Embed Size (px)

Citation preview

Carborundum Universal Limited

CMP: Rs.210 Recommenda<on: Buy Target Price: Rs. 257

Date: 19th September 2014 Growing Stronger

Research Partner Page 1 of 13

Stock vs NIFTY

DetailsNSE Code CARBORUNIVBSE Code 513375Bloomberg/ Reuters Code CU.IN/CRBR.NSMkt. Cap (Rs. Mn) 39,552

Details (Rs Mn) FY14 FY15E FY16ERevenues 21,253 28,922 34,194EBITDA 2,515 3,837 5,022EBITDA Margin (%) 11.8 14.0 15.5PAT 951 1,817 2,565PAT Margin(%) 15.1 6.6 7.9EPS 2.0 9.7 13.6P/E 43.0 21.7 15.4RoE 8.0% 15.0% 18.0%

Shareholding Pattern (%) Jun'14 Mar'14 Dec'13Promoter 42 42 42FII 23 23 23DII 12 11 11Others 24 24 24

Carborundum Universal is a part of the Murugappa Group, which is a

conglomorate with interests in sugar, fertilizer, industrial gears, abrasives,

electrominerals, ceramics. The company was incorporated in 1954 as a

joint venture between Carborundum USA, Universal Grinding Wheel

Company UK and Murugappa. The company has 30 manufacturing plants

spread across 7 countriesm and caters to clients present in over 50

countries.

The company is into the business of abrasives, ceramics and electro-

minerals. The abrasives and electro-minerals segment contribute about

80% to the total revenues of the firm. The firm has a strong global

presence enables the firm to earn about 50% of revenues from abroad. The

firm has strong market position in India, and for select abrasives it is the

market leader in India. The firm is second largest producer of silicon

carbide in the world. The firm is also the market leader for super

refractory.

The company suffered over the past year or so due to global slowdown

which caused weak demand for its products, with a capacity utilization of

only 70% in FY14. However, we expect the global economy to continue its

recovery, and an increase in the industrial production, which will result in

CUMI's revenues and profitability improving going forward.

The company currently trades at a P/E of 42.8x (ttm) and a one year

forward P/E of 25x in FY15E, with a FY16E forward P/E of 20x. We

expect that the firm will have significant upside potential as the global

economy strengthens, which subsequently generates positive signs to the

end user industries. We suggest a BUY with a target price of Rs 257 for the

firm.

Investment Posi;ves

Presence in diversified business segmentsThe firm has established itself in four business segments namely abrasives, electro minerals, super

refractories, and industrial ceramics. Abrasives is a tough and wear resistant substance for polishing and

grinding operations. Electro minerals is the raw material required to manufacture abrasives and super

refractory. Industrial ceramics have high wear resistance, anti-corrosive, and insulating properties which are

used in electrical industry. Super refractory is extremely resistant to heat so they are used in furnace linings.

Source: Company

It offers a range of products under these segments to the infrastructure industries like cement industry. The

other industries which the company serves are bearing industry, pump cylinder liners, valve industry, power

generation industry, boiler, fabrication and textile industry. CUMI has the necessary technology to

manufacture high quality products which is why we expect them to surge in the period ahead. Due to

diversified end user industries, we expect that the firm will report better sales number as all these industries

are expected to recover and rise in the current economic scenario.

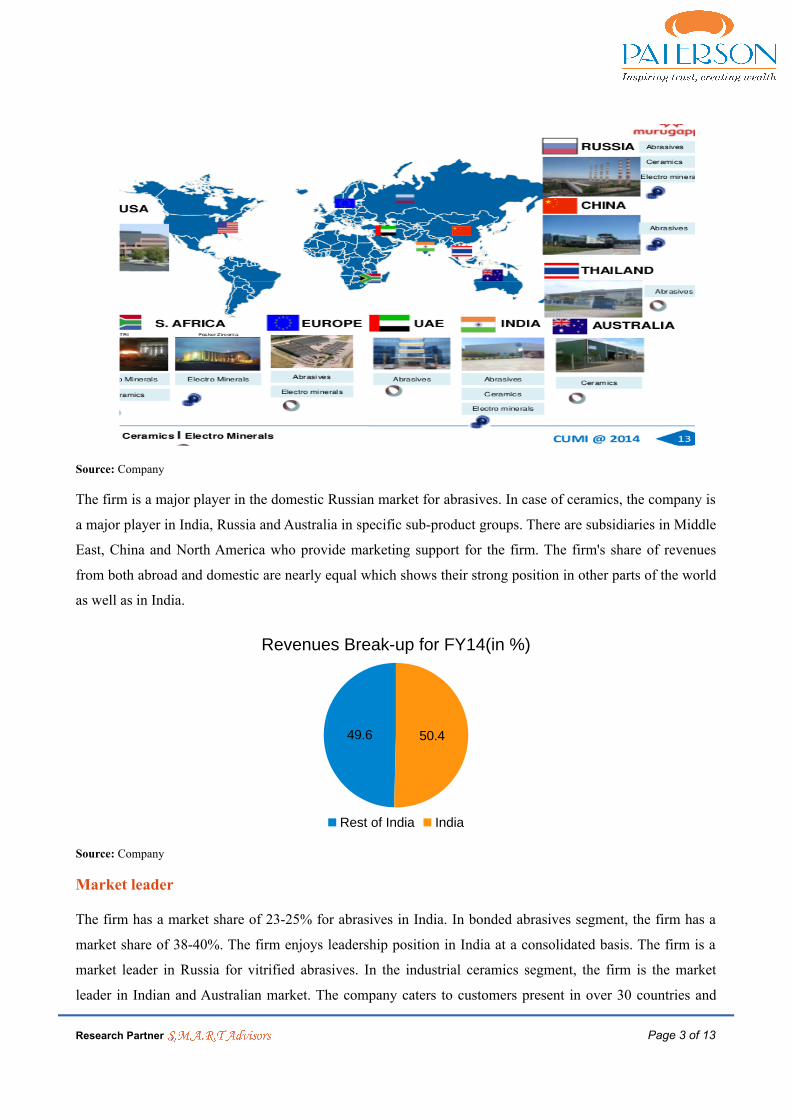

Strong global and domestic presenceThe company has 30 plants located across 7 countries, and its products are available in over 50 countries.

The company has marketing and distribution centres in USA, Europe, UAE, Australia, Thailand. The firm

has manufacturing plants in South Africa, Russia, China and India. Due to its presence across the globe, the

firm has been able to cut costs in the manufacturing process in some areas. The firm enjoys location

advantage of being present in Russia as the power costs and raw material costs for silicon carbide are

cheaper here, which gives cost competitiveness for CUMI.

Research Partner Page 2 of 13

Ceramics Electrominerals Abrasives0

1,0002,0003,0004,0005,0006,0007,0008,0009,000

10,000

Segment wise breakup of revenues

FY10 FY11 FY12 FY13 FY14

(in R

s m

n)

Source: Company

The firm is a major player in the domestic Russian market for abrasives. In case of ceramics, the company is

a major player in India, Russia and Australia in specific sub-product groups. There are subsidiaries in Middle

East, China and North America who provide marketing support for the firm. The firm's share of revenues

from both abroad and domestic are nearly equal which shows their strong position in other parts of the world

as well as in India.

Source: Company

Market leader

The firm has a market share of 23-25% for abrasives in India. In bonded abrasives segment, the firm has a

market share of 38-40%. The firm enjoys leadership position in India at a consolidated basis. The firm is a

market leader in Russia for vitrified abrasives. In the industrial ceramics segment, the firm is the market

leader in Indian and Australian market. The company caters to customers present in over 30 countries and

Research Partner Page 3 of 13

49.6 50.4

Revenues Break-up for FY14(in %)

Rest of India India

around 65% of its production of industrial ceramics is exported. The firm acquired 100% stake in TRI, South

Africa which will help in increasing their market size in high alumina and monolithics. The firm has

leadership position in Indian markets for select products and is an active player in the Russian market in the

refractories segment. In the electromineral, the company is a leading player in the Silicon Carbide and Fused

Zirconia and is the market leader in both the Russian and Indian market.

Source: Company

Strong balance sheet

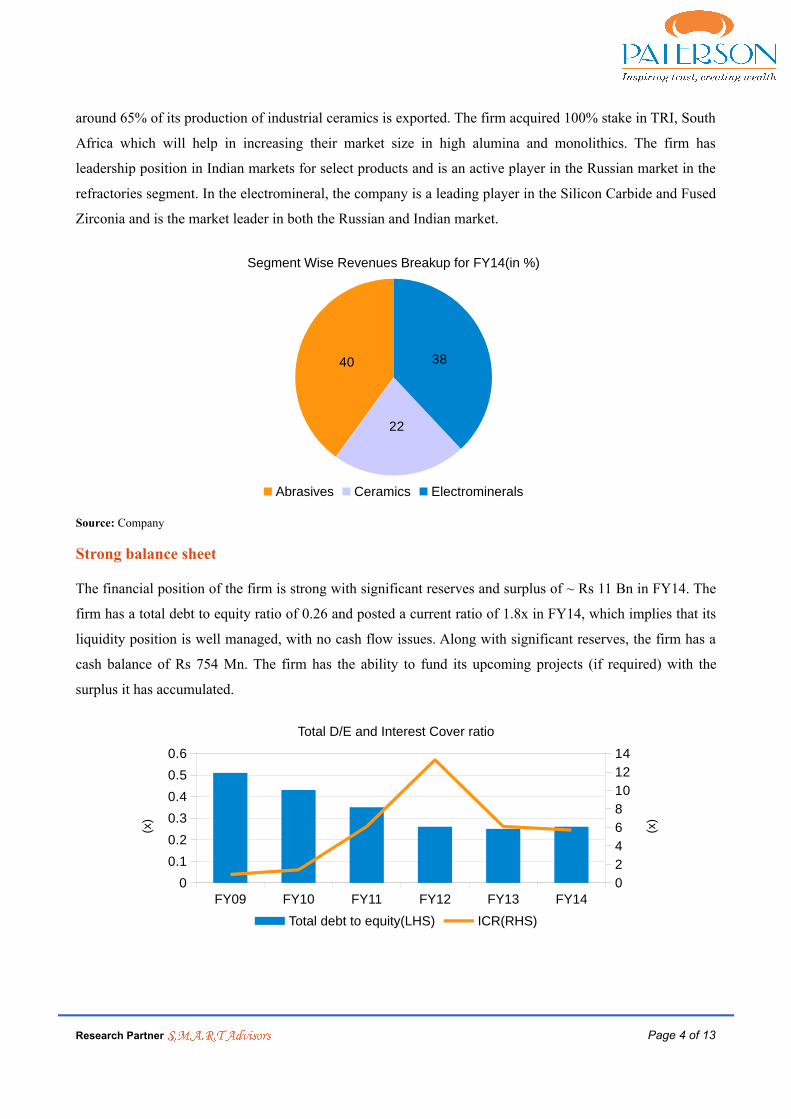

The financial position of the firm is strong with significant reserves and surplus of ~ Rs 11 Bn in FY14. The

firm has a total debt to equity ratio of 0.26 and posted a current ratio of 1.8x in FY14, which implies that its

liquidity position is well managed, with no cash flow issues. Along with significant reserves, the firm has a

cash balance of Rs 754 Mn. The firm has the ability to fund its upcoming projects (if required) with the

surplus it has accumulated.

Research Partner Page 4 of 13

40

22

38

Segment Wise Revenues Breakup for FY14(in %)

Abrasives Ceramics Electrominerals

FY09 FY10 FY11 FY12 FY13 FY140

0.1

0.2

0.3

0.4

0.5

0.6

02468101214

Total D/E and Interest Cover ratio

Total debt to equity(LHS) ICR(RHS)

(x)

(x)

Key Risks

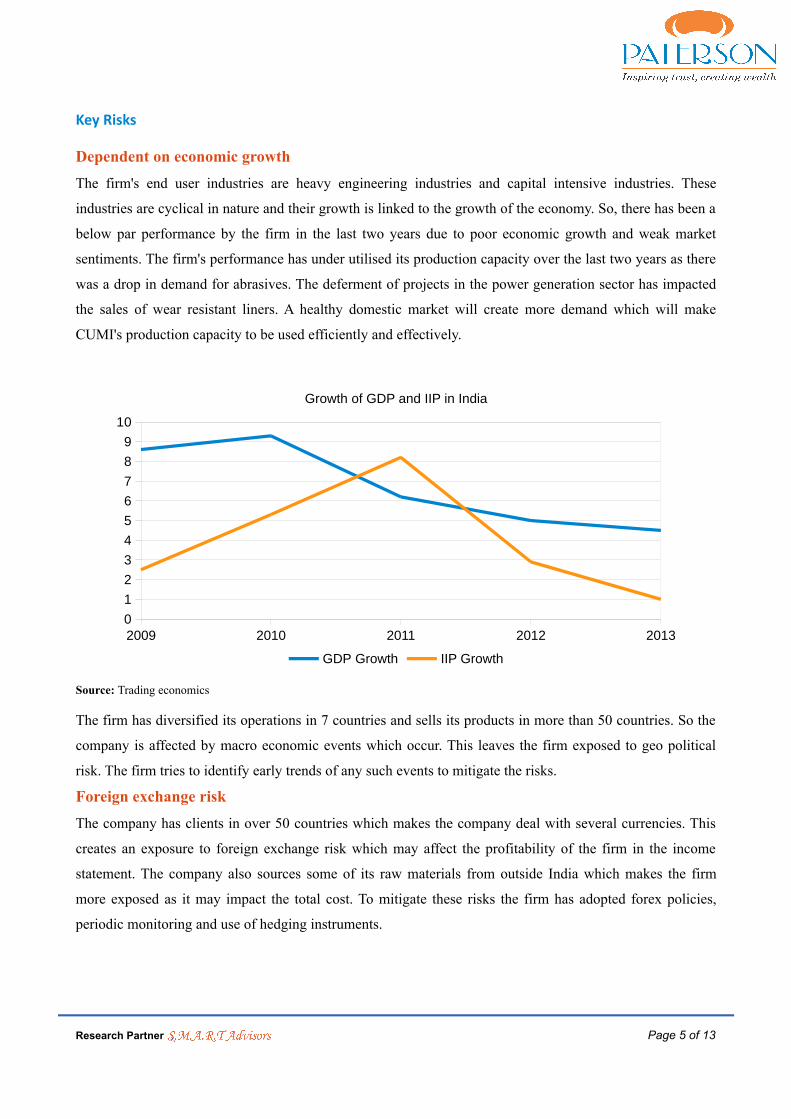

Dependent on economic growthThe firm's end user industries are heavy engineering industries and capital intensive industries. These

industries are cyclical in nature and their growth is linked to the growth of the economy. So, there has been a

below par performance by the firm in the last two years due to poor economic growth and weak market

sentiments. The firm's performance has under utilised its production capacity over the last two years as there

was a drop in demand for abrasives. The deferment of projects in the power generation sector has impacted

the sales of wear resistant liners. A healthy domestic market will create more demand which will make

CUMI's production capacity to be used efficiently and effectively.

Source: Trading economics

The firm has diversified its operations in 7 countries and sells its products in more than 50 countries. So the

company is affected by macro economic events which occur. This leaves the firm exposed to geo political

risk. The firm tries to identify early trends of any such events to mitigate the risks.

Foreign exchange riskThe company has clients in over 50 countries which makes the company deal with several currencies. This

creates an exposure to foreign exchange risk which may affect the profitability of the firm in the income

statement. The company also sources some of its raw materials from outside India which makes the firm

more exposed as it may impact the total cost. To mitigate these risks the firm has adopted forex policies,

periodic monitoring and use of hedging instruments.

Research Partner Page 5 of 13

2009 2010 2011 2012 20130123456789

10

Growth of GDP and IIP in India

GDP Growth IIP Growth

Rise in input costs

For any capital intensive production facility, power and fuel is one of the key important factors. Any shortage

in these would bring barrier to the production process and hence affect the financial position of the firm.

Power cost is one of the key challenges for CUMI. As they are located in diverse geographic places, the

power cost and policies vary from one place to another. Any sudden price rise in the power rates would affect

the profitability due to increase in operating expense.

The firm also faces power constraints in some locations and this makes the firm to choose expensive

methods to generate power. Another important operating expense is fuel. The rise in fuel cost will affect the

profitability of the firm. Fuel is used either as directly raw material or for firing purpose. So any shocks in

the middle east regions would impact the price of fuel which would subsequently affect the firm's earnings.

Peer Comparison

The company's presence across the globe gives them competition from both global and domestic players.

The company faces global competition from:

• 3M

• Saint Gobain

• Sia Abrasives

• Tyrolit

• Winterthur

The company faces domestic competition from

• ACE Refractories

• BHEL

• Grindwell NortonLtd

• John Oakey & Mohan

• Jyothi Ceramics

• Maithan Ceramics

• Orient Abrasives

• SAK Abrasives

Industry Analysis

Global economic growth has picked up in the second half of 2013 to 3.5%, an uptick from the 2.66% in the

previous six months. This growth is because of the development in the advanced economies, whereas

emerging economies grew only moderately during the period.

Research Partner Page 6 of 13

CUMIGrindwell

Orient AbrasivesBHEL

05

10152025

Operating profit margin comparison for FY14

(%)

Source: Company, S.M.A.R.T Advisors

Abrasives

The worldwide demand for abrasive products is expected to expand nearly by 6% per year to USD 40Bn by

2017. Growth from emerging nations like China will boost the demand for abrasives, and among developed

regions of the world like US, Japan and Western Europe recovery is expected which will encourage the

demand for abrasives. The size of global abrasives market is USD 12.9Bn in FY14, whereas the Indian

market with a size of USD 0.49 Bn is just 3.5% of the global market.

Source: Company, S.M.A.R.T Advisors

Industrial Ceramics

The global market for advanced ceramics is more than

USD13 billion, of which alumina based ceramics is

around USD 5 billion. As one of the world's most

populated countries, the Indian ceramic market has a

large domestic demand, which will further drive the

rapid development of the industry. The ceramics

industry is highly segmented into sub-markets such as

wear resistant liner, lined equipment, engineered

ceramics, ceramic insulation, sanitary pottery refractory

tiles, technical tiles etc. The ceramics manufacturing

process needs efficient energy. High energy costs for

manufacturing is changing markets, hindering the

competitiveness of ceramics producers without access to cheap fuels.

Research Partner Page 7 of 13

36%

28%

36%

Region Wise

Coated Super abrasivesBonded

33%

29%

20%

18%

Product Wise

Europe Rest of the worldUSA China

5%20%

70%

2%4%

Alumina based ceramics market

Energy and Aerospace Wear ResistantBio Ceramics DefenseCutting tools

Source: Company, S.M.A.R.T Advisors

Refractories

The refractory market is a USD 30 Bn at a global level and the largest demand for refractory material comes

from China which is around 44% of the global demand. The refractory market in India is estimated to be

around USD 750 Mn. The major products which dominate this market in India are basic refractories, high

alumina and monolithics all three forming about 75% of the market share.

Product wise market size in India Percentage distribution of refractory

(in Rs Mn) demand globally

Company Background

The company was incorporated as a joint venture between Carborundum Company, USA, Universal

Grinding Wheel Company UK and the Murugappa India in 1954. On a consolidated basis, the company has

30 plants spread across 7 countries. The company products are sold in over 50 countries. The company has a

well established marketing and distribution base in USA, Thailand, UAE, Australia.

The firm's business is spread into four areas:

• Abrasives

The major product groups under this are bonded abrasives, coated abrasives, super abrasives, metal

working fluids, and power tools. The end user industries of this are engineering, automobile,

construction, infrastructure and home maintenance. The manufacturing facilities for abrasives are

located in India, Russia, China and Thailand. This division contributes around 41% to the

consolidated revenues.

• Electro minerals

The product ranges include brown fused alumina, white fused alumina, silicon carbide, zirconia,

Research Partner Page 8 of 13

60% 19%

7%14%

Iron and steel Non metalic mineralsOther metals Other markets

12,000

4,000

11,0002,000

5,000

11,000

Basic Dolomite High AluminaSilica Flow control Monolithics

Source: Company, S.M.A.R.T Advisors

specialty minerals. The firm has clients for these products in over 40 countries. The firm is a

established leader in Russia and India in this segment of business. This segment along with

refractories contributes around 39% to the consolidated revenues.

• Ceramics

This segment is divided into three product groups: wear protection, engineered ceramics and

metallized ceramics. Currently, they are in the business of alumina based ceramics. There are twelve

manufacturing facilities around the globe in India, Australia, South Africa and Russia. This division

contributes around 22% to the consolidated revenues.

• Super refractories

The firm is into high alumina, silicon carbide, zirconia based refractories which are capable to

withstand very high temperature. They operate only in fired alumina and monolithics business. The

firm can manufacture complex shapes and it holds the leadership in these select products in the

Indian markets and is an active player in Russia.

Products and end user industries

Products ApplicationAbrasives Bonded abrasives Bearing industry, valve industry, gear

grindingThin wheels General engineering, foundry, fabrication,

rolling millsCoated abrasives Auto OEM, flooring, wood

Industrial Ceramics Wear resistant Power generation, cement industryLined equipment Pulverized fuel bends, cement industryEngineered ceramics Boiler industry, texti le industry,

electronics, pump cylinder linersMetz cylinders and devices Electrical transmission and distribution,

defense, medical electronicsElectro minerals Brown fused alumina Bonded abrasive, coated abrasive

White fused alumina Refractory, metallurgicalSilicon carbide Silicon water slicing, investment castingZirconia Particulate filter

Super refractories Fired refractories Ceramic industries, chemical processindustries, glass, power generationMonolithics

Source: Company

Research Partner Page 9 of 13

Joint Venture and Subsidiaries

• Wendt (India) Limited - Manufactures abrasives for stone/construction industry and special purpose

machines. CUMI acquired 40% of Wendt in 1991.

• Murugappa Morgan Thermal Ceramics Ltd – Manufactures ceramic fibre, which is a refractory

material. In 1983, CUMI entered into JV with MMTCL.

• Ciria India Limited – Design and installation of refractory liners for the petrochemical and fertilizer

industries.

Subsidiaries

Company LocationCUMI America Inc USA

CUMI Australia Pty Limited Australia

Sterling Abrasives Limited India

Southern Energy Development Corporation Limited India

Net Access India Pvt Ltd India

CUMI Middle East FZE UAE

CUMI International Ltd Cyprus

CUMI Canada Inc Canada

OAO Volzky Abrasives Work Russia

Financial Highlights

The company has suffered from the global

slowdown for the past two years as it has reported

low profit levels during this period. It generated a

revenue of Rs 21,253Mn in FY14 which is an

increase 7.8% YoY, however, the profitability of the

company dropped during this period on the back of

higher fuel and power costs and a hike in raw

material prices. The EBITDA margins have

dropped since 2012 due to rise in these input costs.

The EBITDA margin have dropped to 11.8% in

FY14 from 19.5% in FY12.

The company's ROE has dropped by nearly one-third in FY13 and FY14 due to the lower margins.. The

Research Partner Page 10 of 13

FY09FY10

FY11FY12

FY13FY14

FY15EFY16E

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0

5

10

15

20

25

Net Sales and EBITDA Margin

Net Sales(LHS) EBITDA Margin(RHS)

In R

s M

n

%

company recorded 9% ROE and 20% ROCE in FY14. However, we expect that the signs of global recovery

will enable the company to grow, especially since its end user industries are picking up and the industrial

activity across the globe is improving.

The company's liquidity position is strong, and it has maintained a current ratio of 1.8x over the last two

years. The total debt to equity has been consistently reducing from 0.51 in FY09 to 0.26 in FY14. This bodes

well for the company in bad times, as it is able to ride out tough economic conditions better, and in good

economic scenarios, the company will be able to grow faster than its peers as it does not have a debt

overhang.

Final Thoughts

The EBITDA margins of the firm have shown positive signs recording 14.7% margin for the Q1FY15, as

compared to 12% in FY14. The company currently trades at a P/E of 42.8x (ttm) and a one year forward P/E

of 25x in FY15E, with a FY16E forward P/E of 20x. We expect that the firm will have significant upside

potential as the global economy strengthens, which subsequently generates positive signs to the end user

industries. We suggest a BUY with a target price of Rs 257 for the firm.

Research Partner Page 11 of 13

FY09FY10

FY11FY12

FY13FY14

FY15EFY16E

0

0.5

1

1.5

2

2.5

00.10.20.30.40.50.6

Stability Ratios

Current Ratio(LHS) Total debt to equity(RHS)

(x)

(x)

FY09FY10

FY11FY12

FY13FY14

FY15EFY16E

05

10152025303540

010203040506070

Performance Ratios

ROCE(LHS) ROE(RHS)

% %

Profit and Loss

Balance Sheet

Ra;os

Margins

Research Partner Page 12 of 13

P&L (Rs. Mn) FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16ESales 10,783 11,825 15,532 19,950 19,714 21,253 27,404 32,399Purchase of Raw Materials 3,432 3,823 5,302 6,329 6,069 6,777 8,769 10,044Purchase of stock in trade (227) 79 (366) 122 1,058 673 548 486Employee Costs 1,280 1,714 2,401 2,344 2,627 2,900 3,699 4,536Other Expense 4,883 4,357 6,023 7,261 7,588 8,388 10,550 12,312EBITDA 1,416 1,853 2,171 3,895 2,372 2,515 3,837 5,022Interest 1,231 1,047 271 250 272 282 275 274Depreciation 352 414 505 570 712 911 1,000 1,100Other Income 1,475 1,316 950 127 130 220 150 180PBT 1,307 1,708 2,344 3,202 1,518 1,543 2,712 3,828Tax 551 560 742 908 619 592 895 1,263Adjusted Net Profit 3,082 3,795 5,151 2,192 897 915 1,817 2,565

Balance Sheet (Rs. Mn) FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16EShareholders Funds 5,039 5,929 7,455 9,470 10,592 11,060 12,877 15,441Non-Current Liabilities 3,883 3,154 2,678 2,569 2,556 2,516 2,500 2,610Current Liabilities 3,753 3,601 4,158 4,837 5,224 5,672 5,123 5,709Minority Interest 486 490 594 775 738 699 - -Total Liabilities 13,161 13,173 14,886 17,651 19,109 19,947 20,499 23,760

Non Current Assets 6,820 6,943 7,106 7,824 9,601 9,784 10,250 10,555Current Assets 6,341 6,230 7,780 9,826 9,508 10,163 10,249 13,206Misc. Expenditure - - - - - - - -Total Assets 13,161 13,173 14,885 17,650 19,109 19,947 20,499 23,760

Important Ratios FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16EROA (%) 4 5 % 5 5 % 7 2 % 2 8 % 9 % 9 % 1 8 % 2 4 %ROE (%) 6 5 % 6 9 % 7 7 % 2 6 % 9 % 8 % 1 5 % 1 8 %ROCE (%) 3 6 % 3 5 % 3 2 % 3 6 % 2 0 % 2 0 % 1 9 % 2 1 %Current Ra<o 1 . 6 9 1 . 7 3 1 . 8 7 2 . 0 3 1 . 8 2 1 . 7 9 2 . 0 0 2 . 3 1Debt-‐Equity Ra<o 0 . 5 1 0 . 4 3 0 . 3 5 0 . 2 6 0 . 2 5 0 . 2 6 0 . 2 4 0 . 2 2

Margins (%) FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16EEBITDA Margin 13% 16% 14% 20% 12% 12% 14% 16%EBT Margin 12% 14% 15% 16% 8% 7% 10% 12%PAT Margin 29% 32% 33% 11% 5% 4% 7% 8%

Analyst Cer;fica;on:

The Research Analyst(s) who prepared the research report hereby cer<fy that the views expressed in this research report accurately reflectthe analyst(s) personal views about the subject companies and their securi<es. The Research Analyst(s) also cer<fy that the Analyst(s) havenot been, are not, and will not be receiving direct or indirect compensa<on for expressing the specific recommenda<on(s) or view(s) in thisreport.

Disclaimer:

This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision.Nothing in this document should be construed as investment or financial advice, and nothing in this document should be construed as anadvice to buy or sell or solicita<on to buy or sell the securi<es of companies referred to in this document. Each recipient of this documentshould make such inves<ga<ons as it deems necessary to arrive at an independent evalua<on of an investment in the securi<es of companiesreferred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks ofsuch an investment. This document is being supplied to you solely for your informa<on and may not be reproduced, redistributed or passedon, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose.

This document does not cons<tute or form part of any offer for sale or subscrip<on or incita<on of any offer to buy or subscribe to anysecuri<es. Paterson Securi<es makes no representa<on or warranty, express or implied, as to the accuracy, completeness or fairness of theinforma<on and opinions contained in this document. Paterson Securi<es, its affiliates, and the employees of Paterson Securi<es and itsaffiliates may, from <me to <me, effect or have effected an own account transac<on in, or deal as principal or agent in or for the securi<esmen<oned in this document. This report has been prepared on the basis of informa<on, which is already available in publicly accessiblemedia or developed through the independent analysis of Paterson Securi<es.

Copyright in this document vests with Paterson Securi;es

Research Partner Page 13 of 13

![[TTM] Incoterms [Trabajo]](https://img.dokumen.tips/doc/110x75/5571fe0e49795991699a8941/ttm-incoterms-trabajo.jpg)