Embed Size (px)

Citation preview

CAPITAL MARKETS DAY| AMSTERDAM | 29 SEPTEMBER 2016

CAPITAL MARKETS DAY 2016 PANALPINA GROUP

THE NEW CEO

Swiss citizen, born 1973

Married, two children

Began freight forwarding career in 1991 with roles at Danzas and Nedlloyd Lines in Switzerland and U.K.

1997: Joined Panalpina, held various management positions in Europe, Africa, Central Asia and Asia Pacific

2013: Regional CEO Asia Pacific

International executive MBA from I.E. Business School in Madrid

Bachelor degree in International Trade and Freight Forwarding from EIAB, Basel

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Stefan Karlen – President and CEO

2

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Panalpina Executive Board and selected Executive Committee members

SENIOR MANAGEMENT ATTENDING CAPITAL MARKETS DAY

Robert Erni Chief Financial Officer

Karl Weyeneth Chief Commercial Officer

Karsten Breum Chief Human

Resources Officer

Ralf Morawietz Chief Information

Officer

Christoph Hess Chief Legal Officer and

Corporate Secretary

Andy Weber Chief Operating Officer

Rafic Mecattaf Head of Corporate

Development

Lucas Kuehner Global Head of Air Freight

Daryl Ridgway Global Head

of Ocean Freight

Mike Wilson Global Head of Logistics

3

OBJECTIVES OF TODAY’S CAPITAL MARKETS DAY

Demonstrate how we have de-risked the business and laid foundations for future growth

Share strategic priorities for the coming years

Engage with the leadership team

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

4

AGENDA

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Part I: Key achievements since last Capital Markets Day and Q&A

Lunch

Part II: Deep-dive sessions – Strategic priorities Session 1 - Ocean Freight and Productivity

Daryl Ridgeway, Ralf Morawietz, Andy Weber Session 2 - Sales Growth

Karl Weyeneth, Stefan Karlen Session 3 - Air Freight and Perishables

Lucas Kuehner, Colin Wells Session 4 - Logistics and Innovation

Mike Wilson, Peter Weijmarshausen (CEO Shapeways)

Break All groups reconvene in the main room

Wrap-up and conclusions

10:15 – 11:50

11:50 – 12:50

12:50 – 15:20

15:20 – 15:30

15:30 – 16:00

5

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

THE PANALPINA JOURNEY - KEY ACHIEVEMENTS SINCE 2013 CAPITAL MARKETS DAY

6

DILIGENT STRATEGY EXECUTION

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

We have laid the foundation to steadily reach best-in-class profitability and are now focusing on top line growth

2013 AND EARLIER 2016 AND BEYOND

Unclear strategy

Inefficient structure

Operations Transformation Program (OTP) at risk

High volatility in GP and profitability

Low EBIT conversion

Continue operational improvement

Accelerate growth:

Accelerate organic growth

Drive selective bolt-on M&A

Support growth through innovation

Clear and focused strategy Coherent organization and

management upgrade Centralization and offshoring of

functions Roll-out of Finance and

Operational IT systems Increase of return on sales Turnaround of loss-making

operations Cost control Selected market entries and

2 bolt-on acquisitions

2014 + 2015

7

OPERATIONAL IMPROVEMENT

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

It has been hard work….but now we are harvesting the results

Coherent organization and

management upgrade

Centralization and offshoring of functions (GBS)

Roll-out of Finance and

Operational IT systems

Increase of Return on Sales

Turnaround of loss-making operations

Cost control

8

AN EFFECTIVE MANAGEMENT PLATFORM

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Simplified and accountable senior management structure in place

We have:

A matrix organization that works well

Significantly strengthened our top 100 population (64% new since 2013)

A strong Executive Board, well aligned with the Board of Directors

Appointed CEO and 4 ExCom members via internal talents in 2016

A stable organization and are ready to grow Executive Board (EB)

+ Executive Committee (ExCom)

Board of Directors Peter Ulber

Corporate Development Rafic Mecattaf

Chief Operating Officer

Andy Weber

Ocean Freight Daryl Ridgway

Logistics Mike Wilson

Europe Volker Böhringer

Americas Frank Hercksen

Asia Pacific Sven Raudszus

MEAC Peter Triebel

Chief Financial Officer

Robert Erni

Chief Legal Officer

Christoph Hess

Chief Commercial

Officer Karl Weyeneth

Chief HR Officer

Karsten Breum

Chief Information

Officer Ralf Morawietz

Chief Executive Officer Stefan Karlen

Air Freight Lucas Kuehner

Energy Solutions Michel Dubois

9

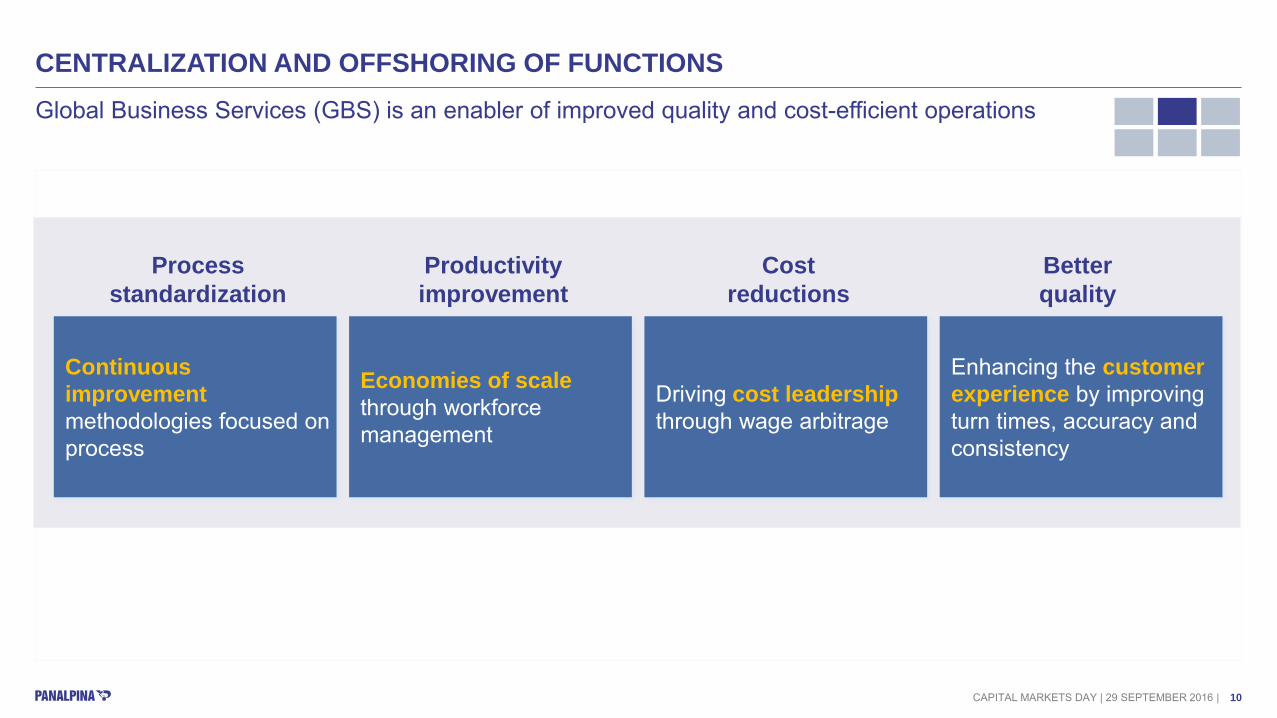

CENTRALIZATION AND OFFSHORING OF FUNCTIONS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Global Business Services (GBS) is an enabler of improved quality and cost-efficient operations

Continuous improvement methodologies focused on process

Economies of scale through workforce management

Driving cost leadership through wage arbitrage

Enhancing the customer experience by improving turn times, accuracy and consistency

Process standardization

Productivity improvement

Cost reductions

Better quality

10

CENTRALIZATION AND OFFSHORING OF FUNCTIONS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

The offshoring initiatives are on-track according to the revised plan

400+

400+ FTEs offshored (excl. outsourced F&A

jobs)

24 hour

Round-the-clock coverage & global reach

3 sites

GBS sites in Manila, Prague & Wuhan

1 network

One globally-integrated GBS network

Off-shore 20% of Air and Ocean freight processes by 2020 Centralization of processes should deliver up to 10% productivity increase annually

within GBS sites

Targets for upcoming years

11

ROLL-OUT OF FINANCE AND OPERATIONAL IT SYSTEMS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

OTP is a complex and costly program (total spending of CHF 250m) but also a prerequisite for future profitable growth and a key competitive edge to increase the gap with competitors

1) Switzerland, Germany, Italy, Singapore, China, USA, Canada, Argentina, Uruguay, Chile, Egypt

OTP Operations Transformation Program

ERP SC - Finance SAP TM - Operations

What is it? Consolidation of disparate environments into one Single Client SAP system

Replacing old legacy system and implementing global processes for Air & Ocean

Why are we doing it?

Transparency: standardized finance processes, improved reporting quality Scalability for new businesses & acquisitions

Operational leverage, streamlined processes Scalability for new businesses & acquisitions Entry ticket for future digitization opportunities

Current Status

Deployment on track Live in 11 countries 1) and Head Office

(55% of total transactions)

SAP TM live in Switzerland and Singapore Italy and Canada completed configuration phase, on

track for go-live in 2016

Outlook Next wave (mostly Western European countries)

to go-live in Q1 2017 Roll-out expected to be finished end 2017

Concept to be proven in a large country in 2017 Target to finalize 60% of transactions by 2017-18 Costs to be kept under control

12

Switzerland Germany Remaining countries

Singapore US

Italy (Q4) China / Hong-Kong

Canada (Q4) Selected Western Europe countries

2016 2017 & 2018 Beyond

ROLL-OUT OF FINANCE AND OPERATIONAL IT SYSTEMS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

SAP TM works well and we are on track to continue with a successful implementation

10%

60% 100%

Share of total shipments

Live in Singapore and Switzerland with ~125’000 shipments executed

No business interruptions

No customer complaints

Positive feedback from our operational users

Confident with our business case

Temporary roll back to old systems seamlessly possible

SAP TM (Operations)

13

Sales academy & induction program

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

INCREASE OF RETURN ON SALES All objectives set in 2013 to increase sales efficiency & effectiveness successfully implemented

890

1,070 1,200

FY 13 FY 14 FY 15

* Energy & Project Solutions

GP per Sales FTE (in CHF k, currency adj., excl. EPS*)

Increased sales efficiency at stable costs

Rebalanced organizational structure

One single CRM tool to drive opportunities

Industry vertical & account growth plans

Automated reporting incl. pipeline & performance visibility

Global incentive & bonus program

Standardized Sales process

14

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

We know how to turn around loss-making operations

TURNAROUND OF LOSS MAKING OPERATIONS

2.9

(49.5)

26.6

14.0

5.8

3.3 2.7 Evolution of 2013’s top 5 loss-making countries’ EBIT in CHFm*

* EBIT per Country after Allocations and management fees

End 2013 End 2015

We have achieved full P&L visibility at regional, country, business unit and department level allowing us to take the right management decision

Country #1

Country #2

Country #3

Country #4 Country #5

15

TURNAROUND OF LOSS MAKING OPERATIONS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Case study of a successful country turnaround – Example of Country #4

INITIAL SITUATION WHAT WAS ACHIEVED

Ranked top 5 player in Air and Ocean

Negative Direct Contribution paired with a continuing economic downtrend

Need for drastic turnaround measures signed off by the Executive Board in 2013

GP margin increased by 4 percentage points

Overhead expenses reduced drastically

EBIT improvement of CHF 3.3 m

Market reputation restored

Increase staff satisfaction

Improvement and elimination of unprofitable business

Rebalancing of sales resources on attractive industry verticals and improvement of sales efficiency

Right-sizing of management and support functions

Centralization of operations

WHAT WAS DONE

Complete “reboot” of the country organization

16

TURNAROUND OF LOSS MAKING OPERATIONS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Logistics business has been profitable for the last 6 quarters and our Energy & Project Solutions set-up is now prepared to take advantage of any sector rebound

~70 site closures and 35 sites transformed into Value-added services

(8.9) (9.2)

(12.5)

(5.5)

1.1

(2.6) (1.3)

1.2 0.3 0.5 0.1

1.8 2.3

2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Quarterly EBIT in MCHF

LOGISTICS ENERGY & PROJECT SOLUTIONS

Oil & Gas and Projects divisions successfully merged in 2014, creating synergies

Dedicated management represented at all organizational levels

Own P&L down to business unit level in relevant countries

Rightsizing of workforce (-25% since January 2015) to reflect recent business decline due to low oil price environment

In progress Done

17

in CHF m Reported FY 2013

Currency impact

Incremental IT project

costs

Other costs increase

/ (decrease)

Reported FY 2015

CAGR FY’13-15

Extrapolation of FY 2016, excl. restructuring 1)

Personnel expenses 960 (85) 4 16 896 (3.4%) ~ 890

Other operating expenses 440 (44) 18 (5) 409 (3.6%) ~ 400

Total costs 1,400 (128) 22 11 1,305 (3.4%) ~ 1,290

COST DEVELOPMENT 2013-2015

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

We have our operational costs under control

1) Corresponding to 2x H1 2016 Reported figures, excluding restructuring expenses

We have maintained our costs at 2013 level and will strive to continue this trend in 2016 and beyond

18

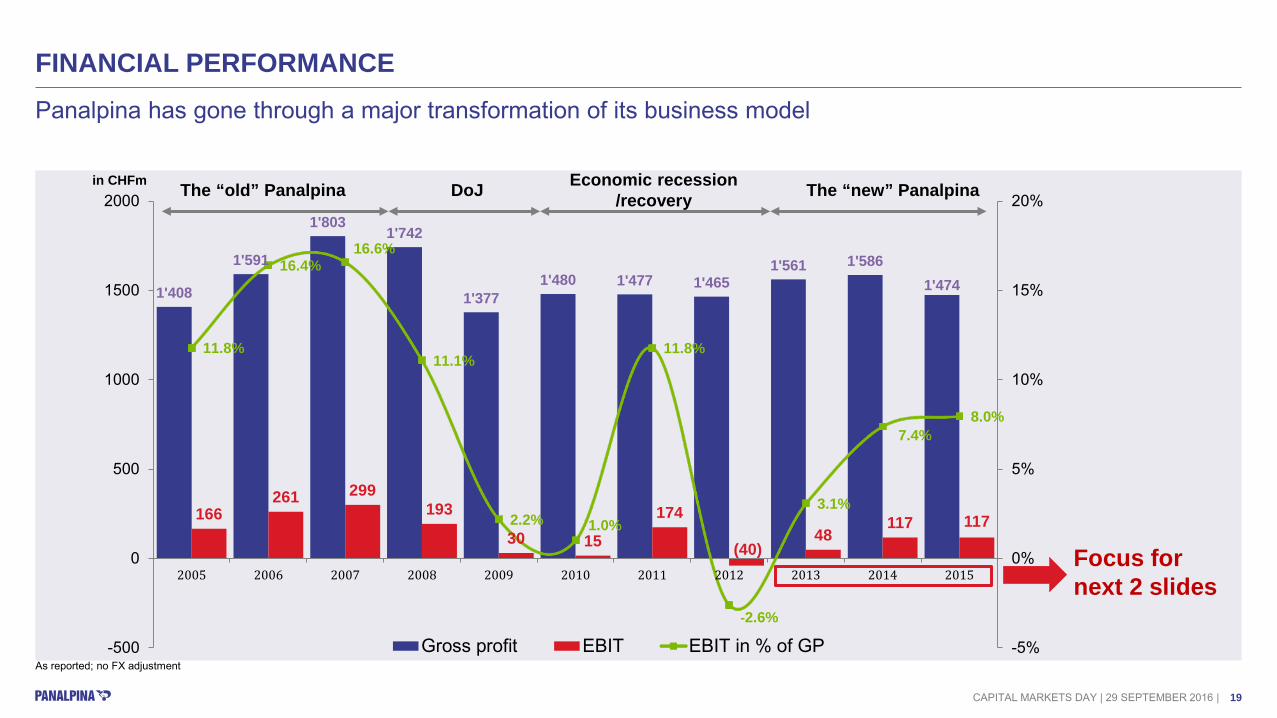

1'408

1'591

1'803 1'742

1'377 1'480 1'477 1'465

1'561 1'586 1'474

166 261 299

193

30 15

174

(40) 48

117 117

11.8%

16.4% 16.6%

11.1%

2.2% 1.0%

11.8%

-2.6%

3.1%

7.4% 8.0%

-5%

0%

5%

10%

15%

20%

-500

0

500

1000

1500

2000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Gross profit EBIT EBIT in % of GP

FINANCIAL PERFORMANCE

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Panalpina has gone through a major transformation of its business model

As reported; no FX adjustment

in CHFm The “old” Panalpina DoJ Economic recession /recovery The “new” Panalpina

Focus for next 2 slides

19

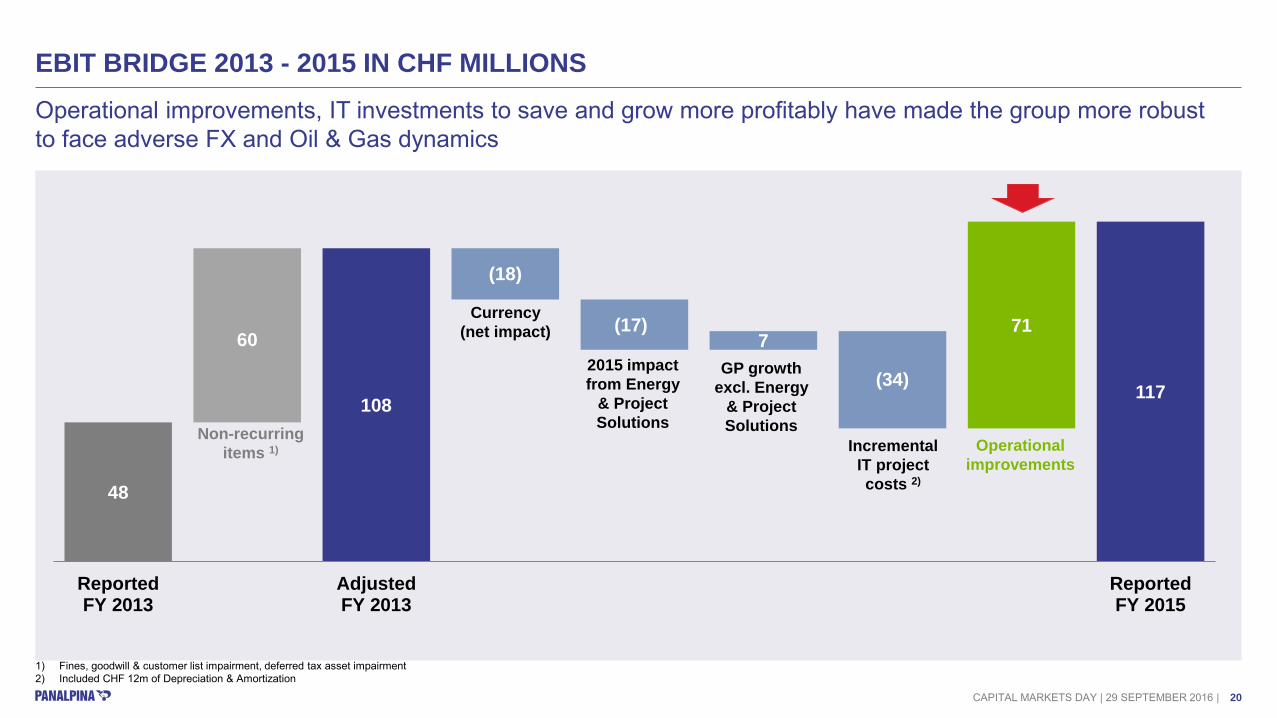

EBIT BRIDGE 2013 - 2015 IN CHF MILLIONS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Operational improvements, IT investments to save and grow more profitably have made the group more robust to face adverse FX and Oil & Gas dynamics

1) Fines, goodwill & customer list impairment, deferred tax asset impairment 2) Included CHF 12m of Depreciation & Amortization

48 48

108 90

62 62

35 35

117

60

(18)

(17) 7

(34)

71

ReportedFY 2013

AdjustedFY 2013

ReportedFY 2015

Incremental IT project costs 2)

GP growth excl. Energy

& Project Solutions

2015 impact from Energy

& Project Solutions

Currency (net impact)

Operational improvements

Non-recurring items 1)

20

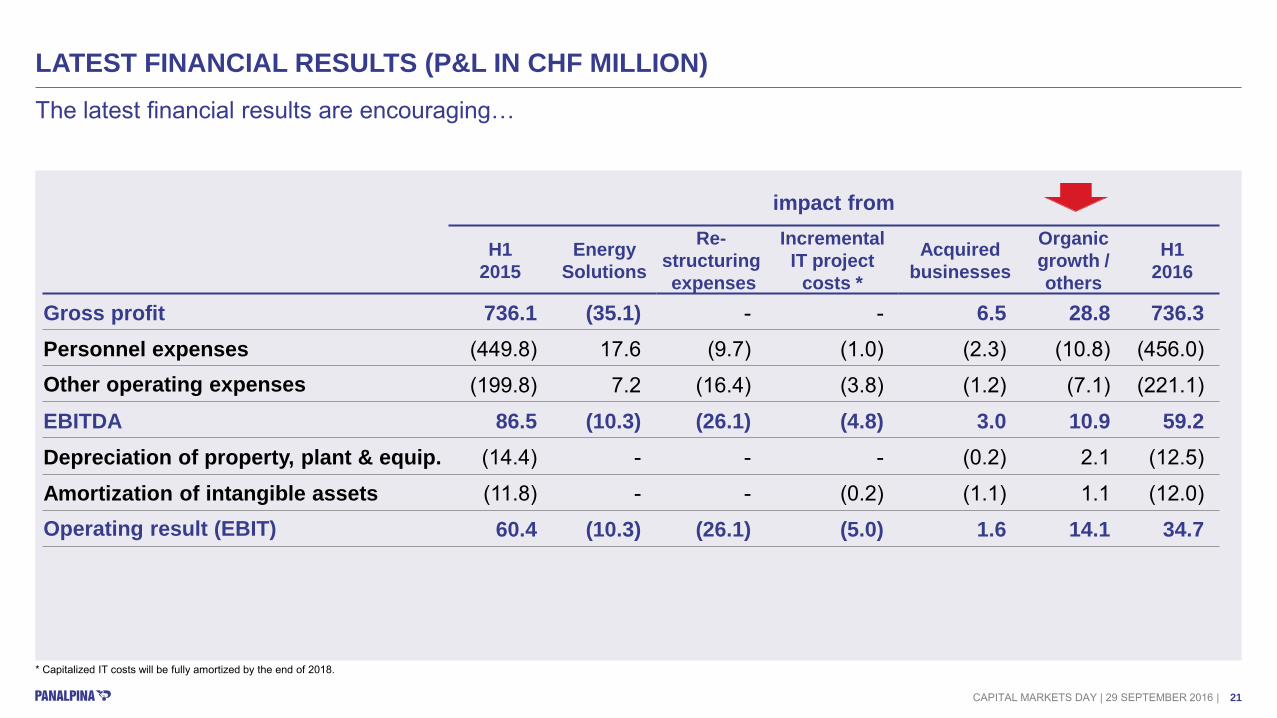

LATEST FINANCIAL RESULTS (P&L IN CHF MILLION)

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

The latest financial results are encouraging…

* Capitalized IT costs will be fully amortized by the end of 2018.

impact from

H1

2015 Energy

Solutions

Re-structuring expenses

Incremental IT project

costs *

Acquired businesses

Organic growth / others

H1 2016

Gross profit 736.1 (35.1) - - 6.5 28.8 736.3 Personnel expenses (449.8) 17.6 (9.7) (1.0) (2.3) (10.8) (456.0) Other operating expenses (199.8) 7.2 (16.4) (3.8) (1.2) (7.1) (221.1)

EBITDA 86.5 (10.3) (26.1) (4.8) 3.0 10.9 59.2 Depreciation of property, plant & equip. (14.4) - - - (0.2) 2.1 (12.5)

Amortization of intangible assets (11.8) - - (0.2) (1.1) 1.1 (12.0) Operating result (EBIT) 60.4 (10.3) (26.1) (5.0) 1.6 14.1 34.7

21

LATEST FINANCIAL RESULTS (STOCK PRICE INDEX)

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

… and have been rewarded by the stock market

1) Total shareholder return (over the period 01/01/2016 to 15/09/16) with dividends reinvested ; Source: Bloomberg

120

101

113 119

75

80

85

90

95

100

105

110

115

120

125

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16

+26%

+8%

+15% +24%

Index as of 15/09/16

Shareholder return 1)

PWTN

KNIN

EXPD DSV

Index (basis 100 = price on 02/01/16)

22

OPERATIONAL IMPROVEMENT 2013 – 2016: ACHIEVEMENTS AND REMAINING CHALLENGES

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

A differentiated and positive picture

Achievements Remaining Challenges

Restructured loss-making operations

Cost discipline is now part of our DNA

Increased return on our Sales Investments

Stable organization

Ready to grow

Diversify customer and industry verticals exposure

Improve productivity and conversion margin

23

A HIGHLY CASH GENERATIVE BUSINESS MODEL

Cash conversion and return on capital employed (ROCE)

Dividends and earnings per share

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Future cash generation will reward shareholders and be invested in growth

1) ROCE after Tax calculated as: (EBIT - Tax) / (Equity - Cash + External Debt)

75%

122%

24% 28%

2014 2015Free cash flow as % of EBIT ROCE after Tax

2.5

3.50 3.68 3.69

2014 2015Dividends per Share (CHF) Earnings per Share (CHF)1)

24

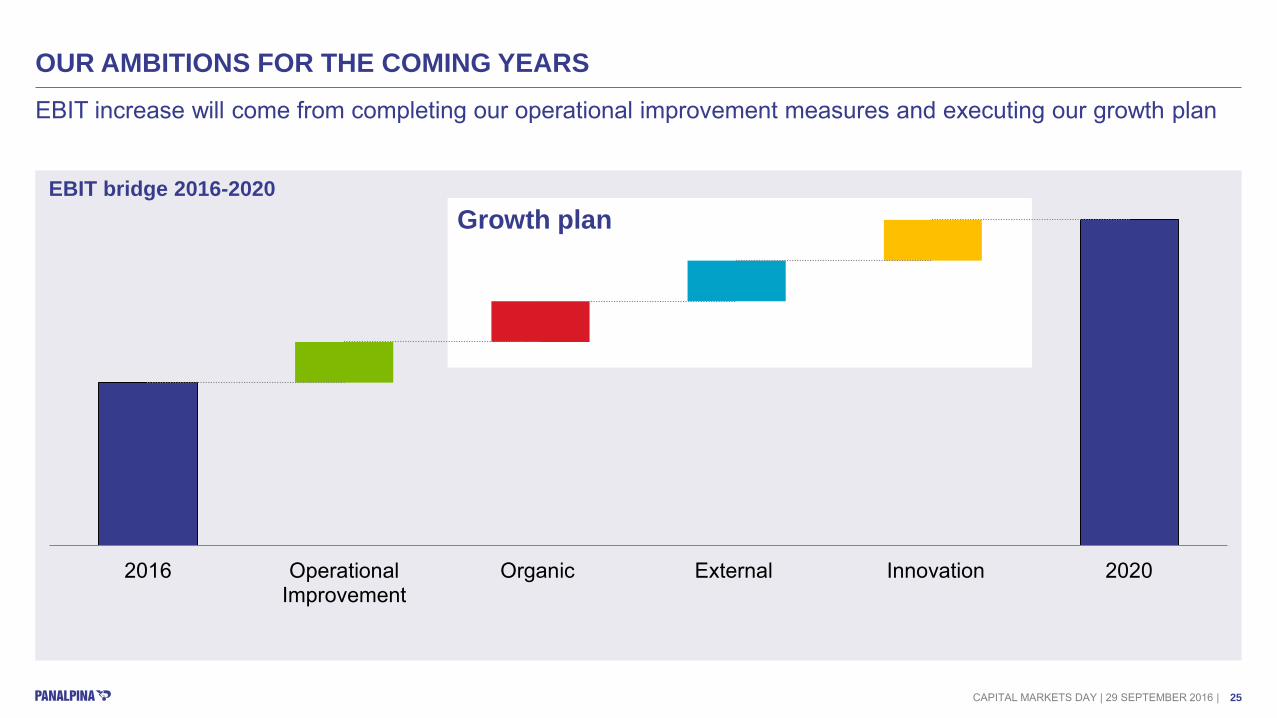

Growth plan

2016 OperationalImprovement

Organic External Innovation 2020

OUR AMBITIONS FOR THE COMING YEARS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

EBIT increase will come from completing our operational improvement measures and executing our growth plan

EBIT bridge 2016-2020

25

WRAP-UP AND STRATEGIC PRIORITIES

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

While we will diligently continue to improve our operations, we are now focusing on growth

Organic growth External growth Growth through Innovation

Increase share of wallet with existing customers

Rebalance our Industry Vertical mix

Develop new business in existing / new verticals

Expand footprint in selected geographies

Expand service portfolio

Explore opportunities from new supply chain trends

Strategic partnerships

Bolt-on M&A

Operational improvement

Restructure loss-making operations

Optimize Charter Network

Optimize GP margin, maintain costs under control

Centralize and offshore functions

Roll-out SAP TM

26

THE AFTERNOON SESSION

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Four interactive deep-dive sessions to illustrate how we execute our strategy

Ocean Freight and Productivity deep-dive

Logistics & Innovation deep-dive

Sales Growth deep-dive

Focus on productivity Focus on organic growth

Focus on Innovation

D. Ridgway – Global Head of Ocean Freight R. Morawietz – Chief Information Officer A. Weber – Chief Operations Officer

M. Wilson – Global Head of Logistics P. Weijmarshausen – CEO Shapeways Group

K. Weyeneth – Chief Commercial Officer S. Karlen – Chief Executive Officer

Air Freight and Perishables deep-dive

Focus on Perishables / Bolt-on M&A

L. Kuehner – Global Head of Air Freight C. Wells – Global Head of Perishables

Organic growth External growth Growth through Innovation

Operational improvement

27

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Q&A

28

AGENDA

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Part I: Key achievements since last Capital Markets Day and Q&A

Lunch in the Patio Restaurant

Part II: Deep-dive sessions – Strategic priorities Session 1 - Ocean Freight and Productivity - Olive

Daryl Ridgeway, Ralf Morawietz, Andy Weber Session 2 - Sales Growth - Beech

Karl Weyeneth, Stefan Karlen Session 3 - Air Freight and Perishables - Lime

Lucas Kuehner, Colin Wells Session 4 - Logistics and Innovation - Sequoia

Mike Wilson, Peter Weijmarshausen (CEO Shapeways)

Break All groups reconvene in the main room

Wrap-up and conclusions

10:15 – 11:50

11:50 – 12:50

12:50 – 15:20

15:20 – 15:30

15:30 – 16:00

29

THE AFTERNOON SESSION

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Groups rotate to their next respective workshop

13:30- 14:00 14:10- 14:40 14:50- 15:20 12:50 -13:20

Logistics and Innovation Sequoia Room

Air Freight and Perishables Lime Room

Sales Growth Beech Room

Ocean Freight and Productivity Olive Room

Group Session

1 2 3 4

30

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

OCEAN FREIGHT AND PRODUCTIVITY

31

DEEP-DIVE SESSION #1 - OCEAN FREIGHT AND PRODUCTIVITY

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

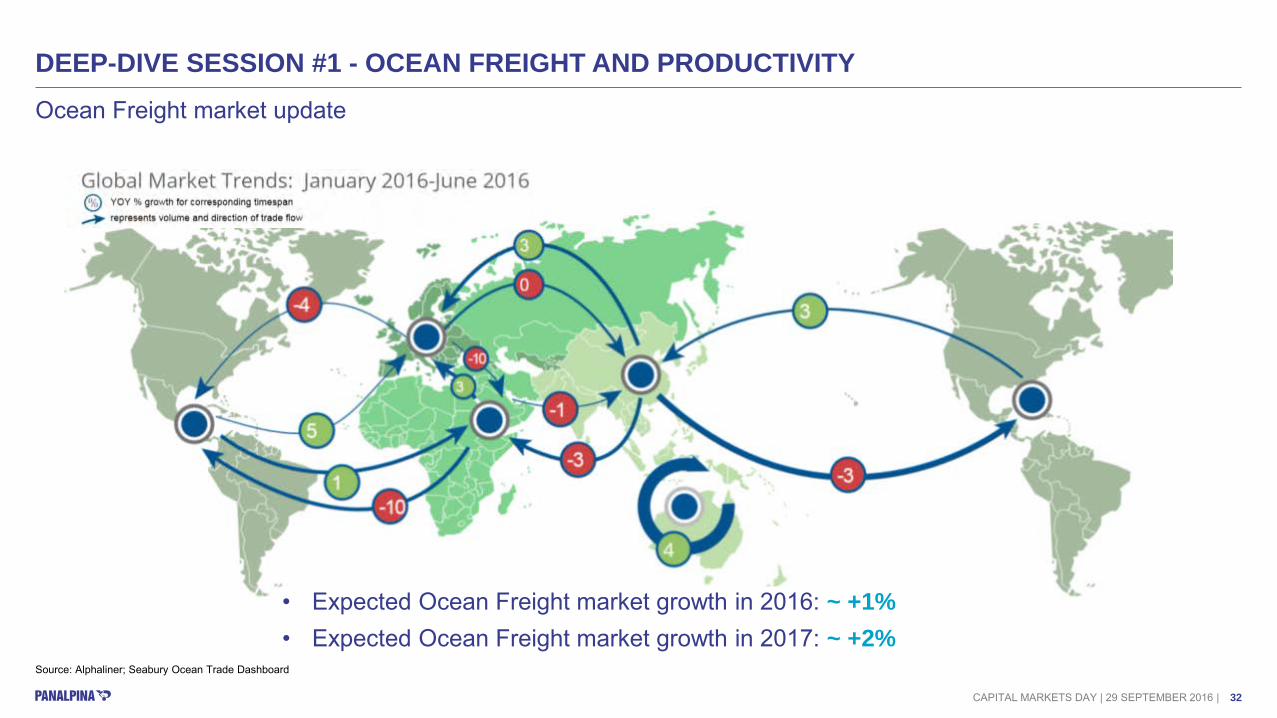

Ocean Freight market update

• Expected Ocean Freight market growth in 2016: ~ +1% • Expected Ocean Freight market growth in 2017: ~ +2%

Source: Alphaliner; Seabury Ocean Trade Dashboard

32

DEEP-DIVE SESSION #1 - OCEAN FREIGHT AND PRODUCTIVITY

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Ocean Freight market update

Source: Alphaliner; Seabury Ocean Trade Dashboard

Market outlook – Volume growth January ‘16 to July ‘16

PERISHABLES

5%

TECHNOLOGY

0%

HEALTHCARE

-3%

GOV. AID & RELIEF 6%

C&R and FASHION

0%

CHEMICALS

0%

AUTO & MANUFACT

-4%

33

DEEP-DIVE SESSION #1 - OCEAN FREIGHT AND PRODUCTIVITY

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Freight Rates & Bunker: still no sustainable levels

‒ SCFI Main Ports fell by almost 50% over the last 3 years

‒ Bunker prices followed the severe drop in crude oil prices

Carriers: merger / alliance activities and bankruptcies

‒ The acquisition of UASC takes Hapag Lloyd to #5 of Top Carrier rank

‒ Hyundai MM joining 2M alliance

‒ Bankruptcy of Hanjin Shipping

SOURCE: ALPHALINER; SEABURY OCEAN TRADE DASHBOARD

Ocean Freight market update

34

OCEAN FREIGHT FY 2013 FY 2015 H1 2016

Net forwarding revenue 2’781 2’587 1’026 Forwarding expenses (2’289) (2’107) (793) Gross profit 492 480 232 in % of NFR 17.7% 18.6% 22.6% Personnel expenses (323) (314) (154) in % of gross profit 65.8% 64.6% 66.4% Other operating expenses (123) (122) (59) in % of gross profit 25% 28.6% 25.4% EBITDA 45 45 19 in % of gross profit 9.2% 9.3% 8.2% D&A (17) (18) (8) EBIT 28 27 11 in % of gross profit 5.7% 5.5% 4.7% Total FTE 3’412 3’383 3’176 OF volumes ('000 TEUs) 1’495 1’593 721 % change YoY 8% (0.8)% (9.1)% GP/TEU (CHF) 329 306 323 % change YoY (1.0)% 3.0% 8.0%

DEEP-DIVE SESSION #1 - OCEAN FREIGHT AND PRODUCTIVITY

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Our journey since last Capital Markets Day

Strategy & objectives set in 2013 What has been achieved

Volume growth and improved procurement

Volume growth: below expectations Diversified carrier, optimized procurement &

allocation management

Additional revenue and profit margin through Managed Solutions

Acquired and implemented significant and complex Managed Solutions customers

Discipline to exit unprofitable business Promising recent business wins & pipeline

Productivity and quality improvement Productivity stagnating and still significantly below target

Maintain position among Top 5 Position #4 defended

Turn around loss-making operations and increase EBIT/GP margin

Turnaround of loss-making operations largely completed

EBIT conversion below expectations

35

DEEP-DIVE SESSION #1 - OCEAN FREIGHT AND PRODUCTIVITY

1. Productivity Improvement: further operational restructuring

and GBS acceleration aiming at a 20% EBIT / GP margin

2. Grow organically and through acquisitions

3. Further diversify Industry Verticals exposure

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Our 3 strategic priorities for the coming years

36

DEEP-DIVE SESSION #1 - OCEAN FREIGHT AND PRODUCTIVITY

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Focus on productivity - There are several levers for Panalpina to trigger in order to increase productivity

Other technology enablers • Robotic Process Automation • Unstructured to structured data • Contextual search • Probabilistic pricing

Non-technology enablers • Continuous adjustment of the operations • Organization & process improvements • Centralization of functions • Business outsourcing (GBS)

272 262 273

H1 2014 H1 2015 H1 2016

Ocean Freight Productivity – # shipments per FTE

Focus for the rest of the session

SAP TM as the main technology enabler 3 enablers for productivity

improvement

37

DEEP-DIVE SESSION #1 - ADAPTING OUR BUSINESS TO THE DIGITAL AGE

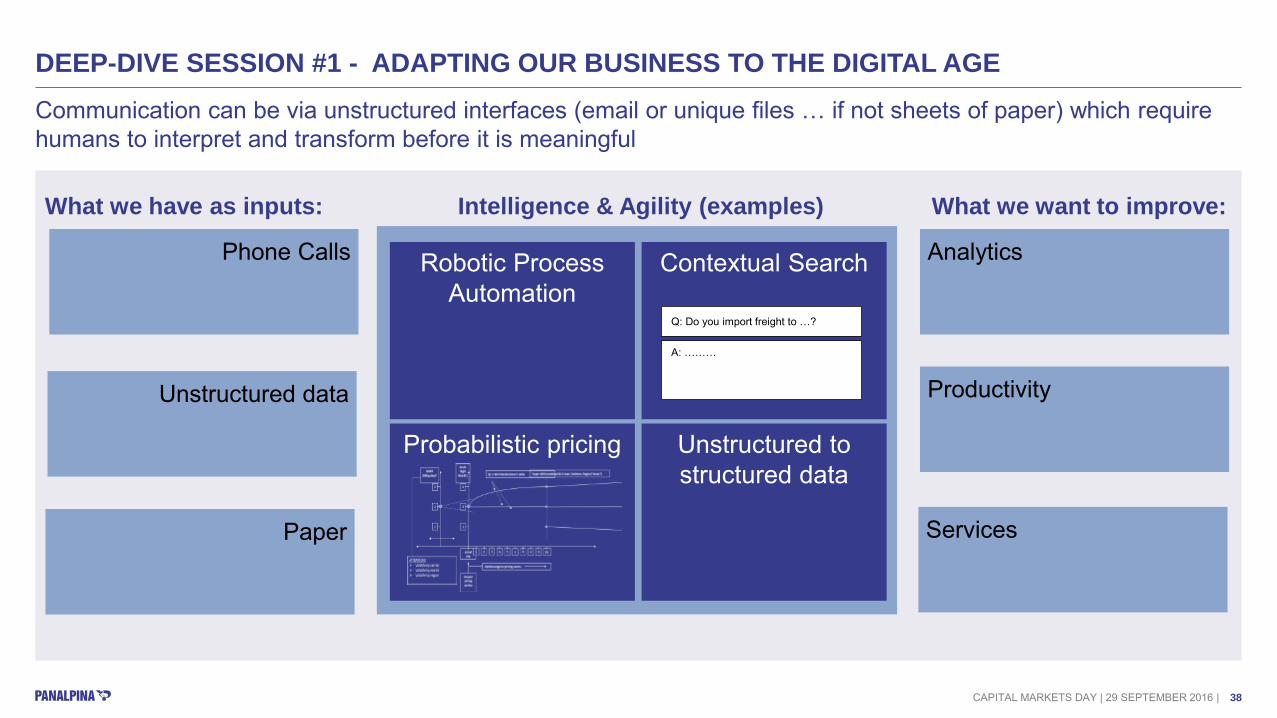

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Communication can be via unstructured interfaces (email or unique files … if not sheets of paper) which require humans to interpret and transform before it is meaningful What we have as inputs: What we want to improve:

Analytics

Productivity

Intelligence & Agility (examples)

Robotic Process Automation

Probabilistic pricing

Contextual Search

Unstructured to structured data

Q: Do you import freight to …?

A: ………

Phone Calls

Unstructured data

Paper

Services

38

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

SALES GROWTH

39

DEEP-DIVE SESSION #2: SALES GROWTH

Our Vision

We want to be the most customer focused global provider of freight forwarding and logistics solutions – a trusted, valued and respected partner

We will not rely on market growth but instead:

1. Continue to increase sales efficiency and effectiveness

2. Diversify our Industry Verticals

3. Deliver organic growth through focused resource allocation and innovative solution selling

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

We have the right strategy and structure to drive organic growth in a stagnant market

Source: Seabury

Global growth p.a. 2000-08 2008-14 2014-2016

Ocean Freight +8% +3% +1%

Air Freight +4% +2% -1%

FORWARDING MARKETS ARE STAGNANT OUR ANSWER

40

Sales academy & induction program

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

INCREASE OF RETURN ON SALES ( REMINDER OF MORNING SESSION) All objectives set in 2013 to increase sales efficiency & effectiveness successfully implemented

* Energy & Project Solutions

GP per Sales FTE (in CHF k, currency adj., excl. EPS*) Rebalanced organizational structure

One single CRM tool to drive opportunities

Industry vertical & account growth plans

Automated reporting incl. pipeline & performance visibility

Global incentive & bonus program

Standardized Sales process

890

1,070 1'200

FY 13 FY 14 FY 15Increased sales efficiency at stable costs

41

MANUFACTURING

< 10% of NFR

PERISHABLES

< 10% of NFR

HEALTHCARE

< 10% of NFR

We are de-risking our exposure to cyclical industry verticals such as Energy & Project Solutions, Hi-Tech and Automotive by increasing our exposure to Perishables and Chemicals

• Focus our sales approach on 10 strategic industry verticals (90% of our revenues) • Increase share of wallet with existing customers • Accelerate growth in selected, non-cyclical industry verticals

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

ENERGY & PROJECT SOLUTIONS

> 10% of NFR

CHEMICALS

< 10% of NFR

AUTOMOTIVE

> 10% of NFR

FASHION

< 10% of NFR

TELECOM

< 10% of NFR

DEEP-DIVE SESSION #2: SALES GROWTH

HI-TECH

> 10% of NFR

CONSUMER AND RETAIL

> 10% of NFR

Note: breakdown of Net Forwarding Revenue (NFR) for YTD August 2016

42

We have a great blue chip customer base to increase our share of wallet…

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

DEEP-DIVE SESSION #2: SALES GROWTH

Customer Segmentation Achieved growth from key accounts, compensating GP loss from Energy Project Solutions (EPS)1) :

‒ Dedicated key account management structure and executive sponsorships

‒ Value added solution selling

Increase in return on sales investments (GP increase per sales FTE)

Global Accounts

Country Accounts

Country Key Accounts

1) Gross Profit YTD July 2016: Energy & Project Solutions CHF -35M resp. All other Industry Verticals CHF +29M (excluding M&A)

43

DEEP-DIVE SESSION #2: SALES GROWTH

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

… enabling us to win major business over competition

Strategic CRF wins

New markets in Europe and South Africa

myPanalpina+ Innovative IT

platform

25,000 m3 LCL freight

TEU over 12 months

31,887 300,000 m3

Two major contracts with adidas

Carrier ocean freight

3PL international freight consolidation

Freight consolidation PO management Vendor management Buyer management

10,000

Increased AF business with adidas

Doubled business Year on Year

Carry 1/3 of adidas’ AF

business

Tons in total award

44

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

AIR FREIGHT AND PERISHABLES

45

DEEP-DIVE SESSION #3 – AIR FREIGHT AND PERISHABLES

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Air Freight market update

Source: Seabury

Capacity outgrowing demand Soft market environment Continuous pressure on rates

Capacity outgrows demand by > 5% Surcharge

Net Yield

46

Market outlook – Volume growth January ‘16 to July ‘16

DEEP-DIVE SESSION #3 – AIR FREIGHT AND PERISHABLES Air Freight market update - Differentiated dynamics across industry verticals

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

HEALTHCARE

1%

AUTO & MANUFACT - 6%

PERISHABLES

8%

C&R and FASHION

2%

CHEMICALS

-1%

TECHNOLOGY

-11%

ENERGY & PROJECT SOLN - 44%

GOV. AID & RELIEF -1%

47

DEEP-DIVE SESSION #3 – AIR FREIGHT AND PERISHABLES

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Our journey since last Capital Markets Day

AIR FREIGHT FY 2013 FY 2015 H1 2016

Net forwarding revenue 3'055.6 2'645.6 1'269.1 Forwarding expenses (2'424.2) (2'061.5) (964.6) Gross profit 631.4 584.1 304.5 in % of NFR 20.7% 22.1% 24.0% Personnel expenses (351.0) (341.3) (175.4) in % of gross profit 55.6% 58.4% 57.6% Other operating expenses (143.1) (135.4) (73.0) in % of gross profit 22.7% 23.2% 24.0% EBITDA adjusted 137.3 107.4 56.1 in % of gross profit 21.7% 18.4% 18.4% D&A (18.0) (18.9) (10.3) EBIT adjusted 119.3 88.5 45.7 in % of gross profit 18.9% 15.2% 15.0% Total FTE 3'493 3'378 3'466 AF volumes ('000 tons) 825.1 836.2 441.2 % change YoY 3.0% -2.5% 8.2% GP/ton (CHF) 765 699 690 % change YoY -2.0% -5.8% -4.1%

Strategy & objectives set in 2013

What has been achieved

Volume growth through development of 5 strategic trade lanes and backhaul lanes

Volume growth: CAGR of +3% (2013-16) Expansion/optimization of Charter Network

(> 200 scheduled charters)

Additional revenue and profit margin through end-to-end value added services

Ongoing insourcing of customs clearance in selected countries

Certifications (GDP for pharma)

Productivity and quality improvement Digitization (paperless flights on ACMI, 1st forwarder to handle 50% of transactions using e-AWB)

Productivity below target

Maintain position among Top 5 Position #4 defended

Turn around loss-making operations and increase EBIT/GP margin

Turnaround of loss-making operations largely completed

EBIT conversion below expectations

48

DEEP-DIVE SESSION #3 – AIR FREIGHT AND PERISHABLES

1. Grow organically and through acquisitions, eg Perishables

2. Further diversify Industry Verticals exposure

3. Keep cost steady and harvest productivity (centralization of

functions, roll-out of SAP TM, deployment of new technologies

in operations) to reach EBIT / GP margin of 25%

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Our 3 strategic priorities for the coming years

49

DEEP-DIVE SESSION #3 – AIR FREIGHT AND PERISHABLES

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

The perishables markets provides attractive growth opportunities …

Note: World map based on the official UN published maps. Source: Seabury

MEST

CIS

ASIA

+3% / +6%

+6% / +6%

+4% / +3%

Global future perishables growth 2016-2020: • Air Freight: +3-4% per year • Ocean Freight: +4-5% per year

+9% / +6%

+3% / +6% +7% / +3%

+7% / +1% +2% / +1%

+3% / +7%

+2% / +2%

+1% / +7% +6%

Perishables - An attractive industry vertical

High volumes

Constant growth of ~5%

Counter-cyclical

Complementary trade lanes (north-bound)

Access to major consumer goods & retail customers

Good EBIT conversion

EUROPE

NORTH AMERICA

SOUTH AMERICA

AUSTRALIA

50

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

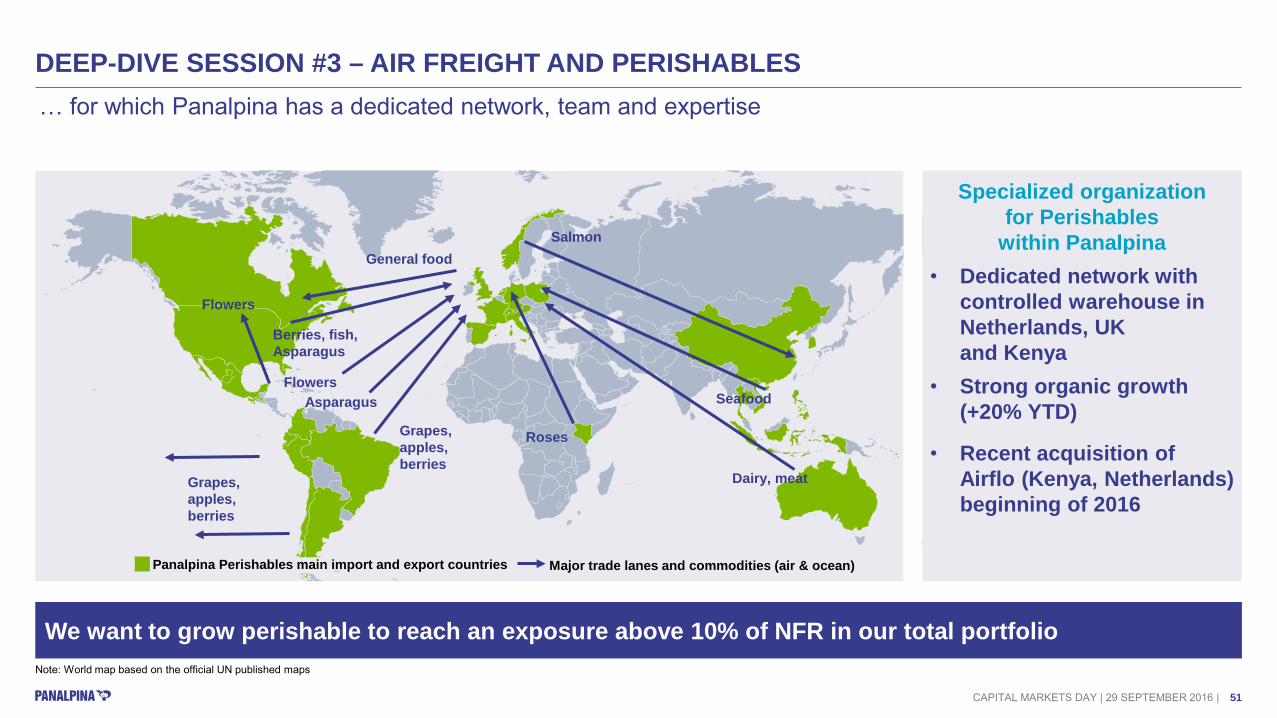

DEEP-DIVE SESSION #3 – AIR FREIGHT AND PERISHABLES … for which Panalpina has a dedicated network, team and expertise

Major trade lanes and commodities (air & ocean)

Grapes, apples, berries

Asparagus

Roses

Salmon General food

Berries, fish, Asparagus

Flowers

Flowers

Grapes, apples, berries

Dairy, meat

Seafood

Specialized organization for Perishables

within Panalpina • Dedicated network with

controlled warehouse in Netherlands, UK and Kenya

• Strong organic growth (+20% YTD)

• Recent acquisition of Airflo (Kenya, Netherlands) beginning of 2016

Note: World map based on the official UN published maps

We want to grow perishable to reach an exposure above 10% of NFR in our total portfolio

Panalpina Perishables main import and export countries

51

DEEP-DIVE SESSION #3 – AIR FREIGHT AND PERISHABLES

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Perishable value chain demands high diligence at every stage; Panalpina has developed such expertise to serve its perishables customers and be competitive in the perishables market

Step-by-step illustration of perishable value chain (example with Panalpina

Airflo movie)

52

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

LOGISTICS AND INNOVATION

53

DEEP-DIVE SESSION #4 – LOGISTICS AND INNOVATION

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

The supply chain of our customers is changing …

Large batch units made in low cost geographies Modular products, personalised close to demand

Linear manufacturing

Linear Supply Chains Circular Supply Chains

Distributed manufacturing

TODAY TOMORROW

54

DEEP-DIVE SESSION #4 – LOGISTICS AND INNOVATION

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

… enabling us to expand our service offer and generate additional profit

Component manufacture

Finished goods assembly

Finished goods storage

$10 $20 $50 -$10 -$5

Transport

$

Trad

ition

al li

near

bu

sine

ss m

odel

End consumer Raw materials

Component manufacture

Production of modules Final Assembly End consumer

$10 $20 $40 -$10 $10

Transport

$

$

PLCE

$10

Dis

trib

uted

, ci

rcul

ar m

odel

Raw materials

55

DEEP-DIVE SESSION #4 – LOGISTICS AND INNOVATION

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Our journey since the last Capital Markets Day

LOGISTICS FY 2013 FY 2015 H1 2016

Net revenue 920.6 622.5 301.5

Expenses (482.9) (213.2) (102.7)

Gross profit 437.7 409.3 198.9

in % of NFR 47.5% 65.8% 66.0%

Personnel expenses (285.6) (240.7) (116.6)

in % of gross profit 65.3% 58.8% 58.6%

Other operating expenses (174.2) (152.2) (72.3)

in % of gross profit 39.8% 37.2% 36.3%

EBITDA (22.1) 16.4 10.0

in % of gross profit -5.0% 4.0% 5.0%

D&A (17.2) (14.2) (5.8)

EBIT (39.3) 2.1 4.1

in % of gross profit -9.0% 0.5% 2.1%

Strategy & objectives set in 2013 What has been achieved

Turn around loss-making operations for sustainable EBIT

~70 site closures and 35 site transformed into value-added services

Positive EBIT since Q1 2015

Productivity and margin increase through continuous improvement (LogEx) and Best-in-class IT platform

LogEx program delivered > 2500 improvement projects and multi-million profit improvements

> 500 employees certified since the launch of the program

E2E offering and customer retention through selective Value Added Services and focused business development

Successful development of a manufacturing solution (LMS)

Successful design and implementation of innovative solutions (D2ID, e-commerce)

56

DEEP-DIVE SESSION #4 – LOGISTICS AND INNOVATION

1. Continue optimization & turnaround of the exiting Contract Logistics portfolio

2. Grow Logistics Manufacturing Services (LMS)

3. Develop new revenue streams through innovation

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Our 3 strategic priorities for the coming years

57

DEEP-DIVE SESSION #4 – LOGISTICS AND INNOVATION

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

The future of 3PL – focus on 3D printing

Why 3D Printing?

Technological innovation that will disrupt supply chain Potential threat to our Air and Ocean freight activities … but also a potential opportunity to develop new services

What do we want to do?

Provide logistics, distribution and value-added manufacturing (by leveraging our global footprint of geographies and customers)

Provide 3D printing services in defined geographies

What is our capabilities?

We are not the technological expert in 3D printing … so we have partnered up with Shapeways, the leading 3D

printing service provider, marketplace and community

58

Redefining Product Creation

Peter Weijmarshausen – CEO / CO-Founder @Weijmarshausen

Bridging the gap between the digital and the physical worlds

60

Who

61

What

62

Where

63

When

64

3D Printing is Redefining Product Creation

Who

What

How

Where

When

Companies

Mass Market

Controlled

Centralized

Months

Today + Future

Individuals

Infinite tail

Networked

Localized

Hours

Historically

65

Localized 3D printers reducing environmental impact

Ever more, ever easier apps for creating products

Leading library of 3D printable consumer products

Software innovations running 3D printers more efficiently

Unboxing sensation Physical experience

Reviews & Feedback

Customization Easy Creators & API 3D model files

Social content discovery Forums & Blogs

Marketplace

Best industry grade 3D printers, materials, and

technologies.

Offer for sale Post to your followers

Spread via social media

3D printing Post production

Quality Assurance

Instant pricing 3D printability checks Tutorials & Lessons Community support

Examples of possibilities Products photos Community stories

What have we learned - Technology

Rise of the home printer Limited innovation

What have we learned – Supply Chain Today: Family owned business Tomorrow: World Class Manufacturing

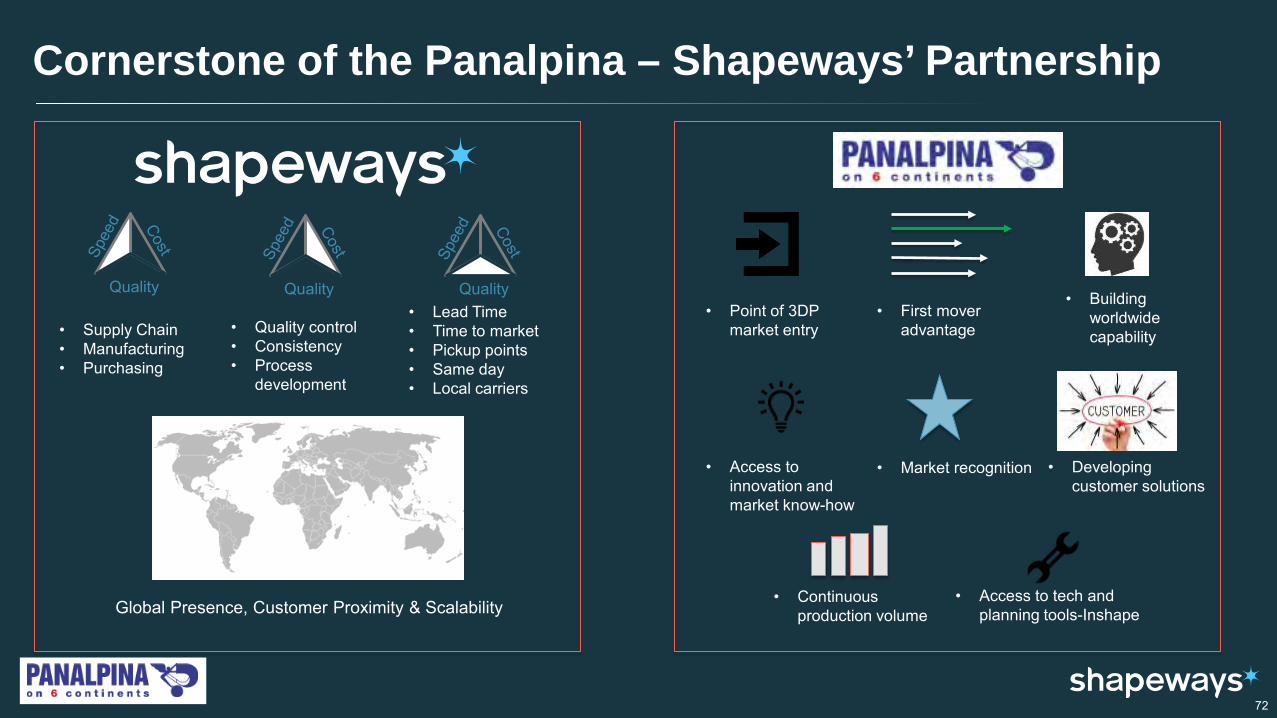

Cornerstone of the Panalpina – Shapeways’ Partnership

Quality Quality Quality • Lead Time • Time to market • Pickup points • Same day • Local carriers

• Supply Chain • Manufacturing • Purchasing

• Quality control • Consistency • Process

development

Global Presence, Customer Proximity & Scalability

• Point of 3DP market entry

• First mover advantage

• Building worldwide capability

• Access to innovation and market know-how

• Market recognition • Developing customer solutions

• Continuous production volume

• Access to tech and planning tools-Inshape

72

Innovation Center

Co-located pilot production & qualification

Co-located pilot production & qualification

Innovation Center

“Learn Locally, Scale Globally”

Roll out plan

Customers want solutions and convenience

Customers want technology and

performance

73

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

WRAP-UP AND CONCLUSIONS

75

100

150

200

250

2000 2002 2004 2006 2008 2010 2012 2014 2016

World GDP Ocean Freight (TEUs) Air Freight (tons)

Source: International Monetary Fund (IMF) April 2016 forecast, Seabury (June 2016 forecast)

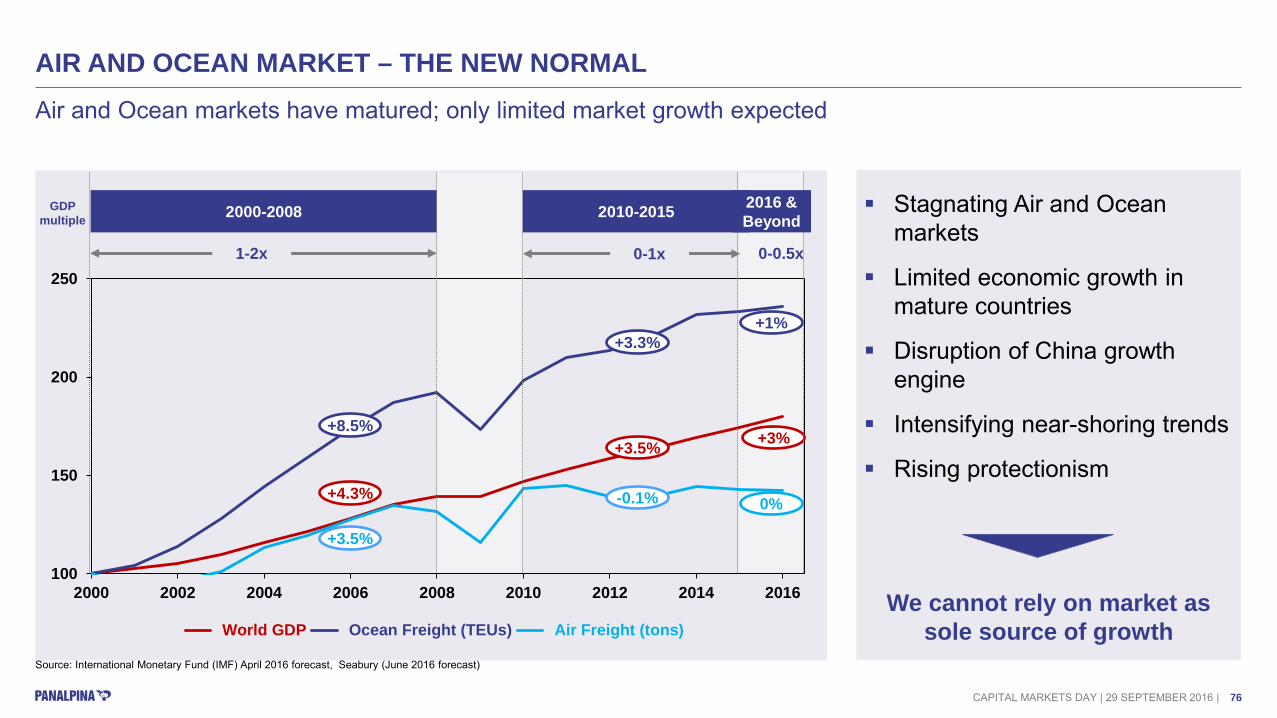

AIR AND OCEAN MARKET – THE NEW NORMAL

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

Air and Ocean markets have matured; only limited market growth expected

2000-2008 GDP multiple

1-2x 0-1x 0-0.5x

2010-2015

+8.5%

+4.3%

+3.5%

+3.3%

-0.1%

+3.5%

+1%

+3%

0%

Stagnating Air and Ocean markets

Limited economic growth in mature countries

Disruption of China growth engine

Intensifying near-shoring trends

Rising protectionism

We cannot rely on market as sole source of growth

2016 & Beyond

76

Growth plan

2016 OperationalImprovement

Organic External Innovation 2020

OUR AMBITIONS FOR THE COMING YEARS

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

EBIT increase will come from completing our operational improvement measures and executing our growth plan

EBIT bridge 2016-2020

77

OUTLOOK AND KEY TAKEAWAYS

We have successfully de-risked the business and are set to perform

We have a strong management team, an agile organization and a culture of performance

We will maintain our cost discipline and complete our operational improvement initiatives

We will intensify our focus on topline growth and diversify our Industry Vertical mix

We are driving innovation and will extend our value-added logistics services

We strive to accelerate growth with selected bolt-on acquisitions

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

We are on the right track…

78

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 |

THANK YOU! NEXT RESULTS: NINE-MONTHS RESULTS ON OCTOBER 25, 2016

79

DISCLAIMER

Investing in the shares of Panalpina World Transport Holding Ltd involves risks. Prospective investors are strongly requested to consult their investment advisors and tax advisors prior to investing in shares of Panalpina World Transport Holding Ltd.

This document contains forward-looking statements which involve risks and uncertainties. These statements may be identified by such words as “may”, “plans”, “expects”, “believes” and similar expressions, or by their context. These statements are made on the basis of current knowledge and assumptions. Various factors could cause actual future results, performance or events to differ materially from those described in these statements. No obligation is assumed to update any forward-looking statements. Potential risks and uncertainties include such factors as general economic conditions, foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

The information contained in this document has not been independently verified and no representation or warranty, express or implied, is made to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein. The information in this presentation is subject to change without notice, it may be incomplete or condensed, and it may not contain all material information concerning the Panalpina Group. None of Panalpina World Transport Holding Ltd or their respective affiliates shall have any liability whatsoever for any loss whatsoever arising from any use of this document, or its content, or otherwise arising in connection with this document.

This document does not constitute, or form part of, an offer to sell or a solicitation of an offer to purchase any shares and neither it nor any part of it shall form the basis of, or be relied upon in connection with, any contract or commitment whatsoever. This information does neither constitute an offer to buy shares of Panalpina World Transport Holding Ltd nor a prospectus within the meaning of the applicable Swiss law.

CAPITAL MARKETS DAY | 29 SEPTEMBER 2016 | 80