Embed Size (px)

Citation preview

Yahoo CFO Ken Goldman on deals, driving growth and

getting back to basics

Tech control

Private equity: What the future holds

Social media assisted M&A

Australia: dealmaking down under

Capital InsightsHelping businesses raise, invest, preserve and optimize capital

Q3

2015

All

data

in C

apita

l Ins

ight

s is

cur

rent

at 3

0 A

ugus

t 201

5 un

less

oth

erw

ise

stat

ed©

Kar

l Att

ard

ContributorsCapital Insights would like to thank the following business leaders for their contribution to this issue:

Peter CookPartner, Gilbert + Tobin

Kevin AlbertGlobal Head of Business Development, Pantheon

Neil MacDougallPartner, Silverfleet Capital

Nigel DansonCEO, Interact

Tim CampbellChairman, Urban Age Institute

Antoine DreanFounder, Triago/Palico

Yasser El-AnsaryCEO, AVCAL

Peter EngelkeResident Senior Fellow, Atlantic Council

Dominique GaillardManaging Partner, Ardian

Robin BishopHead of Macquarie Capital, Australia and NZ

Mounir GuenChief Executive and Founder, Mvision

Alexandra Reed LajouxChief Knowledge Officer, NACD

Sven LidénChief Executive & Head of IR, Adveq

Luke McKeeverChairman, Neighbourly

Caroline MurphyDirector, Strategy & M&A, Fremantle Media

Bob MorseCo-founder and CEO, Strattam Capital

Aaron P. RubinPartner, Morrison & Foerster

Lorne SomervillePartner & Head of TMT, CVC Capital Partners

Adam TurtleCo-founder, Rede Partners

David PetrieHead of Corporate Finance, ICA, England & Wales

Alfredo De MassisProfessor, Lancaster University

Rachael BassilPartner, Gilbert + Tobin

David MurrayDirector, Murray Capital

Rod RichardsManaging Partner, Graphite Capital

Simon TomsCorporate Finance Partner, Allen & Overy

Philippa StonePartner, Herbert Smith Freehills

James WilkinsonPartner, Reed Smith

Shaheena Janjuha-JivrajAssociated Professor, Henley Business School

Tony HillDirector, DealNexus, Intralinks

Janos BarberisFounder, FinTech HK

Ken GoldmanCFO, Yahoo

William DoranPartner, Reed Smith

Capital Insights from EY Transaction Advisory Services

For EYMarketing Directors: Antony Jones, Dawn QuinnProgram Directors: Jennifer Compton, Farhan HusainConsultant Sub-Editor: Luke Von Kotze Compliance Editor: Paul Simon Design Consultant: David Hale Digital Innovation Lead: Mark Skarratts Senior Digital Designer: Christophe Menard

For Remark Global Managing Editor: Nick Cheek Editor: Kate Jenkinson Editor for the Americas: Sean Lightbown Head of Design: Jenisa Patel Designer: Vicky Carlin Production Manager: Sarah Drumm EMEA Director: Simon Elliott

Capital Insights is published on behalf of EY by Remark, the publishing and events division of Mergermarket Ltd, 4th Floor, 10 Queen Street Place, London, EC4R 1BE.

www.mergermarketgroup.com/events-publications

EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Transaction Advisory Services How you manage your capital agenda today will define your competitive position tomorrow. We work with clients to create social and economic value by helping them make better, more informed decisions about strategically managing capital and transactions in fast-changing markets. Whether you’re preserving, optimizing, raising or investing capital, EY’s Transaction Advisory Services combine a unique set of skills, insight and experience to deliver focused advice. We help you drive competitive advantage and increased returns through improved decisions across all aspects of your capital agenda.

© 2015 EYGM Limited.

All Rights Reserved.

EYG no. DE0633

ED 1215

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

The opinions of third parties set out in this publication are not necessarily the opinions of the global EY organization or its member firms. Moreover, they should be viewed in the context of the time they were expressed.

capitalinsights.ey.com

Helping businesses raise, invest, preserve and optimize capital

Pres

erving Optimizing

Raising

Investing

For more insights, visit capitalinsights.ey.com, where you can find our latest thought leadership, including our market-leading Capital Confidence Barometer.

Pip McCrostie

Global Vice Chair Transaction Advisory Services, EY If you have any feedback or questions, please email [email protected]

As M&A activity for 2015 looks set to eclipse the previous highs of 2007 and finally break away from the shadow of the global financial crisis, it’s clear that dealmaking as a route to growth is firmly back on the boardroom agenda.

Deal activity is being driven by disruptive forces, triggered by changing consumer behavior, sector convergence and technology — and our view is supported by FremantleMedia Director of Strategy and M&A, Caroline Murphy (page 10).

We see examples across many sectors — the convergence of automotive and tech is not only leading to driverless, but also web-connected cars. In pharma, the discovery of new drugs is accelerated by increased computing power and advanced modeling in medical trials.

As a result, all sectors have re-engaged in M&A and we are seeing an uplift in the value of deals across a broad range of geographies. In addition, there is increasing focus amongst investors on benchmarking growth relative to competitors. In a global economy where growth is still relatively low, M&A is an increasingly attractive option to accelerate strategic objectives, market share and competitor position.

Although the global deal market appears very frothy, there is evidence to counter claims of it overheating. While deal values are nudging record highs, deal volume remains some way off record 2007 levels and bid-premiums are only on a par with the mid-points of previous M&A cycles. This suggests that dealmakers are acting with relative caution, exercising discipline in selecting the right strategic deals at the right price.

Executives are more confident in the global economy, corporate earnings and attractive interest rates. This is fostering the conditions for companies to make bold M&A moves.

I hope you enjoy this issue of Capital Insights, which explores the expectations of a global M&A market in recovery, breaking free from the shadows of crisis.

shadowsOut of the

capitalinsights.ey.com | Issue 14 | Q3 2015 | 3

Capital Insights from EY Transaction Advisory Services

Capital InsightsHelping businesses raise, invest, preserve and optimize capital

Q3

2015

20Yahoo

Features10 Q&A: Caroline Murphy, FremantleMedia International

The M&A Director discusses change, content and challenges in media and entertainment.

14 Lights, camera, transactionAs the border between media and entertainment blurs, what does this mean for deals in the industry?

20 Cover story: Tech controlYahoo CFO Ken Goldman on how he intends to steer the internet giant back to the top.

26 Private equity: facing the futureAs PE houses sit on more dry powder than ever before, what does the future hold?

30 Rules of attractionThe future of PE funding is under question as private equity enjoys a revival.

33 How social media is changing M&AAs social media use shows no sign of slowing, how can businesses use social platforms for deal success?

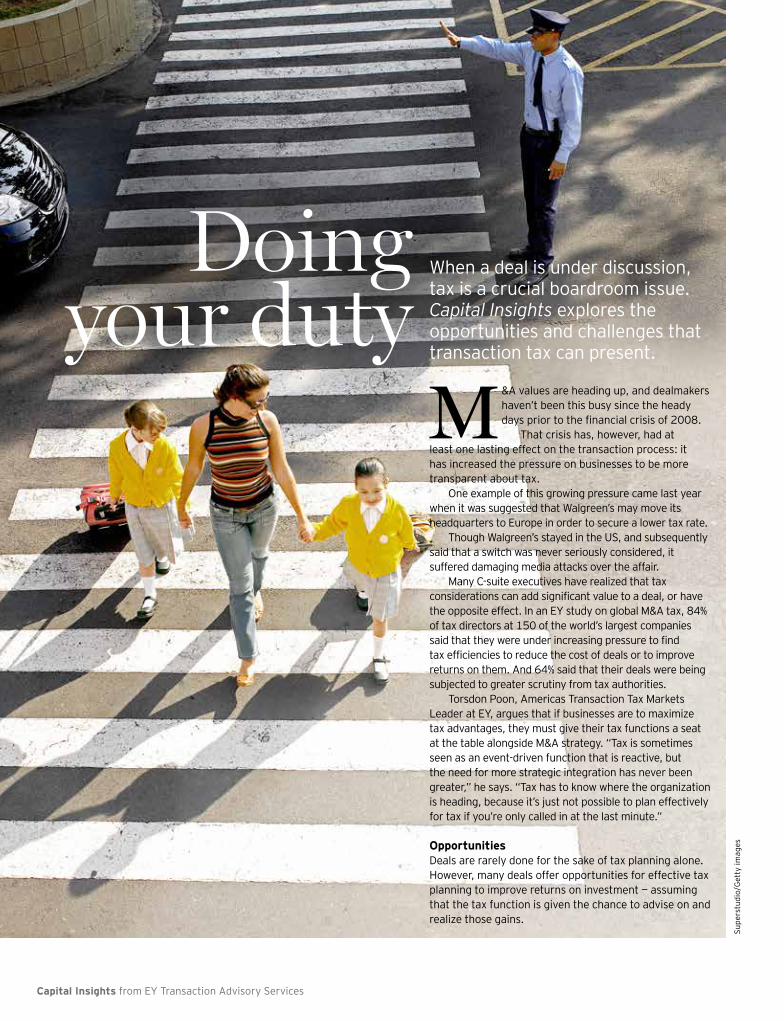

36 Doing your dutyWhat crucial tax considerations need to be made when discussing a deal?

38 Deals down underWith a weak dollar, low interest rates and high asset sales, Australia is ripe for increased M&A activity for the rest of 2015 and beyond.

44 Relative successThere is much that public companies can learn from their family business peers.

48 Capital citiesRapid urbanization presents both opportunities and challenges for dealmakers.

10Entertainment

Frem

antle

Med

ia

© It

o

EY is proud to be the Mergermarket European

Accountancy Firm of the Year

#1 EY — recognized by Mergermarket as top of the European league tables for accountancy advice on transactions in calendar year 2014

© s

ceni

cire

land

.com

/Chr

isto

pher

Hill

Pho

togr

aphi

c/A

lam

y

capitalinsights.ey.com | Issue 14 | Q3 2015 | 5

On the web or on the move?Capital Insights is available online and on your mobile device. To access extra content and download the app, visit capitalinsights.ey.com

Regulars06 HeadlinesThe latest news and trends in the world of capital, and what they could mean for your business.

08 Transaction insightsKey facts and figures from the world of M&A. This issue: half-year 2015 M&A update.

13 EY on the US After a strong first half of 2015 for M&A in the US, H2 could be even more exciting, says EY’s Richard Jeanneret.

19 EY on EMEIAEY’s Andrea Guerzoni explains why 2015 could be a watershed year for M&A in Europe as companies return to the dealmaking table.

43 EY on Asia-PacificEY’s John Hope speaks to colleagues Charlie Alexander and Marc Entwistle, and FinTechHK’s Janos Barneris about the rapid growth of the fintech industry.

50 The last word Guest columnist Alexandra Reed Lajoux discusses the fallen reputation of financial services.

38Australia

The future of private equity 26

John

W B

anag

an/G

etty

imag

es

Chin

a Ph

otos

/Get

ty im

ages

Urbanization48

Capital Insights from EY Transaction Advisory Services

HeadlinesConvergence and consolidation help break TMT recordsThe technology, media and telecommunications (TMT) sector topped the global M&A charts in H1 2015. According to Mergermarket figures, the first half of the year saw 1,322 deals announced, worth US$396.5b and representing 22.8% of the global M&A market. Compared with 2014, value increased by 26.1%, while volume fell by 10.4%.

There were three TMT transactions in the top 10 deals for H1 2015, including Charter Communications’ bid for Time Warner, and British giant BT’s US$19b bid for EE. The main drivers of activity in the TMT sector have been consolidation and cross-sector convergence.

It seems that consolidation will continue, as size matters in this sector. Tom Connolly,

Female-friendly family businessesBy their nature, family businesses often tend to have greater focus on inclusivity and longevity — demonstrated in their higher proportion of female leaders. A survey by EY and Kennesaw State University, Staying Power, found that women make up an average of 22% of the top management team at family businesses, compared with 12.9% at global corporates.

The survey also found that 70% of family businesses are considering a woman for their next CEO. And of those, 30% are strongly considering a woman for the top spot. One woman leading a Fortune 500 family business is Campbell Soup CEO Denise Morrison, who took on the role in 2011. When interviewed in 2014, she said: “Diversity and inclusion is a very important part of building a high-performance culture.”

Social mediaIn a few short years, Facebook, Twitter, YouTube and LinkedIn have become a fundamental part of our lives. And the stats are there to prove it:

2.2b Number of social network users worldwide

304mNumber of monthly active Twitter users

968m The daily active user base of Facebook

300The hours of video uploaded onto YouTube every minute

332mThe number of people on LinkedIn

930The average number of connections for a CEO on LinkedIn

Sources: Wearesocial.com; LinkedIn; Facebook; YouTube; Twitter; Statista

For more on social media and M&A, go to page 33.

EY’s Global Head of Media & Entertainment in Transaction Advisory Services, says: “In an environment where you are trying to negotiate the most favorable deals for your business, being a minor player is a disadvantage.”

In a June survey of TMT companies from law firm Reed Smith, 84% of respondents expected there to be more cross-sector M&A in the next 24 months.

For more on the industry, read our in-depth review of the media and entertainment sector on page 14.

This is a lesson that public, non-family companies can learn from their family business counterparts — particularly at a time when only 3.9% of CEOs across the globe are women. As Carrie Hall, the Americas Family Business Leader at EY, says: “Family businesses may offer a path forward for all businesses seeking to achieve gender parity within their leadership ranks.”

To read more about family businesses, see page 44.t

Mar

tin M

cCar

thy/

iSto

ck b

And

rew

Tot

h/G

etty

imag

es

capitalinsights.ey.com | Issue 14 | Q3 2015 | 7

PE is fighting back As M&A continues to break post-crisis records, private equity (PE) has been conspicuous by its absence. Research from data firm Dealogic reveals that only 5% of deals announced during the first half of this year were PE-backed. This is down from 9% in the same period last year and represents the lowest percentage for 14 years. And figures from Mergermarket for US PE showed that both buyouts and exits were down from a year ago.

Challenges from cash-rich corporates, skyrocketing valuations, more stringent regulations and competition from institutional investors mean that PE firms are having to work harder to get deals across the line. As Jeff Bunder, EY’s Global Private Equity Leader, says: “There’s a competitive aspect to the market, and there’s also a supply-demand imbalance.”

However, the opportunities are there, and the second half of the year may see an upswing in PE activity. Data firm Preqin reported that PE dry powder stood at US$1.3t at the end of H1, the highest amount since records began in 2000.

In addition, a new report from law firm Travers Smith, Calling the shots: The evolution of European PE funding, found that the debt climate is extremely favorable to buyout houses. The survey found that PE sponsors now have a wealth of choice when it comes to financing — indeed, 65% of financing for PE deals in Europe came from alternative debt instruments, such as unitranche and direct lending. With this in mind, PE firms can face the future with renewed optimism. But the overall winners will be those that adapt to this more challenging environment. For more on the future of PE, turn to page 26.

The gloves are offThe hostile deal is back. According to Thomson Reuters’ data, US companies launched 40 hostile campaigns in H1 2015 — double the number for the same period in 2014. The drivers for this activity appear to be consolidation and convergence in sectors such as TMT and pharma and hefty corporate balance sheets. According to Standard & Poor’s, US non-financial companies held US$1.82t in cash and short- and long-term investments at the end of 2014 — 5% up on 2013. Recent unsolicited bids have included drugmaker Shire’s move for biosciences company Baxalta and Mylan’s bid for fellow pharma company Perrigo.

For those companies on the defensive, New York Times Deal Professor Steven Davidoff Solomon has compiled a handy six-point guide on how to “respond to the barbarians at the gate” including “exploring alternatives” and a “just say maybe” defense. You can read the Professor’s full piece by visiting capitalinsights.info and clicking on issue 13.

from top K.N

.V./Shutterstock; Andrew

Burton/Getty im

ages; tamergunal/iStock; TkKurikaw

a/iStock; aluxum/iStock

Dealmaking dynamiteAs H2 2015 commences, boards and investors are surfing a wave of M&A that shows little sign of breaking. According to Mergermarket figures, H1 2015 saw US$1.7t worth of deals, the highest figure for a half-year period since 2007. This figure compares with US$1.52t for the same period last year — a rise of 11.6%. For more on M&A in H1 2015, turn to Transaction insights on page 8.

Megadeals march onDeals valued at over US$10b were the lifeblood of the 2014 M&A revival. Blockbuster deals, including Charter Communications’ US$78b deal for Time Warner, have continued apace during H1 2015, with 28 such deals totaling US$678.1b, according to Mergermarket figures. This is the highest volume and value for megadeals for any H1 on Mergermarket record.

The future is mobile Corporates not harnessing the power of mobile could be left behind. Research from IT advisory company Gartner found that data traffic will reach 52 million terabytes in 2015 — an increase of 59% from 2014. And this is set to triple by 2018. A poll by UK communications watchdog Ofcom discovered that smartphones are the device of choice for 33% of Britons, while 30% prefer laptops.

Offerings up but values downThe first half of 2015 was a mixed bag for IPOs. According to the EY Global IPO Trends report, there were 631 deals globally — a 6% increase on H1 2014. However, total capital raised was 13% lower. Despite this, Maria Pinelli, EY’s Global Vice Chair for Strategic Growth Markets says: “We do not believe the pattern of IPO activity in 2015 reflects a widespread lack of confidence.”

Rising sun, rising M&A Japan has a real yen for cross-border M&A. According to Mergermarket, Japan’s outbound deals for 2015 so far total US$54b, up 63% from the same period in 2014 and surpassing 2014’s total of US$53.3b. The financial services (FS) sector is the most targeted for outbound deals, with 26.8% of the total. Notable deals outside FS include media group Nikkei’s US$1.3b acquisition of the Financial Times.

TransactioninsightsKey facts and figures from the world of M&A. This issue: Half-year update.

Capital Insights from EY Transaction Advisory Services

A fter four consecutive quarters of rising deal volumes, H1 2015 saw deal numbers fall for the first time since H1 2013.

Yet values have continued their upward trajectory, with deal values in H1 2015 worth US$75b more than those in H2 2014. This value growth is fuelling positive predictions for the remainder of the year: “2015 is set to be the best year ever for M&A in terms of value,” says EY’s Deputy Global Vice Chair, Transaction Advisory Services, Steve Krouskos. “The first half of 2015 has seen new deal records, with capacity for even further growth.”

Higher values, in spite of lower volumes, can be attributed to a greater number of megadeals. There were 29 deals worth

more than US$10b in H1 2015, compared to 15 in H2 2014. These included several industry-defining mergers as companies consolidate, such as the US$55.5b Kraft-Heinz deal and Nokia and Alcatel-Lucent’s US$15.2b merger.

Even sector spreadsEight sectors recorded deal values of more than US$100b in H1 2015, compared with seven in H1 2014. Technology saw a huge influx of capital, with more than US$200b in deals in H1 2015 compared with US$121b in H1 2014. Contributing to that total was Avago’s US$35b buyout of Broadcom and Intel’s purchase of Altera for US$15.4b.

Value in Asia and EuropeOn a regional level, Asia and Europe have shown deal value increases in H1 2015, despite falls in overall deal volume. This is particularly true in Asia, where deal value increased by over US$100b from H2 2014 to H1 2015. Much of this

6,740 7,137 6,855 7,7658,464 8,782

7,330

1,028.61,278.1

1,006.11,210.7

1,525.11,691.8 1,767.1

Number of deals Value (US$b)

H1 2012 H2 2012 H1 2013 H2 2013 H1 2014 H2 2014 H1 2015

Global M&A volume and value, H1 2012—H1 2015

Source: Mergermarket

capitalinsights.ey.com | Issue 14 | Q3 2015 | 9

came down to two related deals — the merger of Cheung Kong and Hutchison Whampoa worth US$40.8b and CK Hutchison Holdings, spinning off its property business, Cheung Kong Property Holdings, in a deal worth US$34.9b.

In Europe, deals above US$5b made up 46% of total deal value, amounting to US$211.3b — a 46% year-on-year increase in deals of this type. The UK and Ireland were the top destinations for European M&A, leading in terms of both volume and value, with 23.6% and 52.8%, respectively.

H1 2014 H1 2015

Number of deals Value (US$b)

Business services

Construction

Consumer

Energy, mining & utilities

Financial services

Industrials & chemicals

Pharma, medical & biotech

Real estate

Technology

Telecommunications

982

261

1,025

825

699

1,590

673

159

1,070

88 92

1,022

141

597

1,378

595

554

913

225

958

78.8

63.8

142.3

240.4

113.9

154.4

205.4

74.0

121.1

157.9 176.5

202.4

113.8

211.8

148.5

120.3

308.8

204.1

34.7

97.4

Americas Europe Asia Africa MiddleEast

H12013

H22013

H12014

H22014

H12015

2,413

436.1

1,468

201.0

11116.4

8117.9

826.7

9312.5

9210.3

7411.9

14922.3

13614.3

148

122

22.5

8.0

1,734

304.3

2,038

324.5

1,827

435.5

1,632

245.6

2,844

629.9

2,782

334.7

3,058

306.2

3,275

489.6

3,264

413.0

3,226

704.6

3,240

921.7

2,686

854.5

2,698

458.2

Number of deals Value (US$b)

M&A by sector, H1 2014—H1 2015

M&A volume by geography

Source: MergermarketSour

ce: M

erge

rmar

ket

Capital Insights from EY Transaction Advisory Services

“There is so much changing that sometimes it’s hard to keep up.”As part of Capital Insights’ focus on the media and entertainment sector, Caroline Murphy, FremantleMedia’s Director of Strategy and M&A, talks change, content and challenges.

T he TV industry has changed immeasurably in the past five years. Indeed, it’s possibly a misnomer even to label it TV anymore as so much content is now consumed on tablet, smartphone and laptop.

Meanwhile, the likes of Netflix and Amazon have made the old channel-surfing system seem like a relic from a bygone era.

FremantleMedia has been at the forefront of this televisual revolution with interactive shows such as America’s Got Talent, The X-Factor and the global Idols series. The company was also swift to pick up on the growth in mobile gaming when it purchased Canadian company Ludia five years ago.

In this fevered environment, the role of strategy and M&A director is vital in keeping a step ahead of a media-savvy audience that is hungry for content and new ways to watch it. Caroline Murphy has worked in TV for more than a decade and has been witness to these myriad changes. With the recent upsurge in M&A in the sector and the growing convergence between the televisual and the digital, she explains FremantleMedia’s strategy for staying ahead of the competition.

What is the current state of the media and entertainment M&A landscape?It’s been very busy over the past 12 months. There have been a huge number of big deals going down — people merging or buying

each other. UK media company All3Media was bought by Discovery and Liberty; Time Warner and ITV have been making some big bids. [US giant] Viacom bought [the UK’s] Channel 5, and there

was the merger between [global production houses] Shine, Endemol and Core and more recently Zodiak and Banijay Group. There’s been a lot going on. I think we’re going to see it quieten down a bit now because there’s not really a lot more for the big companies to buy up. Now it’s a matter of letting those deals bed down and seeing how they work out.

What is your acquisition strategy?Our acquisition strategy is quite measured — it could be that a great opportunity comes

Now it’s a matter of letting those deals bed down and seeing how they work out.

FremantleMedia

capitalinsights.ey.com | Issue 14 | Q3 2015 | 11

Investing

Optimizing

up, or it could be that we want to be in a key market where we do not currently have a presence. We will look to grow organically where we can, but where we can’t do it quickly enough, we’ll look at acquisitions. All our acquisitions have to make commercial sense though. Growing our scripted and digital pipeline are priorities for us, so we’re looking at those opportunities at the moment. Recent acquisitions and deals include Miso Film and Corona TV [sister company of Corona Pictures] in scripted and increasing our stake in digital native media company, Divimove.

How do you go about integrating companies?When it comes to integration, I don’t think there is a one-size-fits-all approach. We did a number of deals this year, one of the most recent in February 2015 being with Corona TV. It operates relatively independently, it can create and do all the things that it likes to do, but it gets the benefits of being part of the company’s network — other than that it operates as a standalone company. Similarly, we have a company called Ludia in Canada, which is a mobile gaming company. Ludia is a fantastic business, it has just launched the new game for [summer blockbuster] Jurassic World, which is doing very well. It’s a great business and we help it out in all sorts of ways, but we’re not actively involved in the day-to-day running of the business. Then there are other instances where we buy a company and we fully integrate it. This is something we assess on a case-by-case basis.

Valuations are already high and still rising. What do you predict will be the outcome of all this deal activity? A lot of companies have paid huge sums of money for acquisitions over the past 24 months. I’m a little skeptical as I think people have overpaid for things but time will tell whether that is the case or not.

Once these deals have bedded down, over the next couple of years we’ll see the spinning out of new start-up companies, where you’ll have a whole round of people buying each other once again; it’s very cyclical.

It’s a very exciting time to work in television and there’s a lot of potential growth internationally. TV is a fantastic business to be in and personally really interesting because of the quality content we are producing. It’s also a great time because audience behavior is changing so much. There’s continual innovation about different types of content, presenting on different platforms and different ways of using content. There is so much changing that sometimes it’s hard to keep up.

Jurassic World mobile game, Ludia

Acquitted, new scripted content from FremantleMedia International

Britain’s Got Talent, FremantleMedia International

© Miso Film Norge, TV 2 Norge, SVT, Miso Film

©Ludia 2015

© Splash News 2015

Capital Insights from EY Transaction Advisory Services

What are the greatest changes you have seen in the industry during your career? Digital has been the major change of the last 10 years. Everybody used to watch TV at the same time on a few channels. Then pay TV came along and gave viewers lots more opportunity to watch more content. Digital networks and online platforms have really transformed things. Now people can consume what they want, whenever they want. That has implications for us — you need to make your content accessible everywhere. The fact that people use social media around content, especially the younger audiences, means we need to make sure that people can find our content in places other than TV screens. This is why we have teams of people on Twitter, developing apps, on Facebook, on all social networking sites — you get those real communities around particular shows or particular pieces of content.

What are the challenges that companies in entertainment and media face, and how can they overcome these?I think the big challenge we face, as an indirect result of digital is audience fragmentation. Twenty years ago, you could regularly have 20 million people in the UK watching a TV program. Britain’s Got Talent was a fantastic success this year with over 10 million viewers on a regular basis — but that’s almost unheard of these days.

Audience fragmentation has a number of implications. You need to be where the

audience is. If they’re not watching TV on a Saturday night then you need to be where they will be — whether that’s on YouTube or on Facebook.

Companies these days also need a diverse

content portfolio. While we’ll continue to produce entertainment shows, one area of focus in our new strategy is scripted shows, which have a longer shelf life. A show like Deutschland ’83 [a new cold war drama set among the Pershing Missile Crisis of the 1980s] will still have relevance and resonance for audiences around the world in 10 years’ time.

The industry sees a constant battle between content and distribution. Why is content so important? Content is still king. Distribution is important and innovations in distribution platforms mean that the way people can watch content is ever-changing. But people don’t watch a platform — people get Netflix and Amazon because they’ve got really great content on them. When Netflix started investing in new content like House of Cards and Orange is the New Black; that was really what put it on the map. So, yes, content is absolutely king.

For further insight, please email [email protected]

I think the big challenge we face, as an indirect result of digital is audience fragmentation.

Britain’s Got Talent, FremantleMedia International

Modus, new eight-part series, FremantleMedia International

© Splash News 2015

©Miso Film 2015, Photo Johan Paulin

Richard Jeanneret is the Americas Vice Chair of Transaction

Advisory Services, EY.

EY on the US

Richard Jeanneret

13

Technology, life sciences, health care and financial services are the sectors to watch as we enter H2 2015 in the US. The improving

economy, sustained low-interest-rate environment and strong US dollar is continuing to help drive a growing number of acquisitions.

The first six months of 2015 saw 31 deals announced with a value over US$10b, compared with just 18 in the same period in 2014, according to Dealogic data — and the highest number ever announced for the first half of a year.

Technology and life sciences saw the greatest increases in deal volume in H1, cementing their places among the sectors that are going to be the most interesting to watch in the remainder of the year.

The life sciences and health care industries continue to abound with transformative deals driven by a push for consolidation and convergence. As both sectors face increased competition in a customer-driven marketplace, life sciences and health care companies will both look to strengthen their positions and grow through M&A activity.

The life sciences sector, which claims 4 of the 10 largest US deals for the year so far, continues its two-year streak of active dealmaking. US transaction volume is up 22% from H1 2014, and deal value is up 45.2% to US$236.1b, compared with US$162.6b from the same period last year.

Many pharmaceutical and medical technology companies are growing at a slower rate than the industry overall and risk being left behind; the last two years

Building from a strong start, the second half of 2015 is looking to surpass the first, with even more M&A activity predicted for the US.

have shown that one of the most effective ways for companies to keep pace with business growth is through M&A.

The financial services space has also seen a boom in deal values over H1, with banking and capital markets M&A deal value spiking to US$49.8b, a huge 240% increase on the deal value total from the first half of 2014. While banking and capital markets deal volume dropped off by 5.6%, this precipitous rise in value signals a pickup in the sector that will likely continue through the rest of the year.

US deal pipelines are full, and companies are exuberantly seeking assets to grow and transform their businesses. After a period of intense focus on cost control and organic growth, CEOs are coming off the bench and doing significant deals, but we are seeing a more disciplined approach to the deal frenzy than in previous boom times.

Positive macroeconomic indicators, resurging confidence, shareholder pressure and cross-border momentum all combine to create the perfect recipe for a strong deal market set to continue throughout the remainder of 2015, as companies seek to transform their businesses. Expect second quarter earnings challenges to be a catalyst for inorganic growth as well.

For the past several years, we have been waiting for companies to transact in order to beat out the competition and grow, and, now more than ever, it is imperative that companies manage their capital portfolio for growth before the good assets are all gone. The second half of 2015 will be exciting to watch as deal momentum in the US continues.

Second verse,

© M

att G

reen

slad

e

than the first? stronger

Capital Insights from EY Transaction Advisory Services

Lights, camera, transactionThe media and entertainment sectors are becoming ever more entwined. Capital Insights explores the impact that this is having on M&A.

Confidence is key for any industry, and none more so than the media and entertainment (M&E) sector. The good news is that confidence among executives about M&A in the sector is at its

highest level for four years, according to the latest EY Global Capital Confidence Barometer (CCB), published in May.

Some 50% of the respondents to the CCB survey said that they expected to pursue acquisitions in the next 12 months — an increase of 14 percentage points on the same time last year. And 89% said that cross-border M&A opportunities were on their radar.

Last year saw both volume and value at a five-year high. According to Mergermarket figures, there were 666 deals in the sector, valued at US$76b. So it is unsurprising that H1

2015 — with 262 deals, valued at US$26b — did not quite reach those lofty heights.

However, according to Will Fisher, EY Media and Entertainment Transaction Advisory Services Leader for the UK and Ireland, there are reasons to be optimistic about the market in H2 — not least of which is the fact that his team’s deal pipeline has never been so full.

His confidence is borne out in EY’s CCB, which shows that deal numbers in the M&E pipeline have leapt in the past six months, with 29% saying they have five or more deals on the go, up from 16% in October 2014.

Investing

Optimizing

To only be a broadcaster or a wireless company or a telephone company is just not enough these days.

capitalinsights.ey.com | Issue 14 | Q3 2015 | 15

Lights, camera, transaction

“There was perhaps a pause for the UK election, but since then it has really accelerated,” says Fisher.

“The UK market is particularly hot at the moment. US businesses are looking at Europe because it is harder to find growth in their domestic market. The UK is attractive — it has content that can travel to the US and internationally.”

Tom Connolly, Global Head of Media and Entertainment Transaction Advisory Services at EY, agrees with this assessment. He believes that a few specific factors have led to a pause in the market.

“There is the political turmoil, in Greece, for instance,” he says. “But there is also the movement in the US toward a Title II-type regulatory environment for cable and broadband providers.” This refers to the Federal Communications Commission (FCC) decision to treat the cable and broadband industry like a public utility, enforcing net neutrality.

Connolly believes that such factors, along with US media multinational Comcast’s abandonment in April of its proposed US$45b merger with Time Warner

Raising

Cable, have “caused people to pause, take a step back and reassess the landscape.”

However, this has not slowed the market entirely. There have been a number of big deals in the first half of 2015, including Verizon’s successful US$4.1b bid for AOL.

And as we enter H2 2015, as predicted by EY’s latest M&E CCB, consolidation, convergence, content and cross-border deals will drive M&A in the sector.

Come together“There’s always consolidation,” said Barry Diller, Chairman of US media giant IAC/InteractiveCorp, in a recent

interview. “Consolidation is the nature of things.”

Indeed, some of the most valuable players in the M&E space — such as Disney with the purchases of Pixar, Marvel and Lucasfilm — are products of consolidation in some way.

“In an environment where you are trying to negotiate the most favorable deals for your business, being a minor player is something of a disadvantage. I think there will be a continued drive to get economies of Fr

om le

ft to

rig

ht N

BC/G

etty

imag

es; K

obal

Col

lect

ion;

NBC

/Get

ty im

ages

; Gre

g Pe

ase/

Get

ty im

ages

; NBC

/Get

ty im

ages

Media and entertainment in numbers

50%Of companies expect to pursue acquisitions in the next 12 months

29%Of companies have more than five deals in the pipeline

89%Of companies are looking across borders for M&A

77%Of M&E executive are confident that the state of the global economy is improving

Top M&E M&A destinations1. US2. UK3. Netherlands

4. China5. Australia

Source: EY Media and Entertainment Capital Confidence Barometer May 2015.

In the spotlightCapital Insights reveals the six key factors that will put your company ahead of your rivals in the M&E dealmaking arena.Focus on the end-user. “Ask yourself how, when and why customers are going to consume or access the content,” says EY’s Fisher. “Companies need to understand the technologies that are emerging, and keep an eye on how they will move. They need to be less worried about embracing a technology and then finding out what that means for their content. Instead, they must be flexible to find the technology to suit their content.”

Don’t stifle innovation. When a large media company takes over a smaller, more innovative business, culture can present a challenge. “Fast-growing disruptive companies have often got where they are by ignoring the rules of the game and by operating as aggressively as possible in order to grow,” says EY’s Connolly. “When these young companies become part of a bigger company, they have to adapt, but you do not want to handcuff them.”

Keep talent happy. Identify key employees at the target company, and ensure that they are fully motivated and incentivized post-acquisition.

Get the financial structure right. When M&E businesses acquire smaller, and arguably more innovative businesses, it is common to take a controlling but not 100% stake. And earnout deals, whereby the final price paid for the business is dependent on its post-acquisition performance, are also becoming popular.

“We have seen the earnout structure, which had become less prevalent, coming back,” says Fisher. “A way of bridging the gap between the seller’s and buyer’s perception of value is with earnouts. It also motivates the core talent and founders to stay in the business longer.”

Think about integration from the start. When asked about the biggest obstacles to integrating an acquisition in the

technology, media and entertainment space, 31% of respondents to law firm Reed Smith’s recent Wired Up survey pointed to the difficulty in creating synergies once the deal is done. And 18% said that effecting actual transformative change is also a challenge.

Integration planning must start during the due diligence process. “An effective integration plan needs to be identified, and leaders should be working together well before closing occurs,” says Herb Kozlov, Reed Smith’s Global Corporate Group Head in the Wired Up report.

Strategic thinking. Be clear about why you are buying the business. Particularly if you are a business from outside the core sector looking to converge.

On the webFor more, read the 12th edition of the Media and Entertainment Capital Confidence Barometer at www.capitalinsights.ey.com/M&E

Capital Insights from EY Transaction Advisory Services

scale and deploy capital to get the highest returns,” says Connolly.

FremantleMedia’s Director of M&A and Strategy Caroline Murphy doesn’t always agree. “We don’t necessarily subscribe to the idea that bigger is better ... I’m not convinced that some of these recent deals will bear fruit.”

The nature of the megadeals announced in H1 in media distribution shows that consolidation is on the corporate agenda, and Murphy sees this as part of the industry’s natural cycle; consolidating, growing and divesting in turn.

However, in the US, the FCC and market forces will determine how much consolidation actually takes place. The FCC is currently looking at the proposed tie-up of cable telecoms companies Charter Communications, Time Warner Cable and Bright House Networks. And the regulator also reviewed AT&T’s US$67b takeover of satellite television company DirecTV, which completed on July 24 this year.

Content versus distributionWhen it comes to winning customers, content may still be king, but distribution is very much a kingmaker. These two complementary yet conflicting bedfellows have been competing for decades. However, alliances are being drawn up that could cause repercussions in the market.

Content seems to hold the upper hand — because distribution technology, as it matures, becomes easier to replicate. “Technology is being less used as a differentiator,” says Fisher. “As the technology has become better understood, the focus has swung back to content.”

Amazon, worldwide, and BT in the UK are using content to sell their distribution

Siri

Sta

ffor

d/G

etty

imag

es

capitalinsights.ey.com | Issue 14 | Q3 2015 | 17

platforms as the technology behind those platforms becomes more commonplace. Meanwhile international cable company Liberty Global increased its stake in ITV, the LSE-listed UK commercial broadcaster, to 9.9% in July. But according to Fisher, uncertainty may be delaying further deals in Europe.

“If there is uncertainty, that risk has to be priced in. So people are not keen to sell,” he says. “These are not distressed sales. So where you have unwilling sellers and uncertain buyers, they don’t have to happen.”

Convergence on the cardsOne of the current buzzwords in the M&E sector is “convergence” — the joining together of businesses from across the entertainment, media and communications sectors. And it is something that is bringing another cash-rich and acquisitive sector into the mix — technology.

Wired Up, a report published in June by Mergermarket and law firm Reed Smith, revealed that there were US$34.5b of convergence transactions last year, up 11% on 2013. Furthermore, 84% of respondents to the survey expect to see more convergence deals in the next two years.

“Convergence is likely to be one of the main drivers for M&A activity in the next period, whether it is companies looking to find add-on products to improve their platform or to enable them to deliver different products in different ways as a means of accelerating their growth,” says James Wilkinson, a Reed Smith partner who specializes in Technology, Media and Telecommunications. “To only be a broadcaster or a wireless company or a telephone company is just not enough these days.”

Convergence megadeals in 2014 included:• Gaming technology company Scientific Games

Corporation’s US$5b takeover of gaming entertainment business Bally Technologies in the US

• French advertising and PR group Publicis’ US$3.3b takeover of US tech company Sapient Corporation

• Media group Daum Corporation’s US$3.2b takeover of tech business Kakao Corporation in South Korea

The Wired Up survey also revealed that according to sector business leaders, the main driver of the convergence trend is “media companies looking to improve their technology platforms and delivery tools” — identified by 71% of respondents. This was followed by “companies from the media, entertainment and technology sectors looking to become conglomerates” — identified by 65%.

While convergence is by no means a new phenomenon, it is one that businesses cannot afford to ignore. “Convergence

Local knowledge is crucial when investing in the TMT sector, says CVC Capital Partners’ Lorne Somerville.

A t CVC Capital Partners, we have significant investments in cable and broadband media businesses: Arteria Networks in Japan, Hong Kong Broadband Network (HKBN), Link Net in Indonesia,

Operator R in Spain and Sunrise in Switzerland.M&A is increasingly dominated by strategic consolidation plays. PE

is having to be more selective than usual to find a business, and develop a business case, that can generate the right returns in this environment. Regulators have started to be more understanding. So for now, we will see more strategic opportunities.

Strategic cross-sector and in-market consolidation will be particularly prevalent among European corporates in the sector. The healthy deal flow in the US involves significant PE secondary buyouts, with selling firms buoyed by exit multiples. Convergence of technology and content on platforms is a feature of Europe and the US. But, elsewhere, a variety of dynamics are at play.

Hong Kong is a hyper-competitive market, with pricing near the lowest in the world and broadband speeds near the fastest in the world. This presents an immense value proposition. It is definitely an unconverged market and more of a best-of-breed market. The consumer takes broadband infrastructure from one place and content from elsewhere.

We invested in Indonesian cable company Link Net in 2011, which was followed by a period of organic growth through the rapid rollout to customers in Jakarta, Bali and Surabaya. Last year, Link Net listed on the Jakarta stock exchange, and we retained an approximate 30% stake.

Link Net was a huge greenfield company. And rather than look at the usual metrics, we had to get out in the field to see that they could roll the business out. The success of the investment also involved the recruitment of an effective sales team, largely from Citibank’s credit card team.

Understanding local markets is critical. Youngsters’ love of MTV worldwide and the global popularity of the BBC’s wildlife documentaries may imply that the M&E industry is, globally, a level playing field. But each market has idiosyncrasies as to how content is delivered and consumed. This presents an M&A opportunity for PE. You don’t see US corporates moving into these markets and imposing their corporate culture. And that is the opening for PE, as an importer of best practice and great management, combined, in our case, with our local presence.

Viewpoint

Lorne Somerville is Partner and Head of the TMT team at CVC Capital Partners — a global PE firm with US$60b of assets under management.

M&A in the sector is increasingly being dominated by strategic consolidation plays.

Young companies are hungry for capital and they need larger corporates to get where they want to be. And larger corporates want innovation.

Capital Insights from EY Transaction Advisory Services

is generating a continued drumbeat of buying pressure,” says William Doran, Corporate Partner at Reed Smith. “[This is particularly true] for firms that need to reformulate their strategies to stay competitive. These firms feel the need to acquire because there is often not enough time or ability to develop internally.”

Convergence in the M&E sector is being driven by multiple factors, from rapid consumer adoption of new technology to disruptive innovation. But there are also challenges that need to be overcome,

particularly for companies that are going outside of their comfort zone.

“One major challenge for cross-sector acquirers is understanding a new area of business,” Gregor Pryor, a partner

at Reed Smith, explains in the report. “It’s tough, for example, educating a tech company about music copyrights. Some big music companies may get seduced by the idea that Apple or Google are going to change their commercial paradigm in the next five years. However, for a big tech company, the biggest challenge is understanding the space.”

Cross-border deals Cross-sector M&A is still a nascent trend. But cross-border trading is expected to be one of the major drivers of M&A over the next 12 months to two years.

The Wired Up report revealed that 57% of the technology, media and entertainment (TME) companies surveyed say that their next acquisition is most likely to come from outside their home market. However, challenges persist, including growing regulatory pressures, the European Commission’s view to break down territorial borders, and the regulatory burden on buyers in US deals. One way that companies are trying to tackle these challenges is by exploring possible joint ventures (JVs) or minority stakes.

“Foreign direct investment restrictions in the media are common, and so we see a lot of JVs or partnerships,” explains Connolly. “We are starting to see development of over-the-top services [i.e., the delivery of content over the internet] by Netflix, Google and Amazon. Their original focus was in the US, but they are expanding.”

While it has been a slow start to 2015, the pipeline is now primed, and the four C’s — convergence, consolidation, confidence and cross-border deals — of the M&E dealmaking environment should see the sectors reach the end of the year on a high note.

“The number of these deals is increasing,” says Connolly. “Young companies are hungry for capital, and they need larger corporates to get where they want to be. And larger corporates want innovation. The deals need to be structured so that it works for everybody. The winners will be those that get it right.”

For further insight, please email [email protected]

0

100

200

300

400

500

600

700

800

H1 201520142013201220112010

Num

ber

of d

eals

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Deal value (U

S$b)

Media and entertainment M&A, 2010–H1 2015

Deal volume Deal value

Media and entertainment M&A, target countries, 2010–H1 2015

Value:US$129.37b

China

Deals:35

Value:US$44.59b

USA

Deals:71

Value:US$3.78b

UK

Deals:22

Value:US$13.84b

Canada

Deals:8

US$

76bIn 2014, there were 666 deals in the sector, valued at US$76b(Source: Mergermarket)

US$

26bThe first half of 2015 saw 262 deals, valued at US$26b(Source: Mergermarket)

Andrea Guerzoni is Europe, Middle East, India and Africa (EMEIA)

Transaction Advisory Services Leader, EY.

EY on EMEIA

Andrea Guerzoni

19

Deal value for the first half of 2015 is the second highest on record at US$2.27t, just below the H1 2007 value of US$2.59t.

The numbers would suggest that we’re returning to where we were eight years ago.

One striking difference, however, is the percentage share of the deal value originating from Europe. In 2007, Western European companies acquired assets valued at US$1.18t, 32.3% of all global M&A, and only slightly behind the US$1.19t (32.6%) of deals done by US-based companies.

There was a steep decline in acquisitions by both European and US companies immediately following the global financial crisis, but US companies were far quicker to realize that M&A was a strong route to growth during a downturn. In 2015 so far, US companies have acquired assets almost equal to the value of the deals they did in the whole of 2007 — US$966.1b, according to Mergermarket figures. That equates to 42.2% of global M&A.

In contrast, European acquirers accounted for only 17.8% of global M&A in 2015 (US$408b). China, which accounted for 1.6% of global value in 2007 is responsible for 10.1% so far in 2015. In 2007, Western European companies acquired more than twice as much in assets as companies from Asia-Pacific. In 2015, we can expect Asia-Pacific companies to acquire 40% more assets than their European counterparts.

Europe looks set to emerge from the most severe downturn in a century and achieve sustained growth. We should expect companies to re-engage with dealmaking.

This year could become the highest on record in terms of global deal value as the resurgence of M&A has further accelerated in the first half of 2015.

Despite this, according to Oxford Economic Forecasting, growth across Europe is set to be lower than the US, China and the Asia-Pacific region for at least the next decade. Therefore, it’s vital for the future health and competitiveness of European companies that dealmaking is on the agenda. With Western European GDP expected to average 1.7% growth for 2015–24, against 5.5% for China and 2.6% for the US, European companies should look to secure higher growth outside their own region. The search for innovation will also be a significant part of the M&A story.

Europe’s strong historical, cultural and trading relationships with other regions supports dealmaking, but companies are not taking full advantage of that position. The missing ingredient is C-suite confidence. With a respite to the recurring Greek drama seemingly in place, and encouraging economic data, especially in Germany and Spain, confidence should return. As growth and outlook strengthens, that confidence should translate into deals.

Expect to see a resurgence of intra-European consolidations especially in industrials, health care, consumer products and TMT, and bolder moves outside the region, especially into the US and key markets in South America, Africa and Asia.

Relatively speaking, Western European companies have been absent from the deal table in recent years. Given the sustained recovery in M&A we are experiencing, it’s likely that if European executives aren’t buying, companies from other regions will gladly take their place.

Slow but steady for European M&A recovery

© T

om C

ampb

ell

Capital Insights from EY Transaction Advisory Services

Tech controlSucceeding in the hyper-competitive online space is one of the toughest challenges for businesses, especially for a company that has fallen from grace. Yahoo CFO Ken Goldman explains how he plans to help steer the internet giant back to the top.

Few people have had as much influence over Silicon Valley’s array of technology companies — and for such a lengthy period — as

Ken Goldman. He has worked in finance functions in the Valley for more than 30 years, serving as a CFO for more than 25 of those 30. And his influence spreads far beyond his current company, Yahoo.

“There are probably 15 to 20 CFOs in the Valley at the moment that I hired out of school for me and my companies,” he says. “I really enjoy hiring young talent — whether from graduate or undergraduate schools — mentoring them, promoting them quickly and giving them visibility and responsibility early on in their careers.” Goldman knows about taking on responsibility early. At the age of just 34, he became Chief Financial Officer of VSLI Technology, a semi-conductor firm, taking the company public that year.

Three years into his tenure at Yahoo, he is calling on his vast experience to steer one of the marquee names in tech back to glory. And for Goldman, Yahoo and the

© it

o

capitalinsights.ey.com | Issue 14 | Q3 2015 | 21

wider industry, this means refocusing on the fundamentals of finance.

“Frankly, we got away from it,” he says. “In the go-go days of the late 1990s, we got away from the core CFO job. That’s why companies got into trouble.”

Laying foundations When Goldman was hired by the then-new Yahoo CEO Marissa Mayer in 2012, the company had endured a tough start to the new millennium. The dot-com bubble burst and the company’s share price dropped from over US$100 at the start of 2000 to US$16 per share 12 years later. Mayer herself was Yahoo’s fourth CEO in just over three years. Goldman understood the need for calm.

“The last thing the company needed was for me to come in and say, ‘I know it all, and we are going to change a bunch of stuff to suit my needs,’” he says. “I spent the first 90 days getting a sense of the company and understanding things we had to work on.”

After surveying the landscape, Goldman found that his main priority was to establish

clear business processes. “In terms of doing things that could make a difference, one of the first I remember — and it’s something that seems very mundane — was the approval matrix,” says the CFO.

“I’m a detail-oriented individual, so I want to make sure I’m reviewing a number of expenditures. Just making sure we had the approval matrix, spending time on creating it and seeing what each of us could authorize and approve, ensured we managed our processes here.

“We also created our Capital Authorization Review Committee, where all the key players get together and review our capital authorizations on a weekly basis.”

Another priority was to refine revenue measurement processes. “We worked closely on creating better revenue metrics — by product, by region and by advertising product. We created it so that we had daily metrics — we didn’t have those before. Having the daily, weekly and monthly metrics gave us the knowledge on a regular basis about how our business is working.”

Goldman also emphasizes the importance of reviewing revenue and capital, a process that was previously missing. “We collectively created revenue review meetings,” he says. “We also have weekly deal review meetings. So now we have a regimented approach to reviewing deals and partnerships as well as potential acquisitions.”

Tips for successKen Goldman’s top advice to CFOsAvoid complacency. What occurs at a lot of companies is hubris. I’ve been at firms where everything was going up; however, we let hubris affect the team and missed some of the key trends going on. Avoiding disruptions is important.

It’s not about you. Part of the job is giving the CEO real advice. For that, you need to create processes, procedures and reporting mechanisms tailored to the way the CEO wants to run the business. So we’re creating systems here for the way [CEO] Marissa Mayer wants to run it, not the way I want to run it. You have to create the systems and teams that support the industry you are in and the CEO you work for.

Get to the bottom of the business. One thing I remember with the first company I took public is the business model. lt’s vital to get the business model right early. At Yahoo, we thought long and hard about the business model. How do you make revenue? How do you make money? What are the drivers of that? If you don’t understand the fundamentals of the business model, you’ll never answer those questions.

First, we get the right people in place. Second, we drive the right products. Third, we drive the right engagement. From this, we can drive revenue growth.

Capital Insights from EY Transaction Advisory Services

Key priorities With new processes in place, Goldman was able to focus on growth. And the CFO is clear on what is needed. “I’ve been in technology for going on 40 years, and technology value accretion is all about revenue growth,” says the CFO. “It’s that simple.”

By Goldman’s own admission, Yahoo is still catching up. “We’re not growing as fast as we want, but we’re very focused on

putting the pegs in place so that we can grow,” he says.

How will Yahoo achieve sustainable growth? “It comes down to something I call the wheel of fortune,” says Goldman. “First, we get the right people in place. Second, we drive the right products. Third, we drive the right engagement. And from all of this, we can drive the

revenue growth.” To secure growth, Yahoo is focusing in particular on what it calls “mavens”: mobile, video, native advertising and social. These make up roughly one-third of Yahoo’s revenue, and as Mayer said in an earnings call earlier this year, they are “core to [Yahoo’s] growth.”

Another priority for Goldman is to complete the spin-off of Yahoo’s holding in Chinese online market company Alibaba. Yahoo paid US$1b for 40% of the company in 2005. It sold under half of that stake back to Alibaba for US$7.6b in 2012. And in 2014, it sold a further 8% of Alibaba for

US$5.1b. Yahoo has already announced it is in the process of selling its remaining 15% stake in the company — valued at US$40b.

“We need to accomplish that [spin-off],” says the CFO. “That’s unique to us — a multibillion-dollar asset that we were spinning off once we were able to. ... But the first fundamental, and fundamental to being a tech company, is creating growth.”

Core focus As Yahoo refocuses its growth metrics toward mavens, the wider company’s makeup has also changed. In 2014, Yahoo closed 15 offices and began retiring more than 75 products and services. Goldman believes that such quick rationalizing is necessary in a fast-developing online sector. “Things can happen very fast,” he says. “You have to be able to work around. We have to ask what the core markets are.”

Part of the strategy focused on winding down Yahoo’s ventures in places where there was not a large enough presence to warrant a physical office.

“We looked at offices where, frankly, we don’t have critical mass in terms of people,” says Goldman. “For example, we love Jordan, but it didn’t make sense to have customer service in Jordan for us ... There were a number of places where we just didn’t have critical mass.”

These actions are part of a drive to centralize Yahoo by bringing key talent and core functions closer to the company’s headquarters in Sunnyvale, California.

“One of the things Marissa said last year was that whatever is most important to Yahoo should be brought close to corporate headquarters,” says Goldman. “So in Sunnyvale today, we have the core functions of search and mail and so forth. We wanted to make sure the core functions are close to the center of gravity. We wanted to emphasize what we really are, and what we are is these various products.”

1994 19961995 19991997

Yahoo goes public, raising US$33.8m from its IPO.

Yahoo becomes incorporated and raises approximately US$3m in two rounds of venture capital funding.

Stanford University students David Filo and Jerry Yang set up Jerry and David’s Guide to the World Wide Web in March. They rename it Yahoo in April.

Yahoo makes its first billion-dollar acquisition, buying internet radio service

provider Broadcast.com for US$5.7b.

Yahoo makes its first acquisitions, buying search engine Net Controls in September for US$1.4m and Internet directory Four11 in October for US$92m. Five more acquisitions follow.

capitalinsights.ey.com | Issue 14 | Q3 2015 | 23

Working with shareholders While managing all of these changes, Goldman has had to contend with vociferous activist investors. Last year, investment management firm Starboard Value LP asked the company to combine with fellow internet business AOL.

The CFO emphasizes the importance of allowing investors to voice their opinions. “Sometimes Marissa and I will go visit investors and just listen,” Goldman says. “We don’t have a new story to tell, we just want to do an outreach and ask: ‘What [do] you think about us?’.

“[But] you have to be careful,” the CFO adds. “The most important thing is the work mixture — you have to spend most of your time on the fundamental parts of the business. I will tend to meet with the analysts on an exceptions basis, and we attend a number of tech conferences, do a number of fireside chat Q&As around them, as well as investor meetings.”

Talent spottingGoldman’s strategy of buying companies for their talent, rather than necessarily for the company itself, has helped Yahoo accelerate development in areas where it was lagging. “Frankly, we were behind in mobile. We had very few engineers working in mobile. So what we did was acquire a number of folks through [acquisitions] — what we call talent acquisitions. [These involved] relatively small payments, but allowed us to grab up to 25 people at a swoop, to accelerate the

process as opposed to one-off hiring.” Back in 2013, the acquisitions of start-ups Astrid, GoPollGo, MileWise and Loki Studios saw Yahoo add 22 mobile-focused employees to its payroll.

Product placement Away from smaller talent acquisitions, Yahoo’s M&A strategy is simple: “We only acquire companies, technologies, people or products that are consistent with or complementary to our business.”

Yahoo has recently made three large deals that Goldman says “moved the needle” in terms of size, and were done with mavens’ growth in mind. In 2013, it purchased social media website Tumblr for US$1.1b. One year later, it acquired mobile analytics firm Flurry for US$240m. And later in 2014, it bought video advertising platform BrightRoll for US$640m.

“If you look at the Tumblr deal, that was part of our strategy to drive in social. The BrightRoll acquisition was consistent with our video strategy. Essentially, we look at where the market is going, and we look at acquisitions that would help us to prepare and accelerate our progress into those market areas.”

That acceleration is key. According to internet analytics firm comScore, BrightRoll is the highest-ranked online video advertising property in terms of US population reach, while a May 2015 study by GlobalWebIndex found that Tumblr was the second fastest growing social network, with a 94% increase in active users in 2014.

The CFOKen GoldmanAge: 66

CFO since: October 2012

Educated: BS in Electrical Engineering from Cornell University and an MBA from Harvard Business School.

Previous positions: CFO of Fortinet, SVP Finance and Administration and CFO of Siebel Systems, CFO of Excite@Home, Sybase, Inc., Cypress Semiconductor and VLSI Technology

YahooFounded: 1994

Employees: c.11,000

Countries: offices in 25 countries

Market capitalization: US$30.61b

© it

o

2004 2005 2005 2008 2012

Yahoo rejects takeover offer of over US$44b from Microsoft.

Yahoo pays US$1b for a 40% stake in Chinese online marketplace Alibaba.

Yahoo names Marissa Mayer as CEO.

Yahoo drops Google-powered search results and launches its own web crawling algorithm using technology from 2002 acquisition of Inktomi.

Yahoo and Microsoft pursue unsuccessful merger discussions in 2005, 2006 and 2007.

Capital Insights from EY Transaction Advisory Services

Smooth integrator One challenge posed by acquiring a large number of companies — Yahoo has acquired more than 50 in the last three years — is ensuring that the integration process is as smooth as possible. For Goldman, this means getting the target’s key stakeholders on board, giving them responsibility and ensuring that the target is not pummeled into the acquirer.

“You have to be subtle,” says the CFO. “For example with Tumblr, the thing we did not want to do was destroy the culture and just ‘smush’ them in. You want to make sure that they keep their identity.”

Ensuring that the original owners remain in charge of the target firm helps to keep this identity. “I feel very excited that [founder] David Karp is still running Tumblr. We have the same folks running BrightRoll and Flurry as well. They’re here, and they are all active members of our management team.”

Yet despite ensuring this entrepreneurial spirit is retained, the CFO is also keen, where possible, to spot potential optimization

points in the integration. “In most cases, we’ve kept Tumblr separate, with separate facilities and so forth. But we have recently merged the sales group with our own,” Goldman says. “We believe we can get leverage out of the sales group, which is why we merged it. We are looking at some of the ways we can rationalize back-end costs and data center costs.”

For Goldman, it’s all about finding the right balance. “We want to make sure that the core folks — the product folks, marketing folks, engineers and senior team — are driving the business. We don’t want to lose that entrepreneurial environment, but we want to get some of the benefits [of] integrating those back-end functions.”

Spending wiselyFor Yahoo, capital allocation is based on the potential effect on the balance sheet, Goldman says. The company’s focus on smaller acquisitions helps with this aim. “We look at acquisitions that are what I would call ‘bite-sized,’ so that we can digest them in a

Today’s CFOYahoo’s Ken Goldman outlines his thoughts on what makes a CFO in 2015.There are many roles the CFO has to play today. Part of that is to ensure the sanctity of accounting — you can never forget its importance. You also have to make sure you have the right systems, processes and procedures in place. Alongside that, you have a number of functional roles, making sure you collect your accounting, your quarterly close, your treasury function and so on.

On top of this, the CFO has become more of a leadership position. When I first

started, the CFO might have been some sort of an afterthought member of the team, which it isn’t now. When I went to work at Siebel Systems — and I remember this distinctively — I didn’t tell them what I wanted for compensation, I just said: “I want to be in the top five.” I wanted it to reflect the importance of the role. The CFO now also acts as a good sounding board for the CEO. We don’t have an axe to grind, we don’t have an agenda, so part of the job is calling it how it is.

On top of this, there is much more of an emphasis on the CFO to tell the story of the company — investor outreach has become much more important.

However, while the job has changed in some respects because of its increased significance, some of it hasn’t. It’s still about making sure the accounting, the processes and the budgeting is done right. You cannot delegate any of these things — you have to do them internally. These are critical aspects to the job.

2012 20132013 20142013

For the first time since May 2011, Yahoo sites get the most monthly visitors among internet properties with 196.5 million unique visitors.

Yahoo pays US$1.1b for social network Tumblr.

As Alibaba goes public, Yahoo sells a further 140 million

shares in the company, pocketing US$9.4b.

Seven years after spending US$1b on a 40% stake, Yahoo completes its first share repurchase agreement with Alibaba for US$7.6b.

Yahoo rebrands with a new logo and image.

capitalinsights.ey.com | Issue 14 | Q3 2015 | 25

reasonable way,” he says. “The largest one we’ve done is Tumblr, which was US$1.1b. BrightRoll was about half of that. With the smaller ones, it becomes a ‘talent and tuck-in’ approach, which makes them easier to rationalize.”

Yahoo has also been active in buying back its stock, adding US$2b to its share buyback program in March. “From the beginning of 2012, we’ve bought back something like US$10b of our stock.”

The rationale is simple: “We look at the intrinsic value of our stock. And if we can buy it at a price below that, then we’re very interested,” he says. “There was a period when Alibaba was private, and we had to create a value that we thought was fair. We feel very good about the capital allocation in buying back our stock over the last three years.”

Staking your claim The decision to measure revenue based on mavens is indicative of how much the internet has changed. And while Goldman acknowledges that there are companies operating in similar areas, he believes Yahoo represents something slightly different.

“We have competitors in different spaces,” says Goldman. “In sports, we have ESPN, in finance we have Bloomberg. This is what separates us from the likes of Facebook, Twitter and LinkedIn — they are primarily user-generated content-based companies. We have our own content. We have some similarities. Obviously, we have search,

mail — but I think of them as peer companies.”

Yahoo embraces being in various spaces as it continues to invest along the lines of its mavens-driven strategy. For example, in June, it won the rights to partner with the National Football League (NFL) for its first global live stream, due to broadcast in October. This opportunity enables Yahoo to leverage its mobile and native advertising services. “That’s really important to us — it’s video, it’s social, and we’re putting that on mobile,” says the CFO.

The move to mobile represents a key shift away from Yahoo’s dependence on its legacy desktop business. But while the talent acquisitions and conventional M&A have helped, Goldman admits that there is still some way to go.

“We’re roughly about a third of the way down the road,” he says. “Obviously, PCs aren’t a growth market. So the best you can do is to stabilize that while getting new areas, such as video and mobile, growing. We’re making good progress there. Five years from now, it could be two-thirds mobile and one-third desktop, but we’ll see.”

The strategy appears to be paying dividends, as Yahoo’s Q2 2015 results show mobile revenue was up 54.6% year-on-year, to US$252m. Although on the right path, Goldman knows that there is still a long journey ahead for Yahoo if it is to reclaim its place among the top echelons of tech. Yet he believes that through financial organization, controlled acquisitions and strategic realignment, it can get there.

“Yahoo is a [company] that people think highly of, and I felt it was worth a lot of effort to get it back to where [it was]. People really do use us in their daily lives — whether it be sports, finance, news, weather or email. It’s amazing how many people use and see us on a daily basis.”

© it

o

2014 2014 2015 2015 2015

Yahoo launches Livetext, a live video texting application.

Yahoo’s stock price breaks US$50 in November, the first time in 14 years.

Yahoo announces acquisition of shopping

site Polyvore.

Yahoo partners with Yelp, Inc. to boost its local search results to better compete with services such as Google.

Yahoo announces it will spin off its remaining 15.4% stake in Alibaba.

Capital Insights from EY Transaction Advisory Services

Private equity:

A fter breaking the exit record in 2013, PE-backed deals once again surpassed expectations in 2014, raising US$109.9b

across 211 offerings. Thanks to years of rising stock markets, fund managers could sell portfolio investments, returning record levels of cash to investors.

On the fundraising side, 977 PE funds closed in 2014, raising a total of US$486b, according to Preqin. Values are roughly on par with 2013 figures, but commitments are being shared between fewer managers, as investors become more selective.

Managers are now sitting on more dry powder than ever, with research firm Preqin estimating US$1.2t at their disposal. But prices are rising, and 2015 deal activity is slipping. In the first half of the year, PE firms

invested in 247 deals in the US, valued at US$33b, a 26% decline in value compared with H1 2014.

Fewer large deals is one reason for decline — the number of US$1b-plus deals announced in the first four months of 2015 fell 23% compared with 2014. In April, PE firm Permira and Canada’s Pension Plan Investment Board took control of US-based Informatica in a deal valued at US$5.3b, the largest to date in 2015. But PE needs more large-scale deal flow.

“When you have between US$10b and US$20b to deploy, you have to focus on larger deals — and there aren’t many available,” says Jeff Bunder, EY’s Global Private Equity Leader. “So there’s a supply-demand imbalance.”

Competition on all sidesBunder adds that, on top of replenished funds vying for deals, trade buyers have begun to renew their M&A strategies, going head-to-head with PE firms. Also, some investors who would traditionally have committed to funds are now directly acquiring stakes in companies. Canada’s Alberta Investment

facing the

Private equity houses are sitting on a huge amount of dry powder. But tougher regulation and stiffer competition mean firms must evolve to succeed.

future

capitalinsights.ey.com | Issue 14 | Q3 2015 | 27

Investing

Raising

Best in class

1

234Management Corporation and OMERS

Private Equity acquired risk consultancy Environmental Resources Management from buyout firm Charterhouse for US$1.7b in June. Notably, the sale was made off-market.

“New players, such as sovereign funds, Canadian pension funds and family offices, are jumping into the market and competing with traditional PE players like us,” says Dominique Gaillard, Managing Partner and Head of Direct Funds at Ardian, a France-based PE firm. “Obviously this means there are more investors hungry for deals, and that will push valuations higher still. But it is good for us when we want to exit.”

A hard working futurePE firms of the future will have to work harder to deploy capital reserves prudently,

5

avoid highly competitive auctions and seek new deal structures.