Embed Size (px)

Citation preview

Candidates should be able to define short-run aggregate supply and identify the determinants of the short-run AS curve, such as money wage rates, business taxation and productivity.

Real national output

Price level

SRAS

Y1

P1

Y2

P2

Price level – because we are now looking at the average price for all goods and

services not just one product

Price level – because we are now looking at the average price for all goods and

services not just one product

This is the value of the output of all the goods and services

produced in the given time period. The ‘real’ means the numbers are

adjusted for inflation

This is the value of the output of all the goods and services

produced in the given time period. The ‘real’ means the numbers are

adjusted for inflation

We could use Q for quantity

here. Y stands for national income and because the

value of output is the same as

national income many texts use

a Y

We could use Q for quantity

here. Y stands for national income and because the

value of output is the same as

national income many texts use

a Y

Short run is the Period the time period when at least one factor of production is fixed in supply

Short run is the Period the time period when at least one factor of production is fixed in supply

Real national output

Price level

SRAS

Y1

P1

Y2

P2

The AS (or SRAS) curve is the summation of all the individual supply curves of each firm which all slope upwards because, other things being equal, a higher price means higher profits and it is the profit motive, we assume, that motivates firms.

The AS (or SRAS) curve is the summation of all the individual supply curves of each firm which all slope upwards because, other things being equal, a higher price means higher profits and it is the profit motive, we assume, that motivates firms.

Real national output

Price level

SRAS 1

Q1

P1

SRAS 2

Q2

A change in:

•costs of raw materials,•money wages,•Productivity, •taxes on businesses,

moves the whole SRAS curve

A change in:

•costs of raw materials,•money wages,•Productivity, •taxes on businesses,

moves the whole SRAS curve

Real national output

AS

Yfe

Price level

P1

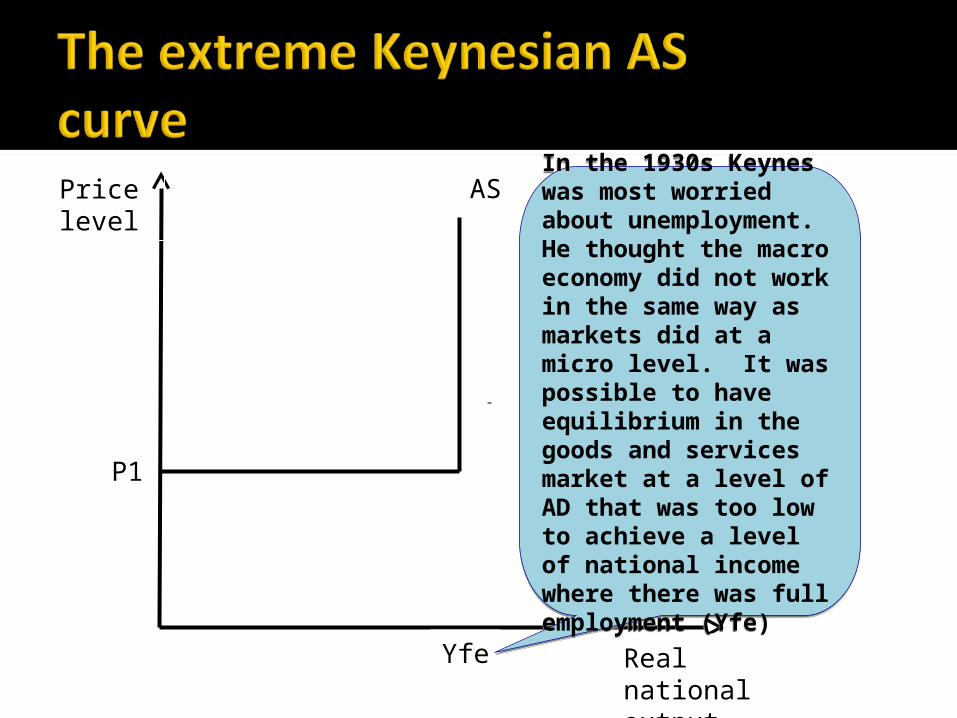

In the 1930s Keynes was most worried about unemployment. He thought the macro economy did not work in the same way as markets did at a micro level. It was possible to have equilibrium in the goods and services market at a level of AD that was too low to achieve a level of national income where there was full employment (Yfe)

In the 1930s Keynes was most worried about unemployment. He thought the macro economy did not work in the same way as markets did at a micro level. It was possible to have equilibrium in the goods and services market at a level of AD that was too low to achieve a level of national income where there was full employment (Yfe)

Real national output

AS

Yfe

Price level

AD1 AD3AD2

P1

Y1 Y2

P3

Keynesians saw AS as perfectly elastic. As AD increases, supply increases until Yfe is achieved (i.e. the economy is on the PPF). Any increase in AD beyond Yfe is inflationary as AS becomes perfectly inelastic.

Keynesians saw AS as perfectly elastic. As AD increases, supply increases until Yfe is achieved (i.e. the economy is on the PPF). Any increase in AD beyond Yfe is inflationary as AS becomes perfectly inelastic. Yfe is the

full-employment level of national income

Yfe is the full-employment level of national income

Real national output

AS

Yfe

Price level

AD1 AD3AD2

P1

Y1 Y2

P3

P2

As output increases spare capacity is reduced and ‘bottlenecks’ in production occur, output can still increase but the prices of the factors of production are bid up too. So AS gradually curves upwards Beyond Yfe the economy is on the PPF and an increase in AD just results in price increases.

As output increases spare capacity is reduced and ‘bottlenecks’ in production occur, output can still increase but the prices of the factors of production are bid up too. So AS gradually curves upwards Beyond Yfe the economy is on the PPF and an increase in AD just results in price increases.

Real national output

AS

Yfe

Price level

AD1 AD3AD2

P1

Y1 Y2

P3

P2

Real national output

LRASPrice level

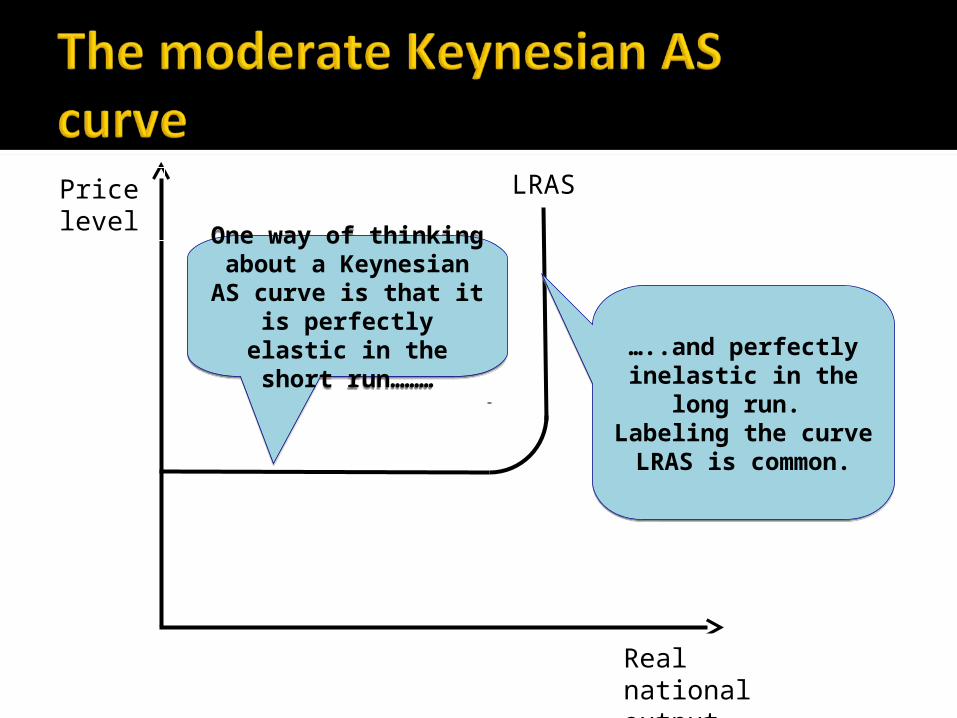

One way of thinking about a Keynesian

AS curve is that it is perfectly elastic in the short run………

One way of thinking about a Keynesian

AS curve is that it is perfectly elastic in the short run………

…..and perfectly inelastic in the

long run. Labeling the curve LRAS is

common.

…..and perfectly inelastic in the

long run. Labeling the curve LRAS is

common.

Real national output

LRAS

Yfe

Price level

Real national output

LRAS

Yfe

Price level

Free market economists believe in “Say’s Law”, meaning “supply creates its own demand”. In the long run markets always achieve equilibrium and so AS is perfectly inelastic.

Free market economists believe in “Say’s Law”, meaning “supply creates its own demand”. In the long run markets always achieve equilibrium and so AS is perfectly inelastic.

We might call these

economists “SUPPLY SIDERS”

We might call these

economists “SUPPLY SIDERS”

Real national output

LRAS

Yfe

Price level

Free market economists believe in “Say’s Law”, meaning “supply creates its own demand”. In the long run markets always achieve equilibrium and so AS is perfectly inelastic.

Free market economists believe in “Say’s Law”, meaning “supply creates its own demand”. In the long run markets always achieve equilibrium and so AS is perfectly inelastic.

Real national output

Yfe

Price level

AD3

AD2

AD1

P1

P2

P3

Any increase in AD merely leads to a higher price

level.

Any increase in AD merely leads to a higher price

level.

LRAS

Real national output

Yfe

Price level

AD3

AD2

AD1

P1

P2

P3

LRAS

Real national output

LRAS

Yfe

Price level

AD3

AD2

AD1

P1

P2

P3

Real national output

SRAS

Yfe

Price level

AD3

AD2

AD1

P1

P2

P3

A few new classical

economists even used to say SRAS

is vertical and because of

rational expectations any

increase in government

spending immediately

causes prices to rise.

A few new classical

economists even used to say SRAS

is vertical and because of

rational expectations any

increase in government

spending immediately

causes prices to rise.

This sometimes get changed to the “NATURAL RATE OF UNEMPLOYMENT” which is a monetarist idea

This sometimes get changed to the “NATURAL RATE OF UNEMPLOYMENT” which is a monetarist idea

Real national output

SRASPrice level

A neo-classical/Keynesian consensus

Real national output

SRAS

Price level

A neo-classical/Keynesian consensus

LRAS

Yfe

Real national output

Price level

SRAS 1

Y2

P1

SRAS 2

Y1

AD

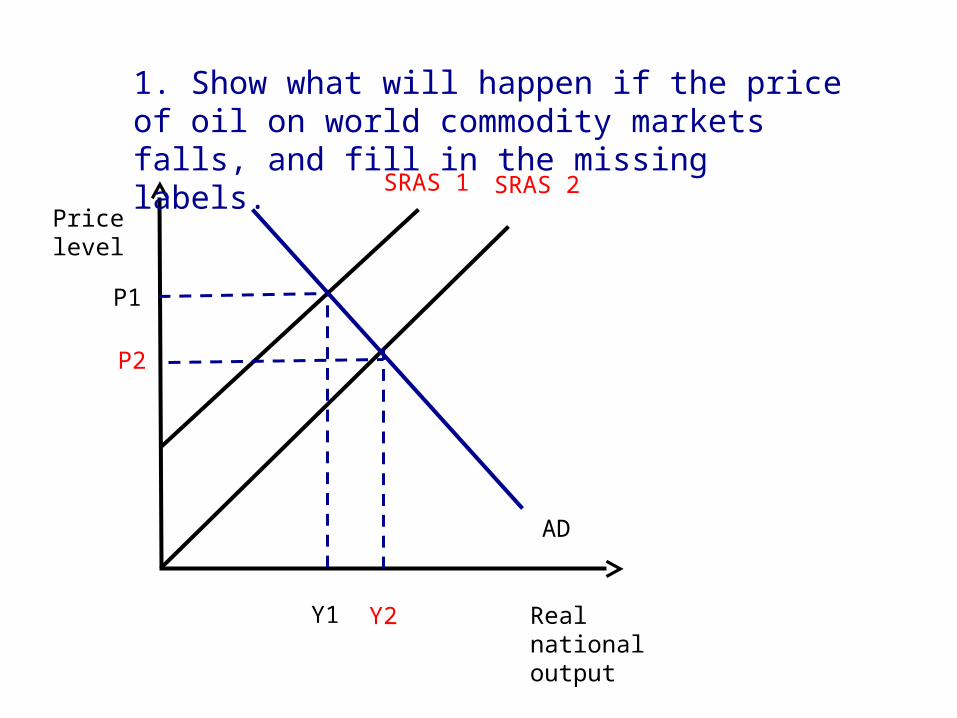

1. Show what will happen if the price of oil on world commodity markets falls, and fill in the missing labels.

P2

Real national output

Price level

P1

Y1

AD

Show what will happen if the price of oil on world commodity markets falls, and fill in the missing labels.

P2

Using a Monetarist/Free market LRAS curve show what will happen if the level of government spending increases.

Real national output

Price level

Using a Monetarist/Free market LRAS curve show what will happen if the level of government spending increases.

Real national output

Price level

Using a Keynesian AS curve show what will happen if the economy is currently in a slump and the level of government spending increases.

Actual GDP

Trend Growth

Short-run growth – percentage change in actual GDP

Long-run growth – the productive potential of the economy increases (shown by the trend line)

Actual GDP

Trend Growth

HYSTERISIS occurs when a recession/depression leads to a loss of skills and deterioration in infrastructure and capital so that the productive potential is harmed and the rate of long-run growth is reduced

PPF1 PPF2

Real National Income

Pricelevel Short-run growth –

percentage change in actual GDP

Long-run growth – the productive potential of the economy increases.

LRAS1 LRAS2

Real National Income

Pricelevel

Actual GDP

Trend Growth =productive potentialof the economy

Negative output gap

Positive output gap

A positive output gap occurs when actual GDP is greater than potential GDP.

A negative output gap occurs when actual GDP is less than potential GDP.

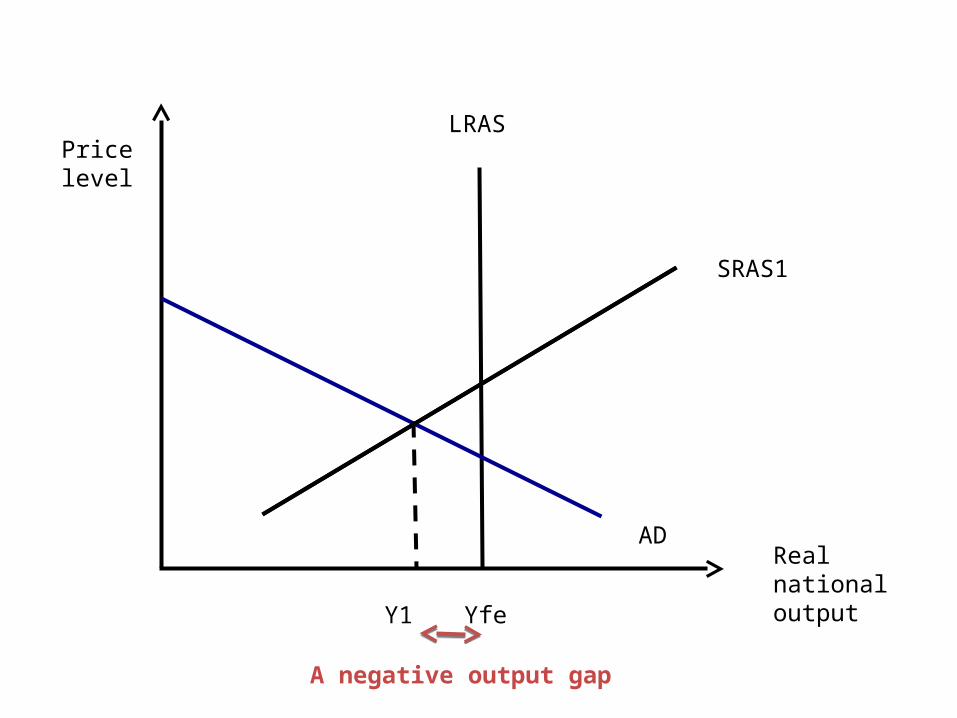

Real national output

LRAS

Yfe

Price level

SRAS1

AD

Y1

A negative output gap

Real national output

LRAS

Yfe

Price level

SRAS1

AD

Y2

A positive output gap

SRAS2

(unsustainable in the LR)

AS Macroeconomics

LRAS1

Real National Income

Pricelevel

LRAS2

Supply-side policies are policies that improve the productive potential / capacity of an economy.

Supply-side policies can be implemented by the public or the private sector.

•Competition policy including privatisation/nationalisation. Deregulation and regulation.

•Policies aimed at stimulating entrepreneurship and the expansion of smaller businesses

•Labour market reforms including tax and benefit changes, migration policy

•Trade policies including membership of the EU single market and WTO commitments •Policies designed to increase spending on investment and research

The key supply-side concepts to focus on are incentives, enterprise, technology, mobility, flexibility and efficiency.

•Improve incentives to find work

•Increase labour and capital productivity •Increase the occupational and geographical mobility of labour •Increase capital investment and R&D spending by firms •Promote competition and stimulate invention and innovation •Provide a platform for sustained non-inflationary growth of an economy

http://bcove.me/5l5u6fre

In Oct 2008, lone parents had move onto JSA and look for work once their youngest child reached the age of 12 rather than 16.

In Oct 2010, lone parents had to switch toJobseekers Allowance (JSA) even earlier, to when their youngest child is seven

Evaluation is it in the long-term interest of society’s well-being to encourage single mothers to leave their children so early on in their childhood?

That’s all