2017 Deloitte Development LLC. All rights reserved. 45

Background

Non-GAAP measures

Dramatic increasein press coverage

and increasing SEC focus

Concerns about the

increased use and

prominenceLarger

differences between such measures and

amounts reported

under GAAP

Potentialfor such

measuresto be

misleading

Issuance of updated C&DIs

Call for registrants to self-correct

Non-GAAP comments

have increasedas a % oftotal SEC comments

Copyright © 2017 Deloitte Development LLC. All rights reserved. 46

Evolution of Non-GAAP measure rules and regulations

Non-GAAP measures

2001

2003

2010

2015

2016

SEC issues “cautionary advice” to registrants

SEC issues Regulation G and S-K Item 10(e)

Compliance & Disclosure Interpretations (C&DI’s) issued by SEC

SEC increases focus on non-GAAP measures as measures increase in use and prominence

New and updated C&DIs issued by SEC

Copyright © 2017 Deloitte Development LLC. All rights reserved. 47

Recent disclosure trends

Non-GAAP measures

Use and prevalence of Non-GAAP measures continues to increase

− Approximately 88% of S&P 500 component companies use non-GAAP measures:1

◦ Non-GAAP performance measures were greater than nearest GAAP equivalent for about 82% of the S&P 500 companies that reported a non-GAAP adjusted net income metric1

− In 2015, 67% of the companies in the Dow Jones Industrial Average reported non-GAAP earnings per share and, on average, the difference between GAAP and non-GAAP earnings per share was approximately 30%, representing a significance increase from approximately 12% in 20142

− Credit Suisse observed through an analysis of the seven large cap US pharma companies it covers that the spread between GAAP and non-GAAP net results has widened, with non-GAAP net income being ~40% higher than GAAP over the past 13 quarters3

“In too many places, the non-GAAP information, which is meant to supplement the GAAP information, has become the key message to investors, crowding out and effectively supplanting the GAAP presentation.”4

-Mary Jo White, former Chair, Securities & Exchange Commission

Sources:

1 Audit Analytics, “Trends in Non-GAAP Disclosures” (December 2015).

2 “Did DJIA Companies Report Higher Non-GAAP EPS in FY 2015?” FactSet Insight (March 11, 2016).

3 Credit Suisse, “US Pharmaceuticals: Minding the (Increasing) GAP Between GAAP and Non-GAAP Results” (July 2016).4 “Keynote Address, International Corporate Governance Network Annual Conference: Focusing the Lens of Disclosure to Set the Path Forward Board Diversity, Non-GAAP, and Sustainability” (June 27, 2016).

Copyright © 2017 Deloitte Development LLC. All rights reserved. 48

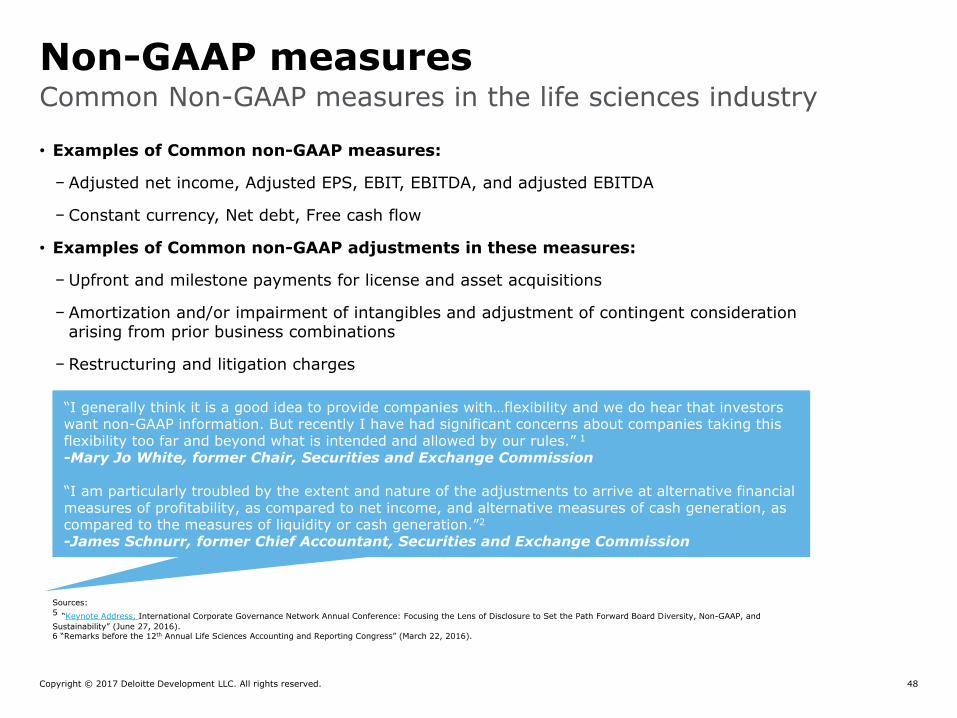

Common Non-GAAP measures in the life sciences industry

Non-GAAP measures

• Examples of Common non-GAAP measures:

− Adjusted net income, Adjusted EPS, EBIT, EBITDA, and adjusted EBITDA

− Constant currency, Net debt, Free cash flow

• Examples of Common non-GAAP adjustments in these measures:

− Upfront and milestone payments for license and asset acquisitions

− Amortization and/or impairment of intangibles and adjustment of contingent consideration arising from prior business combinations

− Restructuring and litigation charges

“I generally think it is a good idea to provide companies with…flexibility and we do hear that investors want non-GAAP information. But recently I have had significant concerns about companies taking this flexibility too far and beyond what is intended and allowed by our rules.” 1

-Mary Jo White, former Chair, Securities and Exchange Commission

“I am particularly troubled by the extent and nature of the adjustments to arrive at alternative financial measures of profitability, as compared to net income, and alternative measures of cash generation, as compared to the measures of liquidity or cash generation.”2

-James Schnurr, former Chief Accountant, Securities and Exchange Commission

Sources:

5 “Keynote Address, International Corporate Governance Network Annual Conference: Focusing the Lens of Disclosure to Set the Path Forward Board Diversity, Non-GAAP, and

Sustainability” (June 27, 2016).6 “Remarks before the 12th Annual Life Sciences Accounting and Reporting Congress” (March 22, 2016).

Copyright © 2017 Deloitte Development LLC. All rights reserved. 49

The Rules

SEC Rule Overview of the requirements

Regulation G • Non-GAAP financial measures must not be misleading.

• The most directly comparable GAAP measure must be presented.

• A quantitative reconciliation of the non-GAAP financial measure to the most comparable GAAP measure must be presented for:

−a historical non-GAAP measure and

− forward-looking information (to the extent available without unreasonable effort)

Item 10(e) of Regulation S-K

Expands upon Reg. G requirements to also include:

• Present most directly comparable GAAP measure with greater or equal prominence of that of the non-GAAP measure

• Disclosure indicating why the registrant believes that the non-GAAP measure is useful to investors

• Disclosure of the additional purposes, if any, for which the registrant uses the non-GAAP measure

Non-GAAP measures

Copyright © 2017 Deloitte Development LLC. All rights reserved. 50

Updated compliance and disclosure interpretationsNon-GAAP measures

• More prominent presentation of non-GAAP measures (C&DI 102.10):

− Full non-GAAP income statement

− Omitting comparable GAAP measures from press release headlines

− Bolder or larger font

− Non-GAAP measure that precedes a comparable GAAP measure

− Equally prominent description for a GAAP measure (e.g., “record performance”)

− Disclosures related to forward looking non-GAAP measures

− Same discussion and prominence for GAAP measures

− Tabular disclosure/reconciliation that starts with a non-GAAP measure

“Non-GAAP measures are intended to supplement …and not supplant the information in the financial statements.”-Jim Schnurr, former Chief Accountant, Office of the Chief Accountant

Copyright © 2017 Deloitte Development LLC. All rights reserved. 51

Updated compliance and disclosure interpretations

Non-GAAP measures

Misleading measures (C&DI 100.01–100.04):

− Financial measures using individually tailored accounting principles (C&DI 100.4)

◦ Using a registrants' own set of accounting principles to determine a non-GAAP measure

◦ Staff may not object to a measure that adjusts to reflect the adoption of the new revenue recognition accounting standard

• Prohibition on presenting liquidity measures on a per share basis (C&DI 102.05):

− Designated performance measures that are really liquidity measures

• Non-GAAP tax expense (C&DI 102.11):

− Tax adjustments commensurate with the non-GAAP measure of profitability

− Clear explanation of how the adjustment was determined

Copyright © 2017 Deloitte Development LLC. All rights reserved. 52

SEC comment letter trends—recent areas of focus

Non-GAAP measures

Prominence: When a registrant presents its non-GAAP financial measures more prominently than its GAAP measures (e.g., the registrant presents them before, or places greater emphasis on them than its GAAP measures, or presents a full non-GAAP Income Statement)

Sample comment:

We note that in your executive summary you focus on key non-GAAP financial measures and not GAAP financial measures which may be inconsistent with the updated Compliance and Disclosure Interpretations issued on May 17, 2016 (specifically Question 102.10). We also note issues related to prominence within your earnings release . . . . Please review this guidance when preparing your nextearnings release.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 53

SEC comment letter trends—recent areas of focus (cont.)

Non-GAAP measures

Purpose and use: Includes comments on whether the disclosures demonstrate the purpose of the measures (i.e., their usefulness to investors and how management uses them).

Sample comment:

Please revise to disclose the reasons why you believe your presentation of each of the non-GAAP financial measures provides useful information to investors regarding your financial condition and results of operations. The justification for the use of the non-GAAP financial measure must be substantive. Merely indicating that you provide such non-GAAP financial measures to give investors additional data to evaluate your operations is not sufficient support for disclosure of the non-GAAP financial measures. Please also revise to expand your disclosure of the additional purposes for which management uses each of the non-GAAP financial measures. Please refer to Item 10(e) of Regulation S-K.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 54

SEC comment letter trends—recent areas of focus (cont.)

Non-GAAP measures

Impact of income taxes: comments on the calculation of the tax impact of non-GAAP adjustments and the related disclosures.

Sample comment:

Please expand your disclosures to explain how you calculated the tax effect for the adjustments to net (loss) income attributable to . . . and per diluted share in accordance with the guidance in Question 102.11 of the Non-GAAP Financial Measures Compliance & Disclosure Interpretations.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 55

SEC comment letter trends—recent areas of focus (cont.)

Non-GAAP measures

Nature of adjustments: Comments on the nature of reconciling adjustments and the related disclosures.

Sample comments:

1. We note that your non-GAAP measures exclude purchased intangible amortization, restructuring costs, asset impairments, acquisition-related costs, and income tax items and that you describe these items as infrequent or unusual although you have reported similar items for multiple fiscal years. Please note that Item 10(e)(1)(i)(A) of Regulation S-K prohibits you from adjusting a non-GAAP performance measure to eliminate or smooth items identified as non-recurring, infrequent or unusual, when the nature of the charge or gain is such that it is reasonably likely to recur within two years or there was a similar charge or gain within the prior two years. In addition, your non-GAAP measures appear to exclude certain normal, recurring, cash operating expenses which is inconsistent with the updated Compliance and Disclosure Interpretations issued on May 17, 2016. Please review this guidance when preparing your next earnings release.

2. Given that your ongoing acquisition of businesses is a critical strategy you employ to achieve and maintain growth in your business, please tell us why you remove the impact of acquisition-related expenses and the amortization of intangible assets you acquire, as well as the impact of other fair value adjustments recorded under acquisition accounting in presenting your non-GAAP financial measures.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 56

What’s next?

Non-GAAP measures

More to come?

Other areas of potential

SEC comments

Enforcement Potential

rulemaking

Copyright © 2017 Deloitte Development LLC. All rights reserved. 57

Non-GAAP measures – what to ask?

1. Is the measure misleading or prohibited?

2. Is the measure presented with the most directly comparable GAAP measure and with no greater prominence than the GAAP measure?

3. Is the measure appropriately defined and described, and clearly labeled as non-GAAP?

4. Does the reconciliation between the GAAP and non-GAAP measure clearly label and describe the nature of each adjustment, and is each adjustment appropriate?

6. Is there transparent and company-specific disclosure of the reason(s) why the measure is useful for investors and the purpose for which management uses the measure?

7. Is the measure balanced (i.e., it adjusts not only for nonrecurring expenses but also for nonrecurring gains) and consistently prepared?

8. Does the measure appropriately focus on material adjustments and not include immaterial adjustments that would not seem to be a focus of management?

9. Do the disclosure controls and procedures address non-GAAP measures?

10. Is the audit committee involved in the oversight of the preparation and use of non-GAAP measures?

Non-GAAP measures

Copyright © 2017 Deloitte Development LLC. All rights reserved. 58

Disclosure controls and procedures

Non-GAAP measures

Disclosure Controls and Procedures (DCPs) over non-GAAP

Design DCPS to ensure that procedures cover:

Compliance NGM presented in compliance with rules, regulations and guidance

Consistency Adjustments evaluated and presented in an appropriate and consistent manner each period

Data quality Calculated based on reliable inputs

Accuracy Calculation is arithmetically accurate

Transparent disclosure

Descriptions of adjustments and required disclosures are clear and not confusing

Review Reviewed by the appropriate levels of management

Monitoring Internal audit, disclosure committee or audit committee reviews the controls or is involved in the oversight

Copyright © 2017 Deloitte Development LLC. All rights reserved. 59

Collaboration arrangements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 60

ASC 808 defines collaborative arrangements as a contractual arrangement that involves a joint operating activity. These arrangements involve two (or more) parties that meet both of the following requirements:

1. They are active participants in the activity

2. They are exposed to significant risks and rewards dependent on the commercial success of the activity

ASC 808

Copyright © 2017 Deloitte Development LLC. All rights reserved. 61

Collaborative arrangements

• Is the party to the collaborative arrangement really a “customer”?− Are they participating in an activity or process in which the

participants share in the resulting benefits or risks rather than obtaining the output of the entity’s ordinary activities?

• Activities currently accounted for under ASC 808-10 not likely to be in scope of ASC 606 because ASC 808-10 requires that entities “share in the risks and rewards” (i.e., they are partners, not necessarily customers).

ASC 808

Copyright © 2017 Deloitte Development LLC. All rights reserved. 62

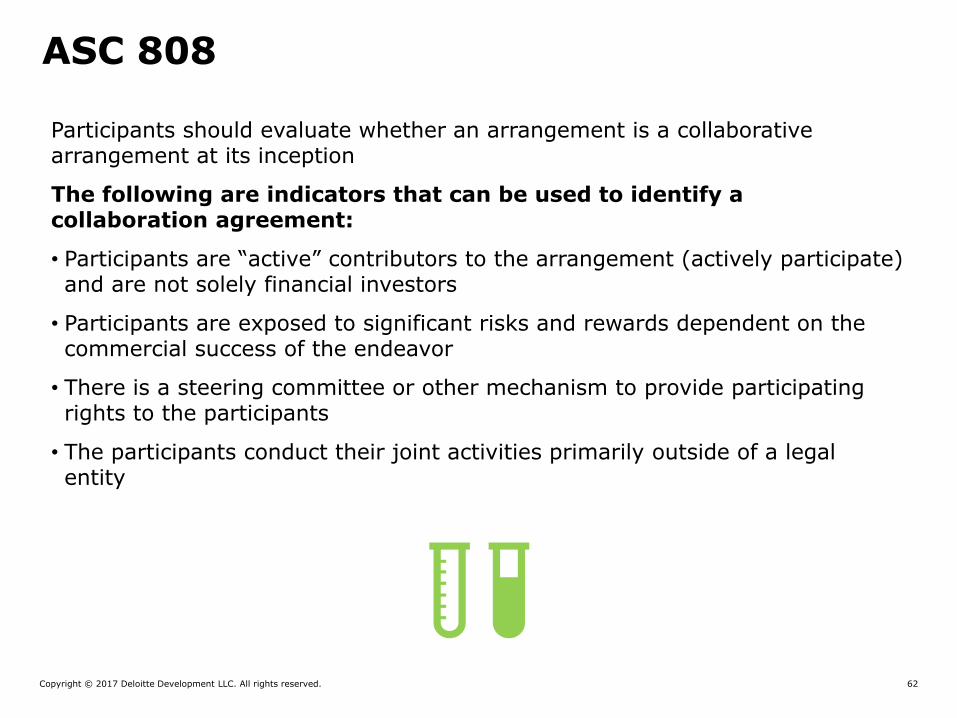

Participants should evaluate whether an arrangement is a collaborative arrangement at its inception

The following are indicators that can be used to identify a collaboration agreement:

• Participants are “active” contributors to the arrangement (actively participate) and are not solely financial investors

• Participants are exposed to significant risks and rewards dependent on the commercial success of the endeavor

• There is a steering committee or other mechanism to provide participating rights to the participants

• The participants conduct their joint activities primarily outside of a legal entity

ASC 808

Copyright © 2017 Deloitte Development LLC. All rights reserved. 63

What it does – ASC 808 provides guidance on the income statement presentation and disclosures related to collaborative arrangements.

What it does not do – Does not address recognition or measurement matters, for example, determining the appropriate units of accounting, the appropriate recognition requirements for a given unit of accounting, or when the recognition criteria are met. Thus, even when a collaboration is within the scope of ASC 808, companies must look to other GAAP (possibly by analogy) to determine the appropriate recognition and measurement for the activities subject to the arrangement.

Looking forward – Collaborative arrangements are specifically scoped out of the newly issued revenue recognition guidance.

ASC 808

Copyright © 2017 Deloitte Development LLC. All rights reserved. 64

Transactions with third parties (parties that do not participate in the arrangement) should be reflected in each entity's respective income statement pursuant to the guidance in ASC 605-45

The principal for a given activity will report revenues and expenses on a gross basis.

Payment between participants are to be classified based upon:

• Nature of the arrangement and business operations

• Contractual terms

• Other income statement classification authoritative accounting literature (apply relevant provisions)

• Analogy to authoritative accounting literature (example – if an arrangement includes reimbursement for R&D costs by entity A to entity B, that portion of the net payment may be classified in entity A’s income statement as R&D expense)

• If no appropriate analogy, use of a reasonable, rational and consistent policy application is allowed

Income statement presentation

Copyright © 2017 Deloitte Development LLC. All rights reserved. 65

Multiple element arrangements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 66

ASU 605-25

• Requires a vendor to evaluate all deliverables in an arrangement to determine whether they represent separate units of accounting.

• Evaluation must be performed at the inception of an arrangement and as each item in the arrangement is delivered.

• No GAAP definition of a “deliverable”

• ASU 2009-13 removed previous separation criterion under EITF Issue 00-21 that objective and reliable evidence of the fair value of any undelivered items must exist for the delivered items to be considered a separate unit of accounting.

• The selling price of deliverables qualifying for separation must be determined using VSOE, third-party evidence of selling price, or by making its best estimate of the selling price.

• The timing and pattern of revenue recognition for a given unit of accounting depends on the nature of the deliverable(s) composing that unit.

Multiple element arrangements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 67

Viewed from the perspective of the customer:

• Distinct action from the vendor?

• Does the exclusion or inclusion of the item cause the arrangement fee to vary by more than an insignificant amount?

• Would failure to deliver result in (1) the customer's receiving a full or partial refund, (2) the vendor's incurring a contractual penalty, or (3) both?

• Are any performance obligations considered ancillary to the "primary" product(s), service(s), or right(s) being sold?

• How essential is an item to the functionality of other products, services, or rights being sold?

• Would the customer consider an item significant or of value separately from other deliverables.

What is a deliverable? (Q&A 605-25-15 #1)

Copyright © 2017 Deloitte Development LLC. All rights reserved. 68

Right of first

refusal provisions

Distribution rights

Steering committee

Development activities

Options to IP

Significant and

incremental discounts

R&D licensing

rights

Supply and manufacturing

Examples of possible deliverables

Copyright © 2017 Deloitte Development LLC. All rights reserved. 69

Deliverables contingent on future events (exercise of option, FDA approval)

May be ignored in initial allocation if:

• Substantive uncertainty about contingency

• Pricing is consistent with the best estimate selling price (BESP)

• Stand alone value of delivered item is not impacted

Contingent deliverables

Copyright © 2017 Deloitte Development LLC. All rights reserved. 70

• Is the undelivered item necessary for the delivered item to have value (i.e., license to IP may not have standalone value without the future R&D)?

• Consider both contractual/legal and practical ability (significant for future manufacturing)

• Does the license provide the customer the ability to have manufacturing performed by others even if intent is for the vendor to manufacturer?

Stand alone value

Copyright © 2017 Deloitte Development LLC. All rights reserved. 71

• Relevant if more than one unit of accounting exist

• Specified prices in contract are generally irrelevant

• Allocation based on relative selling price

• Ignores milestones accounted for under ASC 605-28

Allocation of consideration

Copyright © 2017 Deloitte Development LLC. All rights reserved. 72

Revenue Arrangement – Biotech and Pharma

• Facts

− Biotech licenses exclusive rights to Pharma for Technology A to develop, commercialize and manufacture Drug B, using Technology A for 15 years which is the expected patent life of Drug B, if and when approved.

− Biotech provides R&D services on best-efforts basis devoting four full-time equivalents (FTEs) to R&D activities with ultimate objective of receiving FDA or equivalent approval on Drug B.

− Biotech agrees to manufacture Drug B, if successfully developed, for Pharma for a ten year period.

• Arrangement Consideration

− Biotech receives $5 million upfront

− Biotech receives $2 million upon meeting each of the four substantive milestones

− Biotech receives $250,000 per year for each FTE performing R&D activities

− Biotech receives cost plus 30 percent for manufacturing Drug B.

All payments are nonrefundable, regardless of whether approval is received. Biotech must perform on a best-efforts basis, and is not obligated to achieve the milestones.

Multiple-Element Arrangements – Example

Copyright © 2017 Deloitte Development LLC. All rights reserved. 73

Revenue Arrangement – Biotech and Pharma (cont’d)

• Determine whether the arrangement has multiple deliverables that should be considered for and meet the criteria for separation

− Three deliverables to consider for separation: 1) license, 2) R&D activities, and 3) contract manufacturing

◦ License for Technology A does not have stand-alone value to Pharma without the ensuring R&D activities, which is propriety to Biotech

◦ Pharma could not sell the license to another party without Biotech also agreeing to provide R&D activities

◦ On a combined basis, license and R&D activities may have value as a separate deliverable, giving consideration to:

− Similar arrangements in which Biotech has sold the license and R&D separately from contract manufacturing

− Pharma could sell the combined unit of account to another party

− There are no general rights of return in the arrangement

Multiple-Element Arrangements – Example

Copyright © 2017 Deloitte Development LLC. All rights reserved. 74

SEC comment trends

Copyright © 2017 Deloitte Development LLC. All rights reserved. 75

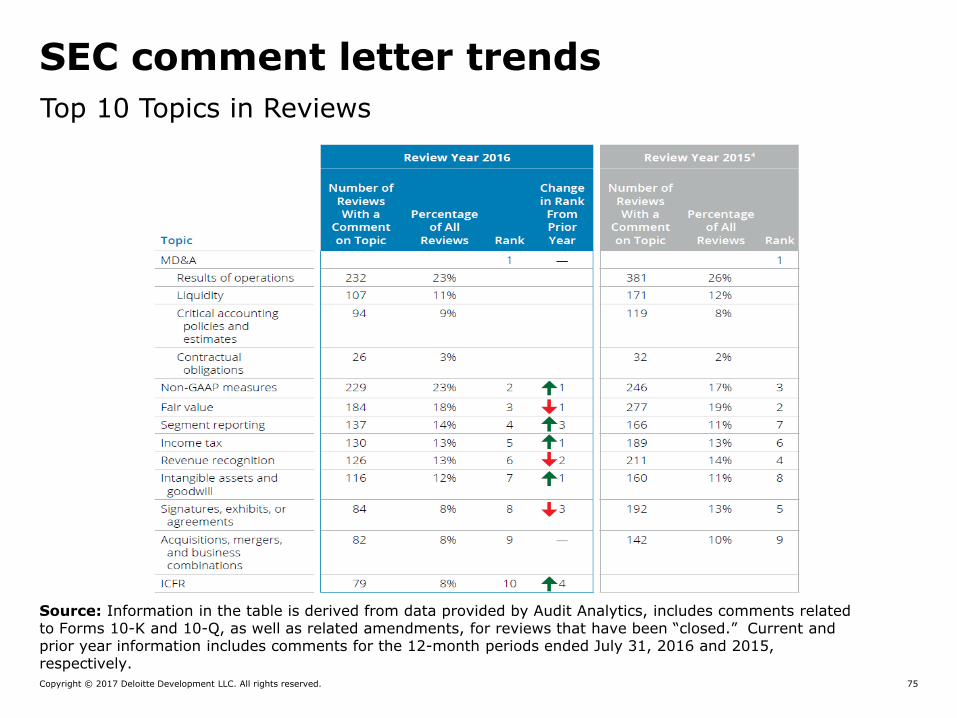

SEC comment letter trends

Top 10 Topics in Reviews

Source: Information in the table is derived from data provided by Audit Analytics, includes comments related to Forms 10-K and 10-Q, as well as related amendments, for reviews that have been “closed.” Current and prior year information includes comments for the 12-month periods ended July 31, 2016 and 2015, respectively.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 76

SEC comment letter trends

Areas of focus

MD&A

• Risks, trends and uncertainties—early warning disclosures

• Results of operations

• Enhanced liquidity and capital resources, critical accounting policy disclosures

• Consistency with other communications

• Focus on clarity (e.g., use of tables and charts)

Metrics

• Clearly define metrics and explain how calculated

• Explain how used by management and why important to investors

• Describe how a metric is related to current or future results of operations

Copyright © 2017 Deloitte Development LLC. All rights reserved. 77

Areas of focus

SEC comment letter trends

Non-GAAP Measures

• Transparency and consistency

• Can’t be used in misleading way

• Recent press and SEC focus

Revenue Recognition

• Disclosures related to revenue recognition policies

• Multiple element arrangements

• Contra-revenue items

• Principal versus agent analysis (gross versus net reporting)

• SAB 74 disclosures (SAB Topic 11M)

Copyright © 2017 Deloitte Development LLC. All rights reserved. 78

Areas of focus

SEC comment letter trends

Segments

• Identification of the Chief Operating Decision Maker (CODM)

• Identification and aggregation of operating segments

• Changes in reportable segments

Fair Value

• Valuation techniques and inputs

• Sensitivity of Level 3 measurements

• Categorization within the fair value hierarchy

Income Taxes

• Repatriation of foreign earnings

• Valuation allowance

• Rate reconciliations

• Unrecognized tax benefits

Copyright © 2017 Deloitte Development LLC. All rights reserved. 79

Business Combinations

• Purchase price allocation

• Contingent consideration

• Required disclosures

• Determining the accounting acquirer

Goodwill and Intangibles Impairment

• Whether or why an interim impairment test was performed

• Specific events that caused the impairment – “why now”

• Early warning disclosures

Areas of focus

SEC comment letter trends

Copyright © 2017 Deloitte Development LLC. All rights reserved. 80

Disclosure effectiveness

What are companies doing?

Source – “What Are Organizations Really Doing About Disclosure Effectiveness”, Leena Roselli, FEI Daily

Copyright © 2017 Deloitte Development LLC. All rights reserved. 81

Cost of good sold and intercompany profit accounting

Copyright © 2017 Deloitte Development LLC. All rights reserved. 82

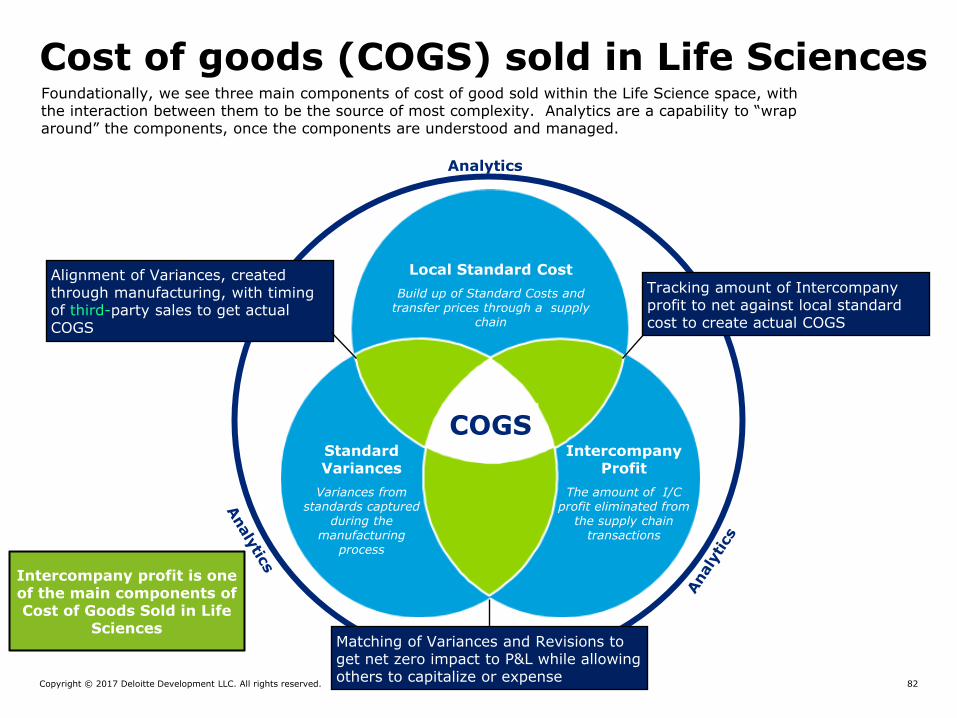

Cost of goods (COGS) sold in Life Sciences

Local Standard Cost

Build up of Standard Costs and transfer prices through a supply

chain

Intercompany Profit

The amount of I/C profit eliminated from

the supply chain transactions

Standard Variances

Variances from standards captured

during the manufacturing

process

Alignment of Variances, created through manufacturing, with timing of third-party sales to get actual COGS

Matching of Variances and Revisions to get net zero impact to P&L while allowing others to capitalize or expense

COGS

Analytics

Tracking amount of Intercompany profit to net against local standard cost to create actual COGS

Intercompany profit is one of the main components of Cost of Goods Sold in Life

Sciences

Foundationally, we see three main components of cost of good sold within the Life Science space, with the interaction between them to be the source of most complexity. Analytics are a capability to “wrap around” the components, once the components are understood and managed.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 83

Regions

Complexities to standard costs and variancesThe complexity of standard costs and resulting variances are complicated. When coupled with expanded footprints, geographic spread, legacy company dissimilarities, and dispirit systems, clarity and transparency becomes a challenge.

Sites

Systems

Portfolio of Business

VariancesCost TypeElements Components

Third-Party Material

Price

Quantity / Usage

Substitution

Scrap

Yield

Labor Rate/Price

Labor Efficiency

Substitution

Absorption / Volume

Spending

Overhead Efficiency

Substitution

Overtime Rate/Qty

Idle Capacity

I/C & Inbound FreightMaterial

Direct Material

Indirect Material

Fixed

Variable

Overhead

Product Cost

Direct Labor

Indirect Labor

Labor

Raw Materials

Auxiliary

Semi-finished

Finished

Packaging

Enabling Functions

Depreciation

Utilities

Setup

Setup

Line Operators

Assembly

Maintenance

Supervisor / Managers

Quality/Testing

Machine Hours

Logistics

Outbound Freight

Warehousing

Distribution

Insurance

I/C Purchase Price

Revaluation

Engineers

Rent

Royalties

Duty/Import

Lot Size

There are additional complexities and challenges related to Intercompany Profit

Copyright © 2017 Deloitte Development LLC. All rights reserved. 84

Intercompany Profit

Process

Commonalities

Dedicated center of excellence for intercompany

profit elimination

Large number of legal entities with a mix of

manufacturing / marketing and hub entities

Accuracy driven by SKU level processes.

Supply chain strategy change contributes

to additional complexity

Significant number of intercompany sales within

financial flow, driven by tax strategies

Multiple lines of business that have

multiple profit and risk profiles

Disparate ERP systems across supply chain

makes tracking flows very difficult

Lack of packaged / vendor-based

solutions available for this process

Intercompany Profit Process Commonalities

These commonalities often lead to similar challenges throughout the industry when managing Intercompany Profit

Intercompany profit process commonalitiesIndustry-wide, several commonalities exist within the Intercompany Profit (ICP) in Inventory Process.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 85

Challenge with intercompany profitA common challenge is that the financial solution creates ‘noise’ for commercial P&L’s when ICP is released. Differing the treatment of ICP in financial and management P&L’s allows for the reduction in ‘noise’ on release.

ICP Category On Elimination Financial P&L Release Management P&L Release

Markup at

standard

Eliminated to the balance sheet at standard at time of intercompany sale

Released to the financial P&L at time of final sale at standard

Implicitly included in the management P&L as part of the latest standard

Production

variances

Eliminated to the balance sheet at standard based on information provided by manufacturing sites

Released to the P&L based on established treatment

Not included as part of management P&L but as a KPI

Price Variance Calculated at time of intercompany sale based on standard markup versus actual at standard rate

Released to the P&L based on established treatment

Not included as part of management P&L but as a KPI

FX Variances Calculated at time of intercompany sale based on standard rate versus actual rate

Released to the P&L based on established treatment

Not included as part of management P&L but as a KPI

Revaluations Calculated based on current inventory at the time of revaluation

Implicitly included in standard release at final sale

Implicitly included in the management P&L as part of the latest standard

Despite the complexities and challenges, focusing on the differences in treatment of intercompany profit, and increasing stakeholder involvement can

create opportunities for additional value

Copyright © 2017 Deloitte Development LLC. All rights reserved. 86

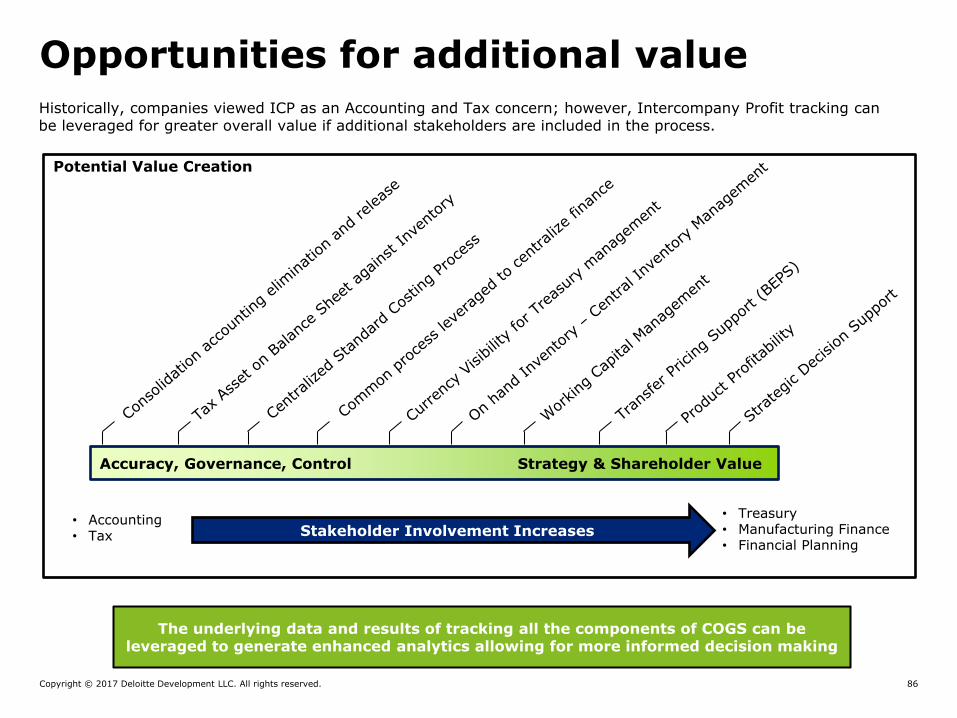

Opportunities for additional value

Historically, companies viewed ICP as an Accounting and Tax concern; however, Intercompany Profit tracking can be leveraged for greater overall value if additional stakeholders are included in the process.

• Accounting• Tax

• Treasury• Manufacturing Finance• Financial Planning

Accuracy, Governance, Control Strategy & Shareholder Value

Potential Value Creation

Stakeholder Involvement Increases

The underlying data and results of tracking all the components of COGS can be leveraged to generate enhanced analytics allowing for more informed decision making

Copyright © 2017 Deloitte Development LLC. All rights reserved. 87

Conclusion - Key takeaways

The landscape of COGS, ICP, Inventory and Analytics is complex, but our learnings would suggest:

COGS processes are interrelated and interdependent, you need to solve as a

system, not as a node

COGS reporting is about predictability and transparency

“Boiling the Ocean” is a failed technique. Create a set of achievable

capabilities and sequence them to get to your end state

Analytical insights begin with Data that can be trusted

Tax, Treasury, Controllers, Manufacturing / Supply Chain, Commercial are all

stakeholders in this process; make sure solution needs are met

1

2

3

4

5

Copyright © 2017 Deloitte Development LLC. All rights reserved. 88

New lease standard

Copyright © 2017 Deloitte Development LLC. All rights reserved. 89

Key Impacts of Lease Standards

The “Big Picture”

Most leases on balance sheet for lessees

Classification will drive expense profile

Lessor model largely unchanged

Most changes result from alignment with ASC 606

FASB tried to make things easier

Classification, reassessment, transition

Effective 2019 and transition impact

Process and systems changes may be required

Potential impact on debt covenants

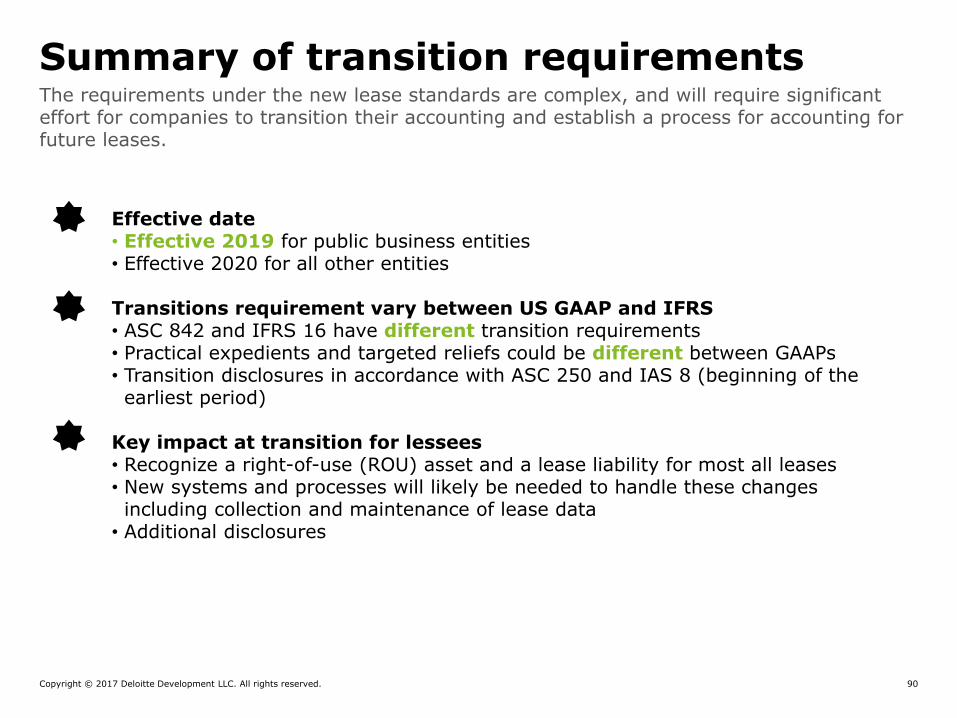

Copyright © 2017 Deloitte Development LLC. All rights reserved. 90

Effective date• Effective 2019 for public business entities • Effective 2020 for all other entities

Transitions requirement vary between US GAAP and IFRS• ASC 842 and IFRS 16 have different transition requirements• Practical expedients and targeted reliefs could be different between GAAPs• Transition disclosures in accordance with ASC 250 and IAS 8 (beginning of the earliest period)

Key impact at transition for lessees• Recognize a right-of-use (ROU) asset and a lease liability for most all leases• New systems and processes will likely be needed to handle these changes including collection and maintenance of lease data

• Additional disclosures

Summary of transition requirementsThe requirements under the new lease standards are complex, and will require significant effort for companies to transition their accounting and establish a process for accounting for future leases.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 91

Financial statement

presentation

Relief package

(adopt all or none)

ApproachLessees and lessors are required to use a modified retrospective

transition method for all existing leases

Present comparative periods under ASC 842 (accordance with ASC 250)

Elect as package to not reassess the following:

Whether any expired or existing contracts are leases or contain leases

Lease classification for any expired or existing leases

Initial direct costs for any existing leases

ASC 842: Transition accounting

Use of hindsight(may be electedseparately or in conjunction with relief package)

Use hindsight in evaluation of the following:

Lease term (e.g. renewal, termination, and purchase options)

Impairment of right-of-use asset

The election packs does not relieve an entity from its obligation to address any errors that may have resulted from the misapplication of past accounting (e.g. classification of lease, accounting a

contract as a service rather than a lease contract)

Copyright © 2017 Deloitte Development LLC. All rights reserved. 92

ROU asset

Lease liability

Lease expense (single line on straight-line

basis)

Lease payments

(Operating)

ROU asset

Lease liability

Amortization expense

Interest expense

Principal (Financing)

Interest (Operating)

Balance Sheet Income Statement Cash Flow Statement

Financing

Lease

Operating

Lease

Lessee model

Presentation consistent with current lessor model:• Balance sheet — presentation depends on lease classification

• Income statement — profit or loss recognized in a manner consistent with

business model

• Cash flow statement — recognized as cash inflows from operating activities

Lessor model

Presentation requirements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 93

Finance lease Operating lease

This table highlights the differences in accounting for the lease under the finance lease and operating lease models:

Lessee accounting modelIllustrative example

Copyright © 2017 Deloitte Development LLC. All rights reserved. 94

Similarities and differences in ASC 842 andIFRS 16: The lessee accounting model

Similarities and Differences ASC 842 IFRS 16

Classification on recognition

Leases on balance sheet Similar Similar

Lease approaches: Lease classification and amortization of ROU asset

Two approaches:• Finance lease• Operating leaseThe classification test is based on the FASB/IASB model.

Single approach model (similar to FASB’s finance lease)

Initial measurement

Lease obligation: Present value of lease payments not yet paid

Similar Similar

ROU asset: Lease Obligation + Initial Direct Costs – Lease Incentives + Prepaid (accrued) Lease Payments

Similar Similar

Subsequent measurement

Lease obligation: Amortized using the effective interest method

Similar Similar

ROU asset: Amortization of lease assets and expense pattern

• Finance lease declinesusing the straight-lineamortization

• Operating lease declines by balancing the amount

Similar to Finance lease, declines using straight-line amortization