Embed Size (px)

Citation preview

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 1/20

CAPITAL MARKET THEORY

SUBMITTED TO: Dr. BHANU PARTAP SINGHSUBMITTED BY: VARUN

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 2/20

Chapter Outline

Returns

Holding-Period Returns

Return StatisticsAverage Stock Returns and Risk-Free Returns

Risk Statistics

Summary and Conclusions

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 3/20

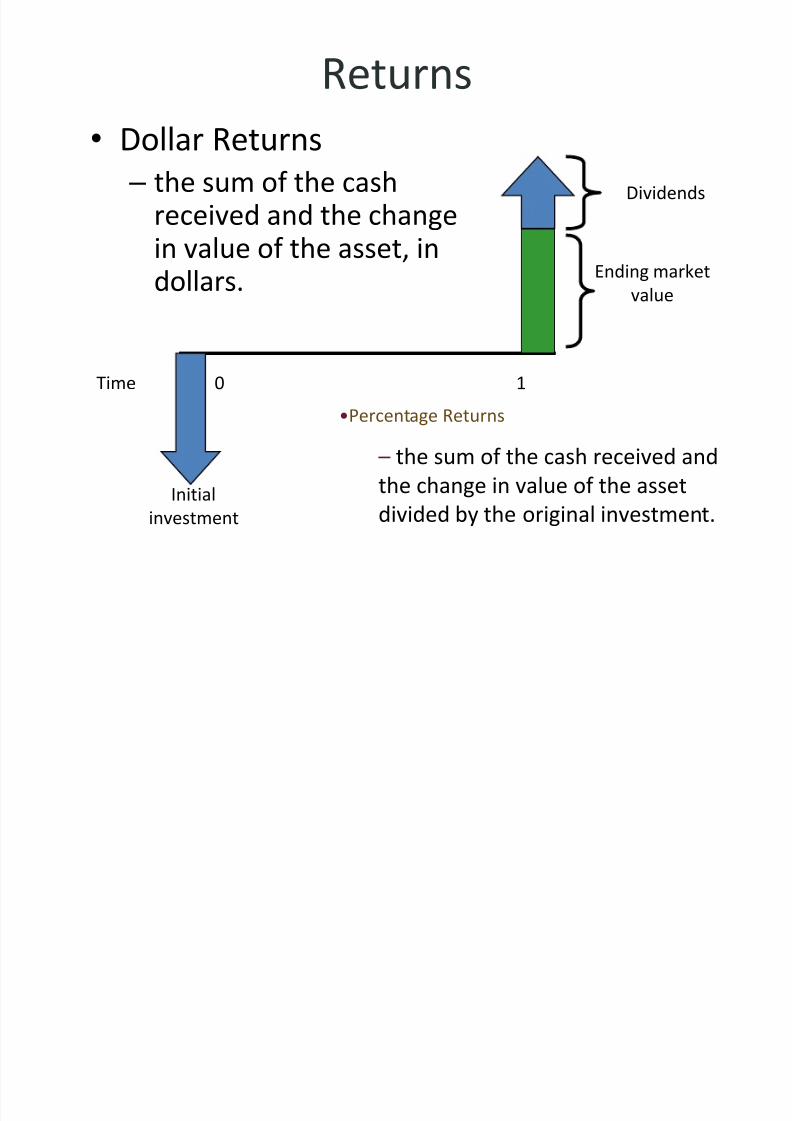

Returns

• Dollar Returns – the sum of the cash

received and the changein value of the asset, in

dollars.

Time 0 1

Initial

investment

Ending marketvalue

Dividends

•Percentage Returns

– the sum of the cash received and

the change in value of the asset

divided by the original investment.

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 4/20

Returns

Dollar Return = Dividend + Change in Market Value

yieldgainscapitalyielddividend

uemarket val beginning

uemarket valinchangedividend

uemarket val beginning

returndollar return percentage

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 5/20

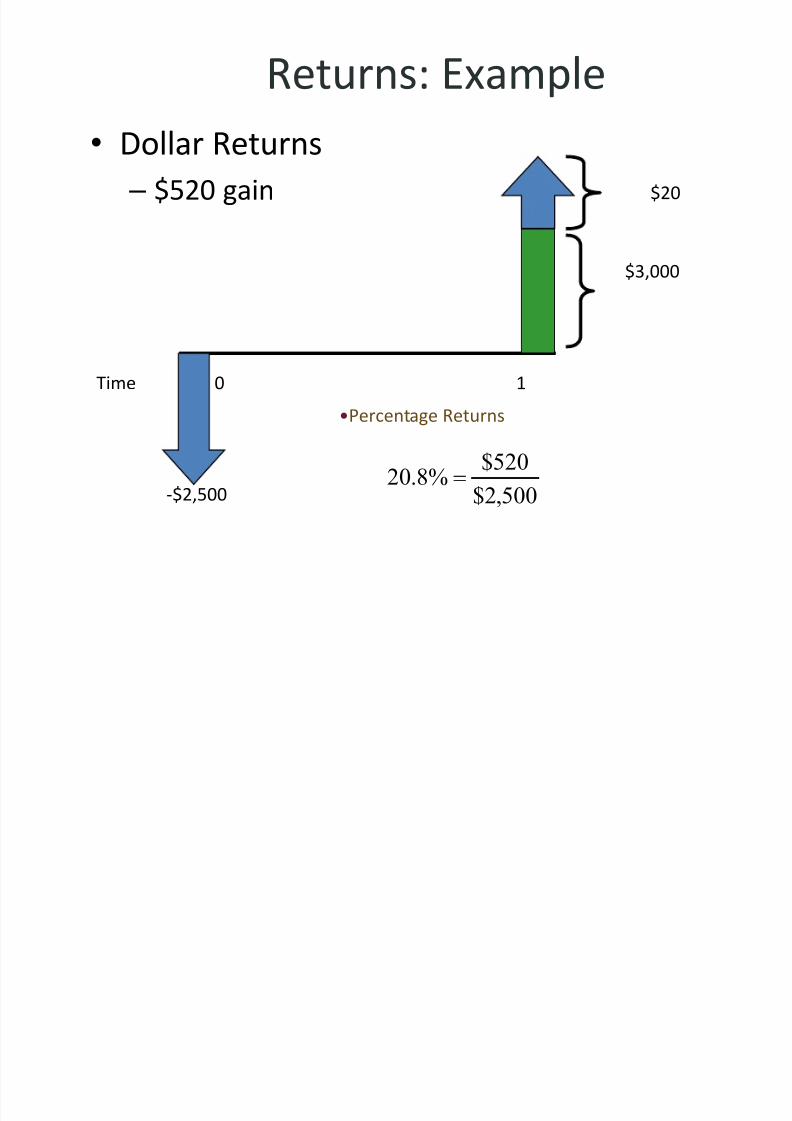

Returns: Example• Suppose you bought 100 shares of BCE one year

ago today at $25. Over the last year, you received

$20 in dividends (= 20 cents per share × 100

shares). At the end of the year, the stock sells for

$30. How did you do?• Quite well. You invested $25 × 100 = $2,500. At the

end of the year, you have stock worth $3,000 and

cash dividends of $20. Your dollar gain was $520 =

$20 + ($3,000 – $2,500).

• Your percentage gain for the year is500,2$

520$%8.20

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 6/20

Returns: Example

• Dollar Returns – $520 gain

Time 0 1

-$2,500

$3,000

$20

•Percentage Returns

500,2$

520$%8.20

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 7/20

Holding Period Returns

• The holding period return is the return that an

investor would get when holding an investment over

a period of n years, when the return during year i is

given as r i :

1)1()1()1(

return periodholding

21

nr r r

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 8/20

Holding Period Return: Example

• Suppose your investment provides the followingreturns over a four-year period:

Year Retur n

1 10%

2 -5%

3 20%

4 15% %21.444421.

1)15.1()20.1()95(.)10.1(1)1()1()1()1(

return periodholdingYour

4321

r r r r

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 9/20

Holding Period Return: Example

An investor who held this investment would haveactually realized an annual return of 9.58%:

Year Retur n

1 10%

2 -5%

3 20%

4 15% %58.9095844.

1)15.1()20.1()95(.)10.1()1()1()1()1()1(

returnaverageGeometric

4

4321

4

g

g

r r r r r r

• So, our investor made 9.58% on his money for fouryears, realizing a holding period return of 44.21%

4)095844.1(4421.1

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 10/20

Holding Period Return: Example

• Note that the geometric average is not the samething as the arithmetic average:

Year Retur n

1 10%

2 -5%

3 20%

4 15%

%10

4

%15%20%5%10

4return averageArithmetic 4321

r r r r

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 11/20

Return Statistics

• The history of capital market returns can besummarized by describing the – average return

– the standard deviation of those returns

– the frequency distribution of the returns.

T R R R T )( 1

1

)()()( 222

21

T

R R R R R RVARSD T

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 12/20

Average Stock Returns and Risk-Free Returns

The Risk Premium is the additional return (over andabove the risk-free rate) resulting from bearing risk.

One of the most significant observations of stockand bond market data is this long-run excess of

security return over the risk-free return.The average excess return from Canadian large-companycommon stocks for the period 1948 through 2000 was

6.89% = 13.09% – 6.20%

The average excess return from Canadian long-termbonds for the period 1948 through 2000 was

1.58% = 7.78% – 6.20%

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 13/20

Risk Premia

• Suppose that The National Post announced thatthe current rate for one-year Treasury bills is 5%.

• What is the expected return on the market of

Canadian large-company stocks?• Recall that the average excess return from

Canadian large-company common stocks for theperiod 1948 through 2000 was 6.89%

• Given a risk-free rate of 5%, we have an expectedreturn on the market of Canadian large-companycommon stocks of 11.89% = 6.89% + 5%

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 14/20

Rates of Return 1948-2000

-30

-20

-10

0

10

20

30

40

50

60

1945 1955 1965 1975 1985 1995

Common Stocks

Long Bonds

T-Bills

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 15/20

Risk Premiums

• Rate of return on T-bills is essentially risk-free.

• Investing in stocks is risky, but there are

compensations.

• The difference between the return on T-bills andstocks is the risk premium for investing in stocks.

• An old saying on Bay Street is “You can either sleep

well or eat well.”

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 16/20

Risk Statistics

• There is no universally agreed-upon definition

of risk.

• The measures of risk that we discuss are

variance and standard deviation.

– The standard deviation is the standard statistical

measure of the spread of a sample, and it will be

the measure we use most of this time. – Its interpretation is facilitated by a discussion of

the normal distribution.

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 17/20

Normal Distribution

• A large enough sample drawn from a normal

distribution looks like a bell-shaped curve.

– 3

– 36.35%

– 2

– 19.87%

– 1

– 3.39%

0

13.09%

+ 1

29.57%

+ 2

46.05%

+ 3

62.53%

Probability

Return on

large companycommon

stocks

68%

95%

> 99%

The probability that a yearly return will fall within 16.48-percent of the mean of

13.09-percent will be approximately 2/3.

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 18/20

Normal Distribution

• The 16.48-percent standard deviation we

found for stock returns from 1948 through

2000 can now be interpreted in the following

way: if stock returns are approximatelynormally distributed, the probability that a

yearly return will fall within 16.48-percent of

the mean of 13.09-percent will beapproximately 2/3.

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 19/20

Normal DistributionS&P 500 Return Frequencies

0

2

5

11

16

9

1212

1

2

11

00

2

4

6

8

10

12

14

16

62%52%42%32%22%12%2%-8%-18%-28%-38%-48%-58%

Annual returns

R e t u r n f r e q u e n c y

Normal

approximation

Mean = 12.8%

Std. Dev. = 20.4%

Source: © Stocks , Bon ds, Bi l ls, and Inf lat ion 2000 Yearbook™, Ibbotson Associates, Inc., Chicago (annually updates work by

Roger G. Ibbotson and Rex A. Sinquefield). All rights reserved.

7/27/2019 capital markket theory2.pptx

http://slidepdf.com/reader/full/capital-markket-theory2pptx 20/20

![[MS-PPTX]: PowerPoint (.pptx) Extensions to the Office ...MS-PPTX].pdf · [MS-PPTX]: PowerPoint (.pptx) Extensions to the Office Open XML File Format ... PowerPoint (.pptx) Extensions](https://img.dokumen.tips/doc/110x75/5ae7f6357f8b9a6d4f8ed3a1/ms-pptx-powerpoint-pptx-extensions-to-the-office-ms-pptxpdfms-pptx.jpg)

![Fundamentos de investigación1.pptx [Autoguardado].pptx](https://img.dokumen.tips/doc/110x75/56d6bd6c1a28ab30168deddb/fundamentos-de-investigacion1pptx-autoguardadopptx.jpg)