Embed Size (px)

Citation preview

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 1 of 66

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK

Michael Harris and Stuart Schapiro )

Individually and on Behalf of All Other ) Civil Action No.: 14-CV-736 (VEC) Persons Similarly Situated, )

) CONSOLIDATED AMENDED Plaintiff, ) COMPLAINT

) v. CLASS ACTION

AMTRUST FINANCIAL SERVICES, INC., BARRY D. ZYSKIND, and RONALD E. JURY TRIAL DEMANDED PIPOLY, JR.,

Defendants.

)

Lead Plaintiffs Michael Harris and Stuart Schapiro ("Plaintiffs"), individually and on

behalf of all other persons similarly situated, by their undersigned attorneys, for their complaint

against defendants, alleges the following based upon personal knowledge as to themselves and

their own acts, and information and belief as to all other matters, based upon, inter alia, the

investigation conducted by and through their attorneys, which included, among other things, a

review of the defendants' public documents, conference calls and announcements made by

defendants, United States Securities and Exchange Commission ("SEC") filings, wire and press

releases published by and regarding AmTrust Financial Services, Inc. (“AmTrust” or the

“Company”), analysts' reports and advisories about the Company, and information readily

obtainable on the Internet. Plaintiffs believe that substantial evidentiary support will exist for

the allegations set forth herein after a reasonable opportunity for discovery.

1

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 2 of 66

NATURE OF THE ACTION

1. This is a federal securities class action under Sections 10(b) and 20(a) of the

Securities Exchange Act of 1934 (the “Exchange Act”) on behalf of all persons other than

defendants who purchased AmTrust common stock and preferred stock between February 15,

2011 and December 11, 2013, inclusive (the “Class Period”) and who did not sell such

securities prior to December 12, 2013, seeking damages against the Company and two of its

top officials.

2. In addition, lead plaintiff Stuart Schapiro brings claims against AmTrust under Section

11 of the Securities Act of 1933 on behalf of a sub-class of persons and entities who purchased

AmTrust Series A preferred stock in or traceable to the public offering on June 5, 2013 (the

“Preferred Offering”) and did not sell those shares prior to December 12, 2013.

3. AmTrust offers insurance coverage to policyholders including

property/casualty, workers’ compensation, special risk, and warranty insurance, and extended

service plans.

4. During the Class Period, AmTrust understated its insured losses or loss and loss

adjustment expense from its insurance operations for the fiscal years ended 2010 through 2012,

in the amount of approximately $289.9 million. Consequently, AmTrust also overstated its

underwriting income earned during the same period by $289.9 million.

5. AmTrust accomplished this fraud by making knowingly unrealistic actuarial

assumptions as to the amount of expected future losses from insurance policies it wrote.

6. Investors evaluate the profitability and quality of an insurance company’s

business by measuring its underwriting income, loss ratio, expense ratio and combined ratio.

2

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 3 of 66

7. Underwriting income is measured as net earned premium, minus (i) loss and

loss adjustment expense, and minus (ii) acquisition costs and other underwriting expenses. 1

8. Net earned premium is the earned portion of premiums received, calculated as

Earned Premium less the portion of the premiums that the insurer cedes to third party

reinsurers under reinsurance agreements.

9. Loss and loss adjustment expense” or “L/LAE”) are losses resulting from

current payments and estimated payments resulting from insurance claims. These represent

the largest expense item and are the main driver of AmTrust’s operating costs and profits. (see

for example the AmTrust 2010 10-K, page 63)

10. Acquisition costs and other underwriting expenses consist of the cost of

acquiring, underwriting, and servicing insurance polies, including agent commissions, salaries

of staff, rent, and other insurance operations overhead.

11. Loss ratio is calculated as loss and loss adjustment expense divided by net

earned premium.

12. Expense ratio is acquisition costs and other underwriting expenses of acquiring,

writing, and servicing insurance polies divided by net earned premium.

13. Combined ratio is the sum of the loss ratio and the expense ratio.

14. Thus, by understating loss and loss adjustment expense, AmTrust inflated

underwriting income, as well as the loss ratio and combined ratio which are all key measures

used by investors and analysts to assess the profitability and value of an insurance company.

1 Until Fiscal 2013, Amtrust had been calculating underwriting income as net earned premium less loss and loss adjustment expense, less acquisition costs and other underwriting expenses, less related party ceding commissions.

3

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 4 of 66

15. One of the unique aspects of financial accounting for an insurance company is

that management has tremendous discretion to determine the current year’s loss and loss

adjustment expense by estimating the expected future costs of claims.

16. Because underwriting income is a direct function of loss and loss adjustment

expense, management is able to manipulate underwriting income by making unrealistically low

estimates of the future costs of resolving claims.

17. For the past 6 years, AmTrust has consistently reported loss ratios and

consequently, combined ratios that are materially lower than industry average ratios.

18. Reporting loss ratios that are consistently lower than the industry average

implies that AmTrust has been able to identify and attract customers in its workers

compensation and general casualty insurance businesses that are injured less and who suffer

less natural disasters than its competitors’ customers. This has led investors to believe

AmTrust is running a highly profitable business underwriting insurance.

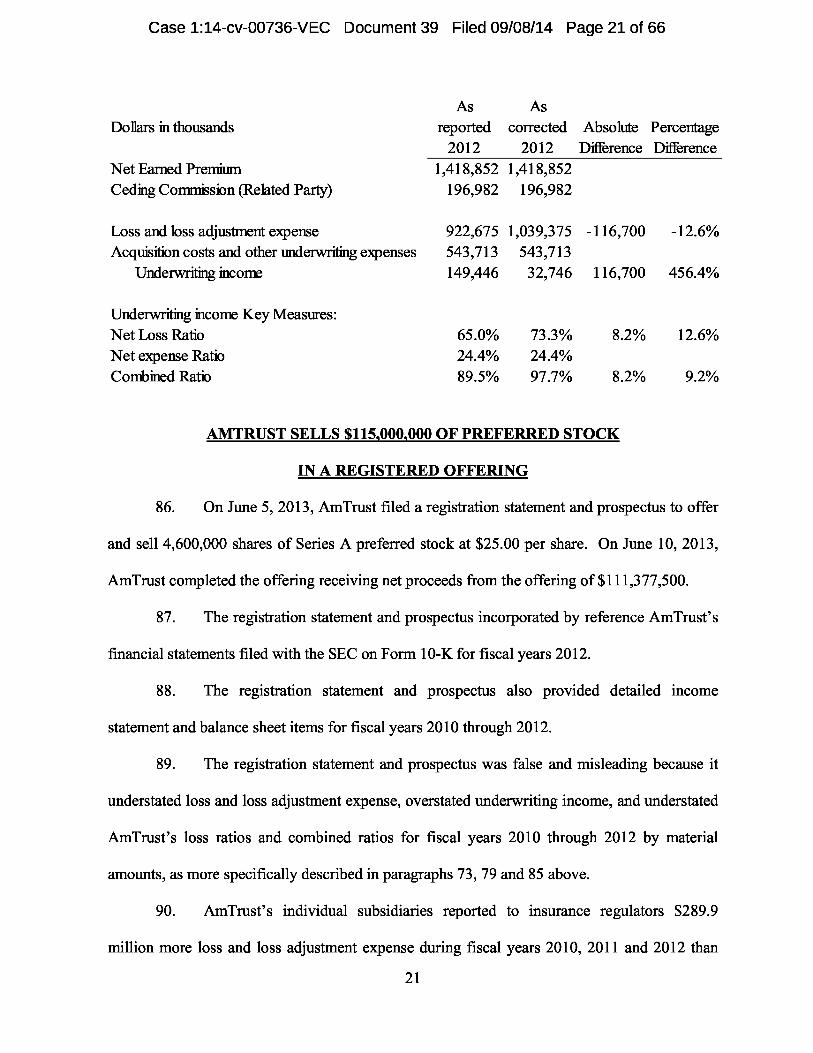

19. Yet, AmTrust is a relative newcomer (15 years old) in a business whose

fundamentals haven’t changed meaningfully in four hundred years.

20. Typically, if an insurance company uses unreasonably low estimates for its

insured losses over a period of five years or so, the chickens come home to roost, its reserves

are depleted, and its profit eventually disappears. As the true cost of claims is incurred, the

company must increase its reserves by recording additional losses to reflect the higher than

expected losses.

21. AmTrust, however, has avoided discovery by increasing its net earned premium

revenue each year, while the rest of the industry has experienced shrinking premium revenue.

It does this by undercutting its competition in pricing its policies and writing more and more

4

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 5 of 66

policies that are individually less profitable because it is insuring the same risk at a lower price

than its competitors. Selling more and more insurance policies that are less profitable than

industry average should result in higher loss ratios – not lower.

22. By increasing its net earned premium revenue each year and hiding its true

losses, AmTrust is able to mask the understatements in its estimates of the true costs of claims

reported in past years. This is because the increasing numerator in its loss ratio (which

represents current estimates of future losses as well as adjustments caused by the true costs of

claims “coming home to roost”) is counterweighted against the ever increasing denominator in

the loss ratio (net earned premium revenue).

23. In order to maintain access to more and more capital to support its premium

growth, AmTrust has had to report consistently high earnings. To do so, it had to hide the

increasing losses it was experiencing as its unrealistically low estimates of insured losses were

incurred and claims were eventually paid out.

24. By improperly misclassifying loss and loss adjustment expense as other non-

underwriting expenses when consolidating its subsidiaries’ financial statements, AmTrust hid

these mounting losses in order to give investors the misleading impression that its insurance

operations were much more profitable than they really were.

25. On December 12, 2013, a report by analyst firm Geoinvesting exposed AmTrust

as a “House of Cards”. Drawing on financial information AmTrust’s subsidiaries filed with

State insurance commissioners in the U.S., and in Bermuda, Geoinvesting demonstrated that

from fiscal 2010 through 2012, AmTrust concealed $289.9 million of losses through

accounting manipulations.

5

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 6 of 66

26. Geoinvesting’s thesis was that AmTrust hid $276.9 million in losses by having

its U.S. subsidiaries cede the losses to its Bermuda reinsurer, which then ceded them to its

Luxembourg subsidiaries, while retaining the corresponding insurance premiums in its

Bermuda subsidiary. Geoinvesting believed that AmTrust consolidated its entire operations

without ever recognizing or revealing to investors the losses ceded to its Luxembourg

subsidiaries. Geoinvesting theorized that, under the guise of using Luxembourg accounting

principles, AmTrust simply didn’t include the $289.9mm in losses in the consolidation process

by fraudulently making them disappear, under the guise that under Luxembourg accounting

principles, the losses were offset or absorbed by the equalization balances.

27. Plaintiffs’ analyses indicate that rather than relying on the Luxembourg

equalization balances to fraudulently erase the $289.9 million in losses, in the process of

consolidating its financial statements, AmTrust “eliminated” the balance of the $289.9 million

in loss and loss adjustment expense by misclassifying them as other non-underwriting expense

items on its consolidated income statement , thereby deceiving investors to believe that

AmTrust’s insurance operations were much more profitable.

28. Thus, when investors and analysts evaluated AmTrust underwriting operations

using conventional metrics such as underwriting income, loss ratio and combined ratio,

AmTrust’s underwriting business looked very profitable and much stronger than its

competitors, thereby inflating its stock price.

29. AmTrust’s subsidiaries’ individual financial reports filed with insurance

regulators showed aggregate loss and loss adjustment expense for 2010 through 2012 that was

$289.9 million greater than the loss and loss adjustment expense that AmTrust reported in its

6

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 7 of 66

consolidated financial statements in its annual reports on Form 10-K filed with the SEC for

2010 through 2012.

30. The sum of the total loss and loss adjustment expense reported for AmTrust’s

subsidiaries should match the total loss and loss adjustment expense reported for AmTrust’s

consolidated operations because the loss and loss adjustment expense reported by the

subsidiaries has already been reduced by the amount of any intercompany transactions. Thus,

the sum of the parts should equal the whole. And while the premium revenue reported by the

subsidiaries adds up and equals the total premium revenue reported in AmTrust’s consolidated

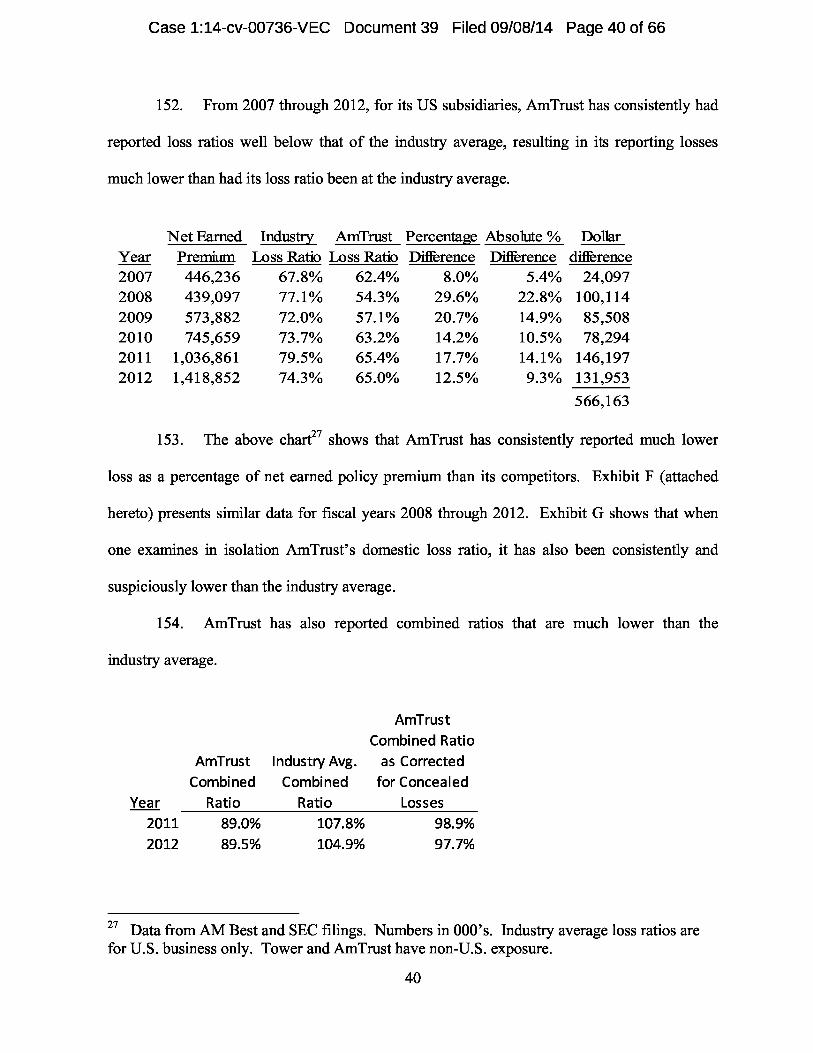

financial statements filed with the SEC, the losses of the subsidiaries do not.

31. That AmTrust’s consolidated financial statements did not accurately report all

of the loss and loss adjustment expense and was in fact missing $289.9 million of loss and loss

adjustment expense reported by its subsidiaries to insurance regulators proves that AmTrust’s

consolidated financial statements filed with the SEC understated losses and overstated

underwriting income by $289.9 million from 2010 to 2012.

32. On publication of the Geoinvesting report disclosing that AmTrust had been

concealing losses and that its underwriting business was less profitable than reported,

AmTrust’s common stock price declined $4.63 per share or 12%, to close at $33.67 per share

and its Series A preferred shares declined $2.55/share on December 12, 2013.

33. Geoinvesting issued a follow up report providing additional evidence supporting

its assertions that AmTrust had not reported all of its subsidiaries’ losses in its consolidated

financial statements, and AmTrust’s common stock share price dropped another $2.54/share

(7.2%) on December 17 and $4.09/share (12.5%) on December 18, 2013 or a total of

$6.63/share or 20.2%.

7

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 8 of 66

34. This is not the first time that AmTrust has misclassified items on its income

statement in order to present its underwriting business to be more profitable. Recently the SEC

forced AmTrust to acknowledge it had made an “error” in its accounting and reclassify related

party ceding commission from a revenue line item to a reduction of an expense line item (to a

reduction of acquisition costs and other underwriting expenses by $196.9mm in 2012 and

$138.3mm in 2011). This reclassification had a material effect on underwriting income

reducing it 14% in 2012 and 31% in 2011. 2 It also had the effect of increasing the expense

ratio by 1.3% in 2012 and 2.6% in 2011. In short, AmTrust has an established pattern of

misclassifying items on its income statement so as to present a rosier, more profitable picture

of its underwriting business.

JURISDICTION AND VENUE

35. The claims asserted herein arise under and pursuant to Sections 10(b) and 20(a)

of the Exchange Act (15 U.S.C. §78j(b) and 78t(a)) and Rule 10b-5 promulgated thereunder

(17 C.F.R. §240.10b-5) and under Sections 11 of the Securities Act (15 U.S.C. §§ 77k and

77o).

36. This Court has jurisdiction over the subject matter of this action pursuant to §27

of the Exchange Act (15 U.S.C. §78aa), Section 22 of the Securities Act (15 U.S.C. §77v) and

28 U.S.C. §1331.

37. Venue is proper in this District pursuant to §27 of the Exchange Act, 15 U.S.C.

§78aa, Section 22 of the Securities Act (15 U.S.C. §77v) and 28 U.S.C. §1391(b) as the

Company's executive offices are located in this District.

2 The SEC had questioned AmTrust’s decision to merely “reclassify” the ceding commissions rather than to issue a “restatement” of its financial statements. AmTrust defended its decision not to restate on the basis that the errors were not material. In any case, the SEC insisted that AmTrust acknowledge that it had made “errors” in its financial statements.

8

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 9 of 66

38. In connection with the acts, conduct and other wrongs alleged in this Complaint,

defendants, directly or indirectly, used the means and instrumentalities of interstate commerce,

including but not limited to, the United States mail, interstate telephone communications and

the facilities of the national securities exchange.

PARTIES

39. Lead Plaintiff Mark Harris purchased AmTrust common stock at artificially

inflated prices during the Class Period and has been damaged upon the revelation of the alleged

corrective disclosures. Mark Harris’s PSLRA certification has previously been filed with the

Court and is incorporated by reference herein.

40. Lead Plaintiff Stuart Schapiro purchased AmTrust Series A preferred stock at

artificially inflated prices during the Class Period pursuant and traceable to the Preferred

Offering and was damaged upon the revelation of the alleged corrective disclosures. Stuart

Schapiro’s PSLRA certification has previously been filed with the Court and is incorporated by

reference herein.

41. Defendant AmTrust is a Delaware corporation with its headquarters located at

59 Maiden Lane, 6th Floor, New York, NY 10038. The Company's common stock is traded on

the NASDAQ Stock Market ("NASDAQ") under the ticker symbol “AFSI”.

42. During the Class Period the Company issued 4.6 million shares of Series A

preferred stock in the Preferred Offering. The Series A preferred stock traded on the New York

Stock Exchange under the ticker symbol “AFSI-PA” during the Class Period.

43. Defendant Barry D. Zyskind ("Zyskind") has served at all relevant times as the

Company's Chief Executive Officer, President and director.

9

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 10 of 66

44. Defendant Ronald E. Pipoly, Jr. ("Pipoly") has served at all relevant times as the

Company's Chief Financial Officer. Prior to AmTrust, Pipoly was the controller and an

executive officer at PRS Insurance Group, the parent company of Credit General, a property

and casualty insurer that was liquidated in 2001 by Ohio regulators after it was revealed that its

CEO, Robert Lucia, had committed fraud, and stolen $30.0 million through transactions with a

series of related party offshore entities. Lucia was federally indicted for his fraud at PRS, pled

guilty, and was sentenced to 10 months in prison and a fine of over $56,000. Another former

Credit General executive officer, Michael Saxon, serves as AmTrust’s Chief Operating Officer.

45. Mr. Pipoly’s knowledge of the fraud at Credit General, particularly the illegal

payments to Mr. Lucia, was recognized by the Bankruptcy Judge overseeing a proceeding to

appoint a trustee to replace Mr. Pipoly’s stewardship of the company following Mr. Lucia’s

removal. In re PRS Insurance Group, Inc., 274 B.R. 381, 387 (Bkrtcy.D.Del. 2001) (“When

confronted with the Hradisky report evidencing over $3.5 million in transfers to Mr. Lucia and

his family, Mr. Pipoly did not pursue an investigation of those transfers. He did not even ask

Mr. Lucia for an explanation.”). Pipoly testified before the Court in an attempt to prevent

appointment of a trustee and the Court found his testimony not credible, as it was contradicted

by the evidence. Id. at 386-87. Interestingly, in the proceedings, Allstate Insurance accused

Lucia and Pipoly of selling assets of PRS Insurance Group to AmTrust at less than fair market

value to benefit themselves.

46. While Mr. Pipoly was CFO of AmTrust he also served as interim CFO of

Maiden Holdings, a public company founded and controlled by the same family that controls

AmTrust (Karfunkle and Zyskind). In the same time period that Pipoly was its CFO, Maiden

Holdings and PriceWaterHouseCoopers concurred that Maiden Holding “had deficiencies that

10

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 11 of 66

in combination represented a material weakness in [its] internal control over financial reporting

due to under-resourcing of the finance department and the concentration of duties in our Chief

Financial Officer.”3 These deficiencies included:

• failure to give appropriate consideration to U.S. GAAP accounting rules or to have

documentation of the basis for [the company’s] opinion and conclusion regarding the

application of U.S. GAAP;

• lack of an independent preparer and reviewer for various accounting tasks,

including the preparation of the financial statements and disclosures; and

• lack of formality regarding certain controls surrounding the control environment.

47. Defendants Zyskind and Pipoly are sometimes collectively referred to herein as

the “Individual Defendants.”

BACKGROUND

48. AmTrust underwrites and provides property and casualty insurance in the

United States and internationally. Its insurance business consists primarily of workers

compensation policies that it underwrites for businesses. Workers compensation insurance is

mandatory for nearly all employers in the United States. It is a highly competitive business.

49. AmTrust and Zyskind are relative newcomers to the insurance business.

AmTrust began in 1998 when it acquired a bankrupt computer warranty insurance business

from Wang Laboratories. Zyskind began working at AmTrust in 1998 and had no prior

insurance experience. He became AmTrust CEO in 2005 at the age of 34 after being in the

insurance business for seven years. Zyskind’s father-in-law, George Karfunkle, is one of the

major shareholders of AmTrust and serves as Chairman of its Board of Directors.

3 Maiden subsequently replaced PWC with BDO USA LPP, which also serves as AmTrust’s auditor.

11

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 12 of 66

50. Pipoly became CFO of AmTrust after he assisted AmTrust in purchasing certain

assets from PRS Group (the parent of Credit General), which as stated earlier, Allstate alleged

were sold at less than fair market value.

REINSURANCE AND CEDING OF PREMIUM AND LOSS

51. Reinsurance is an insurance contract between an insurer and a reinsurer,

wherein the reinsurer agrees to bear a certain amount of fixed risk borne by the insurer under

the policies that it has issued. In exchange for providing reinsurance services, the reinsurer

usually gets a premium from the ceding company, which may be a share of the original

premium minus commissions or another mutually agreed-upon amount. The main aim of

reinsurance is to spread risk to enable the insurance industry to function effectively and

efficiently. Reinsurance allows the ceding company to take on more business than would be

possible without a significant increase in capital and risk.

52. In a reinsurance contract, the ceding company transfers all or a portion of its

risk and obligation on the policy to the reinsurer in return for a portion of the premium

associated with the risk. In addition, the reinsurer typically pays a fee of 5%-10% of the

premium to the ceding company to compensate it for the costs of underwriting the policy.

53. Reinsurance may be with an independent third party or it may be between

affiliates or subsidiaries of a parent company.

54. Captive insurance companies are insurance companies established with the

specific objective of insuring risks emanating from their parent group or groups, but they

sometimes also insure risks of the group's customers.

12

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 13 of 66

55. Under US GAAP, when an insurer cedes premium or loss to an affiliate, such

transactions are netted out or “eliminated” in the consolidation process and the premium and

loss is counted and reported only once at the parent or holding company level.

AMTRUST’S CORPORATE STRUCTURE

56. AmTrust operates eleven domestic U.S. insurance subsidiaries that write

policies, take in insurance premiums and pay out losses incurred on those policies.

57. AmTrust owns a Bermuda reinsurance subsidiary, AmTrust International

Insurance, Ltd. (“AII”), which reinsures the bulk of its US insurance subsidiaries’ written

premiums. AmTrust’s U.S. insurance subsidiaries cede at least 70% of written premium and

70% of associated losses to AII.

58. AmTrust also owns an Irish insurance subsidiary, AmTrust (“AIUL“) and a

United Kingdom insurance subsidiary (“AEL”).

59. AmTrust’s Luxembourg operations include AmTrust Capital Holdings Limited

(“ACHL”, a Luxembourg holding company). ACHL in turn, owns nine captive Luxembourg

insurance subsidiaries, each of which had substantial “equalization” reserves. 4

60. AmTrust bought ACHL in March 2009. Then AmTrust purchased 8 more

Luxembourg-domiciled captive reinsurance companies that became subsidiaries of ACHL. In

total, these captive Luxembourg subsidiaries had approximately $688 million of equalization

reserves.

61. An equalization reserve is defined as “an account where an insurance company

deposits funds to use in an emergency. That is, if an insurer finds itself in a position where it

needs to pay more claims than it had anticipated, it may use funds from the equalization

4 Two of the Luxembourg subsidiaries were acquired in December 2012.

13

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 14 of 66

reserve to ensure that it fulfills its contractual obligations. An equalization reserve helps

prevent any potential cash flow problems for the insurance company. It is especially useful in

the event of an act of God, such as a flood or fire, where many policyholders live in the

affected area.” See Farlex Financial Dictionary. © 2012 Farlex, Inc.

62. Under Luxembourg generally accepted accounting principles (“Luxembourg

GAAP”) and statutory insurance regulations equalization reserves may be used to absorb or

reduce the amount of insured losses and are tax deductible. And while their purpose under

Luxembourg GAAP is to provide a cushion in case of an unforeseen catastrophe, for AmTrust

these have been used as, “cookie jar” reserves to manipulate earnings on a regular basis

without any “unforeseen” or catastrophic events.

63. Under International Financial Reporting Standards (“IFRS”) and US generally

accepted accounting standards (“US GAAP”) an insurer may not use equalization reserves to

reduce losses. This is to prevent management from manipulating earnings and to ensure that

investors are provided an accurate view of the current profitability of the insurance operations.

64. Pursuant to a stop-loss agreement, AII agreed to cede up to $100 million of

losses to AmTrust’s Luxembourg subsidiaries annually.

65. Under the stop-loss agreement, AII ceded $62.12 mm, $96.06 mm, and $86.91

mm of insured losses to AmTrust’s Luxembourg subsidiaries in 2010, 2011 and 2012

respectively.

66. Under U.S. GAAP, when AmTrust consolidates the results of its Luxembourg

subsidiaries, these equalization reserves are not permitted to be used to absorb or eliminate the

losses. Thus, any losses incurred by or ceded to the Luxembourg subsidiaries must ultimately

be recognized as losses in AmTrust’s consolidated financial statements. AmTrust has

14

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 15 of 66

represented to the SEC that it does include these losses in its consolidated financial statements,

though AmTrust has never specified how it accounts for these losses or whether these losses

are reclassified as other types of expense through the use of eliminating entries in the

consolidating process.

67. In AmTrust’s SEC reported financial statements, the eleven domestic

subsidiaries, along with the Bermuda, Irish, UK and Luxembourg subsidiaries financial

statements are consolidated. Thus all of the revenue, losses and income from all AmTrust’s

subsidiaries are consolidated and reported in AmTrust’s Form 10-K annually.

MATERIALLY FALSE AND MISLEADING

STATEMENTS ISSUED DURING THE CLASS PERIOD

68. On February 15, 2011, the Company issued a press release announcing its

financial results for the year ended December 31, 2010. For the year, the Company reported

loss adjustment expense of $471.5 million, a loss ratio of 63.2% and a combined ratio of

85.3%. (attached as Exhibit K)

69. In an investor conference call that same day, Zyskind and Pipoly touted

AmTrust’s fiscal 2010 financial performance. In particular, Pipoly and Zyskind discussed the

amount of loss and loss adjustment expense that AmTrust incurred in 2010, as well as its loss

ratio and combined ratio. Zyskind and Pipoly also made in depth statements about the reasons

for AmTrust’s losses, and loss ratios and the trends it was experiencing for these key metrics.

(attached as Exhibit L)

70. On March 15, 2011, the Company filed its annual report for the year ended

December 31, 2010 on Form 10-K with the SEC signed by, among others, Defendants Zyskind

and Pipoly, and reported underwriting income of $109.6 million and loss and loss adjustment

15

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 16 of 66

expense of $471.5 million. AmTrust also reported a loss ratio of 63.2% and a combined ratio

of 85.3%.

71. In addition, the Form 10-K contained signed certifications pursuant to the

Sarbanes- Oxley Act of 2002 ("SOX") by Defendants Zyskind and Pipoly stating that the

financial information contained in the Form 10-K fairly presents, in all material respects, the

financial condition and results of operations of AmTrust, and that they were not aware of any

fraud, whether or not material, that involves management or other employees who have a

significant role in the registrant’s internal control over financial reporting.

72. In the February 15, 2011 press release and the fiscal 2010 10-K, AmTrust

understated loss and loss adjustment expense for fiscal 2010 by $70.97 million because it failed

to properly record $70.97 million of loss and loss adjustment expenses that were reported by its

subsidiaries to State and Bermuda insurance regulators, but were not included and recorded as

loss and loss adjustment expense in AmTrust’s 2010 year-end consolidated financial

statements. As result, AmTrust overstated its underwriting income by $70.97 million and also

understated its loss ratio and combined ratio.

73. The chart below shows compares AmTrust’s 2010 reported figures with the true

figures if it had properly recorded the $70.97 million in loss and loss adjustment expense when

consolidating its financial statements:

16

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 17 of 66

Dollars in thousands

Net Earned Premium Ceding Commission (Related Party)

Loss and loss adjustment expense

Acquisition costs and other underwriting expenses

Underwriting income

As reported As corrected Absolute Percentage 2010 2010 Difference Difference 745,659 745,659 138,261 138,261

471,481 542,451 -70,970 -15.1% 302,809 302,809

109,630 38,660 70,970 283.6%

Underwriting income Key Measures:

Net Loss Ratio 63.2% 72.7% 9.5% 15.1% Net expense Ratio 22.1% 22.1% Combined Ratio 85.3% 94.8% 9.5% 11.2%

74. On February 15, 2012 the Company issued a press release announcing its

financial results for the fiscal year ended December 31, 2011. For the year, AmTrust reported

loss and loss adjustment expense of $678.3 million. It also reported a loss ratio of 65.4% and a

combined ratio of 89%. (attached as Exhibit M)

75. In an investor conference call that same day, Zyskind and Pipoly touted

AmTrust’s fiscal 2011 financial performance. In particular, Pipoly and Zyskind discussed

AmTrust’s loss ratio and combined ratio and the trends for these key measures. (attached as

Exhibit N).

76. On March 15, 2012, the Company filed an annual report for the period ended

December 31, 2011 on a Form 10-K with the SEC signed by, among others, Defendants

Zyskind and Pipoly. The 10-K reported underwriting income of $114.1 million and net loss

and loss adjustment expense of $678.3 million. AmTrust’s fiscal 2011 10-K also reported a net

loss ratio of 65.4% and a combined ratio of 89%.

17

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 18 of 66

77. In addition, the Form 10-K contained signed certifications pursuant to SOX by

Defendants Zyskind and Pipoly stating that the financial information contained in the Form 10-

K fairly presents, in all material respects, the financial condition and results of operations of

AmTrust, and that they were not aware of any fraud, whether or not material, that involves

management or other employees who have a significant role in the registrant’s internal control

over financial reporting.

78. In the February 15, 2012 press release and the fiscal 2011 10-K, AmTrust

understated loss and loss adjustment expense and overstated fiscal 2011 underwriting income

by $102.3 million because it failed to properly record $102.3 million of losses and loss

adjustment expense that were reported by its subsidiaries to State and Bermuda insurance

regulators, but were not included and recorded as loss and loss adjustment expense in its 2011

year-end consolidated financial statements. As a result, AmTrust also understated its loss ratio

and its combined ratio.

79. The chart below shows compares AmTrust’s 2011 reported figures with the true

figures if it had properly recorded the $102.3 million in loss and loss adjustment expense when

consolidating its financial statements:

18

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 19 of 66

Dollars in thousands As reported As corrected Absolute Percentage 2011 2011 Difference Difference

Net Earned Premium 1,036,861 1,036,861 Ceding Commission (Related Party) 153,953 153,953

Loss and loss adjustment expense

678,333

780,633 -102,300 -15.1% Acquisition costs and other underwriting expenses

398,404

398,404 Underwriting income

114,077

11,777

102,300 968.6%

Underwriting income Key Measures:

Net Loss Ratio 65.4% 75.3% 9.9% 15.1% Net expense Ratio 23.6% 23.6% Combined Ratio 89.0% 98.9% 9.9% 11.1%

80. On February 14, 2013, the Company issued a press release announcing its

financial results for the fiscal year ended December 31, 2012. For the year, the Company

reported loss and loss adjustment expense of $922.7 million, a loss ratio of 65.0% and a

combined ratio of 89.5%. (attached as Exhibit O)

81. In an investor conference call that same day, Zyskind and Pipoly touted

AmTrust’s fiscal 2012 financial performance. In particular, Pipoly and Zyskind discussed

AmTrust’s loss for its subsidiaries, as well as on a consolidated basis. Zyskind and Pipoly also

made in depth statements about the reasons for AmTrust’s loss ratios, and the trends it was

experiencing for this key metric. (attached as Exhibit P)

82. On March 1, 2013, the Company filed an annual report for the period ended

December 31, 2012 on a Form 10-K with the SEC signed by, among others, Defendants

Zyskind and Pipoly. The 10-K reported loss and loss adjustment expense of $922.7 million

and underwriting income of $149.5 million. AmTrust’s fiscal 2012 10-K also reported a net

loss ratio of 65.0% and a combined ratio of 89.5%

19

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 20 of 66

83. In addition, the Form 10-K contained signed certifications pursuant to SOX by

Defendants Zyskind and Pipoly stating that the financial information contained in the Form 10-

K fairly presents, in all material respects, the financial condition and results of operations of

AmTrust, and that they were not aware of any fraud, whether or not material, that involves

management or other employees who have a significant role in the registrant’s internal control

over financial reporting.

84. In the February 14, 2013 press release and in the 10-K for fiscal 2012, AmTrust

understated loss and loss adjustment expense and overstated fiscal 2012 underwriting income

by $116.7 million because it failed to properly record $116.7 million of losses and loss

adjustment expense that were reported by its subsidiaries to State and Bermuda insurance

regulators, but were not included and recorded as loss and loss adjustment expense in its 2012

year-end consolidated financial statements. As a result, AmTrust also understated its loss ratio

and its combined ratio.

85. The chart below shows compares AmTrust’s 2012 reported figures with the true

figures if it had properly recorded the $116.7 million in loss and loss adjustment expense when

consolidating its financial statements:

20

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 21 of 66

Dollars in thousands

Net Earned Premium Ceding Commission (Related Party)

As As reported corrected

2012 2012 1,418,852 1,418,852

196,982 196,982

Absolute Percentage Difference Difference

Loss and loss adjustment expense 922,675 1,039,375 Acquisition costs and other underwriting expenses 543,713 543,713

Underwriting income 149,446 32,746

Underwriting income Key Measures:

Net Loss Ratio 65.0% 73.3% Net expense Ratio 24.4% 24.4% Combined Ratio 89.5% 97.7%

-116,700 -12.6%

116,700 456.4%

8.2% 12.6%

8.2% 9.2%

AMTRUST SELLS $115,000,000 OF PREFERRED STOCK

IN A REGISTERED OFFERING

86

On June 5, 2013, AmTrust filed a registration statement and prospectus to offer

and sell 4,600,000 shares of Series A preferred stock at $25.00 per share. On June 10, 2013,

AmTrust completed the offering receiving net proceeds from the offering of $111,377,500.

87. The registration statement and prospectus incorporated by reference AmTrust’s

financial statements filed with the SEC on Form 10-K for fiscal years 2012.

88. The registration statement and prospectus also provided detailed income

statement and balance sheet items for fiscal years 2010 through 2012.

89. The registration statement and prospectus was false and misleading because it

understated loss and loss adjustment expense, overstated underwriting income, and understated

AmTrust’s loss ratios and combined ratios for fiscal years 2010 through 2012 by material

amounts, as more specifically described in paragraphs 73, 79 and 85 above.

90. AmTrust’s individual subsidiaries reported to insurance regulators $289.9

million more loss and loss adjustment expense during fiscal years 2010, 2011 and 2012 than

21

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 22 of 66

AmTrust reported for those fiscal years on a consolidated basis in the registration statement

and prospectus for the Preferred Offering.

91. AmTrust understated loss and loss adjustment expense by $70.97 million in

2010, $102.3 million in 2011 and $116.7 million in 2012 in the registration statement and

prospectus. As a result, AmTrust overstated its underwriting income by the same amounts in

each year and understated its loss ratios by 15.1%, 15.1% and 12.6%, for fiscal 2010, 2011 and

2012 respectively, and understated its combined ratio by 11.2%, 11.2% and 9.2% for fiscal

2010, 2011 and 2012 respectively.

THE TRUTH EMERGES

92. On December 12, 2013, Geoinvesting published a report entitled, “AmTrust

Financial Services: A House of Cards?” The Geoinvesting report is attached as Exhibit J to

this complaint and incorporated herein.

93. The report asserted in relevant part:

It seems suspicious that a company could take on so many different types of risk while beating consensus estimates for 14 consecutive quarters. We find it difficult to believe that AFSI could quickly enter areas where they had no previous experience and at such a pace without ever missing a step. This has led us to take a deeper look into AFSI’s books and accounting.

... it appears that management is ceding/sending losses to offshore captive reinsurance companies it has purchased since 2009, but not disclosing these losses in SEC financial statements as required.

We will show that AFSI appears to be inflating earnings/net equity via offshore entities, making it difficult for regulators to see the complete picture and/or get accurate information. We think that AFSI could be next in line to face regulatory scrutiny.

Summary of Findings

• A cross section of public documents (AFSI SEC filings, Statutory financial filings by AFSI subsidiaries and Credit Rating information) shows that AFSI appears to be excluding losses of wholly-owned subsidiaries in its SEC filings.

22

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 23 of 66

• From 2009 to 2012 we believe that AFSI has not disclosed a total of $276.9 million in losses ceded to Luxembourg subsidiaries.

94. On this news, AmTrust’s common stock share price declined $4.63 per share or

12%, to close at $33.67 per share on December 12, 2013. That same day AmTrust’s Series A

preferred stock share price declined $2.55/share from $21.02/share to close at $18.47/share.

95. AmTrust immediately responded by denying the facts asserted by Geoinvesting.

Zyskind stated: “Recent negative articles that individuals have distributed are false and

misleading and are being distributed with the intention of manipulating the shares of AmTrust

in order to benefit those who own short position in our shares.”

96. Immediately after the Geoinvesting report issued, George Karfunkle, AmTrust’s

Chairman, major shareholder and father in law of Zyskind, along with his wife attempted to

shore up investor confidence by purchasing $13.2 million of AmTrust stock. Unfortunately,

the market did not view Karfunkle’s gesture as significant relative to his wealth (he’s reported

to be a billionaire).

97. On December 14, 2013, analyst Bronte Capital issued a report attempting to

refute Geoinvesting’s assertions that AmTrust was committing fraud. Bronte asserted,

incorrectly, that Geoinvesting’s analysis was flawed.

98. On December 16, 2013, Geoinevsting published a response the Bronte’s

report’s denial that AmTrust committed fraud. Geoinvesting said in part “With regard to

ACHL, we stand by and reassert that AFSI [AmTrust] (via AII) appears to be ceding losses

without ceding any associated premiums to a wholly-owned subsidiary (ACHL) and that those

transactions do not appear to be properly unwound upon consolidation. (attached as Exhibit

Q)

23

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 24 of 66

99. The second Geoinvesting report provided additional analysis, using AII’s

audited financial statements, to show that the $276.9 mm of losses AII ceded to ACHL were

not being consolidated properly in AmTrust’s annual financial statements on Form 10-K.

100. On December 16, 2013, after the close of trading, AmTrust held an investor

conference call specifically to assuage investors’ concerns that it was concealing losses.

Zyskind and Pipoly denied the Geoinvesting report in a conclusory fashion, but failed address

Geoinvesting’s evidence showing that the sum of the losses reported by each AmTrust

subsidiary exceeded the consolidated losses reported in AmTrust’s 10K.

101. The market was unconvinced by AmTrust’s anemic response on December 16

and its failure to address Geoinvesting’s allegations meaningfully. As a result of the second

Geoinvesting report that clarified and provided additional support for the allegations of fraud

and AmTrust’s pathetic response, AmTrust’s share price dropped another $2.54/share (7.2%)

on December 17 and $4.09/share (12.5%) on December 18 or a total of $6.63/share or 20.2%. 5

102. On January 2, 2014, AmTrust announced that it would repurchase $150 million

of its common stock in the open market in an effort to increase its stock price following the

share price drop caused by the Geoinvesting article.

103. AmTrust’s responses and denials had the effect of maintaining the artificial

inflation and to some extent re-inflating its share price resulting from its concealment of the

true amount of its loss and loss adjustment expense.

104. And while Zyskind and Pipoly vehemently denied in investor conference calls

held on December 16, 2013 and February 13, 2014 that AmTrust was concealing losses as

asserted by Geoinvesting, neither Zyskind, Pipoly, nor anyone else has ever adequately

5 No other significant AmTrust news was released between December 16 and December 18, 2013.

24

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 25 of 66

explained how it is possible for the total loss and loss adjustment expense reported by

AmTrust’s subsidiaries to be $289.9 million greater than the amount of loss and loss

adjustment expense reported by AmTrust in its consolidated financial statements filed with the

SEC.

105. AmTrust has previously represented to the SEC in letter dated May 20, 2014

that the proper way to judge the materiality of new financial information to investors is to

evaluate the stock price movement when the information is disclosed to the market and

determine whether there is a “significant market reaction, positive or negative” and whether

AmTrust was required to “field any questions from investors or analysts about the

[disclosures]”. Here, the market’s immediate and severe negative reaction, followed by

numerous investor and analyst inquiries prompting several management responses to the issues

raised in the Geoinvesting reports demonstrates that the information in the Geoinvesting

reports was new and highly material information for investors.

THE EVIDENCE SHOWING AMTRUST HAS CONCEALED LOSSES

106. Insurer companies authorized to do business in the United States and its

territories are required to prepare statutory financial statements in accordance with statutory

accounting principles (“SAP”) and file them annually with State insurance departments.

Statutory Accounting Principles are detailed within the National Association of Insurance

Commissioners (“NAIC”) Accounting Practices and Procedures Manual.

107. AII filed audited financial statements with the Bermuda Monetary Authority,

prepared in accordance with U.S. GAAP. AII is also required to file annual statutory financial

statements in Bermuda.

25

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 26 of 66

108. If an insurance company files false financial reports with a State insurance

department, including understating losses incurred, the insurance department may bring legal

proceedings against the company and its officers and directors, including seeking financial

sanctions and closure, liquidation or sale of the company. The same is true with Bermuda

regulators. Filing false financial reports with a State insurance department can be a crime.

109. The States maintain at the NAIC the world’s largest insurance financial

database, which provides a 30- year history of annual and quarterly filings on more than 5,200

insurance companies. Periodic financial examinations occur on a scheduled basis. 6 State

financial examiners investigate a company’s accounting methods, procedures and financial

statement presentation. These exams verify and validate what is presented in the company’s

annual statement to ascertain whether the company is in good financial standing. When an

examination of financial records shows the company to be financially impaired, the state

insurance department takes control of the company. Aggressively working with financially

troubled companies is a critical part of the regulator’s role. The examination by the state

insurance department is much more detailed and comprehensive than is the scrutiny that the

SEC gives to a public company’s filings.

110. State and Bermuda insurance regulators scrutinize the statutory filings of

insurance companies very closely to ensure that the insurance companies are sufficiently

capitalized and capable of covering expected losses. If an insurer appears to a State insurance

department to be experiencing greater loss than it is financially capable of absorbing and

paying out, the State will take action to close down the insurer, liquidate it, appoint a receiver,

order it to obtain additional capital, find a sufficiently capitalized acquirer, or take such other

6 Onsite exams usually occur at least once every three years.

26

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 27 of 66

measure deemed appropriate to protect the insurance company’s policy holders, creditors and

other stakeholders.

111. Insurers who fail to comply with regulatory requirements are subject to license

suspension or revocation, and states may exact fines for regulatory violations. In a typical year

as many as 300 insurance companies have their licenses suspended or revoked.

112. A.M. Best is a US-based rating agency that focuses on the insurance industry.

Both the United States Securities and Exchange Commission and the National Association of

Insurance Commissioners have designated the company as a Nationally Recognized Statistical

Rating Organization (NRSRO) in the United States. A.M. Best issues financial-strength

ratings measuring insurance companies’ ability to pay claims. It also rates financial instruments

issued by insurance companies, such as bonds, notes, and securitization products

113. Geoinvesting obtained financial information as to the premiums written and

ceded by each of AmTrust’s subsidiaries for the years from 2009 through 2012. 7 The reports

also show the loss and loss adjustment expense incurred for each AmTrust subsidiary for fiscal

years 2010, 2011 and 2012.

114. The chart in ¶ 116 below shows the Net Premium Written (“NPW”), 8 the Net

Earned Premium (“NEP”) 9 and the Net Losses and Loss Adjustment Expense (“Net L/LAE”)

incurred for each of AmTrust’s insurance subsidiaries. The data for the US subsidiaries, AEL,

AIUL and AII were obtained from A.M. Best reports and AII’s audited financial statements.

7 The regulatory filings include Schedule Y filed annually for AmTrust’s Technology Insurance Company – its largest domestic insurer and also audited 2010 financial statements for AII.

8 Net Written Premium is gross written premium less that portion of premium that AmTrust cedes to third party reinsurers under reinsurance agreements. 9 Net Earned Premium is the earned portion of net written premiums.

27

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 28 of 66

The data for ACHL was obtained from the Schedule Y that AmTrust’s Technology Insurance

Company subsidiary files with the National Association of Insurance Commissioners and AII’s

audited financial statements filed with Bermuda regulators.

115. The loss and loss adjustment expense, as well as NPW and NEP, in the financial

reports AmTrust files with State and Bermuda insurance regulators are calculated in the

identical manner that loss and loss adjustment expense, NPW and NEP are calculated under

U.S. generally accepted accounting principles, which AmTrust is obligated to follow when it

consolidates and reports its financial statements with the SEC.

116. The NPW, NPE and Net L/LAE for each subsidiary is shown separately and

then totaled. The total amounts for NPW, NPE and Net L/LAE are then compared to the

amounts the totals for each item that AmTrust reports to the SEC in its annual financial

statements on Form 10-K. This comparison shows that AmTrust failed to report in its

consolidated financial statements $289.9 million of losses that it reported in its statutory

financial statements filed with State and Bermuda insurance regulators.

28

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 29 of 66

Total per

AM Best

and 10K

2012 NPE & LAE US Subs AEL AIUL AII ACHL Sched. Y Consolidated Difference

NPW 487.20 190.08 40.95 934.67 ‐ 1,652.90 1,648.04 (4.86)

NPE 403.10 163.91 34.64 821.37 ‐ 1,423.02 1,418.85 (4.17)

Net L/LAE 291.05 95.03 31.30 535.08 86.91 1,039.37 922.68 (116.70)

Source: AM Best AM Best AM Best AM Best TIC Sched Y

N/A 10K N/A

Total per

AM Best

and 10K

2011 NPE & LAE US Subs AEL AIUL AII ACHL Sched. Y Consolidated Difference

NPW 361.63 172.32 33.09 701.40 ‐ 1,268.44 1,276.60 8.15

NPE 302.05 128.05 29.08 568.70 ‐ 1,027.88 1,036.86 8.98

Net L/LAE 232.25 51.78 26.72 373.83 96.06 780.63 678.33 (102.30)

Source: AM Best AM Best AM Best AM Best TIC Sched Y

N/A 10K N/A

2010 NPE & LAE USSubs

NPW 289.04

NPE 255.37

Net L/LAE 174.31

AEL AIUL AII 95.23 29.72 412.03

67.55 25.47 395.04

28.97 27.52 249.53

ACHL ‐

‐

62.12

Total per

AM Best

& Sched. 10K

Y Consolidated Difference

826.02 827.23 1.21

743.44 745.66 2.22

542.45 471.48 r (70.97)

117. For each fiscal year, the total NPW and NPE from A.M. Best and Schedule Y

match the total NPW and NPE that AmTrust reported in its consolidated financial statements in

its 10K.

118. However, in its 10-Ks for 2010 through 2012, AmTrust reported total Net

L/LAE that was materially lower than the total Net L/LAE that AmTrust’s subsidiaries

reported to State and Bermuda regulators as reported in AM Best and Schedule Y. 10

10 AII’s audited financial statements show $62.1 million of losses being ceded to ACHL and that no premiums were ceded to ACHL by AII. This matches and confirms the accuracy of the Net L/LAE figures reported in the Schedule Y. In addition, the NPW and NPE reported in AII’s audited financial statements, which do not consolidate ACHL, match the NPW and NPE reported by AM Best. This shows that AM Best used the same financial information in AII’s

29

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 30 of 66

119. Thus, AmTrust understated its Net L/LAE in its 10-K by approximately $70.97

million, $102.3 million and $116.7 million for fiscal years 2010, 2011 and 2012 respectively.

120. Had AmTrust reported Net L/LAE in its 10-K in the same amounts as it did in

its State and Bermuda filings, its underwriting income would have been reduced by 65%,

89.7% and 78% in 2010, 2011 and 2012 respectively – all very material reductions in

underwriting income.

121. Given that the NPW and NPE totals from AM Best and Schedule Y for

AmTrust’s subsidiaries match up to the 10-K consolidated totals almost exactly with only an

immaterial difference of between 0.1% and 0.9%, the Net L/LAE totals from AM Best and

Schedule Y should also match the 10-K consolidated totals. However, the Net L/LAE totals

differ by 15.1% in 2010 and 2011 and by 12.1% in 2012.

122. AmTrust therefore understated its Net L/LAE in its 10-K by material amounts.

123. A similar comparison of the balance sheet items Net L/LEA Reserves 11 and Net

Unearned Premium 12 reported in AmTrust’s fiscal 2010 10K against the figures reported for

each AmTrust subsidiary in AM Best and AII’s audited financial statements confirms that

AmTrust is understating the extent of its losses.

audited financial statements when preparing its reports and that it did not include ACHL’s financial statements when reporting the financial statements of AII. 11 Reserves for insurance losses and loss adjustment expenses are established for the unpaid cost of insured events that have occurred as of a point in time. More specifically, the reserves for insurance losses and loss adjustment expenses represent the accumulation of estimates for both reported losses and those incurred but not reported, including claims adjustment expenses relating to direct insurance and assumed reinsurance agreements. 12 Net Unearned Premium is the premium corresponding to the time period remaining on an insurance policy, less that portion ceded to reinsurers under reinsurance agreements. Unearned premiums are proportionate to the unexpired portion of the risk, for which coverage has been sought by the insured party. Thus, it is deemed to have not yet been earned by the insurer. It appears as a liability on the insurer's balance sheet, as it would have to be paid back upon cancellation of the insurance policy.

30

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 31 of 66

124. Net L/LEA Reserves are calculated as: [Loss and Loss Expense Reserves] +

[reinsurance payable] – [Reinsurance Recoverable]. 13

125. The following chart shows how the total of net loss reserves reported by

AmTrust’s subsidiaries are materially greater than the net loss reserves reported by AmTrust

when it consolidates those subsidiaries and reports the results in its Form 10-K filed with the

SEC.

2010 Net L/LAE Reserves Net Unearned Premium

Source:

US Subs AEL AIUL AII ACHL

223.40 20.70 9.90 244.90 93.98

192.09 60.72 25.90 261.08 0.00 AM Best AM Best AM Best AM Best & AII Financials

AII Financials

Total per AM Best 10K & AII Financials Consolidated Difference

592.88 499.45 93.43

539.79 540.01 -0.22 10K

126. Given that the Net Unearned Premiums reported by each subsidiary match the

total Net Unearned Premiums reported in AmTrust’s consolidated financial statements, but the

Net loss and loss adjustment reserves are $93.43 million greater for the unconsolidated

subsidiaries, this provides further evidence that AmTrust is not recognizing the true amount of

its losses in its consolidated financial statement.

127. The amount of AmTrust’s loss and loss adjustment expense, its loss ratios, as

well as its loss and loss adjustment reserves are key financial performance metrics that are

fundamental to the core operations of the Company. Zyskind and Pipoly as CEO and CFO

knew of contemporaneous facts, and had access to and reviewed, the financial reports filed

with State and Bermuda insurance regulators showing that AmTrust’s loss and loss adjustment

13 The loss and loss adjustment reserves and net unearned premium amounts in the financial reports AmTrust files with State and Bermuda insurance regulators is calculated in the identical manner that loss and loss adjustment reserves is calculated under U.S. generally accepted accounting principles which AmTrust is obligated to follow when it consolidates and reports its financial statements filed with the SEC.

31

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 32 of 66

expense was $289.9 million greater for fiscal 2010-2012, than AmTrust reported in its

consolidated financial statements for that same period.

128. As AmTrust’s CEO and CFO respectively, Zyskind and Pipoly would have

reviewed and approved the statutory financial statements of each of AmTrust’s subsidiaries

prior to their being filed with regulators each year. 14 Therefore, each had knowledge that

AmTrust was not reporting all of the loss and loss adjustment expense that it was incurring

each fiscal year.

129. Pipoly, as AmTrust’s CFO, received quarterly and annual internal reports

detailing each AmTrust subsidiary’s loss and loss adjustment expense, as well as its loss ratios.

This further evidences that Pipoly had actual knowledge that AmTrust was not reporting all of

the loss and loss adjustment expense that it was incurring each fiscal year.

GEOINVESTING’S THESIS AS TO THE MECHANISM OF AMTRUST’S

UNDERSTATEMENT OF LOSSES

130. Based on the discrepancies between the total Net L/LAE reported to State and

Bermuda insurance regulators and those totals reported in AmTrust’s 10K for fiscal 2010-

2012, Geoinvesting hypothesized that AmTrust was making these losses “disappear” by ceding

them to its Luxembourg subsidiaries. Geoinvesting believed that ACHL was using its

equalization reserves to absorb the losses (and make them disappear) which is permissible

under Luxembourg GAAP, but not under US GAAP. Since AmTrust’s consolidated financial

statements must comply with US GAAP, the all of the $276.9 million of loss and loss

adjustment expense that is offset by the Luxembourg equalization reserves must be fully

recognized and reported in AmTrust’s consolidated financial statements in its 10-K.

14 Zyskind served as president of Technology Insurance Company and Rochdale Insurance Company.

32

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 33 of 66

131. The reason Geoinvesting believed the Luxembourg subsidiaries accounting was

the source of the “disappearance” is that the losses ceded to ACHL represented 87.5%, 93.9%

and 74.5% of the discrepancy in 2010 through 2012 respectively, together with the fact that

ACHL has the equalization balances that are used to absorb losses and manipulate earnings.

132. AmTrust states that its Bermuda subsidiary, AII, cedes up to $100 million of

loss each year (without ceding associated premium) through a stop-loss agreement. The

$289.9 million of concealed losses from 2010 to 2012 nearly matches the $300 million of loss

that may be ceded to Luxembourg subsidiaries over the same three year period.

133. In addition, the aggregate amount of loss and loss adjustment reserves reported

by AmTrust’s individual subsidiaries to State and Bermuda insurance regulators was $93.43

million greater than the amount AmTrust reported in its consolidated financial statements on

Form 10-K filed with the SEC. The Schedule Y showed that nearly an identical amount of loss

and loss adjustment reserves ($93.98 million) was reported at ACHL – further pointing to the

Luxembourg subsidiaries as the source of the discrepancies.

134. In its motion to dismiss filed with the Court in this action on August 11, 2014

(Docket #33), AmTrust asserted that it had not used the Luxembourg equalization reserves to

absorb or offset the $276.9 mm in losses that AII had ceded to the Luxembourg captives.

Instead, AmTrust judicially admitted that “the Company has not ‘hidden’ any losses, but rather

has properly eliminated a transaction between subsidiaries—losses ceded by AmTrust

Bermuda and assumed by the subsidiaries in Luxembourg—as part of the consolidation

process under GAAP.” (Docket #33, pgs 14-15).

135. While Geoinvesting may have been mistaken as to the accounting mechanism

by which AmTrust fraudulently concealed $289.9 million of loss and loss adjustment expense,

33

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 34 of 66

it correctly identified that AmTrust had been concealing these losses, albeit through a different

more, clever accounting machination described more fully below.

AMTRUST VIOLATED GAAP BY MISSCLASSIFYING ITS LOSS AND LOSS

ADJUSTMENT EXPENSES IN CONSOLIDATING ITS FINANCIAL STATEMENTS

136. GAAP states that “[t]he purpose of consolidated financial statements is to

present, primarily for the benefit of the owners and creditors of the parent, the results of

operations and the financial position of a parent and all its subsidiaries as if the consolidated

group were a single economic entity.” 15 Simply put, consolidation is adding together the

results of individual companies to be presented on a single set of financial statements. “There

is a presumption that consolidated financial statements are more meaningful than separate

financial statements and that they are usually necessary for a fair presentation when one of the

entities in the consolidated group directly or indirectly has a controlling financial interest in the

other entities.” 16

137. All majority-owned subsidiaries (i.e., all entities in which a parent has a

controlling financial interest) 17 are generally required to be consolidated. 18 Consolidation

involves elimination of intra-entity balances and transactions:

In the preparation of consolidated financial statements, intra-entity balances and transactions shall be eliminated. This includes intra-entity open account balances,

15 ASC 810-10-10-1 16 ASC 810-10-10-1 17 “The usual condition for a controlling financial interest is ownership of a majority voting interest, and, therefore, as a general rule ownership by one reporting entity, directly or indirectly, of more than 50 percent of the outstanding voting shares of another entity is a condition pointing toward consolidation. The power to control may also exist with a lesser percentage of ownership, for example, by contract, lease, agreement with other stockholders, or by court decree.” (ASC 810-10-15-8) 18 ASC 810-10-15-10

34

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 35 of 66

security holdings, sales and purchases, interest, dividends, and so forth. As consolidated financial statements are based on the assumption that they represent the financial position and operating results of a single economic entity, such statements shall not include gain or loss on transactions among the entities in the consolidated group. 19

138. Notes to AmTrust’s consolidated financial statements included in its 2010

through 2012 Forms 10-K disclose AmTrust’s accounting policy to eliminate all “[a]ll

significant intercompany transactions and accounts ... in the consolidated financial

statements.”20 The Defendants’ motion to dismiss filed with the Court (Docket #33, pgs 14-

15) asserts “the Company has not ‘hidden’ any losses, but rather has properly eliminated a

transaction between subsidiaries—losses ceded by AmTrust Bermuda and assumed by the

subsidiaries in Luxembourg—as part of the consolidation process under GAAP.” Thus, the

Defendants’ admit that losses of approximately $289.9 million had been “eliminated” in

consolidation and not through other means of accounting.

139. Elimination entries, when properly recorded, do not result in a change to a

company’s net income or cause one type of an expense to appear as another on a consolidated

entity’s financial statements. In other words, elimination entries do not cause losses transferred

from one subsidiary to another to simply disappear. For the most part, elimination entries for

income statement accounts represent reclassification of related amounts recorded on two

different line items by the related subsidiaries. The purpose of such reclassification it to

simply offset income of one consolidated entity (e.g., management fee income) with a related

expense reported by another (e.g., management fee expense). For that reason consolidation

entries have zero net effect on a company’s net income.

19 ASC 810-10-45-1 20 2010 and 2011 Forms 10-K, page F-8 and 2012 Form 10-K, page F-10

35

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 36 of 66

140. The elimination of intercompany premium revenue and loss and loss adjustment

expense should similarly have a zero net effect on AmTrust’s premium revenue and loss, loss

adjustment expense and underwriting income in the consolidated financial statements.

141. For AmTrust, recording of elimination entries for earned premiums and for loss

and loss adjustment expenses, as they relate to reinsurance contracts between consolidated

subsidiaries, would have been unnecessary because premiums ceded by one subsidiary that

have been assumed by another subsidiary are recorded on the same income statement line. The

same is true for loss and loss adjustment expenses.

142. Therefore, during consolidation, there is no need to record elimination entries

for these transactions and the consolidated amounts should be the sum of the earned premiums

and the loss and loss adjustment expenses reported by individual subsidiaries (i.e., the total

should be the sum of its parts). Premium and losses from each insurance policy must be

counted and reported once (and only once) on the consolidated financial statements. In its

consolidated financial statements, AmTrust counted and reported all of the premium revenue

reported by each of its subsidiaries to insurance regulators in its statutory financial statements

as shown in ¶116, however it failed to report in its consolidated financial statements $289.9

mm of loss and loss adjustment expense primarily from its Luxembourg subsidiaries (AII

ceded $62.12 mm, $96.06 mm, and $86.91 mm of insured losses to AmTrust’s Luxembourg

subsidiaries in 2010, 2011 and 2012). That AmTrust failed to include and report in its

consolidated financial statements all of the loss and loss adjustment expense is evidenced by

the chart in (¶116) which lists the premium and losses reported by each subsidiary to insurance

regulators. The premium and losses reported in (¶116) already account for the effect of any

intercompany transactions. Thus, the sum of the premium revenue and losses and loss

36

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 37 of 66

adjustment expense reported in the chart in (¶116) should match the total premium revenue and

loss and loss adjustment expense reported in AmTrust’s consolidated financial statements in its

annual reports on Form 10-K for fiscal years 2010, 2011 and 2012.

143. When, as is the case with AmTrust, the sum of the parts does not equal the

whole, it indicates that the elimination entries have not been recorded properly. AmTrust has

represented that it has used elimination entries in the consolidation process to eliminate the

$289.9 million in loss and loss adjustment expense (rather than simply fraudulently remove

them from the financial statements). If this is true, AmTrust used these elimination entries to

improperly reclassify or misclassify loss and loss adjustment expenses for the Luxemburg

subsidiaries (and other subsidiaries) to appear on other, unrelated, lines in the AmTrust

consolidated income statements for 2010 through 2012. This would convert underwriting

losses into non-underwriting losses, inflate underwriting income, reduce its loss ratio and

combined ratio, and make its insurance operations appear much more profitable. This is a

material violation of GAAP and has caused AmTrust’s financial statements to be materially

false and misleading.

144. The Statement of Financial Accounting Concepts No. 1, (“CON 1”), Objectives

of Financial Reporting by Business Enterprises, states that the goal of financial reporting is to

provide information about an enterprise's financial performance during a period. 21 “The

financial statements are a central feature of financial reporting and are a principal means of

communicating accounting information to those outside an enterprise.” 22 The concept

statement acknowledges that the primary focus of financial reporting is information about an

enterprise's performance provided by measures of earnings and its components rather than cash

21 CON 1 ¶ 42 22 CON 1 ¶ 6

37

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 38 of 66

flows.23 These components, or elements, of financial statements are the building blocks with

which the financial statements are constructed. 24

145. Recognizing the importance of information communicated to investors by the

various components of financial statements, SEC Regulation S-X, Rule 7-04, prescribes 19

elements which are required to be included in an income statement of an insurance company.

Chief among them are revenues and losses:

The purpose of this rule is to indicate the various line items which, if applicable, should appear on the face of the income statements and in the notes thereto filed for persons to whom this article pertains. (See 210.4-01(a).)

REVENUES

1. Premiums. Include premiums from reinsurance assumed and deduct premiums on reinsurance ceded. Where applicable, the amounts included in this caption should represent premiums earned.

* * *

BENEFITS, LOSSES AND EXPENSES

5. Benefits, claims, losses and settlement expenses. 25

146. Regulation S-X, Rule 4-01, states that when information required to be included

in the financial statements is not provided, such financial statements are presumed to be

misleading:

Financial statements should be filed in such form and order, and should use such generally accepted terminology, as will best indicate their significance and character in the light of the provisions applicable thereto. The information required with respect to any statement shall be furnished as a minimum requirement to which shall be added such further material information as is necessary to make the required statements, in the light of the circumstances under which they are made, not misleading.

23 CON 1 ¶ 43 24 CON 6, HIGHLIGHTS 25 46 FR 54335, Nov. 2, 1981, as amended at 57 FR 45293, Oct. 1, 1992; 74 FR 18615, Apr. 23, 2009.

38

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 39 of 66

Financial statements filed with the Commission which are not prepared in accordance with generally accepted accounting principles will be presumed to be misleading or inaccurate, despite footnote or other disclosures, unless the Commission has otherwise provided. 26

147. By concealing $289.9 million of losses incurred in its subsidiaries from 2010 to

2012, and not properly classifying and recording those same losses as loss and loss adjustment

expense in its consolidated financial statements, AmTrust misleadingly represented its

insurance operations as highly profitable, when in fact, they were not.

ADDITIONAL EVIDENCE THAT AMTRUST IS CONCEALING ITS TRUE LOSSES

148. AmTrust is a relative newcomer to the insurance industry, having been

incorporated in 1998. It has been run for the last 9 years by Barry Zyskind who today has a

total of 16 years of experience in the insurance industry.

149. During the past five years it has grown exponentially while reporting loss and

expense ratios that are vastly superior to its competitors – both current and historical.

150. AmTrust claims to miraculously have materially lower loss ratios than its

competitors – many who have been in the industry for fifty or more years.

151. Notwithstanding that AmTrust’s business is “green”, that is relatively new

compared to the rest of the industry, AmTrust has consistently claimed to materially out-

perform the industry by having a loss ratio substantially less than the industry average. A loss

ratio is the ratio of incurred losses to earned premium. It is an important metric as to whether

an insurer is underwriting risk profitably.

26 Regulation S-X, Rule 4-01. (17 CFR §210.4-01, as amended January 4, 2008)

39

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 40 of 66

152. From 2007 through 2012, for its US subsidiaries, AmTrust has consistently had

reported loss ratios well below that of the industry average, resulting in its reporting losses

much lower than had its loss ratio been at the industry average.

Year 2007 2008 2009 2010 2011 2012

Net Earned Premium 446,236 439,097 573,882 745,659

1,036,861 1,418,852

Industry AmTrust Percentage Absolute % Loss Ratio Loss Ratio Difference Difference

67.8% 62.4% 8.0% 5.4%

77.1% 54.3% 29.6% 22.8%

72.0% 57.1% 20.7% 14.9%

73.7% 63.2% 14.2% 10.5%

79.5% 65.4% 17.7% 14.1%

74.3% 65.0% 12.5% 9.3%

Dollar difference

24,097 100,114 85,508 78,294

146,197 131,953

566,163

153. The above chart27 shows that AmTrust has consistently reported much lower

loss as a percentage of net earned policy premium than its competitors. Exhibit F (attached

hereto) presents similar data for fiscal years 2008 through 2012. Exhibit G shows that when

one examines in isolation AmTrust’s domestic loss ratio, it has also been consistently and

suspiciously lower than the industry average.

154. AmTrust has also reported combined ratios that are much lower than the

industry average.

AmTrust

Combined

Year Ratio

2011 89.0%

2012 89.5%

Industry Avg.

Combined

Ratio

107.8%

104.9%

AmTrust

Combined Ratio

as Corrected

for Concealed

Losses

98.9%

97.7%

27 Data from AM Best and SEC filings. Numbers in 000’s. Industry average loss ratios are for U.S. business only. Tower and AmTrust have non-U.S. exposure.

40

Case 1:14-cv-00736-VEC Document 39 Filed 09/08/14 Page 41 of 66

155. But given that insurance underwriting is based on the law of large numbers,

there is absolutely no basis to believe that the workers, products or property that AmTrust

insures will be injured less, break less or be damaged less than those that its competitors insure.

Nor is there any basis to suggest that AmTrust is able to charge more for its policies. On the

contrary, in order to achieve such spectacular growth in gross premiums written, in the last ten

years, AmTrust has consistently been underpricing its policies relative to its competitors.

156. The extent of AmTrust’s failure to select realistic actuarial loss estimates (loss

ratios) and book realistic reserves is quantified and fully appreciated by looking at its stated

reserves at year end 2012, which were $2,426,400,000. Had AmTrust calculated and reported

its loss reserves using the industry average loss ratio during the period 2007-2012, its loss

reserves would have been $2,992,563,000. This means that had AmTrust used the same

industry average loss ratios to calculate its reserves that most of its competitors use, it would