Embed Size (px)

Citation preview

Causality between Prices and Wages: VECM Analysis for EU-12(*)

Adriatik HOXHA

University of Prishtina [email protected]

Abstract. The literature on causality as well as the empirical

evidence clearly shows that there are two opposing groups of economists, who support different hypotheses with respect to the flow of causality in the price-wage causal relationship. The first group argues that causality runs from wages to price, whereas the second argue that effect flows from prices to wages. Nonetheless, there is at least some consensus that researchers conclusions may be contingent on the type of data employed, applied econometric model, or even that the relationship may vary through economic cycles. This paper empirically examines the price-wage causal relationship in EMU, by using OLS and VECM analysis, and also it provides robust evidence in support of a bilateral causal relationship between prices and wages, both in long-run as well as in the short-run. Prior to designing and estimating the econometric model we have performed stationarity tests for the employed price, wage and productivity variables. Additionally, we have also specified the model taking into account the lag order as well as the rank of co-integration for the co-integrated variables. Furthermore, we have also applied respective restrictions on the parameters of the estimated VECM and finally model robustness checks indicate that results are statistically robust. Although far from closing the issue of causality between prices and variables, this paper at least provides some fresh evidence for the case of EMU.

Keywords: causality; co-integration; granger; determinants of

inflation; VECM. JEL Codes: C39, E31. REL Codes: 3D, 20F.

* This paper was extracted from the doctoral dissertation titled “An empirical review of the price-wage causal relationship in EU-12, EU-27, Germany and United Kingdom”, completed in October 2009.

Theoretical and Applied Economics Volume XVII (2010), No. 5(546), pp. 27-48

Adriatik Hoxha

28

1. Introduction The issue of causality between prices and wages has been intensively

discussed in the literature. However, despite utmost empirical efforts to resolve the issue on which the cause is and which the effect is, the consensus is still far from being reached. Arguably, there have been two strands of economists. Whilst the first one arguing that causality runs from wages to prices, whereas the second one argues that causality runs from prices to wages. The modern analysis of philosophical discussion of causality began in the 18th century with Hume (1739). He made the scientific hunt for causes possible, by freeing the concept of causality from the metaphysical chains that his predecessors had used to pin it down. Since Hume, the applicability of causality concept has been ever increasingly used in social sciences as well as in the field of economics. In addition to this, the analysis has been sophisticated by intensive use of mathematical and econometrical techniques, which have immeasurably increased the quality of economic analysis. Moreover, computing power and speed has tremendously increased also.

Nonetheless, all these significant advancements have not helped in completely resolving the issue of causality between the prices and wages. The evidence from literature is conflicting and there is evidence in favor of both hypotheses. The aim of this paper is to analyze and derive the pattern of causality for EU-12 (twelve member states of European Monetary Union). This paper is organized as follows. Section 2 reviews the literature on causality, in general, as well as that on causality between prices and wages, in particular. Section 3 explains the methodology that has been utilized to examine the causal relationship. Section 4 described the variables as well as the data that have been employed in our analysis. Section 5, is organized in two sub-sections and presents Ordinary Least Squares (OLS) and Vector Error Correction Model (VECM) regression results, from which the pattern of causality has been derived. Finally, Section 6 concludes by summarizing the main findings of this paper.

2. Literature review The purpose of literature review is to lay down some theoretical

definitions, characteristics and arguments on causality, in general, and on the price-wage causal relationship, in particular. This summary of previous studies would not only be useful to derive some theoretical definitions of causality and critically assess them, but will also be the basis for the empirical analysis, which will be mainly focused on causality between wages and prices. First part reviews the causality literature from the theoretical perspective, whereas the

Causality between Prices and Wages: VECM Analysis for EU-12

29

second part focuses on empirical studies that have specifically examined the causality between prices, wages and productivity. Causality is a relevant concept, both in natural and social sciences. As we have already emphasized, the modern analysis of philosophical discussion of causality began in the 18th century with Hume (1739). In his view, causality, as it is in the world, is a regular succession of event-types: one thing invariably following another(1).

However, it was the 20th century, and especially its last decades, that saw its gained prominence. Undoubtedly, Havlemo (1994) was one of the first to contribute in advancing causality analysis. His view, which is almost universally acknowledged, is that economic theory must be always formulated in stochastic terms. Certainly, one of the most prominent modern studies on causality analysis in economics was conducted by Granger in his seminal paper “Investigating Causal Relations by Econometric Models and Cross Spectral Methods” in 1969. An important follow-up analysis of causality was carried out by Ashley et al. 1980, who analyzed the causality between advertising and aggregate consumption. They argue that a universally acceptable definition of causality may well not be possible, but they put forward the following definition:

“Let Ωn represent all the information available in the universe at time n.

Suppose that at time n optimum forecasts are made of Xn+1 using all the information in Ωn and also using all of this information apart from the present values of Yn-j, j ≥ 0 of the series Yt. If the first forecast, using all the information, is superior to the second, then the series Yt has some special information about Xt not available elsewhere, and Yt is said to cause Xt”

It is well understood in economics that the existence of a relationship

between two variables does not prove causality or the direction of influence. However, in the context of time series data, it may be possible to exploit the fact that time does not run backwards (so called “time arrow”). This relies on the assertion that the future cannot cause the past, and it is an a priori and fundamental feature of the way in which one orders its experience and not either an observed regularity or an analytic truth (Gilbert, 2004). Table 1 provides a short summary of some studies that have examined in depth the causality analysis. Certainly, these studies can relatively encompass the developments in recent years.

Adriatik Hoxha

30

Table 1 A summary of some studies on causality presented in chronological order

Studies Title Context/Method Asshley, Granger and Schmalensee (1980)

Advertising and Aggregate Consumption Granger causality; Box-Jenkins technique

Sims (1999) Granger Causality Definitions; causality and exogeneity. Jung and Seldon (1995)

The Macroeconomic relation between Advertising and consumption Granger causality, Error Correction Model;

Gilbert (2004) Economic Causality Economic causation, intervention and exogeneity; VAR modeling practice; implications on inference.

LeRoy (2004) Causality in Economics Formal analysis of causal relations; graphical analysis; definitions on causality.

Andersson (2005) Testing for Granger Causality in the presence of measurement errors

Problems of Granger-tests; consequences on forecastability.

Empirical facts on the price, wage and productivity relationship The debate on the direction of causality between wages and prices is one

of the central questions surrounding the literature on the determinants of inflation. The purpose of this review is to identify the key theories, concepts or ideas explaining the causality issue between prices and wages. Besides, it seems sensible to assess what has been addressed so far on the relevant questions and problems related to the analysis of the relationship between prices and wages. There have been a number of studies that have analyzed price-wage relationship, and most of them have employed US data. Table 2 presents a summary of relevant studies on this relationship.

Table 2 Asummary of some studies on the price, wage and productivity relationship

presented in a chronological order Studies Title Context/Method

Moschos (1983) Aggregate price responses to wages and productivity changes: Evidence from US

Error Correction Model (ECM); Instrumental Variable (IV);

Emery and Chang (1996) Do wages help predict inflation? Granger causality

ECM (Error Correction Model)

Palley (1999) The US inflation process: Does nominal wage inflation cause price inflation, vice-versa, or neither Granger causality;

Hess and Schweitzer (2000) Does wage inflation cause price inflation Granger causality;

ECM (Error Correction Model) Garcia and Restrepo (2001) Price and wage inflation in Chile ECM (Error Correction Model)

Jonsson and Palmqvist (2004) Do higher wages cause inflation? Two Sector Dynamic General

Equilibrium (DGE) Model Strauss and Wohar (2004)

The linkage between, prices wages and producti-vity: a panel study of manufacturing industries

Granger causality; Panel Model;

Lemos (2004) The effect of minimum wage on prices Review of empirical research Pu, Flaschel and Chihying (2006) A causal analysis of the wage-price spiral Granger causality

VAR (Vector Autoregressive) Model

Goretti (2008) Wage-price setting in new EU Member States ECM (Error Correction Model); and Panel Model;

Causality between Prices and Wages: VECM Analysis for EU-12

31

The available studies focusing on price-wage causality use various methodologies and can be broadly divided into two categories. The first strand of studies focuses on estimation of the effect of wages on prices using data from various economic sectors, while the second strand estimates the effect of wages on inflation by using the aggregate (national) level data. Alternatively, empirical studies on the price wage causality can be divided into two categories with regard to the direction of effect. The first category of studies arguing that causation runs from wages to prices, while the second one studies arguing that causation runs from prices to wages. Given the prominent evidence, the latter categorization is more suitable, thus, it will be adopted in order to provide a concise account of empirical studies on the price-wage causal relation. In what follows, I will, first, review and critically assess evidence and arguments in support of hypothesis that causal chain runs from wages to prices, and secondly, I will present arguments and empirical evidence in favor of hypothesis that prices cause wages.

A common feature of most of these studies is that many researchers have applied the Granger-causality concept described above which, as we have already emphasized, is easily applicable in economics. Regarding the econometrical models applied in examining the long-run relationship between prices and wages, the Error Correction Models (ECM) appear to dominate the alternative econometric methods. While it is commonly acknowledged in the academic literature that prices and wages move strongly together, Hess and Schweitzer (2000) argue that there is a sharp division amongst economists on whether wages cause prices or vice-versa. In order to explain such a causal relation economists very often use the “Granger-causality” by examining whether lagged values of one series (say wages) have significant in-sample explanatory power for another variable (say prices). Additionally, both variables may Granger-cause one another, in which case one can conclude only that both economic series are determined simultaneously. If this is the case, the researcher may be unable to infer that one series has independent causal effect on the other.

The matters may become more puzzling if the series in question are co-integrated, which is the case when the levels of the series move together over the long-run, even though the individual series are best modeled in growth terms. In that case, the researcher must be careful to include the “error correction terms” in Granger-causality tests to allow the series to catch up with one another. The significance of the ECM terms in the Granger-causality tests simply reflects the fact that the series in question are driven to return to a long-run equilibrium relationship that it is non-causal. In addition to this, the researchers conclusions on the causal relationship often depend on the sample length, the number of explanatory variables used (including the number of lags

Adriatik Hoxha

32

of each variable) and in particular the measure of prices used(2) (Hess, Schweitzer, 2000).

Importantly, Emery and Chang (1996) empirically highlight the fact that the significance of Granger causal relation depends on the choice of price series, and it is relevant to any researcher to avoid data mining in designing models. It is appropriate to remind on Palley (1999) argument that the relation also varies by business cycles, i.e. causality order between prices and wages may alter over time. A fundamental reason why there has been a lack of evidence in favor of hypothesis that wages cause prices may well be the fact that, as Lemos (2004) acknowledges, the international literature has mainly utilized the data from the US where price effects are small. The selection of different variables may also play a significant role on the strength of results as well. For example, money supply indicators are often found to contain essential information for forecasting future behavior of prices, and that needs to be considered as it may ultimately improve the robustness of the model. Above all, when analyzing the causality relation between wages and prices, it is relevant to control for labor productivity (i.e. supply effects).

3. Methodology Without a doubt the crux of the matter in empirical research is to design a

model which truly represents a certain DGP or economic phenomena. The presence of a bilateral causal relationship between two or more variables not only complicates, but certainly it makes more complex and challenging the process of model building. Although OLS regressions may produce highly significant parameters, it is the regression diagnostics, in particular the presence of autocorrelation that raises serious doubts on the robustness of simple OLS models. Often, it is this limitation in remedying autocorrelation that necessitates the use of more sophisticated models that are able to analyze more thoroughly complex relationships, such as that between prices and wages. Certainly, the VECM models are frequently applied in examining models with more than one endogenous variable. As Isaac Asimov(3) has pointed out, “though science can cause problems, it is not by ignorance that we will solve them.” Hence, the aim of this paper is to analyze the price-wage relationship with different methods using the same data, in order to check whether the causal relationship between prices and wages holds robustly.

Causality between Prices and Wages: VECM Analysis for EU-12

33

Theoretical relationship between prices, wages and productivity This relation has been expressed in various forms, i.e. different causal

ordering. First, the wage can be expressed as a function of price and productivity. Second, the price can be expressed as a function of wage and productivity. Thirdly, real wage (wages/prices) can be expressed as a function of productivity. The relations that are subject matter of this dissertation and which will be analyzed in this chapter are only the first two causal orderings. Besides, there are numerous studies that have explicitly studied price wage causal relationship (see for example Moschos, 1983, Emery, Chang, 1996, Palley, 1999, Hess, Schweitzer, 2000, DeGrauwe, 2003, Strauss, Wohar, 2004). Other variables may also be considered and included in the model. Nevertheless, increasing the number of variables and equations does not necessarily lead to a better model because by including greater number of variables it becomes more difficult to capture the dynamic and inter-temporal relations between relevant variables due to loss of power. As a matter of fact, in some forecast comparisons univariate time series models were found to perform better than the large scale econometric models. Lütkhepohl and Krätzig (2004) suggest that a possible reason for the failure of larger models is their insufficient representation of the dynamic interactions in a system of variables.

Applied econometric methods – in analyzing the causal relationship we will utilize two methods. First, we will use basic OLS regressions model, with the purpose of examining the relationship. Second, we shall apply the VECM in order to derive statistically robust estimates. Prior to estimation of the latter models one should also examine the respective model selection criteria for deter-mining the lag order/lagged differences as well as the rank of co-integration. Due to the space limitations there will only be a brief presentation of respective steps.

4. Data For empirical analysis of the price-wage causal relationship in EU-12

countries we will employ quarterly data covering period 1996:Q1-2007:Q4. Unfortunately, due to the unexpected events of global recession and its consequences, the author has been forced to exclude the data for 2008-2009, which in econometric terms represents a significant structural break. Thus inclusion of the data for that period may significantly raise questions on the applicability of VECM. The following variables have been selected for empirical analysis: Price (P) variable is represented by the Harmonized Index of Consumer Prices (HICP), Monthly data, 2005=100. The quarterly data were obtained by taking three month average of monthly data. Hereinafter, price variable for EU-12 will be denoted by PEU 12; Wage (W) variable is

Adriatik Hoxha

34

represented by the Labor Cost Index (LCI) quarterly data, i.e. wages and salaries in industry and services (excluding public administration), nominal value, seasonally adjusted and adjusted data by working days, Index 2000=100. Hereinafter, wage variable for EU-12 will be denoted by WEU12; Productivity (Q) variable is represented by the quarterly index representing person based labor productivity for total economy at constant prices (fixed composition), seasonally adjusted, not working day adjusted, total, ECU/euro, index. Hereinafter, productivity variable for EU-12 will be denoted by QEU12. The source of data for all three variables is EUROSTAT (www.ec.europa.eu/eurostat).

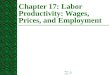

Additionally, in this section we have thoroughly analyzed the stationary properties of the time series data. The plots for both level series of all three variables suggest a trending movement and little evidence of returning to a fixed mean value. Furthermore the plots are inconsistent with the series containing stochastic trends. In contrast, the plots for the differenced series suggest evidence of mean reversion and some evidence that the series may be stationary (Appendix C.1). Additionally the correlograms for the level series of all three variables appear to have a long memory and the decay rate appears slow with persistence up to the 12th lag. This tentatively suggests that both series could be characterized by a stochastic trend where shocks persist. In an opposite manner, the correlograms for the differenced series tend to decay much more rapidly. This could be taken to suggest that shocks do not persist (Appendix C.1). As Table C.2 shows, the formal stationarity tests, the Augmented Dickey Fuller (ADF) and Phillips-Perron tests, in all cases the null hypothesis that the series in levels contain a unit root cannot be rejected by the data. In contrast, the null hypothesis that the differenced series contain a unit root is rejected in all cases for both series. This implies that all series require differencing just once to render them stationary. Therefore, all levels series contain a unit root and appear to be characterized by the presence of a stochastic trend (Appendix C.3).

5. Results In the first sub-section we will examine the OLS results, whereas in the

second sub-section we will analyze the VECM model. All the tests and results are presented in Appendix E.

5.1. OLS estimates The OLS regressions were subjected to autocorrelation tests, on the basis

which it is evident that the inability of simple OLS models to remedy the

Causality between Prices and Wages: VECM Analysis for EU-12

35

problem of autocorrelation, in particular, necessitates the utilization of more sophisticated models, in order to produce statistically robust models as well as estimates. Certainly, this may well be a result that the lagged variables of respective series were not included in the model. Furthermore, the simple OLS regressions models are incapable of capturing the co-integration relationships that may exists between two or more variables. However, OLS models are a good start for any empirical analysis, as it gives us first insights when testing different relationships. In our initial OLS empirical analysis, we have also compared the models with intercept, and without intercept. On the basis of the Ramsey’s RESET test it appears that intercept is not present at all in the price-wage relationship, hence its exclusion would produce a better model. Complete OLS results are presented in Table 3.

Table 3 OLS Regression results for EU-12 using level, log-level, first differences and first

differences of the log-level

Variables Prices = F (Wages, Productivity) (a) Wages = F (Prices, Productivity)

(b) (1) (2) (3) (4) (5) (6) (7) (8)

ln w ***0.61 ***0.55 ln p ***1.27 ***1.76 ln q 0.21 ***0.43 ln q *0.46 ***-0.72

const 0.70 n/a const ***-3.25 n/a

AC Test ***0.00 ***0.00

AC Test ***0.00 ***0.00 Ramsey

Test ***0.00 Ramsey Test ***0.00

Δln w 0.29 ***0.68 Δln p 0.05 ***0.74 Δln q -0.05 0.02 Δln q -0.07 ***0.57 const 0.00 n/a const ***0.00 n/a

log

AC test ***0.00 ***0.00

AC test ***0.00 0.10 Ramsey

Test ***0.00 Ramsey Test ***0.00

Note 1: *** – significant at 1% level of significance; ** – significant at 5% level of significance; * – significant at 10% level of significance. The AC tests indicate the p-value of the Breusch-

Godfrey LM test for autocorrelation with HD: no serial correlation and Ha: HD is not true. The OLS regression in columns (3) and (7) can be expressed as: Dttt LQLWLP βββ ++= 21 ; where βD is intercept, β1 is the slope coefficient which measures the elasticity of prices on wages, and β2 is slope coefficient which measures the elasticity of prices on productivity. In contrast, when intercept is excluded, columns (4) to (8) the OLS regression may be expressed as follows: ttt LQLWLP 21 ββ += ; where parameters β1 and β2 are interpreted in the same way as above. In the case of first differences only the letter D is added in front of variables, whereas the formulas are identical.

Note 2: Ramsey RESET Tests check whether the model without intercept better represents the DGP between prices and wages, compared to the model with intercept (Maddala, 1999, Gujarati, 2002, Wooldridge, 2003).

Adriatik Hoxha

36

For example the results are interpreted as follows: the coefficient of wages in column (3) is statistically significant at 1 percent level and it indicates a positive impact of wages on prices measuring 0.61 percent, i.e. if wages increase by one percent, on average and ceteris paribus, the prices will increase by 0.61 percent. Otherwise, this coefficient measures the elasticity of prices on wages. In contrast, the coefficient of productivity is not statistically different from zero. Unfortunately, according to the Breusch-Godfrey test, it appears that one may firmly reject the null hypothesis of no serial correlation, with test statistic being high and p value zero. On the basis of Ramsey’s RESET test one may exclude the intercept from model, as it results in a better representation of DGP, in both cases when log-levels and first differences of the respective time series data are utilized. Finally, it can be argued that on the basis of estimated coefficients there appears to be a bilateral causal relationship running from wages to prices and vice-versa. Additionally, Table 4 presents the pattern of causality for the EU-12. Based on the evidence there appears to be a bilateral causal relationship between prices and wages for both log-level and differenced series, significant at 5 percent level, though only when intercept is excluded.

Table 4

The pattern of causality in EU-12 based on OLS model Country Log-Levels First differences

(1) (2) (3) (4) intercept EU-12

no intercept

Note: indicates bilateral (feedback) causality; or indicates unilateral causality; no causality.

* indicates that relationship is significant at 10 percent level. Finally, one may ask whether we can draw a firm conclusion from the

causality tests that are presented in Table 3. Without a doubt, one has to concede that the presence of autocorrelation harms the reliability of the OLS estimates, if not destroys them. However, the purpose of OLS analysis was to test the existence of the price-wage relationship, as well as the uniqueness of causal orderings, and to get some useful insight, even if no conclusive evidence emerges from these analyses. Certainly, one has to concede that there is solid evidence in support of a strong causal relationship, and that the causal ordering in this relationship is not unique. Even so, let’s leave to VECM analysis to deliver the final verdict on this issue.

Causality between Prices and Wages: VECM Analysis for EU-12

37

5.2. VECM estimates On the basis of information criteria, the optimal number of lagged

differences for endogenous variables is (p – 1) = 3. Whereas the information criterion Akaike Information Criterion (AIC) tends to overestimate the optimal lag order, whilst Hannan-Quinn information criterion (HQ) provides the most consistent estimates, thus it will be considered as the most reliable criterion. By analyzing the lag order for exogenous variables and statistical significance of coefficients, the optimal lag order for exogenous variable is q = 1. Notice that owing to the three lagged differences and additional observation lost when the first differences of the variables were taken, only data from 1997:Q1–2007:Q4 are actually used as sample values, thus the actual sample size is T= 44. Notably, choosing the order too small can lead to size distortions for the tests. Conversely, selecting an order which is too large may imply the reduction in the power of tests. It is exactly this fact that makes so critical the issue of choice of the number of lagged differences (Appendix E.1).

Rank of co-integration (rk(Π)) – the co-integration were performed between LPEU12 and LWEU12. The reskts of all tests are summarized in Table 5. On the basis of Johansen Trace Test one would proceed analysis with a model containing one co-integration relation, since in all cases the test statistic is significant at 1 percent level, hence, clearly indicating that there is sufficient evidence to reject the null hypothesis that rk(Π) = 0, in favor of alternative hypothesis that rk(Π) = 1. Similarly, the Saikkonen and Lütkhepohl (1997) test suggests that one clearly finds the rank of one being appropriate, as in all cases the test statistic is significant at 5 percent level. Hence, there is sufficient evidence to proceed the analysis with one co-integration relation, i.e. use r = 1, in the VECM model.

Table 5

Specification of the co-integration rank by co-integration tests

Johansen Trace Test Saikkonen and Lütkhepohl Variables Deterministic terms Lag order LR-stat p-value Lag order LR-stat p-value

Const 4 25.20 0.0082 4 21.50 0.0009 Const and Trend 8 54.60 0.0000 8 17.13 0.0292

and

Orthogonal trend 8 21.44 0.0048 8 11.44 0.0249

Adriatik Hoxha

38

Estimation – The VECM model was estimated using the Two Stage procedure (S2S), with Johansen procedure being used in the first stage and Feasible Generalized Least Squares (FGLS) procedure being used in the second stage. The estimated results are presented in Appendix E, with the JMulTi software generating the output of all the related loading matrix, co-integration matrix and short-run parameters. The standard t ratios and F tests retain their usual asymptotic properties if they are applied to short-run parameters in VECM. Hence, when appropriate, it is a good idea to impose restrictions on the VECM parameters. As a replacement for the statistical testing procedures, restrictions for individual parameters or groups of parameters in VECM may also be based on the model selection criteria. In the view of this, as proposed by Brügeman and Lütkhepohl (2001) and Lütkhepohl and Krätzig (2004) the Sequential Elimination of Regressors (SER) has been utilized in order to delete those regressors that lead to the largest reduction of the model selection criteria (in this case HQ criterion), until no further reduction is possible (Lütkhepohl, Krätzig, 2004, Lütkhepohl, Krätzig, 2005). All the coefficients with t ratios lower than two have been eliminated or restricted to zero.

Loading coefficients – even though they may be considered as arbitrary to

some extent due to the fact that they are determined by normalization of co-integrating vectors, their t ratios may be interpreted in the usual way as being conditional on the estimated co-integration coefficients (Lütkhepohl, Krätzig, 2004, Lütkhepohl, Krätzig, 2005). In this case the loading coefficient of the first equation has a t ratio of 5.08, which is significant at 1 percent level, whereas the loading coefficient for second equation has a t ratio of 2.695 and is also significant at 1 percent level. Thus, based on the presented evidence, it can be argued that co-integration relation resulting from the normalization of the co-integrating vector enters significantly in both equations.

Co-integration vectors – by selecting LPEU12t as the first variable in the

model, it means that the coefficient of this variable in the cointegration relation will be normalized to 1 in the maximum likelihood estimation procedure. This normalization is tricky if LPEU12t is not actually present in the co-integration relation here, and hence, it has a coefficient equal to zero. Nevertheless, taking into account the t test it looks that there is sufficient evidence to suggest that LPEU12t is strongly cointegrated with LWEU12t. It may be stressed that the coefficient of the trend term in co-integration relation has an asymptotic normal distribution under standard assumptions, and thus its t ratio can be interpreted in the usual way. Evidently, it appears that its coefficient is significantly different

Causality between Prices and Wages: VECM Analysis for EU-12

39

from zero at all conventional levels with t state being 11.86. The estimation was also performed with trend variable not being restricted in the co-integration relation. However, in that case the loading coefficients proved to be statistically insignificant. Hence, the decision was taken to restrict the trend term in the co-integration relation. Consequently the model takes the form,

)86.11()27.240(004.012984.012 ttt

EGLSt LWEULPEUec

−+−= (1)

where the numbers in parenthesis represent t ratios. When (1) is arranged, the new expression takes the form,

EGLStttt ecLWEULPEU ++=

− )86.11()27.240(004.012984.012 (2)

considering that the logs of variables have been used, the relation in (2) expresses the elasticity of prices on wages, hence the coefficient of 0.984 is the estimated price elasticity. If the log wages increase by 1%, it is expected that the log of prices would increase by 0.98 percent. In other words, a 1 percent increase in the log wages would induce a 0.984 percent increase in the log of prices. In addition to this the value of standard deviation is very low, indicating a high efficiency of the estimated parameter.

Short-run parameters – The estimators of parameters associated with

lagged differences of variables may be interpreted in the usual way. All coefficients with values that are not different from zero have been eliminated. The t ratios are asymptotically normal under these assumptions. In contrast, this may not be true for parameters associated with deterministic terms, which t ratios are just given for completeness (Lütkhepohl, Krätzig, 2004). Four out of six seasonal dummies have significant coefficients, however their coefficient values are very small and do not indicate a large impact.

Adriatik Hoxha

40

Table 6 VECM Diagnostic Tests

Type of Test p-value VECM VECM Model statistic 0.84 √ LM Autocorrelation Test 0.34 √ Non-normality test Dornik and Hansen (1994) 0.72 √ Lütkepohl (1993) 0.78 √ ARCH-LM u1 0.79 √ u1 0.31 √ Plots of Residuals n/a √ ACF and PAC n/a √ Cross-correlations n/a √

Note: √ – test indicates no problems with diagnostic criteria; x – indicates that there is

some problems with the diagnostic criteria. Testing the model robustness checks – most of them rely on the residuals

of final VECM, with some applying to the residuals of individual equations and others are based on the full residual vectors. Graphical tools may also shed light on potential defects of the model and, thus, provide a useful insight on the robustness of the model. The VECM model statistic indicates that one may not reject the null hypothesis that restricted model has a better representation of DGP, compared to unrestricted model. The p value is 0.84 which provides sufficient evidence that no information is lost if restrictions are imposed in some of the short run parameters. Likewise, autocorrelation, non-normality tests as well as ARCH test indicate no problem with the model with diagnostic test statistics firmly not rejecting the robustness of VECM model. This impression is also supported by the visual inspection of graphical tools, such as plots of residuals, AC, PAC and cross correlations.

Finally, based on the evidence, one can argue that LPEU12t and LWEU12t

are strongly co-integrated, and furthermore co-integration relation enters significantly in both equations of the system. Put differently, there is sufficient evidence of bilateral causality between prices and wages. In addition to long-run relationship, one can also argue that short-run parameters also indicate a statistically significant bilateral causal relationship. Furthermore, the robustness checks firmly indicate that VECM model is well designed and does not suffer from any econometric problem.

Causality between Prices and Wages: VECM Analysis for EU-12

41

Conclusion As we have seen there are two groups of economists that are split with

regards to the direction of causality between prices and wages. First, those who argue that wages cause prices, and second, those economists who argue that prices cause wages. Agreeing with Lemos (2004) we can also suggest that the researchers’ conclusions on the causal relationship may be contingent on a number of elements such as sample length, the number of explanatory variables used (including the number of lags of each variable), particular measure of prices used etc. or a Palley (1999) suggests, the causal relationship may also change with economic cycles. Despite most of the studies usually giving one way causality this study of the price-wage causal relationship in EU-12 supports the case of bilateral causality.

The OLS regression results strongly support the case of bilateral causality, though these results are scientifically questionable due to the presence of high autocorrelation in the residuals of estimated OLS models. Nonetheless, the most significant findings emerging from OLS estimations are potentially strong causal relationship and non-presence of intercept in the relationship. The VECM model has been specified by taking into account various information criteria and co-integration tests, which were carefully performed and analyzed, though only the parsimonious model has been presented. Based on the VECM coefficients one can firmly argue in favor of a strong bilateral causal relationship, both in long-run as well as in the short-run. Furthermore the robustness checks indicate no problems with the designed model, hence one may not reject the null hypothesis that model is correctly specified. Although, far from completely resolving the issue of causality, this article provides a modest analysis in the case of EU-12. Without a doubt, an analysis taking into account larger group of countries may be more productive in delivering a stronger answer and future efforts in that direction would be very fruitful.

Notes

(1) His famous definition of causality runs as follows: “We may define a CAUSE to be «An object precedent and contiguous to another, and where all the objects resembling the former are placed in like relations of precedency and contiguity to those objects, that resemble the latter» (1978 ed., p. 170). http://science.jrank.org/pages/8538/ Causality-Hume.html (2) See Emery and Chang (1996). (3) Quoted in Dunleavy P. (2003), “Authoring a PhD”, Palgrave, 2003.

Adriatik Hoxha

42

References

Andersson, J., „Testing for Granger Causality in the presence of measurement errors”,

Economics Bulletin, vol. 3, No. 47, 2005, pp. 1-13 Ashley, R., Granger, C.W.J., Schmalensee, „Advertising and Aggregate Consumption: An

Analysis of Causality”, Econometrica, Vol. 48, No. 5, July 1980, pp. 1149-1167 DeGrauwe, P. (2003). Economics of Monetary Union, fifth edition, Oxford University Press,

ISBN 0-19-925651-9 Dunleady, P. (2003). Authoring a PhD, Palgrave Emery, K.M., Chang, C.P., „Do Wages Help Predict Inflation?”, Federal Reserve Bank of

Dallas, Economic Review of the First Quarter, 1996 Garcia, C.J., Restrepo, J.G., „Price and wage inflation in Chile”, BIS Papers, No. 8, (part 5),

November 2001 Gilbert, C.L., „Economic Causality”, paper prepared for the 2004 Annual Causality,

Metaphysics and Methods Conference, LSE, London, 15-17 June, 2004 Goretti, M., „Wage-Price Setting in New EU Member States”, IMF Working Paper,

WP/08/243, 2008 Granger, C.W.J., „Some properties of the time series data and their use in econometric model

specification”, Journal of Econometrics, 16, 1981, pp. 121-130 Gujarati, D. (2002). Basic Econometrics, fourth (international) edition, McGraw-Hill Higher

Education, ISBN 0-07-112342-3 Haavlemo, T., „The probability Approach in Econometrics”, Econometrica, 12, Issue

Supplement (July, iii-vi, 1-115), 1994 Hess, G.D., Schweitzer, M.E., „Does Wage inflation cause price Inflation?”, Federal Reserve

Bank of Cleveland, Policy Discussion Paper Number 10, April 2000 Jarque, C.M., Berra, A.K., „A test for normality of observation and regression residuals”,

International Statistical Review, 55, 1987, pp. 163-172 Jonsson, M., Palmqwist, S., „Do Higher Wages Cause Inflation?”, Sveriges Riskbank, Working

Paper Series, April 2004 Jung, C., Seldon, B., „The Macroeconomic Relation between Advertising and Consumption”,

Southern Economic Journal, Vol. 61, 1995 Lemos, S., „The Effect of the Minimum Wage on Prices”, University of Leicester, Working

Paper No. 04/7, March 2004 LeRoy, S.F., „Causality in Economics”, Centre for Philosophy of Natural and Social Science

Causality: Metaphysics and Methods, Technical Report, 20/04, 2004 Lütkhepohl, H., Krätzig, M. (2004). Applied Time Series Econometrics, Cambridge University

Press, October 2004, ISBN 0 521 54787 3 Lütkhepohl, H., Krätzig, M., „VECM Analysis in JMulTi”, 2005, www.jmulti.de Lütkhepohl, H., Krätzig, M., Boreiko, D., „VAR Analysis in JMulTi”, 2006, www.jmulti.de Lütkhepohl, H., Krätzig, M., „Initial Analysis in JMulTi”, 2006, www.jmulti.de Madala, D.S. (2001). Econometrics, Wiley, 3rd edition, ISBN 978-0471497288

Causality between Prices and Wages: VECM Analysis for EU-12

43

Moschos, D., „Aggregate Price Responses to Wage and Productivity Changes: Evidence from the US”, Empirical Economics, Vol. 8, 1983, pp. 169-75

Palley, T.I., „The U.S. Inflation Process: Does Nominal Wage Inflation Cause Price Inflation, Vice-versa, or Neither?”, The annual ASSA/URPE Conference, held in New York, NY, 2-3 January 1999

Perron, P., „The Great Crash, The Oil Price Shock, and the Unit Root Hypothesis”, Econometrica, Vol 57, No. 6, November, 1998, pp. 1361-1401

Pu C., Flaschel, P., Chihying, H., „A Causal Analysis of the Wage-Price Spiral”, Working Paper, March 14, 2006

Saikkonen, P., Lütkhepohl, H., „Local power of likelihood ratio tests for the cointegrating rank of a VAR process”, Econometric Theory, 15, 1999, pp. 50-78

Sims, C., „Money, Income and Causality”, The American Economic Review, Vol. 62, no. 4, September, 1972, pp. 540-552

Sims, C., „Granger Causality”, Econ. 513, Time Series Econometrics, Fall 1999 Strauss, J., Wohar, M.E., „The Linkage between prices, wages and productivity: a panel study

of manufacturing industries”, Southern Economic Journal, April 2004 Wooldridge, J., „Introductory Econometrics: A Modern Approach”, South-Western, Div. of

Thomson Learning; 2nd revised edition, 10 Aug 2002, ISBN-10: 0324113641

Adriatik Hoxha

44

APPENDICES Table C.1

Description of the price, wage and productivity variables for EU-12 Variable Description of variables

Software Statistical

TREND t Trend variable

PEU Prices for EU-12 LPEU Log of P for EU-12 1DPEU

First Difference of P for EU-12

1DLPEU

First Difference of the log of P for EU-12

WEU Wages for EU-12 LWEU

Log of W for EU-12

1DWEU

First Difference of W for EU-12

1DLWEU

First Difference of the log of W for EU-12

QEU Productivity for EU-12 LQEU Log of Q for EU-12 1DQEU

First Difference of Q for EU-12

1DLQEU

First Difference of the log of Q for EU-12

Price Wage Productivity

(a)

8590

9510

010

5PE

U12

1996q1 1999q1 2002q1 2005q1 2008qtime

9010

011

012

013

0W

EU

12

1996q1 1999q1 2002q1 2005q1 2008q1time

9510

010

5Q

EU12

1996q1 1999q1 2002q1 2005q1 2008q1time

(b)

0.5

11.

5D

PEU

12

1996q1 1999q1 2002q1 2005q1 2008q1time

.4.6

.81

1.2

DW

EU

12

1996q1 1999q1 2002q1 2005q1 2008q1time

-.50

.51

DQ

EU12

1996q1 1999q1 2002q1 2005q1 2008q1time

Figure C.1A. Plots of price, wage and productivity variables:

a) levels and b) first difference of levels

Causality between Prices and Wages: VECM Analysis for EU-12

45

Price Wage Productivity

(a)

4.45

4.5

4.55

4.6

4.65

LPE

U12

1996q1 1999q1 2002q1 2005q1 2008q1time

4.5

4.6

4.7

4.8

LWEU

12

1996q1 1999q1 2002q1 2005q1 2008q1time

4.55

4.6

4.65

LQEU

12

1996q1 1999q1 2002q1 2005q1 2008qtime

(b)

0.0

05.0

1.0

15D

LPE

U12

1996q1 1999q1 2002q1 2005q1 2008q1time

.004

.006

.008

.01

.012

DLW

EU12

1996q1 1999q1 2002q1 2005q1 2008q1time

-.005

0.0

05.0

1D

LQE

U12

1996q1 1999q1 2002q1 2005q1 2008time

Figure C.1B. Plots of price, wage and productivity variables: a) log-levels and b) first

difference of log-level

Table C.2 Formal Unit Root Tests for individual series of price, wage and productivity variable

Test Procedure/Variables ADF -1.186 -1.846 -10.645 -11.374 Phillips-Perron -0.049 -1.023 -10.413 -11.638 Test Procedure/Variables ADF -1.929 -0.917 -3.364 -3.689 Phillips-Perron -1.997 -1.439 -3.443 -3.812 Test Procedure/Variables ADF -2.294 -2.417 -5.017 -5.029 Phillips-Perron -2.545 -2.630 -4.986 -5.002

Note: Critical values are as follows: a) levels series, 0.05 = -3.512; b) differenced series, 0.05 = -2.941. Appendix E.1 Determination of the number of lagged differences *** Tue, 30 Jun 2009 01:29:36 *** OPTIMAL ENDOGENOUS LAGS FROM INFORMATION CRITERIA endogenous variables: LPEU12 LWEU12 exogenous variables: LQEU12 exogenous lags (fixed): 1 deterministic variables: S1 S2 S3 TREND sample range: [1998 Q2, 2007 Q4], T = 39 optimal number of lags (searched up to 8 lags of 1. differences): Akaike Info Criterion: 8 Final Prediction Error: 3 Hannan-Quinn Criterion: 3 Schwarz Criterion:

Adriatik Hoxha

46

Appendix E.2 Complete results

*** Sat, 20 Jun 2009 02:01:20 *** VEC REPRESENTATION endogenous variables: LPEU12 LWEU12 exogenous variables: LQEU12 deterministic variables: S1 S2 S3 TREND endogenous lags (diffs): 3 exogenous lags: 1 sample range: [1997 Q1, 2007 Q4], T = 44 estimation procedure: Two stage. 1st=Johansen approach, 2nd=EGLS Lagged endogenous term: ======================= d(LPEU12) d(LWEU12) ------------------------------------ d(LPEU12)(t-1)| -0.735 --- | (0.135) ( ) | {0.000} { } | [-5.434] [ ] d(LWEU12)(t-1)| --- --- | ( ) ( ) | { } { } | [ ] [ ] d(LPEU12)(t-2)| -0.326 -0.239 | (0.148) (0.073) | {0.027} {0.001} | [-2.207] [-3.259] d(LWEU12)(t-2)| 0.345 0.577 | (0.201) (0.126) | {0.085} {0.000} | [1.720] [4.584] d(LPEU12)(t-3)| --- -0.330 | ( ) (0.082) | { } {0.000} | [ ] [-4.048] d(LWEU12)(t-3)| 0.549 0.355 | (0.224) (0.131) | {0.014} {0.007} | [2.455] [2.715] ----------------------------------- Current and lagged exogenous term: ================================== d(LPEU12) d(LWEU12) --------------------------------- LQEU12(t) | --- -0.152 | ( ) (0.059) | { } {0.010} | [ ] [-2.571] LQEU12(t-1)| --- 0.153 | ( ) (0.059) | { } {0.010} | [ ] [2.577] --------------------------------- Deterministic term: =================== d(LPEU12) d(LWEU12) ------------------------------ S1(t)| -0.003 --- | (0.001) ( ) | {0.012} { } | [-2.519] [ ] S2(t)| 0.004 -0.002 | (0.001) (0.001) | {0.000} {0.004} | [4.289] [-2.888] S3(t)| --- -0.001 | ( ) (0.001) | { } {0.005} | [ ] [-2.783] -------------------------------

Loading coefficients: ===================== d(LPEU12) d(LWEU12) ------------------------------- ec1(t-1)| 0.071 0.023 | (0.014) (0.009) | {0.000} {0.007} | [5.083] [2.695] ------------------------------- Estimated cointegration relation(s): =================================== ec1(t-1) --------------------- LPEU12(t-1)| 1.000 | (0.000) | {0.000} | [0.000] LWEU12(t-1)| -0.984 | (0.004) | {0.000} | [-240.267] TREND(t-1) | 0.004 | (0.000) | {0.000} | [11.859] --------------------- VAR REPRESENTATION modulus of the eigenvalues of the reverse characteristic polynomial: |z| = ( 1.3231 1.3231 1.2525 1.2525 1.4362 1.4362 0.9729 1.0000 ) Legend: ======= Equation 1 Equation 2 ... ----------------------------------- Variable 1 | Coefficient ... | (Std. Dev.) | {p – Value} | [t – Value] Variable 2 | ...... ----------------------------------- Lagged endogenous term: ======================= LPEU12 LWEU12 ------------------------------- LPEU12(t-1)| 0.336 0.023 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] LWEU12(t-1)| -0.070 0.977 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] LPEU12(t-2)| 0.409 -0.239 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] LWEU12(t-2)| 0.345 0.577 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] LPEU12(t-3)| 0.326 -0.091 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000]

LWEU12(t-3)| 0.204 -0.222 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] LPEU12(t-4)| 0.000 0.330 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] LWEU12(t-4)| -0.549 -0.355 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] ------------------------------- Current and lagged exogenous term: ================================== LPEU12 LWEU12 ------------------------------- LQEU12(t) | --- -0.152 | ( ) (0.059) | { } {0.010} | [ ] [-2.571] LQEU12(t-1)| --- 0.153 | ( ) (0.059) | { } {0.010} | [ ] [2.577] ------------------------------- Deterministic term: =================== LPEU12 LWEU12 --------------------------------- S1 (t)| -0.003 0.000 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] S2 (t)| 0.004 -0.002 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] S3 (t)| 0.000 -0.001 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] TREND(t-1)(t)| 0.000 0.000 | (0.000) (0.000) | {0.000} {0.000} | [0.000] [0.000] ---------------------------------

Causality between Prices and Wages: VECM Analysis for EU-12

47

Appendix E.3 Model statistics

*** Sat, 20 Jun 2009 02:08:37 *** VECM MODEL STATISTICS sample range: [1997 Q1, 2007 Q4], T = 44 Log Likelihood: 4.565134e+02 Determinant (Cov): 3.335622e-12 Covariance: 3.274698e-06 -3.503604e-07 -3.503604e-07 1.056090e-06 Correlation: 1.000000e+00 -1.883992e-01 -1.883992e-01 1.000000e+00 LR-test (H1: unrestricted model): 4.2203 p-value(chi^2): 0.8367 degrees of freedom: 8.0000

Appendix E.4 Analysis of residual

*** Sat, 20 Jun 2009 02:10:39 *** PORTMANTEAU TEST is not implemented if exogenous variables are in the model. *** Sat, 20 Jun 2009 02:10:40 *** LM-TYPE TEST FOR AUTOCORRELATION with 5 lags LM statistic: 21.9492 p-value: 0.3433 df: 20.0000 *** Sat, 20 Jun 2009 02:10:40 *** TESTS FOR NONNORMALITY Reference: Doornik & Hansen (1994) joint test statistic: 2.0894 p-value: 0.7193 degrees of freedom: 4.0000 skewness only: 0.7231 p-value: 0.6966 kurtosis only: 1.3663 p-value: 0.5050 Reference: Lütkepohl (1993), Introduction to Multiple Time Series Analysis, 2ed, p. 153 joint test statistic: 1.7488 p-value: 0.7818 degrees of freedom: 4.0000 skewness only: 0.7396 p-value: 0.6909 kurtosis only: 1.0092 p-value: 0.6038 *** Sat, 20 Jun 2009 02:10:40 *** JARQUE-BERA TEST variable teststat p-Value(Chi^2) skewness kurtosis u1 0.7863 0.6749 0.3054 2.7637 u2 1.7284 0.4214 0.0140 3.9706 *** Sat, 20 Jun 2009 02:10:40 *** ARCH-LM TEST with 16 lags variable teststat p-Value(Chi^2) F stat p-Value(F) u1 11.3396 0.7881 1.1911 0.3922 u2 18.2268 0.3108 3.2637 0.0261 *** Sat, 20 Jun 2009 02:10:40 *** MULTIVARIATE ARCH-LM TEST with 5 lags VARCHLM test statistic: 38.0512 p-value(chi^2): 0.7589 degrees of freedom: 45.0000

Adriatik Hoxha

48

Plot of residual Plot of squared residual

Plot of Autocorrelation (AC) and Partial Autocorrelation (PAC) of Residuals

Cross-correlations between residuals dhe

Figure E.5. Diagnostic Checks