Embed Size (px)

Citation preview

Submitted to: World Bank

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy Final Report

Submitted By: March 2010

The Power of Experience

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report i

Contents

Section Page

Section 1 Executive Summary 1-1 1.1 Introduction .................................................................................................................. 1-1 1.2 Approach ...................................................................................................................... 1-6 1.3 Load Forecast ............................................................................................................... 1-6 1.4 Fuel Supply .................................................................................................................. 1-9 1.5 Project and Technology Analysis .............................................................................. 1-10 1.6 Regional Strategies .................................................................................................... 1-25 1.7 Country Summaries ................................................................................................... 1-26 1.8 Recommendations ...................................................................................................... 1-42

Section 2 Introduction 2-1 2.1 Background .................................................................................................................. 2-1 2.2 Study Team .................................................................................................................. 2-2

Section 3 Approach 3-1 3.1 Approach ...................................................................................................................... 3-1 3.2 Brief Description of Study Steps ................................................................................. 3-1

Section 4 Data 4-1 4.1 Data Collection Process ............................................................................................... 4-1

Section 5 Existing and Planned Generation, Summary of Transmission 5-1 5.1 Existing and Planned Generation Plants ...................................................................... 5-1 5.2 Existing Transmission Systems ................................................................................. 5-14 5.3 Description and Analysis of Power Generation Market ............................................ 5-14

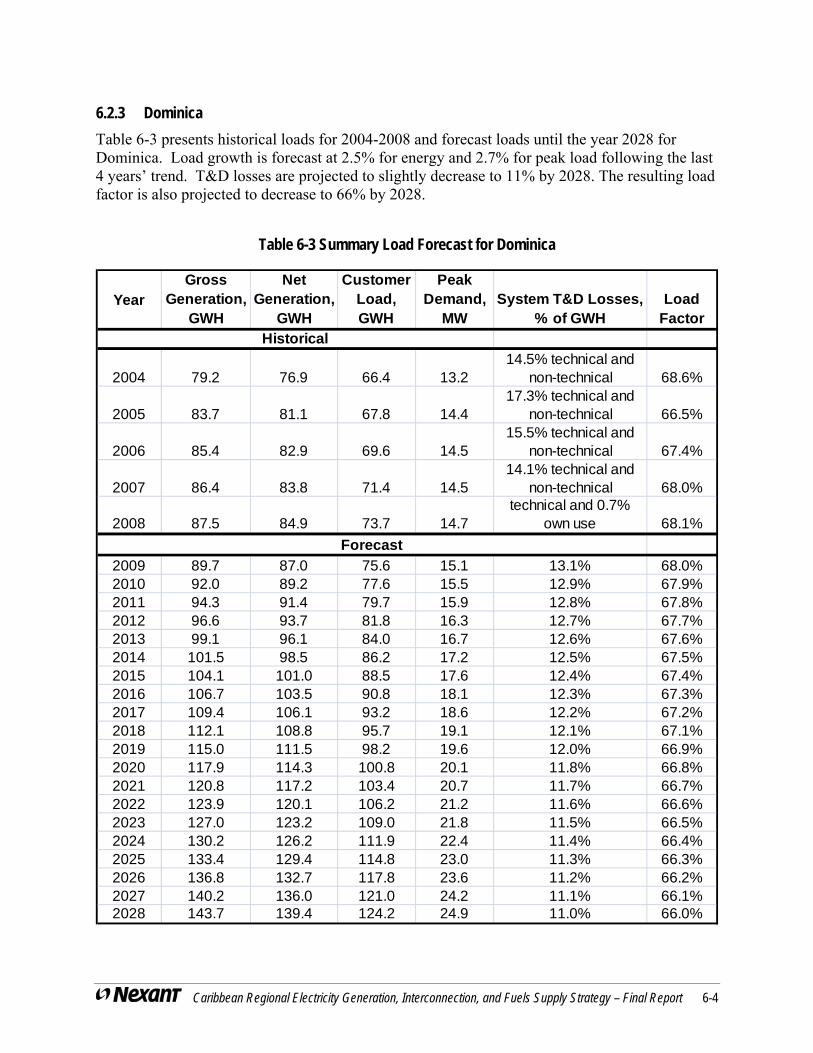

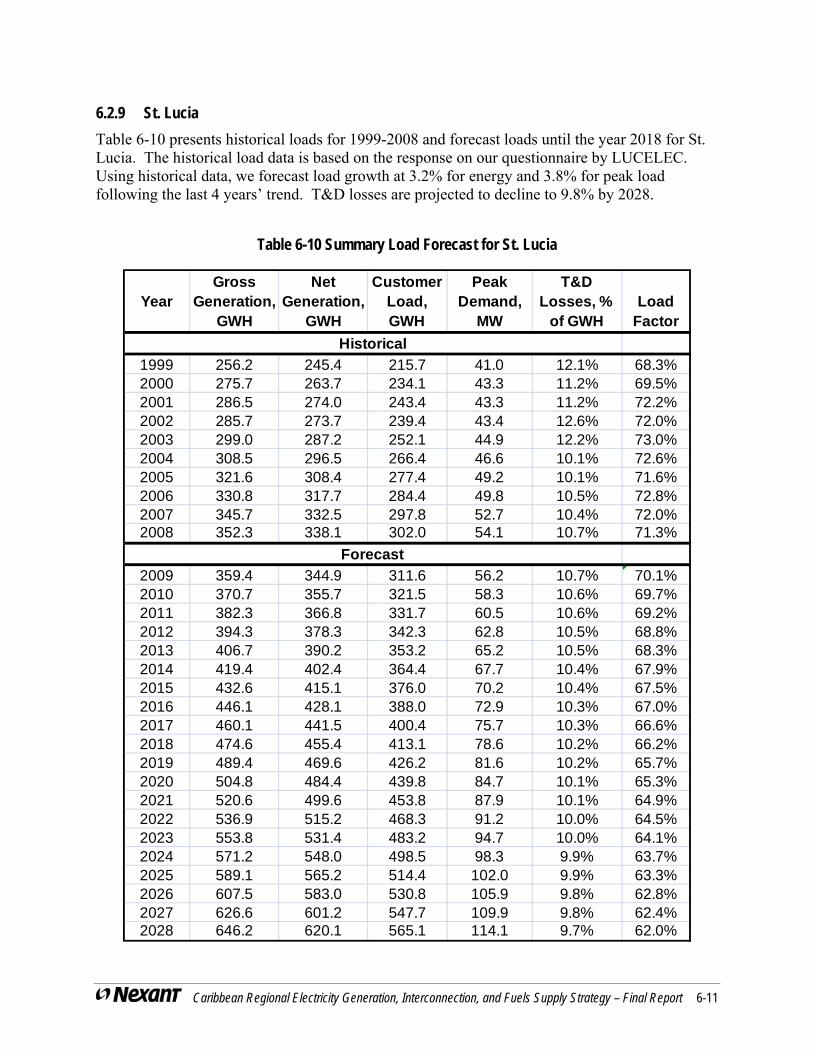

Section 6 Load Forecast 6-1 6.1 Load Forecasting Approach ......................................................................................... 6-1 6.2 Current Demand and Electricity Forecast by Country ................................................. 6-1 6.3 Regional Load Forecast ............................................................................................. 6-15

Section 7 Fuel Supply 7-1 7.1 Existing Fuel Supply .................................................................................................... 7-1 7.2 Potential Fuel Supply Options ..................................................................................... 7-2 7.3 Fuel Storage Options .................................................................................................. 7-23 7.4 Fuel Prices and Projections ........................................................................................ 7-27

Section 8 Generation Technologies and Expansion Options 8-1 8.1 Regional Overview ...................................................................................................... 8-1 8.2 Fossil Fuel Technologies – Costs and Performance .................................................... 8-4 8.3 Renewable Energy Technologies – Power Plant Costs and Performance ................. 8-11 8.4 Renewable Technologies – Resource Availability .................................................... 8-32 8.5 Upgrade and Retrofit of Existing Units ..................................................................... 8-38 8.6 Renewable Energy Projects ....................................................................................... 8-39

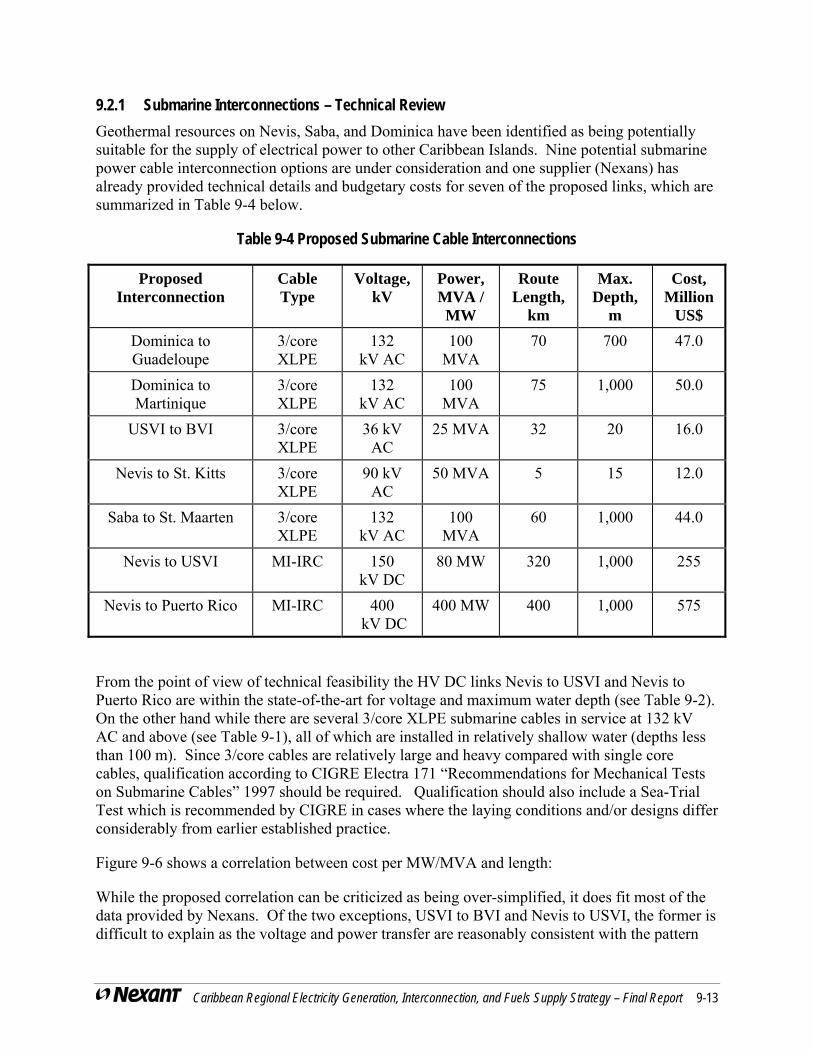

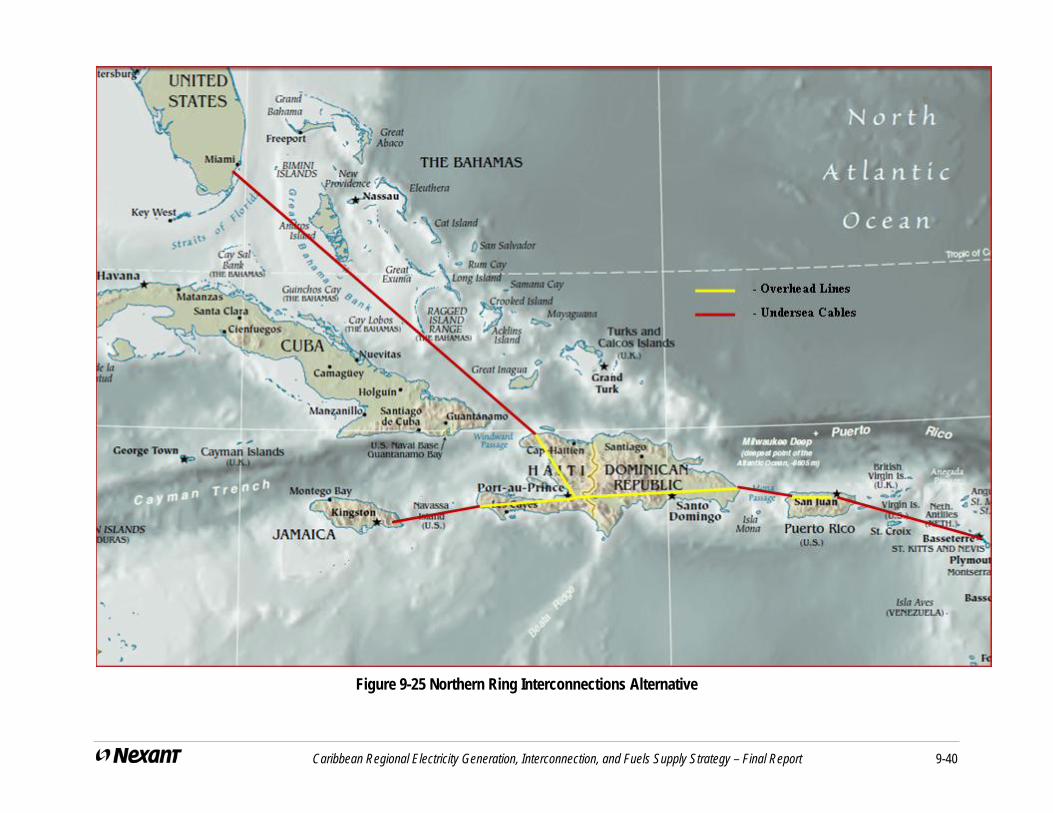

Section 9 Submarine Cables and Interconnection Options 9-1 9.1 Overview of Submarine Cables ................................................................................... 9-1 9.2 Existing/Proposed Sub-regional Interconnection Options ......................................... 9-12 9.3 Northern Ring Interconnection .................................................................................. 9-36

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report ii

Section 10 Study Analytical Approach 10-1 10.1 Overview of Analytical Procedures ........................................................................... 10-1 10.2 Screening Analysis Approach .................................................................................... 10-1 10.3 Approach for Developing Scenarios .......................................................................... 10-5 10.4 Power System Expansion Planning and Analysis Approach ..................................... 10-6

Section 11 Screening Analysis Results 11-1 11.1 Fossil Fuels ................................................................................................................ 11-1 11.2 Screening Curves for Individual Islands .................................................................... 11-5 11.3 The Impact of CO2 “Costs” ..................................................................................... 11-20

Section 12 Scenarios 12-1 12.1 Base Case Scenario .................................................................................................... 12-1 12.2 Fuel Scenario ............................................................................................................. 12-2 12.3 Interconnection/Renewable Scenario ......................................................................... 12-2 12.4 Integrated Scenario .................................................................................................... 12-3

Section 13 Scenario Analysis Results 13-1 13.1 Base Case Scenario Summary ................................................................................... 13-2 13.2 Fuel Scenario ............................................................................................................. 13-6 13.3 Interconnection/Renewable Scenario ......................................................................... 13-9 13.4 Integrated Scenario .................................................................................................. 13-13

Section 14 Study Results Evaluation 14-1 14.1 Comparison of Scenario Results ................................................................................ 14-1 14.2 Recommended Development Scenario ...................................................................... 14-4

Section 15 Conclusions and Recommendations 15-1 15.1 Conclusions ................................................................................................................ 15-1 15.2 Recommendations ...................................................................................................... 15-6

Attachment A provides detailed scenario analysis results Attachment B provides a discussion of submarine power cable reliability Attachment C provides a discussion of submarine power cable repair procedures

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report iii

Table Page

Acronyms and Abbreviations ...................................................................................................... viii Table 1-1 Net Peak Demand Load Forecast (MW) ..................................................................... 1-7 Table 1-2 Net Generation Forecast (GWh) .................................................................................. 1-8 Table 1-3 Fuel Prices Based on Yearly Demand 2014-2028 ....................................................... 1-9 Table 1-4 Scenario NPV Cost Differences - Base Case Minus Other Scenario Costs (million

US$) ................................................................................................................................... 1-26 Table 5-1 Fuels, Fuel Types, and Where the Fuel Prices Apply ................................................. 5-2 Table 5-2 Existing Generating Units ........................................................................................... 5-3 Table 5-3 Planned Generating Units ............................................................................................ 5-9 Table 5-4 Transmission System Frequency and Highest Voltages ........................................... 5-14 Table 6-1 Summary Load Forecast for Antigua and Barbuda ..................................................... 6-2 Table 6-2 Summary Load Forecast for Barbados ........................................................................ 6-3 Table 6-3 Summary Load Forecast for Dominica ....................................................................... 6-4 Table 6-4 Summary Load Forecast for Dominican Republic ...................................................... 6-5 Table 6-5 Summary Load Forecast for Grenada .......................................................................... 6-6 Table 6-6 Summary Load Forecast for Haiti ............................................................................... 6-7 Table 6-7 Summary Load Forecast for Jamaica .......................................................................... 6-8 Table 6-8 Summary Load Forecast for St. Kitts .......................................................................... 6-9 Table 6-9 Summary Load Forecast for Nevis ............................................................................ 6-10 Table 6-10 Summary Load Forecast for St. Lucia ..................................................................... 6-11 Table 6-11 Summary Load Forecast for St. Vincent and Grenadines ....................................... 6-12 Table 6-12 Summary Load Forecast for Martinique ................................................................. 6-13 Table 6-13 Summary Load Forecast for Guadeloupe ................................................................ 6-14 Table 6-14 Net Peak Demand Load Forecast (MW) ................................................................. 6-16 Table 6-15 Net Generation Forecast (GWh) .............................................................................. 6-17 Table 7-1 Fuels Used by Country ................................................................................................ 7-1 Table 7-2 Pipeline Transportation Costs – All Islands Connected .............................................. 7-9 Table 7-3 Pipeline Transportation Costs – St. Lucia Not Connected ........................................ 7-10 Table 7-4 Pipeline Transportation Costs – St. Lucia and Guadeloupe Not Connected ............. 7-10 Table 7-5 Pipeline Transportation Costs – Barbados is Only Island Connected ....................... 7-11 Table 7-6 Mid-scale LNG Comparison ..................................................................................... 7-17 Table 7-7 Regional Petroleum Consumption ............................................................................ 7-25 Table 7-8 Summary of Economic Analysis ............................................................................... 7-26 Table 7-9 Transportation Cost Parameters ................................................................................ 7-28 Table 7-10 EIA US Fuel Prices, $/GJ ........................................................................................ 7-30 Table 7-11 Fuel Prices Based on Yearly Demand 2014-2028 ................................................... 7-30 Table 7-12 Yearly Prices for Fuels for Caribbean Power Plants ............................................... 7-31 Table 8-1 Typical Performance and Cost Estimates for Conventional Coal Plants .................... 8-5 Table 8-2 Typical Performance And Cost Estimates for CFB Plants .......................................... 8-6 Table 8-3 Typical Performance and Cost Estimates for Simple Cycle Combustion Turbines .... 8-7 Table 8-4 Typical Performance And Cost Estimates for Combined Cycle Plants ...................... 8-9 Table 8-5 Typical Performance And Cost Estimates for Diesel Engines .................................. 8-10 Table 8-6 Wind Class and Corresponding Wind Speed and Wind Power ................................ 8-13 Table 8-7 Typical Performance And Cost Estimates for Wind Turbines .................................. 8-15

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report iv

Table 8-8 Typical Performance And Cost Estimates for Geothermal Plants ............................ 8-19 Table 8-9 Typical Performance And Cost Estimates for Small Hydro Plants ........................... 8-20 Table 8-10 Typical Performance And Cost Estimates for Solar Trough Plants ........................ 8-27 Table 8-11 Typical Performance And Cost Estimates for PV Systems ..................................... 8-30 Table 8-12 Typical Performance And Cost Estimates for Biomass and LFG Plants ................ 8-31 Table 8-13 Renewable Resource Estimate for the Caribbean Region ....................................... 8-36 Table 9-1 List of Some of the World’s Major AC Submarine Cable Links ................................ 9-4 Table 9-2 List of Some of the World’s Major DC Submarine Cable Links ................................ 9-6 Table 9-3 Submarine Cable Project Costs ................................................................................... 9-9 Table 9-4 Proposed Submarine Cable Interconnections ............................................................ 9-13 Table 9-5 Cost Comparison – Nexans Estimates and Historical Formula ................................. 9-15 Table 9-6 Basic Data and Cost Estimates for Submarine Cable Interconnections .................... 9-37 Table 11-1 Added Cost of Fuels Based on CO2 Cost of US$50/tonne ................................... 11-21 Table 11-2 Impact of CO2 Costs on Fuel Costs ...................................................................... 11-21 Table 13-1 Base Case Production Cost Summary (Million 2009 US$) .................................... 13-5 Table 13-2 Base Case Investment Cost Summary (Million 2009 US$) .................................... 13-5 Table 13-3 Fuel Scenario Production Cost Summary (Million 2009 US$) ............................... 13-8 Table 13-4 Fuel Scenario Investment Cost Summary (Million 2009 US$)............................... 13-8 Table 13-5 Interconnection/Renewable Scenario Production Cost Summary (Million 2009 US$)

.......................................................................................................................................... 13-11 Table 13-6 Interconnection/Renewable Scenario Investment Cost Summary (Million 2009 US$)

.......................................................................................................................................... 13-11 Table 13-7 Interconnection/Renewable Scenario Interconnection Cost Summary (Million 2009

US$) ................................................................................................................................. 13-12 Table 13-8 Integrated Scenario Production Cost Summary (Million 2009 US$) .................... 13-15 Table 13-9 Integrated Scenario Investment Cost Summary (Million 2009 US$) ................... 13-15 Table 13-10 Integrated Scenario Interconnection Cost Summary (Million 2009 US$) .......... 13-16 Table 14-1 Scenario NPV Cost Comparison (Million US$) ..................................................... 14-1 Table 14-2 Scenario NPV Cost Differences - Base Case Minus Other Scenario Costs (Million

US$) ................................................................................................................................... 14-2 Table 14-3 Investment Requirement, 2009 US$ Million, by Scenario ...................................... 14-5 Table 14-4 Production Cost Summary, 2009 US$ Million, by Scenario................................... 14-6 Table 15-1 Fuel Prices Based on Yearly Demand 2014-2028 ................................................... 15-1 Table 15-1 Scenario NPV Cost Differences - Base Case Minus Other Scenario Costs (Million

US$) ................................................................................................................................... 15-6

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report v

Figure Page

Figure 1-1 Caribbean Regional Map ............................................................................................ 1-3 Figure 1-2 Countries Included in the Study ................................................................................. 1-4 Figure 1-3 Other Relevant Countries Addressed in the Study ..................................................... 1-5 Figure 1-4 Fossil LCL for Dominican Republic ........................................................................ 1-11 Figure 1-5 Other Options for Dominican Republic ................................................................... 1-12 Figure 1-6 Eastern Caribbean Gas Pipeline (ECGP) Proposed Route ....................................... 1-14 Figure 1-7 Dominica Interconnections ...................................................................................... 1-16 Figure 1-8 Nevis – Puerto Rico and Nevis – US Virgin Islands Interconnections .................... 1-17 Figure 1-9 Saba – St. Maarten Interconnection ......................................................................... 1-18 Figure 1-10 Haiti – Dominican Republic Interconnection ........................................................ 1-19 Figure 1-11 United States (Florida) – Cuba Interconnection ..................................................... 1-20 Figure 1-12 Northern Ring Set of Interconnections .................................................................. 1-21 Figure 1-13 Northern Ring Interconnections Alternative .......................................................... 1-22 Figure 1-14 Distillate LCL vs. Renewable Energy Options ...................................................... 1-24 Figure 1-15 Barbados LCL vs. Renewable Energy Options ...................................................... 1-24 Figure 7-1 Coal Transportation Costs .......................................................................................... 7-5 Figure 7-2 LNG Transportation Costs ....................................................................................... 7-16 Figure 7-3 CNG Transportation Costs ....................................................................................... 7-22 Figure 8-1 Existing Generation Technologies ............................................................................. 8-1 Figure 8-2 Capital Cost Estimate for Power Projects in US ........................................................ 8-3 Figure 8-3 Wind Turbine Components ..................................................................................... 8-14 Figure 8-4 Output Profile – Wind Speed vs. kW output for Gamesa G58 Turbine .................. 8-15 Figure 8-5 Flash Steam Geothermal Power Plant Schematic .................................................... 8-18 Figure 8-6 Parabolic Trough Collector Plant ............................................................................. 8-21 Figure 8-7 10 MW Solar 2 Project near Barstow, CA ............................................................... 8-22 Figure 8-8 Ausra and Sky Fuel CLFR Lay Outs ....................................................................... 8-24 Figure 8-9 Parabolic Dish with Stirling Engine ......................................................................... 8-25 Figure 8-10 Two Tank Thermal Storage System ....................................................................... 8-26 Figure 8-11 Typical PV Solar Module....................................................................................... 8-29 Figure 8-12 Typical PV System Configuration ......................................................................... 8-29 Figure 8-13 Least Cost Line for Distillate Fuel ......................................................................... 8-42 Figure 8-14 Distillate LCL vs. Renewable Energy Options ...................................................... 8-43 Figure 8-15 Fossil Least Cost Line for Dominica and Nevis with No Geothermal .................. 8-47 Figure 8-16 Fossil Least Cost Line for Dominica and Nevis vs. Geothermal ........................... 8-48 Figure 9-1 3-Core XLPE Submarine Cable ................................................................................. 9-2 Figure 9-2 Photograph of a Sample of the 525 kV Vancouver Island Cable .............................. 9-3 Figure 9-3 Transmission Cable System Selection Criteria for Various Cable Types and

Capacities (Courtesy of Prysmian Cables and Systems). .................................................... 9-8 Figure 9-4 HV DC MI-IRC Cable ............................................................................................. 9-10 Figure 9-5 Correlation Between Cable Length and Cost (2009 $) ........................................... 9-11 Figure 9-6 Correlation between Cost per MW/MVA and Length ............................................. 9-14 Figure 9-7 Fossil Least Cost Line for St. Kitts vs. Geothermal Plant / Submarine Interconnection

............................................................................................................................................ 9-16 Figure 9-8 Fossil Least Cost Line for Martinique with No Geothermal .................................... 9-18

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report vi

Figure 9-9 Fossil Least Cost Line for Martinique and Guadeloupe vs. Geothermal Plant / Submarine Interconnection at 100 MW Each .................................................................... 9-19

Figure 9-10 Fossil Least Cost Lines for Martinique and Guadeloupe vs. Geothermal Plant / Submarine Interconnection at 50 MW Each ...................................................................... 9-20

Figure 9-11 Fossil Least Cost Line for Guadeloupe with No Geothermal ................................ 9-21 Figure 9-12 Fossil Least Cost Lines for Guadeloupe vs. Geothermal Plant / Submarine

Interconnection at 100 MW ............................................................................................... 9-22 Figure 9-13 Fossil Least Cost Line for Guadeloupe vs. Geothermal Plant / Submarine

Interconnection at 50 MW ................................................................................................. 9-23 Figure 9-14 HFO Steam Plant for Puerto Rico vs. Fossil Fuel Options for Florida and

Interconnection at 400MW ................................................................................................ 9-24 Figure 9-15 Fossil Fuel Option for USVI vs. Geothermal Plant / Submarine Interconnection . 9-25 Figure 9-16 Fossil Fuel Option for Sint Maarten vs. Geothermal plant / Submarine

Interconnection at 100MW ................................................................................................ 9-27 Figure 9-17 Fossil Fuel Option for Cuba vs. Fossil Plants / Submarine Interconnection at 400

MW .................................................................................................................................... 9-28 Figure 9-18 Fossil Fuel Option for Haiti vs. Fossil Plants / Land Interconnection at 130 MW 9-30 Figure 9-19 Dominica Interconnections .................................................................................... 9-31 Figure 9-20 Nevis – Puerto Rico and Nevis – US Virgin Islands Interconnections .................. 9-32 Figure 9-21 Saba – St. Maarten Interconnection ....................................................................... 9-33 Figure 9-22 Haiti – Dominican Republic Interconnection ........................................................ 9-34 Figure 9-23 United States (Florida) – Cuba Interconnection ..................................................... 9-35 Figure 9-24 Northern Ring Set of Interconnections .................................................................. 9-39 Figure 9-25 Northern Ring Interconnections Alternative .......................................................... 9-40 Figure 10-1 Cost Representation for Screening Analysis Method ............................................ 10-2 Figure 10-2 Illustrative Development of Least Cost Line (LCL) .............................................. 10-3 Figure 10-3 Least Cost Line Plus Renewable Energy Resources .............................................. 10-4 Figure 11-1 Screening Curves for Distillate-fueled Technologies ............................................ 11-2 Figure 11-2 Distillate vs. HFO Cost Comparison ...................................................................... 11-3 Figure 11-3 Screening Curves for Coal-fueled Technologies ................................................... 11-5 Figure 11-4 Fossil LCL and Wind for Antigua and Barbuda, Grenada, and St. Vincent and the

Grenadines ......................................................................................................................... 11-6 Figure 11-5 Fossil LCL for Barbados ........................................................................................ 11-7 Figure 11-6 Other Options for Barbados ................................................................................... 11-8 Figure 11-7 Fossil LCL for Dominican Republic ...................................................................... 11-9 Figure 11-8 Other Options for Dominican Republic ............................................................... 11-10 Figure 11-9 Fossil LCL for Guadeloupe .................................................................................. 11-11 Figure 11-10 Other Options for Guadeloupe ........................................................................... 11-12 Figure 11-11 Fossil LCL for Haiti ........................................................................................... 11-13 Figure 11-12 Other Options for Haiti ...................................................................................... 11-14 Figure 11-13 Fossil LCL for Jamaica ...................................................................................... 11-15 Figure 11-14 Other Options for Jamaica ................................................................................. 11-16 Figure 11-15 Fossil LCL for Martinique ................................................................................. 11-17 Figure 11-16 Other Options for Martinique............................................................................. 11-18 Figure 11-17 Fossil LCL for St. Lucia..................................................................................... 11-19 Figure 11-18 Other Options for St. Lucia ................................................................................ 11-20

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report vii

Figure 11-19 CO2 Cost Impact on Islands Using Only Distillate ........................................... 11-22 Figure 11-20 CO2 Cost Impact on Islands with Coal on Fossil LCL ...................................... 11-23 Figure 11-21 CO2 Cost Impact on Islands with Gas on Fossil LCL ....................................... 11-25 Figure 11-22 CO2 Cost Impact on Country with Lowest Non-gas Fuel Prices ...................... 11-26

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report viii

Acronyms and Abbreviations

ABS American Bureau of Shipping AC Alternating current ADO Automotive diesel oil APC Antigua Power Company APUA Antigua Public Utility Authority ASME American Society of Mechanical Engineers Aus Australia BL&P Barbados Light and Power BPD Barrels per day CC, CCGT Combined cycle gas turbine CFB Circulating fluidized bed CHP Combined heat and power CLFR Compact linear Fresnel reflector CNG Compressed natural gas CO Carbon monoxide CO2 Carbon dioxide Cogen Cogeneration CSP Concentrating solar power CT Combustion turbine DC Direct current DNV Det Norske Veritas DOMLEC Dominica Electricity Services Limited DR Dominican Republic ECGP Eastern Caribbean Gas Pipeline ECGPC Eastern Caribbean Gas Pipeline Company EDF, EdF Electricite de France EDH, EdH Electricite d'Haiti EGS Engineered geothermal systems EHV Extra high voltage EIA Energy Information Administration EIR Environmental impact report EPR Ethylene-propylene- rubber EPRI Electric Power Research Institute ESMAP Energy Sector Management Assistance Program ESP Electrostatic precipitator FGD Flue gas desulfurization Fin Finland FSRU Floating Storage and Re-gasification Units Ger Germany GJ Gigajoule GP Gas pipeline GRENLEC Grenada Energy Services Ltd. GT Gas turbine

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report ix

GWH, GWh Gigawatt-hour HDR Hot dry rocks HFO Heavy fuel oil HHV Higher heating value HPFF High pressure fluid filled HRSG Heat recovery steam generator HTF Heat transport fluid HV High voltage Hz Hertz (cycles per second) IBRD International Bank for Reconstruction and Development IC Internal combustion ICGPL Intra Caribbean Gas Pipeline Limited IDA International Development Association ISO International Organization for Standardization JPS Jamaica Public Service kcmil Thousand circular mils kg Kilogram kJ Kilojoule km Kilometer kV Kilovolt kW Kilowatt kWh Kilowatt-hour LCL Least cost line LFG Landfill gas LHV Lower heating value LNG Liquefied natural gas LSD Low speed diesel LUCELEC St. Lucia Electricity Services Ltd. m Meter MEM Ministry of Energy and Mining (Jamaica) MI Mass-impregnated MI-IRC MI cable with and integral return conductor MMBTU Million British Thermal Units MMscf Million standard cubic feet MMscfd Million standard cubic feet per day mm2 Square millimeters MOU Memorandum of understanding MPa Megapascal (1 MPa = pressure about equal to 145 pounds/square

inch) mph Miles per hour MSD Medium speed diesel Mt Metric ton Muni Municipal MVA Megavolt-ampere MW Megawatt MWe Megawatts electric

Contents

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report x

MWt Megawatts thermal NGC National Gas Company of Trinidad & Tobago NL Netherlands Nor Norway NOx Nitrogen oxide (NO or NO2) NPV Net present value NREL National Renewable Energy Laboratory O&M Operations and maintenance PC Pulverized coal PV Photovoltaic ROC Republic of China ROV Remotely operated vehicle SCFF Self-contained, fluid-filled SCGT Simple cycle gas turbine SCR Selective catalytic reduction SEGS Solar electric generating system SNCR Selective non-catalytic reduction SOx Sulfur dioxide and sulfur trioxide SSD Slow speed diesel Swe Sweden TES Thermal energy storage TOR Terms of Reference UK United Kingdom USA United States of America US DOE United States Department of Energy USVI United States Virgin Islands V Volt VINLEC St. Vincent Electricity Service Ltd. VSC Voltage source control W Watt WIPC West Indies Power Company XLP Special cross-linked polymeric insulated DC cables XLPE Cross-linked polyethylene 3/c XLPE 3-core XLPE cable (i.e., each of the three phases is in one of three

separate conductors within a common armor) yr Year

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-1

Section 1 Executive Summary

1.1 INTRODUCTION

The objective of this Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy (the Study) is to analyze the availability of technically and financially sound regional and sub-regional energy solutions for power generation rather than specific energy solutions for each Caribbean country.

The energy solutions involve new fuels or fuel transport modes (pipeline gas, CNG, LNG, coal), new energy resources for power generation (primarily wind and geothermal), and new electrical interconnections among islands, none of which are presently interconnected. The immediate goal of studying these areas was to reduce the Caribbean islands’ dependence on high price imported distillate and HFO. A related goal was that solutions would emerge that reduced costs, reduced environmental impacts, and increased the integration of the Caribbean islands. The entire Caribbean region is presented on Figure 1-1.

We note at the outset that we have identified no truly regional energy solutions, not even one covering the nine countries of primary emphasis mentioned in the second paragraph below. We have identified and analyzed, to varying degrees of detail, 11 submarine cable electrical interconnections between two countries and one land-based interconnection. Some of these two-country sub-regional interconnections are part of larger schemes involving three or more countries. The only sub-regional fuel project the Study evaluated was the five-country Eastern Caribbean Gas Pipeline (ECGP). Schemes involving LNG or CNG implicitly or explicitly rely on some common facilities when more than one country is a user, but in that sense they are not different from the current delivery modes for distillate and heavy fuel oil (HFO) and were analyzed on a country-by-country basis.

It is interesting that the goal of reducing dependence on high price imported oil products and the goal of reducing environmental impacts and increasing the integration of the region turned out to be complementary. The most direct benefit of an interconnection comes when one country has a source of low cost power and its neighbor does not. The three lowest cost resources for operation at capacity factors above about 30% are renewables: geothermal, wind (including the cost of backup generation), and small hydro. This assumes that high quality sites can be identified and acquired. Geothermal is the source of generation and drives the benefits for many of the interconnections. Thus geothermal on a local and sub-regional basis, and wind on a local basis, provide a path toward a less oil-dependent, lower cost, lower environmental impact, more sustainable future.

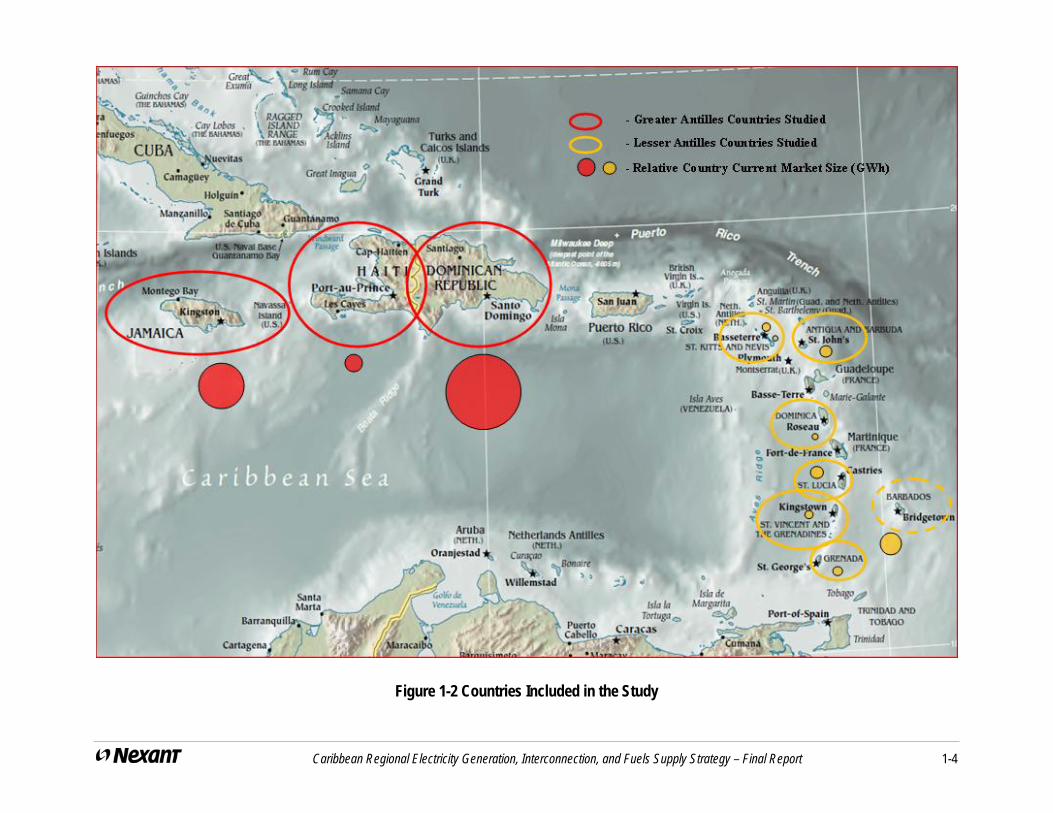

The primary emphasis of the Study is on the nine countries in the Caribbean eligible for support from the International Development Association (IDA) and/or the International Bank for Reconstruction and Development (IBRD). Those countries are presented, together with their relative electricity market share, on Figure 1-2. These nine include:

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-2

Six small countries in the Lesser Antilles: St. Lucia, St. Vincent and the Grenadines, Grenada, Antigua and Barbuda, St. Kitts and Nevis, and Dominica, total combined population about 600,000

Three countries located on two of the four islands in the Greater Antilles: Haiti and the Dominican Republic, both on the island Hispaniola, and Jamaica, total population about 22,000,000

The Study also considered other relevant countries, presented on Figure 1-3, that might be part of a regional energy solution. In addition to the nine countries mentioned above, we visited or obtained significant data on Barbados1, Trinidad and Tobago, and Martinique; somewhat less on Guadeloupe; and cursory information on Puerto Rico, Sint Maarten, and Cuba. We also obtained cursory information on power generation in Florida.

1 Barbados was addressed in more details as par of the Eastern Caribbean Gas Pipeline project analysis.

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-3

Figure 1-1 Caribbean Regional Map

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-4

Figure 1-2 Countries Included in the Study

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-5

Figure 1-3 Other Relevant Countries Addressed in the Study

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-6

1.2 APPROACH

Our approach included the following main steps:

Collect the foundation data needed to conduct the work

Prepare a peak and energy demand forecast for each country and the Study countries as a whole

Forecast fuel costs for all fuels used, including pipeline gas, LNG, CNG, and coal

Estimate fuel transportation costs for each fuel to each country and determine effective fuel price

Determine the performance and cost parameters of all existing power generation units

Determine the performance and cost parameters of power generation units suitable for meeting future demand

Evaluate the cost and performance parameters for power generation from renewable energy, and estimate the availability of renewable energy resources

Evaluate submarine cable technology

Identify and evaluate submarine cable and land-based transmission interconnections

Develop scenarios that include a range of approaches to regional power generation, and combine the most attractive components in an proposed scenario

Report on and present the results (such as in this report)

1.3 LOAD FORECAST

Tables 1-1 and 1-2 provides peak and energy demand forecasts for each country / island and for the region as a whole.

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Interim Report 1-7

Table 1-1 Net Peak Demand Load Forecast (MW)

YearAntigua

and Barbuda

Barbados DominicaDominican Republic

Grenada Haiti Jamaica St. Kitts Nevis St. LuciaSt. Vincent

and Grenadines

Martinique Guadeloupe Total

2009 54 170 15 2,353 31 226 680 29 10 56 27 242 250 4,142

2010 57 176 15 2,447 33 237 707 30 10 58 28 247 256 4,302

2011 60 182 16 2,544 34 249 736 31 11 61 30 255 263 4,472

2012 63 188 16 2,640 36 261 767 32 11 63 32 263 269 4,643

2013 65 195 17 2,727 38 274 799 33 12 65 35 272 276 4,808

2014 67 201 17 2,803 40 288 832 35 13 68 37 281 284 4,965

2015 69 208 18 2,896 42 303 867 36 13 70 40 290 291 5,143

2016 71 216 18 2,992 45 318 904 37 14 73 42 297 298 5,324

2017 73 223 19 3,091 47 334 943 38 15 76 45 303 305 5,512

2018 75 231 19 3,194 50 350 983 40 16 79 48 310 313 5,708

2019 77 239 20 3,300 52 368 1,026 41 17 82 52 317 321 5,911

2020 80 247 20 3,409 55 386 1,071 43 18 85 55 324 329 6,121

2021 82 256 21 3,522 58 405 1,116 44 19 88 59 331 337 6,339

2022 85 265 21 3,638 61 426 1,165 46 20 91 63 339 346 6,565

2023 87 274 22 3,758 64 447 1,214 47 21 95 68 346 354 6,798

2024 90 284 22 3,882 68 469 1,267 49 23 98 72 354 363 7,041

2025 92 294 23 4,010 72 493 1,322 51 24 102 77 362 372 7,293

2026 95 304 24 4,143 75 517 1,379 52 25 106 83 370 381 7,555

2027 98 314 24 4,280 80 543 1,439 54 27 110 88 378 391 7,827

2028 101 325 25 4,421 84 570 1,502 56 29 114 94 387 400 8,109

Growth Rate

3.3% 3.5% 2.7% 3.4% 5.4% 5.0% 4.3% 3.5% 5.9% 3.8% 6.9% 2.5% 2.5% 3.6%

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Interim Report 1-8

Table 1-2 Net Generation Forecast (GWh)

YearAntigua

and Barbuda

Barbados DominicaDominican Republic

Grenada Haiti Jamaica St. Kitts Nevis St. LuciaSt. Vincent

and Grenadines

Martinique Guadeloupe Total

2009 318 1,039 87 12,638 198 660 4,490 161 60 345 156 1,575 1,663 23,391

2010 315 1,073 89 13,142 209 726 4,674 166 67 356 167 1,620 1,720 24,322

2011 312 1,107 91 13,663 220 799 4,865 171 74 367 178 1,672 1,775 25,295

2012 410 1,143 94 14,179 232 878 5,066 175 82 378 191 1,727 1,832 26,387

2013 422 1,180 96 14,646 244 966 5,277 180 86 390 204 1,783 1,888 27,363

2014 434 1,218 99 15,054 257 1,063 5,494 186 90 402 218 1,840 1,947 28,303

2015 447 1,258 101 15,554 270 1,169 5,726 191 94 415 233 1,900 2,003 29,362

2016 461 1,298 104 16,070 285 1,286 5,974 196 99 428 249 1,938 2,060 30,448

2017 475 1,340 106 16,601 300 1,415 6,232 202 103 442 266 1,978 2,117 31,576

2018 489 1,384 109 17,154 316 1,556 6,497 208 107 455 284 2,018 2,174 32,751

2019 503 1,428 112 17,724 333 1,712 6,777 214 111 470 304 2,058 2,233 33,979

2020 519 1,475 114 18,309 350 1,883 7,073 220 115 484 325 2,100 2,284 35,252

2021 534 1,522 117 18,914 369 1,977 7,376 226 119 500 348 2,142 2,337 36,483

2022 550 1,572 120 19,539 389 2,076 7,696 233 124 515 372 2,186 2,390 37,761

2023 567 1,622 123 20,184 409 2,180 8,024 239 129 531 397 2,230 2,445 39,082

2024 583 1,675 126 20,851 431 2,289 8,370 246 134 548 425 2,275 2,501 40,454

2025 600 1,729 129 21,539 454 2,403 8,734 253 139 565 454 2,321 2,559 41,881

2026 618 1,785 133 22,251 478 2,523 9,114 261 145 583 485 2,368 2,618 43,361

2027 636 1,843 136 22,986 504 2,650 9,510 268 150 601 519 2,416 2,679 44,897

2028 654 1,902 139 23,745 530 2,782 9,924 276 156 620 555 2,465 2,741 46,490

Growth Rate

3.9% 3.2% 2.5% 3.4% 5.3% 7.9% 4.3% 2.9% 5.2% 3.1% 6.9% 2.4% 2.7% 3.7%

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-9

1.4 FUEL SUPPLY

The forecast levelized price of distillate over 2014-2028, the assumed study period for the new projects being considered, is US$22.45/GJ. Each country except Dominica has at least one lower cost fuel option, and many countries have more than one. Table 1-3 provides the comparative prices. Distillate, LNG, and pipeline gas can be compared directly because they can fuel the same generators. Coal fuels generators with higher capital costs and higher heat rates, which must be taken into account in comparing fuel options. The prices of all fuels except distillate vary from country to country because they include transportation costs that vary.

Table 1-3 Fuel Prices Based on Yearly Demand 2014-2028

Country

Fuels Selected in Addition to Coal and

Distillate

Levelized Fuel Price, US$/GJ Fuel

Selected Coal Distillate Antigua and Barbuda None N/A 12.31 22.45 Barbados Pipeline Gas 7.39 7.77 22.45 Dominica Distillate only N/A N/A 22.45 Dominican Republic LNG 8.73 4.19 22.45 Grenada None N/A 12.31 22.45 Guadeloupe Pipeline Gas 10.88 7.77 22.45 Haiti LNG 12.73 7.77 22.45 Jamaica LNG 10.16 4.85 22.45 Jamaica North LNG 10.90 4.85 22.45 Martinique Pipeline Gas 8.99 7.77 22.45 St. Kitts and Nevis None N/A 12.31 22.45 St. Lucia Pipeline Gas 10.49 9.04 22.45 St. Vincent and Grenadines

None N/A 12.31 22.45

Coal is an optional fuel for every country except Dominica, where preliminary analysis showed it to be more costly than distillate on a US$/GJ basis.

Table 1-3 shows the following:

Every country except Dominica has at least one fuel option lower in price than distillate

Pipeline gas is the lowest cost natural gas option for every country reached by the ECGP: Barbados, Martinique, St. Lucia, and Guadeloupe

Coal is the only optional fuel for Antigua and Barbuda, Grenada, St. Kitts and Nevis, and St. Vincent and Grenadines

LNG is the lowest cost natural gas option for Dominican Republic, Haiti, Jamaica, and Jamaica North

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-10

CNG was considered and was the lowest cost gas option for several countries, but for those countries was always higher in cost than distillate and therefore does not appear in Table 15-1. It was considerably lower than distillate for some countries, but was more costly than LNG in those countries.

Though not studied in the same detail as the other fuel options, mid-scale LNG may provide an economically attractive option for some countries.

1.5 PROJECT AND TECHNOLOGY ANALYSIS

Screening analysis is an approach to comparing the costs of different technologies to determine the least cost technology across the range of annual capacity factors:

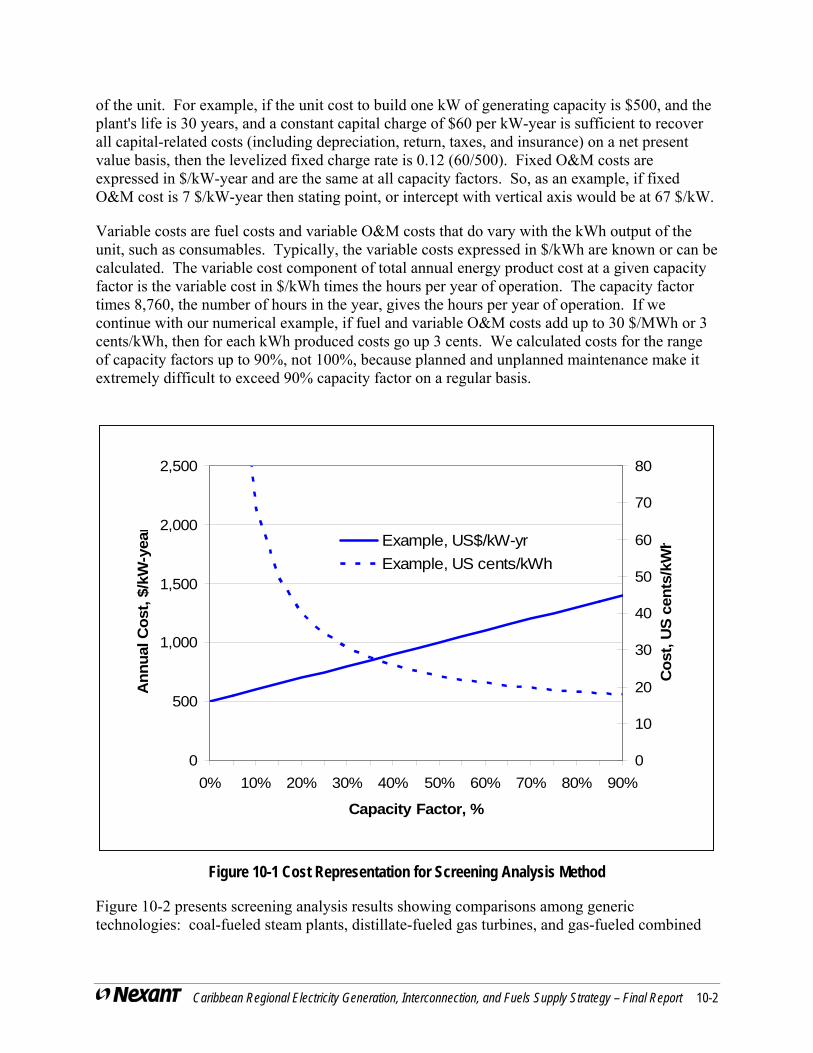

Uses simplified representations of generation costs to help identify least cost generating technologies

Plots annual cost in $/kW-year vs. capacity factor for a set of power plant and/or fuel options

The cost in $/kW-yr can also be easily expressed in cents/kWh, which are also of interest but are curved and somewhat harder to interpret than the straight lines in $/kW-yr

Annual cost is sum of:

Annualized investment-related costs based on initial capital investment, discount rate, and plant lifetime

Fixed annual operation and maintenance (O&M)

Variable cost (includes fuel cost and variable O&M costs) per kWh times capacity factor times hours per year

Selects lowest cost resources at each capacity factor, producing the “least-cost line” for that set of resources

1.5.1 Isolated Countries / Islands

Figure 1-4 illustrates the screening analysis approach. It presents the Fossil Least Cost Line (Fossil LCL) that applies for the Dominican Republic. The word “Fossil” means that only fossil fueled generation is included in determining the LCL. The scale in $/kW-yr for the solid lines is on the left, the scale in cents/kWh for the dotted lines is on the right. The Fossil LCL comprises 50 MW GT on LNG for capacity factors of zero through 20%, the 300 MW CC on LNG for capacity factors from 25% through 40%, and the conventional coal plant for capacity factors from 45% through 90%. In other words, the generation expansion plan based on this analysis would include gas turbines for peaking duty, combined cycles for mid-range duty, and conventional coal for base load duty.

In order to achieve the Fossil LCL the Dominican Republic would have to undertake large capital investments for expansion related to coal and LNG transportation, and for coal plants themselves. This may pose a challenge, even if the desire to do so exists. LNG is preferable for application at lower capacity factors, coal for application at higher capacity factors. The scenario analysis provides more information on which is preferable overall, if doing both is not feasible.

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-11

Figure 1-5 expands upon Figure 1-4 by adding wind, small hydro, and fossil options to the graph of Figure 1-1. The small hydro line coincidentally overlaps with the wind with backup line at capacity factors from 30% to 40%. Wind with backup, which is typically a better comparison than wind without backup, is now marginally economic at the capacity factors where it might operate at a good site. Wind with backup simply adds the full cost of operation of a 50 MW gas turbine at 5% capacity factor to the costs of wind without backup, which also adds 5% to the capacity factor.

Figure 1-5 also illustrates what might occur if neither coal nor LNG is available for future generation for the Dominican Republic. The periwinkle line represents the cost of a 300 MW HFO-fueled steam plant. Without expanded supplies of LNG or coal, costs will more than triple at high capacity factors.

Dominican Republic has under construction or planned considerable new small hydro and wind generation. Figure 1-5 illustrates the desirability of such an approach where good sites can be identified.

0

500

1,000

1,500

2,000

2,500

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Capacity Factor, %

An

nu

al C

ost

, $/k

W-y

ear

0

10

20

30

40

50

60

70

80

Co

st, U

S c

en

ts/k

Wh

Fossil Least Cost Line, US/kW-yr50 MW GT LNG US$/kW-yr300 MW CC LNG US$/kW-yr300 MW Conv Coal, US$/kW-yrFossil LCL, US cents/kWh

Figure 1-4 Fossil LCL for Dominican Republic

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-12

0

500

1,000

1,500

2,000

2,500

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Capacity Factor, %

An

nu

al C

ost

, $/

kW-y

ear

0

10

20

30

40

50

60

70

80

Co

st, U

S c

en

ts/k

Wh

Fossil Least Cost Line, US/kW-yr1.5 MW Wind US$/kW-yr1.5 MW Wind w/Backup US$/kW-yr300 MW ST HFO DR US$/kW-yrSmall Hydro US$/kW-yrFossil LCL, US cents/kWh

Figure 1-5 Other Options for Dominican Republic

The bullets below summarize the least cost technology/fossil fuel combination by country as determined by screening analysis. This considers the countries and islands as isolated systems. For some countries, imports via submarine cable (to be discussed later) provide a lower cost solution. We eliminated the technology/fuel combinations that were least cost at only one annual capacity factor, such as zero or 90%. Scenario analysis generally supports these conclusions, though multiple fuels were not used as much.

Individual Countries

Antigua and Barbuda, Grenada, and St. Vincent and Grenadines: 10 MW MSD on distillate for peaking and mid-range duty, and the coal-fueled CFB for base load duty

Coal-fueled CFB is only marginally more economic than distillate fueled medium speed diesels (MSD) plants; CO2 costs of US$50/tonne would make the distillate-fueled units more economic than the coal-fueled units

Dominica, St. Kitts, and Nevis: 5 MW MSD on distillate for peaking, mid-range, and base load duty

St. Kitts and Nevis are fortunate that a geothermal resource sufficient to serve all their demand has been confirmed and is in the process of development. For Dominica it seems highly probable that a geothermal resource sufficient to serve at least local demand will be confirmed and developed. None of these islands may not need to install any new distillate-fueled generation.

Dominican Republic: 50 MW GT on LNG for peaking duty, 300 MW CC on LNG for mid-range duty, and 300 MW conventional coal plant for base load duty

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-13

The Dominican Republic already has an LNG terminal and coal-fueled power plants. Scenario analysis shows that coal is preferred if only one fuel can be selected for future additions. However, incorporating CO2 costs in the analysis would compromise coal’s advantage. With the Dominican Republic’s large demand, expanding the use of both fuels may be feasible, even if new facilities are needed.

Haiti: 20 MW LSD on LNG for peaking, mid-range, and base load duty.

LNG provides very large benefits but requires significant up-front capital expenditures

Jamaica and Jamaica North: 50 MW GT on LNG for peaking duty, 20 MW LSD on LNG for mid-range duty, and 50 MW coal-fueled CFB base load duty

Today Jamaica and Jamaica North have neither fuel. It seems unlikely that they would want to develop both fuels. If only one is to be developed, LNG is preferred, and its advantage would increase if CO2 costs are incorporated in the analysis.

We emphasize that for some countries, imports via submarine cable provide a lower cost solution. This is addressed in the next subsection.

Sub-regional Gas Market

The ECGP links the markets of the four countries and provides the benefits of economies of scale compared to individual development.

Barbados, Guadeloupe, Martinique, and St. Lucia: 20 MW GT on pipeline gas for peaking duty and 20 MW LSD on pipeline gas for mid-range and base load duty

For all four countries the pipeline gas is less than half as costly as distillate. For all but St. Lucia, LNG is more costly than pipeline gas but significantly less costly than distillate.

The low gas price reduces the benefits of renewables and for Martinique and Guadeloupe makes importing geothermal power from Dominica via submarine cable marginal.

Figure 1-6 illustrates the ECGP gas connections among the countries.

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-14

Figure 1-6 Eastern Caribbean Gas Pipeline (ECGP) Proposed Route

1.5.2 Sub-regional Electricity Markets

The first three bullets below show the interconnections studied with greatest emphasis. All the interconnections were submarine cables except the Dominican Republic – Haiti link noted in the bottom bullet. The interconnections are presented in Figures 1-7 to 1-13. For each interconnection we note its capacity in MW, length in km, cost per kW for interconnection and related facilities only, source of export power, and economic attractiveness.

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-15

Nevis – St. Kitts, 50 MW submarine cable capacity, 5 km submarine cable length, US$328/kW (interconnection and related facilities only), geothermal power export, highly economic

Dominica – Martinique, 100 MW, 70 km, US$588/kW (interconnection and related facilities only), geothermal power export, marginally economic if displaced fuel is gas from ECGP, more economic if displaced fuel is higher cost

Dominica – Guadeloupe, 100 MW, 70 km, US$588/kW (interconnection and related facilities only), geothermal power export, moderately economic if displaced fuel is gas from ECGP, more economic if displaced fuel is higher cost

Nevis – Puerto Rico, 400 MW, 400 km, US$1,791/kW (interconnection and related facilities only), geothermal power export, highly economic if displaced fuel is HFO, not economic if displaced fuel is LNG

Nevis – US Virgin Islands, 80 MVA, 320 km, US$3,541/kW (interconnection and related facilities only), geothermal power export, only marginally economic even though the displaced fuel is distillate

Saba – St. Maarten, 100 MW, 60 km, US$528/kW (interconnection and related facilities only), geothermal power export, highly economic if displaced fuel is distillate and St. Maarten can accept 100 MW

United States (Florida) – Cuba, 400 MW, 400 km, US$1,791/kW (interconnection and related facilities only), export from coal-fueled steam plant or gas-fueled combined cycle, highly economic if displaced fuel is HFO

Dominican Republic – Haiti, 250 MW, 563 km, US$1,899/kW (interconnection and related facilities only), land interconnection, export from HFO fueled steam plant, not economic unless export is from lower cost unit/fuel combination

We also developed basic data and cost estimates for four potential interconnections that might form part of a “Northern Ring”, a conceptual set of interconnections in the northern Caribbean, potentially linking Florida – Cuba – Haiti – Dominican Republic – Puerto Rico – Nevis, or some subset of those areas. The Northern Ring interconnections not covered above include:

Puerto Rico – Dominican Republic, 400 MW, 150 km, US$705/kW (interconnection and related facilities only)

Haiti – Cuba, 400 MW, 200 km, US$705/kW (interconnection and related facilities only)

Haiti – Jamaica, 400 MW, 250 km, US$998/kW (interconnection and related facilities only)

Florida – Haiti, 400 MW, 1,100 km, US$3,488/kW (interconnection and related facilities only

We did not conduct economic analysis on these four interconnections. The cost per kW for the three shorter interconnections is in what might be an economically viable range if the sending country had low power costs and the importing country’s displaced fuel was distillate, HFO, or crude. The Florida – Haiti interconnection appears to be outside that range. Costs for the middle

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-16

islands would involve their sharing some of the costs of interconnections closer to the low-cost source, making favorable economics more difficult to achieve.

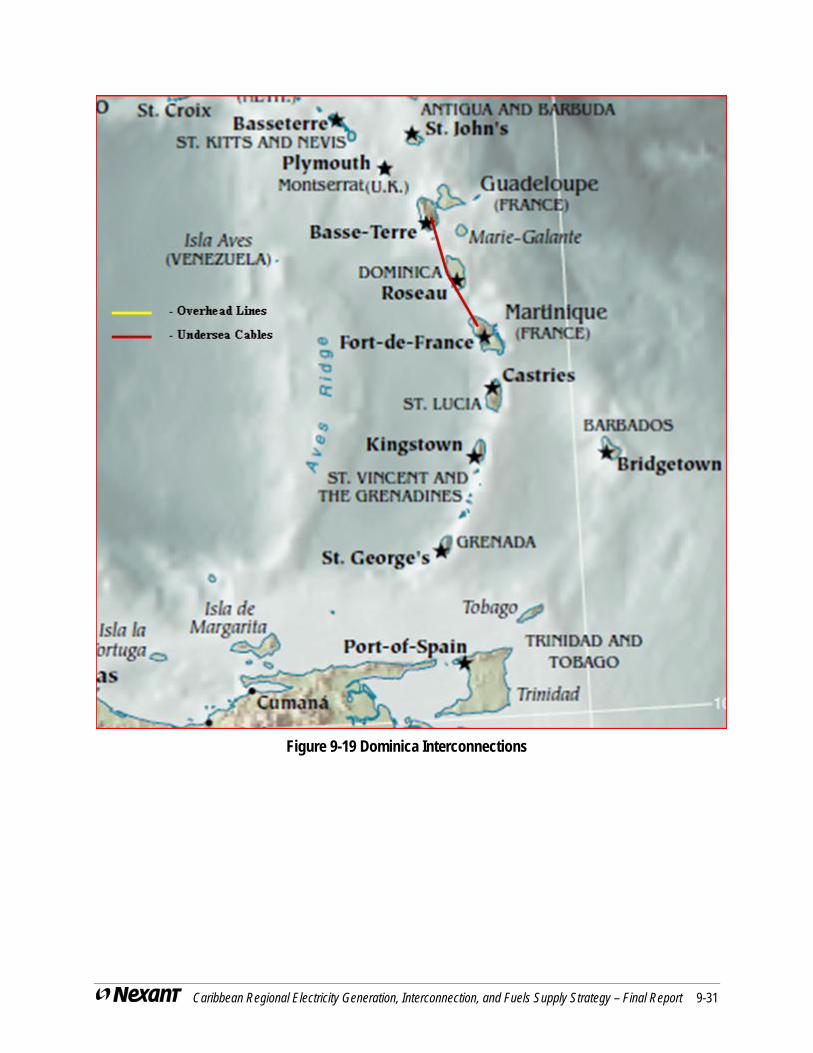

Figure 1-7 Dominica Interconnections

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-17

Figure 1-8 Nevis – Puerto Rico and Nevis – US Virgin Islands Interconnections

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-18

Figure 1-9 Saba – St. Maarten Interconnection

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-19

Figure 1-10 Haiti – Dominican Republic Interconnection

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-20

Figure 1-11 United States (Florida) – Cuba Interconnection

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-21

Figure 1-12 Northern Ring Set of Interconnections

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-22

Figure 1-13 Northern Ring Interconnections Alternative

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-23

1.5.3 Renewable Energy

Wind, geothermal, small hydro, and biomass technology/fuel combinations have the potential, at a good site, to be considerably less costly than distillate fueled power generation. The three lowest cost resources for operation at capacity factors above about 30% are renewables: geothermal, wind (including the cost of backup generation), and small hydro. This assumes that high quality sites can be identified and acquired. Solar PV and solar trough CSP are not competitive for bulk power generation. There are many small solar PV installations in Martinique due to subsidies, and solar PV is competitive for off-grid locations. If a lower cost fuel such as pipeline gas were the competitive fuel, the advantage of the renewable technology would be less.

Figure 1-14 compares renewable technologies to the Distillate LCL that results when distillate is the only fuel available. The scale in $/kW-yr for the solid lines is on the left, the scale in cents/kWh for the dotted lines is on the right. The Distillate LCL, in blue, represents the benefit of a renewable energy option. Its generation would displace generation at a cost along that line. Where a renewable energy option’s line is below the blue line, there is a net benefit. It reduces costs elsewhere that are more than its own costs. Where it is above the blue line, it represents a net cost.

Most of the renewable technologies are shown at a range of capacity factors they might reasonably achieve at a good site. Geothermal is also based on a good site, and is shown over the entire capacity factor range because it is not limited by resource availability once the resource has been defined. Wind with backup simply adds the full cost of operation of a 20 MW LSD at 5% capacity factor to the costs of wind without backup, which also adds 5% to the capacity factor. Biomass costs assume that biomass costs the same as export coal in the US.

Figure 1-14 shows that all but two of the renewable energy technologies have the potential, at a good site, to be considerably less costly than distillate fueled power generation. Solar PV and solar trough with six hour storage are above the Distillate LCL. If a lower cost fuel such as pipeline gas were the competitive fuel, the advantage of the renewable technology would be less and might disappear.

Figure 1-15 compares renewable technologies to the Fossil LCL for Barbados, which has the lowest cost gas fuel of any of the countries studied. The renewable technologies offer much smaller net benefits, small hydro and wind with storage are marginally economic, biomass is not economic, and the technologies that were not economic before are less competitive.

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-24

0

500

1,000

1,500

2,000

2,500

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Capacity Factor, %

An

nu

al C

ost,

$/k

W-y

ear

0

10

20

30

40

50

60

70

80

Co

st, U

S c

ents

/kW

h

Distillate LCL, US$/kW-yr1.5 MW Wind Turbine1.5 MW Wind w/BackupCommercial PV 500 kW20 MW GeothermalSmall HydroBiomassSolar Trough 6 hr StorageDistillate LCL, US cents/kWh

Figure 1-14 Distillate LCL vs. Renewable Energy Options

0

500

1,000

1,500

2,000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Capacity Factor, %

An

nu

al C

ost

, $/k

W-y

ear

0

10

20

30

40

50

60

Co

st,

US

ce

nts

/kW

h

Fossil Least Cost Line, US/kW-yr1.5 MW Wind Turbine1.5 MW Wind w/BackupSolar Trough 6 hr StorageSeries6Commercial PV 500 kW20 MW GeothermalSmall HydroBiomassFossil LCL, US cents/kWh

Figure 1-15 Barbados LCL vs. Renewable Energy Options

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-25

1.5.4 CO2 Costs

If a tax or similar levy were attributed to each tonne of CO2 emissions, the cost of using fuels would increase. This would open wider the economic window for technologies that produce lower or no CO2 emissions. However, all the countries today primary fuel is distillate and/or HFO, so the window is already quite wide. We investigated the impact if a cost of US$50/tonne were attributed to CO2 emissions.

At US$50/tonne, the effective price of fuels would increase in a range from US$2.52 for distillate to US$4.41 for coal, representing increases ranging from 15% for distillate to 91% for the lowest cost coal for the Study islands.

In the bullets below we measure the impact of CO2 costs by how technology choices change when it is applied.

Countries with small demand: The fuel prices are high even when coal fuels some of the least-cost generation.

For Antigua and Barbuda, Grenada, and St. Vincent and Grenadines, the preferred fuel would switch from coal to distillate.

The renewable energy resources that were economic before are now somewhat more economic, and those that were not economic edge closer to being competitive.

Countries with medium or high demand. The fuels are much less expensive than distillate and therefore the displaced generation is lower in cost, narrowing the economic window for alternatives.

For the Dominican Republic, Jamaica, and Jamaica North, incorporating CO2 costs in the analysis would probably eliminate coal’s advantage over LNG or increase LNG’s advantage over coal.

With no CO2 cost the renewables that were economic for the islands with small demand are still economic, though in some cases only marginally so. Incorporating CO2 costs makes renewables more competitive.

1.6 REGIONAL STRATEGIES

For all Study countries combined, costs including fuel savings from exports and interconnection costs were:

US$31,985 million for the Base Case Scenario

US$29,424 million for the Fuel Scenario

US$29,415 million for the Interconnection/Renewable Scenario

US$27,619 million for the Integrated Scenario

Table 1-4 presents cost differences among Scenarios by system as well as differences in Scenario total costs. The Fuel Scenario and Interconnection/Renewable Scenarios both reduce costs by about US$2.5 billion compared to the Base Case. The Integrated Scenario reduces costs by

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-26

about US$ 4.3 billion, showing that the Integrated Scenario captures most of the individual benefits of each of the other two Scenarios.

Table 1-4 Scenario NPV Cost Differences - Base Case Minus Other Scenario Costs (million US$)

Fuel Scenario

Interconnection/ Renewable Scenario

IntegratedScenario

Antigua and Barbuda 12 20 31

Barbados 906 39 912

Dominica 0 604 10

Dominican Republic 444 350 721

Grenada 32 17 45

Haiti 433 76 476

Jamaica 500 138 628

St. Kitts 0 159 159

Nevis 0 1,135 1,135

St. Lucia 216 18 221

St. Vincent and Grenadines 18 14 29

Total 2,561 2,570 4,365

The costs of the interconnections and the fuel savings from the exports of geothermal power are attributed to Dominica and Nevis. All numbers in Table 15-2 have positive values (except for zeros for Dominica, St. Kitts, and Nevis for the Fuel Scenario), meaning that each Scenario and each country in each Scenario provides cost savings compared to the Base Case.

1.7 COUNTRY SUMMARIES

Each country summary below presents paragraphs on:

Overview

Current and Forecast Load

Fossil Fuel Options

Renewable Generation Potential

Development Scenarios (development plans for the Base Case Scenario, the Fuel Scenario, the Interconnection/Renewable Scenario, and the Integrations Scenario)

Discussion of Country Results

1.7.1 Antigua and Barbuda

Overview: Antigua Public Utility Authority (APUA) is responsible for the power generation, transmission, and distribution of electricity in Antigua and Barbuda. APUA purchases most of the power from Antigua Power Company (APC), a private company. Antigua and Barbuda

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-27

currently rely exclusively on diesel for power generation. Efforts are underway to convert some of the diesel engines to HFO as an alternate fuel.

Current and Forecast Load: The country’s 2009 peak demand is just over 50 MW, with net generation of over 300 GWh. By 2028 peak demand is projected to increase to around 100 MW, with net generation increasing to around 650 GWh (increase rate of 3.9% per year). Losses in the transmission and distribution system are projected to decrease from over 30% in 2009 to around 10% by 2028.

Fossil Fuel Options: Imported coal was considered as an alternative fuel. Due to the location and electricity demand on the island, the Study did not find natural gas to be an economically viable fuel option.

Renewable Generation Potential: Wind is the most promising renewable resource for Antigua and Barbuda. A 2008 Energy Engineering Corp. report indicated that up to 400 MW of wind power can be developed on the islands, primarily on Barbuda. Solar PV potential is estimated at 27 MW of installed capacity, but bulk power development would not be economic based on current estimates.

Development Scenarios: All four Study Scenarios assumed that the committed system additions of the Casada Gardens units will be installed during 2011-2013. With those unit additions, system reserve margin requirements would be satisfied until 2019. During 2020-2028 the system demand growth will require building additional generation units.

For the Base Case Scenario, new unit additions are assumed to be 10 MW medium speed diesel units using distillate oil. By 2028 the system will need another 30 MW (3 x 10 MW units) to meet the required capacity.

For the Fuel Scenario, coal-fueled circulating fluidized bed (CFB) plants are marginally more economic than distillate fueled medium speed diesels (MSD) plants; new unit additions are assumed to be 10 MW CFB units using imported coal. CO2 costs of US$50/tonne would make the distillate-fueled units more economic than the coal-fueled units. Conventional (large-scale) LNG is more costly than either (distillate or coal) option. Though not studied in the same detail as the other fuel options, mid-scale LNG may provide an economically attractive option. By 2028 the system will need another 30 MW (3 x 10 MW units) to meet the required capacity. The Fuel Scenario results show that the introduction of coal provides net present worth savings of US$12 million compared to the Base Case Scenario.

The Interconnection/Renewable Scenario assumed development of new diesel units as in the Base Case Scenario, with the addition of 14 MW of new wind units. This assumes that sites with good winds and low development costs can be identified and acquired. There is no electrical interconnection. The Interconnection/Renewable Scenario results show that the introduction of wind generation provides net present worth savings of US$20 million compared to the Base Case Scenario.

The Integrated Scenario assumed new generation units are 10 MW CFB units, as in the Fuel Scenario, and the addition of 14 MW of new wind units, as in the Interconnection/Renewable Scenario. The Integrated Scenario results show that including both coal as a fuel and wind

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-28

generation provides combined savings of US$31 million over the Base Case Scenario. The Integrated Scenario results show savings close to the sum of the savings of other two Scenarios.

Discussion of Country Results

Adding coal-fueled CFB technology reduces net present worth costs by US$12 million compared to the Base Case Scenario, with a cost advantage compared to distillate-fueled MSD technology ranging from 2% at 55% capacity factor to 10% at 80% capacity factor. That cost advantage disappears if costs of US$50/tonne are attributed to CO2 emissions.

Conventional LNG is more costly than distillate, but mid-scale LNG might be a viable fuel option, justifying a more detailed analysis.

Development of wind generation reduces net present worth costs by US$20 million compared to the Base Case Scenario, assuming that sites with good winds and low development costs can be identified and acquired. With that assumption wind is much lower in cost than distillate fueled generation. Small hydro and biomass would also be economic, if good sites can be identified. The benefits are relatively unaffected by the choice of fuel for the country’s fossil units.

1.7.2 Barbados

Overview: Barbados Light and Power (BL&P), a private company, is responsible for power generation, transmission, and distribution of electricity in Barbados. Existing installed generation of around 240 MW, mostly comprising of low and medium speed diesel units, substantially exceeds peak demand and provides a comfortable reserve margin. BL&P is looking to diversify its fuel mix which is mostly dependent on imported oil products.

Current and Forecast Load: The country’s 2008 peak demand was 164 MW, with net generation of over 1,000 GWh. By 2028 peak demand is projected to double to around 325 MW, with net generation increasing to around 1,900 GWh (increase rate of 3.5% per year).

Fossil Fuel Options: Natural gas, delivered as LNG or through the Eastern Caribbean Gas Pipeline (ECGP), and imported coal were considered as alternative fuel options. Due to the location and electricity demand on the island, the Study found natural gas delivered through ECGP to be the most economically attractive fuel option.

Renewable Generation Potential: No studies on country-specific overall wind and solar potential are available. We estimated Barbados wind potential to be at least 10 MW based on an already approved project. Solar PV potential is estimated at 26 MW of installed capacity, but bulk power development would not be economic based on current estimates.

Development Scenarios: All four Scenarios assumed that the committed system additions of the nine 16 MW Trent units will be installed. The first six units were added during 2011-2013 while the next three units were added when required to match the load growth. All Trent unit additions would satisfy reserve margin requirements until 2025. During 2026-2028 the Barbados system will require new capacity additions.

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-29

For the Base Case Scenario, new additions are assumed to be 20 MW low speed diesel units using distillate oil. By 2028 the system will need another 40 MW (2 x 20 MW units) to meet the required capacity.

For the Fuel Scenario, assumed system additions are the same as for the Base Case Scenario. The difference is that in this scenario most existing and all new units are assumed to use natural gas as a fuel, supplied through the ECGP. The Fuel Scenario shows that the introduction of ECGP natural gas provides net present worth savings of US$906 million compared to the Base Case Scenario..

For the Interconnection/Renewable Scenario, most assumed system additions are the same as for the Base Case Scenario. The difference in this Scenario is the addition of 45 MW of new wind units. This assumes that sites with good winds and low development costs can be identified and acquired. There is no electrical interconnection. The Interconnection/Renewable Scenario shows that the introduction of wind generation provides net present worth savings of US$39 million compared to the Base Case Scenario.

For the Integrated Scenario, the availability of natural gas is assumed, as in the Fuel Scenario, combined with the addition of 45 MW of new wind units, as in the Interconnection/Renewable Scenario. The Integrated Scenario results show net present worth savings of US$912 million over the Base Scenario, only slightly more than for the Fuel Scenario.

Discussion of Country Results

Barbados has four fossil fuel options that offer significant economic benefits compared to continued reliance on oil products: natural gas via the ECGP, LNG, CNG, and coal. By far the most attractive is the ECGP option, which provides net present worth savings of $906 million compared to the Base Case Scenario. Its cost per kWh compared to distillate fueled generation ranges from less than half at 20% capacity factor to less than 40% at 80% capacity factor.

If the ECGP does not materialize, the other fuel options should be considered. They would offer significant savings compared to distillate, though not as dramatic as ECGP gas offers.

Development of wind generation reduces Interconnection/Renewable Scenario net present worth costs by US$39 million compared to the Base Case Scenario, assuming that sites with good winds and low development costs can be identified and acquired. However, when ECGP gas is available, as is assumed in the Integrated Scenario, adding wind generation increases savings by only US$6 million. Wind is only marginally economic, as would be small hydro if good sites can be identified, but biomass would be marginally uneconomic. This illustrates the high dependence of wind generation savings on the assumed fuel supply option, and the possibility that wind generation penetration might be limited to only a few of the best wind sites.

1.7.3 Dominica

Overview: Dominica Electricity Services Limited (DOMLEC) is a sole producer responsible for the power generation, transmission, and distribution of electricity in Dominica. Existing installed generation, comprising high and medium speed diesel units and hydro units, exceeds peak

Caribbean Regional Electricity Generation, Interconnection, and Fuels Supply Strategy – Final Report 1-30

demand by 35% providing a comfortable reserve margin. Dominica is looking to diversify its fuel mix, which is mostly dependent on imported oil products.

Current and Forecast Load: The country’s current peak demand is around 15 MW, with net generation of around 90 GWh. By 2028 peak demand is projected to increase to 25 MW, with net generation increasing to around 150 GWh (increase rate of 2.5% per year).

Fossil Fuel Options: Due to the low electricity demand on the island, the least-cost fuel is distillate because the fixed costs associated with all other fuels produce higher unit costs in US$/GJ.

Renewable Generation Potential: Based on the ongoing assessment of potential at the Watton Waven field in central Dominica, and West Indies Power’s exploration in the Soufriere area, geothermal potential is estimated to be adequate to supply 100 MW of geothermal power plants. Drilling of the first three slim (exploratory) wells is scheduled to start in June 2010 in the Soufriere area near the southern coast. Solar PV potential is estimated at 45 MW of installed capacity, but bulk power development would not be economic based on current estimates. Dominica also has small-size hydro and wind potential.

Development Scenarios: Starting in 2012 Dominica will require new capacity additions.

For the Base Case Scenario, new additions are assumed to be 5 MW medium speed diesel units using distillate oil. By 2028 the system will need another 15 MW (3 x 5 MW units) to meet the required capacity. Dominica does not have a potentially less expensive fossil fuel option.

The Interconnection/Renewable Scenario assumes the addition of a 20 MW geothermal unit in 2012 to satisfy local needs. It also assumes submarine cable electrical interconnections with Martinique and Guadeloupe, and the addition of two 92.5 MW units in 2014 to support exports to those two countries. The results show large benefits of geothermal development in this Scenario, with net present worth savings of US$604 million compared with the Base Case Scenario.