Embed Size (px)

Citation preview

Cancer:The Challenge Goes CommercialAN EXPLORATION OF THE FORCES SHAPING THE ONCOLOGY MARKET

After three decades of research and development, advances incancer therapy are at last rekindling the hope that swelled in1972 when U.S. President Richard Nixon declared a war onthe scourge of cancer. He predicted,“…there will not beany single cure, it will not come suddenly…but wheneverand wherever the answers come, they are going to representthe final steps of a long journey.”1 We may still be many stepsfrom the end of that journey, but recent scientific break-throughs in targeted agents, oral delivery and even cancervaccines have propelled us a great distance along the path.

This revolution — and the accompanying surge in newproduct development — are creating a treatment landscapethat will fundamentally change the economics of theoncology marketplace.

The crux of the matter is that targeted therapies aresplintering the market into narrower segments.Thus, evenfor cancers causing significant mortality and morbidity, newproducts target relatively small numbers of patients.And inorder to expand a product’s indication to other types ofpatients or other tumor types, companies must makesubstantial investments in additional clinical trials. It istherefore not surprising that research companies shouldseek a premium price that reflects not only the innovationquotient of the molecule, but also the investment cost ofmultiple clinical studies with uncertain outcomes.

That said, new molecules introduced over the past sevenyears have more than realized their initial clinical potentialand also addressed new segments and tumor types. Demandhas, therefore, expanded faster than predicted, making itincreasingly difficult for payers to finance the growth.However, relief may be on the way for payers.As moremolecules come to the market (and seven new oncologyproducts are predicted for 2007) payers will eventually havealternatives from which to choose, leading to more com-petitive pricing.And, over the next five years, four currentoncology blockbusters will go off patent, easing payers’extremely difficult task of developing cost/benefit parametersto guide their spending. Another option for payers is todemand higher levels of performance in terms of remissionand survival in order for a drug to qualify for reimbursement,or even to sustain the launch price over time.

It is ironic that just as theclinical battle against cancer is being won, companies mustnow fight a fresh battle on thecommercial front.

1U.S. President Richard M. Nixon remarks to a National Cancer Conference in Los Angeles, CA, September 28,1972.

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 1

Thus, the oncology class is finally reaching the sameinflection point already seen in other classes. Oncologyproducts now face commercial risks that are separate fromtheir clinical risks, and companies will find it vastly morechallenging to make the economics work. Manufacturers’success in this market will depend upon how they set theirindication strategy, determine and support their price andmanage the needs of the various stakeholders involved.

It is ironic that just as the clinical battle against cancer isbeing won, companies must now fight a fresh battle on thecommercial front.

FACING A DRASTIC REAPPRAISAL The economic evolution within the oncology market isprovoking a debate that strikes at the heart of societalethics…the fundamental constructs that govern a State’scommitment to providing healthcare…and the valuepropositions making a consensus between the pharmaceuticalindustry and other stakeholders in healthcare possible.And asseen in HIV/AIDS, patients will be instrumental in shapingthe consensus which must be sought.

The ethical issue concerns whether a payer — increasinglythe State (even in the U.S.) — has the right to restrict accessto life-saving or life-extending medications, and whether thecriteria for determining access are rational and defensible.This question has been faced before, but not in connectionwith a range of potentially lethal diseases such as cancer.

The fundamental construct around access to healthcare,first embedded in the Beveridge Report published in theU.K. just after WWII and adopted to some extent by mostdemocracies, demands equality of access. It has been abusedfrequently, but the question now is whether cancer repre-sents the tipping point at which the “contract” between the payer (usually the State) and society will have to berewritten. Karol Sikora, Professor of Cancer Medicine atImperial College London, has recently commented thatcancer may become a chronic disease by 2020. As cancerpredominantly afflicts the elderly, this achievement wouldextend life expectancy, increasing the total healthcareburden and amplifying the debate over the nature andextent of a payer’s financial commitment.

The pharmaceutical industry’s concern is that artificialconstraints on the uptake of innovative medicines will

diminish returns and hinder further investment in intractablediseases where the risks of R&D failure are especially high.Consider stroke, for example — a devastating and frequentlylethal event with a significant cost for rehabilitating survivors.For the past 30 years, the industry has persevered withexpensive research in the hope of a breakthrough and nothad a single success. It is hardly surprising that the industryshould feel aggrieved when payers respond to breakthroughs(such as those in several of the most prevalent cancers) byrestricting patient access.

This article will explain why we have reached this tippingpoint, bring the current commercial issues to light andsuggest in broad terms what manufacturers must nowconsider as they develop oncology products and bringthem to market in a very uncertain environment.

ENTERING A GOLDEN AGE OF ONCOLOGYIn 2005, the President of the American Society of ClinicalOncology (ASCO) announced that cancer therapy wasentering a “golden age.” The past 30 years of research anddevelopment, which had yielded only a few breakthroughsuntil the late 1990’s, have finally started to pay off.

In the past eight years, three specific breakthroughs havedone more than change the way cancer is treated — theyhave changed the way we think of the disease itself. In 1998,Genentech introduced Herceptin® to treat metastatic breastcancer. The first targeted therapy supported by a specificdiagnostic test, Herceptin has revolutionized treatment of the 20-25% of breast cancers that are HER2-positive.

The second was Gleevec®, an oral therapy for chronicmyeloid leukemia, launched in 2001 by Novartis. Gleevecopened the possibility of treating the disease through long-term maintenance therapy.“Gleevec allowed us to think ofa cancer as a chronic illness, rather than a life-ending one,”remarks Dr. Pierre Anhoury, IMS Director, Pricing andMarket Access. “It thus has significance far beyond thescope of just treating leukemia.”

And the latest development embraces a key principle ofpublic health, i.e., vaccination.With the HPV vaccines,Gardasil®, which launched in 2006, and Cervarix®, whichshould launch in 2007, the industry has attacked the rootcause of a disease in the cancer spectrum for the first time,making a form of cancer preventable. Anhoury continues,

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 2

“Preventing the disease itself has been the ‘holy grail’ ofmedical science, and now it’s achievable.”

The result here is a dramatic consensus among all stake-holders: through the industry’s innovation, scientific advancesare indeed winning individual battles against the disease.Medical experts suggest that this is just the beginning, withscience poised for a huge leap forward in bringing continuedimprovement in treatment outcomes. Specifically, optimismsprings from our understanding of genetic factors and sub-cellular biology as well as improvements in diagnostictechnology and chemoprevention.

A PROFILE OF THE ONCOLOGY MARKET TODAY AND TOMORROWA few facts suffice to paint the oncology market ascomplex, dynamic and positively burgeoning with growth:

• Cancer consists of more than 200 different diseases andultimately affects one in three persons.The most commonlyoccurring cancers are those of the lung, breast and colon(See Figure 1) and it is these tumors that recent productlaunches have addressed.

• The global incidence of cancer is forecast to grow by 50 percent between 2000 and 2020 due to the prioritythat government healthcare policies give to cancerdetection and treatment.

• The size of the oncology market has more than doubledin the past five years, reaching $31 billion in 2006.

• Seventy-seven percent of today’s oncology sales arederived from products launched in the past 10 years.Recent growth is largely driven by targeted therapies suchas Herceptin in breast cancer,Avastin® and Erbitux® in coloncancer, and Gleevec in chronic myeloid leukemia, whileTarceva® is driving growth in non-small cell lung cancer.Apart from advances such as these in major tumor types,drugs like Alimta®, Sutent® and Nexavar® are broadeningthe range of tumors responsive to chemotherapy, thuspromoting further growth.The HPV vaccines, Cervarixand Gardasil, will help to drive growth still further.

• Globally, the oncology class is now growing three timesfaster than the pharmaceutical market as a whole and isforecast to become the dominant pharmaceutical businesssector by 2010. (See Figures 2 and 3)

• Ten major pharmaceutical companies currently accountfor about 75 percent of global oncology sales.As manyother companies are about to enter the market withexciting new compounds, it is very unlikely that thecancer market will remain as concentrated.

FIGURE 1: INNOVATION IN THE PAST 10 YEARS HASFOCUSED ON CANCERS WITH THE HIGHEST MORBIDITIES

CANCER INCIDENCE

Source: GLOBOSCAN 2002, published September 2005

FIGURE 2: GLOBAL ONCOLOGY SALES GROWING ATMORE THAN THREE TIMES THE GLOBAL PHARMA RATE

Source: IMS MIDAS, MAT JUNE 2006

200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,0000

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 3

THE UNSTOPPABLE MARCH OF PROGRESSGiven recent scientific advances, there is an inexorableprocess at work: established players and new entrants areinvesting heavily in new product development, especially in biologically-led, targeted therapy.The oncology pipelineis the richest in number and potential of any therapeuticcategory. (See Figures 4 and 5) Up to 55 New ChemicalEntities (NCEs) could enter the market within the nextfive years, some of which will lack clear differentiation interms of efficacy, toxicity and convenience.

Thus, the oncology market, which could never have beendescribed as crowded or competitive in the past, is about to become so.

FIGURE 4: THE ONCOLOGY SECTOR IS WITNESSING APERIOD OF UNPRECEDENTED R&D INVESTMENT

Size of bubbles = forecast sales 2009

Note: * = Growth of value sales

Source: IMS Health Consulting

CAGR

2004

-200

9*

R&D Activity in Main Therapeutic Areas

# PHASE II & ONWARDS PIPELINE PRODUCTS

FIGURE 3: GLOBAL GROWTH FORECAST IS TWICETHE RATE OF THE OVERALL PHARMA MARKET: $66 BILLION IN 2010

Source: IMS MIDAS, IMS Therapy Forecaster 2006 and IMS Health Consulting

FIGURE 5: SEVERAL MANUFACTURERS ARE MAKINGA SIGNIFICANT INVESTMENT IN ONCOLOGY

Note: *Includes vaccinesSource: IMS R&D Focus; IMS Knowledge Link; IMS Health Consulting

LEADING THERAPY CLASSES, 2005-2010

70

60

50

40

30

20

10

0

SALE

S(U

S$BI

LLIO

NS)

#PR

ODU

CTS

INDE

VELO

PMEN

T

NUMBER OF ONCOLOGY NCEs* IN LATE STAGE DEVELOPMENT BY COMPANY

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 4

THE UNINTENDED CONSEQUENCES OF PROGRESS Because the conquest of cancer has been an elusive goal ofinestimable value, payers have allowed manufacturers morepricing freedom than in other classes.To date, the industry’sability to charge a premium price for its oncology productshas correlated strongly with its ability to innovate.This hasbeen fortuitous because development costs have beenescalating with the need for more clinical trials to validateproduct efficacy.

Graham Lewis,Vice President, IMS Global Pharma Strategy,comments,“The industry has always assumed that oncologydrugs would be able to command high prices at launch and would remain relatively protected throughout theirlifecycles.” However, through a confluence of marketconditions occurring globally, the historical method forproduct valuation is about to be turned on its head.

Targeted therapies were designed to treat more finitesegments of the oncology population. However, empiricalexperience is demonstrating that, when used in combinationwith more systemic drugs, targeted therapies producebenefits across a wider range of patients within the firsttumor type approved, and subsequently in other tumortypes.The use of these drugs is shifting more quickly fromadvanced to early-stage treatment, while the expansion toother tumor types continues as before.

This “shift” has put more pressure on payers, so they havebegun to scrutinize the benefits derived from innovativetherapies more rigorously and to compare these benefits tothose gained in treating other diseases. Payers are makingthe comparison not because the diseases are similar, butbecause they are urgently seeking a new value paradigmthat will help them distribute their budgets more rationallyin an inherently irrational situation.

In retrospect, it is clear that all stakeholders miscalculatedthe consequences of recent rapid progress in extendingremission and survival.This had nothing to do with avarice

or inadequate intellect; it had everything to do with anassumption drawn from real-time experience.The assump-tion was that new drugs would mimic their predecessors,bringing marginal improvements to limited populationsubsets. On the basis of this assumption, pharmaceuticalcompanies set their pricing strategies and payers acceptedthem. Subsequent clinical experience has confoundedempirical reasoning.

IMPLICATIONS FOR MANUFACTURERS Of course, increased competition will heighten theimportance of manufacturers’ marketing competence.This is especially true since the key stakeholders are notincreasing numerically, so that only the best productswill be accessible. But perhaps less obvious — it will alsoaffect decisions made long before a product enters themarket, beginning with what indication to target first.Companies must choose the right point of entry for amolecule, given that some indications will be sharedwith competitors sooner rather than later.

“R&D companies may find that it is advantageous totake the ‘road less traveled’ to enjoy some exclusivity in the market,” suggests Dr. Simone Seiter, Principal,IMS Consulting.“They may be more interested in firstentering smaller, niche markets where the competitionis less fierce, and saving additional indications in thelarger markets for later.The marketing activities tosupport a niche product launch are far less intense than those needed in a major market wherecompetition already exists.”

In any event, companies must now think about wherethey launch, the sequence of successive launches andhow their products will be differentiated from others to command and sustain a premium price.

Through a confluence of market conditions occurring globally,the historical method for product valuation is about to be turnedon its head.

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 5

If this could have been foreseen, pharmaceutical companiesmay have opted for a different pricing model and payersmay have set alternative cost/benefit parameters. Now,the various stakeholders are pausing for thought andattempting to find a business model that is acceptable to all. Pharmaceutical companies are widely employingcompassionate use programs, payers are erecting barriers to access (which, unfortunately, has brought the legalprofession into the fray) and providers are caught betweentheir budget-holding masters, their patients’ desire for themost effective treatments, and their intellectual convictionthat the pharmaceutical industry actually is delivering.Thedilemma was summed up by an expert Oncologist at therecent European Society for Medical Oncology (ESMO)meeting in Turkey:

“This is not a straightforward cost containment issue.There arediscrepancies in cancer treatment outcomes both within andbetween different EU states in terms of access to top quality

surgery, radiotherapy, drugs and information.”

Professor Roberto LabiancaChair, ESMO MOSES Task Force

PAYERS FLEX THEIR MUSCLE The coffers are being emptied everywhere as payersstruggle to meet the growth in oncology sales with limitedbudgets.“We are reaching a point,” states Lewis,“wheneven the most liberal and sympathetic payers will have toapply price or access controls in order to make ends meet.”To illuminate the challenge that payers will face, considerthat if the two new HPV vaccines are adopted successfully,their peak sales will exceed the value of all vaccine sales inthe U.S. today!

In the E.U., health authorities have already been restrictingaccess to certain populations as a means of controlling theirdrug budgets. Figure 6 lists the type of access restrictions inplace within the E.U. for just four leading oncologytreatments.

And the situation is bound to get worse. At a 2006 con-ference held by Cambridge Pharma Consultancy, a Unit ofIMS, Dr. McCabe, former Director of the National Institutefor Health and Clinical Excellence (NICE) Decision SupportUnit in the UK, said,“Drug budgets will have to increasemarkedly if the oncology market is to continue expandingwith new products and new medications.This is at a time

FIGURE 6: IN PARTS OF EUROPE, PAYERS HAVE ALREADY TAKEN STEPS TO MANAGE ACCESS OF CERTAIN AGENTS

Gleevec

Herceptin

Avastin(in CRC)

Erbitux(in CRC)

Repeat Rx can only be made by certain

specialists

None

None

None

None

None

None

None

None

None

None None

None None

NICE has minor restrictions beyond label

Uneven take up despite NICE approval

Late stage BC - positive NICEreview took 2 yrs

Rejected by both NICE & theScottish Medicines Consortium

Rejected by both NICE & theScottish Medicines Consortium

> 6 month delaybetween EMEA

approval & launch

Price vol agreement,observational studies& prior authorizationIN

CREA

SING

PAYE

RM

ANAG

EMEN

T

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 6

when the National Health Service (NHS) budget is widelyexpected to plateau after 2007, which raises the distinctpossibility of market access restrictions and/or pricereductions in response to growing demand.”

“At the moment, pricing and market access limitations area country-by-country affair,” explains Anhoury.“But in thefuture they will take the form of a Europe-wide effort thatis centrally coordinated. This will start with oncology andthen move to other therapeutic categories.”

In the U.S., payers are still recommending “appropriate use,”rather than applying restrictions, but they may well followthe E.U.’s lead in time.Traditionally, U.S. health plans hadneither the motivation nor the means to manage oncologypricing.Almost all expenditures were administered throughMedicare Part B, with most oncology patients being elderlyand receiving therapy closely linked to physician services.Today, there are two shifts in the U.S. that will cause

additional scrutiny of oncology costs: first, the implemen-tation of Medicare Part D, and second, the influx of oraltherapies covered under this part of the Medicare plan.Whatwas previously a more stable situation — with most therapiesbeing reimbursed under Medicare Part B — is now becomingmore complex — with greater demand on payers to coveroral therapies under Medicare Part D.With new andinnovative therapies helping to turn cancer into a chronicdisease, patients are living longer, but they are also increasingthe cost of therapy and the pressure on plans to pay.

The budget drain is giving payers ample incentive to changethe way they manage their oncology expenses.And thegrowing number of therapy options presented by competitionwill support payers’ cost savings goals, giving them theleverage to insist on the least expensive alternative, or toforce patients to pay the difference.

IMPLICATIONS FOR MANUFACTURERSThe biggest challenge for manufacturers operating inthis new environment will be to get the price right atlaunch.“If you come out with a price that is higherthan the market will bear, you’ll be hit with accessrestrictions,” asserts Pamela Santoni, IMS SeniorPrincipal for Pricing.“Conversely, if you start with a

price that is too low, you’ll have to live with it. If youincrease your price later, you’ll risk alienating physicians.In the U.S., physicians are subsidizing price increases forproducts covered under Medicare Part B.”

It is probable that a high unmet need will no longer besufficient on its own to command a high price, andcompanies that base their pricing decisions on analoguesfrom the past — even the recent past — will make astrategic mistake.To justify premium pricing or achieveunfettered access, companies will need to demonstratethat their products deliver improved outcomes relative to competing products using metrics that matter most to each stakeholder.

“Typically, these would be proof of extended time torelapse or increased survival,” says Mike Aristides, IMSPrincipal, Health Economic and Outcomes.“Surrogateendpoints, such as tumor response will not be sufficientfor pricing and reimbursement negotiations. If NICE isthe bellwether, then health economics will also beimportant to justify access and uptake.” Indeed a meta-analysis across NICE deliberations and across all diseaseareas strongly suggests that the organization is usingfinancial benchmarks in its decisions. (See Figure 7)

Note: Includes vaccinesSource: IMS Consulting

FIGURE 7: NICE DECISIONS BY COST/QALY

* QALY = Quality Adjusted Life Years

Source: Presentation by Professor Sir Michael Rawlins, Chair, NationalInstitute for Health and Clinical Excellence. ‘A NICE time at NICE’.

PERC

ENT

REJE

CTED

COST PER QALY*

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 7

Although economic issues are still second to clinical ones inreimbursement decisions, the balance between the two willshift towards equilibrium.The proverbial writing appears tobe on the wall. Payers will come to use the same rationalefor determining payment with oncology drugs that theycurrently use in other therapy areas.We can expect thatpayers’ new philosophy will manifest itself in:

• Pricing limits, even in free-pricing markets.

• Restrictions on treatment initiation. Payers may requireevidence that a patient has failed to respond to existingtreatment before authorizing reimbursement for anothermore expensive therapy. Or, payers could make reimburse-ment dependent upon the results of specific tests verifyingthat a patient will respond to a given treatment.Theycould also limit reimbursement for off-label use of drugs.

• Restrictions on therapy continuation. Payers may requireclinical evidence that a product is actually reducing thesize of a tumor or insist that continued treatment bedependent on certain biological tests.Their decisioncriteria will increasingly depend on the availability ofsurvival as well as remission data.

“The big question is, of course, ‘When will it change?’ Itwon’t happen in the blink of an eye,” reasons Santoni.“Itwill happen gradually. A few aggressive payers will takeaction and others will follow. Plans will try things and they’llget push back from patient advocates and employers. Wecan expect to see many iterations without ever reaching asteady state.”

Two recent events, though, suggest that the industry isanticipating these events. Amgen has introduced its newcancer therapy,Vectibix™, at a 20 percent discount to itsnearest competitor, Erbitux.Two European governmentshave granted GlaxoSmithKline permission to introducetwo specific products at the company’s chosen price,subject to a contractual agreement that GlaxoSmithKlinewill undertake Phase IV studies to evaluate the agreedperformance parameters.The price may subsequently bemodified up or down. It is not known if the two productsare in the cancer arena, but from a payer’s perspective, this

modus operandi would work well in oncology because thenumber of patients who can be evaluated during theregulatory and pricing and reimbursement process is verysmall. Real-world experience can thus produce differentoutcomes from clinical trials, as evidenced by AstraZeneca’sIressa® which failed to demonstrate a survival benefit andwas even linked to patient deaths, following fast-trackapproval on the basis of tumor shrinkage.

IMPLICATIONS FOR MANUFACTURERS Companies must have a respected voice in stakeholderdeliberations concerning a rational access policy forinnovative compounds in the cancer space.The recentgrowth in the market has benefited pharma players inoncology, and the short-term outlook is also positive.However, there are many major companies with adisproportionately large part of their active pipeline in oncology and they and their investors have placedbets on a continuation of significant returns.

If payers change the game, and there are signs that they are doing so already, Pharma cannot stand by andwait for third-party decisions to determine their fate.Experience in other markets shows how damaging andunpredictable that can be, making effective planningvery difficult.

Some companies have already taken active steps tocounter rising public criticism of oncology drug prices.ImClone/BMS announced that it was reviewing a pricecap for Erbitux. Novartis announced its intent to provideGleevec to any patient that needed it, regardless ofinsurance status.And Genentech is considering acharitable trust to help disadvantaged patients with the cost of oncology treatment.

Companies must remember that public opinion isfickle.That can work for and against anyone looking to the public for support.

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 8

THE DEBATE BECOMES PUBLIC Since it affects patients, the price/access issue won’t bedebated and negotiated privately between the commercialparties involved; it is going to have a very public profile.This is apparent in the media coverage given the Herceptindecisions made in 2005 in the U.K. Following a very publicappeal by a patient to gain access to Herceptin, NICE issuedfinal guidance in September 2006 recommending thatHerceptin be used in early breast cancer and be paid for by the state health service. (See Figure 8)

Interestingly, the advent of targeted therapies has given theprice of treatment for which there is no alternative a newlevel of legitimacy.When there is a clear identification of a cancer type and a proven solution, there’s a strong moralobligation to find the money to pay for treatment. Europeangovernments have not always managed to do so and havehad to ration treatment to stay within their budgets, butpatients have been on firmer ground in fighting rationingdecisions.

The introduction of legal challenges and direct politicalintervention makes oncology an increasingly fraught arenafor all stakeholders, including pharma.

Already in the U.S., public opinion is beginning to questionthe price of oncology products, but when the solutionbecomes to delay or deny access to life-prolonging care,the public will respond with more than questions. For the industry, being in the spotlight is a two-edged sword:manufacturers are lauded as heroes for their discovery anddevelopment, and at the same time vilified for their pricingpractices in which they are held responsible for treatmentdenial or restricted access.

The only solution is to use health economics to define andproduce consistent and comparable criteria and to conductevaluations that can be scrutinized by all stakeholders.Thiswould allow some patients to pay for treatment even if thereis limited or no reimbursement, and however unpalatablethat would at least be a rational basis for decision making.At present this does not exist.

(Figure 9)

2002

NICE recommendsHerceptin be availablefor women with HER2positive advancedbreast cancer

North Stroke PrimaryCare Test rejects ElaineBarber’s appeal touse Herceptin onthe grounds thatthey are notconvinced of thedrug’s safety orcost-effectiveness

North Stroke PrimaryCare Test changes rulingthat rejected ElaineBarber’s appeal

Health Secretary PatriciaHewitt notes healthmanagers should not usecost as anexcuse forrefusing to give patientsHerceptin

NICE has committed toaccelerate its consideration ofHerceptin and publish itsguidance in October 2006

Decision on EuropeanMedicines Agency for a licensefor the use of Herceptin in thetreatment of early stagebreast cancer expected

Ann Marie Rogers losesher High Court battleover Swindon PCT’srefusal to fundHerceptin treatment

Herceptin portrayed in theUK popularmedia as a curefor breast cancer, skin to amiracle treatment

Women in the UK aredenied Herceptin for usein the early breast cancer anda number take this issue tothe courts

2004-2005 Oct 2005

Herceptin

The UK experience withHerceptin highlights thechallenges with a premium-priced therapy

What will be the global consequences of NICE’s recommendation onHerceptin?

Nov 2005 March 2006 Summer/Fall 2006

FIGURE 8: THE UK EXPERIENCE WITH HERCEPTIN HIGHLIGHTS THE CHALLENGES WITH A PREMIUM-PRICED THERAPY

What will be the global consequences of NICE’s recommendation on Herceptin?

Herceptin portrayed in theUK popular media as acure for breast cancer,akin to a miracletreatment

Women in the UK aredenied Herceptin for usein early breast cancer anda number take this issueto the courts

Ann Marie Rogers losesher High Court battle overSwindon Primary CareTrust’s refusal to fundHerceptin treatment

The European Commissionapproved Herceptin forearly-stage HER2-positivebreast cancer in May 2006

NICE recommendsHerceptin be available forwomen with HER2-positiveadvanced breast cancer

North Stoke Primary CareTrust rejects ElaineBarber’s appeal to useHerceptin on the groundsthat they are notconvinced of the drug’ssafety or cost-effectiveness

North Stoke Primary CareTrust changes ruling thatrejected Elaine Barber’sappeal

Health Secretary PatriciaHewitt notes healthmanagers should not usecost as an excuse forrefusing to give patientsHerceptin

Fulfiling its commitmentto accelerate considerationof Herceptin, NICE issuedits guidance in August2006 (recommendingHerceptin as a treatmentoption for early-stageHER2-positive breastcancer after surgery and chemo)

2002 2004-2005 Oct 2005 Nov 2005 March 2006 Summer 2006

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 9

CONCLUSIONUltimately — and rather perversely — the industry’sinvestment in oncology research and development mayoffer the basis for a more rational era in oncology pricingand reimbursement provision as:

• Repetitive innovation will create new benchmarks ofperformance.

• Oncologists will have more choice.

• Increasing competition between pharmaceuticalcompanies will lead to keener pricing and incrementalvalue propositions.

• The development of more sensitive diagnostic tests willallow targeted therapies to be used in the patients mostlikely to respond positively.

All this will occur while payers prepare for generic versionsof valuable products such as Taxotere® and Gemzar®.

“For the moment, companies in the oncology market areenjoying the success that comes from their years ofinnovation, relatively unhampered by the influence ofpayers,” declares Lewis,“but in a sense, companies willbecome the victims of their own success.Their experienceis attracting others to the market, and this competition will

give payers the leverage they need to strengthen theirtechnology assessments, clamp down on prices and createaccess barriers as needed.The special freedoms manufac-turers have enjoyed in the oncology market will go the wayof all outmoded conventions. Oncology products will besubject to the same managed care influences as products inother markets.”

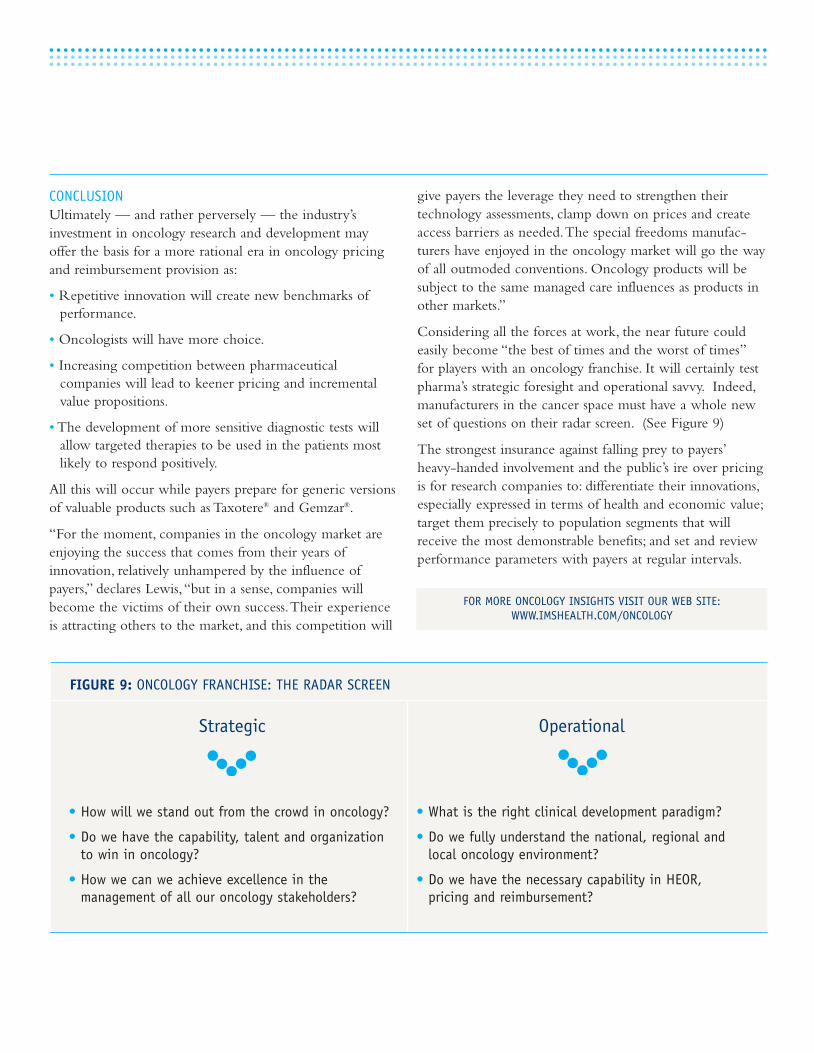

Considering all the forces at work, the near future couldeasily become “the best of times and the worst of times”for players with an oncology franchise. It will certainly testpharma’s strategic foresight and operational savvy. Indeed,manufacturers in the cancer space must have a whole newset of questions on their radar screen. (See Figure 9)

The strongest insurance against falling prey to payers’heavy-handed involvement and the public’s ire over pricingis for research companies to: differentiate their innovations,especially expressed in terms of health and economic value;target them precisely to population segments that willreceive the most demonstrable benefits; and set and reviewperformance parameters with payers at regular intervals.

FOR MORE ONCOLOGY INSIGHTS VISIT OUR WEB SITE:WWW.IMSHEALTH.COM/ONCOLOGY

FIGURE 9: ONCOLOGY FRANCHISE: THE RADAR SCREEN

• What is the right clinical development paradigm?

• Do we fully understand the national, regional andlocal oncology environment?

• Do we have the necessary capability in HEOR,pricing and reimbursement?

Strategic Operational

• How will we stand out from the crowd in oncology?

• Do we have the capability, talent and organizationto win in oncology?

• How we can we achieve excellence in themanagement of all our oncology stakeholders?

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 10

06215-A

ABOUT IMS HEALTH

Operating in more than 100 countries, with $1.8 billion in 2005revenue, IMS provides clients with evidence-based, customizedintelligence about the pharmaceutical and healthcare markets —delivering critical information, analytics and consulting that drivesuperior client business strategies, decisions and results.

IMS HEALTH®

THE AMERICAS660 West Germantown PikePlymouth Meeting, PA 19462USATel: 800.523.5333

EUROPE/AFRICA/MIDDLE EAST7 Harewood AvenueUnited KingdomTel: 44.020.7393.5100

ASIA PACIFIC10 Hoe Chiang RoadKeppel Towers #23-01/02 Singapore 089315 Tel: 65.6227.3006

www.imshealth.com

©2006 IMS Health Incorporated or its affiliates. All Rights Reserved.

06215 oncology whitepaper.qxd 1/9/07 4:41 PM Page 11

![ElectrochemicalBehaviorofBiologically …downloads.hindawi.com/journals/ijelc/2011/154804.pdfcancer [2], antioxidant [3], antirheumatoidal [4], and anti-HIV [5, 6]. Studies showed](https://img.dokumen.tips/doc/110x75/5f61e87cd8a3b055dd17da94/electrochemicalbehaviorofbiologically-cancer-2-antioxidant-3-antirheumatoidal.jpg)