Embed Size (px)

Citation preview

Capital ManagementDEEP DIVE

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

REGULATORY BACKGROUND

TYPHON CAPITAL MANAGEMENT, LLC IS REGISTERED WITH THE U.S. COMMODITY FUTURES TRADING COMMISSION (THE "CFTC") AS A COMMODITY POOL

OPERATOR (“CPO”) AND IS EXEMPT FROM REGISTRATION WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION (THE “SEC”) UNDER SECTION 203(B)(6) OF

THE INVESTMENT ADVISERS ACT OF 1940, AS MODIFIED BY THE DODD-FRANK ACT, AND UNDER SECTION 3(C)(1) OF THE INVESTMENT COMPANY ACT OF 1940.

THIS OFFERING IS EXEMPT FROM REGISTRATION WITH THE SEC BY REASON OF SECTION 4(A)(2) OF THE SECURITIES ACT OF 1933 AND RULE 506 PROMULGATED

THEREUNDER.

PURSUANT TO AN EXEMPTION FROM THE CFTC IN CONNECTION WITH POOLS WHOSE PARTICIPANTS ARE LIMITED TO QUALIFIED ELIGIBLE INVESTORS. A PPM

FOR THESE POOLS IS NOT REQUIRED TO BE, AND HAS NOT BEEN FILED WITH THE CFTC. THE CFTC DOES NOT PASS UPON THE MERITS OF PARTICIPATING IN A

POOL OR UPON THE ADEQUACY OR ACCURACY OF A PRIVATE PLACEMENT MEMORANDUM. CONSEQUENTLY, THE CFTC HAS NOT REVIEWED OR APPROVED THIS

OFFERING OR ANY PPM FOR THESE POOLS.

PURSUANT TO RULE 506(B) OF REGULATION D, THIS POOL IS OFFERED AS A PRIVATE OFFERING UNDER SECTION 4(A)(2) AND ITS INVESTORS ARE LIMITED TO

CERTAIN QUALIFIED INVESTORS.

RISK DISCLOSURE STATEMENT

THE RISK OF LOSS IN TRADING COMMODITIES CAN BE SUBSTANTIAL. YOU SHOULD THEREFORE CAREFULLY CONSIDER WHETHER SUCH TRADING IS SUITABLE

FOR YOU IN LIGHT OF YOUR FINANCIAL CONDITION. IN CONSIDERING WHETHER TO TRADE OR TO AUTHORIZE SOMEONE ELSE TO TRADE FOR YOU, YOU SHOULD

BE AWARE OF THE FOLLOWING:

IF YOU PURCHASE A COMMODITY OPTION YOU MAY SUSTAIN A TOTAL LOSS OF THE PREMIUM AND OF ALL TRANSACTION COSTS.

IF YOU PURCHASE OR SELL A COMMODITY FUTURE OR SELL A COMMODITY OPTION YOU MAY SUSTAIN A TOTAL LOSS OF THE INITIAL MARGIN FUNDS AND ANY

ADDITIONAL FUNDS THAT YOU DEPOSIT WITH YOUR BROKER TO ESTABLISH OR MAINTAIN YOUR POSITION. IF THE MARKET MOVES AGAINST YOUR POSITION,

YOU MAY BE CALLED UPON BY YOUR BROKER TO DEPOSIT A SUBSTANTIAL AMOUNT OF ADDITIONAL MARGIN FUNDS, ON SHORT NOTICE, IN ORDER TO MAINTAIN

YOUR POSITION. IF YOU DO NOT PROVIDE THE REQUIRED FUNDS WITHIN THE PRESCRIBED TIME, YOUR POSITION MAY BE LIQUIDATED AT A LOSS, AND YOU

WILL BE LIABLE FOR ANY RESULTING DEFICIT IN YOUR ACCOUNT.

UNDER CERTAIN MARKET CONDITIONS, YOU MAY FIND IT DIFFICULT OR IMPOSSIBLE TO LIQUIDATE A POSITION. THIS CAN OCCUR, FOR EXAMPLE, WHEN THE

MARKET MAKES A “LIMIT MOVE.” THE PLACEMENT OF CONTINGENT ORDERS BY YOU OR BY YOUR TRADING ADVISOR SUCH AS A “STOP-LOSS” OR “STOP-LIMIT”

ORDER, WILL NOT NECESSARILY LIMIT YOUR LOSSES TO THE INTENDED AMOUNTS, SINCE MARKET CONDITIONS MAY MAKE IT IMPOSSIBLE TO EXECUTE SUCH

ORDERS.

A “SPREAD” POSITION MAY NOT BE LESS RISKY THAN A SIMPLE “LONG” OR “SHORT” POSITION.

THE HIGH DEGREE OF LEVERAGE THAT IS OFTEN OBTAINABLE IN COMMODITY TRADING CAN WORK AGAINST YOU AS WELL AS FOR YOU. THE USE OF LEVERAGE

CAN LEAD TO LARGE LOSSES AS WELL AS GAINS.

IN SOME CASES, MANAGED COMMODITY ACCOUNTS ARE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT AND ADVISORY FEES. IT MAY BE NECESSARY

FOR THOSE ACCOUNTS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR

ASSETS. THE RELEVANT OFFERING DOCUMENTS CONTAIN A COMPLETE DESCRIPTION OF EACH FEE TO BE CHARGED TO YOUR ACCOUNT BY THE COMMODITY

TRADING ADVISOR.

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY TRADING ADVISOR MAY ENGAGE IN TRADING FOREIGN FUTURES OR OPTIONS CONTRACTS.

TRANSACTIONS ON MARKETS LOCATED OUTSIDE THE UNITED STATES, INCLUDING MARKETS FORMALLY LINKED TO A UNITED STATES MARKET, MAY BE SUBJECT

TO REGULATIONS WHICH OFFER DIFFERENT OR DIMINISHED PROTECTION. FURTHER, UNITED STATES REGULATORY AUTHORITIES MAY BE UNABLE TO COMPEL

THE ENFORCEMENT OF THE RULES OF REGULATORY AUTHORITIES OR MARKETS IN NON-UNITED STATES JURISDICTIONS WHERE YOUR TRANSACTIONS MAY BE

EFFECTED. BEFORE YOU TRADE YOU SHOULD INQUIRE ABOUT ANY RULES RELEVANT TO YOUR PARTICULAR CONTEMPLATED TRANSACTIONS AND ASK THE FIRM

WITH WHICH YOU INTEND TO TRADE FOR DETAILS ABOUT THE TYPES OF REDRESS AVAILABLE IN BOTH YOUR LOCAL AND OTHER RELEVANT JURISDICTIONS.

THIS BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER SIGNIFICANT ASPECTS OF THE COMMODITY MARKETS. YOU SHOULD THEREFORE

CAREFULLY STUDY THIS DISCLOSURE DOCUMENT AND COMMODITY TRADING BEFORE YOU TRADE INCLUDING THE DESCRIPTION OF PRINCIPAL RISK FACTORS IN

THE RELEVANT OFFERING DOCUMENTS.

THIS COMMODITY TRADING ADVISOR IS PROHIBITED BY LAW FROM ACCEPTING FUNDS IN THE TRADING ADVISOR’S NAME FROM A CLIENT FOR TRADING

COMMODITY INTERESTS. YOU MUST PLACE ALL FUNDS FOR TRADING IN THIS TRADING PROGRAM DIRECTLY WITH A FUTURES COMMISSION MERCHANT.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

Etymology

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Name: Ty·phon

Pronunciation: \ˈtī-ˌfän\

Etymology: Latin, from Greek Typhōn

n: (Greek mythology) a monster with a hundred heads and one of

the whirlwinds; son of Typhoneus and Echidna; father of

Cerberus and the Chimera and the Sphinx.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

n: a deconstructed multi-strategy trading firm, where niche

managers can focus only on trading under an umbrella of unified

operations, compliance, independent risk management, and

business development. Clients can access these modular exposures

a la carte or via custom portfolios in Cayman or U.S. funds, or

managed accounts.

.

Passive Commodities Have No Intrinsic Returns

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

“Commodities are like dead money. They do not pay any interest or dividends

and are not expected to earn any return over the inflation rate. A bar of gold does

not generate any cash and will never turn into two bars of gold. Year

after year it just sits there, costing you money in storage, insurance and perhaps a

management fee if you invest in a gold ETF.”

Rick Ferri- http://online.wsj.com/news/articles/SB10001424127887323681904578643822549165446

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

Typhon Generates Alpha with Tactical Trading

http://managed-futures-blog.attaincapital.com/2014/08/25/trade-commodities-instead-of-invest-in-them/

Tactical traders can

profit from moves

to the downside of

commodity prices.

Unlike with equities,

it is simple to short

commodities, and

active trading

strategies have no

directional bias.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

What Typhon looks for in a Manager

Defined edge

DifferentiatedStrategy

Uncorrelated returns

Typhon looks for managers that

have a clearly defined edge within

the markets they trade. In most

cases, this leads us to focused,

niche managers.

Typhon’s strategies are

uncorrelated to each other as well

as the broader universe of stocks,

bonds, real estate, hedge funds,

and CTAs.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

Typhon Benefits

Favorable Tax Treatment

Typhon investments have 60/40 long-term/short-term capital gains taxation for U.S. investors.

Liquidity

Typhon SMAs have daily liquidity, while our strategies available on platforms have intra-month liquidity.

Transparency

Typhon offers full transparency in near real-time.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

Typhon Risk Management

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Independence The Risk Committee is independent from each of our trading groups. We protect our investors by ensuring that our managers are operating within their guidelines.

Empowered The Risk Committee has the authority to reduce exposure in the event that a manager has breached its risk limits. It is important to draw a distinction between risk management and risk monitoring.

Proprietary Tools Typhon has developed a suite of proprietary tools that are customized for each strategy.

Pre-established Risk Limits Risk criteria is not ad-hoc. The Risk Committee establishes risk guidelines for each manager before it starts trading on our platform.

Regular Review of all Strategies All strategies are reviewed on a regular basis; not just when there are issues. The Risk Committee is constantly aware of the trading positions. It wants to be aware of any potential issues before they develop and work collaboratively with our managers to help them best position their portfolios.

Value-Additive Feedback Because the Risk Committee is comprised of experienced risk managers, we work with our managers to help them structure positions with the most appropriate risk profile. We strive to be collaborative not solely overseers.

Risk Reporting We make our risk analytics available to our investors. We view this as an important part of our ongoing transparency.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

The Typhon DistinctionMarket Coverage Typhon is plugged-in to the universe of emerging traders, and identifies distinctive specialists with defined edges.

Due Diligence Typhon has a rigorous due diligence process to cull the universe of emerging managers before bringing them into Typhon.

Operational Support Typhon provides its managers with best-in-class legal, compliance, accounting and administrative support. This tempers one of the largest risks associated with emerging traders.

Risk Oversight Typhon has an independent, empowered risk management committee that monitors our strategies on a daily basis.

Investor Relations Typhon has well-established relationships across the universe of investors in emerging and tactical traders.

No Additional Fees We work with our managers, not in addition to our managers. Our investors do not incur any fees, unlike with fund-of-funds or consultants.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Typhon Capital Management

Market Coverage

Due Diligence

Operational Support

Risk Oversight

Investor Relations

No Additional

Fees

.

Investor Protection

Commitment

Client Advocacy

Integrity

Typhon protects clients by:

• Advocating for customer protections. Our

CEO co-founded the Commodity

Customer Coalition and represented

approximately 10,000 MF Global

customers to help bring about a 100%

recovery for them, completely pro bono. He

also served on the Board of Directors and

Executive Committee of the National

Futures Association.

• Playing an active role in ensuring that

market participants are properly

represented.

• Ensuring those same ethical standards are

upheld by our managers and staff.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

Typhon’s Divisions

Our strategies are specialized,

modular, and structure agnostic.

Each is available a la carte in

separately managed accounts or in

U.S. or Cayman funds within our

Argos Alternative Funds Platform.

Clients can build their own custom

portfolios, or have us construct one

that provides acceptable risk based

on the demands of the overall

portfolio.

Typhon never charges layered fees,

even for multi-manager products.

A Modular Approach to Allocations

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

leonidasEnergy/Macro

plutusGrain

vulcan Metals

proteusVolatility

chironCurrency

helios Deutsche

stoicRules-Based

zephyrusLivestock

.

Typhon Organization

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

James KoutoulasChief Executive Officer

Operations and Compliance

Diana RydbeckManaging Director

Alex KaraDirector of Operations

Due Diligence and Risk

David KlusendorfChief Investment Officer

Portfolio Management

Agricultural

Jerod LemanPortfolio Manager

Nick NickolsPortfolio Manager

Metals

James Gallo

Portfolio Manager

Anthony Cicileo

Senior Trader

Ed Smith

Senior Trader

Crypto, Energy, Macro

George Michalopoulos

Portfolio Manager

Stoic Rules-Based

Alex GreenPortfolio Manager

SystematicCurrency

Simon HarrisPortfolio Manager

Luca BonoCurrency Strategist

James MitchellSenior Trader

Nicholas BloomPortfolio Manager

SystematicStock Index

Hubert Van den Bergh

Portfolio Manager

Damian Taylor

Portfolio Manager

SystematicVolatility

Matthew Thompson

Portfolio Manager

Michael Thompson

Portfolio Manager

Business Development

Robin Ravel Director

Ernst Kosower Director

.

Strategies at a Glance

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Please see each strategy's one-page performance summary and offering materials for detailed information about the above

calculations. Strategies with less than 12 months track record do not have annualized return statistics.

Our Argos Alternative Funds Platform allows investors to access Typhon’s unique tactical trading

strategies with low minimum investment sizes within pooled, limited liability structures in either the

U.S. or Cayman Islands. Investors may invest in any individual strategy independently, or create

custom portfolios. Argos utilizes top service providers such as BMO for custody, Deloitte for

audit, Foley & Lardner for legal, and NAV Consulting for administration.

Our Argos Alternative Funds Platform

trade

generation

sharpe

ratio

annualized

return

leonidas Cryptocurrency Multi-Strategy

leonidas Macro Multi-Strategy

proteus Dynamic ETP Hybrid 0.8 15.3%

stoic Rules-Based Strategies Systematic 1.0 29.2%

vulcan Metals Discretionary 2.5 17.8%

vulcan Metals SP Discretionary 2.4 17.1%

.

Strategies at a Glance

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Please see each strategy's one-page performance summary and disclosure document for detailed information about the above calculations. Futures trading is inherently risky and past

performance is not necessarily indicative of future returns. Typhon Capital Management only provides services for Qualified Eligible Participants and non-US Investors. Strategies with less

than 12 months track record do not have annualized return statistics.

Separately Managed Accounts

Typhon strives to offer sophisticated clients maximum flexibility in structuring its strategies.

All of our futures-based strategies are available in separately managed accounts with daily

liquidity, position-level transparency, cross-margining and choice of virtually any clearing

broker which accepts give-ups.

trade

generation

sharpe

ratio

annualized

return

notional

funding

available

chiron Currency Systematic 0.5 2.5% 5:1

helios Deutsche Systematic 0.9 7.5% 4:1

leonidas Cryptocurrency Quantitative 1:1

leonidas Energy Discretionary 5:1

proteus Dynamic Volatility Systematic 0.4 3.1% 5:1

plutus Grain Discretionary 0.8 6.9% 5:1

vulcan Metals Discretionary 2.3 15.5% 5:1

zephyrus Livestock Discretionary 1.5 45.7% 3:1

trade

generation

sharpe

ratio

annualized

return

notional

funding

available

chiron Currency Systematic 0.5 2.5% 5:1

helios Deutsche Systematic 0.9 7.5% 4:1

leonidas Cryptocurrency Quantitative 1:1

leonidas Energy Discretionary 5:1

proteus Dynamic Volatility Systematic 0.4 3.1% 5:1

plutus Grain Discretionary 0.8 6.9% 5:1

vulcan Metals Discretionary 2.3 15.5% 5:1

zephyrus Livestock Discretionary 1.5 45.7% 3:1

METALSvulcan METALS GROUP

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

vulcan Metals Group

Strategy at a Glance

The Vulcan Metals Group trades metals on a discretionary basis and is comprised of James Gallo, Edward Smith, and

Anthony Cicileo. Utilizing a global network of information on mining, usage, historical movements, and need, and

proprietary research, the methodology is exacting yet flexible enough to capitalize on daily market irregularities. Vulcan

trades a variety of metals including copper, gold, silver, platinum and palladium. Vulcan primarily engages in relative value

futures spreads, roll arbitrage, LME/COMEX arbitrage, and flow trading. The full Vulcan methodology which includes

additional strategies for futures market making and physical metals warrants is available in US and Cayman funds on our

Argos Alternative Funds platform.

AUM $39.4M

Minimum Investment US $100k fund, $10M SMA

Management Fee 2%

Incentive Allocation 20%

Max Notional Funding 5:1

Max Margin : Equity 10.0%

Liquidity SMA Daily

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

vulcan Metals Fund

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Performance prior to June 2016 is proprietary pro forma for 2/20 fees, at a 2.25M nominal account size, and an estimated $1,000 per month in extra commissions to

reflect non-member rates by NAV Consulting, Inc. Performance from June 2016 through February 2017 is a composite of client managed accounts net of actual fees,

and the performance of the Vulcan Metals Fund net of all fees and expenses thereafter. Please see offering materials for more notes and risk factors.

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 0.13% 1.63% 1.76%

2017 (0.79%) 0.56% 0.84% 2.34% 0.37% 0.73% 0.16% 0.48% 0.80% 1.53% 0.52% 1.49% 9.38%

2016 2.04% 0.31% (1.81%) 2.37% 2.70% 0.31% 0.43% 0.28% 0.14% 0.06% (0.50%) (1.12%) 5.23%

2015 1.60% 5.23% 1.35% 0.29% 1.54% 3.50% 2.54% 5.25% 0.42% (0.49%) 5.54% 0.32% 30.41%

2014 1.61% 8.29% 0.89% 4.07% 1.34% 0.08% 0.65% 2.10% 0.84% 2.42% 2.40% 0.39% 27.84%

2013 1.04% 0.34% 1.82% 2.40% (0.06%) 3.28% 1.03% 1.62% 1.08% (0.60%) 2.56% 0.67% 16.20%

2012 2.47% 0.19% 1.43% 7.93% 0.37% 2.92% 4.23% 2.97% 2.64% 1.24% (4.44%) (0.47%) 23.15%

2011 1.01% 0.33% 1.34%

Monthly Net Performance

Growth of $1,000

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 0.13% 1.63% 0.85% 2.63%

2017 (0.79%) 0.56% 0.84% 2.34% 0.37% 0.73% 0.16% 0.48% 0.80% 1.53% 0.52% 1.49% 9.38%

2016 2.04% 0.31% (1.81%) 2.37% 2.70% 0.31% 0.43% 0.28% 0.14% 0.06% (0.50%) (1.12%) 5.23%

2015 1.60% 5.23% 1.35% 0.29% 1.54% 3.50% 2.54% 5.25% 0.42% (0.49%) 5.54% 0.32% 30.41%

2014 1.61% 8.29% 0.89% 4.07% 1.34% 0.08% 0.65% 2.10% 0.84% 2.42% 2.40% 0.39% 27.84%

2013 1.04% 0.34% 1.82% 2.40% (0.06%) 3.28% 1.03% 1.62% 1.08% (0.60%) 2.56% 0.67% 16.20%

2012 2.47% 0.19% 1.43% 7.93% 0.37% 2.92% 4.23% 2.97% 2.64% 1.24% (4.44%) (0.47%) 23.15%

2011 1.01% 0.33% 1.34%

Monthly Net Performance

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

$0

$500

$1,000

$1,500

$2,000

$2,500

11/11 11/12 11/13 11/14 11/15 11/16 11/17

Vulcan Fund Monthly Return Vulcan FundBarclayHedge CTA Index HFRX COM

Vulcan Fund BH1 HFR COM 1

Annualized Return 17.77% 0.71% (1.90%)

Max Drawdown (4.91%) (7.38%) (11.98%)

Largest Gain 8.29% 3.07% 3.80%

Largest Loss (4.44%) (2.21%) (4.86%)

Sharpe Ratio 2.51 0.19 (0.39)

Sortino Ratio 2.36 0.08 (0.15)

Volatility (σ) 6.64% 4.14% 4.67%

Correlation (r) 0.20 0.09

Selected Statistics

.

vulcan Metals Strategy

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Performance prior to June 2016 is proprietary pro forma for 2/20 fees, at a 2.25M nominal account size, and an estimated $1,000 per month in extra commissions to

reflect non-member rates by NAV Consulting, Inc. Performance thereafter is a composite of client accounts net of actual fees. For more information on the HFRX

Commodity and BarclayHedge CTA indices, please see hfr.com and barclayhedge.com, respectively. Please see offering materials for more notes and risk factors.

Growth of $1,000

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

$0

$500

$1,000

$1,500

$2,000

$2,500

11/11 11/12 11/13 11/14 11/15 11/16 11/17

Vulcan Monthly Return Vulcan

BarclayHedge CTA Index HFRX COM

Vulcan BH1 HFRX COM 1

Margin:Equity Avg, Max 2.5%, 10%

Annualized Return 15.49% 0.71% (1.90%)

Max Drawdown (4.91%) (7.38%) (11.98%)

Largest Gain 8.29% 3.07% 3.80%

Largest Loss (4.44%) (2.21%) (4.86%)

Sharpe Ratio 2.30 0.19 (0.39)

Sortino Ratio 2.19 0.08 (0.15)

Volatility (σ) 6.74% 4.14% 4.67%

Correlation (r) 0.19 0.13

Selected Statistics

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 0.71% 0.32% (0.02%) 1.01%

2017 (0.77%) 0.58% 1.51% 0.37% 0.02% (0.23%) 0.64% 0.10% 0.20% (0.08%) 0.30% 0.15% 2.79%

2016 2.04% 0.31% (1.81%) 2.37% 2.70% 0.36% 0.45% 0.28% 0.14% 0.15% (0.47%) (1.10%) 5.42%

2015 1.60% 5.23% 1.35% 0.29% 1.54% 3.50% 2.54% 5.25% 0.42% (0.49%) 5.54% 0.32% 27.09%

2014 1.61% 8.29% 0.89% 4.07% 1.34% 0.08% 0.65% 2.10% 0.84% 2.42% 2.40% 0.39% 25.08%

2013 1.04% 0.34% 1.82% 2.40% (0.06%) 3.28% 1.03% 1.62% 1.08% (0.60%) 2.56% 0.67% 15.18%

2012 2.47% 0.19% 1.43% 7.93% 0.37% 2.92% 4.23% 2.97% 2.64% 1.24% (4.44%) (0.47%) 21.48%

2011 1.01% 0.33% 1.34%

Monthly Net Performance

.

vulcan Strategy Focus

Vulcan trades a variety of metals including copper, gold, silver, platinum and palladium. Vulcan adapts to changing market

conditions, the strategy employs intra-commodity spreads to yield additional low risk returns. The majority of Vulcan’s

trades are relative value future spreads, but it also utilizes some outrights, options-on-futures, NYMEX/LME arbitrage,

and, in our funds, sub-strategies involving physical delivery of warehouse receipts.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Silver

Copper

Gold Palladium

Platinum

.

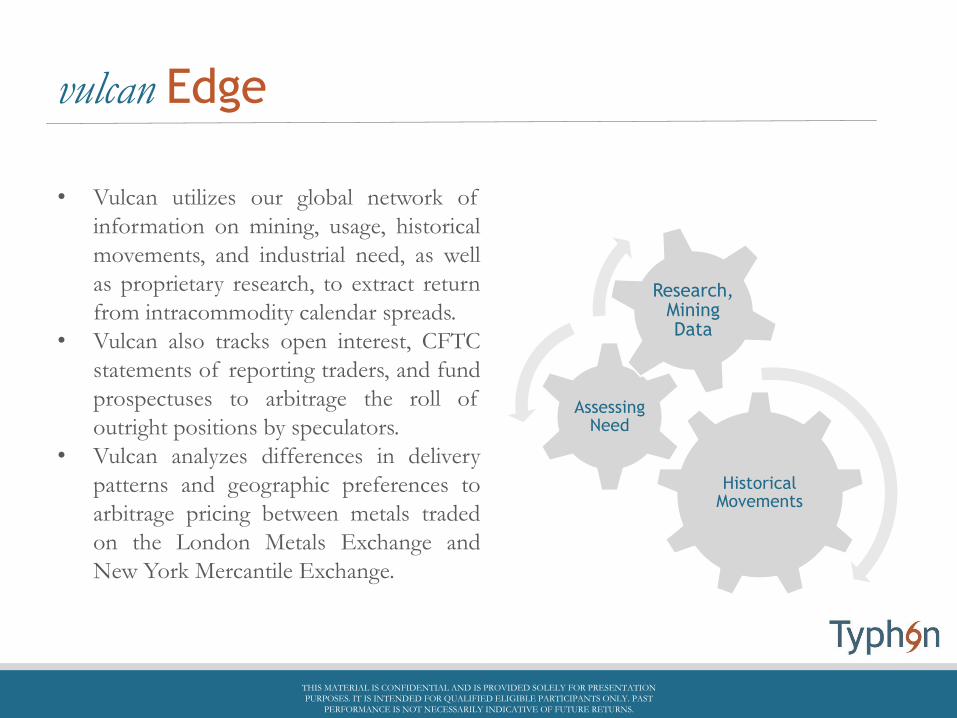

vulcan Edge

Historical Movements

Assessing Need

Research, Mining Data

• Vulcan utilizes our global network of

information on mining, usage, historical

movements, and industrial need, as well

as proprietary research, to extract return

from intracommodity calendar spreads.

• Vulcan also tracks open interest, CFTC

statements of reporting traders, and fund

prospectuses to arbitrage the roll of

outright positions by speculators.

• Vulcan analyzes differences in delivery

patterns and geographic preferences to

arbitrage pricing between metals traded

on the London Metals Exchange and

New York Mercantile Exchange.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

vulcan Risk Management

Protection is a key element in generating

returns - robust risk management is at the

core of this protection. We believe that

associated costs are more than

compensated for in times of market stress,

and the strategy generates strong positive

returns in rising markets.

Risk is actively managed through strict risk

budget limits at portfolio and individual

metals levels, with drawdown limits set and

enforced by Typhon’s Independent Risk

Committee.

Vulcan’s portfolio managers have traded

this strategy for between 20 and 30 years

each with their own money and all have

skin in the game.

Budget Limits

Positive Returns

Robust Risk Management

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

AGRICULTUREplutus GRAIN STRATEGY

zephyrus LIVESTOCK STRATEGY

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

plutus Grain Strategy

Strategy at a Glance

The Plutus Grain Strategy is a discretionary, diversified grain strategy designed to capture returns from the grain

markets with a low correlation to traditional assets. This methodology prioritizes capital preservation and seeks to

provide returns at a low level of volatility when compared to most other grain strategies.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

AUM $19.25mm

Minimum Investment US $250k for SMA

Management Fee 2%

Incentive Allocation 20%

Max Notional Funding 5 : 1

Max Margin : Equity 5%

Liquidity SMA Daily

.

plutus Grain Strategy

Performance prior to September 2010 is proprietary pro forma for 2/20 fees and a composite of client net returns thereafter. For more information on the

BarclayHedge CTA and HFR Commodity indices, please see barclayhedge.com and HFR.com, respectively. Please see offering materials for more notes and risk

factors.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Growth of $1,000 Plutus BH1 HFR COM1

Annualized Return 6.94% 1.43% (2.18%)

Max Margin to Equity 5.00%

Max Drawdown (10.34%) (10.74%) (22.41%)

Largest Gain 11.74% 3.54% 3.80%

Largest Loss (7.66%) (2.94%) (4.86%)

Sharpe Ratio 0.76 0.32 (0.41)

Sortino Ratio 0.35 0.14 (0.16)

Volatility (σ) 9.16% 4.75% 5.07%

Correlation (r) -0.21% -5.18%

Selected Statistics

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 (0.17%) (0.51%) 2.22% 1.54%

2017 (1.13%) 1.03% 0.77% 1.58% 0.73% 4.41% (2.28%) (2.80%) 0.65% 0.50% 0.04% 0.30% 3.80%

2016 0.65% 0.40% 0.50% (5.18%) (1.23%) 0.35% 1.09% (1.98%) 0.13% (0.29%) 0.13% 0.71% (4.72%)

2015 0.81% (0.46%) 2.20% 0.55% 0.92% (1.34%) 3.49% 0.79% (0.76%) 0.16% 0.41% 0.35% 7.12%

2014 (0.54%) (4.16%) (1.55%) (1.73%) 1.46% 3.42% 1.96% 0.51% 0.17% (5.16%) 2.25% 0.96% (2.41%)

2013 (0.03%) 1.10% 0.52% 0.36% 1.49% (0.56%) 0.97% 0.13% 0.59% (0.05%) (0.16%) 0.88% 5.24%

2012 1.83% (0.57%) (3.75%) (0.86%) 0.93% 0.02% 2.01% 1.52% 0.06% 1.33% (0.59%) 0.08% 2.01%

2011 0.01% 0.14% 2.56% 2.32% 1.57% 2.66% 0.90% (1.81%) 2.22% 1.18% 1.13% (0.85%) 12.03%

2010 11.74% (0.78%) 0.96% 6.14% (1.53%) 7.32% (6.21%) 1.79% 1.97% 2.26% 1.02% 0.70% 25.38%

2009 1.32% (7.66%) (2.68%) 1.43% 6.01% 7.04% (4.30%) 3.49% 1.42% 4.46% 1.31% (7.04%) 4.81%

2008 8.05% 4.05% 0.09% 0.76% 0.57% (0.03%) (0.48%) 1.55% 0.07% 14.63%

Monthly Net Performance

.

plutus Approach

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

The Plutus Grain Strategy is a

discretionary strategy based on a

combination of supply/demand

fundamentals and technical analysis

which attempts to define trends and/or

changes in trends in various agricultural

commodity markets. Fundamental

analysis incorporates factors such as

production, domestic and foreign

demand, storage cost and availability,

governmental issues, and weather, both

in the United States and around the

world. Plutus primarily trades

agricultural futures spreads including

but not limited to corn, soybeans,

wheat, soybean meal, soy oil, oats, and

rice.

production

foreign demand

domestic demand

availability

government issues

weather

storage cost

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

plutus Risk Management

The Plutus Grain Strategy primarily

expresses trading views through

spreads in order to reduce volatility.

Approximately 90% of Plutus’

positions utilize futures spreads,

some of which are described in the

diagram on the right.

Plutus may take positions in the

futures and or options markets when

market conditions meet our risk

parameters. The strategy generally

maintains a sub-5% margin-to-equity

ratio, and never exceeds 10%.

Plutus does not sell naked options.

Intra-commodity spreads between calendar months,

example: December corn vs. March corn

Inter-commodity spreads between

different commodities,

example: December soy oil vs. December

soybean meal

plutus

Inter-market spreads between markets, example: Chicago

December wheat vs. Kansas City

December wheat

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

plutus Edge

Information Flow

The portfolio manager for the strategies remains active in the cash markets, structuring futures and swap hedges for many pure users and producers of agricultural commodities. This gives us a significant information advantage and insight into fundamentals ahead of the broader market.

Risk Management

Typhon strives to provide a low-volatility return profile across its strategies. Unlike most fundamental ag programs, plutus maintains low margin-to-equity usage and defined stops and profit targets on every trade. Both programs use technicalsto guide entries and exits. Frequently positions are developed prior to markets catalyzing execution.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

zephyrus Livestock Strategy

Strategy at a Glance

The Zephyrus Livestock Strategy is a discretionary livestock strategy designed to capture returns from the

hog and cattle markets with a low correlation to traditional assets. This methodology incorporates both

fundamental data and technical analysis and prioritizes capital preservation and seeks to provide returns at

a moderate level of volatility.

AUM 250k

Minimum Investment U.S. 250k

Management Fee 0%

Incentive Allocation 30%

Liquidity Daily

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

zephyrus Livestock Strategy

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Performance figures are a composite of live returns net of all expenses with fees pro forma to 0/30. For more information on the BarclayHedge CTA and HFR

Commodity indices, please see barclayhedge.com and HFR.com, respectively. Please see offering materials for more notes and risk factors.

Growth of $1,000

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 6.24% 1.92% 2.91% 11.07%

2017 5.60% 6.37% (6.53%) 7.47% 7.62% 26.10% 5.78% (6.59%) 4.90% (13.97%) 8.24% 1.06% 46.05%

Monthly Net Performance

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

$0

$500

$1,000

$1,500

$2,000

1/17 1/18

Zephyrus Monthly Return Zephyrus BarclayHedge CTA Index HFRX COM

Zephyrus BH1 HFR COM 1

Annualized Return 45.70% 2.12% (2.87%)

Max Margin to Equity 25%

Max Drawdown (15.66%) (1.68%) (5.15%)

Largest Gain 26.10% 1.92% 3.80%

Largest Loss (13.97%) (1.03%) (4.86%)

Sharpe Ratio 1.48 0.80 (0.45)

Sortino Ratio 0.80 0.44 (0.18)

Volatility (σ) 30.82% 2.67% 6.03%

Correlation (r) -56.98% 20.90%

Selected Statistics

.

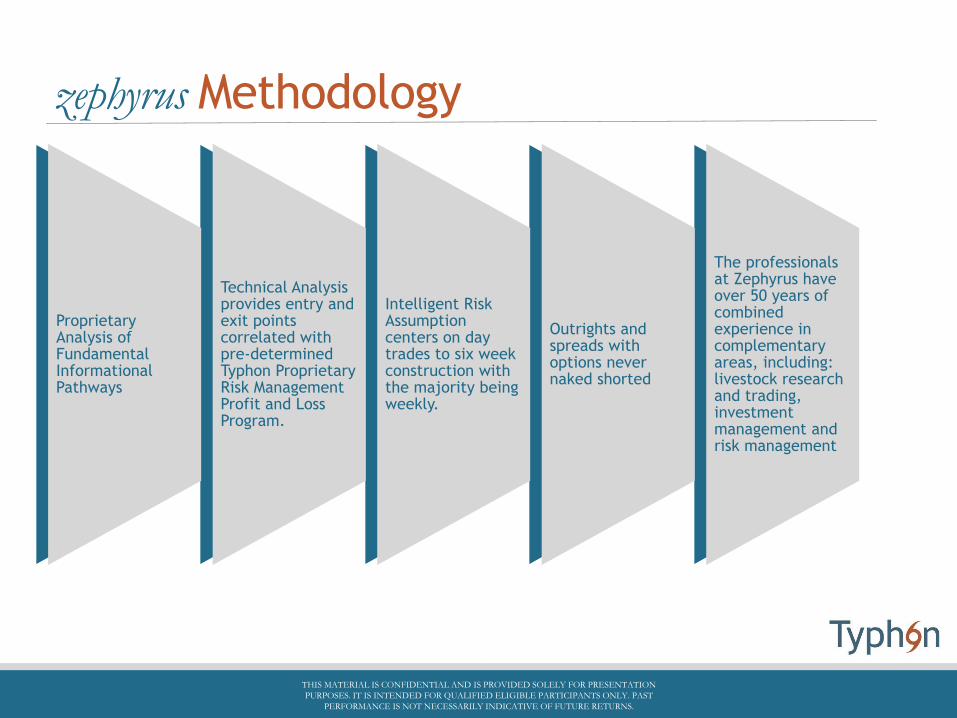

Proprietary Analysis of Fundamental Informational Pathways

Technical Analysis provides entry and exit points correlated with pre-determined Typhon Proprietary Risk Management Profit and Loss Program.

Intelligent Risk Assumption centers on day trades to six week construction with the majority being weekly.

Outrights and spreads with options never naked shorted

The professionals at Zephyrus have over 50 years of combined experience in complementary areas, including: livestock research and trading, investment management and risk management

zephyrus Methodology

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Proprietary Analysis of Fundamental Informational Pathways

Technical Analysis provides entry and exit points correlated with pre-determined Typhon Proprietary Risk Management Profit and Loss Program.

Intelligent Risk Assumption centers on day trades to six week construction with the majority being weekly.

Outrights and spreads with options never naked shorted

The professionals at Zephyrus have over 50 years of combined experience in complementary areas, including: livestock research and trading, investment management and risk management

.

zephyrus Summary

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Fundamental analysis incorporates factors such as production,

domestic and foreign demand, storage cost

and availability, governmental issues, and weather, both in the United States and

around the world.

Zephyrus trades are structured with

quantitative reasoning using the most appropriate

instruments, evaluating risk and

reward prior to execution

Zephyrus puts fundamental

information into analytical context with a structured approach to monitoring market

extremes

Typhon Capital provides institutional-caliber operations and risk

management capabilities

CRYPTOCURRENCYleondias CRYPTOCURRENCY GROUP

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

leonidas Crypto Market Opportunity

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

While cryptocurrency is incredibly risky and volatile, it has enabled some market participants to

generate spectacular returns to date, Mr. Michalopoulos believes much of the opportunity lays ahead.

“As with any new regime-changing technology in its early days, there is a lot of confusion as to what

the technology actually does, how much of it is hype, how much is real, and how to trade something

as volatile as it is, responsibly.

That confusion means there is opportunity. Experience trading crypto measured in years when

others measure it in months, is an advantage. Intimate familiarity with using the technology and

knowing its limitations is an advantage. Years of trading experience and risk management in yet

another volatile commodity – oil – is another advantage. Together it’s a unique combination of

advantages in a market rife with opportunities and risks.”

We recommend that only clients with very high risk tolerance engage in cryptocurrency

speculation, as doing so they risk the complete loss of principal while investing directly in

cryptocurrency or via a limited liability fund vehicle, and risk a loss greater than their

principal when investing in cryptocurrency futures or a managed account utilizing

cryptocurrency futures.

.

leonidas Crypto Market Opportunity

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Data courtesy of coinmarketcap.com and is as of 11/21/17

.

Why Us?

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

With the euphoria surrounding cryptocurrencies, there has been a proliferation of funds starting

to service it. Many of their principals have never traded other asset classes, down markets, or

managed a regulated fund with proper internal controls. Typhon and Leonidas, on the other hand,

have an incredible amount of experience in the space:

• Leonidas’s Head Portfolio Manager was a senior energy derivatives trader at Citadel and has

been trading crypto using institutional strategies since 2012

• Typhon has been managing client assets in commodities since 2008, with independent risk

management resulting in low volatility return streams within volatile markets, and proper

internal controls

• Typhon’s CEO has programmed public key encryption software since 1995, began his trading

career with technology stocks in a similar environment to today’s crypto scene, and is a

vanguard of investor protection, recovering $6.7B for MF Global fraud victims, pro bono. He

was the youngest person elected to the Board and Executive Committee of the regulator for

derivatives and crypto.

.

leonidas Cryptocurrency Program

Strategy at a Glance

The Leonidas Cryptocurrency Program is managed by George Michalopoulos and exclusively trades

exchange-cleared derivatives, such as futures on cryptocurrencies such as Bitcoin as they become available.

The strategy is short-term quantitative in nature. The strategy is available in managed accounts only and

may also trade options on cryptocurrencies futures should they become available.

AUM 250k

Minimum Investment US 250K

Management Fee 0% (until Q2 2018, then 2%)

Incentive Allocation 20%

Max Notional Funding 2:1

Max Margin : Equity 40.0%

Liquidity Daily

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

Performance is live performance of a managed account running the program net of commission and pro forma for 2/20, and is not automatically compounded. The program

began within the Leonidas Macro Fund in December 2017. That account was closed 12/31/2017 and a new managed account was opened within the Leonidas

Cryptocurrency Fund in January 2018. YTD returns are calculated for capital invested from January 1 and do not reflect compounding. Actual returns may differ from

reported results due to differences in contribution dates, commissions, and fee structures.1-Any indices and other financial benchmarks shown are provided for illustrative

purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Data is of date of publication and may be a MTD

estimate. For more information regarding the indices included herein, see barclayhedge.com and gemini.com. Please see offering materials for more notes and risk factors.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

leonidas Cryptocurrency Program

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 1.44% 3.82% (1.59%) 3.64%

2017 0.68% 0.68%

Monthly Net Performance

.

leonidas Cryptocurrency Fund

Strategy at a Glance

The Leonidas Cryptocurrency Fund is managed by George Michalopoulos and trades a basket of

cryptocurrencies such as Bitcoin and Ether, as well as exchange traded derivatives on cryptocurrencies,

and may participate in initial coin offerings and trade those coins in secondary markets. The fund uses a

blend of discretionary algorithmic strategies. The Fund currently uses Bittrex, Gemini, and Phillip

Securities as its custodians.

Minimum Investment US $550k

Management Fee 0% (until Q2 2018, then 2%)

Incentive Allocation 20%

Liquidity Quarterly

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

leonidas Cryptocurrency Fund

Performance is of the Leonidas Cryptocurrency Fund is prepared by NAV Consulting, Inc., is net of all fees and expenses, and compounded monthly. Please see offering

materials for more notes and risk factors.

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 (8.20%) (1.22%) (14.36%) (22.34%)

Monthly Net Performance

.

leonidas Cryptocurrency Index

Strategy at a Glance

The Leonidas Cryptocurrency Fund is managed by George Michalopoulos and will be a long-only, passive,

0 performance fee product available for investors looking for smart beta in the space, and also available on

our Argos Alternative Funds Platform. The Fund will use Gemini and Kingdom Trust as its initial

custodians.

AUM Pre-Launch

Minimum Investment US $100k

Management Fee 3%

Incentive Allocation 0%

Liquidity Quarterly

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

leonidas Cryptocurrency

The Leonidas Cryptocurrency Program launched December 10th, 2017 and the Fund launched January, 2018 under lead

portfolio manager George Michalopoulos. The fund trades Bitcoin (BTC), Ethereum (ETH), and other vetted

cryptocurrencies such as Monero (XMR), Zcash (ZEC), Ripple (XRP) and Dash (DASH), as well as CME and CBOE

Futures. The SMA strategy is futures-only currently, but may add options-on-futures as they become available. George

has been trading cryptocurrencies since 2012, and commodities since 2006 when he joined Citadel and eventually

became sole PM of the crude oil options business. The Index is pending launch. The Leonidas Cryptocurrency Group

has three approaches to the sector:

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

discretionary strategy based on fundamental analysis

algorithmic strategies to capitalize on the extreme volatility in the asset class

passive, long-only indexing approach

Management Fee

Only Product

.

Technical Analysis provides entry and exit points correlated with pre-determined Typhon Proprietary Risk Management Profit and Loss Program.

Intelligent Risk Assumption centers on day trades to six week construction with the majority being weekly.

Outrights and spreads with options never naked shorted

The professionals at Zephyrus have over 50 years of combined experience in complementary areas, including: livestock research and trading, investment management and risk management

leonidas Methodology

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Limit investing universe by screening coins for integrity

Assess coin supply and demand. Make relative and tradeable statements about each

Enter and exit based on changing S&D dynamics

Maintain long bias while being prepared to cut risk dramatically.

.

leonidas Cryptocurrency Exchange FocusLeonidas only invests with established cryptocurrency platforms with credible management teams andproper governance structures. Regulated, US-based Exchanges are a cornerstone of the trading strategies.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Established Platforms

InsuredExchange Traded

DerivativesGovernance

.

leonidas Coin Pair Example

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Ethereum (ETH)

Bitcoin (BTC)

Analysis uses proprietary

quantitative relationships

between coin pairs and

qualitative assessments about

integrity and adoptions

potential.

.

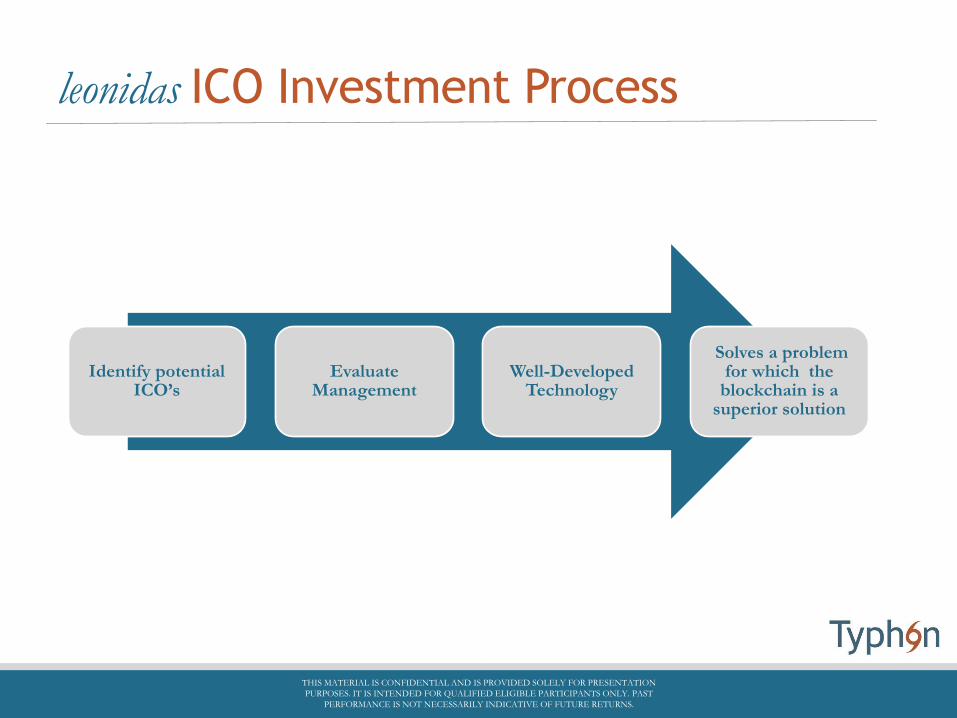

leonidas ICO Investment Process

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Identify potential ICO’s

Evaluate Management

Well-Developed Technology

Solves a problem for which the

blockchain is a superior solution

.

leonidas Multiple Approaches

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Mr. Michalopoulos has formulated three main strategies since starting to trade

cryptocurrencies in 2012.

His first approach uses a discretionary strategy based on fundamental analysis. The

analysis uses relationships between coin pairs and their corresponding supply and

demand.

His second approach uses algorithmic strategies to capitalize on the extreme volatility

in the asset class. Mr. Michalopoulos sees this as a rare window of opportunity as

barriers to entry are still comparatively low, “but won’t remain that way for long.”

His third approach is a passive, long-only indexing approach. It is outside of the scope

of this fee structure, but is available for interested investors as a management fee only

product.

.

leonidas Risk Management

Protection is a key element in

generating returns - robust risk

management is at the core of this

protection. We believe that

associated costs are more than

compensated for in times of market

stress, and the strategy generates

good positive returns in rising

markets.

Risk is actively managed through

strict risk budget limits at portfolio

and individual metals levels, with

drawdown limits.

Budget Limits

Positive Returns

Robust Risk Management

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

ENERGY/MACROleonidas ENERGY STRATEGY

leonidas MACRO FUND

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

leonidas Energy Strategy

Strategy at a Glance

The Leonidas Energy Strategy is a pure discretionary macro trading strategy managed by George Michalopoulos, who was an energy portfolio

manager for Citadel Investment Group for six years. Mr. Michalopoulos has a unique understanding of global supply and demand dynamics as they

relate to WTI, Brent, and Henry Hub natural gas. Because these are physically-delivered contracts, there arises a unique trading advantage for those

understanding the fundamental dynamics. Often without taking the risk profile of outright positioning (long/short) in the underlying commodity.

This can be expressed in grade differentials, like WTI-BRT, WTI spreads, BRT spreads, and even WTI vs BRT spreads.

AUM $500k

Minimum Investment US $100K Fund, $500k SMA

Management Fee 2%

Incentive Allocation 20%

Max Notional Funding 5 : 1

Max Margin : Equity 10%

Liquidity SMA: Daily, Fund: Monthly

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

leonidas Energy Strategy Returns

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Performance is live performance of an energy-only managed account within the Leonidas Macro Fund, net of commission and pro forma for 2/20, and is not automatically

compounded. For more information on the HFRX Commodity and BarclayHedge CTA indices, please see hfr.com and barclayhedge.com, respectively. Please see offering

materials for more notes and risk factors.

Growth of $1,000

-3%

-2%

-1%

0%

1%

2%

3%

$500

$600

$700

$800

$900

$1,000

$1,100

4/17 10/17

LE Monthly Return Leonidas Energy BarclayHedge CTA Index HFRX COM

Leonidas Energy BH1 HFR COM1

Margin:Equity Avg, Max 2.5%, 10%

Annualized Return

Max Drawdown (3.67%) (1.03%) (5.15%)

Largest Gain 1.53% 1.92% 3.80%

Largest Loss (1.32%) (1.03%) (4.86%)

Sharpe Ratio

Sortino Ratio

Volatility (σ) 2.57% 2.58% 6.79%

Correlation (r) (0.22) (0.62)

Selected Statistics

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 (0.99%) 1.53% (1.32%) (0.80%)

2017 0.22% (0.88%) (0.22%) (0.18%) (0.83%) (0.19%) (0.30%) (0.35%) 0.22% (2.49%)

Monthly Net Performance

.

leonidas Energy Strategy

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

The Leonidas Energy Strategy launched in April 2017 and is managed by George

Michalopoulos. The strategy trades exchange-traded energy contracts and was used

successfully by George at Citadel for 6 years. It is available in Separately Managed Accounts

with a 500k nominal minimum.

The Leonidas Energy Strategy has a unique understanding of global supply and demand

dynamics as they relate to WTI, Brent, and Henry Hub natural gas.

Because these are physically-delivered contracts, there arises a unique trading advantage for

those understanding the fundamental dynamics. Often without taking the risk profile of

outright positioning (long/short) in the underlying commodity. This can be expressed in

grade differentials, like WTI-BRT, WTI spreads, BRT spreads, and even WTI vs BRT

spreads.

energy gasoil

.

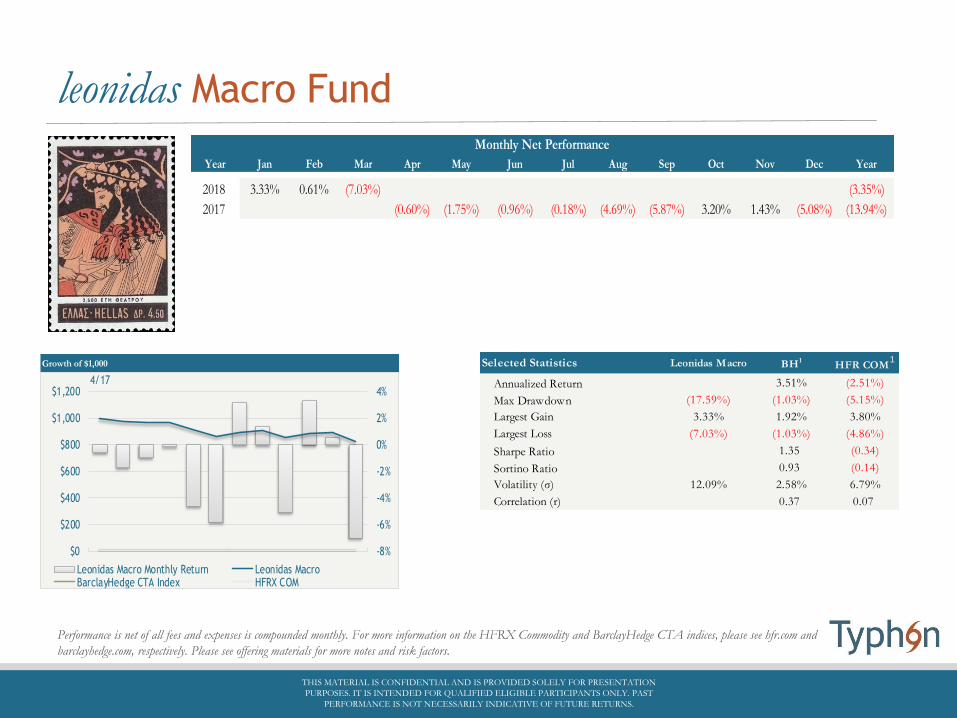

leonidas Macro Fund

Strategy at a Glance

The Leonidas Macro Fund is a purely discretionary global macro strategy managed by George Michalopoulos. Leonidas

analyzes global monetary and fiscal policy, specifically how they change, or how they might change given certain catalysts

such as rate policy meetings, and analyzes a portfolio that is as outcome-agnostic as possible. Leonidas attempts to express

such catalysts through trades constructed with off-setting correlations, while maintaining positive expected value on as many

elements of that portfolio as possible.

AUM $1.4M

Minimum Investment US $100K Fund, $10M SMA

Management Fee 2%

Incentive Allocation 20%

Max Notional Funding 5 : 1

Max Margin : Equity 10%

Liquidity SMA: Daily, Fund: Monthly

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

leonidas Macro Fund

Performance is net of all fees and expenses is compounded monthly. For more information on the HFRX Commodity and BarclayHedge CTA indices, please see hfr.com and

barclayhedge.com, respectively. Please see offering materials for more notes and risk factors.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Growth of $1,000

-8%

-6%

-4%

-2%

0%

2%

4%

$0

$200

$400

$600

$800

$1,000

$1,2004/17

Leonidas Macro Monthly Return Leonidas MacroBarclayHedge CTA Index HFRX COM

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 3.33% 0.61% (7.03%) (3.35%)

2017 (0.60%) (1.75%) (0.96%) (0.18%) (4.69%) (5.87%) 3.20% 1.43% (5.08%) (13.94%)

Monthly Net Performance

Leonidas Macro BH1HFR COM

1

Annualized Return 3.51% (2.51%)

Max Drawdown (17.59%) (1.03%) (5.15%)

Largest Gain 3.33% 1.92% 3.80%

Largest Loss (7.03%) (1.03%) (4.86%)

Sharpe Ratio 1.35 (0.34)

Sortino Ratio 0.93 (0.14)

Volatility (σ) 12.09% 2.58% 6.79%

Correlation (r) 0.37 0.07

Selected Statistics

.

leonidas Macro Fund

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

The Leonidas Macro Fund launched in April 2017 and is managed by George Michalopoulos. The strategy a

purely discretionary global macro strategy. Leonidas analyzes global monetary and fiscal policy, specifically

how they change, or how they might change given certain catalysts such as rate policy meetings, and analyzes a

portfolio that is as outcome-agnostic as possible. Leonidas attempts to express such catalysts through trades

constructed with off-setting correlations, while maintaining positive expected value on as many elements of

that portfolio as possible.

Ste

p 1 Identify

dominant macro trends S

tep

2 Identify central drivers of trends S

tep

3 Identify offsetting risk assets if drivers change

Ste

p 4 Screen

potential offsetting risk assets that have positive expected value in status quo

Ste

p 5 Construct

appropriately risk-manged portfolio to correct size and ratios, such that the desired daily and shock-simulated VAR metrics are within Typhon guidelines

Ste

p 6 Dynamically

adjust ratios and sizing to take advantage of above- and below-trend returns and/or adjust to new market realities and return to step 1

Leonidas Macro Fund Investment Process

Rules-Basedstoic RULES-BASED STRATEGIES FUND

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

stoic Rules-Based Strategies Fund

AUM $3.5M

Minimum Investment U.S. $100k

Management Fee 0%

Incentive Allocation 40%

Liquidity Quarterly

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Strategy at a Glance

The Stoic Rules Based-Strategies Fund combines three components to produce a unique event-driven

fund. Stoic is currently comprised of three sub-strategies: event-driven single name equity options,

comparative single name stocks, and VIX-based derivatives. All components systematically produce

directional biases that the portfolio manager then executes with discretion. No naked options are used.

.

stoic Rules-Based Strategies Fund

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Performance figures prior to January 2018 are a composite of live returns net of all expenses with fees pro forma to 0/40. All performance thereafter is that of the Stoic

Rules-Based Strategies Fund and is calculated net of all expenses, management fees and incentive fees. For more information on the S&P 500 index, please see

standardandpoors.com. Please see offering materials for more notes and risk factors.

Growth of $1,000

-20%

-10%

0%

10%

20%

30%

40%

$0

$500

$1,000

$1,500

$2,000

$2,500

6/14 12/14 6/15 12/15 6/16 12/16 6/17 12/17

Stoic Monthly Return Stoic S&P 500

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 (0.42%) (3.78%) (6.62%) (10.53%)

2017 8.55% 0.49% 11.02% (3.31%) 7.66% (0.15%) 1.84% (10.48%) 15.53% 1.75% 1.33% 3.70% 41.75%

2016 (2.01%) (0.22%) 11.13% (3.63%) 10.67% (0.70%) 6.43% 5.13% (0.79%) (9.21%) 15.29% 7.64% 43.92%

2015 (4.66%) 8.02% (8.82%) 3.07% 33.22% 4.73% (14.42%) 16.52% (1.27%) 1.73% (1.45%) (4.23%) 27.65%

2014 2.26% (5.97%) 4.88% 0.42% 2.53% 5.30% 4.80% 14.58%

Monthly Net Performance

Stoic S&P1

Annualized Return 29.61% 9.16%

Max Drawdown (14.42%) (8.89%)

Largest Gain 33.22% 8.30%

Largest Loss (14.42%) (6.26%)

Sharpe Ratio 1.04 0.93

Sortino Ratio 0.58 0.45

Volatility (σ) 28.49% 10.01%

Correlation (r) 23.72%

Selected Statistics

.

stoic Summary

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Stoic trades rules-based strategies and

are never data mined

2 of the 3 current strategies are event-

driven and trade single name stocks and options. The

3rd strategy trades VIX futures.

The strategies are traded on a

notional basis, with each trade being a pre-determined

percentage of the notional.

Typhon Capital provides

institutional-caliber operations and risk

management capabilities

.

_ _ _ _

stoic Methodology

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

general trading

perspective

back tested for validity, not data-

mined

identify trade entry

and exit

Trades are executed

on a percentage

of notional

basis

.

stoic Methodology

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Every strategy Stoic considers must make sense from a general trading perspective. Potential strategies are

thought of and then back tested for validity, not data-mined. Stoic’s methodology is not based on scanning

price curves or other data sources for predictive patterns. Rules are followed to identify trade entry/exit, and

trades are executed manually. This prevents the portfolio manager from second-guessing the strategy or

becoming married to any trades.

Stoic concurrently trades three rules-based strategies at the present time. These strategies are traded on a

notional basis, with each trade being a certain percentage of the notional value of the fund. Two of the three

current strategies are event-driven and trade single name stocks and options. These two strategies are typically

less than 50% invested on a notional basis, so the fund typically will have a large cash balance. Hold times are

typically one week for the option strategy and typically 1.5 months for the stock strategy. The option strategy is

long only options and the stock strategy is long only stock, so there is no open-ended risk.

The third strategy trades VIX futures. This is a directional strategy driven by the shape of the curve, that can

be long, short, or not invested. This allows the strategy to profit in low vol periods as well as potentially profit

in market downturns when VIX spikes.

Strategies may be added in the future. Each strategy must be profitable on its own, and provide a differentiated

return stream to the other strategies.

Systematic - Quantitativechiron CURRENCY PROGRAM

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

chiron Currency Program

Strategy at a Glance

The Chiron Currency Program is an intraday-only currency overlay that trades G10 currency futures. The

strategy is 100% systematic and acts as a liquidity provider within a clearly defined daily risk budget.

AUM $2mm

Minimum Investment US $250k for SMA

Management Fee 2%

Incentive Allocation 20% Monthly

Max Notional Funding 5 : 1

Max Margin : Equity 0%

Liquidity SMA Daily

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

chiron Currency Program

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Performance from February 2008 to January 2010 was calculated on proprietary performance of the system, pro forma for fees and reflects automatic compounding. Performance

from February 2010 through February 28, 2012 is of the Arktos Currency Program within the Xenfin Diversified Fund, SPC and was audited by Baker Tilly. Performance

thereafter is a composite of client managed accounts managed by Typhon and does not reflect automatic compounding.

Growth of $1,000

-4%

-2%

0%

2%

4%

6%

$0

$500

$1,000

$1,500

2/08 2/10 2/12 2/14 2/16 2/18

Chiron Monthly Return Chiron

Chiron BH1 HFR COM 1

Annualized Return 2.48% 1.89% (1.43%)

Max Margin to Equity

Max Drawdown (7.46%) (10.74%) (21.29%)

Largest Gain 5.35% 5.52% 9.11%

Largest Loss (3.38%) (2.94%) (4.86%)

Sharpe Ratio 0.46 0.40 (0.22)

Sortino Ratio 0.22 0.19 (0.10)

Volatility (σ) 5.20% 5.01% 5.82%

Correlation (r) -1.67% 10.27%

Selected Statistics

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 2.59% 0.04% (1.61%) 1.02%

2017 (0.67%) (0.52%) (0.11%) (0.83%) (0.30%) (0.52%) 0.60% 0.06% 0.16% 0.31% (1.01%) (0.57%) (3.40%)

2016 2.16% 2.82% 0.95% (1.74%) (0.78%) (1.04%) (0.31%) (0.04%) 0.27% 0.76% 2.17% 0.19% 5.41%

2015 0.98% (1.42%) (0.93%) 2.02% (3.27%) 1.51% (1.23%) 1.86% (1.82%) (0.62%) (1.43%) (0.99%) (5.34%)

2014 (0.01%) 1.17% (0.70%) (0.24%) 0.58% (1.04%) 0.28% (0.21%) 0.76% 0.58% 0.89% (0.33%) 1.73%

2013 (0.61%) 1.15% 1.30% (1.96%) 0.14% 2.41% (1.53%) (1.87%) (1.77%) 2.01% (0.27%) 0.60% (0.40%)

2012 (1.26%) 1.06% (1.72%) (0.27%) 1.25% 0.31% (2.43%) (0.16%) 0.48% (0.21%) 0.87% (1.30%) (3.38%)

2011 1.05% 0.63% 1.52% 0.80% 0.18% (2.23%) 0.45% 1.27% (0.40%) 2.38% (0.07%) 0.51% 6.19%

2010 0.33% 0.34% 0.47% (0.31%) 2.05% 1.47% 1.58% 0.03% (0.26%) (0.20%) 0.77% 0.04% 6.46%

2009 4.30% 1.21% (1.15%) (2.47%) 0.75% 5.05% (3.38%) 0.50% 0.11% (0.94%) (2.94%) (0.81%) (0.14%)

2008 0.55% 1.66% 0.52% (0.80%) 2.77% 0.83% 2.41% 3.25% (0.13%) 5.35% (0.16%) 17.32%

Client Monthly Net Performance

.

chiron Philosophy

chiron

USD

EUR

JPY

GBP

CHF

CAD

The Chiron Currency Program was born out of a

need to protect assets when markets are doing poorly

and to generate acceptable returns when core markets

are doing well.

Currency markets were chosen for their liquidity,

trading efficiency, transparency and diversification.

For global investors as a diversifying source, Chiron

mitigates exposure to equity and bond market beta,

providing portfolio protection when necessary.

The investment approach is both pragmatic and

realistic. Chiron strives to both protect capital and

generate returns, while containing costs without

sacrificing framework for the security of the assets

managed.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

chiron Strategy Focus

The Chiron Currency Program is intraday-only and trades G10 currency futures. The strategy is 100%systematic and acts as a liquidity provider within a clearly defined daily risk budget. Chiron dynamicallyapplies risk weightings which reduce exposure in adverse market environments. Chiron trades a diversifiedbasket of currencies based on a quantitatively-determined directional bias with a volatility-based cashmanagement model setting pre-defined entry, exit, and stop levels for each trade within a daily risk budget.

chiron MSCI World

2008 +16.25% vs -42.00%

2011 +6.09% vs -7.60%

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

chiron Edge

Diversification

Downside Protection

Liquidity

Chiron is a concentrated

portfolio for existing CTAs

and currency investors, using

six currency pairs and carefully

controlled managed risk for

downside protection.

Chiron is also a diversifying

source of return for a global

investment portfolios, notably

mitigating exposure to equity

market beta.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

chiron Risk Management

Protection is a key element in

generating returns - robust risk

management is at the core of this

protection. We believe that

associated costs are more than

compensated for in times of

market stress, and the strategy

generates good positive returns in

rising markets.

Risk is actively managed through

strict risk budget limits at portfolio

and individual pair levels, with

drawdown limits.

Budget Limits

All open positions close by 8pm GMT, with no overnight

positions

Robust Risk Management

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

SYSTEMATIC- STOCK INDEXhelios DEUTSCHE PROGRAM

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

helios Deutsche Program

Strategy at a Glance

The Helios Deutsche Program, managed by Damian Taylor and Hubert Van Den Bergh, uses a

proprietary short-term systematic model to trade DAX® futures in an attempt to generate absolute returns

uncorrelated to other asset classes. The DAX®'s volatility and price action have made it an ideal

instrument for expressing the Helios methodology.

AUM $14M

Minimum Investment $500k SMA

Management Fee 2%

Incentive Allocation 20%

Max Notional Funding 4:1

Max Margin : Equity 15.0%

Liquidity SMA Daily

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

.

helios Deutsche Program

THIS MATERIAL IS CONFIDENTIAL AND IS PROVIDED SOLELY FOR PRESENTATION

PURPOSES. IT IS INTENDED FOR QUALIFIED ELIGIBLE PARTICIPANTS ONLY. PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RETURNS.

Prior to October 2015, performance is proprietary pro forma for 2/20, and thereafter, of the McLean Systematic Fund Class D, net of actual fees and has

been audited by a big 4 auditor. For more information about the DAX® and BarclayHedge CTA indices, see https://www.dax-indices.com/ and

barclayhedge.com, respectively. Please see offering materials for more notes and risk factors.

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year

2018 3.37% (1.98%) 3.37% 4.76%

2017 (1.66%) 2.03% (0.25%) 2.84% 0.03% (2.16%) 1.95% (0.88%) 0.52% 0.12% (0.42%) (0.17%) 1.95%

2016 (4.16%) 2.45% (0.41%) 2.28% (4.93%) 4.91% 0.90% 2.85% (1.32%) (1.10%) (1.63%) 2.31% 2.15%

2015 4.31% 2.80% 4.44% (2.84%) (1.01%) (2.06%) 4.10% 2.40% (0.76%) 3.09% 1.09% (2.41%) 13.15%

2014 (0.22%) 1.61% 0.28% 1.42% 0.88% 1.60% (3.09%) 2.93% 2.74% 8.15%

Monthly Net Performance

Growth of $1,000 Helios DAX®1

BH1

Margin:Equity 15%

Annualized Return 7.54% 6.80% 2.08%

Max Drawdown (7.18%) (20.65%) (6.32%)

Largest Gain 4.91% 12.32% 3.07%

Largest Loss (4.93%) (9.28%) (2.14%)

Sharpe Ratio 0.92 0.49 0.51

Sortino Ratio 0.44 0.20 0.24

Volatility (σ) 8.18% 15.87% 4.19%

Correlation (r) 0.38 0.22

Selected Statistics

-6%

-4%

-2%

0%

2%

4%

6%

$0

$500

$1,000

$1,500

4/14 4/15 4/16 4/17

Helios Monthly Return Helios

DAX BarclayHedge CTA Index

.