Embed Size (px)

DESCRIPTION

FM -case study

Citation preview

Financial ManagementCapital Budgeting

Presented By:-

Amarinder SinghManan SharmaArvind KumarIndorjot singhMohit singlaMBA General (Sec-A)

Submitted To:-

Prof. Dr. Meena Sharma

Case Study-1

DETAILS ABOUT G.S.PETROPULL COMPANY:1. GSPC is a fast growing profitable company.

2. The company is situated in Western India. Its sales are expected to grow about three times from Rs 360 million in 2003-04 to Rs 1,100 million in 2004-05.

3. The company is considering of commissioning a 35 km pipeline between two areas to carry gas to a state electricity board.

4. The project will cost Rs 250 million. The pipeline will have capacity of 2.5MMSCM.

5. The company will enter into a contract with the state electricity board (SEB) to supply gas.

6. The revenue from the sale to SEB is expected to be Rs 120 million per annum.

7.The pipeline will also be used for transportation of LNG to other users in the area. This is expected to bring additional revenue of Rs 80 million per annum.

8.The company management considers the useful life of the pipeline to be 20 years.

9.The financial manager estimates cash profit to sales ratio of 20% per annum for the first 12 years of the projects operations and 17% per annum for the remaining life of the project.

10.The project has no salvage value. The project being in a backward area is exempt from paying any taxes. The company requires a rate of return of 15 per cent from the project.

Discussion Questions:

1. What is the project’s payback and ARR? 2. Compute the project’s NPV and IRR. 3. Should the project be accepted? Why?

Information Extracted From Case

• Current sales : Rs 360 million (2009 )• Expected sales : Rs 1,100 million (2010)Future Projects and Revenues:

– Gas pipelines : Cost Rs 250 million– Revenue from sale to SEB is expected to be Rs 120 million per

annum.– Additional revenue from transportation of LPG is Rs 80 million per

annum.– cash profit to sales ratio of 20% per annum for first 12years and

17% per annum for the remaining life of the project.– Expected life of the project 20 years.– The company requires a rate of return of 15% from the project.

Particulars Year Cash flows(in mm.)

Cumulative Cash flows(Rs mm.)

Cost of project (Rs million) 250 0 -250 -250Revenue from SEB (Rs million) 120 1 40 -210Revenue from other users (Rs million)

80 2 40 -170

Total revenue (Rs million) 200 3 40 -130Cash profit,20% from year 1 to 12 (Rs million)

40 4 40 -90

Cash profit, 17% from year 13 to 20 (Rs million)

34 5 40 -50

Average cash profit (Rs million) 37.6 6 40 -10Average investment (Rs million) 125 7 40 30ROI 30.1% 8 40 70

9 40 110

Payback

ARR

Discount rate 15% 10 40 150

PVFA 12,15% 5.4206 11 40 190PVFA 20,15% 6.2593 12 40 230PVFA (20,12),15% 0.8387 13 34 264PV of cash profit, year 1 to 12 (Rs million)

216.82 14 34 298

PV of cash profit, year 13 to 20 (Rs million)

28.52 15 34 332

NPV (Rs million) -4.66 16 34 366

17 34 40018 34 43419 34 46820 34 502

NPV -4.66IRR 14.65%Pay back >6 years6 years and 3 months

to be precise

Q2:Should the project be accepted and why?

ANSWER: We can see from the previous slide that the NPV is negative and Internal rate of return is less than the expected rate of return.

Thus, the project should not be accepted.

Case Study-2

Details About Calmex Company

1. Calmex Company Ltd is an overhead water tank manufacturing company situated in North India.

2. The Company is contemplating manufacturing a new type of water tanks for the Southern cities.

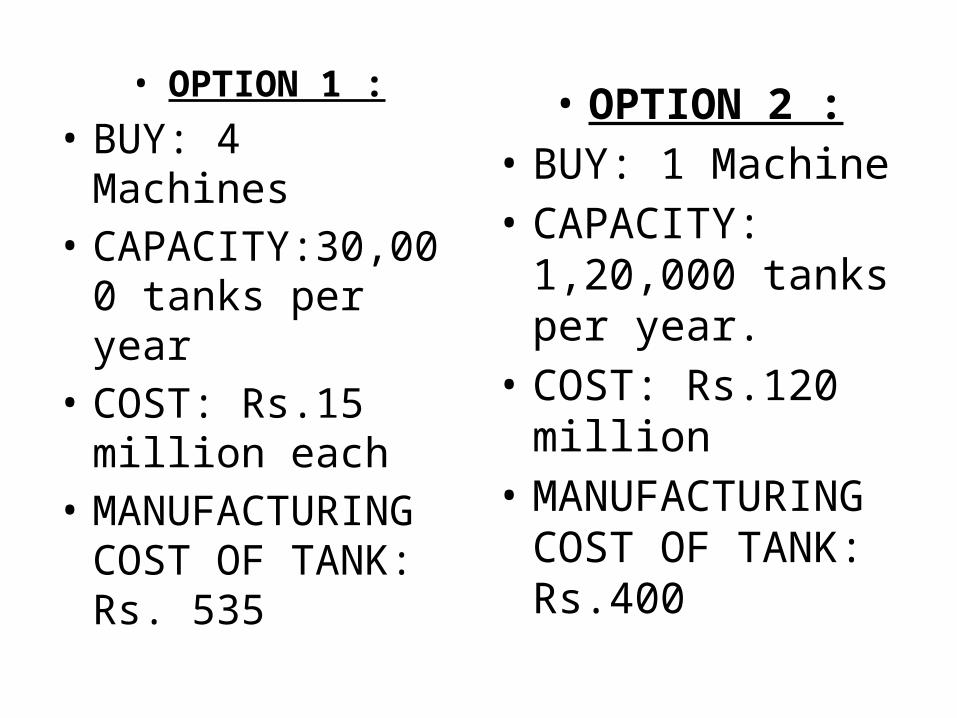

3. The Company has two options and both require buying new machinery.

• OPTION 1 :• BUY: 4 Machines• CAPACITY:30,000

tanks per year• COST: Rs.15 million

each• MANUFACTURING

COST OF TANK: Rs. 535

• OPTION 2 :• BUY: 1 Machine• CAPACITY: 1,20,000

tanks per year.• COST: Rs.120 million• MANUFACTURING

COST OF TANK: Rs.400

• The Company has a required rate of return of 12 percent and it does not pay any taxes.

Problems for Discussion:P.1:- Which option shall the company accept?

P.2:- Why do you think that the method chosen by you is the most suitable method in evaluating the proposed investment? Give the computation of the alternative methods.

Considering Alternative-1Number of tanks 1,20,000

Price (Rs) 700

Revenue(Rs million)(1,20,000*700) 84

Small machines

Cost of four small machines(Rs million) (15 * 4) 60

Op. and mfg. cost(Rs) 535

Total Op. and mfg. cost(Rs million)(0.12 * 535)

64.2

Net revenue (Rs million) (84 - 64.2) 19.8

Discount rate 12%

Project life (years) 6

PVFA 6, 12% 4.1114

PV of cash inflows (Rs million) (19.8 * 4.114) 81.4

NPV (Rs million) (81.4 - 60) 21.4

IRR 24%

Considering Alternative-2Large machine

Cost of large machine (Rs million) 120

Op. and mfg. cost (Rs) 400

Total op. and mfg. cost (Rs million)(0.12 * 400)

48

Net revenue (Rs million) (84-48) 36

Discount rate 12%

Project life (years) 6

PVFA 6, 12% 4.1114

PV of cash inflows (Rs million) (36 * 4.114) 148

NPV (Rs million) (148 - 120) 28.0

IRR 20%

Incremental ApproachIncremental cash flows

Cost (Rs million) (120 - 60) 60

Net revenue (Rs million) (36 - 19.8) 16.2

Discount rate 12%

Project life (years) 6

PVFA 6, 12% 4.1114

PV of cash inflows (Rs million) (16.2 * 4.114) 66.6

NPV (Rs million) (66.6 - 60) 6.60

IRR 16%

INTERPRETATIONS

• As we observe from the tables, NPV is greater in case of the alternative of buying the larger machine whereas IRR is greater in the case of alternative of buying smaller machines. This leads to a conflicting situation.

• The reason is while the NPV method is based on the total yield/earnings/NPV, IRR are concerned with the rate of return/earnings on investment.

• .

The NPV method is conceptually superior to that of the IRR method as the former has the virtue of having a uniform rate which can be consistently applied to all investment proposals.

While IRR method is not compatible with the objective of financial decision making of the firm, the recommendation of NPV is consistent with the goal of the firm of maximizing shareholders’ wealth.

The NPV method is the more suitable method of evaluation so we will select the alternative of buying larger machine .

The conflict between NPV and IRR can be resolved by modifying the IRR (by adopting the incremental approach)to give results identical to the NPV method. The logic is that the firm would get the profits promised by the smaller outlay investment project plus the profit on the incremental investments required in the project involving larger outlay.

• As the IRR of differential cash flow exceeds the required rate of return so we would select the project having greater investment outlays.

• By this convention we would choose the alternative of selecting the larger machine as it involves greater investment outlays.

• THANK YOU