Embed Size (px)

Citation preview

CAPITAL STRUCTURE

� Two primary funding sources: debt and equity

� Each source has different risk level

� Each funding source must be compensated for opportunitycost of what suppliers of funds can earn elsewhere, oninvestments of equivalent risk

� In order to be accepted, projects must increase owners’expected utility of wealth

Each project must provide, on a risk adjusted basis, enoughCF to pay required returns to equity and debt holders, payback original investments, and leave something extra toincrease owners’ (equity holders’) EU of wealth.

� Cost of capital: minimum risk adjusted return toshareholders

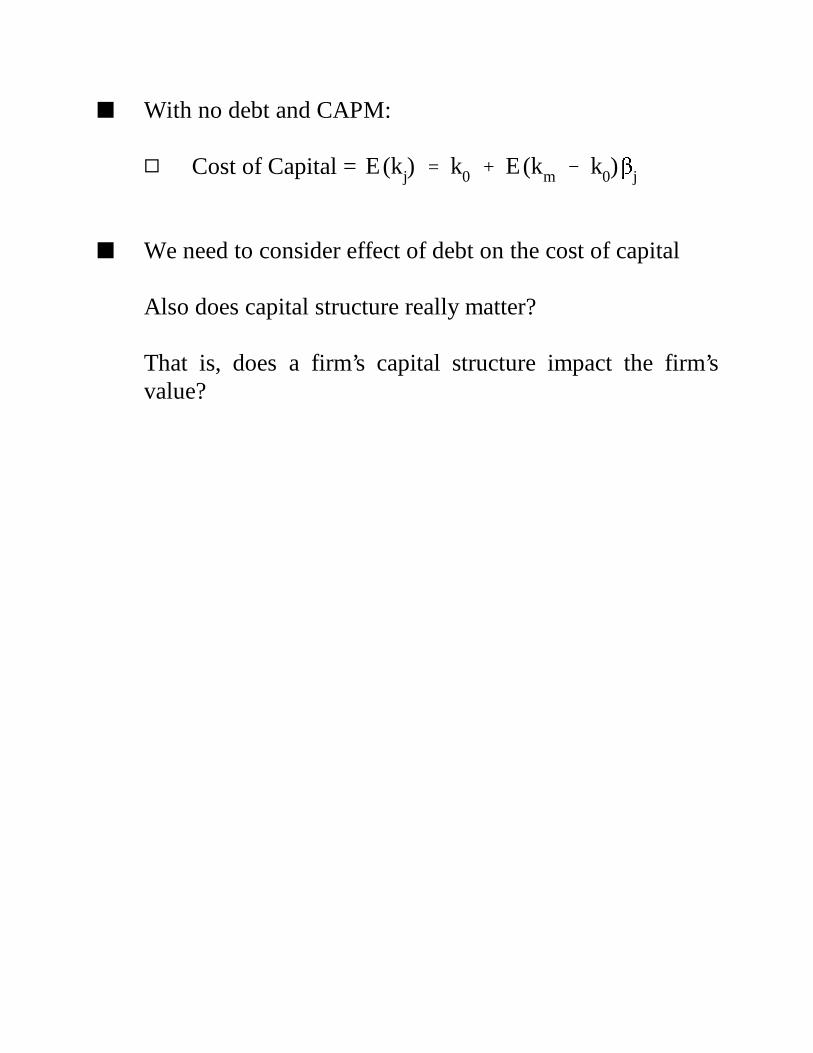

� With no debt and CAPM:

� Cost of Capital = E(kj) � k0 � E(km � k0) j

� We need to consider effect of debt on the cost of capital

Also does capital structure really matter?

That is, does a firm’s capital structure impact the firm’svalue?

VALUE OF THE FIRM WITH CORPORATE TAXES

� Value of a Levered Firm

� Modigliani and Miller (1958, 63)

� Capital markets are frictionless� Borrow and lend at the risk-free rate� No cost to bankruptcy� Two types of claims: risk-free debt and (risky)

equity� All firm’s in the same risk class� Only corporate taxes� All CFs are perpetuities (no growth)� No signaling opportunities� Managers maximize shareholder wealth

� Many of the assumptions can be relaxed without changingmajor conclusions

� e.g., risk-free assumption on debt can be relaxedwithout impacting results

� Bankruptcy and personal tax assumptions do have criticalimpact on results

� Clarification: All firms in the same risk class

� Implication: Risky CFs vary only by a scale factor

where = constant scale factorCFi � CFj

In other words, CFs are perfectly correlated

Consider gross returns

rit �CFit � CFit&1

CFit&1

CFi � CFj � rit �CFjt � CFjt&1

CFjt&1

�CFjt � CFjt&1

CFjt&1

� rjt

So if CFs differ only by scale factor, they will have thesame distribution of returns, the same risk, and will requirethe same expected return.

� Assume the firm’s assets generate the same distribution ofoperating CFs each period after-taxes forever.

Thus value of the firm without any debt is

V u �E(c)ku

where

Vu = present value of an unlevered firm

= expected after-tax cash flow in perpetuityE(c)

ku = discount rate for all equity firm

Remember stuff on estimating CF

˜ATCF � ˜NIAT � Dep

� (R � Vc � Fc � Dep)(1 � tc) � Dep

� no other accruals� no interest cost because no debt� no growth

V u �E(c)ku

�E( ˜EBIT)(1 � tc)

ku

We've assumed c is generated in perpetuity.

This implies depreciation each year must be replaced byinvestment in order to keep the same amount of capital inplace.

Thus we're assuming Dep = I where I is capital investmenteach year.

= c ˜NIAT � Dep � I

= ( ˜Rev � Vc � Fc � Dep)(1 � tc) � Dep � I

= ( ˜Rev � Vc � Fc � Dep)(1 � tc)

= ( ˜EBIT)(1 � tc) � ˜NIAT

When all CFs are perpetuities, CFs to investors is the sameas NIAT, so

� Now assume the firm issues debt

After-tax CFs must be split between debt and equityholders

� Equity holders get: ˜NIAT � Dep � I

Debt holders get: kd D

where kd = interest rate on debtD = face value of debt

� Thus to total CF to debt and equity holders is

( ˜NIAT � Dep � I) � kd D �

( ˜Rev � Vc � Fc � Dep � kd D)(1 � tc) � Dep � I � kd D

� Assuming no growth (Dep = I), the total CF is

= ˜NIAT � kd D ˜EBIT(1 � tc) � kd Dtc � �

CF to unlevered Tax shield from firm . Will have using debt (risk-free(c) same risk level. by assumption).

V L �E( ˜EBIT)(1 � tc)

ku

�kd Dtc

k0

� Discounting each CF by the appropriate discount rate forits risk class, we find the value of the levered firm to be

where VL = value of levered firmk0 = risk-free rate

Note: kdD is the perpetual stream of risk-free paymentsto debt holders

This implies the market value of the risk-freedebt is

B = = market value of debt (bonds)kd D

k0

� Rewriting we find,

VL = Vu + Btc

Value of a levered firm is equal to the value of theunlevered firm plus the present value of the tax shieldprovided by debt.

Note that in the absence of any market imperfections(i.e. tc = 0), the value of the firm is not dependent onthe capital structure of the firm

V L � V u (if tc � 0)

This famous result is known as Modigliani-MillerProposition I (MMI).

MMI (Arbitrage argument) (tc = 0)

2 firms, identical except for capital structures

Lever Company Unlevered CompanyE(EBIT) = $200 E(EBIT) = $200VL = ? Vu = $1000BL = 500 Bu = 0EL = ? Eu = 1000kd = .10 ku = .20

V u �E(EBIT)

k u�

200.20

� $1000

Strategy I: Buy 10% of Unlevered

Investment Cash Flow

.10($1000) = $100 .10( ˜EBIT) = .10(Vu)

� Strategy II: Buy 10% of Levered Company’s Equity

Investment Cash Flow.10(EL) = .10(VL - BL) .10( ˜EBIT � kd BL)

Common argument: VL (and EL/share) should be lowerbecause of increased riskassociated with leverage.

� Strategy III: Buy 10% of Unlevered using combination ofborrowed funds and equity funds

Borrow 10% of BL and combine with equity funds to buy10% of Vu.

Investment Cash Flow

Borrow 10% of BL -.10BL -.10 kd BL

Buy 10% of Vu .10Vu .10( ˜EBIT)

Total .10(Vu - BL) .10 - kdBL)( ˜EBIT

Important Point: Cash flows from buying levered firm areidentical to borrowing and buying unleveredfirm.

(CF to Strategy II = CF to Strategy III)

Therefore: Cost of each strategy must be the same.

Cost of Strategy II Cost of Strategy III

.10 (VL - BL) .10(Vu - BL)

Thus rational investors will require

VL = Vu (MMI)

� Critically important result in finance

� Before MMI, effects of leverage misunderstood

MMI shows if levered firms are priced too high, individuals willsimply borrow on their own accounts and buy shares inunlevered firms.

� Leverage doesn’t effect value of firm!

Example

Consider decision to use debt in BigAg Company.

Financial Structure (tc = 0)

Current Proposal Assets $8,000,000 $8,000,000Debt 0 4,000,000Equity 8,000,000 4,000,000Interest Rate 10% 10%Shares 400,000 200,000Value/Share $20 $20

IMPACT OF CAPITAL STRUCTURE ON RETURNS

No Debt Debt = $4,000,000 @ 10%

Recession Expected Expansion Recession Expected Expansion

ROA 5% 15% 25% 5% 15% 25%

EBIT $400,000 $1,200,000 $2,000,000 $400,000 $1,200,000 $1,200,000

Int 0

0 0 400,000 400,000 400,000

NIAT 400,000 1,200,000 2,000,000 0 800,000 1,600,000

ROE 5% 15% 25% 0 20% 40%

EPS $1.00 $3.00 $5.00 0 $4.00 $8.00

Analysis: Effect of financial leverage depends on company’s income.

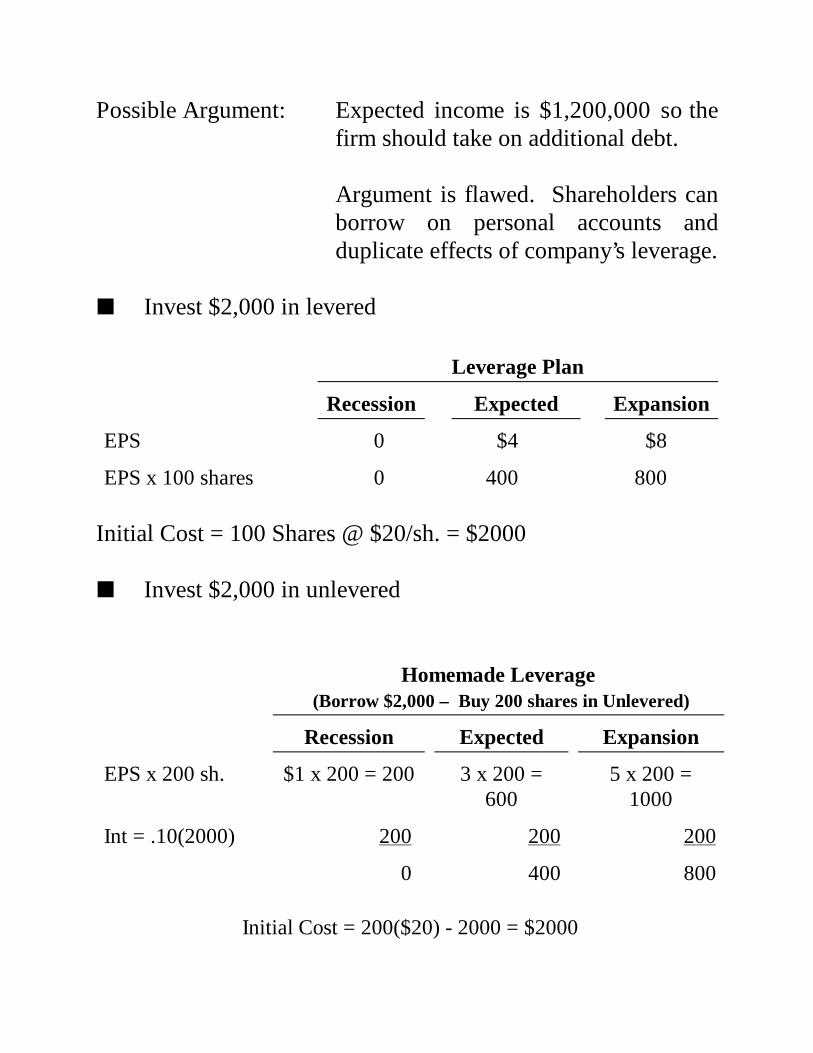

Possible Argument: Expected income is $1,200,000 so thefirm should take on additional debt.

Argument is flawed. Shareholders canborrow on personal accounts andduplicate effects of company’s leverage.

� Invest $2,000 in levered

Leverage Plan

Recession Expected Expansion

EPS 0 $4 $8

EPS x 100 shares 0 400 800

Initial Cost = 100 Shares @ $20/sh. = $2000

� Invest $2,000 in unlevered

Homemade Leverage (Borrow $2,000 – Buy 200 shares in Unlevered)

Recession Expected Expansion

EPS x 200 sh. $1 x 200 = 200 3 x 200 =600

5 x 200 =1000

Int = .10(2000) 200 200 200

0 400 800

Initial Cost = 200($20) - 2000 = $2000

V L � V u � Btc

� This is another illustration of MMI. In a world withouttransaction costs, capital structure doesn’t matter.

Effectively, increases in expected returns from leverage areoffset by additional risk (more later).

� Doesn’t match reality

� Letting tc > 0,

giving debt preferential tax treatment (allowing a taxdeduction for interest payments) increases the value of thefirm as the firm takes on more and more debt.

� firms should use almost all debt financing.

� Doesn’t match reality

WEIGHTED AVERAGE COST OF CAPITAL (WACC)

Suppose project is funded with

B = $ by debt holdersE = $ by equity holders

I = $ of initial investment

I = B + E

The WACC is defined so that suppliers of capital receive theirrespective required return given the risk they must bear.

Debt holders require kd. After-tax cost = kd(1 - tc)

Equity holders require ke.

I kw = B kd(1 - tc) + E ke

kw = WACC

kw �BI

kd (1 � tc) �EI

ke

kw � wd kd (1 � tc) � we ke (WACC)

Let wd �BI

and we �EI

� Could allow multiple debt and equity types

� wd and we often assumed set at some "target level" (morelater)

� kw supplies required return to each contributor of capital

V u ku � tcBkd � Eke � Bkd

ke �V u

Eku � (1 � tc)

BE

kd

Relationship between ke and debt

VL = Vu + Btc

� Expected ATCF into levered firm

Vu (ku) + (kd)Btc� �

same risk same risk as as c kd D

� Expected ATCF to debt and equity holders

Eke � Bkd

� Cash inflows = cash outflows (no growth)

Remember

V L � V u � tcB � B � E

so V u � E � B(1 � tc)

Substituting,

ke �E � B(1 � tc)

Eku � (1 � tc)

BE

kd

� ke � ku � (1 � tc) (ku � kd)BE

(MMII)

� Opportunity cost of equity capital increases linearly

with a change in .BE

� With no debt, ke = ku.

Example:

AGFIRM is currently unlevered. It is considering restructuringto allow $200 in debt. Company expects to generate $151.52 inEBIT (perpetuity). Corporate tax rate = 34%. Cost of debt is10%. Unlevered firms in the industry require a 20% return.

� What will AGFIRM’S value be if it restructures?

E( ˜ATCFu) � E( ˜EBIT)(1 � tc)

� $151.52(1 � .34)

� $100

V u �E(ATCF u)

k u�

100.20

� $500

V L � V u � tcB � $500 � 200(.34) � $500 � $68

� $568

Suppose AGFIRM started with 500 shares

Share priceu = V u

shares�

$500500

� $1

Share priceL = V L � B

shares�

$568�$200300

� $1.23

Value of equityL = EL = VL - B = $568 - $200 = $368

� What is the required return on AGFIRM’s equity?

ke � ku � (1 � tc) (ku � kd)BE

� .20 � (1 � .34)(.20 � .10) 200368

� .2359

Use of debt increased required return on equity fromku = .20 to ke = .2359

Check

E L �(E(EBIT) � kd B)(1 � tc)

ke

= $368�(151.52 � .10(200)) (1 � .34)

.2359

� Find AGFIRM’s WACC

wd �B

V L�

200568

� .352 we �368568

� .648

kw = weke + wdkd (1- tc)

= (.648)(.2359) + (.352) (.10)(1 - .34)

= .15286 + .02323

= .1761

The firms WACC decreased from kw = ku = 20% tokw = 17.61% as a result of the debt use.

Check value of the firm

$568V L �E(EBIT)(1 � tc)

kw

�151.52(1 � .34)

.1761�

Suppose the firm holds a $100 in assets. Required paymentto capital suppliers = I · kw

= 100 · .1761= $17.61

Funding Required Cash Source Investment Return

Flow

Equity .648(100) = $64.88 .2359 $ 1 5 .28

Debt .352(100) = 35.20 .10 3.52Govt. tax shield = $3.52(.34) (1.20)Total 100 .1761 $17.60

%

ku

ke=ku+(ku-kd) B/S

kw = ku

kd

B/E

kw � weke � wd kd

�E

B�Eke �

BB � E

kd

�E

B�E(k u � (k u � kd)

BE

) �B

B�Ekd

�E

B�Ek u �

BB�E

(k u � kd) �B

B�Ekd

� k u

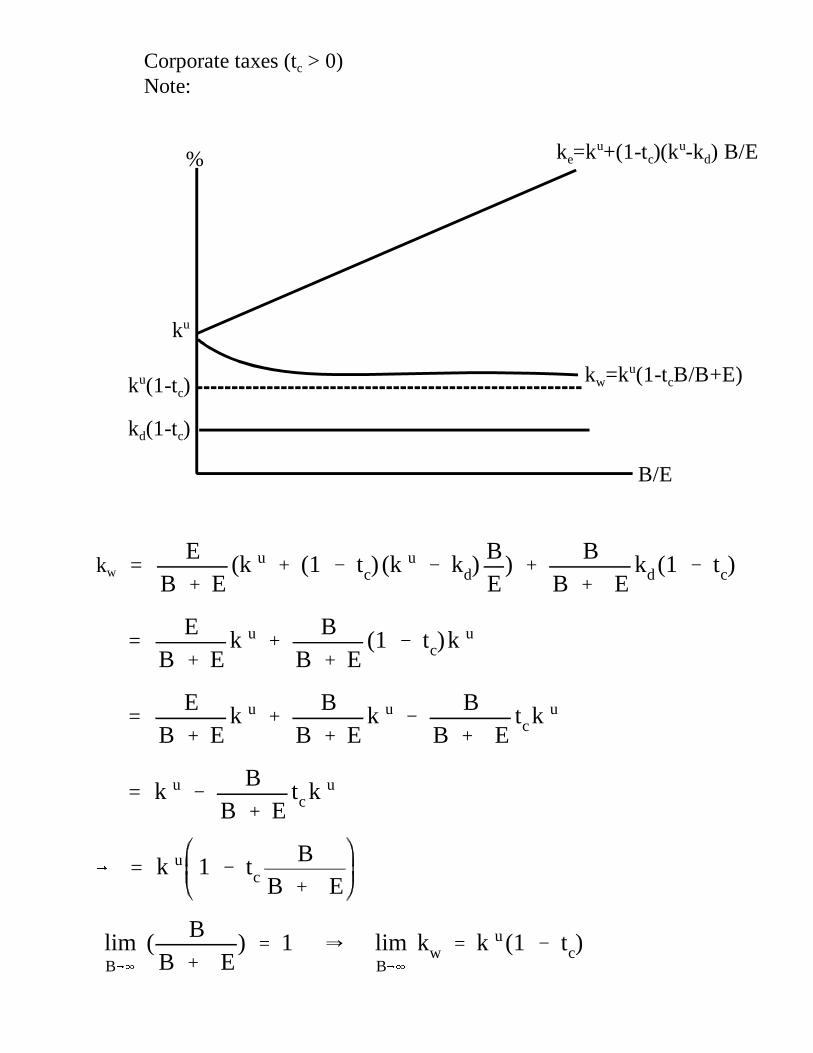

GRAPHICAL LOOK AT COST OF CAPITAL

� No taxes

Note:

%

ku

ke=ku+(1-tc)(ku-kd) B/E

B/E

kw=ku(1-tcB/B+E)ku(1-tc)

kd(1-tc)

Corporate taxes (tc > 0)Note:

kw = E

B � E(k u � (1 � tc) (k u � kd)

BE

) �B

B � Ekd (1 � tc)

= E

B � Ek u �

BB � E

(1 � tc)k u

= E

B � Ek u �

BB � E

k u �B

B � Etck u

= k u �B

B � Etc k u

6 = k u 1 � tcB

B � E

limB64

(B

B � E) � 1 � lim

B64kw � k u (1 � tc)

With or without taxes, increasing debt increases ke because of higherrisk (also higher expected return).

However, value of firm and equity claims only change as a result oftax shield.

V L �E(EBIT)(1 � tc)

kw

� Btc

Without taxes reduces to

V L �EBIT

k u

Results so far:

Without taxes — Capital structure irrelevant

Corporate taxes — Firms should use almost all debt

CAPITAL STRUCTURE — LIMITS TO DEBT USE

� Remember: world without personal taxes

VL � V u � tcB

� Firms should use all debt financing

� Inconsistent with real world

� MM theory help point out possible answers

� Financial distress costs

� Personal taxes

� Bankruptcy: Risk or Cost?

� Debt provides tax benefits

� Debt also puts financial pressure on firm

� Ultimate financial distress � bankruptcy

� Bankruptcy costs can offset benefits of debt

Example (no taxes)

Day Company and Knight Company both plan to operate one moreyear.

Knight Company: $49 principle and interest obligationDay Company: $60 principle and interest obligation

Both companies have the same operating CFs.

Knight Company DayCompany

Boom Rec Boom Rec

Prob. (.50) (.50) (.50) (.50)

CF 100 50 100 50

Debt 49 49 60 60 50

Distribution toStockholders

51 1 40 0

Day Company bankrupt in regression

Assume: Risk neutral investorsInterest rate ke = kd = 10%

Ek�(.5) (51)� (.5) (1)

1.10�23.64 ED�

(.5) (40)� (.5) (0)1.10

�$18.18

Bk�(.5)49� (.5) (49)

1.10�44.54 BD�

(.5) (60)� (.5) (50)1.10

�50 Vk 68.18 VD 68.18

� Firms have same value

� Debt holders recognize bankruptcy impacts

Promised payment $60, but debt holders only willing topay $50.

Required payment without bankruptcy

= $54.5560

(1 � .10)

Actual yield on Day’s debt

(junk bond)6050

� 1 � .20 or 20%

Example is unrealistic

Reality: lawsuits, liquidation, other cost increaserealized bankruptcy costs

Suppose these costs = $15

$50Debt

$100 $50

$60Debt

$40Eq.

$100 $50

$60Debt

$40Eq.

$15B. cost

$35Debt

Day Company(.5)

Boom(.5)Rec

CF 100 50 - 15 ED �(.5) (40) � (.5) (0)

1.10� 18.18

Debt 60 60 50 35 BD = = 43.18(.5)(60) � (.5) (35)

1.10

Distributionto Equity

40 0 VD 61.36

� Bankruptcy "costs" reduce value of firm

� Bankruptcy "risk" did not impact firm value

Without bankruptcy costs

With bankruptcy costs

Debt and Equityholders no longersplit earnings

Bondholders account for bankruptcy "costs" in returns

$60$43.18

� 1 � 39.0%

Bond holders pay fair price after accounting for prob. andcosts of bankruptcy

SupposeRepayment Amount

Rec Prob Bankruptcy Cost Promise Borrowed

0 0 60 $54.55 .5 0 60 50.00 .5 $15 60 43.18

� Bankruptcy costs increase cost of debt

� Financial distress causes same impact as bankruptcycosts

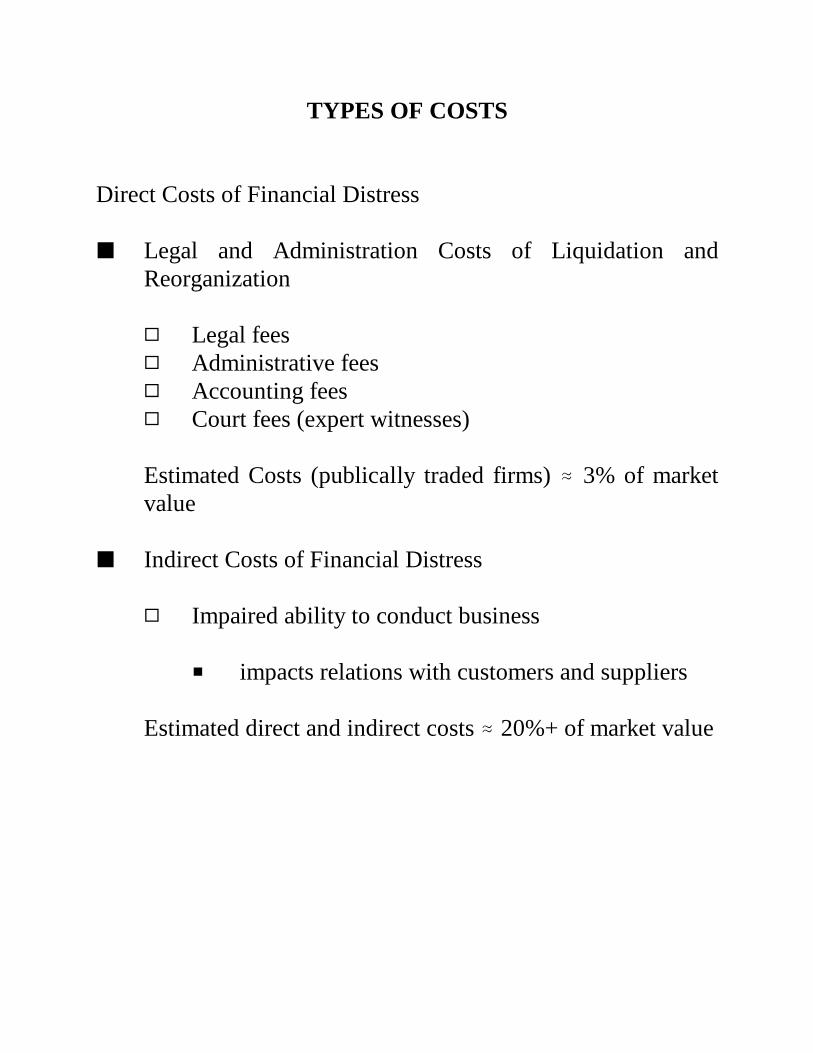

TYPES OF COSTS

Direct Costs of Financial Distress

� Legal and Administration Costs of Liquidation andReorganization

� Legal fees� Administrative fees� Accounting fees� Court fees (expert witnesses)

Estimated Costs (publically traded firms) � 3% of marketvalue

� Indirect Costs of Financial Distress

� Impaired ability to conduct business

� impacts relations with customers and suppliers

Estimated direct and indirect costs � 20%+ of market value

AGENCY COSTS

Conflict of interest between shareholders and debt holders

1. Incentives to take large risks

� Firms near bankruptcy take larger risks

Suppose promised debt payment is $100

Low Risk Project Prob. Value = Equity + Debt

Rec. .5 $100 = 0 + 100Boom .5 200 = 100 + 100

VL� (.5) (100) � (.5) (200) � $150

High Risk Project Prob. Value = Equity + Debt

Rec. .5 $ 50 = 0 + 50 (bankrupt)Boom .5 240 = 140 + 100

VH � (.5) (50) � (.5) (240) � $145

All equity firm would select low risk project

VL > VH

However equity value is

EL= (.5)(0) + (.5)(100) = 50EH = (.5)(0) + (.5)(140) = 70

Equity holders will want high risk project when debt isused.

2. Incentive toward under investment

New investment may help debt holders at shareholdersexpense

Consider firm

$4,000 debt payment due at end of yearBankrupt in recession

Project cost $1,000 and brings in $1,700

Firm without Project Firm with Project (.5) (.5) (.5) (.5)Boom Rec Boom Rec

CFs 5,000 2,400 6,700 4,100Debt 4,000 2,400 4,000 4,000

1,000 0 2,750 100

Debt holders prefer project

Suppose $1,000 cost of project comes from equity

Ew/o = (.5) 1,000 + (.5) 0 = $500

Ew = (.5) (2,700) + (.5)(100) - 1,000 = $400

Equity holders prefer to reject project.

Equity holders contribute entire investment but must sharerewards.

3. Milk Property — like strategy 2 except instead ofdeciding not to invest you actuallydivest through increasing dividends.

� These strategies only occur when there is a possibilityof bankruptcy

Again — increases the cost of debt

� May be reduced through "protective covenants" inloon documents

� Negative Covenants (limit actions)

restrict dividends, collateral, mergers, assetsales, debt levels

� Positive covenant (specify action)

NWC, financial statements

� Debt Consolidation also reduces bankruptcy costs

MaximumValue

Value ofFirm

B*Debt

(Optional debt level)

Vu

VL = Vu + tcB

PV of financialdistress cost

PV of taxshield

� Combining the tax effects and financial distresscosts

Tax shield � � value of firm

Distress costs � � value of firm

VALUATION UNDER PERSONALAND CORPORATE TAXES

� Earlier we saw gains in leverage with only corporate taxes:

G � V L � V u � tcB

� Now consider value of firm in a world with both corporateand personal taxes

Equity holders receive (EBIT - kdB)(1 - tc)(1 - te)

Debt holders get kdD(1 - td)

Total CF to all stakeholders:

(EBIT � kd D)(1 � tc) (1 � te) � kd D(1 � td)

or

EBIT (1 - tc)(1 - te) + kdD(1 - td) 1 �(1 � tc) (1 � te)

(1 � td)

� �CF to unlevered CF to debtfirm after taxes holders after

taxes

So

VL � Vu � B 1 �(1 � tc) (1 � te)

(1 � td)

where B = kdD (1 - td) / kd

Gain from leverage in world with personal taxes

G � B 1 �(1 � tc) (1 � te)

(1 � td)

Notes:

� When te = td, gain is same as in world without personaltaxes

� When te < td, gain from leverage is reduced from worldwithout personal taxes

� Reasons te may be less than td

� capital gains tax break� capital gains may be delayed by reinvestment� gains and losses in a portfolio may offset each other� dividend exclusions for corporations

when te < td, more taxes get paid in a levered firm, thanan unlevered firm at the personal level

$

B

$

B

VL = Vu + tcB when te = td

VL = Vu + B[1-(1-td)

]

when (1-td) > (1-tc)(1-te)

(1-tc)(1-te)

VL = Vu when

(1-td) = (1-tc)(1-te)

� If , gain from leverage is zero.(1 � tc) (1 � te) � (1 � td)

Lower corporate taxes from leverage are exactly offset byhigher personal taxes.

TAX POLICY AND FINANCING INCENTIVES

Before 1986: Corporate Income – 46% maximumInterest and Dividends – 50% maximumCapital Gains – 20%

Suppose firm pays no dividends and capital gains are deferredso that the effective tax rates are te = 10%, td = 50% and tc = 46%.

Interest Equity IncomeIncome before tax $1.00 $1.00Less Corporate tax @ 46% 0.00 0.46Income after Corporate tax 1.00 0.54Less Personal tax (te=.10 and td=.50) 0.50 0.054Income after tax $0.50 $0.496

Small advantage to debt = $.004

Essentially no advantage to debt

1999: Corporate Income – 35% maximumInterest and Dividend – 39.6% maximumCapital Gains – 20%

Suppose effective capital gains rate is 20%/2 = 10% and that nodividends are paid.

Interest Equity IncomeIncome before tax $1.00 $1.00Less Corporate tax (tc = 35) 0.00 0.35Income after Corporate tax 1.00 0.65Personal tax (td=.396 and te=.10) 0.396 0.065Income after tax $0.604 $0.585

Advantage to debt = $0.019

Now suppose the same firm in 1999 pays out 1/2 of equityincome as dividends.

Effective tax rate on equity (.396 + .10)/2 = .248)

Interest Equity IncomeIncome before tax $1.00 $1.00Less Corporate tax (tc=.35) 0.00 0.35Income after Corporate tax 1.00 0.65Personal tax (td=.396 and te=.248) 0.396 0.161Income after tax $.604 $0.489

Advantage to debt = $.115

� Advantage tends to favor debt

� Magnitude not clear and depends on tax rates of equity anddebt holders as well as dividend payout rates

EXAMPLE

(perpetuity)E(EBIT) � $100,00

tc � 34% te � 12% td � 28%

ku (1 � tc) � 15%

Currently all equity, but considering borrowing $120,000at 10%.

V u �$100,000(1� .34)(1� .12)

.15(1� .12)� $440,000

VL � $440,000 � $120,000 1 �

(1 � .34)(1 � .12)(1 � .28)

� $463,200

= $23,230G � VL � Vu � 463,200 � 440,000

Smaller than tcB = .34(120,000) = $40,800

Extra tax on debt (td > te) at personal level lowers gainsfrom debt

� Implications

� Gains from leverage still positive (probably) butsmaller than thought if te < td

� "Grossed" up return on debt to equate after-tax returns(if te < td) offsets same debt advantage

Result

� Framework also lays out arguments for equilibriumaggregate debt levels (another day)

� How firms establish capital structure

� Practical difficulties — no "formula" for optimaldebt structure

� Empirical Evidence

� Most firms have "low" D/E.

U.S. average D/E : .3 to .5

Firms pay substantial taxes but clearly don't issuedebt to point where tax shield is exhausted

� Announced increases (decreases) in anticipatedleverage tend to increase (decrease) firm value

� Capital structures differ by industry

� Profitability� Growth� Intangible assets

� Firms tend to maintain target levels at D/E

FACTORS TO CONSIDER IN DETERMININGTARGET D/E

� Taxes (tax shield)

� Financial Distress Cost

� Variable income � increase probability of financialdistress

� Tangible assets � less financial distress� Intangible assets � more financial distress

� Credit Reserves

� External equity can be expensive to issue relative tointernal equity

� Maintain credit capacity (low D/E) to allow capitalexpenditures without issuing new equity

� Industry D/E Ratios

Reconciling M-M and CAPM

Unifies approach to determining discount rate (cost of capital)

Type ofCapital CAPM MM

Debt kd = krf + (km-krf) d kd = krf , d = 0

Unlevered Equity ku = krf + (km-krf) u ku = ku

Levered Equity ke = krf + (km-krf) L ke = ku + (ku -kd)(1-tc) B/E

WACC kw = weke + wdkd(1 - tc)

kw � ku 1 � tcB

B�E

wd �B

B�Ewc �

EB�E

Can easily modify MM risk-free debt assumption:

kd � krf � (km � krf) d

Relationship between L + u

ke � krf � (km � krf) L � ku � (ku � kd) (1 � tc)BE

Substitute kd � krf � (km � krf) d

ku � krf � (km � krf) u

Rearrange and simplify

L � u � ( u � d) (1 � tc)BE

� u (1 � (1 � tc)BE

) � d (1 � tc)BE

If we observe L, we can estimate u

u �

L � d (1 � tc)BE

1 � (1 � tc)BE

EXAMPLE

Currently wd = .2 (market value)Considering wd = .35

kd = krf = .07 ( d = 0)tc = .5km = .17

L = .5 (wd = .20)

� Find the current values of ke and kw

ke � krf � (km � krf) L

� .07 � (.17 � .07) .5

� .12 or 12% (at wd � .2)

kw � weke � wd kd (1 � tc)

� (.8) (.12) � (.2) (.07)(1 � .5)

� .103 or 10.3% (at wd � .2)

� Find kw if the new target capital is wd = .35

Remember ke will increase as the debt level rises relative toequity

MM’s definition of kw says

kw � ku 1 � tcB

B � E

which implies (using observed results at wd = .20)

ku �kw

1 � tcB

B � E

�.103

1 � (.5)(.2)� .1144

So if wd = .35, MM’s definition of kw says

kw = .1144 (1 - (.5)(.35)) = .09438 or 9.438%

� We could have calculated the new L and ke and precededwith the standard kw approach directly

At wd = .2, Remember d = 0u �L

1 � (1 � tc)BE

�.5

(1 � (1 � .5)(.25))� .4444

So at wd = .35, the new L will be

L � 1 � (1 � tc)BE u

� [1 � (1 � .5)(.5385)] (.4444)

� .5641 (at wd � .35)

Thus ke = krf + (km - krf) L = .07 + (.17 - .07) .5641

= .1264

and

kw � wd ke � wd kd (1 � tc) (at wd � .35)

� (.65)(.1264) � (.35)(.07)(1 � .5)

� 0.944 or 9.44%

� Suppose project has same systematic risk as firm, L, andprovides expected return at 9.25%. Should project betaken?

%

B/E

ke

25% 53.85%

12.6%

12%

10.39.4

ku(1 - tc)kd(1 - tc)

kw = ku (1 - tc (B/B+E))

E(kp) � .0925 < kw � .0944

� Evaluating projects with different risk levels than the firm.

� Find the required return assuming all equityinvestment.

� Adjust for the firm’s capital structure using theapproach(s) from the previous section.

Example: uj � 1.2, krf � .07, km � .17

� = krf + (km - krf) k uj

uj

= .07 + (.17 - .07) 1.2 = .19 or 19%

� kw = ku (1 - (1 - tc) B/B+E)

= .19 (1 - (.5) (.20)) = .171 or 17.1% at wd = .2

= .19 (1 - (.5) (.35)) = .157 or 15.7% at wd = .35

� Comment on RTA vs. RTE

� Comment on business organizations