Embed Size (px)

Citation preview

Capital Adequacy and Risk Management

Pillar 3 Disclosure Report

As of 31 December 2014

1

Capital Adequacy and Risk Management

Pillar 3 Disclosure Report

DHB BANK

2014

Table of Contents

I. BACKGROUND AND OVERVIEW .............................................................................. 2

II. RISK AND CAPITAL MANAGEMENT.................................................................... 4

1. Regulatory development .............................................................................................. 4

2. Risk Governance ........................................................................................................... 5

3. Risk Appetite ................................................................................................................ 8

4. Capital Management Framework ................................................................................ 10

III. CAPITAL BASE ....................................................................................................... 14

IV. PILLAR 1 RISKS AND CAPITAL REQUIREMENTS ........................................... 15

V. CREDIT RISK .............................................................................................................. 18

1. Overview of credit risk management ........................................................................ 18

2. Credit risk profile ...................................................................................................... 18

3. Counterparty risk and derivatives ............................................................................ 21

4. Credit risk mitigation ................................................................................................ 22

5. Asset quality .............................................................................................................. 22

VI. MARKET RISK ........................................................................................................ 25

VII. OPERATIONAL RISK ............................................................................................. 26

VIII. PILLAR 2 RISKS .................................................................................................. 27

1. Interest rate risk in the banking book (IRRBB) ........................................................ 27

2. Liquidity risk ............................................................................................................. 29

3. Concentration risk .................................................................................................... 30

4. Other risks: Legal, compliance and reputation risk.................................................. 30

IX. CAPITAL ADEQUACY CONCLUSION ................................................................. 32

2

I. BACKGROUND AND OVERVIEW

This document discloses DHB’s risk profile, risk management practices and capital adequacy

position to fulfill the Basel III disclosure requirements, as stipulated in the Capital Requirements

Regulation and Directive IV (CRR/CRD IV).

The CRD IV was enforced in the Dutch law as amendments to the ‘Wet op het financieel toezicht’

and further accompanying regulations. Jointly, these regulations represent the new regulatory

framework applicable in the Netherlands to, among other things, capital, leverage and liquidity as

well as Pillar 3 disclosures.

The Basel III framework holds three pillars. Each pillar concentrates on a different aspect of

banking regulation:

- Pillar 1 defines the way banking institutions calculate their regulatory capital requirements in

order to cover credit risk, market risk and operational risk.

- Pillar 2 addresses the banks’ risk management structure and processes for assessing overall

capital adequacy in relation to risks, including other risks not identified in the first pillar such as

concentration risk. Pillar 2 also introduces the Supervisory Review and Evaluation Process

(SREP), the response of the Supervisor to the internal capital adequacy assessment process

(ICAAP) conducted by banking institutions.

- Pillar 3 complements the first two pillars of Basel III by requiring a range of disclosures on

capital and risk assessment. Its aim is to encourage market discipline by enhancing

transparency that will allow market participants to make a better assessment of the bank’s

capital, risk exposure, risk assessment processes, and hence the capital adequacy of the

institution.

The new regulatory framework became effective on January 1, 2014, subject to certain transitional

rules. This report fulfills the disclosure required in the CRD IV regulation.

The Pillar 3 report consists of both quantitative and qualitative information as at 31 December

2014. The quantitative exposures in this report are not directly comparable to the numbers in the

2014 Annual Report. The numbers in the Annual Report refer to book values and classifications in

line with the International Financial Reporting Standards (IFRS). In this document, credit

exposure is defined as the estimate of the amount lost in the event of default or through the decline

in value of asset. This estimate takes into account contractual commitments to undrawn amounts.

In contrast, an asset in the Bank’s balance sheet, as published in the Annual Report, is reported as a

3

drawn balance only. This is one of the reasons why exposure values in the Pillar 3 report can differ

from asset values as reported in the published accounts.

Where this document discloses (credit) risk exposures or capital requirements, DHB has followed

the scope and application of its Pillar 1 capital adequacy calculations. Where figures for

impairment or losses are disclosed within this document, DHB has followed the IFRS definitions as

used in DHB’s Annual Report.

Furthermore, the bank’s Pillar 3 report supplements the qualitative information provided in the

2014 Annual Report on corporate governance, risk and capital management as well as the Notes to

the financial statements.

The information is not required to be and therefore has not been subject to external audit.

However, it has been subject to internal review procedures broadly consistent with those

undertaken for interim reports. DHB publishes Pillar 3 disclosures annually on its website:

www.dhbbank.com.

4

II. RISK AND CAPITAL MANAGEMENT

1. Regulatory development

New capital adequacy regulations were introduced in 2014. Regulation 575/2013 EU (CRR)

came into force in the EU on 1 January 2014 and is directly applicable in the Netherlands.

Directive 2013/36/EU (CRD IV) was also implemented in the Dutch law by the Wft. The

directive specifically monitors the reinforcement of the capital and liquidity of banks and

investment firms.

The new requirements stipulate that the bank must have common equity tier 1 capital of at least

4.5 percent, tier 1 capital of at least 6 percent, and own funds that correspond to at least 8 percent

of the total risk-weighted exposure amount for credit risks, market risks and operational risks.

In addition to maintaining capital to meet the minimum capital requirement, the Bank must also

maintain common equity tier 1 capital to comply with combined buffer requirements, which will

be phased in over coming years, and requirements under Pillar 2 of the regulations. The

requirements are decided by the supervisory authority after the Bank performs an ICAAP, in

which all risks and capital requirements are assessed rigorously.

In the forthcoming years, banks will be subjected not only to demanding capital and liquidity

requirements but also to other closely related evolving regulations such as on how to proceed in

case of financial distress (Recovery and Resolution Planning). On 15 April 2014, the European

Parliament adopted the Bank Recovery and Resolution Directive (BRRD), which came into force

on 1 January 2015. Its implementation in Dutch legislation has not been completed yet.

The purpose of a Resolution Plan is to document how a bank can be resolved in case the recovery

plan does not prevent the institution from reaching the point of non-viability. The recovery plan

documents the ability of banks to recover from a situation where their business model is so

challenged by the economic environment that it is necessary to revise its strategy in order to avoid

reaching a point of non-viability. DHB delivered an update of its recovery plan to DNB in

January 2015.

The BRRD introduces a Minimum Requirement for own funds and Eligible Liabilities (MREL).

The liability items qualifying for the bail-in buffer are referred to as Eligible Liabilities. These

‘own funds and eligible liabilities’ form a buffer to absorb losses. In this connection, the aim of

BRRD is to introduce a bail-in regime with effect from 1 January 2016. This means that, in the

event of a bank failure, first the shareholders and lenders are ‘charged’ for an amount of at least 8

percent of the balance sheet total or 20 percent of the risk-weighted assets. Only then can any

5

public funds be used. The amount in retail deposits exceeding Euro 100 thousand will not fall

under the 8% 'bail-in'.

Another important development in 2014 was the the enactment of the Policy Rule on Maximizing

the Deposits and Exposures Ratio under the Act on Financial Supervision (hereafter referred to as

New Business Model Policy Rule) in February 2014.

In nutshell, the New Policy Rule requires Dutch banks to comply with a certain ratio between the

banks’ exposure outside the European Economic Area (EEA) and their deposits under the

coverage of the Dutch deposit guarantee scheme, with the required ratio determined in relation to

the respective banks’ balance sheet size. Accordingly, DHB will continue to shift its lending

activities more towards the EEA, thus continuing in a direction that the bank had already started

to pursue following the 2008 crisis in the context of its strategic alignment. This strategic path

will further strengthen the bank’s commercial standing by increasing the diversification in its

assets. It is notable that country risk diversification would not only strengthen the Bank’s risk

posture but would also allow it to reduce Pillar 2 capital add-on requirements under the current

capital regime.

Overall, the banking sector continues to face a growing number of ever stricter international and

regulatory requirements and a more severe monitoring of compliance by supervisors.

Furthermore, data and reporting requirements are expected to increase substantially. DHB has

assigned appropriate resources to the implementation of the regulations and is prepared to meet

the consequences of the new regulatory requirements proactively.

2. Risk Governance

Risk and capital management are key success factors for DHB’s business and play a crucial role

in enabling management to operate more effectively in a changing environment. The Bank

assumes various risks, the most important being credit risk. Other relatively important risks are

liquidity risk, interest rate risk and operational risk.

DHB continually strives to further strengthen the bank-wide risk and capital management

framework in terms of organizational structure, processes and responsibilities, as well as the

methods for identification, measurement, monitoring and control of risks. Accordingly, the Bank

ensures that all risk-related policies are fully communicated and adopted at all levels.

6

The Bank’s risk governance framework is based on the risk strategy and the risk appetite, which

is integrated within the risk organization, policies and methods. The framework aims to safeguard

the Bank’s risk profile and steer risk management processes in line with the risk appetite of the

Bank.

The Supervisory Board has the final authority to approve the risk strategy and the risk appetite

statement proposed by the Managing Board, exercising its oversight of risk management

principally through the Board’s Risk & Audit Committee (RAC), supported by assessments and

reports prepared by the Internal Audit Department (IAD), Risk Management Department (RMD)

and Compliance & Legal Department (CL). RAC is responsible for the oversight of policies and

processes by which risk assessment and management are carried out within the governance

structure. RAC also reviews internal control and financial reporting systems that are relied upon

to ensure integrated risk measurement and disclosure processes.

The responsibility for risk management resides at all levels of the organization, from members of

the board to individuals in the business units. The control environment in the Bank is based on the

three lines of defense principles for segregation of duties. The structure starts with lines of

business being responsible for managing risks in their operations within approved risk appetites.

The three lines of defense structure provide clarity to every staff with regard to their role and the

level of risk awareness that is expected at difference phases in the lifecycle of respective risks.

With business units assuming the first line of defense function, RMD (Risk Management

Department), Credit Analysis Department and Compliance & Internal Control department form

the main second line of defense. They support the business units in their decision-making, but

also have sufficient independence and countervailing power in managing risks. The Internal

Audit Department as the third line of defense oversees and assesses the functioning and

effectiveness of the first two lines.

Formal risk governance processes are established in the Bank, whereby the management of risk is

guided and monitored by a number of committees.

Within the governance structure, DHB’s Risk Management Committee (RMC), Credit Committee

and Asset & Liability Management Committee (ALCO) oversee particular risks. RMC oversees

the management and control of the Bank’s risks on an aggregate level, in addition to the

committees and specialized functions that focus on specific risk areas. RMC also discusses and

ultimately endorses the methodology and outcomes of the ICAAP and the ILAAP by RMD.

7

The RMC consists of Managing Board members, two Assistant General Managers responsible for

credit analysis and for operational processes, respectively, the head of risk management

department, the ORCA (Operational Risk and Control Assessment) project leader and the

Compliance Officer. Chief Internal Auditor also participates in the meetings as an

observer/adviser in order to provide the committee with insight from an audit perspective.

IT related risk factors are controlled and monitored by different committees. The access control to

the core banking application resides on SPD (System Analysis and Process Improvement

Department) while technical control is exercised by the IT Department. Information security in

the broadest sense (including access control, technical control and business continuity policies

and activities) is ensured by the Information Security Manager (referred to as “ISM”). SPD, ISM

and IT units are assigned together in the IT & IS Steering Committee, a platform for

communication and decision on IT-related procedures and measures.

IT related risk factors are controlled and monitored through the IT & IS Steering Committee that

is chaired by the responsible Managing Board member and the Assistant General Manager,

responsible also for operational risk policies. To mitigate the IT related risk exposure further, an

(Information) Security Assessment and Response Team (referred to as “SART”) has been

established, which reports to the IT & IS Steering Committee. SART, chaired by the ISM,

consists of four IT specialists to bring in expertise to the committee in the fields of database &

core banking applications, network, Internet and third-party interfaces.

In the framework of compliance, the Security Officer, beside anti-money laundering measures, is

responsible for the incident and the complaint management systems. In addition to the immediate

benefits, the ultimate aim for maintaining these systems is gathering sufficient data needed to

model operational risks in time.

The overall control with respect to the non-financial risks is carried out by the Internal Control

Unit (referred to as “ICU”) and the internal and the external auditors. The ICU executes

predefined operational controls daily, weekly or quarterly depending on the risks attributed to the

concerned activities. The internal and external auditors also execute their inspections on the risk

management systems, policies and practices. Finally the Compliance Officer, who reports directly

to the Managing Board, is responsible for integrity and compliance in the broadest context.

Both financial risks and non-financial risks are reported to the Risk Management Committee

meeting at least four times a year with a special focus on regulatory risk, earnings risk, capital

risk and strategy risk. The Managing Board is in turn responsible for reporting to the Risk &

8

Audit Committee and the Supervisory Board. With this structure, a consistent segregation of

duties is achieved between risk generating, measuring, controlling and reporting units. The

independent organizational structure of the Internal Audit Department and the Compliance

Department, with a direct information line to the RAC, also ensures an effective control in the

respective fields.

The risk governance at DHB is depicted in the following figure:

3. Risk Appetite

Risk appetite framework is central to an integrated approach to risk, capital and business

management and supports the bank in achieving its strategic objectives as well as being a key

element of meeting the bank’s obligations under the supervisory review process.

The Bank defines risk appetite after performing the assessment of key risk sources and

perspectives of all key stakeholders (i.e. shareholders, regulators, external rating agencies,

auditors and customers) in the context of the Bank’s prevailing strategy.

9

A clear articulation of the overall risk appetite that reflects multiple risk perspectives, stakeholder

expectations and business objectives not only help protect the Bank’s performance and comply

with regulations and safeguard reputation, but it also moves risk management well beyond risk

mitigation toward optimization of risk and return characteristics across the business as well as

toward the identification of unused risk capacity.

Risk appetite is articulated by the Managing Board of DHB as part of the strategic planning

process, assessed by the Risk & Audit Committee, and approved by the Supervisory Board prior

to communicating the respective document to the wider organization involved with risk

management and to the stakeholders via various disclosures.

The articulation of risk appetite is also linked to the results of a comprehensive risk assessment,

which is periodically performed during ICAAP and ILAAP. On an annual basis, the Risk

Appetite Statement (RAS) is discussed and re-evaluated by the Supervisory Board’s Risk &

Audit Committee to enable the alignment of the Bank’s future strategy with the chosen risk

appetite, as and if circumstances and various stakeholders’ risk expectations change. RAS can

also be revised during the year when there are material changes in the Bank’s strategy or business

environment.

To facilitate monitoring, risk appetite is quantified (to the extent possible) and expressed through

risk based performance targets and limits. In addition, the Bank also uses stress testing and

scenario analysis to formulate risk appetite, especially in liquidity and capital adequacy

management. Periodic risk assessment and reporting of inherent risks in the Bank’s activities is

part of the risk management framework to allow for an aggregated view of risks. If risk limits and

targets are breached, or an activity or a product seems to be straying from the approved risk

profile, decisions must be made timely and pro-actively.

RAS is communicated to the head of departments and country managers and used as the main

starting point for quarterly risk assessment reports for discussion in RMC and RAC. RAS, and

also other policy documents, are accessible for all relevant staffs. By communicating within the

organization and embedding it in the internal processes, the Bank encourages a more conscious

risk taking behavior and reinforces risk culture within the organization. A strong and widespread

risk culture is in its turn an essential catalyst that elevates a risk appetite statement from a set of

words into a statement of action.

10

4. Capital Management Framework

The bank’s risk environment requires continual monitoring and assessment in order to identify

and manage complex interactions. The risk governance and ownership, risk appetite as well as the

scope and nature of monitoring and reporting processes that DHB has put in place are aimed at

meeting these challenges.

Furthermore, DHB ensures that it has adequate own resources to cover unexpected losses arising

from discretionary risks such as credit risk and market risk, or non-discretionary risks, which are

risks arising by virtue of its operations, such as operational risk and reputation risk.

DHB essentially has two approaches for the calculation of its capital need: a regulatory and an

internal approach.

The regulatory approach is largely based on fixed, uniform rules for covering the bank’s risks in

accordance with the Basel II/III standards.

The internal approach sets capital adequacy targets and uses the bank’s risk appetite along with its

risk profile and business plans as a basis. Other determining factors are expectations and/or

requirements of the stakeholders as well as the position of the bank in the Dutch banking sector. As

a consequence, the internal approach has to encompass the regulatory approach in order to be

comprehensive, effective and consistent.

The requirements/expectations of regulators concerning capital adequacy are not only driven by the

Basel guidelines for Pillar 1 and Pillar 2 risks, but also by a new capital add-on requirement

introduced in the Netherlands in July 2010 to achieve a certain prudential objective, namely to

reduce banks’ credit risk concentration in emerging countries.

The internal capital management approach is embedded in a formal ICAAP whose regulatory

framework is rooted in the CRD IV. DHB defines the ICAAP by which the Managing Board

examines the bank’s risk profile from both regulatory and economic capital viewpoints and ensures

that the level of available capital:

i. Exceeds the bank’s minimum regulatory capital requirements by an agreed margin,

ii. Remains sufficient to support the bank’s risk profile,

iii. Remains consistent with the bank’s strategic goal,

iv. Is sufficient to absorb potential losses under severe stress scenarios.

Although the regulatory approach and constraint have become more dominant as indicated above,

11

the ICAAP framework of DHB as an integral part of risk management retains its relevance since

it ensures a coherent link between the bank’s risk profile, its risk management, risk mitigation and

capital. The bank’s ICAAP framework also promotes a continuous monitoring of the risk

environment and an integrated evaluation of risks and their interactions. It represents a bank-

wide approach to deal with all material risks and all business activities of DHB.

The process itself starts with risk identification, assessment and measurement, which involves all

relevant departments. DNB‘s Financial Institutions Risk Analysis Method (FIRM) has been

chosen by DHB as an integral part of the ICAAP for its comprehensiveness in identifying and

assessing risks and control qualities. Identified risk types are classified into low, medium and

high risk levels based on the assessment of their relevance and potential impacts.

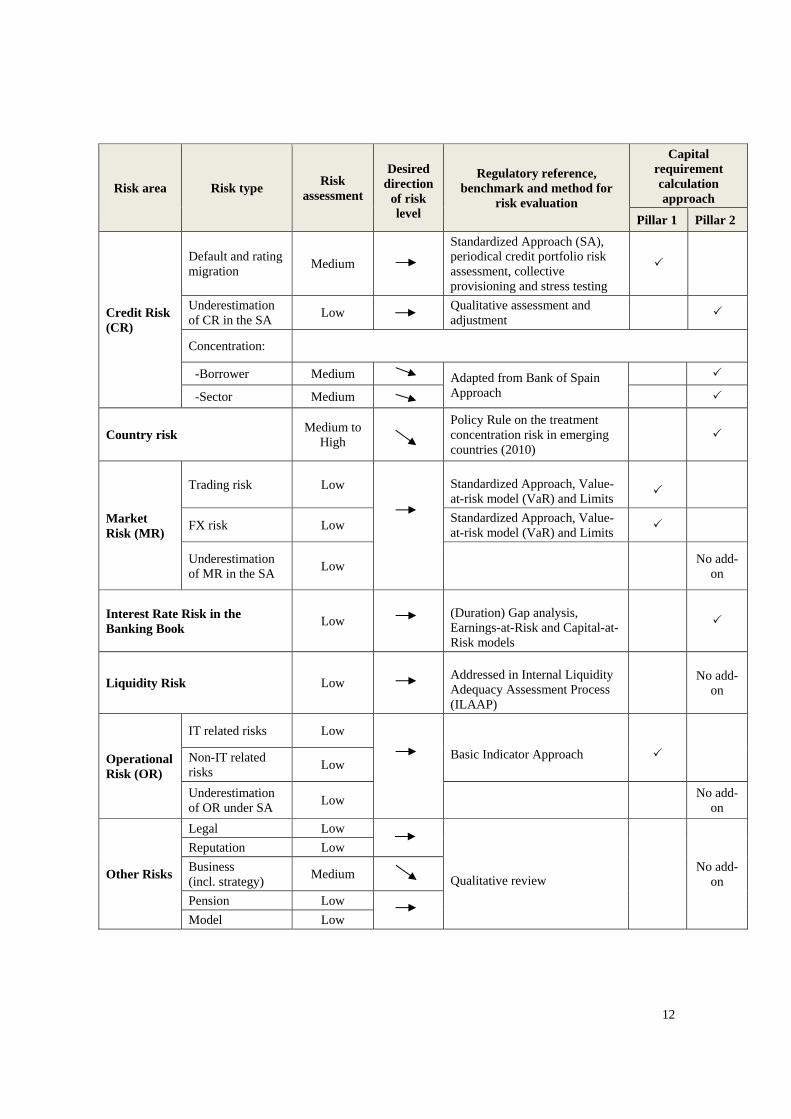

The table below shows a summary of the risk assessment results and methodologies under the

ICAAP framework for FYE 2014:

12

Risk area Risk type Risk

assessment

Desired

direction of risk level

Regulatory reference, benchmark and method for

risk evaluation

Capital requirement calculation approach

Pillar 1 Pillar 2

Credit Risk (CR)

Default and rating migration

Medium

Standardized Approach (SA), periodical credit portfolio risk assessment, collective provisioning and stress testing

Underestimation of CR in the SA

Low Qualitative assessment and

adjustment

Concentration:

-Borrower Medium Adapted from Bank of Spain Approach

-Sector Medium

Country risk Medium to

High

Policy Rule on the treatment concentration risk in emerging countries (2010)

Market Risk (MR)

Trading risk Low

Standardized Approach, Value-at-risk model (VaR) and Limits

FX risk Low Standardized Approach, Value-at-risk model (VaR) and Limits

Underestimation of MR in the SA

Low No add-

on

Interest Rate Risk in the Banking Book

Low

(Duration) Gap analysis, Earnings-at-Risk and Capital-at-Risk models

Liquidity Risk Low

Addressed in Internal Liquidity Adequacy Assessment Process (ILAAP)

No add-

on

Operational Risk (OR)

IT related risks Low

Basic Indicator Approach Non-IT related risks

Low

Underestimation of OR under SA

Low No add-

on

Other Risks

Legal Low

Qualitative review

No add-on

Reputation Low

Business (incl. strategy)

Medium

Pension Low

Model Low

13

Stress tests are part of the bank’s capital planning in the ICAAP and an important tool for

analyzing the bank’s risk profile. By incorporating appropriate stress testing and capital

planning, the ICAAP result is expected to reflect internal measures to establish if the bank is

adequately capitalized now and in the future.

The bank has also developed its capital management framework by benchmarking its ICAAP and

stress testing methodology against recommended good practices. As the regulation and

supervision of financial institutions are currently undergoing a period of significant change in

response to the global financial crisis, the bank has dedicated considerable time to monitor policy

actions that may influence its capital position and capital management framework. Refinement of

the internal methodology has been performed regularly since its first implementation in

2007/2008.

DHB performs regular internal stress tests designed to replicate shocks that are particularly

relevant for the bank’s existing business mix and macro environment. The stress test reveals how

the capital need varies during a stress scenario, and how the financial position, Pillar I capital

requirement and target capital ratio are affected. Outcomes of the stress tests are also used as

early warning indicators to evaluate the adequacy of the above mentioned recovery plan.

14

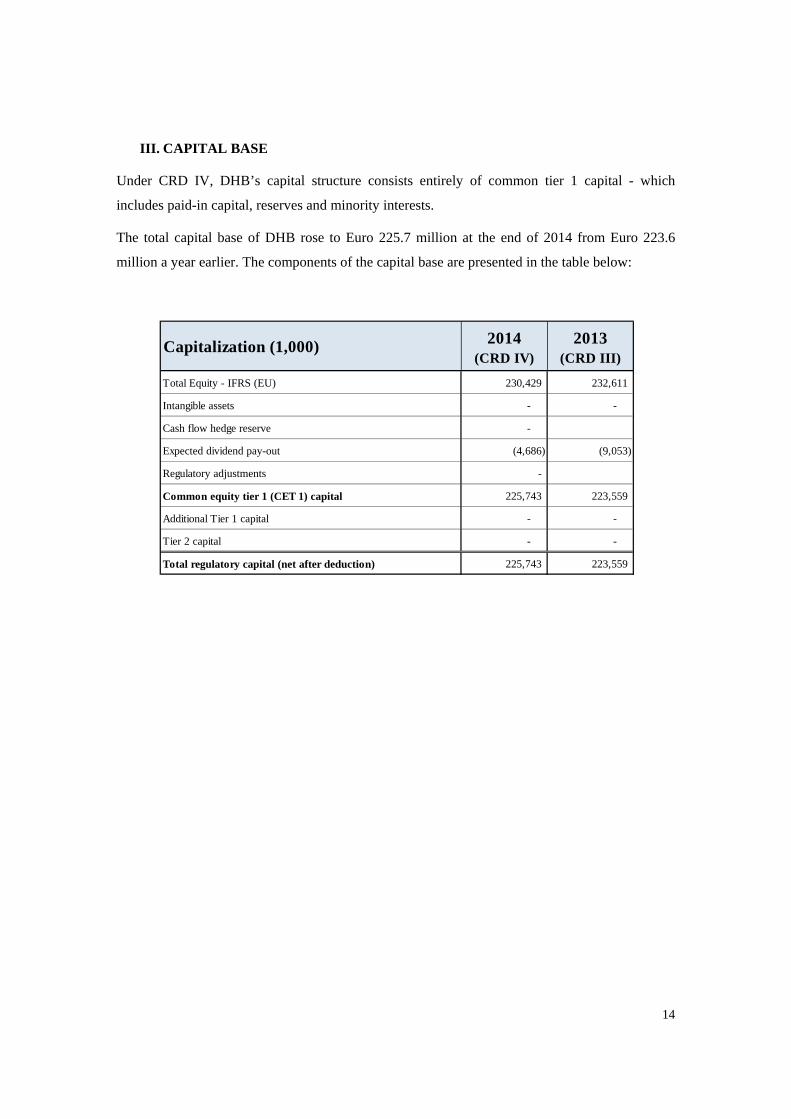

III. CAPITAL BASE

Under CRD IV, DHB’s capital structure consists entirely of common tier 1 capital - which

includes paid-in capital, reserves and minority interests.

The total capital base of DHB rose to Euro 225.7 million at the end of 2014 from Euro 223.6

million a year earlier. The components of the capital base are presented in the table below:

Capitalization (1,000) 2014(CRD IV)

2013(CRD III)

Total Equity - IFRS (EU) 230,429 232,611

Intangible assets - -

Cash flow hedge reserve -

Expected dividend pay-out (4,686) (9,053)

Regulatory adjustments -

Common equity tier 1 (CET 1) capital 225,743 223,559

Additional Tier 1 capital - -

Tier 2 capital - -

Total regulatory capital (net after deduction) 225,743 223,559

15

IV. PILLAR 1 RISKS AND CAPITAL REQUIREMENTS

This section describes DHB’s regulatory capital requirements that arise from Pillar 1 risks in the

CRD, namely credit, market and operational risks as of 31 December 2014.

The regulatory minimum capital requirement is expressed as eight percent of risk weighted assets

(RWA). To calculate RWA according to the Basel II/III framework, DHB adopted the

Standardized Approach (SA) for credit and market risk, and the Basic Indicator Approach for

operational risk. The adopted approach is consistent with the size, complexity and nature of its

activities in 2014.

In order to calculate the regulatory capital requirements under the SA, the bank uses eligible

external ratings from Standard & Poor’s, Moody’s and Fitch Ratings. These are applied to all

relevant exposure classes in the SA. If more than one rating is available for a specific borrower,

the selection criteria as set out in the CRR are applied in order to determine the relevant risk

weight for the capital calculation.

The following standardized exposure classes apply to DHB:

Sovereigns

Exposures to governments consist of sovereign governments, central monetary institutions and

agencies guaranteed by a sovereign government. Sovereign exposures are risk weighted based on

their credit ratings. Exposures to central governments within the European Union are assigned a

risk weight of 0%, where such claims are denominated and funded in the relevant domestic

currency of that sovereign.

Banks

Exposures to banks relate to all claims on financial institutions authorized and supervised by the

competent authorities and subject to prudential requirements comparable to those in the European

Union. Exposures to a bank are risk weighted based on the ratings assigned to them by eligible

rating agencies. Exposures to a bank of up to three months residual maturity for which a credit

assessment by eligible rating agencies is available are assigned risk weights that are generally one

category more favorable than the standard risk weights applied to banks exposures (see CRR

Article 120).

16

Corporates

Exposures to corporates include exposures to large non-bank corporations as well as to small and

medium-sized companies, which do not meet the conditions of retail exposure. Exposures to

corporates with external credit ratings by eligible rating agencies are assigned a risk weight from

20% to 150%. Exposures without external rating are assigned a risk weight of 100%.

Retail

Exposures are classified as retail exposures upon meeting the conditions stipulated in the Dutch

Regulation on Solvency Requirements for Credit Risk. Retail exposures are assigned a risk

weight of 75%.

Exposure secured on real estate property

This exposure class refers to the exposures or any part of an exposure secured by mortgages on

residential property. Exposures in this class are assigned a risk weight of 35%.

Past due items

In line with the requirements of the Dutch Central Bank, this exposure class only includes claims

which are past due more than 90 days. Shorter past due items are included in the corresponding

exposure classes mentioned above. The unsecured part of any past due item is assigned a risk

weight of 150% if value adjustment allowances are less than 20% and 100% if value adjustments

allowances are no less than 20% of the unsecured part.

Others

Other items consist of fixed assets, prepayments and other assets for which no counterparty can

be determined. Other items are assigned a risk weight of 100%.

17

An overview of the capital requirements and the RWA at the year-ends of 2014 and 2013 divided

into the different risk types is presented in the table below.

RWA (Basel III)

Capital Requirement

8%

RWA(Basel II)

Capital Requirement

8%1,263,373 101,070 1,211,354 96,908

of which: Sovereign - - 0Banks 337,237 26,979 358,899 28,712Corporates 897,923 71,834 810,700 64,856Retail 2,948 236 23,581 1,887Exposure secured on real estate property 3,274 262 3,505 280Past due items 8,240 659 1,151 92Others 13,751 1,100 13,517 1,081

Market risk 6,856 548 2,845 228 Operational risk 70,343 5,627 70,713 5,657

4 -

1,340,576 107,245 1,284,912 102,793

Credit valuation adjustment (CVA)

2014 2013

Pillar 1 Risks and Capital Requirement, Euro (1,000)

TOTAL

Credit risk

18

V. CREDIT RISK

Credit risk is the largest risk making up 94.2% of the total RWA at 31 December 2014. The

information in this section is analyzed in several dimensions to give an in-depth view of the

distribution of the credit portfolio in different exposure classes, risk weights, geography, and

industry.

1. Overview of credit risk management

DHB manages credit risk in a coordinated manner at all relevant levels within the organization.

A primary element of the credit approval process is a thorough risk assessment of the credit

exposure associated with each borrower and obligor. An obligor is defined as a group of

individual borrowers that are linked to one another by various numbers of criteria, including

capital ownership, demonstrable control over business or other indication of group affiliation.

The Bank measures and consolidates all claims on the same obligor (“one obligor principle”),

requiring the aggregation of all facilities (direct or contingent) to the borrower itself, its

subsidiaries, parent and related affiliates.

The creditworthiness of a borrower or an obligor is represented by internal rating. While DHB

uses the standardized approach for credit risk, internal rating system has been further refined in

order to strengthen the Bank’s credit risk management system. In addition to the internal rating on

obligor, the Bank’s risk assessment procedures also take into consideration the risks specific to

the type of credit facility or exposure.

DHB dedicates considerable resources to controlling credit risk effectively. Credit monitoring is

carried out through credit reviews on obligor level by the Credit Risk Management that reports to

the Credit Committee on a regular basis. An independent credit portfolio risk assessment is

conducted monthly by the Risk Management Department, which reports directly to the Managing

Board.

2. Credit risk profile

This section presents an overview of DHB’s credit risks in terms of key credit risk dimensions.

All exposures in this document refer to on-and off balance sheet items after specific provisions

and the application of credit conversion factors.

In the following table, the credit exposures are broken down into risk weights at the end of 2014

and 2013.

19

The next tables provide the distribution of DHB’s total exposure by remaining maturity at the end

of 2014 and 2013 respectively.

ExposuresRWA

(Basel III) Exposures

RWA(Basel III)

0% 202,633 - 195,468 020% 163,434 32,687 96,139 19,228 35% 9,356 3,274 10,014 3,505 50% 550,384 275,192 507,804 253,902 75% 3,930 2,948 5,011 3,758

100% 949,269 949,269 922,403 922,403 150% 2 3 5,706 8,558

Other risk weights - - - -

TOTAL 1,879,008 1,263,373 1,742,545 1,211,354

2014 2013Credit exposures by risk weights, Euro (1,000)

Credit Exposures by maturity at 31 December 2013, Euro (1,000)

< 3 months3 < 6

months6 < 12

months1-3 years > 3 years TOTAL

Sovereign 102,494 - - - 5,821 108,315 Banks 117,150 111,652 227,480 279,268 33,924 769,474 Corporates 283,087 101,751 82,890 333,428 163,746 964,902 Retail 5,623 136 646 1,597 3,884- 4,118 Exposure secured on real estate property - - 4 138 9,214 9,356 Past due items 3,258 - - 3,670 1,311 8,239 Other items - - 14,605 - - 14,605 Total Credit Exposures 511,612 213,539 325,625 618,101 210,132 1,879,009

Credit Exposures by maturity at 31 December 2013, Euro (1,000)

< 3 months3 < 6

months6 < 12

months1-3 years > 3 years TOTAL

Sovereign 120,106 - - 2,000 - 122,106 Banks 130,578 105,310 97,113 326,652 66,316 725,968 Corporates 393,839 66,008 38,381 220,887 116,303 835,418 Retail 7,005 117 351 12,376 13,783 33,633 Exposure secured on real estate property - - - 167 9,847 10,014 Past due items 768 - - - - 768 Other items - - 14,637 - - 14,637 Total Credit Exposures 652,296 171,435 150,483 562,082 206,249 1,742,545

20

The following table breaks down the main exposure categories according to the sectors of DHB’s

counterparties at the year-ends of 2014 and 2013.

The tables below show the credit exposures divided into main geographical areas according to the

location of the ultimate shareholder at the end of 2014 and 2013 respectively.

2014 2013

Sovereign 108,316 122,106

Banks 769,473 725,968

Corporates 964,903 835,418

of which: Non‐bank Financial institutions 257,619 374,451

Construction and infrastructure 133,504 98,068

Tranportation 57,992 39,287

Metals 75,162 47,090

Energy 48,833 46,748

Communications and post 16,836 32,766

Textile 33,481

Food beverages 25,594 9,299

Media advertising 40,128 ‐

Petroleum refining & related industries 2,271 2,665

Domestic & International trade 45,142 27,248

Chemicals 30,584 21,123

Mining and quarrying ‐

Tourism 23,838 21,370

Automative 43,486 22,607

Oil & gas 19,689 23,324

Plastics 6,464

Real estate 40,840 5,106

Agricultural products 10,144 6,786

Electrical equipment 840

Paper 3,674 4,350

Corporate individuals 22,123 6

Retail individuals 30,808 ‐

Other 36,635 12,339

Retail 4,117 26,717

Exposure secured on real estate property 9,356 7,431

Past due items 8,239 569

Other items 14,605 24,536

Total Credit Exposures 1,879,008 1,742,745

Credit Exposures by exposure class and industry, Euro

(1,000)

Credit exposures by exposure class and geographyat 31 December 2014, Euro (1,000)

NetherlandsOther

EuropeTurkey CIS Others TOTAL

Sovereign 102,469 5,846 - - 108,315

Banks 148,234 220,725 279,183 20,055 101,276 769,473

Corporates 25,216 342,092 398,500 71,052 128,042 964,902

Retail 3,437 17 663 - 4,117

Exposure secured on real estate property 1,940 7,265 130 - 20 9,355

Past due items 22 5,132 3,086 - 8,240

Other items 5,720 8,885 - - 14,605

Total Credit Exposures 287,038 589,962 681,562 91,107 229,338 1,879,007

21

3. Counterparty risk and derivatives

Derivatives not only affect the market risk but also counterparty risk measured within the

calculation of RWA related to the credit risk. DHB uses derivatives to manage interest rate and

currency risks on an ongoing basis.

Counterparty risk is the risk that DHB’s counterparts in a derivative contract defaults prior to

maturity of the contract and that DHB at that time has a claim on the counterpart.

As per year-ends of 2014 and 2013, the main sources of counterparty risk were currency swap

and interest rate swap.

DHB uses the mark-to-market method to calculate the exposure value according to the credit risk

framework in CRR. Counterparty credit exposure comprises the sum of current exposure

(replacement cost) and potential future exposure. The potential future exposure is an estimate

that reflects possible changes in the market value of the individual contract during the remaining

life of the contract, and is measured as the notional principal amount multiplied by a risk weight.

The size of the risk weight depends on the contract’s remaining lifetime and the underlying asset.

The Bank applies limits to mitigate counterparty risk similar to any other credit risk. In addition,

the Bank enters into collateral agreements with all major counterparties.

Credit exposures by exposure class and geographyat 31 December 2013, Euro (1,000)

NetherlandsOther

EuropeTurkey CIS Others TOTAL

Sovereign 120,007 2,099 - - - 122,106

Banks 64,893 157,392 203,061 153,417 147,205 725,968

Corporates 15,415 165,282 519,781 74,069 60,871 835,418

Retail 4,612 18,173 10,848 - - 33,633

Exposure secured on real estate property 2,754 6,659 579 - 22 10,014

Past due items 101 1 666 - - 768

Other items 6,485 8,152 - - - 14,637

Total Credit Exposures 214,267 357,757 734,936 227,487 208,098 1,742,545

Exposures*RWA

(Basel III)Capital

requirement Exposures*

RWA(Basel II)

Capital requirement

Interest rate contracts 3,082 1,655 132 9,764 2,380 190 Foreign exchange contracts 2,816 671 54 24,408 2,570 206 Other contract - - - TOTAL 5,898 2,326 186 34,172 4,950 396

2014 2013Derivative Contracts Euro (1,000)

*The exposures represent the credit exposure to derivative transaction after taking account of legally enforceable netting agreements and collateral arrangements

22

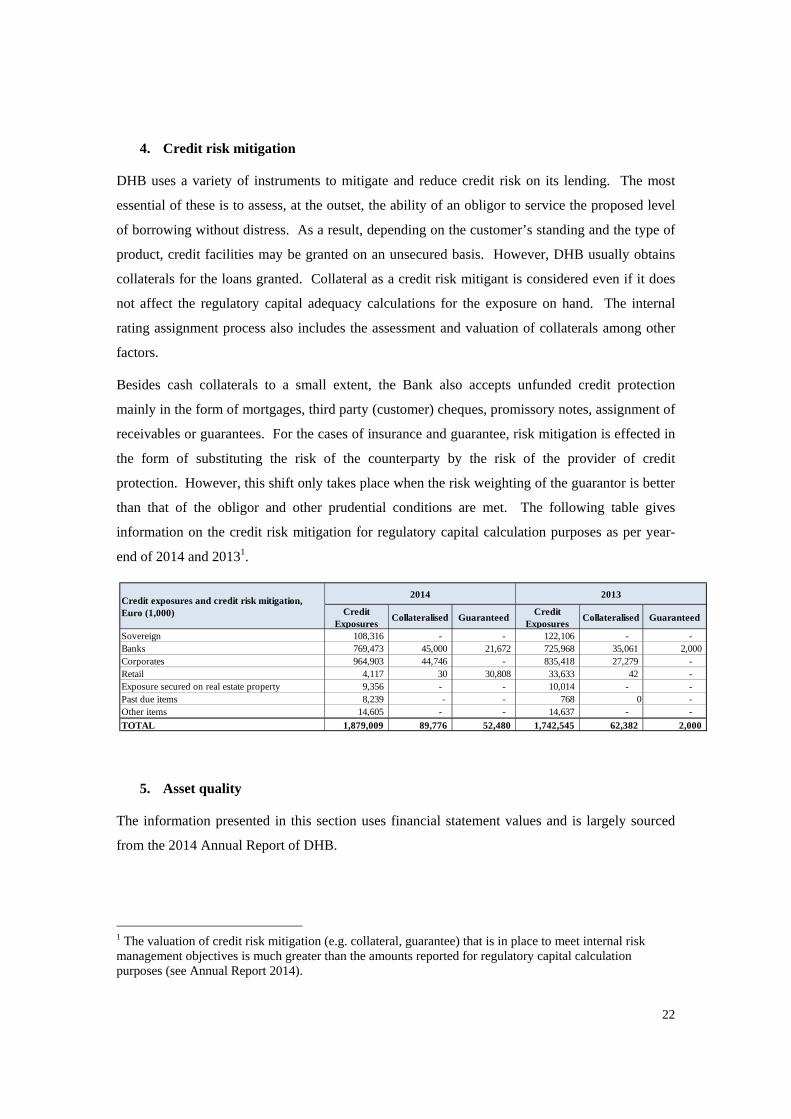

4. Credit risk mitigation

DHB uses a variety of instruments to mitigate and reduce credit risk on its lending. The most

essential of these is to assess, at the outset, the ability of an obligor to service the proposed level

of borrowing without distress. As a result, depending on the customer’s standing and the type of

product, credit facilities may be granted on an unsecured basis. However, DHB usually obtains

collaterals for the loans granted. Collateral as a credit risk mitigant is considered even if it does

not affect the regulatory capital adequacy calculations for the exposure on hand. The internal

rating assignment process also includes the assessment and valuation of collaterals among other

factors.

Besides cash collaterals to a small extent, the Bank also accepts unfunded credit protection

mainly in the form of mortgages, third party (customer) cheques, promissory notes, assignment of

receivables or guarantees. For the cases of insurance and guarantee, risk mitigation is effected in

the form of substituting the risk of the counterparty by the risk of the provider of credit

protection. However, this shift only takes place when the risk weighting of the guarantor is better

than that of the obligor and other prudential conditions are met. The following table gives

information on the credit risk mitigation for regulatory capital calculation purposes as per year-

end of 2014 and 20131.

5. Asset quality

The information presented in this section uses financial statement values and is largely sourced

from the 2014 Annual Report of DHB.

1 The valuation of credit risk mitigation (e.g. collateral, guarantee) that is in place to meet internal risk management objectives is much greater than the amounts reported for regulatory capital calculation purposes (see Annual Report 2014).

Credit Exposures

Collateralised GuaranteedCredit

ExposuresCollateralised Guaranteed

Sovereign 108,316 - - 122,106 - - Banks 769,473 45,000 21,672 725,968 35,061 2,000 Corporates 964,903 44,746 - 835,418 27,279 - Retail 4,117 30 30,808 33,633 42 - Exposure secured on real estate property 9,356 - - 10,014 - - Past due items 8,239 - - 768 0 - Other items 14,605 - - 14,637 - -

TOTAL 1,879,009 89,776 52,480 1,742,545 62,382 2,000

2014 2013Credit exposures and credit risk mitigation, Euro (1,000)

23

An assessment is made at each balance sheet date to test whether there is objective evidence that

a specific financial asset or group of financial assets may be impaired (‘loss event’).

Developments that lead to loss events may include:

- A breach of contract, such as default in the payment of interest or principal;

- Significant financial difficulty of the issuer or obligor;

- Restructuring of the loan where a concession is granted due to the borrower’s financial

difficulty.

If such evidence exists, an impairment loss is recognized in the statement of income.

An indication of the overall credit quality of DHB’s financial assets can be derived from the table

below as per year-ends of 2014 and 2013.

The creditworthiness of the customers that are not rated by external rating agencies is assessed

with reference to the Bank’s internal credit rating system. The internal rating is based on many

factors derived from both financial and non-financial assessments of the borrower. The internal

rating system is an essential tool for managing and monitoring the credit risk for the Bank.

The assessment and administration of past due and impaired loans, write-offs and provisions fall

under the responsibilities of the credit risk management units and the Credit Committee.

Provisions are set aside for estimated losses in outstanding loans for which there is doubt about

the borrower’s capacity to repay the principal and/or interest. Provision amounts are determined

through a combination of specific reviews, historical data and estimates. Provisions for loan

losses are determined separately for each exposure for wholesale loans, and according to a pre-

defined model for retail loans.

Provisions against a particular impaired loan may be released when there is improvement in the

quality of the loan. The Bank’s write-off policies are determined on a case-to-case basis. For

Asset Quality Euro (1,000) 2014 2013

Neither past due nor impaired 1,869,689 1,730,036

Past due and/or impaired 27,025 23,757

of which impaired 26,029 23,137

Provisions (17,706) (11,248)

Total 1,879,008 1,742,544

24

restructured loans, the policy enables reclassification of a restructured loan into a performing loan

when a certain number of repayments are executed.

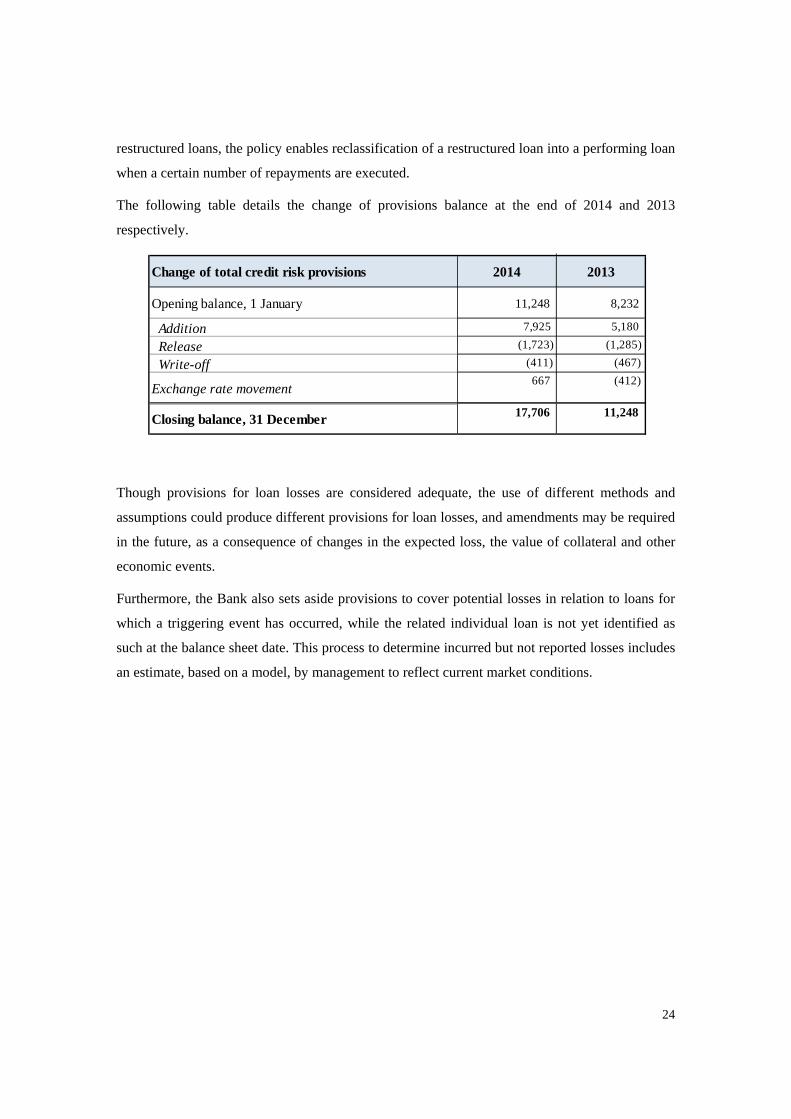

The following table details the change of provisions balance at the end of 2014 and 2013

respectively.

Though provisions for loan losses are considered adequate, the use of different methods and

assumptions could produce different provisions for loan losses, and amendments may be required

in the future, as a consequence of changes in the expected loss, the value of collateral and other

economic events.

Furthermore, the Bank also sets aside provisions to cover potential losses in relation to loans for

which a triggering event has occurred, while the related individual loan is not yet identified as

such at the balance sheet date. This process to determine incurred but not reported losses includes

an estimate, based on a model, by management to reflect current market conditions.

Change of total credit risk provisions 2014 2013

Opening balance, 1 January 11,248 8,232

Addition 7,925 5,180

Release (1,723) (1,285)

Write-off (411) (467)

Exchange rate movement 667 (412)

Closing balance, 31 December 17,706 11,248

25

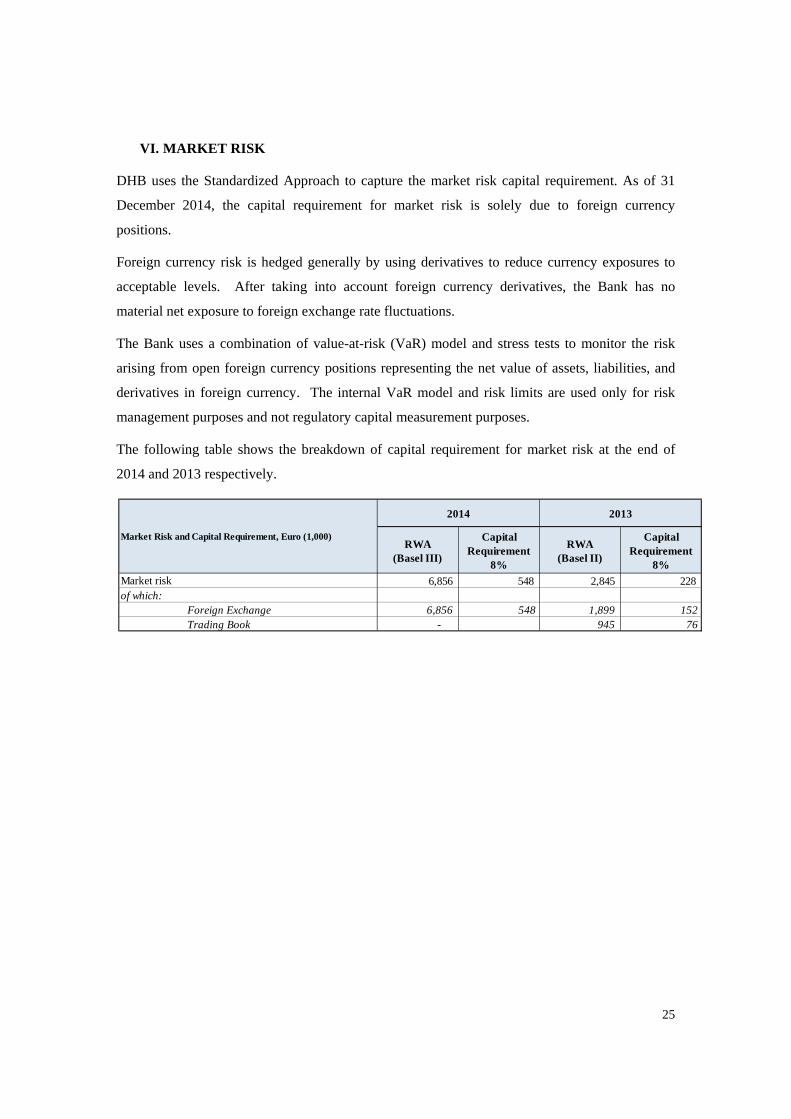

VI. MARKET RISK

DHB uses the Standardized Approach to capture the market risk capital requirement. As of 31

December 2014, the capital requirement for market risk is solely due to foreign currency

positions.

Foreign currency risk is hedged generally by using derivatives to reduce currency exposures to

acceptable levels. After taking into account foreign currency derivatives, the Bank has no

material net exposure to foreign exchange rate fluctuations.

The Bank uses a combination of value-at-risk (VaR) model and stress tests to monitor the risk

arising from open foreign currency positions representing the net value of assets, liabilities, and

derivatives in foreign currency. The internal VaR model and risk limits are used only for risk

management purposes and not regulatory capital measurement purposes.

The following table shows the breakdown of capital requirement for market risk at the end of

2014 and 2013 respectively.

RWA(Basel III)

Capital Requirement

8%

RWA(Basel II)

Capital Requirement

8%

6,856 548 2,845 228 of which:

Foreign Exchange 6,856 548 1,899 152Trading Book - 945 76

Market risk

2014 2013

Market Risk and Capital Requirement, Euro (1,000)

26

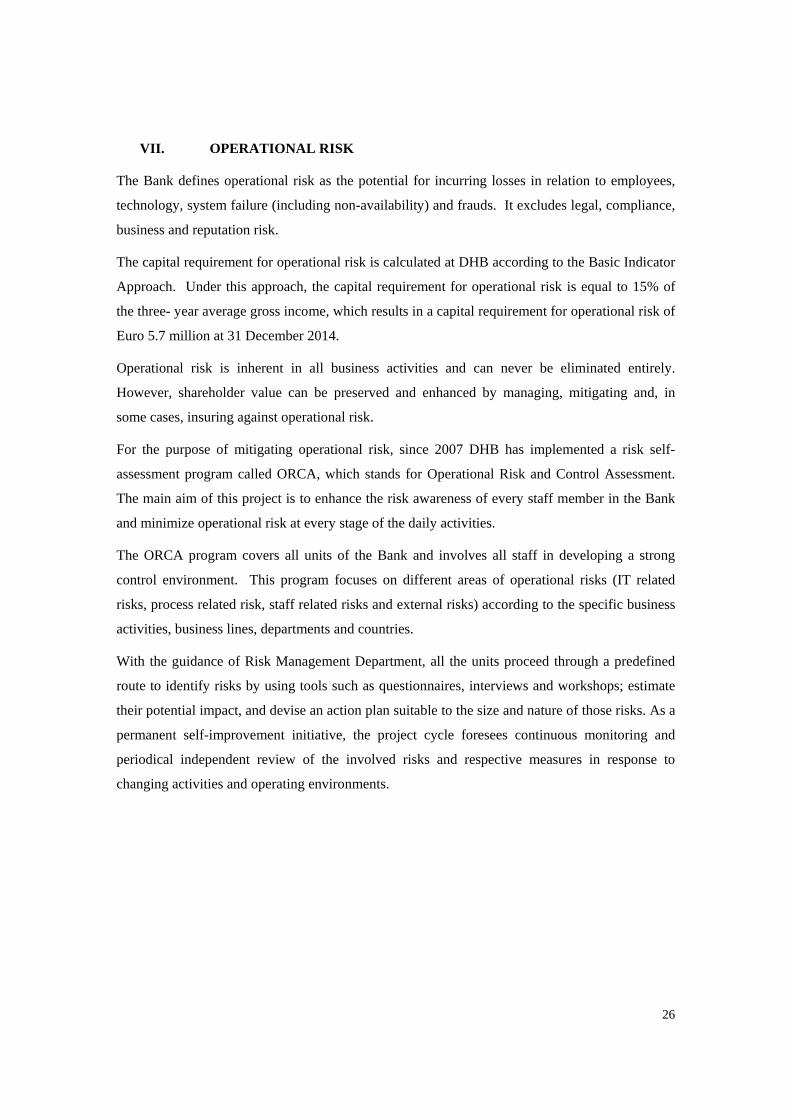

VII. OPERATIONAL RISK

The Bank defines operational risk as the potential for incurring losses in relation to employees,

technology, system failure (including non-availability) and frauds. It excludes legal, compliance,

business and reputation risk.

The capital requirement for operational risk is calculated at DHB according to the Basic Indicator

Approach. Under this approach, the capital requirement for operational risk is equal to 15% of

the three- year average gross income, which results in a capital requirement for operational risk of

Euro 5.7 million at 31 December 2014.

Operational risk is inherent in all business activities and can never be eliminated entirely.

However, shareholder value can be preserved and enhanced by managing, mitigating and, in

some cases, insuring against operational risk.

For the purpose of mitigating operational risk, since 2007 DHB has implemented a risk self-

assessment program called ORCA, which stands for Operational Risk and Control Assessment.

The main aim of this project is to enhance the risk awareness of every staff member in the Bank

and minimize operational risk at every stage of the daily activities.

The ORCA program covers all units of the Bank and involves all staff in developing a strong

control environment. This program focuses on different areas of operational risks (IT related

risks, process related risk, staff related risks and external risks) according to the specific business

activities, business lines, departments and countries.

With the guidance of Risk Management Department, all the units proceed through a predefined

route to identify risks by using tools such as questionnaires, interviews and workshops; estimate

their potential impact, and devise an action plan suitable to the size and nature of those risks. As a

permanent self-improvement initiative, the project cycle foresees continuous monitoring and

periodical independent review of the involved risks and respective measures in response to

changing activities and operating environments.

27

VIII. PILLAR 2 RISKS

1. Interest rate risk in the banking book (IRRBB)

Interest rate risk inherent in the banking book consists of exposures deriving from the balance

sheet and is measured in several ways in accordance with the financial supervisory authority’s

guidelines. The IRRBB is monitored and controlled both from a value perspective (such as using

the duration of equity and PV01 measure) and from an income perspective (sensitivity in net

interest income, NII)2.

Through its management of interest rate risk, DHB aims to hedge the effect of prospective

interest rate movements that could reduce its future net interest income, while balancing the cost

of such hedging activities on the current net revenue stream.

Regarding the income perspective, NII is exposed to external factors such as yield curve

movements and competitive pressure. The NII risk depends on the overall business profile,

especially mismatches between interest-bearing assets and liabilities in terms of volumes and

repricing periods. The IRRBB is minimized as the Bank’s rate sensitive assets and liabilities are

mostly floating rate, where duration is lower. In general, DHB aims to use matched currency

funding and usually converts fixed rate instruments to floating rate to better manage the duration

in the asset book.

The following tables indicate the Bank’s interest rate sensitivities in the banking book from the

income perspective at the end of 2014 and 2013 respectively. It is notable that the interest

sensitivity results are based on the regulatory assumption that the level of interest rates after

downward rate shocks do not fall below zero percent.

2 Non-maturity interest rate sensitive assets and liabilities are bucketed in the short term. The bank’s equity is considered a non-interest sensitive component and is excluded from the interest rate risk computations.

200 bp decrease 200 bp increase

EURO 436 ‐1,012

US Dollar ‐176 ‐262

Other ‐18 ‐30

TOTAL 242 ‐1,304

NII sensitivities by major currencies

at 31 Dec 2014, Euro (000)

Interest rate shock of +/‐ 200 bp

28

In addition to the regular monitoring of the interest rate risk using the above mentioned metrics,

on a monthly basis DHB performs stress testing to calculate the immediate net effect on the fair

value (FV) of a range of parallel shocks in rates, by currency. Furthermore, the Bank reports

PV01 to measure changes in economic value resulting from a one basis point (0.01%) parallel rise

in interest rates. The PV01 measure incorporates the entire rate sensitive segment of the balance

sheet for the Bank and is classified into appropriate buckets.

As per the regulatory requirements, interest rate risk reporting also include the measurement of

the ‘outlier criterion’, which refers to the maximum loss of market value expressed as a

percentage of capital base in the event of a parallel rate hike or drop of 200 basis points. The

‘outlier criterion’ is subject to a limit of 20%. The following tables show a range of severe

interest rate shocks with positions at the end of 2014 and 2013 respectively. At 31 December

2014, the standard instantaneous parallel shock (decline) of 200 bps leads to a potential decrease

of Euro 5.7 million, or 2.6% of the capital base. In term of the outlier criterion, the Bank’s

interest rate risk position increased somewhat in 2014 to a risk level that is generally considered

low in view of the abovementioned 20% threshold.

200 bp decrease 200 bp increase

EURO 4,609 2,951

US Dollar 759 ‐1,100

Other 12 ‐87

TOTAL 5,380 1,764

NII sensitivities by major currencies

at 31 Dec 2013, Euro (000)

Interest rate shock of +/‐ 200 bp

Fair value sensitivity to interest rate

shocks at 31 Dec 2014, Euro (000)‐300 ‐200 ‐100 +100 +200 +300 PV01

Euro 8,265 5,504 2,749 ‐2,743 ‐5,480 ‐8,212 ‐27

USD 584 362 167 ‐139 ‐251 ‐335 ‐2

Other 25 18 9 ‐10 ‐21 ‐32 0

TOTAL 8,874 5,884 2,925 ‐2,892 ‐5,752 ‐8,579 ‐29

Capital base 225,743

Standard 200 bps shock as % of

capital‐2.55%

Fair value sensitivity to interest rate

shocks at 31 Dec 2013, Euro (000)‐300 ‐200 ‐100 +100 +200 +300 PV01

Euro ‐49 32 48 ‐112 ‐289 ‐530 ‐2

USD 3,297 2,087 988 ‐877 ‐1,643 ‐2,299 ‐8

Other 92 63 33 ‐35 ‐72 ‐111 0

TOTAL 3,340 2,182 1,069 ‐1,024 ‐2,004 ‐2,939 ‐10

Capital base 223,559

Standard 200 bps shock as % of

capital‐0.90%

29

2. Liquidity risk

Liquidity risk is the risk of being able to meet liquidity commitments only at increased cost or,

ultimately, being unable to meet obligations as they fall due.

Liquidity risk is categorized into two risk types - funding liquidity and market liquidity:

a. Funding liquidity risk occurs when the Bank cannot fulfill its obligations as they come

due without incurring excessive losses. Payments have to be executed on the day when

they are due, or the Bank is declared illiquid if it fails to perform.

b. Market liquidity risk occurs when the Bank is unable to sell specific assets without losses

in price.

In the aftermath of the global financial crisis, regulators have introduced stricter supervisory

guidelines in many areas, notably in the Netherlands, with regard to liquidity standards. The

Netherlands is also among the first country in the EU that has started to monitor and observe the

local (Dutch) banks’ compliance plan with Basel III.

The liquidity and funding position of DHB in 2014 comfortably met the requirements. The

Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) are well above the

expected future regulatory requirements of 100%.

Furthermore, DHB has also carried out an internal liquidity adequacy assessment process

(ILAAP) based on DNB’s ILAAP Policy Rule and submitted the required documentation to DNB

for purposes of supervisory review and evaluation process (SREP). The internal process,

governance and consultative dialogue with the regulatory supervisory body required to meet the

ILAAP rules are similar to the ICAAP mentioned above.

Policy statements that are part of the ILAAP package stipulate that DHB’s liquidity management

reflects a conservative attitude towards liquidity risk. The Bank defines the liquidity risk appetite

by setting limits for applied liquidity risk measures. The most central measure is the Survival

Horizon, which defines the risk appetite by setting a minimum survival of 3 months under a

combination of bank-specific and market-wide stress scenarios with limited mitigation actions3.

Furthermore, to ensure funding in situations where DHB is in urgent need of cash and the normal

funding sources do not suffice, the Bank holds a liquidity buffer that consists of ECB eligible

debt securities and highly liquid assets.

3 The stress scenario used to measure compliance with the risk appetite framework includes among others an assumption of saving deposit outflows amounting to respectively 30%, 40% and 50% in one-month , three-month and six-month periods along with significant haircuts on the bank’s liquidity buffer.

30

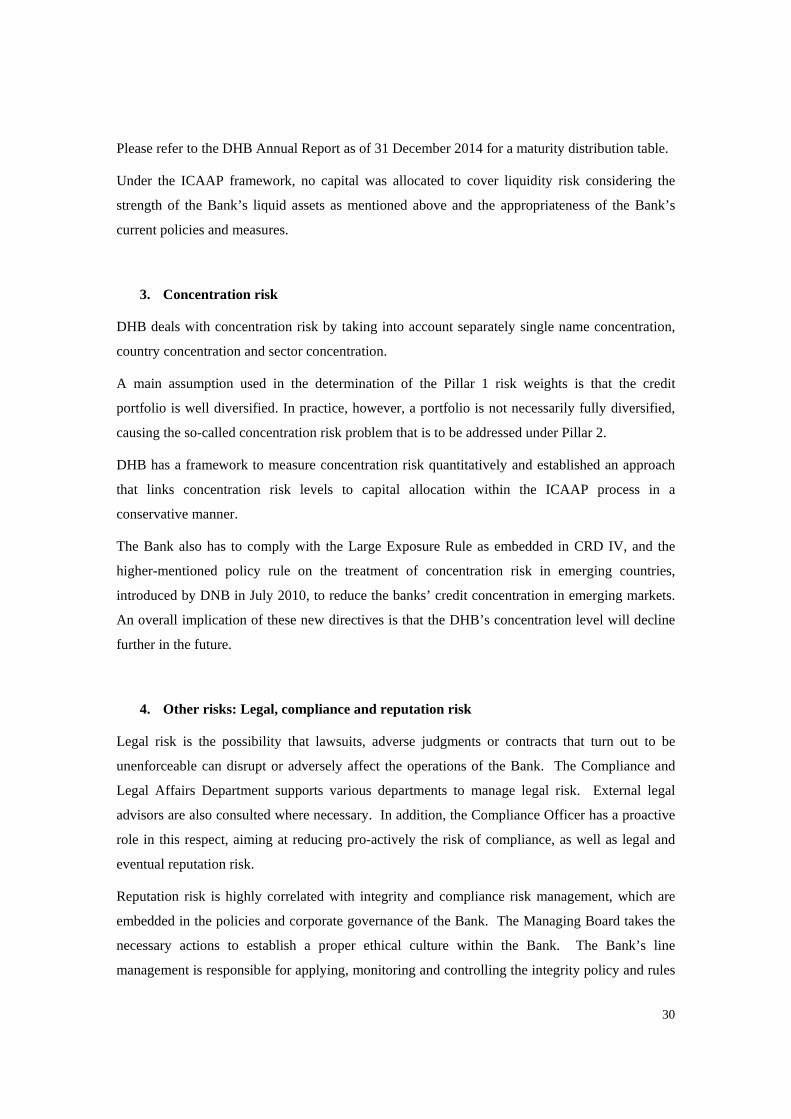

Please refer to the DHB Annual Report as of 31 December 2014 for a maturity distribution table.

Under the ICAAP framework, no capital was allocated to cover liquidity risk considering the

strength of the Bank’s liquid assets as mentioned above and the appropriateness of the Bank’s

current policies and measures.

3. Concentration risk

DHB deals with concentration risk by taking into account separately single name concentration,

country concentration and sector concentration.

A main assumption used in the determination of the Pillar 1 risk weights is that the credit

portfolio is well diversified. In practice, however, a portfolio is not necessarily fully diversified,

causing the so-called concentration risk problem that is to be addressed under Pillar 2.

DHB has a framework to measure concentration risk quantitatively and established an approach

that links concentration risk levels to capital allocation within the ICAAP process in a

conservative manner.

The Bank also has to comply with the Large Exposure Rule as embedded in CRD IV, and the

higher-mentioned policy rule on the treatment of concentration risk in emerging countries,

introduced by DNB in July 2010, to reduce the banks’ credit concentration in emerging markets.

An overall implication of these new directives is that the DHB’s concentration level will decline

further in the future.

4. Other risks: Legal, compliance and reputation risk

Legal risk is the possibility that lawsuits, adverse judgments or contracts that turn out to be

unenforceable can disrupt or adversely affect the operations of the Bank. The Compliance and

Legal Affairs Department supports various departments to manage legal risk. External legal

advisors are also consulted where necessary. In addition, the Compliance Officer has a proactive

role in this respect, aiming at reducing pro-actively the risk of compliance, as well as legal and

eventual reputation risk.

Reputation risk is highly correlated with integrity and compliance risk management, which are

embedded in the policies and corporate governance of the Bank. The Managing Board takes the

necessary actions to establish a proper ethical culture within the Bank. The Bank’s line

management is responsible for applying, monitoring and controlling the integrity policy and rules

31

in their units, and reports to the Managing Board and the Compliance Officer. As a third line of

defense, the Internal Audit Department also evaluates integrity issues in particular and

compliance issues in general during its regular and specific audits.

32

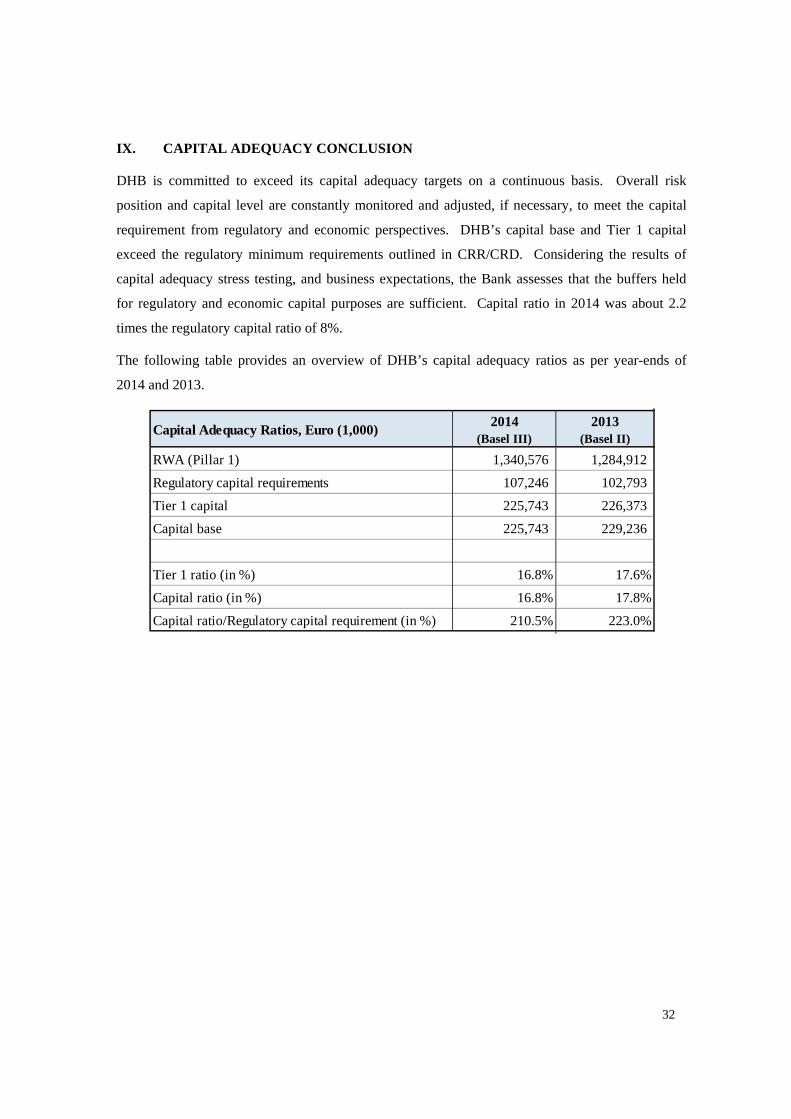

IX. CAPITAL ADEQUACY CONCLUSION

DHB is committed to exceed its capital adequacy targets on a continuous basis. Overall risk

position and capital level are constantly monitored and adjusted, if necessary, to meet the capital

requirement from regulatory and economic perspectives. DHB’s capital base and Tier 1 capital

exceed the regulatory minimum requirements outlined in CRR/CRD. Considering the results of

capital adequacy stress testing, and business expectations, the Bank assesses that the buffers held

for regulatory and economic capital purposes are sufficient. Capital ratio in 2014 was about 2.2

times the regulatory capital ratio of 8%.

The following table provides an overview of DHB’s capital adequacy ratios as per year-ends of

2014 and 2013.

Capital Adequacy Ratios, Euro (1,000)2014

(Basel III)2013

(Basel II)

RWA (Pillar 1) 1,340,576 1,284,912

Regulatory capital requirements 107,246 102,793

Tier 1 capital 225,743 226,373

Capital base 225,743 229,236

Tier 1 ratio (in %) 16.8% 17.6%

Capital ratio (in %) 16.8% 17.8%

Capital ratio/Regulatory capital requirement (in %) 210.5% 223.0%