Embed Size (px)

Citation preview

Capital Flows, Crises, and Growth

Joseph Stiglitz, Senior Vice President and Chief EconomistThe World BankDecember, 1998

Outline of the Talk

• Africa and the International Financial Crisis• Learning from East Asia• Preventing Crises: The Right and Wrong

Lessons from East Asia• Responding to Crises: A Systemic Approach

Global Growth of Capital Flows

Net Long-Term Capital Flows to Developing Countries

0.0

1.0

2.0

3.0

4.0

5.0

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Pe

rce

nt

of

GD

P

Private

Official

Capital Flows to Sub-Saharan Africa

Net Long-Term Capital Flows to Sub-Saharan Africa

-1

0

1

2

3

4

5

6

7

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Pe

rce

nt

of

GD

P

Private

Official

Capital Flows to Africa in the Wake of the Crisis

Gross Private-Source Long-Term Debt Flows(Current US$ Billions)

1996 1997 1998* Percent change96/97 average to 98

DevelopingCountries

204.6 291.0 183.3 -26%

Sub-SaharanAfrica

7.2 10.5 4.2 -53%

East Asia andPacific

71.5 74.7 25.9 -65%

South Asia 10.4 12.6 3.4 -85%

Europe andCentral Asia

26.5 51.4 46.0 -71%

Latin Americaand Caribbean

84.0 121.6 89.7 -13%

Middle East andNorth Africa

5.0 20.2 14.2 +12%

* Estimate based on the flows from January through September 1998 annualized.Source: World Bank’s Global Economic Prospects 1998-99 and calculations.

Effects of the Crisis on Africa

(1) Falling commodity prices

(2) Slowing foreign direct investment (due to falling commodity prices and the easing of substantial FDI from East Asia into Sub-Saharan Africa)

Summary: Why These Issues Matter For Africa

• Africa needs to adjust to declining aid flows and get more of the benefits of private capital flows

• But it needs to avoid the costs and crises associated with these flows

• Africa is affected by international economic conditions and is a participant in shaping the international economic system

Learning from the East Asian Miracle

• Dramatic economic growth and poverty reduction:– Per capita income growth of 5 percent and higher

– Stable growth with few if any downturns

– Indonesian poverty fell from 64 percent in 1975 to 11 percent in 1995.

• Many of the old lessons are unchanged:– Importance of education and technology

– Benefits of foreign direct investment

– Benefits of an export orientation

Overview: Causes of the Crisis -- Right and Wrong Lessons

• Coping with surges of capital flows

• The issue of short-term debt

• Did crony capitalism cause the crisis?

Capital Flows and Social Welfare

Key mistake: governments (and international institutions) trusted the market’s decisions:

Social risk private risk– Individual borrowers impose credit risk on economy

– Short-term debt may increase probability of a crisis

– Private debt increases the probability of a bailout

Limitations of Macroeconomic Policy in Coping with Inflows

• It was unknown if inflows were temporary or permanent

• Quandaries of exchange rate management given the constraints of fixed exchange rates, open capital markets, and financial liberalization.

– Not obvious how a different exchange rate could have helped

– Tight monetary policy helped encourage short-term inflows

– Fiscal policy was already very tight and even tighter fiscal policy conflicted with other objectives

Financial Restraint and Robust Economies

• The key problem was the externalities in the capital inflows and financial decisions.

• This could not be solved by macroeconomic policy alone.

• The solution lies not just in better Basle-style financial regulation, but more financial restraint (e.g. restrictions on lending to real estate)

Average Growth in Selected Countries,

1976-1993

0

0.5

1

1.5

2

2.5

3

3.5

Low High Low High

Ave

rage

Gro

wth

Initial Conditions

Stock Market Liquidity Financial Depth

Calculations by Ross Levine, World Bank

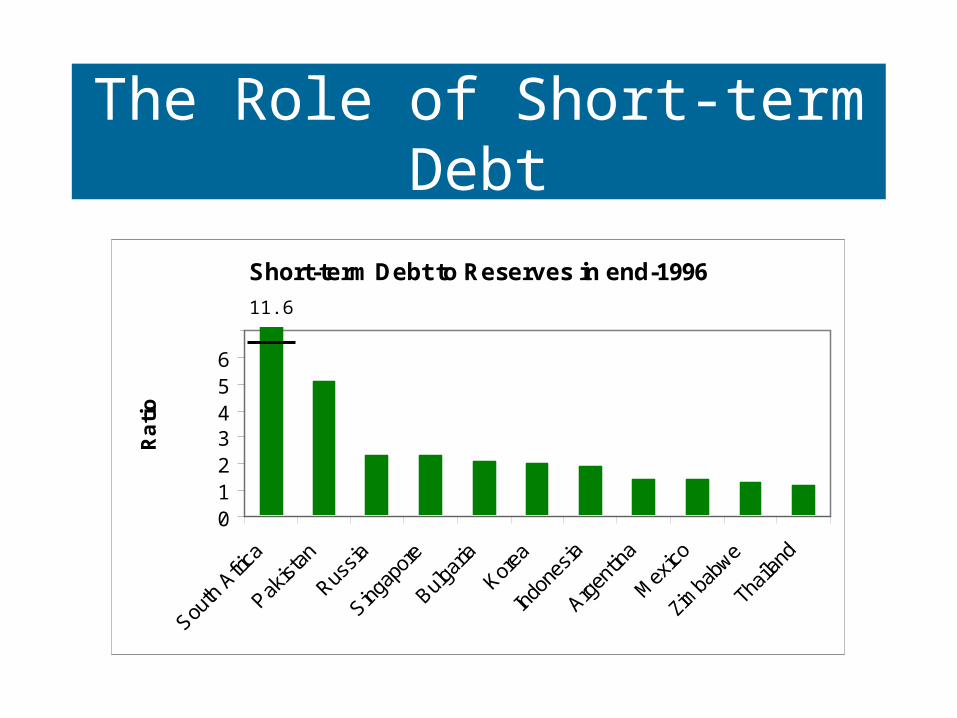

The Role of Short-term Debt

Short-term Debt to Reserves in end-1996

01234567

Ra

tio

11.6

Why the Relationship Between Short-term Debt and Crises?

• Sign of bad policies?• Vulnerability to a self-fulfilling collapse of

confidence?• Coordination mechanism for international

investors?

5

Economic Growth, Investment, and Capital Account Liberalization

-8

-6

-4

-2

0

2

4

6

8

-1 -0.5 0 0.5 1 1.5

Degree of Capital Account Liberalization

GD

P G

row

th 1

978-

1989

-15

-10

-5

0

5

10

15

-1 -0.5 0 0.5 1 1.5

Degree of Capital Account Liberalization

Inve

stm

ent/

GD

P 1

978-

1989

SOURCE: Dani Rodrik (1998). These are the residual growth and investment/GDP that are not explained by per-capita income, secondary education, quality of government institutions, and regional dummies for East Asia, Latin America and Caribbean, and Sub-Saharan Africa.

Implications of Short-term Debt

It raises questions about complete capital account liberalization

Policy responses:

(1) Better information

(2) Better financial regulation

(3) Direct restraints

Transparency and Economic Crises: Empirical Evidence

(1) There is no econometric evidence that lack of transparency increases the probability of a crisis

(2) The East Asian countries (except Indonesia) were not more corrupt or less transparent than other middle-income countries

(3) International transparency ratings were improving for all of the countries, including Indonesia

Transparency and Crises: Theoretical Perspectives

• When lack of transparency is common knowledge it should not affect expectations on average

• Theoretical models show that the relationship between transparency and credit rationing, credit collapses, and volatility are ambiguous

• Can write down models where lack of transparency worsens a crisis once it begins

GDP Growth Before and After Crises, 1975-1994

Output Loss From Crises

0

1

2

3

4

5

6

7

CurrencyCrashes

Banking Crises Currency andBanking Crises

GD

P s

ho

rtfa

ll re

lati

ve

to

tre

nd

(p

erc

en

t)

World

Industrial

Developing

Source: IMF World Economic Outlook, May 1998

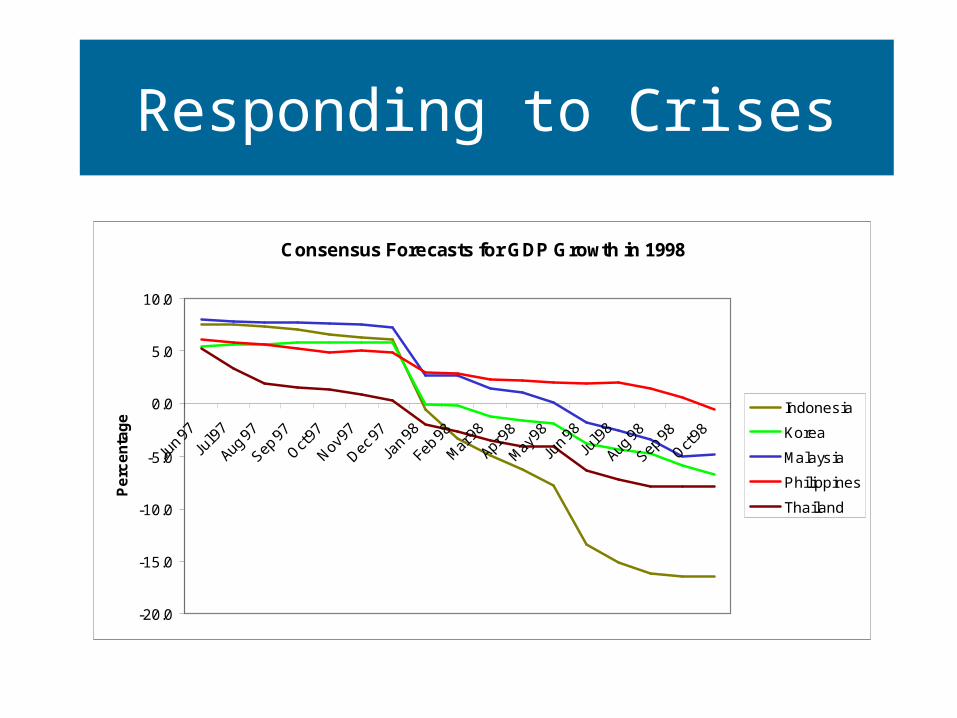

Responding to Crises

Consensus Forecasts for GDP Growth in 1998

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

Pe

rce

nta

ge

Indonesia

Korea

Malaysia

Philippines

Thailand

Constraints on Macroeconomic Policy

• Irreversibilities (it is easier to produce macroeconomic contraction than expansion)

• Nonlinearities (small shocks may self correct; large shocks may not)

• Persistence of macroeconomic shocks• Asymmetric social consequences

Defending Exchange Rates with Temporarily High Interest Rates

•Higher interest rates increase the promised rate of return. They also increase the probability of bankruptcy. Therefore the effect on the expected rate of return (and thus the exchange rate) is ambiguous.

•Key issue is why a temporary increase in interest rates would cause a permanent change in the exchange rate.

– Change in beliefs (+)

– Persistent change in economic health (-)

Balancing the Goals of Structural Policy

• Ex ante incentives

• Ex post incentives

• Distributional equity and fairness

• Macroeconomic consequences

The Role of Social Policy

• Fairness: minimize the suffering of the innocent

• Economic: social safety nets can have high fiscal multipliers

• Political economy: build consensus for other structural reforms and maintain socio-political stability and thus confidence

A Systematic Approach to Crisis Response

• Many types of policies (macroeconomic, structural, social) are necessary

• The focus should be on mitigating the downturn, not necessarily on steps to reduce distortions slowing long-run growth

The International Dimension of Crisis Response

• The international community needs to be involved because of the capital flows and other international issues.

• One way to be involved is to coordinate standstills and international debt workouts.

• Another way is to coordinate countries away from beggar-thy-neighbor policies. This recognizes the positive externalities from economic health.

For economic research

• We need to think seriously about microeconomic underpinnings of macroeconomic policies.

• We need to think through the consequences of market failures, especially in the financial sector, for the behavior of the economy in both crisis and non-crisis situations

• We need more research on crisis response

Conclusions

For policy

• We need robust policies, including some restrictions on short-term capital flows, while encouraging long-term flows and FDI.

• We need to think systematically about crisis response and focus on maintaining economic strength.

• We need to protect the victims of crises, not blame them.

Conclusions