Embed Size (px)

Citation preview

www.cassaddpp.it

Cassa depositi e prestiti spa

Cassa Depositi e Prestiti’s role in Financing Public Investments and the Mechanism used to Improve the Capacity of Municipalities to

Access Funding for Infrastructure Projects.

Michele Mascolo

Ankara, March 4th 2008

spaCassa depositi e prestiti

2

Lending to local authorities. The Italian market

The local authorities funding

The local authorities funding. Cdp role

Cassa depositi e prestiti – key historical developments

The instruments

Status changes

Last status change

Cassa depositi e prestiti today

Status & mission

The regulatory framework

The Functioning Model

The separate account

The Ordinary account

Present and future

CDP Activity in Third Party Funds

Active Management of Public assets, a new opportunity

Active management of public assets: real estate

spaCassa depositi e prestiti

Lending to local authorities. The Italian market

spaCassa depositi e prestiti

4

The local authorities funding in Italy

Main features of the reference market Stock of debt and CDP market share

As of November 2007 local authorities’ outstanding debt reached € 113 bln.

Stock of loans was € 70 bln. while stock of bonds was € 33 bln. Loans repayable from Central Government amounted to € 58 bln.

Market growth significantly slowed down in 2007, local authorities’ sector increasing only by 4,2% on 2006 data, when compared to 2006 over 2005 growth rate (+20%), and 2005 over 2004 growth rate (+17%)

Albeit, CDP confirmed its market share in almost all segments

90

108113

5158 58

20

30

40

50

60

70

80

90

100

110

120

2005 2006 nov-07

20%

25%

30%

35%

40%

45%

50%

55%

Local Authorities debtCentral Govt. LoansCDP mkt share on Local Authorities debtCDP mkt share on Central Govt Loans

Debt (€ billion) CDP market share (%)

53%

31%

Source: Bank of Italy.

spaCassa depositi e prestiti

5

The local authorities funding in Italy. Cdp role

CDP confirmed its market share on Local Authorities (enti territoriali) segment at 30,6% (29% in 2006); 52,5% (52% in 2006) on loans repayable by Central Government, 17,4% (16,6% in in 2006) for Regions and 45,5% for Local Entities (Comuni) (42,9% in 2006)

Thus confirming its role and mission in the global scenario of the local authorities financing strategy

CDP market share

Source: Bank of Italy.

CDP market share on outstanding loans to the public sector

16,6% 17,4%

42,9%45,5%

29,2% 30,6%

51,8% 52,5%

49,3%50,5%

0%

10%

20%

30%

40%

50%

60%

2006 I quarter 2007 II quarter 2007 III quarter 2008 november 2007

Regions Local Entities Local Authorities Central Gov. loans Total public sector loans

spaCassa depositi e prestiti

6

Cassa depositi e prestiti – key historical developments

spaCassa depositi e prestiti

7

Key historical developments of CDP

1850: the CDP is established in Turin to accept deposits as an institution of “public trust”

1857: the CDP grants loans through Royal Decrees on the condition that borrowers have sufficient means to make repayment

1863: the Piedmont-based CDP absorbs the other “Casse” of the Kingdom into a new institution, which is based first in Florence, then in Rome

spaCassa depositi e prestiti

8

Key historical developments of CDP: the instruments

1875: postal savings passbooks are introduced. The funds raised are used by the CDP to finance local authority investment in public works and repayment of past debts

1924: the introduction of interest-bearing postal savings bonds, whose small denominations, extensive distribution around the country, safe yields, high degree of liquidity and State guarantee make it easier to raise funds than with Treasury bills, whose issue is even suspended temporarily

spaCassa depositi e prestiti

9

Key historical developments of CDP: status changes

1898: the CDP is transformed into a Directorate General of the Treasury

1983: institutional reform of the CDP to grant it full organizational autonomy (Law 197/1983)

1993: the CDP is granted separate legal personality

1999: the status of the CDP as a state agency with separate legal personality and regulatory, organizational and financial independence acting in the general economic interest is confirmed. The CDP is not subject to all of the provisions of the 1993 Banking Law, while the European Community excludes the CDP from the scope of Community directives on credit. As far as economic and financial accounts are concerned in accordance with ESA 95 criteria, the CDP is classified under the general government sector

spaCassa depositi e prestiti

10

Key historical developments of CDP: last status change

On December 12th, 2003 the Cassa depositi e prestiti was transformed into a limited liability company, in order to respond more effectively to the far-reaching changes that have occurred in the regulatory and institutional framework of its reference market. The transformation has increased its capacity for action and made operations more flexible and functional

spaCassa depositi e prestiti

11

Cassa depositi e prestiti today

spaCassa depositi e prestiti

12

Cassa depositi e prestiti today: Status & Mission

Cassa depositi e prestiti S.p.a. (“CDP”) is a limited liability joint stock company established on December 2003 by transformation of CDP –Public Company as of art. 5 of Law Decree 269 of 30 September 2003

The CDP’s mission is to foster the development of public investment, local utility infrastructure works and major public works of nationalinterest, ensuring an adequate return for its shareholders while preservingits long-term financial and economic balance

The CDP intends to remain the key financial counterparty for localauthorities and for the owners and operators of infrastructure.

spaCassa depositi e prestiti

13

Cassa depositi e prestiti today: the Regulatory Framework

Ministerial Decree of 6 October 2004 (Part III) has defined guidelines for the organizational and accounting separation between CDP’s activities in order to:

• Ensure the economic equilibrium of CDP

• Provide useful data for the MEF in order to exercise its power of establishing guidelines

• Ensure compliance with regulations governing State Aid, competition and transparency

spaCassa depositi e prestiti

14

Cassa depositi e prestiti today: the Regulatory Framework

Despite not being classified as a financial intermediary according to Legislative Decree 385/93 (Italian Banking Act -Testo Unico Bancario), CDP S.p.A. falls under the supervision of Bank of Italy; supervision is applied, taking into account CDP S.p.A.’s peculiarities and is harmonized with the specific regulations set for the management of the segregated account

The MEF sets the strategic guidelines and supervises the activity of the segregated account. Moreover, the segregated account is audited by the Italian Court of Accounts (Corte dei Conti)

30 % of CDP S.p.A. share capital is owned by private investors with public interest mission: the banking Foundations ( Fondazioni Bancarie), while the MEF retains 70% majority

spaCassa depositi e prestiti

15

Cassa depositi e prestiti today: the Regulatory Framework

On September 2006, CDP has been classified by the Bank of Italy as a “credit institution” (as defined in Article 4 of the Directive 2006/48/EC of the European Parliament and the Council of 14 June 2006)

As a result, effective as of 30 September 2006 the company is due to undergo to some of the rules required by the European provisions on the European Central Bank System. In particular, CDP has become subject to:

The miminum reserve requirements applicable to “credit institutions”in compliance with Regulation (EC) 1745/2003 of the European Central Bank of 12 September 2003

The statistical reporting requirements applicable to “credit institutions” and other “financial monetary institutions” in compliance with Regulation (EC) 2423/2001 of the European Central Bank of 22 November 2001

spaCassa depositi e prestiti

16

Cassa depositi e prestiti today: the Functioning Model

Upon its transformation, CDP has established two operational areas within the same legal entity to manage public mandate and open-market activities separately for accounting and organisational purposes only, as requested by law:

Market funding

Financing to P.A. + Local

Authorities

Economic Development

Financing

Equity

OrdinaryAccount

(No State Guarantee)

Postal

Savings

CDP spa

Financing to P.A. + Local

Authorities

Economic Development

Financing

Participations

Separate Account

(State Guarantee)

spaCassa depositi e prestiti

17

Cassa depositi e prestiti today: the Functioning Model

Current organization

Board & General Director

Finance PublicInvestments

Infrastructure andstrategic projects

Development PoliciesManagement and Support

Support units

Accounting separation

= Separated Account

= Ordinary Account

= Common ServicesCorporate center

Business Units

Postal savings

Market Funding ( EMTN & Covd. Bonds)

spaCassa depositi e prestiti

18

Cassa depositi e prestiti today: the ‘Separate Account’

The first Area, known as the “Separate Account”, acts its general economic interest mission. It provides the funding at homogeneous conditions of investment of local authorities, public agencies and other public-law bodies, together with the other activities performed by CDP under its public interest role

The Ministry for the Economy and Finance (MEF) issues guidelines and exercise its supervisory and regulatory powers, while the Parliamentary Supervisory Committee will continue to oversee the activities of this area

Postal

Savings CDP spa

Financing to P.A. + Local

Authorities

Economic Development

Financing

Participations

Separate Account

(State Guarantee)

spaCassa depositi e prestiti

19

Cassa depositi e prestiti today: the ‘Separate Account’

Public sector lending remains CDP’s main business. Loans of the GestioneSeparata are a “service of general economic interest” and as such are governed in compliance with criteria that guarantee “accessibility, uniform treatment, predetermination of rates and non-discrimination”

CDP then continues to grant specific-purpose loans to finance public investments, having ascertained the existence of the requirements provided for by law governing the borrowing of the loan applicant and the compliance with the conditions established by CDP for homogeneous categories;

CDP may also provide financing on different terms and conditions from those of specific-purpose loans for public-interest projects; such financing shall be granted for homogeneous categories of entities or purposes and interest rates shall be determined by CDP on the basis of the purposes of the project, the characteristics of the investment and the characteristics of the borrower

Lending

spaCassa depositi e prestiti

20

Cassa depositi e prestiti today: the ‘Separate Account’

Lending to Local Authorities is funded through traditional State-guaranteed savings products placed by the Poste Italiane network (A1 stable/A+ negative by Moody’s and S&P) with retail investors

As per the Ministerial Decree of 6 October 2004:

Postal savings are a “service of general economic interest” and as such are managed in compliance with criteria determined by the MEF

Funding levels of Postal Bonds are set by in line with the cost of equivalent funding instruments of the Italian Government

CDP (i) sets terms and conditions for all issuance of postal savings; (ii) may establish new postal savings instruments benefiting from theRepublic of Italy guarantee; (iii) may suspend the issuance of Postal Bonds

The above mentioned provisions enable CDP to manage postal savings instruments dynamically within MEF guidelines and to respond appropriately to market needs, both in terms of speed of adjustment and variety of products

Funding

spaCassa depositi e prestiti

21

Cassa depositi e prestiti today: the ‘Separate Account’

Passbooks Passbooks

Passbooks are short-term, variable-rate investment products issued by Cassa Depositi e Prestiti and distributed exclusively by Poste ItalianePassbooks are guaranteed by the

Republic of ItalyInterests are accrued from the

deposit date until reimbursement. Interests are capitalised annuallyPassbooks are comparable to short

term deposits distributed by retail banksPassbooks can be issued in the

form of personal saving books or in a bearer formBearer passbook balancecannot be

larger than €12,500

Postal bonds are securities issued by Cassa Depositi e Prestiti and distributed exclusively through Poste Italiane S.p.A. networkThe main features are:• Zero-coupon interest accruing at a

compounded rate annually

• Guaranteed by the Republic of Italy and issued in dematerialised or materialised form

• Placed only to retail investors with a maximum ticket size of €5,000 and a minimum of €50 for materialised bonds and €250 for dematerialised bonds

• Postal bonds are puttable at any time by investors after the first year. Penalties apply to redemption of “Buoni a termine” series before any contractual maturity

The ‘SEPARATE ACCOUNT’ Funding instruments: Passbooks & Postal Bonds

Postal bondsPostal bonds

spaCassa depositi e prestiti

22

Cdp today: the ‘Separate Account’ - Funding data

Recent performance of the stock Postal savings (€ mln.)

Postal savings Stock as of 31 december 2007 amounts to €157.219 mln., +9% when compared to 2006 dataProduct breakdown:

• € 80.956 mln. postal bonds

• € 76.264 mln. passbooks

Postal bonds performance in 2007 is +9% on 2006

Almost same data in year 2007 for the passbooks: +8% on 2006

56.81773.957 80.956

65.403

70.58376.264

dec 05 dec 06 dec 07

Postal bonds Passbooks

122.220

144.540

157.219+18%

+9%

spaCassa depositi e prestiti

23

Cassa depositi e prestiti today: the ‘Ordinary Account’

The second area (“Ordinary Account”) is devoted to the funding of works, plant, networks and equipment for the provision of local public utilities and infrastructure, as such utilities have been or are being spun-off from Local Authorities. Financing is made on an open market basis and CDP may raise funds through the issue of securities, borrowing and other financial operations without State guarantees

Market funding CDP spa

Financing to P.A. + Local

Authorities

Economic Development

Financing

Equity

Ordinary

Account

(No State Guarantee)

spaCassa depositi e prestiti

24

Cassa depositi e prestiti today: the ‘Ordinary Account’

The mission of the “Ordinary Account” is lending to public utilities and other private companies involved in infrastructure management at market conditions

The new infrastructure lending activity is guided by economic principles and operates on market terms: loans are granted on the basis of credit worthiness criteria developed by CDP and funding is obtained through market instruments without government guarantees

The Ordinary account financing strategy

spaCassa depositi e prestiti

25

Cassa depositi e prestiti today: the ‘Ordinary Account’

Loans disboursed

515

9571.164

75

127

68

60

3648

dic-05 dic-06 dic-07Finanziamenti corporate Project finance Altri

1.101

1.351The amount of disbursed loans as of 31 December 2007 reached €1.351 mln., with a significant (+23%) growth on year end 2006, more than doubled with respect to 2005, when the Ordinary Account started its activity

At the same time ( end 2007) stock of loans granted has reached € 1.824 mln, with a strong ( +28,5%) increase when comparing to 31 December 2006 data

600

+84%

+23%

spaCassa depositi e prestiti

26

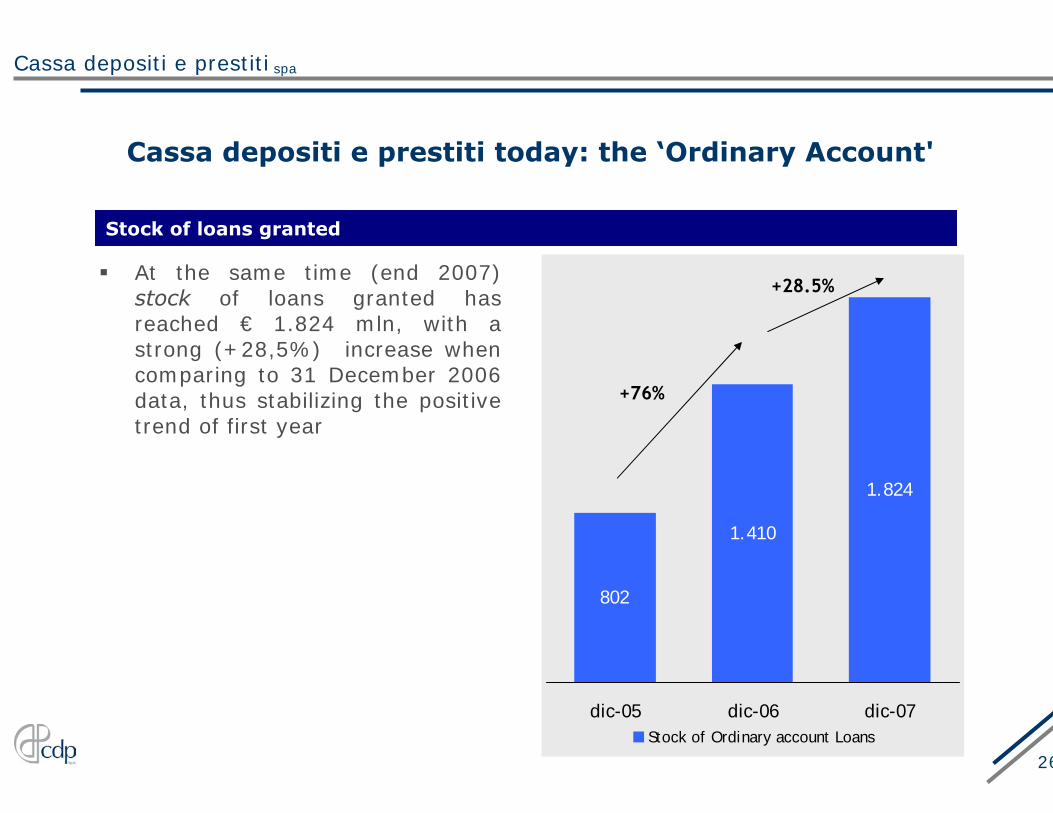

Cassa depositi e prestiti today: the ‘Ordinary Account'

Stock of loans granted

802

1.410

1.824

dic-05 dic-06 dic-07Stock of Ordinary account Loans

At the same time (end 2007) stock of loans granted has reached € 1.824 mln, with a strong (+28,5%) increase when comparing to 31 December 2006 data, thus stabilizing the positive trend of first year

+76%

+28.5%

spaCassa depositi e prestiti

27

Cassa depositi e prestiti today: the ‘Ordinary Account’

Funding strategy for the “Gestione Ordinaria” provides for a direct correlation between the volume of funds raised and the amount of lending. Funding is currently based on the following instruments:

Issues under the EMTN & Covered Bonds programmes

Drawdowns on credit facility granted by EIB under framework agreement signed in July 2005

Funding

spaCassa depositi e prestiti

28

Present and future: CDP Activity in Third Party Funds

The need of new infrastructures is widespread all over the world

Even in market – oriented economic systems a strong presence of “public”players acting close to and together with the private players is felt as necessary

This partnership enables the promotion of innovative instruments

An important example of this partnership is the growing market of third party infrastructure Funds

spaCassa depositi e prestiti

29

Present and future: CDP Activity in Third Party Funds

In an uncertain scenario the demand for investment instruments with a risk/reward smooth profile is rapidly growing

As a consequence the interest for financial instruments strictly linked to public infrastructures and real estate is very strong

Because their return is long term and stable

State guarantee and projected stable cash flows are the keys to issue long term securities that can match this kind of investment attitude

PPP= Private Public Partnership can then represent a solution toinfrastructure financing in this particular historical phase

spaCassa depositi e prestiti

30

Present and future: CDP Activity in Third Party Funds

In Italy Local Authorities investment expenses amounts to 87% of the total General Government size

This is mainly due to the huge set of responsibilities (including financial ones) transferred from Central Government to Local Authorities

As a consequence, Local Authorities currently play a major and central role in infrastructure growth in Italy

Along with the growth of investments, stock of local debt is also growing

EU controls on public finance force to think about new ways to finance investments and debt

Along with traditional sources (taxation, transfer from CG, loans) innovative ways are showing up, such as project finance and several financial instruments based on public assets

spaCassa depositi e prestiti

31

Present and future: CDP Activity in Third Party Funds

Worldwide more than 60 Infrastructure Funds are active, with a total capitalization of about € 52 bln.

In Europe 18 funds are active with a capitalization of € 16,5 bln.

In Italy some of them are already active, with a capitalization of about € 3 bln.

They invest in public transportation, public utilities, power, distribution networks and other local projects

CDP is a central player in this challenge

CDP promoted Fund F2i, joined by Italian and international major players, took part to European initiatives like Fund Galaxy (partnership with French CDC and German KfW) and to other “targeted” initiatives like PPP Fund

spaCassa depositi e prestiti

32

Present and future: CDP Activity in Third Party Funds

Large size Infrastructure Focus on Italy:

F2i(Sponsor)

PPP Projects + Greenfield,Focus on Italy

Small size asset:Fondo PPP Italia

(Subscriber)

Social Connotation, Real Estate Sector, Regional relevance:

Fondo Abitare Sociale 1(Subscriber)

Transport Infrastrucure, medium size asset,

European and International Focus:Galaxy

(Sponsor)

spaCassa depositi e prestiti

33

Present and future: CDP Activity in Third Party Funds

In 2006, CDP’s Ordinary Account started to invest in infrastructural fundssuch as:

Galaxy, is a dedicated transportation infrastructure equity fund investing primarily in Europe and in OECD countries:

Total size of the fund amounts to EUR 250 million, of which EUR 100 million committed by CDC and CDP each and the remaining EUR 50 million committed by KfW

Infrastructure private Equity

Transport Infrastrucure, medium size asset,

European and International Focus:Galaxy

(Sponsor)

spaCassa depositi e prestiti

34

Present and future: CDP Activity in Third Party Funds

On December 2006 the Fondo PPP Italia was launched:

Main investment focus is on projects of public-private partnership (ppp) (investing on housing projects, public utilities, and greenfield, focusedon Italy)

Other partecipants: KfW, BEI, Compagnia San Paolo, Fin.Opi, FondazioneCariplo, Fondazione Cariparo, Banco Espirito Santo de Investimento

Infrastructure private Equity

PPP Projects + Greenfield,Focus on Italy

Small size asset:Fondo PPP Italia

(Subscriber)

spaCassa depositi e prestiti

35

Present and future: CDP Activity in Third Party Funds

On January 2007 CDP launched a new Infrastructure Fund: F2i partnering with some major banking groups such as Unicredit, Banca Intesa some of the main Banking Foundations and Pension Funds

The size of the fund will be in the range of approx. EUR 1.5 – 2 billion

As of today CDP stakes is 31,4% of the SGR company capital .The to be size is planned to be around 14%

Main investment focus will be on Italian infrastructure projects

The fund will invest in a broad range of infrastructure assets, which will include:Transportation: motorways, toll bridges, tunnels, railways, airports and portsUtilities: electric and gas grids, water companies, renewable energy, waste

managementPublic services: hospitals, parking, environment, etc.

Infrastructure private Equity

Large size Infrastructure Focus on Italy:

F2i(Sponsor)

spaCassa depositi e prestiti

36

Present and future: CDP Activity in Third Party Funds

CDP also invested in the Abitare Sociale 1 Fund whose main task is investing in projects of social housing

Other investors are: Fondazione Cariplo, Regione Lombardia, BancaIntesa Sanpaolo, Banca Popolare di Milano, Cassa Geometri, Assicurazioni Generali, Gruppo Pirelli/Telecom

Size of the Fund: € 85 mln, of which € 20 mln. as total commitment of CDP

Infrastructure private Equity

Social Connotation, Real Estate Sector, Regional relevance:

Fondo Abitare Sociale 1(Subscriber)

spaCassa depositi e prestiti

37

Present and Future: Active Management of Public assets, a new opportunity

Public assets management recently became an important source of funding for Central Government and for Local Authorities

In the next future public, non instrumental, assets sale is set play a significant role to finance public investments in infrastructure

This is higly predictable not only with reference to real estate, but also toother public assets like local networks, stakes in local corporate, and other rights

Among local authorities assets a central role can be played by networks

They can be an active element of the financing, as a substitute of guarantees, the value and the future revenues coming from the use of the network may be the key to repay the cost of financing the new infrastructure

spaCassa depositi e prestiti

38

Present and Future: Active Management of Public assets, the Real Estate assets

A major role among public assets is played by non instrumental - real estate assets

Local Authorities real estate assets are about 80% of total public assets

Its value is valued – at market value – around € 350 - 400 bln.

Most of it belong to Local Authorities and a conservative appraisal of the part immediately available for sale is between 3 – 5 % of the total

As a projection, Local Authorities could be able to get resources from 2 to 5 bln. € per year through sale of the assets or improving their value

spaCassa depositi e prestiti

39

Present and Future: Active Management of Public assets, the Real Estate assets

The Real Estate Fund appears to be the most adequate instrument to extract value from sale and valorisation of public real estateThe Fund:

Is a flexible instrument with regard to the size and the typology of the assets to manage

Gives the chance to create multi-originator Funds, with the opportunity to create a portfolio resulting from different owners

Is compliant with a long term scenario to finalize the sale/valorisation, against a quick revenue

Gives the opportunity to manage the deal in line with industrial policy plans agreed with Local Authorities and the market players, (i.e.: determining city plan and real estate destination)

Is highly politically “acceptable” since Local Authorities can play an important role from the beginning of the transaction

spaCassa depositi e prestiti

40

Present and Future Role

The infrastructure financing issue and the supporting role of CDP towards Local Authorities (accomplishing 87% of total public investments in Italy) is crucial for the development policy of the Country

An active role for CDP must prefigure:

Advisory, counselling activity

Financial assistance

Direct participation as stakeholder in different initiatives

spaCassa depositi e prestiti

41

Present and Future Role

In an environment where there a strong need for capital adequacy must deal with rules & constraint of public balance sheets, a strong interaction among institutional players, the banking system and capital market must be pursued

CDP can act as financial intermediary AND as relevant institutional investor, at the same time playing as advisor and stakeholder in innovative projects created with the Local Authorities, in an effort to actively manage public assets

This can be a hint for a reference model where CDP, Local authorities and the banking system constitute the core of a reference model of public-private-partnership focused on the realization of infrastructure