Embed Size (px)

Citation preview

Capital Raising Prospectus 2017 Securing the UK’s Digital Future

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION.

If you are in any doubt as to what action you should take, you are recommended to seek your own financial advice immediatelyfrom your stockbroker, bank manager, solicitor, accountant, fund manager or other appropriate independent financial adviser,who is authorised under the Financial Services and Markets Act 2000 (“FSMA”) if you are resident in the United Kingdom or, ifnot, from another appropriately authorised independent financial adviser.

If you sell or have sold or otherwise transferred all of your Existing Ordinary Shares, please send this document, and Form of Proxy atonce to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for delivery tothe purchaser or transferee, except that such documents should not be distributed, forwarded to or transmitted in or into any jurisdictionwhere to do so might constitute a violation of local securities laws or regulations, including but not limited to the United States and any ofthe other Excluded Territories.

The distribution of this document, any other offering or publicity material relating to the Placing and/or the Offer for Subscriptionand/or any Application Forms into jurisdictions other than the United Kingdom may be restricted by law or regulation. Personsinto whose possession these documents come should inform themselves about and observe any such restrictions. In particular,subject to certain exceptions, such documents should not be distributed, forwarded to or transmitted in or into the United States orany other Excluded Territory. The transfer of the New Ordinary Shares may also be so restricted by law or regulation. Any failureto comply with these restrictions may constitute a violation of the securities laws or regulations of any such jurisdiction. The NewOrdinary Shares are not transferable except in accordance with, and the distribution of the foregoing documents is subject to, therestrictions set out in section 5 of Part 2 of this document. No action has been taken by CityFibre, Citi, finnCap, Liberum, Macquarie orRothschild, that would permit an offer of the New Ordinary Shares, or possession, distribution, forwarding or transmission of the foregoingdocuments in or into any jurisdiction where action for that purpose is required, other than the United Kingdom.

CityFibre Infrastructure Holdings plc(Incorporated and registered in England and Wales, with registered number 08772997)

Proposed Placing of 363,636,364 Placing Shares at 55 pence per Placing Share

Proposed Offer for Subscription of up to 27,272,727 Offer for Subscription Shares at 55 pence perOffer for Subscription Share

Notice of General Meeting

Sole Global Co-ordinator, JointBookrunner and Joint Underwriters

Nominated Advisor andJoint Bookrunner and Joint

Underwriters

Joint Bookrunner and JointUnderwriters

Joint Bookrunner and JointUnderwriters

Financial Advisor

AIM is a market designed primarily for emerging or smaller companies to which a higher investment risk tends to be attachedthan to larger or more established companies. AIM securities are not admitted to the official list of the United Kingdom ListingAuthority.

A prospective investor should be aware of the risks of investing in such companies and should make the decision to invest onlyafter careful consideration and, if appropriate, consultation with an independent financial adviser.

Each AIM company is required pursuant to the AIM Rules for Companies to have a nominated adviser. The nominated adviser isrequired to make a declaration to the London Stock Exchange on admission in the form set out in Schedule Two to the AIM Rulesfor Nominated Advisers.

The London Stock Exchange has not itself examined or approved the contents of this document.

This document, which comprises a prospectus and a circular relating to CityFibre Infrastructure Holdings plc and the Capital Raising andan AIM admission document, has been prepared in accordance with the Prospectus Rules of the UK Listing Authority made under section73A of FSMA, has been approved by the Financial Conduct Authority in accordance with section 85 of FSMA, and is made available tothe public in accordance with Rule 3.2.4(3) of the Prospectus Rules. This document is available at www.cityfibre.com and a printed copyof this document is available on request and free of charge from the Company and finnCap.

The Existing Ordinary Shares have been admitted to trading on AIM. Application will be made to the London Stock Exchange for the NewOrdinary Shares to be admitted to trading on AIM. It is expected that admission of the New Ordinary Shares on AIM will become effective,and dealings in the New Ordinary Shares on AIM will commence, at 8.00 a.m. on 28 July 2017. The New Ordinary Shares are not dealt in onany other recognised investment exchange and no application has been, or is intended to be, made for the New Ordinary Shares to be admittedto trading on any other such exchange. It is emphasised that no application is being made for the admission of the New Ordinary Shares to theOfficial List.

The whole of this document should be read. Shareholders and any other persons contemplating an acquisition of New OrdinaryShares should review the section of this document entitled “Risk Factors” for a discussion of certain factors that should be consideredwhen deciding on what action to take in relation to the Placing and/or the Offer for Subscription or deciding whether or not tosubscribe for or acquire New Ordinary Shares. In making an investment decision each investor must carry out their ownexamination, analysis and enquiry of the Company and the terms of the Capital Raising, including the merits and risks involved.

The latest time and date for application and payment in full for the Offer for Subscription Shares under the Offer for Subscription is11.00 a.m. on 26 July 2017. The procedure for application and payment is set out in Part 2 of this document and, if relevant, also inthe Application Form which is set out at the back of this document.

Notice of a General Meeting of the Company to be held at 11.30 a.m. on 27 July 2017 at CMS Cameron McKenna Nabarro OlswangLLP, Cannon Place, 78 Cannon St, London EC4N 6AF is set out at the end of this document. A Form of Proxy for use in connectionwith the General Meeting is enclosed and, to be valid, should be completed and returned as soon as possible, by post toComputershare Investor Services PLC, Corporate Action Projects, Bristol BS99 6AH or by hand to Computershare Investor ServicesPLC, The Pavilions, Bridgwater Road, Bristol BS13 8AE, by not later than 11.30 a.m. on 25 July 2017. Return of Forms of Proxy willnot prevent Shareholders from attending the General Meeting.

Citigroup Global Markets Limited (“Citi”), which is authorised by the Prudential Regulation Authority and regulated by thePrudential Regulation Authority and the FCA, is acting as sole global co-ordinator, Joint Bookrunner and Joint Underwriter toCityFibre and no one else in connection with the Capital Raising, and will not be responsible to any person other than CityFibre forproviding the regulatory and legal protections afforded to clients of Citi nor for providing advice in relation to the contents of thisdocument or any matter, transaction or arrangement referred to in it.

finnCap Ltd (“finnCap”), which is authorised and regulated by the FCA, is acting as Nominated Adviser, Joint Bookrunner and JointUnderwriter to CityFibre and no one else in connection with the Capital Raising, and will not be responsible to any person other thanCityFibre for providing the regulatory and legal protections afforded to clients of finnCap nor for providing advice in relation to thecontents of this document or any matter, transaction or arrangement referred to in it. The responsibilities of finnCap, as NominatedAdviser under the AIM Rules for Nominated Advisers, are owed solely to London Stock Exchange and are not owed to CityFibre orany Director or to any other person in respect of their decision to acquire New Ordinary Shares in reliance of any part of thisdocument.

Liberum Capital Limited (“Liberum”), which is authorised and regulated by the FCA, is acting as Joint Bookrunner and JointUnderwriter to CityFibre and no one else in connection with the Capital Raising and will not be responsible to any person other thanCityFibre for providing the regulatory and legal protections afforded to clients of Liberum, nor for providing advice in relation to thecontents of this document or any matter, transaction or arrangement referred to in it.

Macquarie Capital (Europe) Limited (“Macquarie”), which is authorised and regulated by the FCA, is acting as Joint Bookrunnerand Joint Underwriter to CityFibre and no one else in connection with the Capital Raising and will not be responsible to any personother than CityFibre for providing the regulatory and legal protections afforded to clients of Macquarie, nor for providing advice inrelation to the contents of this document or any matter, transaction or arrangement referred to in it.

N M Rothschild & Sons Limited (“Rothschild”), which is authorised and regulated by the FCA, is acting as financial adviser toCityFibre and no one else in connection with the Capital Raising, and will not be responsible to any person other than CityFibre forproviding the regulatory and legal protections afforded to clients of Rothschild nor for providing advice in relation to the contents ofthis document or any matter, transaction or arrangement referred to in it.

Apart from the responsibilities and liabilities, if any, which may be imposed on Citi, finnCap, Liberum, Macquarie and Rothschild byFSMA or the regulatory regime established thereunder or otherwise under law, Citi, finnCap, Liberum, Macquarie and Rothschilddo not accept any responsibility whatsoever for the contents of this document, and no representation or warranty, express or implied,is made by Citi, finnCap, Liberum, Macquarie and Rothschild in relation to the contents of this document, including its accuracy,completeness or verification or regarding the legality of any investment in the New Ordinary Shares by any person under the lawsapplicable to such person or for any other statement made or purported to be made by it, or on its behalf, in connection withCityFibre, the New Ordinary Shares or the Capital Raising and nothing in this document is, or shall be relied upon as, a promise orrepresentation in this respect, whether as to the past or the future. To the fullest extent permissible Citi, finnCap, Liberum,Macquarie and Rothschild accordingly disclaim all and any responsibility or liability whether arising in tort, contract or otherwise(save as referred to above) which they might otherwise have in respect of this document or any such statement.

NOTICE TO OVERSEAS PERSONS

This document does not constitute an offer of, or a solicitation to subscribe for or purchase, any securities in any jurisdiction in which suchoffer or solicitation is unlawful or to any person to whom it is unlawful to make such offer or solicitation. Shareholders in the United States,subject to certain exemptions, may not subscribe for or acquire any New Ordinary Shares in connection with the Capital Raising.

The Existing Ordinary Shares and the New Ordinary Shares have not been and will not be registered under the US Securities Act, or under thesecurities laws of any state or other jurisdiction of the United States and may not be offered, sold, pledged, taken up, resold, transferred ordelivered, directly or indirectly, into or within the United States except pursuant to an applicable exemption from, or in a transaction notsubject to, the registration requirements of the US Securities Act and in compliance with any applicable securities laws of any state or otherjurisdiction of the United States. The New Ordinary Shares offered outside the United States are being offered in reliance on Regulation Sunder the US Securities Act. The New Ordinary Shares offered inside the United States are being offered in reliance on an exemption fromthe registration requirements of the US Securities Act. There will be no public offer of the New Ordinary Shares in the United States.

i

The Company, Citi, finnCap, Liberum, Macquarie and Rothschild do not make any representation to any offeree, subscriber or acquirer of theNew Ordinary Shares regarding the legality of an investment in the New Ordinary Shares by such offeree, subscriber or acquirer under thelaw applicable to such offeree, subscriber or acquirer. Each investor should consult with his or its own advisers as to the legal, tax, business,financial and related aspects of an acquisition of the New Ordinary Shares.

The New Ordinary Shares and this document have not been recommended, approved or disapproved by the SEC, any state securitiescommission in the United States or any other US regulatory authority, nor have any of the foregoing authorities passed upon orendorsed the merits of the offering of the New Ordinary Shares or the accuracy or adequacy of this document. Any representation tothe contrary is a criminal offence in the United States.

The New Ordinary Shares may not be offered, sold, pledged, taken up, resold, transferred or delivered, directly or indirectly, within any of theExcluded Territories (excluding, for these purposes, the United States) except pursuant to an applicable exemption from registration and incompliance with any applicable securities laws. There will be no public offer of the New Ordinary Shares in any of such Excluded Territories.

EXCEPT AS OTHERWISE PROVIDED FOR HEREIN, NEITHER THIS DOCUMENT NOR THE APPLICATION FORMCONSTITUTES AN OFFER OF NEW ORDINARY SHARES TO ANY PERSON WITH A REGISTERED ADDRESS, OR WHO ISLOCATED OR RESIDENT, IN THE UNITED STATES OR ANY OF THE OTHER EXCLUDED TERRITORIES.

The Underwriters may arrange for any Placing Shares not taken up in the Placing to be offered and sold only (i) outside the United States inaccordance with Regulation S under the US Securities Act or (ii) inside the United States to persons reasonably believed to be “qualifiedinstitutional buyers” (“QIBS”) within the meaning of Rule 144A under the US Securities Act in reliance on an exemption from theregistration requirements of the US Securities Act. Any such persons are notified that such offers may be made in reliance on the exemptionfrom the registration requirements of the US Securities Act provided by Rule 144A.

The New Ordinary Shares sold in reliance on Rule 144A are subject to restrictions on transferability and resale and may not be transferred orresold except as permitted under the US Securities Act and applicable securities laws. In jurisdictions where the shares are subject torestrictions on transferability and resale, such shares may not be transferred or resold except as permitted under applicable securities laws andregulations. Prospective subscribers should be aware that they may be required to bear the financial risks of this investment for an indefiniteperiod of time.

In addition, until 40 days after Admission, an offer, sale or transfer of the New Ordinary Shares into or within the United States by a dealer(whether or not participating in the Capital Raising) may violate the registration requirements of the US Securities Act.

All Overseas Persons and any person (including, without limitation, a nominee or trustee) who has a contractual or legal obligation to forwardthis document or any Application Form, if and when received, or any other document to a jurisdiction outside the United Kingdom shouldread section 5 of Part 2 of this document.

ENFORCEABILITY OF US JUDGMENTS

THE COMPANY IS A PUBLIC LIMITED COMPANY INCORPORATED UNDER THE LAWS OF ENGLAND AND WALES.MOST OF THE DIRECTORS AND EXECUTIVE OFFICERS OF THE COMPANY RESIDE OUTSIDE THE UNITED STATES.IN ADDITION, ALL OR SUBSTANTIALLY ALL OF THE ASSETS OF THE COMPANY, THE DIRECTORS AND THECOMPANY’S EXECUTIVE OFFICERS ARE LOCATED OUTSIDE THE UNITED STATES. AS A RESULT, IT MAY NOT BEPOSSIBLE FOR INVESTORS TO EFFECT SERVICE OF PROCESS WITHIN THE UNITED STATES UPON ANY OF THECOMPANY, THE DIRECTORS OR EXECUTIVE OFFICERS OF THE COMPANY LOCATED OUTSIDE OF THE UNITEDSTATES OR TO ENFORCE AGAINST THEM ANY JUDGMENTS OF US COURTS, INCLUDING JUDGMENTS PREDICATEDUPON CIVIL LIABILITIES UNDER THE SECURITIES LAWS OF THE UNITED STATES OR ANY STATE OR TERRITORYWITHIN THE UNITED STATES. THERE IS SUBSTANTIAL DOUBT AS TO THE ENFORCEABILITY IN THE UNITEDKINGDOM IN ORIGINAL ACTIONS, OR IN ACTIONS FOR ENFORCEMENT OF JUDGMENTS OF US COURTS, BASED ONTHE CIVIL LIABILITY PROVISIONS OF US FEDERAL SECURITIES LAWS. IN ADDITION, PUNITIVE DAMAGES INACTIONS BROUGHT IN THE UNITED STATES OR ELSEWHERE MAY BE UNENFORCEABLE IN ENGLAND ANDWALES.

FOR INVESTORS IN AUSTRALIA ONLY:

This prospectus is not a prospectus under Chapter 6D.2 of the Australian Corporations Act 2001 (Cth) (Corporations Act) and has not beenlodged with the Australian Securities & Investments Commission.

This prospectus is intended for distribution in Australia only to persons to whom it is lawful to offer the securities without a prospectus,because one or more of the exceptions set out in section 708 of the Corporations Act applies. No securities will be issued or sold incircumstances that would require the giving of a prospectus under Chapter 6D.2 of the Corporations Act. You should contact your adviser ifyou are uncertain as to whether a prospectus is required for the offer to you.

The Company is not licensed to provide financial product advice in Australia in relation to the securities. You are recommended to seek yourown advice from your lawyer, accountant or other professional adviser before investing. No cooling off period applies in relation to this offerunder the Corporations Act.

NOTICE TO EEA INVESTORS

In relation to each EEA State (except for the United Kingdom) which has implemented the Prospectus Directive (each a “relevant memberstate”), no New Ordinary Shares have been offered or will be offered pursuant to the Capital Raising to the public in that relevant memberstate prior to the publication of a prospectus in relation to the New Ordinary Shares which has been approved by the competent authority inthat relevant member state or, where appropriate, approved in another relevant member state and notified to the competent authority in therelevant member state, all in accordance with the Prospectus Directive, except that, with effect from and including the relevantimplementation date, offers of New Ordinary Shares may be made to the public in that relevant member state at any time:

(A) to any legal entity which is a qualified investor as defined in the Prospectus Directive;

ii

(B) to fewer than 100 or, if the relevant member state has implemented the relevant provision of the PD Amending Directive, 150natural or legal persons (other than qualified investors as defined in the Prospectus Directive) in such relevant member state; or

(C) in any other circumstances falling within Article 3(2) of the Prospectus Directive,

provided that no such offer of New Ordinary Shares shall result in a requirement for the publication by the Company, Citi, finnCap, Liberum,Macquarie or Rothschild of a prospectus pursuant to Article 3 of the Prospectus Directive or any measure implementing the ProspectusDirective in that relevant member state.

For this purpose, the expression “offer of any New Ordinary Shares to the public” in relation to any New Ordinary Shares in any relevantmember state means the communication in any form and by any means of sufficient information on the terms of the Capital Raising and anyNew Ordinary Shares to be offered so as to enable an investor to decide to subscribe for or acquire any New Ordinary Shares, as the samemay be varied in that relevant member state by any measure implementing the Prospectus Directive in that relevant member state.

NOTICE TO ALL INVESTORS

Any reproduction or distribution of this document, in whole or in part, and any disclosure of its contents or use of any information containedin this document for any purpose other than considering an investment in the New Ordinary Shares is prohibited. By accepting delivery of thisdocument, each offeree of the New Ordinary Shares agrees to the foregoing.

The contents of this document are not to be construed as legal, business or tax advice. Each prospective investor should consult his or its ownlegal adviser, financial adviser or tax adviser for legal, financial or tax advice.

Without limitation, the contents of Company’s website do not form part of this document.

Capitalised terms have the meanings ascribed to them in Part 14 of this document entitled “Definitions”.

The date of this document is 11 July 2017.

iii

CONTENTS

Page

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

PRESENTATION OF INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

EXPECTED TIMETABLE OF PRINCIPAL EVENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

DIRECTORS, COMPANY SECRETARY, REGISTERED OFFICE AND ADVISERS . . . . . . . . . . . . . . . . . 31

CAPITAL RAISING STATISTICS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

QUESTIONS AND ANSWERS ABOUT THE CAPITAL RAISING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

WHERE TO FIND HELP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

PART 1 LETTER FROM THE CHAIRMAN OF CITYFIBRE INFRASTRUCTURE HOLDINGSPLC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

PART 2 TERMS AND CONDITIONS OF THE OFFER FOR SUBSCRIPTION . . . . . . . . . . . . . . . . . . . . . 50

PART 3 INFORMATION ON CITYFIBRE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

PART 4 SELECTED FINANCIAL AND OTHER INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

PART 5 OPERATING AND FINANCIAL REVIEW OF CITYFIBRE . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

PART 6 INFORMATION ON ENTANET . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

PART 7 UNAUDITED PRO-FORMA FINANCIAL INFORMATION OF THE ENLARGED GROUP . . 106

PART 8 TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

PART 9 INFORMATION CONCERNING THE NEW ORDINARY SHARES . . . . . . . . . . . . . . . . . . . . . . 122

PART 10 ADDITIONAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

PART 11 HISTORICAL FINANCIAL INFORMATION OF THE GROUP . . . . . . . . . . . . . . . . . . . . . . . . . . 161

PART 12 HISTORICAL FINANCIAL INFORMATION ON ENTANET . . . . . . . . . . . . . . . . . . . . . . . . . . . 230

PART 13 HISTORICAL FINANCIAL INFORMATION ON ENTANET INTERNATIONAL . . . . . . . . . . 260

PART 14 DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 279

PART 15 GLOSSARY OF TECHNICAL TERMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 286

NOTICE OF GENERAL MEETING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 288

APPLICATION FORM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 290

NOTES ON HOW TO COMPLETE THE APPLICATION FORM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 294

SUMMARY

Summaries are made up of disclosure requirements known as “Elements”. These Elements are numbered inSections A-E (A.1-E.7).

This summary contains all the Elements required to be included in a summary for this type of (i) issuer and(ii) issue of securities. Because some Elements are not required to be addressed, there may be gaps in thenumbering sequence of the Elements.

Even though an Element might be required to be addressed in the summary because of the type of securitiesand issuer, it is possible that no relevant information can be given regarding the Element. In this case a shortdescription of the Element is included in the summary with the mention of the words “not applicable”.

Section A – Introductions and warnings

A.1 Warning

This summary should be read as an introduction to this document. Any decision to invest in theNew Ordinary Shares should be based on consideration of this document as a whole. Where a claimrelating to the information contained in this document is brought before a court, the claimantinvestor might, under the national legislation of the member states of the EEA, have to bear thecosts of translating this document before the legal proceedings are initiated. Civil liability attachesonly to those persons who have tabled the summary including any translation thereof, but only ifthe summary is misleading, inaccurate or inconsistent when read together with the other parts ofthis document or it does not provide, when read together with the other parts of this document, keyinformation in order to aid investors when considering whether to invest in such securities.

A.2 Resale or final placement of securities through financial intermediaries

Not applicable. No consent has been given by the Company or any person responsible for drawingup this prospectus to the use of this prospectus for subsequent resale or final placement of securitiesby financial intermediaries.

Section B – Issuer

B.1 Legal and commercial name

CityFibre Infrastructure Holdings plc (the “Company”).

B.2 Domicile/legal form/legislation under which the issuer operates/ country of incorporation

The Company is a public limited company, incorporated on 13 November 2013 in England andWales with its registered office situated in England and Wales. The Company operates under theCompanies Act 2006.

B.3 Current operations/Principal activities/Principal markets

CityFibre provides fibre connectivity services through designing, building, owning, and operatingfibre optic network infrastructure. The Group is a wholesale operator of fibre networks in townsand cities outside London. The Group provides open access, shared fibre infrastructure that enablesgigabit-capable connectivity for Channel Partners and mobile network operators, who in-turndeliver digital connectivity solutions to their end customers spanning the public sector, business,mobile operator and residential markets.

CityFibre operates across the UK, and currently has full fibre optic metropolitan area networks in42 towns and cities including: Aberdeen, Bristol, Coventry, Edinburgh, Glasgow, Manchester,Milton Keynes, Peterborough, and York. Furthermore, the Company owns and operates a longdistance fibre-optic network that interconnects 22 of its current towns and cities.

CityFibre is a provider of ‘full fibre’ infrastructure, meaning there is no copper or co-axial cableused for the provision of data connectivity services in CityFibre’s networks. This sets it apart fromother infrastructure competitors, notably Openreach and Virgin Media, who rely heavily on legacycopper and co-axial cables for connecting to premises on all but a small percentage of theirnetworks.

1

CityFibre’s network is constructed to provide high capacity fibre infrastructure that serves fourprimary market verticals:

Š Public sector – fibre connectivity to council buildings, schools, hospitals, CCTV;

Š Business – fibre connections to enterprises and SMEs (often referred to as Fibre to thePremises – FTTP);

Š Mobile operators – fibre connections to mobile base stations and small cells for 4G andfuture 5G mobile services (often referred to as Fibre to the Tower – FTTT); and

Š Consumers – fibre connections to homes (often referred to as Fibre to the Home – FTTH).

B.4a Current trends, trading and outlook

The Group continued its network footprint expansion throughout 2016, through a combination ofacquisitions, organic growth and incremental sales on existing and acquired assets.

In 2017, CityFibre continued to focus on growing revenues and connections across its existingfootprint, as well as undertaking selective investments in new towns and cities. Financialperformance relating to metro towns and cities was in line with management’s expectations. At theend of May 2017, the Group had entered into contracts with Channel Partners, enabling CityFibreto launch business services into seven further towns and cities, and securing in excess of £8.3million of new contracted revenue. Furthermore, the unrealised value of the Group’s contracts was£102.2 million, giving the Group good visibility of future income

The profile of CityFibre’s growth is characterised by securing a relatively small volume of largervalue contracts that provide fibre connectivity to multiple sites. This is supplemented by securingsmaller contracts at various times for individual fibre connections from existing Channel Partners.Therefore, timing of the larger contracts can affect month by month performance. The Groupsecured few large contracts in the first quarter of 2017, with a higher number of larger contractsexpected in the second quarter and throughout the second half of 2017. The strong and growingpipeline of opportunities means that the Group expects to deliver overall 2017 financialperformance in line with management expectations.

In January 2017, CityFibre announced its intention to construct a new fibre network in Stirlinghaving secured a seven-year anchor contract to provide full fibre connectivity to the public sector,followed in March 2017 with anchor contracts in the business market vertical to construct newnetworks in Cheltenham and Gloucester, two locations located near to the Company’s national longdistance network.

CityFibre will continue to seek opportunities to enter new towns and cities underpinned by suitableanchor contracts. The Directors believe that current trading activity and its pipeline of opportunitieswill enable the Group to progress towards its stated medium-term target to reach no less than 50towns and cities by 2020.

In its existing towns and cities, CityFibre is undertaking investments in active platforms to providewholesale Ethernet services to complement its current dark fibre offering. The Company is on trackto deliver its active platforms into not less than five further towns and cities in the first half of 2017,and is targeting to expand Ethernet services to a further six towns and cities by the end of the year.In expanding its Ethernet services to the business market vertical, CityFibre intends to enter intolaunch partner contracts with Channel Partners to provide fibre connectivity to more businesses inits existing footprint. In April 2017 CityFibre announced contracts to support construction inSlough, Maidenhead and Wakefield followed in June 2017 with contracts in Plymouth and Exeter.These launch partner contracts demonstrate that CityFibre is making further progress tocommercialise the network assets acquired from KCOM and Redcentric Solutions Limited in 2016.

In the public sector, the Directors believe that recent government policy for full fibre, together withplanned government stimulus to encourage local government to anchor new full fibre core metronetworks, will accelerate opportunities for fibre connectivity to more public sector sites. CityFibreis engaged in a significant number of discussions with local authorities and Channel Partners and isbuilding a pipeline of public sector opportunities with the potential for contracts to be awarded tothe Group in the second half of 2017 and beyond.

In 2016 CityFibre completed two landmark network deployments for the UK market: the FTTTnetwork construction in Hull and the FTTH trial in York. As a result, the Company is now

2

exploring opportunities to deploy FTTT and FTTH in more UK towns and cities, and is progressingcommercial negotiations with mobile operators and major Channel Partners accordingly. CityFibrehas engaged in commercial discussions with major ISPs and a number of smaller ISPs, to secureChannel Partner relationships intended to provide full fibre broadband services to consumers usingCityFibre’s future FTTH infrastructure. These discussions are advanced and may or may not lead tobinding agreements in due course. The Group has engagement with Channel Partners across all fourprimary market verticals, supported by market demands for fibre connectivity and policies thatencourage the deployment of full fibre and 5G infrastructure to many homes and businesses. TheDirectors believe that CityFibre is well positioned to exploit these opportunities and to continue toexpand its operations.

B.5 Group structure

The Company is the parent company of the Group.

The table below contains a list of the principal subsidiaries of the Company (each of which isconsidered by the Group to be likely to have a significant effect on the assessment of the assets,liabilities, the financial position and/or the profits and losses of the Group):

Name of subsidiary Country ofincorporation

Percentage owned Proportion of votingpower held

CityFibre HoldingsLimited

England and Wales 100% by the Company 100%

CityFibre NetworksLimited

England and Wales 100% by the Company 100%

FibreCity Holdings Ltd England and Wales 100% by the Company 100%

Gigler Limited England and Wales 100% by the Company 100%

CityFibre MetroNetworks Limited

England and Wales 100% by the Company 100%

FibreCityBournemouth Ltd

England and Wales 100% by the Company 100%

CityFibre Limited England and Wales 100% by the Company 100%

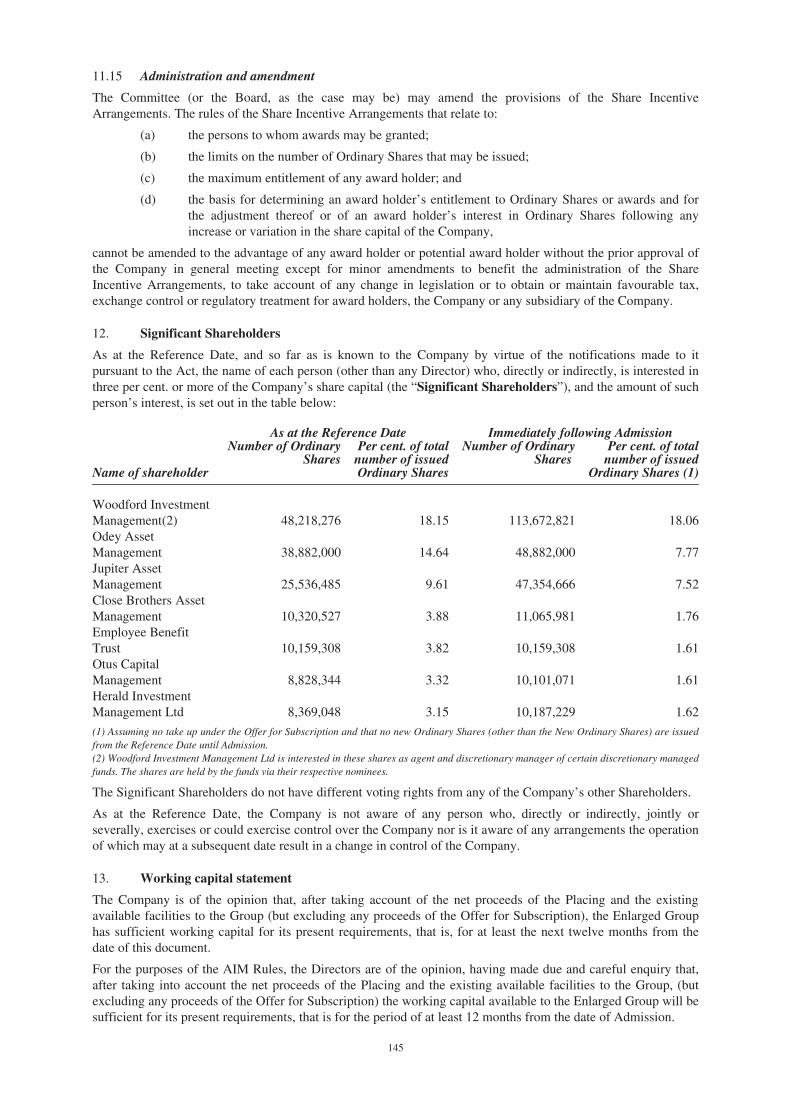

B.6 Notifiable interests

As at the Reference Date, the Company had been notified of, or was otherwise aware of, thefollowing persons who are directly or indirectly interested in 3 per cent. or more of the existingissued ordinary share capital of the Company:

As at the Reference Date Immediately following Admission

Name of shareholder Number of OrdinaryShares

% of total numberof issued Ordinary

Shares

Number ofOrdinary

Shares

% of total number ofissued Ordinary

Shares(1)

Woodford InvestmentManagement(2)

48,218,276 18.15 113,672,821 18.06%

Odey AssetManagement

38,882,000 14.64 48,882,000 7.77%

Jupiter AssetManagement

25,536,485 9.61 47,354,666 7.52%

Close Brothers AssetManagement

10,320,527 3.88 11,065,981 1.76%

Employee BenefitTrust

10,159,308 3.82 10,159,308 1.61%

Otus CapitalManagement

8,828,344 3.32 10,101,071 1.61%

Herald InvestmentManagement Ltd

8,369,048 3.15 10,187,229 1.62%

(1) Assuming no take up under the Offer for Subscription and that no new Ordinary Shares (other than the New OrdinaryShares) are issued from the Reference Date until Admission.

(2) Woodford Investment Management Ltd is interested in these shares as agent and discretionary manager of certaindiscretionary managed funds. The shares are held by the funds via their respective nominees.

3

As at the Reference Date, the Company is not aware of any person who, directly or indirectly,jointly or severally, exercises or could exercise control over the Company nor is it aware of anyarrangements the operation of which may at a subsequent date result in a change in control of theCompany.

As at the Reference Date, the Company had been notified of, or was otherwise aware of, itsDirectors, being persons discharging managerial responsibilities within the Company, beinginterested, directly or indirectly, in its issued ordinary share capital of the Company as follows:

As at the Reference Date Immediately following AdmissionName of Director Number of

Ordinary Shares% of total number of

issued OrdinaryShares

Number ofOrdinary

Shares

% of total number ofissued Ordinary

Shares (1)

Greg Mesch (2) 572,803 0.2 572,803 0.09%

Mark Collins (2) 162,987 0.06 162,987 0.03%

Terry Hart (2) 43,007 0 43,007 0.01%

Leo van Doorne (2)(via Kimardo II B.V.) 3,727,767 1.4 3,727,767 0.59%

Gary Mesch (2)(4) 1,166,831 0.4 1,166,831 0.19%

Sally Davis (2) 14,910 0 14,910 0.00%

Steve Charlton (2) – – – 0.00%

Chris Stone (3) – – 1,181,818 0.19%

(1) Assuming no take up under the Offer for Subscription and that no new Ordinary Shares (other than the New Ordinary Shares) are issuedfrom the Reference Date until Admission.

(2) Excludes interests in Ordinary Shares pursuant to Share Incentive Arrangements and a warrant instrument dated 13 January 2014.

(3) Chris Stone has agreed to subscribe for 1,181,818 Placing Shares at the Offer Price. Chris Stone will not be applying for any Offer forSubscription Shares. The number of Shares do not include the Shares to be awarded to Chris Stone under the Non-Employee LTIP.

(4) 1,080,151 of the Ordinary Shares are held by TJL Investment Corporation, a company which Gary Mesch and persons connected with himhave an interest in and 59,590 of the Ordinary Shares are held by persons connected with Gary Mesch.

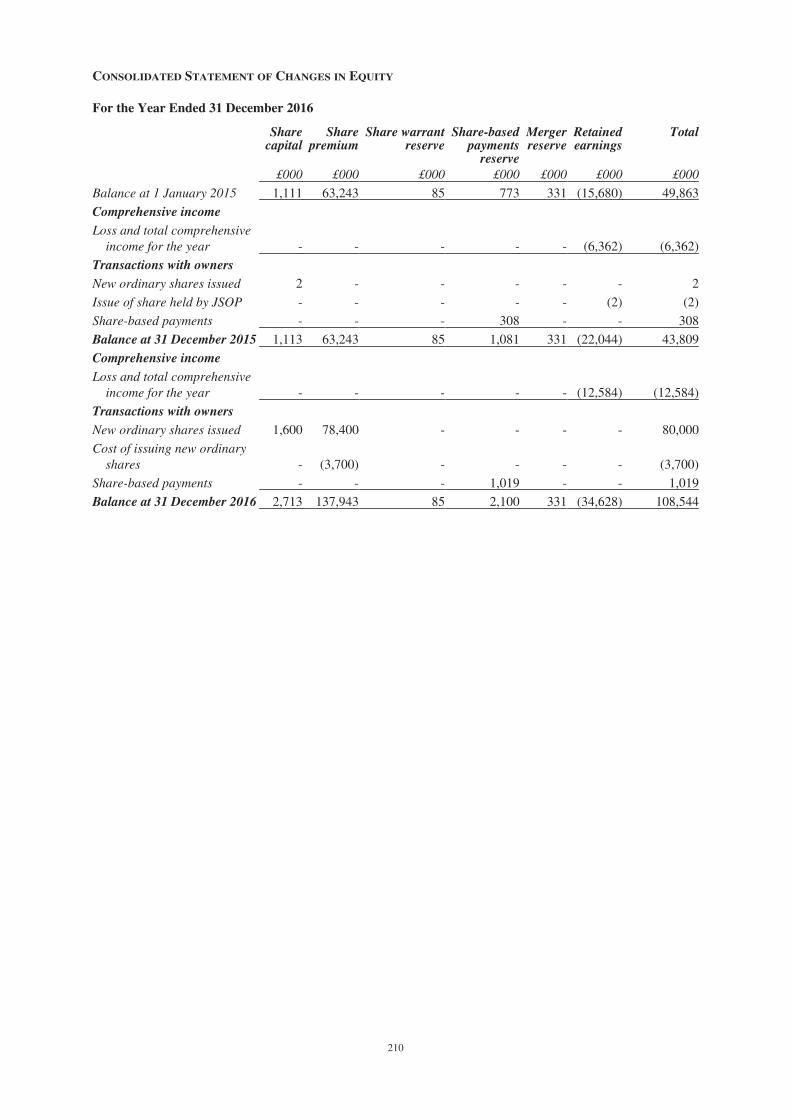

B.7 Selected historical key financial information

Selected key historical financial information of the Group

The selected historical financial information relating to the Group set out below has been extractedwithout material adjustment from the audited reports and accounts of the Group prepared underIFRS for the financial years ended 31 December 2014, 31 December 2015 and 31 December 2016:

Consolidated income statement

Year ended 31 December2014 2015 2016£000 £000 £000

Revenue 3,844 6,408 15,363

Cost of sales (568) (888) (1,827)

Gross profit (loss) 3,276 5,520 13,536

Administrative expenses (10,726) (11,679) (18,677)

Operating (loss) (7,450) (6,159) (5,141)

Finance income 779 170 45

Finance charges (344) (278) (7,341)

Share of results from associates and joint ventures (42) (126) (147)

(Loss) before taxation (7,057) (6,393) (12,584)

Taxation 31 31 -

(Loss) for the year (7,026) (6,362) (12,584)

Loss per share £(0.09) £(0.06) £(0.05)

4

Consolidated balance sheetAs at 31 December

2014 2015 2016£000 £000 £000

Assets

Non-current assets 33,160 45,501 156,803

Current assets 36,989 15,915 28,778

Total assets 70,149 61,416 185,581

Liabilities

Non-current liabilities (12,343) (10,194) (66,821)

Current liabilities (7,943) (7,413) (10,216)

Total liabilities (20,286) (17,607) (77,307)

Net assets 49,863 43,809 108,544

Share capital 1,111 1,113 2,713

Share premium 63,243 63,243 137,943

Share warrant reserve 85 85 85

Share based payments reserve 773 1,081 2,100

Merger reserve 331 331 331

Retained earnings (15,680) (22,044) (34,628)

Total equity 49,863 43,809 108,544

Consolidated statement of cash flowsYear ended 31 December

2014 2015 2016£000 £000 £000

Net cash utilised in operating activities (3,552) (5,360) (2,367)

Net cash (utilised in)/from investing activities (34,336) 13,782 (115,027)

Net cash from/(utilised in) from financing activities 41,788 (2,877) 124,385

Net increase in cash and cash equivalents 3,900 5,545 6,991

Cash and cash equivalents at the beginning of the year 286 4,186 9,731

Cash and cash equivalents at the end of the year 4,186 9,731 16,722

The following significant changes in the Group’s financial condition and operating results occurredin the years ended 31 December 2014, 2015 and 2016.

Revenue increased by £2.6 million (66.7 per cent.) from £3.8 million in the year ended 31December 2014 to £6.4 million in the year ended 31 December 2015. This increase was driven byorganic growth (that is, the continued expansion in CityFibre’s footprint along with the delivery ofincremental revenues from both existing and new towns and cities). Revenues from the businessmarket vertical improved by £1 million. The Group has been growing business revenues on newnetworks since the second half of 2014 when it started commercialising constructed and acquirednetworks of scale in addition to its York network. Significant growth and geographicaldiversification of revenues occurred in 2015. Gross profit increased by £2.2 million (68.5 per cent.)from £3.3 million in the year ended 31 December 2014 to £5.5 million in the year ended 31December 2015. Gross margin increased by 0.9 percentage points from 85.2 per cent. in the yearended 31 December 2014 to 86.1 per cent. in the year ended 31 December 2015, reflecting theslightly higher profitability of new business added during the period.

5

Revenue increased by £9 million (139.7 per cent.) from £6.4 million in the year ended31 December 2015 to £15.4 million in the year ended 31 December 2016. This increase was drivenby organic growth, and contributions from the KCOM and Redcentric Solutions Limited leasebackagreements, following completion of the asset acquisitions from KCOM and Redcentric SolutionsLimited in 2016. Gross profit increased by £8 million (145.2 per cent.) from £5.5 million in theyear ended 31 December 2015 to £13.5 million in the year ended 31 December 2016. Gross marginincreased by two percentage points, from 86.1 per cent. in the year ended 31 December 2015 to88.1 per cent. in the year ended 31 December 2016, reflecting the continuing addition of moreprofitable incremental new business on the assets during the period. The KCOM commitment had adirect gross margin of 83 per cent.

There has been no significant change in the Group’s financial or trading position since31 December 2016, the date of the last annual report and audited consolidated accounts of theGroup.

Selected key historical financial information of Entanet

The selected historical financial information relating to Entanet for the eleven month period ended31 December 2014 and the financial years ended 31 December 2015 and 31 December 2016 as setout in the following tables has been extracted without material adjustment from the auditedfinancial information in Part 12 of this document:

Consolidated income statement

Period ended31 December Year ended 31 December

2014 2015 2016£000 £000 £000

Turnover 25,753 31,887 35,754

Cost of sales (19,650) (24,075) (28,637)

Gross profit 6,103 7,812 7,117

Administrative expenses (5,298) (4,405) (6,403)

Operating profit 805 3,407 714

Finance income 15 13 15

Finance charges (1,987) (1,087) (1,136)

(Loss)/profit before taxation (1,167) 2,333 (407)

Taxation 27 298 144

(Loss)/profit for the period/year (1,140) 2,631 (263)

6

Consolidated balance sheet

As at 31 December

2014 2015 2016£000 £000 £000

AssetsNon-current assets 9,579 9,068 9,221

Current assets 5,065 10,219 8,057

Total assets 14,644 19,287 17,278

LiabilitiesNon-current liabilities (10,075) (11,545) (10,319)

Current liabilities (4,149) (4,991) (4,471)

Total liabilities (14,224) (16,536) (14,790)

Net assets 420 2,751 2,488

Equity

Share capital 25 25 25

Share premium 625 625 625

Merger reserve 300 - -

Retained earnings (530) 2,101 1,838

Total equity 420 2,751 2,488

Consolidated statement of cash flowsPeriod ended31 December Year ended 31 December

2014 2015 2016£000 £000 £000

Net cash inflow from operating activities 1,136 2,838 1,705

Net cash inflow (outflow) from investing activities 919 (561) (765)

Net cash (outflow) from financing activities (416) (1,342) (1,345)

Net increase (decrease) in cash and cash equivalents 1,639 935 (405)

Cash and cash equivalents at the beginning of the period/year 5 1,644 2,579

Cash and cash equivalents at the end of the year 1,644 2,579 2,174

The following significant changes in Entanet’s financial condition and operating results occurred inthe eleven month period ended 31 December 2014, and the years ended 31 December 2015 and2016.

Turnover grew from £25.8 million in the period ended 31 December 2014 to £31.9 million in theyear ended 31 December 2015. The majority of growth was driven by increasing demand forEthernet circuits, either as standalone connectivity or as the backbone of wider network solutions.Gross profit, which excludes core network costs grew from £6.1 million in the period ended 31December 2014 to £7.8 million in the year ended 31 December 2015, representing a 24.5 per cent.gross margin. Although this was an improvement on the prior year there was an increase in marginpressure during 2015 arising from aggressive pricing by competitors, continued price deflationparticularly in smaller capacity circuits and the increasing ease with which customers can obtainonline quotes for circuits from competing wholesalers.

During 2015, an exceptional item of £1.9 million income was recognised within administrativeexpenses, being the settlement of certain claims against a former shareholder and certain partiesconnected to that shareholder. Underlying EBITDA excluding exceptional items increased to£3.1 million in the year ended 31 December 2015 at a similar margin to the prior period.

7

Turnover grew from £31.9 million in the year ended 31 December 2015 to £35.8 million in the yearended 31 December 2016. The growth was largely driven by demand for Ethernet circuits, both instandalone connectivity and in IP based network solutions. There was also significant growth inEntanet’s broadband base as a result of strong demand from a large consumer-focussed ChannelPartner. Gross profit reduced from £7.8 million in the year ended 31 December 2015 to £7.1million in the year ended 31 December 2016, representing a 19.9 per cent. gross margin. The fall ingross margin, from 24.5 per cent. in the year ended 31 December 2015, was driven predominantlyby the direct acquisition cost of the growth in the consumer broadband base. The reduction in grossmargin and increased investment in operational and developmental resources led to a reduction inunderlying EBITDA excluding exceptional items from £3.1 million in the year ended 31 December2015 to £2 million in the year ended 31 December 2016.

There has been no significant change in Entanet’s financial or trading position since 31 December2016, the date of the last annual report and audited accounts of Entanet.

The selected historical financial information relating to Entanet International for the seven weeksended 20 February 2014 as set out in the following tables has been extracted without materialadjustment from the audited financial information in Part 13 of this document:

Income statementFor the period ended

20 February 2014For the period ended

31 December 2014£000 £000

Revenue 4,072 25,753Cost of sales (2,985) (19,650)

Gross profit 1,087 6,103Administrative expenses (479) (3,876)Depreciation (65) (460)

Operating profit 543 1,767

Finance income - 19Finance expense - (5)

Profit before taxation 543 1,781Taxation (125) 30

Profit for the period 418 1,811Other comprehensive income - -

Total comprehensive profit for the period 418 1,811

Balance SheetAs at 20 February

2014As at 31 December

2014£000 £000

AssetsNon-current assets 1,318 1,853Current assets 6,196 6,713

Total assets 7,514 8,566

LiabilitiesNon-current liabilities - (202)Current liabilities (5,079) (4,118)

Total liabilities (5,079) (4,320)

Net assets 2,435 4,246

EquityIssued share capital 200 200Retained profits 2,235 4,046

2,435 4,246

8

Statement of cash flows

Net cash inflow/(outflow) from operating activities 2,028 (325)

Net cash outflow from investing activities (44) (608)

Net cash outflow from financing activities (343) (154)

Net increase/(decrease) in cash and cash equivalents 1,641 (1,087)

Cash and cash equivalents beginning of period 1,046 2,687

Cash and cash equivalents at end of period 2,687 1,600

B.8 Selected key pro forma financial information

The following unaudited pro forma statement of net assets and pro forma income statement (the“Pro Forma Financial Information”) have been prepared to show the effect on the consolidatednet assets of the Group had the Entanet Acquisition occurred on 31 December 2016 and the effecton the income statement of the Group had the Entanet Acquisition occurred on 1 January 2016.

The Pro Forma Financial Information has been prepared for illustrative purposes only and in accordancewith Annex II of the Prospectus Directive Regulation, and should be read in conjunction with the notesset out below. Due to its nature, the Pro Forma Financial Information addresses a hypothetical situationand, therefore, does not represent the Group’s actual financial position or results.

Pro forma income statement

AdjustmentsThe GroupYear ended

31 December2016 (1)

EntanetYear ended

31 December2016 (2)

Otheradjustments

(3)

Pro formaearnings of

the EnlargedGroup

£000 £000 £000 £000

Revenue 15,363 35,754 - 51,117

Cost of sales (1,827) (28,637) - (30,464)

Gross profit 13,536 7,117 - 20,653

Total administrative expenses (18,677) (6,403) (4,987) (30,067)

Operating (loss) profit (5,141) 714 (4,987) (9,414)

Finance income 45 15 - 60

Finance cost (7,341) (1,136) - (8,477)

Share of post-tax losses of equityaccounted Joint Venture

(147) - - (147)

Loss before taxation (12,584) (407) (4,987) (17,978)

Income tax - 144 - 144

Loss for the year and totalcomprehensive income (12,584) (263) (4,987) (17,834)

Notes:

1. The results of the Group for the year ended 31 December 2016 have been extracted without materialadjustment from the financial statements of the Group for the year ended 31 December 2016 set out inPart 11 of this document.

2. The results of Entanet have been extracted without material adjustment from the financial information onEntanet for the year ended 31 December 2016, set out in Part 12 of this document.

3. This adjustment comprises the estimated costs of the Entanet Acquisition and the estimated costs of thePlacing that cannot be set off against the share premium account.

4. No account has been taken of the effects of any synergies and of the costs for measures taken to achievethose synergies that may have arisen had the acquisition occurred on 1 January 2016 and that maysubsequently have affected the results of the Group in the year ended 31 December 2016.

5. No account has been taken of the trading performance of either the Group or Entanet since 31 December2016 nor of any other event save as disclosed above.

6. Save for the costs of the Entanet Acquisition and the Placing, the pro forma income statement adjustments areexpected to have a continuing effect on the Enlarged Group.

9

Pro forma statement of net assetsAdjustments

The GroupAs at

31 December2016 (1)

EntanetAs at

31 December2016 (2)

EntanetAcquisition

(3)

NetPlacing

proceeds(4)

Pro formanet assets of

the EnlargedGroup

£000 £000 £000 £000 £000

Assets

Non-current assetsProperty, plant and equipment 155,159 2,684 - - 157,843Intangible assets 1,211 6,537 15,859 - 23,607Investment in Joint Venture 433 - - - 433

156,803 9,221 15,859 - 181,883

Current assetsInventory 3,986 - - - 3,986Trade and other receivables 8,070 5,883 - - 13,953Cash and cash equivalents 16,722 2,174 (29,000) 191,013 180,909

Total current assets 28,778 8,057 (29,000) 191,013 198,848

Total assets 185,581 17,278 (13,141) 191,013 380,731

Liabilities

Non-current liabilitiesInterest bearing loans and borrowings (55,280) (10,186) 10,186 - (55,280)Deferred revenue (11,091) - - - (11,091)Deferred consideration (450) - - - (450)Deferred tax - (133) - - (133)

Total non-current liabilities (66,821) (10,319) 10,186 - (66,954)

Current liabilitiesInterest bearing loans and borrowings - (467) 467 - -Deferred revenue (2,864) - - - (2,864)Trade and other payables (7,352) (4,004) - - (11,356)

Total current liabilities (10,216) (4,471) 467 - (14,220)

Total liabilities (77,037) (14,790) 10,653 - (81,174)

Net assets 108,544 2,488 (2,488) 191,013 299,557

Notes:

1. The net assets of the Group at 31 December 2016 have been extracted without material adjustment fromthe financial statements of the Group for the year ended 31 December 2016 set out in Part 11 of thisdocument.

Adjustments

2. The net assets of Entanet have been extracted without material adjustment from the financialinformation on Entanet for the year ended 31 December 2016, set out in Part 12 of this document.

3. An adjustment has been made to reflect the estimated intangible assets arising on the EntanetAcquisition.

For the purposes of this pro forma information, no adjustment has been made to the separate assets andliabilities of Entanet to reflect their fair value. The difference between the net assets of Entanet as statedat their book value at 31 December 2016 and the estimated consideration has therefore been presentedas a single value in “Intangible assets”. The net assets of Entanet will be subject to a fair valuerestatement as at the effective date of the transaction. Actual intangible assets included in the Group’snext published financial statements may therefore be materially different from those included in the proforma statement of net assets.

The estimated consideration for Entanet is £29 million (on a debt free and cash free basis and subject toadjustments), of which a proportion will be used to repay Entanet’s indebtedness. It has been assumedthat all of the deferred consideration will be payable in cash.

10

£000

Consideration payable in cash 29,000

Repayment of debt (10,653)

Consideration for Entanet’s equity 18,347

Book value of net assets of Entanet as at 31 December 2016 (2,488)

Estimated intangible assets arising on the transaction 15,859

The repayment of debt is based on the balance outstanding at 31 December 2016. The actual balancerepaid is likely to differ from this amount.

4. The Placing will raise net proceeds of £191 million (£200 million gross proceeds less estimatedexpenses of £9 million). No account has been taken of any proceeds from the Offer for Subscription.

5. No account has been taken of the financial performance of the Group or Entanet since 31 December2016 nor of any other event save as disclosed above.

B.9 Profit forecast and Estimate

Not applicable; the Company has not made a profit forecast or estimate.

B.10 Qualification in the audit reports

Not applicable; the audit reports on the historical financial information contained in this documentare not qualified.

B.11 Working capital qualification

Not applicable; the Company is of the opinion that, after taking account of the net proceeds of thePlacing and the existing available facilities to the Group (but excluding any proceeds of the Offerfor Subscription), the Enlarged Group has sufficient working capital for its present requirements,that is for at least the next 12 months from the date of this document.

Section C – Securities

C.1 Type and class of the securities

The Capital Raising comprises an offering of ordinary shares of £0.01 in the Company.

C.2 Currency of the securities issue

The Existing Ordinary Shares are priced in Sterling, and the New Ordinary Shares will be quotedand traded in Sterling.

C.3 Shares issued/Value per share

As at the Reference Date, the Company had in issue 265,672,644 fully paid Ordinary Shares of£0.01 each.

As at the Reference Date, the Company had in issue 5,653,865 Deferred Shares of £0.01 each.

C.4 Description of the rights attaching to the securities

The New Ordinary Shares will be issued as fully paid and will rank pari passu in all respects withthe Existing Ordinary Shares, including for voting purposes and the right to receive dividends orother distributions declared, made or paid after Admission.

C.5 Restrictions on free transferability of the securities

The Ordinary Shares are freely transferable and there are no restrictions on transfer in the UK.

C.6 Admission/Regulated markets where the securities are traded

The Ordinary Shares have been admitted to trading on AIM. Application will be made to theLondon Stock Exchange for the New Ordinary Shares to be admitted to trading on AIM. Noapplication has been made or is currently intended to be made for the Ordinary Shares to beadmitted to listing or trading on any regulated market or any other exchange.

11

C.7 Dividend policy

The objective of the Directors is to achieve capital growth for Shareholders through the continuedexpansion of its fibre infrastructure. Consequently, they do not anticipate that the Company willpay dividends to Shareholders in the short to medium term. The Directors will keep this positionunder review and would intend, at an appropriate stage in the future, to pay a proportion of profitsin each year to Shareholders by way of dividend.

Section D – Risks

D.1 Summary information on the key risks that are specific to the Company or its industry

The Group’s infrastructure is used by Channel Partners and, therefore, revenues depend on ChannelPartner relationships. However, many Channel Partners have existing relationships with othernetwork providers such as Openreach. If the Group is unable to secure satisfactory relationshipswith Channel Partners, on terms favourable to the Group, it may be unable to implement itsbusiness plan in full.

The Group’s business requires the maintenance, upgrade and periodic replacement of facilities andnetworks to continue to function as expected. If there is damage to the network, the Group will berequired to incur expenses to repair the network, which depending on the issue, could besubstantial. Furthermore, as the Group’s network elements become obsolete or reach their designlife capacity, the Group’s operating and capital expenses could significantly increase depending onthe nature and extent of repairs or replacements.

Advances in the process of delivering ultrafast communications could allow the Group’scompetitors to produce products and communications infrastructure faster and more efficiently, andat a substantially lower cost than the Group. If the Group is unable to adapt or incorporatetechnological advances into its operations, its offering could become less competitive.

The deployment of the Group’s networks requires large-scale civil engineering to construct ductand fibre either below the ground or overhead via poles. The Group depends on skilled third partycontractors for the construction and maintenance of its infrastructure. The Group’s operations maybe adversely affected should there be a lack of available contract resources, higher than expectedlabour costs, under performance or insolvency of a contractor.

The Group believes that its future revenue growth depends on the its ability to provide customers withquality service that meets and then exceeds customer service expectations. Interruptions in service orperformance problems, for whatever reason, could undermine confidence in its services, damage itsreputation and consequently limit its ability to retain existing customers or attract new customers.

The communications market is regulated by Ofcom and the Communications Act 2003. Theregulatory framework may change (including as a result of the UK’s decision to leave the EuropeanUnion) in a way that may be prejudicial to the Group’s operations.

Ofcom exercises a degree of control over Openreach by imposing access conditions and chargecontrols that affect Openreach products and pricing. There is a possibility that wholesale pricingwill change and/or access conditions be amended. If these changes result in excessive orunpredicted price reductions being imposed on Openreach wholesale products, this couldnegatively affect the Company’s pricing of competitive fibre.

Ofcom is seeking to make Openreach more independent and this has led to BT agreeing to separateOpenreach into a new company within the BT group. Any adverse change or significant delays toOfcom’s proposals may adversely affect the Company’s ability to implement its business plan in full.

The market in which the Group operates is dominated by one major entity, BT, which has muchgreater capital resources than the Group. Together with Virgin Media, these competitors, amongstothers, will have significantly greater financial, technical, marketing and servicing resources thanthe Group and have longer operating histories or greater name recognition, with a more extensivenetwork and significantly larger customer bases. The Group’s relatively smaller size may thereforebe considered negatively by prospective customers. In addition, the Group’s competitors may beable to respond more quickly to changes in customer requirements and devote greater resources tothe enhancement, promotion or sale of their products.

12

The Group is currently reliant on a limited number of key customers. If the Group loses one or moreof its key customers, or if one or more of its key customers significantly decreases use of the Group’sservices, the Group’s business would be materially and adversely affected. The Group’s futureoperating results will depend on the success of these customers and its other large customers, and itssuccess in selling services to them. If it were to lose a significant portion of the revenue from any ofits top customers, the Group would not be able to replace that revenue in the short term.

The Company will in the longer term require further capital through debt or equity financing orfrom other sources. The Group may be unable to obtain additional financing on acceptable terms orat all if market and economic conditions, the financial condition or operating performance of theGroup or investor sentiment are unfavourable. The Group’s inability to raise additional fundingmay hinder its ability to grow in the longer term.

D.3 Key information on the key risks that are specific to the securities

The market price of the Ordinary Shares could be subject to significant fluctuations due to a changein sentiment in the market regarding the Ordinary Shares. The fluctuations could result fromnational and global economic and financial conditions, factors the Group does not control includingthe market’s response to the Capital Raising, and regulatory changes. Any of these events couldresult in a decline in the market price of the Ordinary Shares.

There is no assurance that the public trading market price of the Ordinary Shares will not declinebelow the Offer Price. Should that occur, Shareholders who have acquired New Ordinary Shares inthe Capital Raising and then sell their Ordinary Shares will suffer an immediate unrealised loss as aresult. Moreover, there can be no assurance that, following Shareholders’ acquisition of NewOrdinary Shares, Shareholders will be able to sell their New Ordinary Shares at a price equal to orgreater than the acquisition price for those shares.

Shareholders will experience dilution in their ownership and voting interests pursuant to the Placingwhether or not Shareholders participate in the Offer for Subscription. Shareholders who do not (orcannot) participate in the Placing will be diluted by 57.8 per cent. (excluding the impact of theOffer for Subscription) or 59.5 per cent. (assuming full take up under the Offer for Subscription).The percentage of the Company’s issued share capital that the Existing Ordinary Shares representwill be reduced by 57.8 per cent. to 42.2 per cent. as a result of the Capital Raising (excluding theimpact of the Offer for Subscription) or by 59.5 per cent. to 40.5 per cent. (assuming full take upunder the Offer for Subscription).

Section E – Offer

E.1 Total net proceeds and costs of the issue

CityFibre expects to raise net proceeds of £191 million by way of the Placing (after deduction ofestimated expenses, including underwriting commissions but excluding VAT, of approximately£9 million) and net proceeds up to £14.8 million by way of the Offer for Subscription (afterdeduction of estimated expenses of approximately £0.2 million assuming the Offer for Subscriptionis taken up in full).

E.2a Reasons for the offer/use of the proceeds

Of the net proceeds, £29 million (on a cash free debt free basis and subject to adjustments) will beused to acquire Entanet, substantially increasing the Company’s wholesale capabilities and itsrelationships with its Channel Partners, especially in the business and consumer market verticals,thereby extending CityFibre’s channels to market. CityFibre intends to apply the balance of the netproceeds to fund the growth of the Group’s full fibre network across UK towns and cities, servingthe four primary market verticals of public sector, mobile, business and consumer.

E.3 Terms and conditions of the offer

The offer in respect of the Capital Raising comprises:

i. an offer of 363,636,364 Placing Shares at the Offer Price to Placees pursuant to thePlacing; and

ii. an offer of up to 27,272,727 Offer for Subscription Shares at the Offer Price pursuant tothe Offer for Subscription.

13

The Placing is fully underwritten by the Underwriters on the terms and conditions of the UnderwritingAgreement and is conditional upon (among other things) (i) the Resolutions being passed at theGeneral Meeting, (ii) the Underwriting Agreement having become unconditional in all respects (savefor the condition relating to Admission) and (iii) Admission becoming effective by not later than8.00 a.m. on 28 July 2017 (or such later date as the Company and the Underwriters may agree).

The Underwriting Agreement may be terminated by the Underwriters prior to Admission upon theoccurrence of certain specified events, in which case neither the Placing nor the Offer forSubscription will proceed.

The Placing

The Company is offering 363,636,364 Placing Shares (representing 136.9 per cent. of the Company’sexisting issued share capital and 55.4 per cent. of the Company’s enlarged issued share capitalimmediately following completion of the Capital Raising, assuming that the Offer for Subscription istaken up in full) as part of the Placing to certain Shareholders and prospective institutional investors.

The Placing is to be made at the Offer Price. The Offer Price represents a 9.09 per cent. discount to theclosing price of 60.50 pence per Ordinary Share on 4 July 2017 (being the last Business Day beforeannouncement of the Capital Raising). The Offer Price in respect of Placing Shares is payable in fullupon Admission, which is expected to become effective at 8.00 a.m. on 28 July 2017.

The Placing will raise gross proceeds of £200 million.

The Placing is fully underwritten by the Underwriters on the terms and conditions of theUnderwriting Agreement. The Placing Shares will be placed with certain Shareholders andprospective institutional investors in transactions exempt from, or not subject to, the registrationrequirements of the US Securities Act.

The Placing Shares will rank pari passu in all respects with each other and all Existing OrdinaryShares, and the Offer for Subscription Shares, as well as for voting purposes and the right to receivedividends or other distributions declared, made or paid after Admission.

The Offer for Subscription

Up to 27,272,727 Offer for Subscription Shares are being made available under the Offer forSubscription at the Offer Price (representing 10.3 per cent. of the Company’s existing issued sharecapital and 4.2 per cent. of the Company’s enlarged issued share capital immediately followingcompletion of the Capital Raising, assuming in both cases that the Offer for Subscription is takenup in full). Applications under the Offer for Subscription must be for a minimum of 2,000 Offer forSubscription Shares (the “Minimum Subscription”) and thereafter in multiples of 2,000 Offer forSubscription Shares. Any application for less than the Minimum Subscription or which is not for amultiple of 2,000 Offer for Subscription Shares will be rejected.

The Offer for Subscription will raise gross proceeds of up to £15 million.

The Placing has been fully underwritten by the Underwriters. The Offer for Subscription is notbeing underwritten by the Underwriters or anyone else.

Application will be made for the Offer for Subscription Shares to be admitted to trading on AIM. Itis expected that Admission will become effective on 28 July 2017 and that dealings for normalsettlement in the Offer for Subscription Shares will commence at 8.00 a.m. on 28 July 2017.

The Offer for Subscription Shares will rank pari passu in all respects with each other and allExisting Ordinary Shares, and the Placing Shares, as well as for voting purposes and the right toreceive dividends or other distributions, made or paid after Admission.

E.4 Interests that are material to the issue/Conflicting interests

Not applicable; there is no interest that is material to the Capital Raising.

E.5 Selling Shareholders and lock-up arrangements

Not applicable; there are no selling Shareholders nor lock-up arrangements in relation to the CapitalRaising.

14

E.6 Dilution

Following completion of the Capital Raising, Shareholders who do not (or cannot) participate in thePlacing will suffer a dilution of approximately 57.8 per cent. pursuant to the Placing (excluding theimpact of the Offer for Subscription) or 59.5 per cent. (assuming full take up under the Offer forSubscription).

E.7 Estimated expenses charged to the investor

Not applicable; the Company will not directly charge any expenses to the investors.

15

RISK FACTORS

Any investment in the New Ordinary Shares is subject to a number of risks and uncertainties. Prior to investingin the New Ordinary Shares, prospective investors should carefully consider the factors, risks and uncertaintiesassociated with any such investment, the Group’s business, strategy and the industry in which it operates,together with all other information contained in this document including, in particular, the risk factors describedbelow. Prospective investors should note that the risks and uncertainties identified in the Summary are the risksand uncertainties that the Directors believe to be the most relevant to an assessment by a prospective investor ofwhether to consider an investment in the New Ordinary Shares. However, as the risks and uncertainties whichthe Group faces relate to events and depend on circumstances that may or may not occur in the future,prospective investors should consider not only the information on the key risks summarised in the Summary butalso, among other things, the risks and uncertainties described below.

The following is not an exhaustive list or explanation of all risks that prospective investors may face whenmaking an investment in the New Ordinary Shares and should be used as guidance only. The order in which risksare presented is not necessarily an indication of the likelihood of the risks actually materialising, of the potentialsignificance of the risks or of the scope of any potential harm to the Group’s business, operating results,financial condition, prospects or future operations. Additional risks and uncertainties relating to the Group thatare not currently known to the Group, or that the Group currently deems immaterial, may individually orcumulatively also have a material adverse effect on the Group’s business, operating results, financial condition,prospects or future operations. If any of the risks referred to below, or any new risks, should materialise, theprice of the New Ordinary Shares may decline and investors could lose all or part of their investment. Investorsshould carefully consider whether an investment in the New Ordinary Shares is suitable for them in the light ofthe information in this document and their personal circumstances.

Part A: Risks Relating to the Company

The Group’s business is dependent on establishing and maintaining relationships with Channel Partners whocan use its fibre infrastructure

The Group’s infrastructure is used by Channel Partners and, therefore, revenues depend on Channel Partnersrelationships. However, many Channel Partners have existing relationships with other network providers such asOpenreach. Although the Directors believe the Group’s fibre infrastructure and wholesale product portfolio isattractive to Channel Partners, if the Group is unable to secure satisfactory relationships with Channel Partners,on terms favourable to the Group, it may be unable to implement its business plan in full.

Moreover, Channel Partners may in the future decide to provide their own infrastructure rather than relying, forexample, on that of the Group, which would adversely affect the Group’s operations. Any failure by the Group toestablish and maintain relationships with relevant Channel Partners may have a material adverse effect on theGroup’s business, operating results, financial condition, prospects or future operations.

The growth of the Group’s business is partly reliant on procuring contracts with public sector bodies

The Group intends to enter into contracts with public sector ICT providers, local councils and other publicbodies, amongst other types of customer. Public sector contracts may be subject to formal procurementprocesses, which are competitive and may cause delays to the implementation of the Group’s business plan.Furthermore, the local council or public body may operate with only a pre-qualified framework of suppliers,which may exclude the Group.

Any delay or failure to win public sector contracts may have a material adverse effect on the Group’s business,operating results, financial condition, prospects or future operations.

Additionally, future budgetary cuts could reduce public sector appetite for fibre contracts, thereby having anegative impact on the Group’s results.

Contracts awarded pursuant to public procurement may be open to challenge or termination

Contracts awarded pursuant to public procurement may, in some circumstances, be open to challenge by thirdparties claiming a breach of procurement rules or that payments made under the contract constitute state aid inviolation of applicable laws and regulations. In the event that a public sector contract awarded to the Group, or toa private sector Channel Partner to the Group, is challenged, the Group may suffer delays in implementing theproject or the contract may be terminated if the challenge is successful.

Loss of one or more contracts awarded by public procurement or otherwise may have a material adverse effect onthe Group’s business, operating results, financial condition, prospects or future operations.

16

The Group’s business is dependent upon the on-going maintenance, upgrading, and replacement of itsnetwork, components and facilities

The Group’s business requires the maintenance, upgrade and periodic replacement of facilities and networks tocontinue to function as expected in a cost-effective manner. This requires both management time as well ascapital expenditure.

If there is damage to the network, the Group will be required to incur expenses to repair the network which,depending on the issue, could be substantial. Furthermore, as the Group’s network elements become obsolete orreach their design life capacity, the Group’s operating and capital expenses could significantly increasedepending on the nature and extent of repairs or replacements.

Additionally, the operation of the network requires the coordination of specialist hardware and software. Failureof the Group to maintain or appropriately operate this could render a fibre system unable to perform at designspecifications, or at all, which could lead to further interruptions and impacts on business continuity. This couldhave an adverse effect on the Group’s ability to implement the business plan and in some cases may have amaterial adverse effect on the Group’s business, operating results, financial condition, prospects or futureoperations.

Exclusivity requirements in future agreements may adversely affect the Group’s business

As part of the Company’s strategy to grow using anchor tenant contracts, the Group at times may provideservices to these tenants on an exclusive basis for a defined period of time. This could limit the potential to fullyleverage and commercialise the assets across the network during that time period which may adversely affect theability to implement the business plan in full.

The Group has incurred operating losses in the past, and it may not be able to achieve or subsequentlymaintain profitability

Since the Group’s inception, it has incurred significant operating losses, and, as of 31 December 2016, the Grouphad retained losses of £34.6 million. Although the Group’s revenue has grown rapidly, increasing from£3.8 million in 2014 to £15.4 million in 2016, the Directors believe that the Group’s future revenue growth willdepend on, among other factors, its ability to execute its strategies set out elsewhere in this document.Accordingly, investors should not rely on the revenue growth of any prior period as an indication of the Group’sfuture performance. If the Group is unable to generate adequate revenue growth and to manage its expenses, itmay continue to incur losses in the future and may not be able to achieve or maintain profitability.

Slow-down in demand for the Group’s infrastructure may have an adverse impact on the Group’s business