Embed Size (px)

Citation preview

PROJECT REPORT

ON

FINANCIAL

MARKETS

Prepared By:

Sagar Gupta (50347)

Shantnu Singh (50357)

ACKNOWLEDGEMENT

We take this opportunity to express our deep sense of gratitude to all our friends and seniors who

helped and guide us to complete this project successfully. I am highly grateful and indebted to our

project guide Dr. HK Porwal for his excellent and expert guidance in helping us in completion of

project report.

Index

Serial

No.

Particulars

1 Financials Market

2 Primary and Secondary Markets

3 Money Market

4 Capital market

5 Regulators

6 Private Placements

7 ADR/GDR

8 European Instruments

9 Indian Financial Markets and Global Integration

Introduction

The following report aims at exploring the various financial markets prevalent in the global

economy and their implications in India. Through a study of types of financial markets and their

respective structures and instruments, we aim to study the complex scenarios that investors and

economies face today. Starting with the basic overview of financial markets in general, the report

goes on to categorize different types of financial markets, enlist their structural differences and

gather information on their Indian versions. Moving on to the foreign financial instruments, we

study the basics of ADR, GDR and European instruments followed by the integration of Indian

economy with the global ones. The report also talks about other stakeholders of the financial

markets like the regulators (SEBI in Indian context) and seeks to measure out their duties and

responsibilities.

In the nutshell, the report will prove to be hands on guide for any student or a person otherwise

who wishes to get along with the basics of financial markets.

Literature Review

And

Research Methodology

The primary source of information employed throughout the research was secondary and primary

data taken from various sources online. The subject in itself is already explored to great lengths by

numerous industry experts and the required information was easily obtained through the same

however the aim of the report stays to give the basic knowledge to the reader regarding the

financial markets. Articles by various academicians and industry experts were utilized for the

purpose. Secondary research, as mentioned is the primary mode of data collection as it is apt

according to our subject here.

Financial Markets

A financial market is a market in which people and entities can trade financial securities,

commodities, and other fungible items of value at low transaction costs and at prices that reflect

supply and demand. Securities include stocks and bonds, and commodities include precious

metals or agricultural goods.

There are both general markets (where many commodities are traded) and specialized markets

(where only one commodity is traded). Markets work by placing many interested buyers and

sellers, including households, firms, and government agencies, in one "place", thus making it

easier for them to find each other. An economy which relies primarily on interactions between

buyers and sellers to allocate resources is known as a market economy in contrast either to a

command economy or to a non-market economy such as a gift economy.

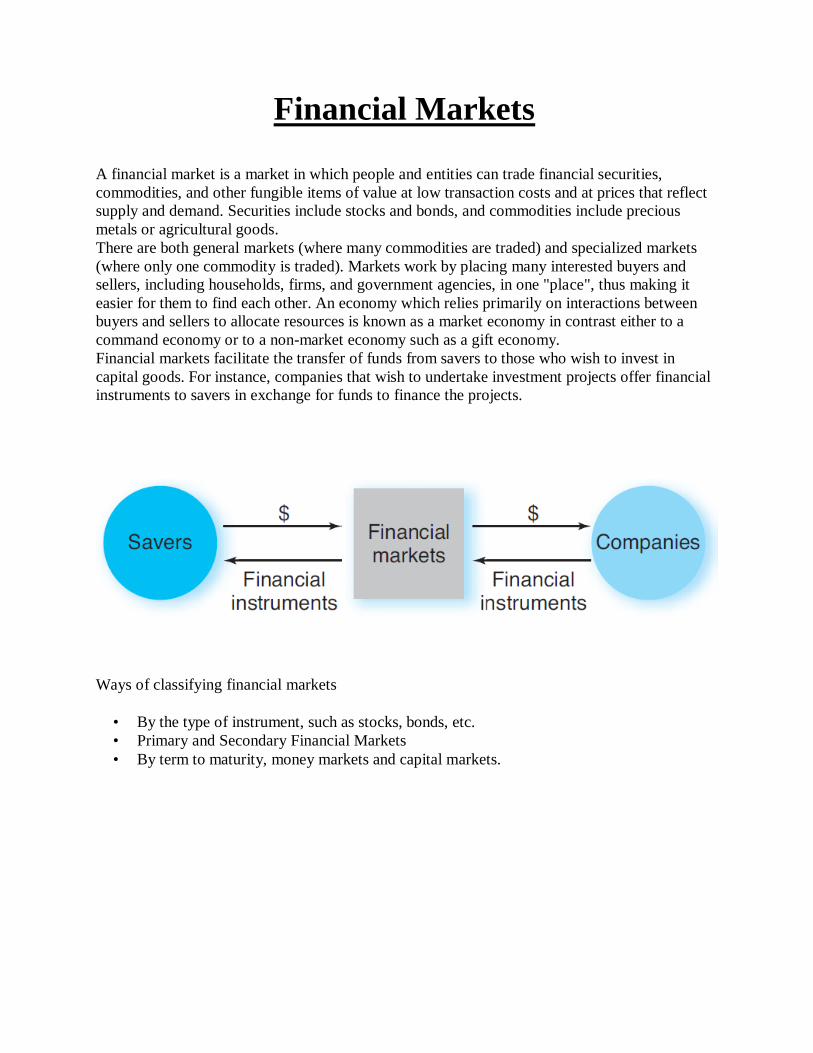

Financial markets facilitate the transfer of funds from savers to those who wish to invest in

capital goods. For instance, companies that wish to undertake investment projects offer financial

instruments to savers in exchange for funds to finance the projects.

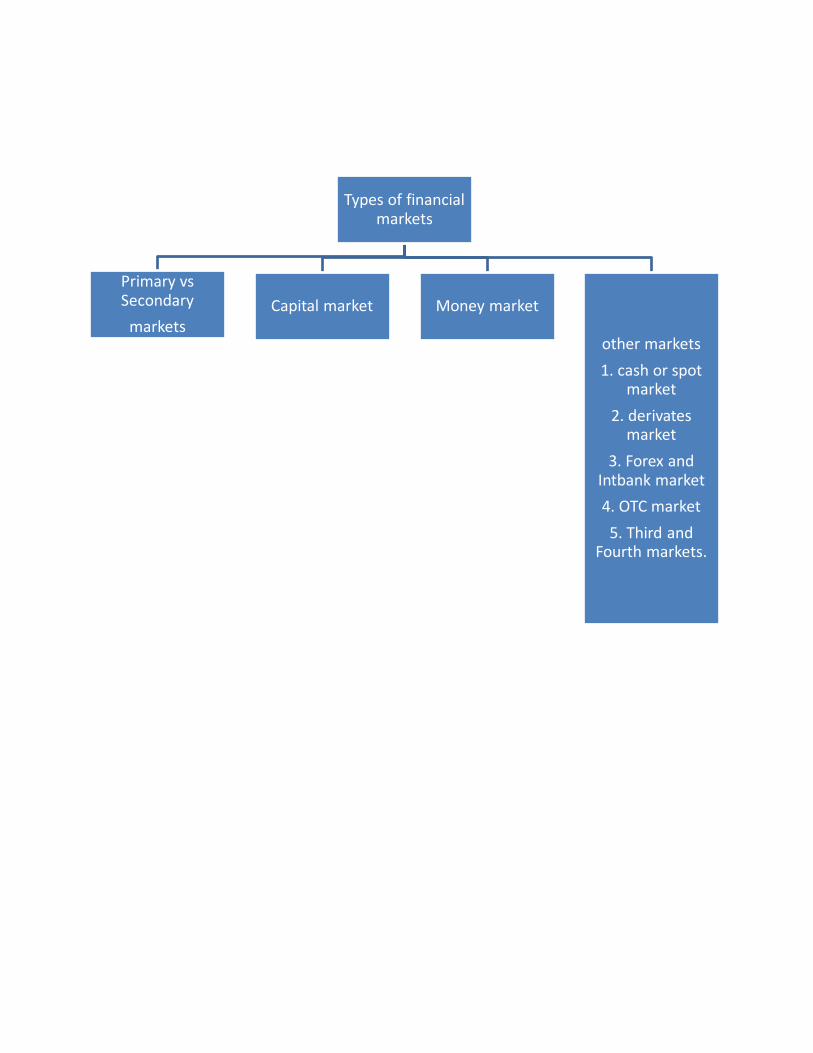

Ways of classifying financial markets

• By the type of instrument, such as stocks, bonds, etc.

• Primary and Secondary Financial Markets

• By term to maturity, money markets and capital markets.

Other Financial Markets

• Cash or Spot Market

Investing in the cash or "spot" market is highly sophisticated, with opportunities for both big

losses and big gains. In the cash market, goods are sold for cash and are delivered immediately.

By the same token, contracts bought and sold on the spot market are immediately effective.

Prices are settled in cash "on the spot" at current market prices. This is notably different from

other markets, in which trades are determined at forward prices.

The cash market is complex and delicate, and generally not suitable for inexperienced traders.

The cash markets tend to be dominated by so-called institutional market players such as hedge

funds, limited partnerships and corporate investors. The very nature of the products traded

requires access to far-reaching, detailed information and a high level of macroeconomic analysis

and trading skills.

Forex and the Interbank Market

The interbank market is the financial system and trading of currencies among banks and financial

institutions, excluding retail investors and smaller trading parties. While some interbank trading is

performed by banks on behalf of large customers, most interbank trading takes place from the

banks' own accounts.

The forex market is where currencies are traded. The forex market is the largest, most liquid

market in the world with an average traded value that exceeds $1.9 trillion per day and includes

all of the currencies in the world. The forex is the largest market in the world in terms of the total

cash value traded, and any person, firm or country may participate in this market.

There is no central marketplace for currency exchange; trade is conducted over the counter. The

forex market is open 24 hours a day, five days a week and currencies are traded worldwide

among the major financial centers of London, New York, Tokyo, Zürich, Frankfurt, Hong Kong,

Singapore, Paris and Sydney.

• Third and Fourth Markets

These don't concern individual investors because they involve significant volumes of shares to be

transacted per trade. These markets deal with transactions between broker-dealers and large

institutions through over-the-counter electronic networks. The third market comprises OTC

transactions between broker-dealers and large institutions. The fourth market is made up of

transactions that take place between large institutions. The main reason these third and fourth

market transactions occur is to avoid placing these orders through the main exchange, which

could greatly affect the price of the security. Because access to the third and fourth markets is

limited, their activities have little effect on the average investor.

Types of financial markets

Primary vs Secondary

markets Capital market Money market

other markets

1. cash or spot market

2. derivates market

3. Forex and Intbank market

4. OTC market

5. Third and Fourth markets.

Primary Market

Also called the new issue market, it is the market for issuing new securities. Many companies,

especially small and medium scale, enter the primary market to raise money from the public to

expand their businesses. They sell their securities to the public through an initial public offering.

The securities can be directly bought from the shareholders, which is not the case for the

secondary market. The primary market is a market for new capitals that will be traded over a

longer period.

In the primary market, securities are issued on an exchange basis. The underwriters, that is, the

investment banks, play an important role in this market: they set the initial price range for a

particular share and then supervise the selling of that share.

Investors can obtain news of upcoming shares only on the primary market. The issuing firm

collects money, which is then used to finance its operations or expand business, by selling its

shares. Before selling a security on the primary market, the firm must fulfill all the requirements

regarding the exchange. After trading in the primary market the security will then enter the

secondary market, where numerous trades happen every day. The primary market accelerates

the process of capital formation in a country's economy

The primary market categorically excludes several other new long-term finance sources, such as

loans from financial institutions. Many companies have entered the primary market to earn profit

by converting its capital, which is basically a private capital, into a public one, releasing securities

to the public. This phenomena is known as "public issue" or "going public."

There are three methods though which securities can be issued on the primary market: rights

issue, Initial Public Offer (IPO), and preferential issue. A company's new offering is placed on

the primary market through an initial public offer.

Secondary Market

It is the market where, unlike the primary market, an investor can buy a security directly from

another investor in lieu of the issuer. It is also referred as "after market". The securities initially

are issued in the primary market, and then they enter into the secondary market. All the

securities are first created in the primary market and then, they enter into the secondary market.

In the New York Stock Exchange, all the stocks belong to the secondary market.

In other words, secondary market is a place where any type of used goods is available. In the

secondary market shares are maneuvered from one investor to other, that is, one investor buys an

asset from another investor instead of an issuing corporation. So, the secondary market should be

liquid. Example of Secondary market:

In the New York Stock Exchange, in the United States of America, all the securities belong to

the secondary market.

Secondary Market has an important role to play behind the developments of an efficient capital

market. Secondary market connects investors' favoritism for liquidity with the capital users' wish

of using their capital for a longer period. For example, in a traditional partnership, a partner

cannot access the other partner's investment but only his or her investment in that partnership,

even on an emergency basis. Then if he or she may breaks the ownership of equity into parts and

sell his or her respective proportion to another investor. This kind of trading is facilitated only by

the secondary market

Money Market and Its Instruments

Money Market: Money market means market where money or its equivalent can be traded. Money is synonym of liquidity. Money market consists of financial institutions and dealers in

money or credit who wish to generate liquidity. It is better known as a place where large institutions and government manage their short term cash needs. For generation of liquidity, short

term borrowing and lending is done by these financial institutions and dealers. Money Market is

part of financial market where instruments with high liquidity and very short term maturities are traded. Due to highly liquid nature of securities and their short term maturities, money market is

treated as a safe place. Hence, money market is a market where short term obligations such as

treasury bills, commercial papers and banker’s acceptances are bought and sold.

Benefits and functions of Money Market: Money markets exist to facilitate efficient transfer of

short-term funds between holders and borrowers of cash assets. For the lender/investor, it provides a good return on their funds. For the borrower, it enables rapid and relatively inexpensive

acquisition of cash to cover short-term liabilities. One of the primary functions of money market

is to provide focal point for RBI‘s intervention for influencing liquidity and general levels of

interest rates in the economy. RBI being the main constituent in the money market aims at ensuring that liquidity and short term interest rates are consistent with the monetary policy

objectives.

Money Market & Capital Market: Money Market is a place for short term lending and

borrowing, typically within a year. It deals in short term debt financing and investments. On the

other hand, Capital Market refers to stock market, which refers to trading in shares and bonds of companies on recognized stock exchanges. Individual players cannot invest in money market as the

value of investments is large, on the other hand, in capital market, anybody can make

investments through a broker. Stock Market is associated with high risk and high return as against money market which is more secure. Further, in case of money market, deals are transacted on

phone or through electronic systems as against capital market where trading is through

recognized stock exchanges.

Money Market Futures and Options: Active trading in money market futures and options

occurs on number of commodity exchanges. They function in the similar manner like any other

futures and options.

Money Market Instruments: Investment in money market is done through money market

instruments. Money market instrument meets short term requirements of the borrowers and

provides liquidity to the lenders. Common Money Market Instruments are as follows:

Treasury Bills (T-Bills): Treasury Bills, one of the safest money market instruments, are short term borrowing instruments of the Central Government of the Country issued through the

Central Bank (RBI in India). They are zero risk instruments, and hence the returns are not so attractive. It is available both in primary market as well as secondary market. It is a

promise to pay a said sum after a specified period. T-bills are short-term securities that

mature in one year or less from their issue date. They are issued with three-month, six-month and one-year maturity periods. The Central Government issues T- Bills at a price less than

their face value (par value). They are issued with a promise to pay full face value on maturity. So,

when the T-Bills mature, the government pays the holder its face value. At present, the Government of India issues three types of treasury bills through auctions, namely, 91-day,

182-day and 364-day. There are no treasury bills issued by State Governments.

Treasury bills are available for a minimum amount of Rs.25K and in its multiples. The

Reserve Bank of India issues a quarterly calendar of T-bill auctions which is available at the Banks‘ website. It also announces the exact dates of auction, the amount to be auctioned and

payment dates by issuing press releases prior to every auction.

Repurchase Agreements:

Repurchase transactions, called Repo or Reverse Repo are transactions or short term loans

in which two parties agree to sell and repurchase the same security. They are usually used for overnight borrowing. Repo/Reverse Repo transactions can be done only between the parties

approved by RBI and in RBI approved securities viz. GOI and State Govt Securities, T-Bills,

PSU Bonds, FI Bonds, Corporate Bonds etc. Under repurchase agreement the seller sells specified securities with an agreement to repurchase the same at a mutually decided future date

and price. Similarly, the buyer purchases the securities with an agreement to resell the same to

the seller on an agreed date at a predetermined price. Such a transaction is called a Repo when

viewed from the perspective of the seller of the securities and Reverse Repo when viewed from the perspective of the buyer of the securities. Thus, whether a given agreement is termed as a

Repo or Reverse Repo depends on which party initiated the transaction. The lender or

buyer in a Repo is entitled to receive compensation for use of funds provided to the counterparty. Effectively the seller of the security borrows money for a period of time (Repo

period) at a particular rate of interest mutually agreed with the buyer of the security who has

lent the funds to the seller. The rate of interest agreed upon is called the Repo rate. The Repo rate

is negotiated by the counterparties independently of the coupon rate or rates of the underlying securities and is influenced by overall money market conditions.

Commercial Papers:

Commercial paper is a low-cost alternative to bank loans. It is a short term unsecured promissory note issued by corporates and financial institutions at a discounted value on face value. They are usually issued with fixed maturity between one to 270

days and for financing of accounts receivables, inventories and meeting short term liabilities. Say, for example, a company has receivables of Rs 1 lacs with credit period 6

months. It will not be able to liquidate its receivables before 6 months. The company is in

need of funds. It can issue commercial papers in form of unsecured promissory notes at

discount of 10% on face value of Rs 1 lacs to be matured after 6 months. The company has

strong credit rating and finds buyers easily. The company is able to liquidate its receivables

immediately and the buyer is able to earn interest of Rs 10K over a period of 6 months. They yield higher returns as compared to T-Bills as they are less secure in comparison to these

bills; however chances of default are almost negligible but are not zero risk instruments.

Certificate of Deposit:

It is a short term borrowing more like a bank term deposit account. It is a promissory

note issued by a bank in form of a certificate entitling the bearer to receive interest.

The certificate bears the maturity date, the fixed rate of interest and the value. It can be

issued in any denomination. They are stamped and transferred by endorsement. Its

term generally ranges from three months to five years and restricts the holders to

withdraw funds on demand. However, on payment of certain penalty the money can be

withdrawn on demand also. The returns on certificate of deposits are higher than T-Bills

because it assumes higher level of risk. While buying Certificate of Deposit, return

method should be seen. Returns can be based on Annual Percentage Yield (APY) or

Annual Percentage Rate (APR). In APY, interest earned is based on compounded

interest calculation. However, in APR method, simple interest calculation is done to

generate the return. Accordingly, if the interest is paid annually, equal return is

generated by both APY and APR methods. However, if interest is paid more than once

in a year, it is beneficial to opt APY over APR.

Banker‘s acceptance-

• It is a short term credit investment created by a non-financial firm and guaranteed by a

bank to make payment. It is simply a bill of exchange drawn by a person and accepted by a

bank. It is a buyer‘s promise to pay to the seller a certain specified amount at certain date.

The same is guaranteed by the banker of the buyer in exchange for a claim on the goods as collateral. The person drawing the bill must have a good credit rating otherwise the Banker‘s

Acceptance will not be tradable. The most common term for these instruments is 90 days.

However, they can vary from 30 days to180 days. For corporations, it acts as a negotiable time draft for financing imports, exports and other transactions in goods and is highly

useful when the credit worthiness of the foreign trade party is unknown. The seller need

not hold it until maturity and can sell off the same in secondary market at discount from the

face value to liquidate its receivables.

Capital market

The capital market is the market for securities, where Companies and governments can raise

long-term funds. It is a market in which money is lent for periods longer than a year. A

nation's capital market includes such financial institutions as banks, insurance companies, and

stock exchanges that channel long-term investment funds to commercial and industrial

borrowers. Unlike the money market, on which lending is ordinarily short term, the capital

market typically finances fixed investments like those in buildings and machinery.

Debt or Bond market

The bond market (also known as the debt, credit, or fixed income market) is a financial market

where participants buy and sell debt securities, usually in the form of bonds. As of 2009, the

size of the worldwide bond market (total debt outstanding) is an estimated $82.2 trillion , of

which the size of the outstanding U.S. bond market debt was $31.2 trillion according to BIS

(or alternatively $34.3 trillion according to SIFMA).

Market structure

Bond markets in most countries remain decentralized and lack common exchanges like stock,

future and commodity markets. This has occurred, in part, because no two bond issues are

exactly alike, and the variety of bond securities outstanding greatly exceeds that of stocks.

However, the New York Stock Exchange (NYSE) is the largest centralized bond market,

representing mostly corporate bonds. The NYSE migrated from the Automated Bond System

(ABS) to the NYSE Bonds trading system in April 2007 and expects the number of traded

issues to increase from 1000 to 6000.

Stock market-

A stock market or equity market is a public market (a loose network of economic

transactions, not a physical facility or discrete entity) for the trading of company stock and

derivatives at an agreed price; these are securities listed on a stock exchange as well as those

only traded privately.

Types of equity-

• Common stock:

Shares of corporate ownership that entitle the owner to vote on management

issues but offer no guarantees of dividends or of market value in the event of

corporate bankruptcy.

• Preferred stock:

Shares of corporate ownership that entail no voting rights but entitle the owner

to dividends if any are paid by the corporation and to any residual value of the

corporation after other creditors have been paid.

Function and purpose

1. The stock market is one of the most important sources for companies to raise money.

This allows businesses to be publicly traded, or raise additional capital for expansion by

selling shares of ownership of the company in a public market.

2. History has shown that the price of shares and other assets is an important part of the

dynamics of economic activity, and can influence or be an indicator of social mood.

The stock market is often considered the primary indicator of a country's economic

strength and development. Rising share prices, for instance, tend to be associated with

increased business investment and vice versa.

3. Exchanges also act as the clearing house for each transaction, meaning that they collect

and deliver the shares, and guarantee payment to the seller of a security. This eliminates

the risk to an individual buyer or seller that the counterparty could default on the

transaction.

The smooth functioning of all these activities facilitates economic growth in that lower costs

and enterprise risks promote the production of goods and services as well as employment. In

this way the financial system contributes to increased prosperity.

Some Stock exchanges-

• New York Stock Exchange (NYSE)

The oldest (1792) and largest exchange where roughly half of the stock trading

in the United States is done—shares of more than 3,000 companies are traded

there.

The number of NYSE membership positions, called ―seats,‖ is fixed at 1366.

• Over-the-counter (OTC) stocks:

Equity shares offered by companies that do not meet listing requirements for

major stock exchanges, or choose not to be listed there, and instead are traded in

decentralized markets.

• National Association of Securities Dealers Automated Quotation (Nasdaq):

The electronic network of 500 dealers over which most over-the-counter stocks

are traded.

Microsoft, Intel, and Cisco trade on this exchange.

Capital market instruments

A capital market is a market for securities (debt or equity), where business enterprises and

government can raise long-term funds. It is defined as a market in which money is provided for

periods longer than a year, as the raising of short-term funds takes place on other markets (e.g., the

money market). The capital market is characterized by a large variety of financial instruments: equity

and preference shares, fully convertible debentures (FCDs), non-convertible debentures (NCDs) and

partly convertible debentures (PCDs) currently dominate the capital market, however new

instruments are being introduced such as debentures bundled with warrants, participating preference

shares, zero-coupon bonds, secured premium notes, etc.

1. SECURED PREMIUM NOTES

SPN is a secured debenture redeemable at premium issued along with a detachable warrant,

redeemable after a notice period, say four to seven years. The warrants attached to SPN gives

the holder the right to apply and get allotted equity shares; provided the SPN is fully paid.

There is a lock-in period for SPN during which no interest will be paid for an invested

amount. The SPN holder has an option to sell back the SPN to the company at par value after

the lock in period. If the holder exercises this option, no interest/ premium will be paid on

redemption. In case the SPN holder holds it further, the holder will be repaid the principal

amount along with the additional amount of interest/ premium on redemption in installments

as decided by the company. The conversion of detachable warrants into equity shares will

have to be done within the time limit notified by the company.

Ex-TISCO issued warrants for the first time in India in the year 1992 to raise 1212 crore.

2. DEEP DISCOUNT BONDS

A bond that sells at a significant discount from par value and has no coupon rate or lower

coupon rate than the prevailing rates of fixed-income securities with a similar risk profile.

They are designed to meet the long term funds requirements of the issuer and investors who

are not looking for immediate return and can be sold with a long maturity of 25-30 years at a

deep discount on the face value of debentures.

Ex-IDBI deep discount bonds for Rs 1 lac repayable after 25 years were sold at a discount

price of Rs. 2,700.

3. EQUITY SHARES WITH DETACHABLE WARRANTS

A warrant is a security issued by company entitling the holder to buy a given number of

shares of stock at a stipulated price during a specified period. These warrants are separately

registered with the stock exchanges and traded separately. Warrants are frequently attached to

bonds or preferred stock as a sweetener, allowing the issuer to pay lower interest rates or

dividends.

Ex-Essar Gujarat, Ranbaxy, Reliance issue this type of instrument.

4. FULLY CONVERTIBLE DEBENTURES WITH INTEREST

This is a debt instrument that is fully converted over a specified period into equity shares. The

conversion can be in one or several phases. When the instrument is a pure debt instrument,

interest is paid to the investor. After conversion, interest payments cease on the portion that is

converted. If project finance is raised through an FCD issue, the investor can earn interest

even when the project is under implementation. Once the project is operational, the investor

can participate in the profits through share price appreciation and dividend payments

5. EQUIPREF

They are fully convertible cumulative preference shares. This instrument is divided into 2

parts namely Part A & Part B. Part A is convertible into equity shares automatically

/compulsorily on date of allotment without any application by the allottee.

Part B is redeemed at par or converted into equity after a lock in period at the option of the

investor, at a price 30% lower than the average market price.

6. SWEAT EQUITY SHARES

The phrase `sweat equity' refers to equity shares given to the company's employees on

favorable terms, in recognition of their work. Sweat equity usually takes the form of giving

options to employees to buy shares of the company, so they become part owners and

participate in the profits, apart from earning salary. This gives a boost to the sentiments of

employees and motivates them to work harder towards the goals of the company.

The Companies Act defines `sweat equity shares' as equity shares issued by the company to

employees or directors at a discount or for consideration other than cash for providing know-

how or making available rights in the nature of intellectual property rights or value additions,

by whatever name called.

7. TRACKING STOCKS

A tracking stock is a security issued by a parent company to track the results of one of its

subsidiaries or lines of business; without having claim on the assets of the division or the

parent company. It is also known as "designer stock". When a parent company issues a

tracking stock, all revenues and expenses of the applicable division are separated from the

parent company's financial statements and bound to the tracking stock. Oftentimes, this is

done to separate a subsidiary's high-growth division from a larger parent company that is

presenting losses. The parent company and its shareholders, however, still control the

operations of the subsidiary.

Ex- QQQQ, which is an exchange-traded fund that mirrors the returns of the Nasdaq 100

index

8. DISASTER BONDS

Also known as Catastrophe or CAT Bonds, Disaster Bond is a high-yield debt instrument that

is usually insurance linked and meant to raise money in case of a catastrophe. It has a special

condition that states that if the issuer (insurance or Reinsurance Company) suffers a loss from

a particular pre-defined catastrophe, then the issuer's obligation to pay interest and/or repay

the principal is either deferred or completely forgiven.

Ex- Mexico sold $290 million in catastrophe bonds, becoming the first country to use a World

Bank program that passes the cost of natural disasters to investors. Goldman Sachs Group

Inc. and Swiss Reinsurance Co. managed the bond sale, which will pay investors unless an

earthquake or hurricane triggers a transfer of the funds to the Mexican government.

9. MORTGAGE BACKED SECURITIES (MBS)

MBS is a type of asset-backed security, basically a debt obligation that represents a claim on

the cash flows from mortgage loans, most commonly on residential property. Mortgage-

backed securities represent claims and derive their ultimate values from the principal and

payments on the loans in the pool. These payments can be further broken down into different

classes of securities, depending on the riskiness of different mortgages as they are classified

under the MBS.

10. GLOBAL DEPOSITORY RECEIPTS/ AMERICAN DEPOSITORY RECEIPTS

A negotiable certificate held in the bank of one country (depository) representing a specific

number of shares of a stock traded on an exchange of another country. GDR facilitate trade of

shares, and are commonly used to invest in companies from developing or emerging markets.

GDR prices are often close to values of related shares, but they are traded and settled

independently of the underlying share.

Listing on a foreign stock exchange requires compliance with the policies of those stock

exchanges. Many times, the policies of the foreign exchanges are much more stringent than

the policies of domestic stock exchange. However a company may get listed on these stock

exchanges indirectly – using ADRs and GDRs.

If the depository receipt is traded in the United States of America (USA), it is called an

American Depository Receipt, or an ADR. If the depository receipt is traded in a country

other than USA, it is called a Global Depository Receipt, or a GDR.

But the ADRs and GDRs are an excellent means of investment for NRIs and foreign nationals

wanting to invest in India. By buying these, they can invest directly in Indian companies

without going through the hassle of understanding the rules and working of the Indian

financial market – since ADRs and GDRs are traded like any other stock, NRIs and

foreigners can buy these using their regular equity trading accounts!

Ex- HDFC Bank, ICICI Bank, Infosys have issued both ADR and GDR

11. FOREIGN CURRENCY CONVERTIBLE BONDS(FCCBs)

A convertible bond is a mix between a debt and equity instrument. It is a bond having regular

coupon and principal payments, but these bonds also give the bondholder the option to

convert the bond into stock. FCCB is issued in a currency different than the issuer's domestic

currency.

The investors receive the safety of guaranteed payments on the bond and are also able to take

advantage of any large price appreciation in the company's stock. Due to the equity side of

the bond, which adds value, the coupon payments on the bond are lower for the company,

thereby reducing its debt-financing costs.

Advantages

Some companies, banks, governments, and other sovereign entities may decide to

issue bonds in foreign currencies because, as it may appear to be more stable and

predictable than their domestic currency

Gives issuers the ability to access investment capital available in foreign markets

Companies can use the process to break into foreign markets

The bond acts like both a debt and equity instrument. Like bonds it makes regular

coupon and principal payments, but these bonds also give the bondholder the option

to convert the bond into stock

It is a low cost debt as the interest rates given to FCC Bonds are normally 30-50

percent lower than the market rate because of its equity component

Conversion of bonds into stocks takes place at a premium price to market price.

Conversion price is fixed when the bond is issued. So, lower dilution of the company

stocks

Advantages to investors

Safety of guaranteed payments on the bond

Can take advantage of any large price appreciation in the company‘s stock

Redeemable at maturity if not converted

Easily marketable as investors enjoys option of conversion in to equity if resulting to

capital appreciation

Disadvantages

Exchange risk is more in FCCBs as interest on bond would be payable in foreign

currency. Thus companies with low debt equity ratios, large forex earnings potential

only opted for FCCBs

FCCBs means creation of more debt and a FOREX outgo in terms of interest which is

in foreign exchange

In case of convertible bond the interest rate is low (around 3 to 4%) but there is

exchange risk on interest as well as principal if the bonds are not converted in to

equity. If the stock price plummets, investors will not go for conversion but

redemption. So, companies have to refinance to fulfill the redemption promise which

can hit earnings It remains a debt in the balance sheet until conversion

13. DERIVATIVES

A derivative is a financial instrument whose characteristics and value depend upon the

characteristics and value of some underlying asset typically commodity, bond, equity,

currency, index, event etc. Advanced investors sometimes purchase or sell derivatives to

manage the risk associated with the underlying security, to protect against fluctuations in

value, or to profit from periods of inactivity or decline. Derivatives are often leveraged, such

that a small movement in the underlying value can cause a large difference in the value of the

derivative.

Derivatives are usually broadly categorised by:

The relationship between the underlying and the derivative (e.g. forward, option,

swap)

The type of underlying (e.g. equity derivatives, foreign exchange derivatives and

credit derivatives)

The market in which they trade (e.g., exchange traded or over-the-counter)

Futures

A financial contract obligating the buyer to purchase an asset, (or the seller to sell an asset),

such as a physical commodity or a financial instrument, at a predetermined future date and

price. Futures contracts detail the quality and quantity of the underlying asset; they are

standardized to facilitate trading on a futures exchange. Some futures contracts may call for

physical delivery of the asset, while others are settled in cash. The futures markets are

characterized by the ability to use very high leverage relative to stock markets.

Some of the most popular assets on which futures contracts are available are equity stocks,

indices, commodities and currency.

Options

A financial derivative that represents a contract sold by one party (option writer) to another

party (option holder). The contract offers the buyer the right, but not the obligation, to buy

(call) or sell (put) a security or other financial asset at an agreed-upon price (the strike

price) during a certain period of time or on a specific date (exercise date).

A call option gives the buyer, the right to buy the asset at a given price. This 'given price' is

called 'strike price'. It should be noted that while the holder of the call option has a right to

demand sale of asset from the seller, the seller has only the obligation and not the right. For

eg: if the buyer wants to buy the asset, the seller has to sell it. He does not have a right.

Similarly a 'put' option gives the buyer a right to sell the asset at the 'strike price' to the buyer.

Here the buyer has the right to sell and the seller has the obligation to buy.

So in any options contract, the right to exercise the option is vested with the buyer of the

contract. The seller of the contract has only the obligation and no right. As the seller of the

contract bears the obligation, he is paid a price called as 'premium'. Therefore the price that is

paid for buying an option contract is called as premium.

The primary difference between options and futures is that options give the holder the right to

buy or sell the underlying asset at expiration, while the holder of a futures contract is

obligated to fulfill the terms of his/her contract.

14. PARTICIPATORY NOTES

Also referred to as "P-Notes" Financial instruments used by investors or hedge funds that are

not registered with the Securities and Exchange Board of India to invest in Indian securities.

Indian-based brokerages buy India-based securities and then issue participatory notes to

foreign investors. Any dividends or capital gains collected from the underlying securities go

back to the investors. These are issued by FIIs to entities that want to invest in the Indian

stock market but do not want to register themselves with the SEBI.

RBI, which had sought a ban on PNs, believes that it is tough to establish the beneficial

ownership or the identity of ultimate investors.

15. HEDGE FUND

A hedge fund is an investment fund open to a limited range of investors that undertakes a

wider range of investment and trading activities in both domestic and international markets,

and that, in general, pays a performance fee to its investment manager. Every hedge fund has

its own investment strategy that determines the type of investments and the methods of

investment it undertakes. Hedge funds, as a class, invest in a broad range of investments

including shares, debt and commodities.

As the name implies, hedge funds often seek to hedge some of the risks inherent in their

investments using a variety of methods, with a goal to generate high returns through

aggressive investment strategies, most notably short selling, leverage, program trading,

swaps, arbitrage and derivatives.

Legally, hedge funds are most often set up as private investment partnerships that are open to

a limited number of investors and require a very large initial minimum investment.

Investments in hedge funds are illiquid as they often require investors keep their money in the

fund for at least one year.

16. FUND OF FUNDS

A "fund of funds" (FoF) is an investment strategy of holding a portfolio of other investment

funds rather than investing directly in shares, bonds or other securities. This type of investing

is often referred to as multi-manager investment. A fund of funds allows investors to achieve

a broad diversification and an appropriate asset allocation with investments in a variety of

fund categories that are all wrapped up into one fund.

17. EXCHANGE TRADED FUNDS

An exchange-traded fund (or ETF) is an investment vehicle traded on stock exchanges, much

like stocks. An ETF holds assets such as stocks or bonds and trades at approximately the

same price as the net asset value of its underlying assets over the course of the trading day.

Most ETFs track an index, such as the S&P 500 or MSCI EAFE. ETFs may be attractive as

investments because of their low costs, tax efficiency, and stock-like features, and single

security can track the performance of a growing number of different index funds (currently

the NSE Nifty) 18. GOLD ETF

A gold Exchange Traded Fund (ETF) is a financial instrument like a mutual fund

whose value depends on the price of gold. In most cases, the price of one

unit of a gold ETF approximately reflects the price of 1 gram of gold. As the

price of gold rises, the price of the ETF is also expected to rise by the same

amount. Gold exchange-traded funds are traded on the major stock exchanges

including Zurich, Mumbai, London, Paris and New York There are also closed-

end funds (CEF's) and exchange-traded notes (ETN's) that aim to track the gold

price.

Hybrid financing instruments-

As hybrid source of financing has characteristics of both straight debt and straight equity

falling somewhere in between. The important hybrid instruments of financing are-

1. Preference share capital

It is a unique type of long term financing in that it combines some of the features of equity as

well as debentures. As a hybrid form of financing, it is similar to debenture insofar as:

1. It carries a fixed rate of dividend.

2. It ranks higher than equity as a claimant to income/assets.

3. It normally does not have voting rights.

4. It does not have a share in residual earnings/assets.

It also partakes some of the attributes of equity capital namely-

1. Dividend on preference capital is paid out of divisible tax profit, that is, it is not tax

deductible.

2. Payment of preference dividend depends on the discretion of management, that is, it is

not an obligatory payment and non-payment does not force liquidation.

3. Irredeemable type of preference shares have no fixed maturity date.

Evaluation- preference share as a source of long term financing has merits and demerits from

the point of view of investors as well as shareholders.

Merits-

1. No Legal Obligation for Dividend Payment: There is no compulsion of payment of

preference dividend because nonpayment of dividend does not amount to bankruptcy.

This dividend is not a fixed liability like the interest on the debt which has to be paid

in all circumstances.

2. Improves Borrowing Capacity: Preference shares become a part of net worth and

therefore reduces debt to equity ratio. This is how the overall borrowing capacity of

the company increases.

3. No dilution in control: Issue of preference share does not lead to dilution in control

of existing equity shareholders because the voting rights are not attached to issue of

preference share capital. The preference shareholders invest their capital with fixed

dividend percentage but they do not get control rights with them.

4. No Charge on Assets: While taking a term loan security needs to be given to the

financial institution in the form of primary security and collateral security. There are

no such requirements and therefore the company gets the required money and the

assets also remain free of any kind of charge on them.

Demerits-

1. Costly Source of Finance: Preference shares are considered a very costly source of

finance which is apparently seen when they are compared with debt as a source of

finance. The interest on debt is a tax deductible expense whereas the dividend of

preference shares is paid out of the divisible profits of the company i.e. profit after

taxes and all other expenses. For example the dividend on preference share is 9% and

interest rate on debt is 10% with prevailing tax rate of 50%. The effective cost of

preference is same i.e. 9% but that of the debt is 5% {10% * (1-50%)}. The tax shield

is the main element which makes all the difference. In no tax regime, the preference

share would be comparable to debt but such a scenario is just an imagination.

2. Skipping Dividend Disregard Market Image: Skipping of dividend payment may

not harm the company legally but it would always create a dent on the image of the

company. While applying for some kind of debt or any other kind of finance, the

lender would have this as a major concern. Under such a situation, counting skipping

of dividend as an advantage is just a fancy. Practically, a company cannot afford to

take such a risk.

3. Preference in Claims: Preference shareholders enjoy similar situation like that of an

equity shareholders but still gets a preference in both payment of their fixed dividend

and claim on assets at the time of liquidation.

Convertible debentures/ bonds-

A type of loan issued by a company that can be converted into stock by the holder and, under

certain circumstances, the issuer of the bond. By adding the convertibility option the issuer

pays a lower interest rate on the loan compared to if there was no option to convert. These

instruments are used by companies to obtain the capital they need to grow or maintain the

business.

Convertible debentures are different from convertible bonds because debentures are

unsecured; in the event of bankruptcy the debentures would be paid after other fixed income

holders. The convertible feature is factored into the calculation of the diluted per-share

metrics as if the debentures had been converted. Therefore, a higher share count reduces

metrics such as earnings per share, which is referred to as dilution.

Valuation-

The convertible debentures in india can be of three types:

1. Compulsory convertible within 18 months.

2. Optionally convertible within 36 months.

Convertible after 36 months with call and put features. However only the first two are popular.

3. Warrants

Warrants are capital markets instruments that give the holder the right, but not the

obligation, to buy ('call' warrant) or to sell ('put' warrant) an underlying asset at a specified

price (the 'strike' price or 'exercise' price) on or before a predetermined date where such

right is exercised by registered delivery or cash settlement.

The holder of a warrant buys not the underlying security itself, but the right to buy or sell

such underlying security, against the payment he makes.

Warrants;

-are securitized options;

▫ listed on an equity exchange and traded in the relevant market segment.

▫ traded in the secondary market.

▫ settled in the same way as other securities.

-are financial instruments of type called “structured products” are not issued for financial

needs of the issuers

-are solely under the responsibility of the issuer.

-entitle the holder to buy (from) or to sell (to) the issuer an underlying security, a basket of

securities, or an index, on or before a particular date, at a predetermined price, against the

premium he pays.

-represent a right, and not an obligation, for the holder.

Regulation of the Capital Market

Every capital market in the world is monitored by financial regulators and their respective

governance organization. The purpose of such regulation is to protect investors from fraud

and deception. Financial regulatory bodies are also charged with minimizing financial

losses, issuing licenses to financial service providers, and enforcing applicable laws.

The Securities and Exchange Board of India (frequently abbreviated SEBI) is the regulator

for the securities market in India. It was established on 12 April 1992 through the SEBI Act,

1992. The SEBI is managed by its members, which consists of following: a) The chairman

who is nominated by Union Government of India. b) Two members, i.e. Officers from Union

Finance Ministry. c) One member from The Reserve Bank of India. d) The remaining 5

members are nominated by Union Government of India, out of them at least 3 shall be whole-

time members.

Functions and responsibilities

SEBI has to be responsive to the needs of three groups, which constitute the market:

The issuers of securities

The investors

The market intermediaries.

SEBI has three functions rolled into one body: quasi-legislative, quasi-judicial and quasi-

executive. It drafts regulations in its legislative capacity, it conducts investigation and

enforcement action in its executive function and it passes rulings and orders in its judicial

capacity. Though this makes it very powerful, there is an appeal process to create

accountability. There is a Securities Appellate Tribunal which is a three-member tribunal and

is presently headed by a former Chief Justice of a High court - Mr. Justice NK Sodhi. A

second appeal lies directly to the Supreme Court.

Powers For the discharge of its functions efficiently, SEBI has been vested with the following

powers:

to approve by−laws of stock exchanges.

to require the stock exchange to amend their by−laws.

inspect the books of accounts and call for periodical returns from recognized stock

exchanges.

inspect the books of accounts of a financial intermediaries.

compel certain companies to list their shares in one or more stock exchanges.

levy fees and other charges on the intermediaries for performing its functions.

grant license to any person for the purpose of dealing in certain areas.

delegate powers exercisable by it.

prosecute and judge directly the violation of certain provisions of the companies Act.

power to impose monetary penalties.

Private Placement

What is private placement?

The sale of securities to a relatively small number of select investors as a way of raising capital.

Investors involved in private placements are usually large banks, mutual funds, insurance companies

and pension funds. Private placement is the opposite of a public issue, in which securities are made

available for sale on the open market.

Since a private placement is offered to a few, select individuals, the placement does not have to be

registered with the Securities and Exchange Commission. In many cases, detailed financial

information is not disclosed and a the need for a prospectus is waived. Finally, since the placements

are private rather than public, the average investor is only made aware of the placement after it has

occurred.

Who invests in private placements?

Investments in private placements carry a high degree of risk for various reasons. Securities sold

through private placements are not publicly traded and, therefore, are less liquid. Additionally,

investors may receive restricted stock that may be subject to holding period requirements.

Companies seeking private placement investments tend to be in earlier stages of development and

have not yet been fully tested in the public marketplace.

Investing in private placements requires high risk tolerance, low liquidity concerns, and long-term

commitments. Investors must be able to afford to lose their entire investment. For those reasons,

these offerings may be made available only to certain institutional investors and high net worth

individuals and entities. As with all alternative investments, investors must meet certain eligibility

tests to qualify as purchasers.

How do private placements work?

A company seeking a private placement issues a Private Placement Memorandum, or PPM. The PPM

details the company's financial situation and business plan, as well as any other pertinent

information about the company and the offering. However, a great deal of preparation is required

before the PPM is issued. The first step is to consult attorneys who specialize in private placements.

They should oversee all of the paperwork included in the PPM to help to ensure that the company is

meeting SEC and state requirements during the process.

Although potential investors will typically conduct independent research, companies should be

careful about how they promote themselves in the PPM. Investors may try to bring suit against the

issuer if they feel that the company failed to live up to representations made in the PPM.

An investment bank typically acts as an intermediary between the company issuing the PPM and potential investors. Once investors decide to invest, they complete a subscription agreement.

What is ADR

ADR is the full form of American Depository Receipts. This is the recent method adopted by

many large and well respected companies from India to raise funds from American Markets.

How ADR Operates

Indian companies have direct access to raise funds from Indian public by way of issuing

Shares, Debentures etc. However Indian companies cannot do so, in such a direct manner,

when it comes to raising funds from American people. That would entail the Indian

companies to adopt US Accounting Norms which is also called as GAAP, maintain

accounting practices as per American Financial Year (Which starts in January and ends in

December of any particular year), as also follow variety of stringent standards as per

American norms. Effectively, it would mean that the Indian company would have to follow

two different set of rules simultaneously, one to comply with the laws of Indian Companies

Act, and the other to comply with the American Laws.

The method to circumvent the American norms, but still raise funds from American people is

available by way of ADR or American Depository Receipts. In this system, the Indian

company deposits certain amount of its Indian shares with designated American Banks. The

banks, in turn, issues receipts that are equivalent in values (And also based on the intrinsic

value the Indian Company‘s shares would fetch in the American market) to the Indian

Company. These receipts essentially would be in number of receipts. Then these Indian

Companies can trade these ADRs or American Depository Receipts with the American

public. These ADRs can be purchased and traded freely without any encumbrances in the

American Stocks and Shares Market. This way the Indian company is able to enter into the

American Stocks and Shares market, and raise funds from the American public.

The role of the American bank which has issued these receipts is very crucial, since it is they

who stand guarantee to the issued receipts. Hence they do exhaustive study of the Indian

company from all perspectives, and only then issue the ADR to the Indian company.

What is GDR and how it operates

The full form of GDR is Global Depository Receipt. It is not a different financial instrument,

as it may sound, from that of ADR. In fact if the Indian Company which has issued GDRs in

the American market wishes to further extend it to other developed and advanced countries

such as Europe, then they can sell these ADRs to the public of Europe and the same would be

named as GDR.

Indian Companies with ADR & GDR

There are quite a lot of successful Indian companies that have now issued ADRs and GDRs.

Some such companies are given underneath.

Dr. Reddys

HDFC Bank

ICICI Bank

Infosys Technologies

MTNL

VSNL

WIPRO

Eurocurrency market

A Eurocurrency market is a money market that provides banking services to a variety of customers by using foreign currencies located outside of the domestic marketplace. The concept does not have

anything to do with the European Union or the banks associated with the member countries, although

the origins of the concept are heavily derived from the region. Instead, it represents any deposit of

foreign currencies into a domestic bank. For example, if Japanese yen is deposited into a bank in the United States, it is considered to be operating under the auspices of the Eurocurrency market.

This market has its roots in the World War II era. While the war was going on, political challenges

caused by the takeover of the continent by the Axis Powers meant that there was a limited

marketplace for trading in foreign currency. With no friendly government operations within the European marketplace, the traditional economies of the nations were displaced, along with the

currencies. To combat this, especially due to the fact that many American companies were tied to the

well-being of business behind enemy lines, banks across the world began to deposit large sums of foreign currency, creating a new money market.

Euro commercial paper-

An unsecured, short-term loan issued by a bank or corporation in the international money

market, denominated in a currency that differs from the corporation's domestic currency.

For example, if a U.S. corporation issues a short-term bond denominated in Canadian dollars

to finance its inventory through the international money market, it has issued euro

commercial paper.

Eurocurrency deposits-

A short-term certificate of deposit with a fixed interest rate made in a currency outside the

jurisdiction of the issuing central bank. For example, one may purchase a CD in U.S.

dollars and deposit it in a bank in Great Britain. Eurocurrency deposits help persons and

businesses hedge against short-term fluctuations in exchange rates.

Indian Financial Markets and Global

Integration

India‘s growth story has important implications for the capital market, which has grown

sharply with respect to several parameters — amounts raised number of stock exchanges

and other intermediaries, listed stocks, market capitalization, trading volumes and

turnover, market instruments, investor population, issuer and intermediary profiles.

The capital market consists primarily of the debt and equity markets. Historically, it

contributed significantly to mobilizing funds to meet public and private companies‘

financing requirements. The introduction of exchange-traded derivative instruments such

as options and futures has enabled investors to better hedge their positions and reduce

risks.

India‘s debt and equity markets rose from 75 per cent in 1995 to 130 per cent of GDP in

2005. But the growth relative to the US, Malaysia and South Korea remains low and

largely skewed, indicating immense latent potential. India‘s debt markets comprise

government bonds and the corporate bond market (comprising PSUs, corporates,

financial institutions and banks).

India compares well with other emerging economies in terms of sophisticated market

design of equity spot and derivatives market, widespread retail participation and resilient

liquidity.

SEBI‘s measures such as submission of quarterly compliance reports, and company

valuation on the lines of the Sarbanes-Oxley Act have enhanced corporate governance. But

enforcement continues to be a problem because of limited trained staff and companies not

being subjected to substantial fines or legal sanctions.

India‘s stock market rose five-fold since mid-2003 and outperformed world indices with

returns far outstripping other emerging markets, such as Mexico (52 per cent), Brazil (43

per cent) or GCC economies such as Kuwait (26 per cent) in FY-06.

In 2006, Indian companies raised more than $6 billion on the BSE, NSE and other regional

stock exchanges. Buoyed by internal economic factors and foreign capital flows, Indian

markets are globally competitive, even in terms of pricing, efficiency and liquidity.

US subprime crisis:

The financial crisis facing the Wall Street is the worst since the Great Depression and will

have a major impact on the US and global economy. The ongoing global financial crisis

will have a ‗domino‘ effect and spill over all aspects of the economy. Due to the Western

world‘s messianic faith in the market forces and deregulation, the market friendly

governments have no choice but to step in.

The top five investment banks in the US have ceased to exist in their previous forms. Bears

Stearns was taken over some time ago. Fannie Mae and Freddie Mac are nationalised to

prevent their collapse. Fannie and Freddie together underwrite half of the home loans in the

United States, and the sum involved is of $ 3 trillion—about double the entire annual

output of the British economy. This is the biggest rescue operation since the credit crunch

began. Lehman Brothers, an investment bank with a 158 year-old history, was declared

bankrupt; Merrill Lynch, another Wall Street icon, chose to pre-empt a similar fate by

deciding to sell to the Bank of America; and Goldman Sachs and Morgan Stanley have

decided to transform themselves into ordinary deposit banks. AIG, the world‘s largest

insurance company, has survived through the injection of funds worth $ 85 billion from the

US Government.

The question arises: why has this happened?

Besides the cyclical crisis of capitalism, there are some recent factors which have

contributed towards this crisis. Under the so-called ―innovative‖ approach, financial

institutions systematically underestimated risks during the boom in property prices, which

makes such boom more prolonged. This relates to the shortsightedness of speculators and

their unrestrained greed, and they, during the asset price boom, believed that it would stay

forever. This resulted in keeping the risk aspects at a minimum and thus resorting to more

and more risk taking financial activities. Loans were made on the basis of collateral whose

value was inflated by a bubble. And the collateral is now worth less than the loan. Credit

was available up to full value of the

property which was assessed at inflated market prices. Credits were given in anticipation

that rising property prices will continue. Under looming recession and uncertainty, to pay

back their mortgage many of those who engaged in such an exercise are forced to sell their

houses, at a time when the banks are reluctant to lend and buyers would like to wait in the

hope that property prices will further come down. All these factors would lead to a further

decline in property prices.

Effect of the subprime crisis on India:

Globalization has ensured that the Indian economy and financial markets cannot stay

insulated from the present financial crisis in the developed economies.

In the light of the fact that the Indian economy is linked to global markets through a full

float in current account (trade and services) and partial float in capital account (debt and

equity), we need to analyze the impact based on three critical factors: Availability of

global liquidity; demand for India investment and cost thereof and decreased consumer

demand affecting Indian exports.

The concerted intervention by central banks of developed countries in injecting liquidity is

expected to reduce the unwinding of India investments held by foreign entities, but

fresh investment flows into India are in doubt.

The impact of this will be three-fold: The element of GDP growth driven by off-shore flows

(along with skills and technology) will be diluted; correction in the asset prices which were

hitherto pushed by foreign investors and demand for domestic liquidity putting pressure on

interstates. While the global financial system takes time to ―nurse its wounds‖ leading to

low demand for investments in emerging markets, the impact will be on the cost and related

risk premium. The impact will be felt both in the trade and capital account.

Indian companies which had access to cheap foreign currency funds for financing their

import and export will be the worst hit. Also, foreign funds (through debt and equity) will

be available at huge premium and would be limited to blue-chip companies. The impact of

which, again, will be three-fold: Reduced capacity expansion leading to supply side

pressure; increased interest expenses to affect corporate profitability and increased demand

for domestic liquidity putting pressure on the interest rates. Consumer demand in developed

economies is certain to be hurt by the present crisis, leading to lower demand for Indian

goods and services, thus affecting the Indian exports.The impact of which, once again, will

be three-fold: Export-oriented units will be the worst hit impacting employment; reduced

exports will further widen the trade gap to put pressure on rupee exchange rate and

intervention leading to sucking out liquidity and pressure on interest rates.

The impact on the financial markets will be the following: Equity market will continue to

remain in bearish mood with reduced off-shore flows, limited domestic appetite due to

liquidity pressure and pressure on corporate earnings; while the inflation would stay under

control, increased demand for domestic liquidity will push interest rates higher and we are

likely to witness gradual rupee depreciation and depleted currency reserves. Overall, while

RBI would inject liquidity through CRR/SLR cuts, maintaining growth beyond 7% will be a

struggle.

The banking sector will have the least impact as high interest rates, increased demand for

rupee loans and reduced statutory reserves will lead to improved NIM while, on the other

hand, other income from cross-border business flows and distribution of investment

products will take a hit.

Banks with capabilities to generate low cost CASA and zero cost float funds will gain the

most as revenues from financial intermediation will drive the banks‘ profitability. Given the

dependence on foreign funds and off-shore consumer demand for the India growth story,

India cannot wish away from the negative impact of the present global financial crisis but

should quickly focus on alternative remedial measures to limit damage and look in-wards to

sustain growth.

Role of capital market during present crisis-

In addition to resource allocation, capital markets also provided a medium for risk

management by allowing the diversification of risk in the economy. The well-functioning

capital market improved information quality as it played a major role in encouraging the

adoption of stronger corporate governance principles, thus supporting a trading

environment, which is founded on integrity.

For a long time, the Indian market was considered too small to warrant much attention.

However, this view has changed rapidly as vast amounts of international investment have

poured into our markets over the last decade. The Indian market is no longer viewed as a

static universe but as a constantly evolving market providing attractive opportunities to the

global investing community.

Now during the present financial crisis, we saw how capital market stood still as the symbol

of better risk management practices adopted by the Indians. Though we observed a huge fall

in the Sensex and other stock market indicators but that was all due to low confidence

among the investors. Because balance sheet of most of the Indian companies listed in the

Sensex were reflecting profit even then people kept on withdrawing money.

While there was a panic in the capital market due to withdrawal by the FIIs, we saw Indian

institutional investors like insurance and mutual funds coming for the rescue under SEBI

guidelines so that the confidence of the investors doesn‘t go low.

SEBI also came up with various norms including more liberal policies regarding

participatory notes, restricting the exit from close ended mutual funds etc. to boost the

investment.

While talking about currency crisis, the rupee kept on depreciating against the dollar mainly

due to the withdrawals by FIIs. So , the capital market tried to attract FIIs once again. SEBI

came up with many revolutionary reforms to attract the foreign investors so that the

depreciation of rupee could be put to hault.

Factors affecting capital market in India-

The capital market is affected by a range of factors. Some of the factors which influence

capital market are as follows:-

A) Performance of domestic companies:-

The performance of the companies or rather corporate earnings is one of the factors which

has direct impact or effect on capital market in a country. Weak corporate earnings indicate

that the demand for goods and services in the economy is less due to slow growth in

per capita income of people . Because of slow growth in demand there is slow growth in

employment which means slow growth in demand in the near future. Thus weak

corporate earnings indicate average or not so good prospects for the economy as a whole in

the near term. In such a scenario the investors ( both domestic as well as foreign ) would be

wary to invest in the capital market and thus there is bear market like situation. The

opposite case of it would be robust corporate earnings and it‘s positive impact on the capital

market.

B) Environmental Factors :-

Environmental Factor in India‘s context primarily means- Monsoon . In India around 60 %

of agricultural production is dependent on monsoon. Thus there is heavy dependence on

monsoon. The major chunk of agricultural production comes from the states of Punjab ,

Haryana & Uttar Pradesh. Thus deficient or delayed monsoon in this part of the country

would directly affect the agricultural output in the country. Apart from monsoon other

natural calamities like Floods, tsunami, drought, earthquake, etc. also have an impact on the

capital market of a country.

C) Macro Economic Numbers :-

The macroeconomic numbers also influence the capital market. It includes Index of

Industrial Production (IIP) which is released every month, annual Inflation number

indicated by Wholesale Price Index (WPI) which is released every week, Export – Import

numbers which are declared every month, Core Industries growth rate ( It includes Six Core

infrastructure industries – Coal, Crude oil, refining, power, cement and finished steel)

which comes out every month, etc. This macro –economic indicators indicate the state of

the economy and the direction in which the economy is headed and therefore impacts the

capital market in India.

D) Global Cues :-

In this world of globalization various economies are interdependent and interconnected. An

event in one part of the world is bound to affect other parts of the world , however the

magnitude and intensity of impact would vary. Thus capital market in India is also affected

by developments in other parts of the world i.e. U.S. , Europe, Japan , etc. Global cues

includes corporate earnings of MNC‘s, consumer confidence index in developed countries,

jobless claims in developed countries, global growth outlook given by various

agencies like IMF, economic growth of major economies, price of crude –oil, credit rating

of various economies given by Moody‘s, S & P, etc.

An obvious example at this point in time would be that of subprime crisis &

recession. Recession started in U.S. and some parts of the Europe in early 2008 .Since then

it has impacted all the countries of the world- developed, developing, less- developed

and even emerging economies.

E) Political stability and government policies:-

For any economy to achieve and sustain growth it has to have political stability and pro-

growth government policies. This is because when there is political stability there is

stability and consistency in government‘s attitude which is communicated through

various government policies. The vice- versa is the case when there is no political stability

.So capital market also reacts to the nature of government, attitude of government, and

various policies of the government.

F) Growth prospectus of an economy:-

When the national income of the country increases and per capita income of people

increases it is said that the economy is growing. Higher income also means higher

expenditure and higher savings. This augurs well for the economy as higher expenditure

means higher demand and higher savings means higher investment. Thus when an

economy is growing at a good pace capital market of the country attracts more money from

investors, both from within and outside the country and vice -versa. So we can say that

growth prospects of an economy do have an impact on capital markets.