Embed Size (px)

Citation preview

Building Institutional

Capacity and

International

Enrollment through

Public-Private

Partnerships

NACUBO Annual Meeting July 2012

Presenters

Andrew Colin

Chairman

INTO University Partnerships

Amy Parsons

Vice President for University Operations

Colorado State University

Nick Setteducato

Exec. Director for Financial Management & Resource Planning

Academic Affairs, University of South Florida

Brian Thorsness

Director of Business Services

Oregon State University

Challenging Times for Universities

• Funding and regulatory issues

• Increased student expectations

• New entrants and new strategies

• The challenge of institutional

development – adapting to changing

circumstances

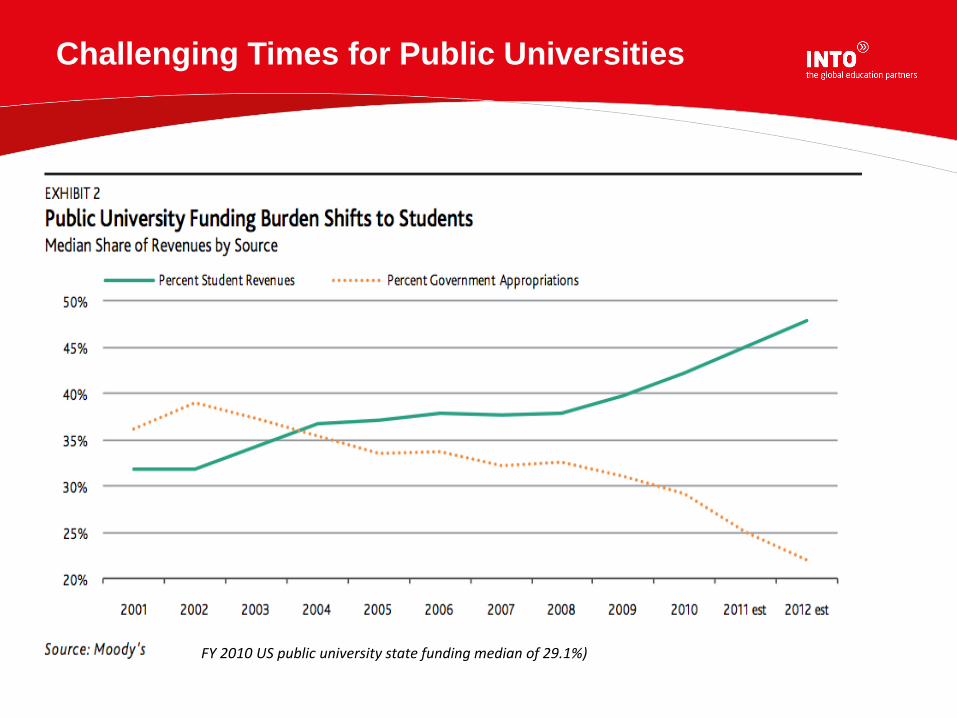

Challenging Times for Public Universities

FY 2010 US public university state funding median of 29.1%)

Why Enhance International Enrollment?

• Provide new, independent revenue streams

• Enhance the quality of the college experience

• Provide a more global perspective

• Expand the university brand globally

• Maximize best use of resources and best practices

• and provide new, independent revenue streams

Megatrends Shaping Supply and Demand

Globalization Demand for quality

education Global policy

contexts

Unrealized power of HE brands

Technological Change

Employment Preparation

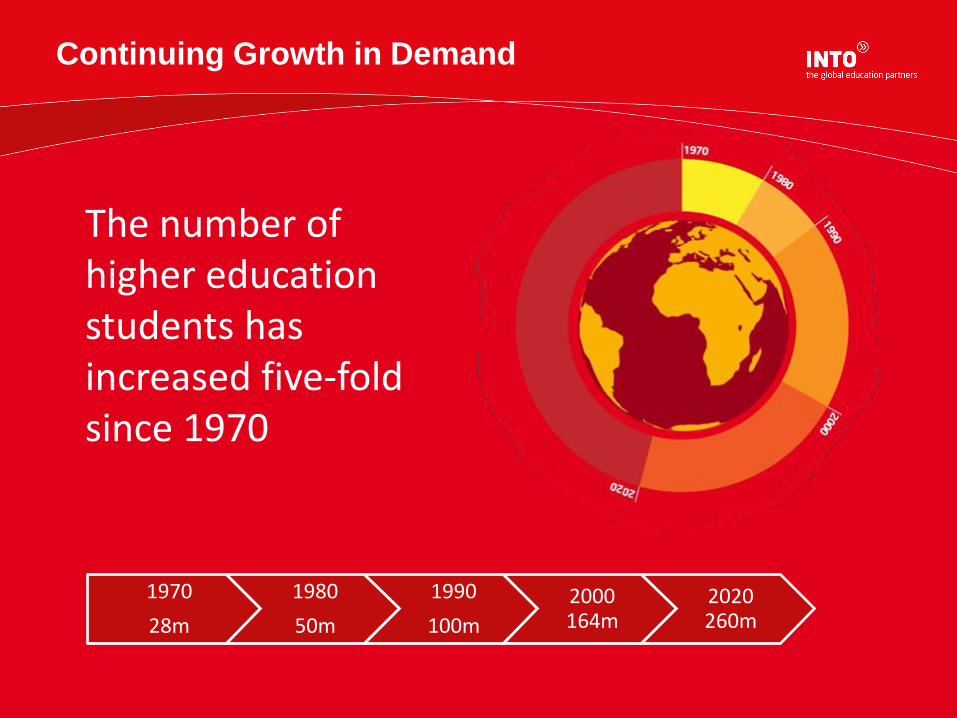

The number of higher education students has increased five-fold since 1970

Continuing Growth in Demand

1970

28m

1980

50m

1990

100m

2000 164m

2020 260m

In 1975, there were 800,000

students studying outside their own country

By 2020, there are projected to

be over 7,000,000

International Mobility

Strategic Options to Internationalize Enrollment

9

• Short term

• Loss of competitive edge

• Opportunity cost

Do Nothing DIY • Limited reach

• Scarce resources

• Lack of institutional buy-in

Outsource • Short term

• Risk to reputation

• Tactical NOT strategic

Partner

• Complementary assets

• Shared investment

• Shared risk • Shared reward

About INTO

Through innovative

partnerships with

leading universities,

we expand

opportunities for

higher education,

ensuring success

and transforming

the lives od our

students and staff.

Unique Public-Private Partnership Model

Joint Venture with leading universities

that offers

• Common academic principles

• A flexible business model

• 50/50 equity and risk

Deeply embedded

partnerships that engage

and benefit the entire

university long term

The INTO Model

Shared Global Partner Network

Senior Management Team

Internationally Recognized Education Professionals

Growth of the INTO Network

Providing capacity building solutions to 15 partner universities since 2006

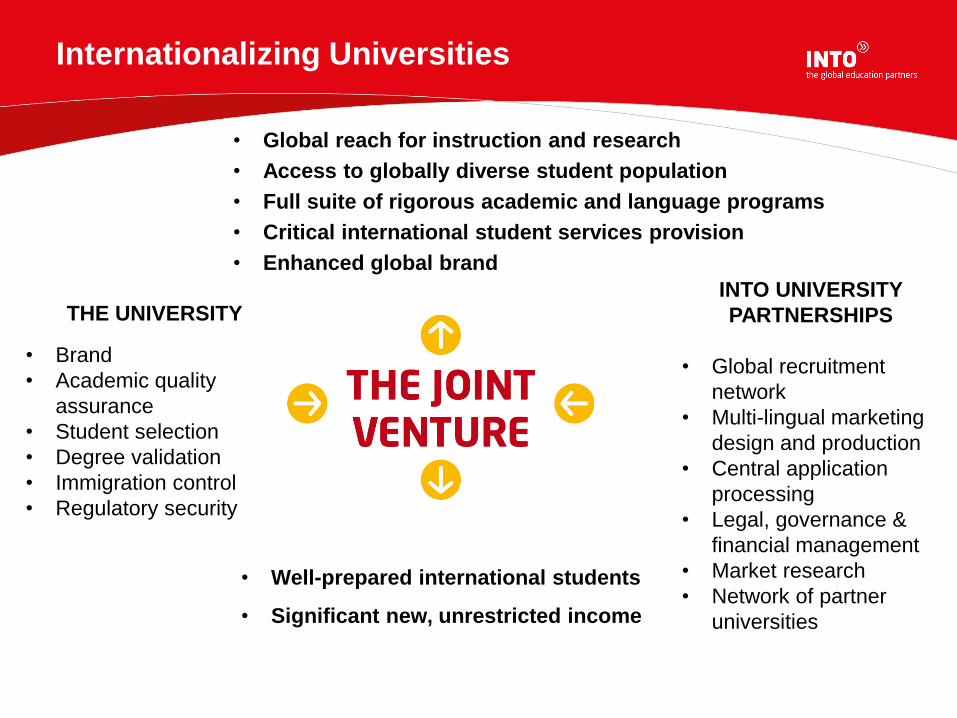

Internationalizing Universities

• Global reach for instruction and research

• Access to globally diverse student population

• Full suite of rigorous academic and language programs

• Critical international student services provision

• Enhanced global brand

• Well-prepared international students

• Significant new, unrestricted income

INTO UNIVERSITY

PARTNERSHIPS

• Global recruitment

network

• Multi-lingual marketing

design and production

• Central application

processing

• Legal, governance &

financial management

• Market research

• Network of partner

universities

THE UNIVERSITY

• Brand

• Academic quality

assurance

• Student selection

• Degree validation

• Immigration control

• Regulatory security

THE INTO OSU EXPERIENCE

Internationalization at Oregon State

OSU’s Commitment to Internationalization • Goals and Vision

• 2008 Strategic Plan

• Recruitment Efforts • Grow International Population from 4.5% to 10%

• Reality • Internal Effort Too Costly

• Partnership Model

• Why INTO University Partnerships?

• Partnership Advantages • Global Network • Investment

275 308

399

468

624 593

710

776

85 114

155 184

145 151

270 278

11

68 83

141 172 169 184

360

433

622

735

910 916

1149

1238

0

200

400

600

800

1000

1200

1400

Fall 2009 (A) Spring 2010(A)

Fall 2010 (A) Spring 2011(A)

Fall 2011 (A) Spring 2012(A)

Fall 2012 (F) Spring 2012(F)

English

UG PW

Grad PW

Total

Snapshot Historical Performance & Forecast

|------Projected--------|

* Note: TOEFL entry requirement for UG Pathway was raised from 475 to 500 in Fall 2011. This change required many

students to take at least one term of Academic English prior to Pathway start, resulting in decreased PW and increased AE.

Progression Statistics & Predictions

Actual after 3 terms Predicted with 3+ terms

All INTO-OSU Pathway Students 61% (target 60-70%) 80% (exceeds target 60-70%)

UG Pathway 69% 85%

Grad Pathway MEng 60% (predicted*) 78%

Grad Pathway MBA 55% (predicted*) 77%

• 4.3% International Student Population

• Goal: Reach 10% by 2014 2008

• 8% International Student Population

• Reached 80% of Goal after only 3 years 2012

* Grad PW students are taking GRE and GMAT tests this summer.

The Partnership Model

Revenue Flow

INTO OSU

Oregon State University

OSU Student Services

Tuition and Fees from INTO OSU students

IUP: Supplies Mktng, other resources & receives 50% of surplus

OSU: Supplies academic programs, facilities, & receives 50% of surplus

OSU Colleges

OSU profits are reinvested in the University, not in the INTO OSU Center. ¾ of the surplus goes

directly to OSU academic colleges and

¼ goes to OSU student support units.

Focus for the Future

• Achieving closer integration with OSU

• Assuring academic quality and brand

• Integration of students

• Opportunities for domestic students

• New $52M living-learning center

• Updates to programs

• Admissions

• Embracing the network

• Assisting with Direct Admits

THE INTO USF EXPERIENCE

• Why Internationalization?

• USF Background

• Options considered

• Challenges

• Experience since start

• Successes

Consideration of a joint venture model

Why Internationalization?

USF’s strategic plan includes targets for an increase in the international student population in order to be better aligned with globally competitive institutions

Qualitative and quantitative metrics supporting:

1. Recruiting the best and brightest intellectual talent

2. Enhancing the quality and relevance of education at USF

3. Enhancing USF’s global reach

4. Providing for an economic stimulus for our community

5. Alternative revenue generation for reinvestment in the university

Background: The University of South Florida

• Three campuses: Tampa (Main Campus including USF Health), St. Petersburg, and Sarasota-Manatee

• > 47,000 students system-wide

• Carnegie-Designated Research University (Very High Research Activity), Community Engaged

• 27th Top American Research Universities (TARU)

• Economic impact $3.7bn

• Ranked 44th total research expenditures

• Awarding 11,000+ degrees annually

• 212,000 alumni in all 50 states and 124 nations

• Common dilemma of reduced state appropriations

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

UF * FIU UCF USF FSU

Source: International Edcuational Exchange (IIE) Open Doors database, 2008-09 data

4% of total student

population

9%

of total student

population

5% of total student

population

8% of total student

population

4% of total student

population

Background: International Students USF vs. State University System Peers

(2008-09)

What options were considered?

1. Invest in internal international recruitment located in Tampa – Cost prohibitive – Effectiveness questionable without local presence in country

2. Invest in internal international recruitment with presence in key international locations coordinated centrally from Florida – In addition to the issues cited above:

• Logistics • Lack of expertise

3. Third-party options: – Outsource expertise

• If only to compliment internal options cited above, the above barriers still pertain

– Public-private partnership with established presence and results

• Allows USF to focus on its core strengths

• Removes reliance upon public funding for out-of-state enrollment growth

• Short list included INTO_UP who was recognized as the most reputable and effective leader in this business model

Why INTO?

• Proven, powerful international recruiting model and regional network

• Several very successful JV’s already in existence at the time:

– 9 in UK – Oregon State in the US

• Planned future growth is centered within the US market

• Represented an opportunity for USF to get in on ‘bottom floor’ of their US expansion (Particularly in the Southeast region)

• Provided for a public/private partnership (i.e., 50% / 50% ownership) thereby creating potentially “fungible profits”

Successes

• Growing, integrated and engaged international student base

• Refreshing, dynamic and synergistic relationship

• Ahead-of-plan rates: Progression-to-degree-seeking / graduation rates: Over 275 student have matriculated from pathways to USF degree programs since inception in Fall 2010

Over 20 ‘former’ pathway students have graduated from their degree program

• Initial investments have ‘paid back’ ahead of plan: – Tuition funds are flowing back to colleges for instruction – Profits from partnership are accumulating for strategic use – More full fee paying internationals at USF (30% increase)

• JV is operating at profit ahead of planned timing

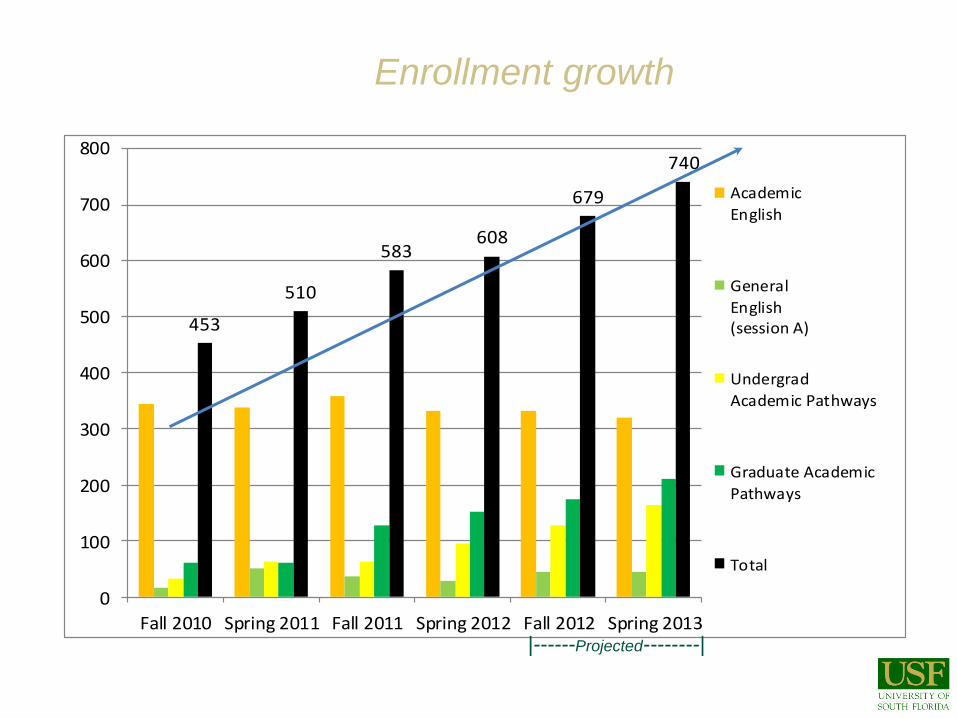

Enrollment growth

453

510

583608

679

740

0

100

200

300

400

500

600

700

800

Fall 2010 Spring 2011 Fall 2011 Spring 2012 Fall 2012 Spring 2013

Academic

English

General

English(session A)

Undergrad

Academic Pathways

Graduate Academic

Pathways

Total

|------Projected--------|

Challenges

• Creating the separation contractually and operationally

• Integrating systems and facilitating reporting needed – Tracking charges between USF and INTO USF – Communication and Processes

• Immigration and cultural challenges

• Providing ‘fast track’ processing for Admissions – Streamlined Application – Pre-screening – Outsourcing transcript evaluation

• General ‘growing pains’ – Staffing

– Academic progression

– Balancing private and public expectations

– Interim facilities vs. permanent

Looking to the future

• Continued growth expected

• Steady-state of organization staffing

• New International center on campus

• Continued innovations in joint recruiting and marketing

• Demographic distribution

• Customization and “niche” programs

• Win-win for both partners

THE INTO CSU EXPERIENCE

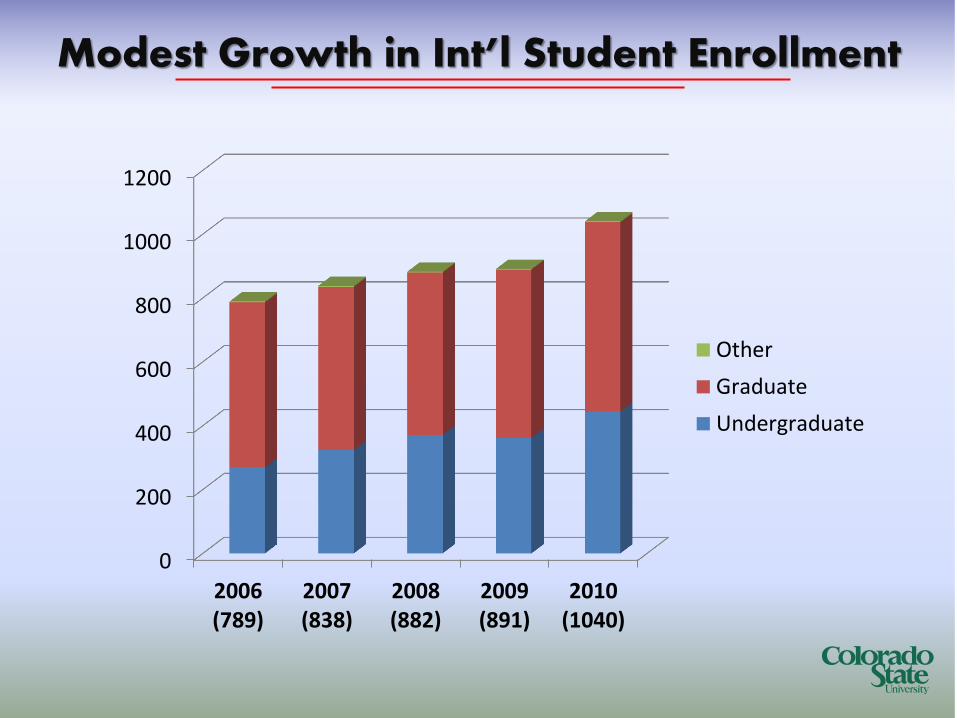

0

200

400

600

800

1000

1200

2006(789)

2007(838)

2008(882)

2009(891)

2010(1040)

Other

Graduate

Undergraduate

Modest Growth in Int’l Student Enrollment

Potential for Significant Growth International Students

as a Percent of the Total Student Population

______________________________________________________________________________________________________________________________________________________

Purdue University 15%

Iowa State University 11%

Michigan State University 11%

Texas A & M University 9%

North Carolina State University 8%

Ohio State University 8%

Oklahoma State University 8%

Oregon State University 8%

Washington State University 6%

Colorado State University 4%

University of California, Davis 4%

INTO’s Proposal to CSU INTO proposes the establishment of a long-term joint venture partnership with Colorado State University to develop a state-of-the-art international student center called INTO Colorado State University to support and expand the University’s comprehensive internationalization agenda

The partnership will have three key objectives:

1. To accelerate the internationalization of Colorado State University by increasing the quality, quantity, diversity and sustainability of the international student population.

2. To enhance the probability of success for international students to matriculate to, actively participate in and successfully complete CSU’s mainstream undergraduate and graduate degree programs by providing a wide range of academic pathways and English language programs.

3. To raise CSU’s global profile and yield significant financial returns to CSU by driving and sustaining revenue growth from non-resident tuition.

INTO CSU

May, 2011 Exploration of INTO Partnership

Oct., 2011 Signed MOU

Feb., 2012 Familiarization Visit

Signed Partnership Agreement

Recruitment Begins

Aug., 2012 First Students to Arrive at CSU

Jan., 2013 Projected Enrollment: 375

Alder Hall

Spruce Hall

INTO University Partnerships

IN SUMMARY

Positive Student Outcomes

90% overall student satisfaction

163% growth 2007/08 - 2011/12 (to date)

New Enrollments

30

2562

4177

5017

6004

6753

0

1000

2000

3000

4000

5000

6000

7000

8000

2006/7 2007/8 2008/9 2009/10 2010/11 2011/12(ytd)

University Impact

Financial Impact

Be

Success for partners

The additional revenue from our partnership with INTO has allowed us to invest in 75 new members of our tenure track faculty and support staff to complement those hires this year and next.

Mark McCambridge Vice-President for Finance and Administration

Oregon State University

QUESTIONS?

Please do not hesitate to contact us directly with questions

David Stremba Managing Director, North America [email protected]

Keep in touch