Embed Size (px)

Citation preview

1

Catholic Crosscultural Services

Canadian Tax System & Doing Business in Ontario

Sonja Chong, FCA Partner – Income Taxation

Harris & Chong LLP

Chartered Accountants 2225 Sheppard Avenue East

Suite 1202, Atria III Toronto, Ontario M2J 5C2

Telephone: (416) 499-3112, Ext. 309

Fax: (416) 499-7372 Email: [email protected]

February 25, 2013

INDEX

Pages

1. Canadian tax system 3 - 9

2. Record Keeping, Financial Statements and Tax Returns 10 - 14

3. Selection of Business Structure 15 - 19

4. Tax Rates and Tax Case Studies for carrying

on businesses in Ontario 20 - 26

5. Tax Planning for New Tax Residents 27 – 31

NOTE: This presentation was prepared in early 2012, and have not been updated. The information contained herein is for general informational purposes only. We recommend professional advice always be sought before taking specific planning steps.

Provided by Sonja Chong, FCA 2

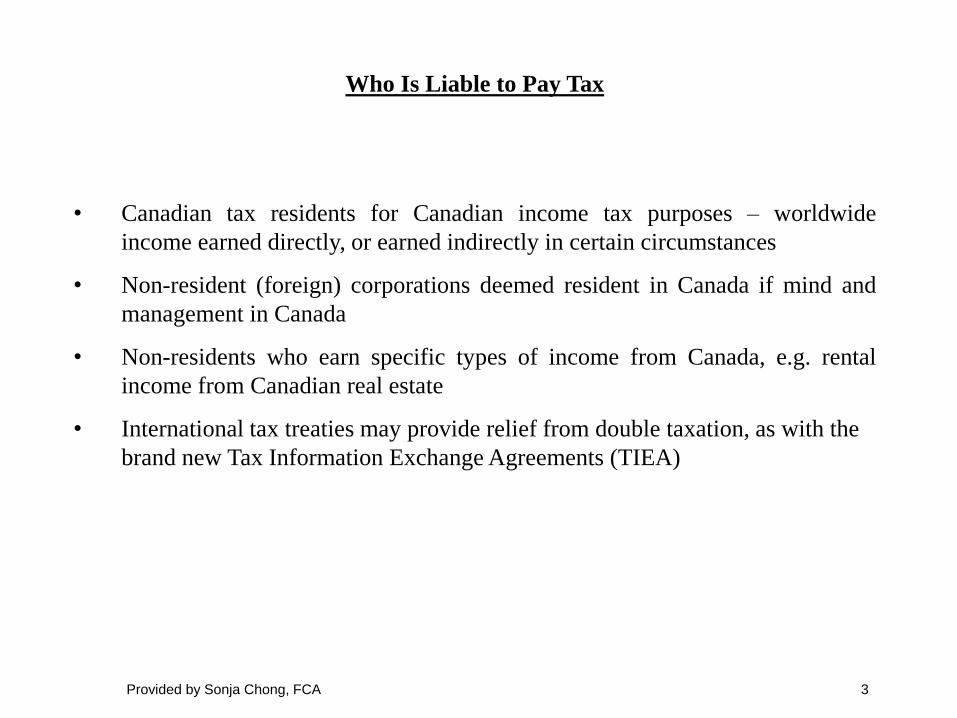

Who Is Liable to Pay Tax

• Canadian tax residents for Canadian income tax purposes – worldwide

income earned directly, or earned indirectly in certain circumstances

• Non-resident (foreign) corporations deemed resident in Canada if mind and

management in Canada

• Non-residents who earn specific types of income from Canada, e.g. rental

income from Canadian real estate

• International tax treaties may provide relief from double taxation, as with the

brand new Tax Information Exchange Agreements (TIEA)

Provided by Sonja Chong, FCA 3

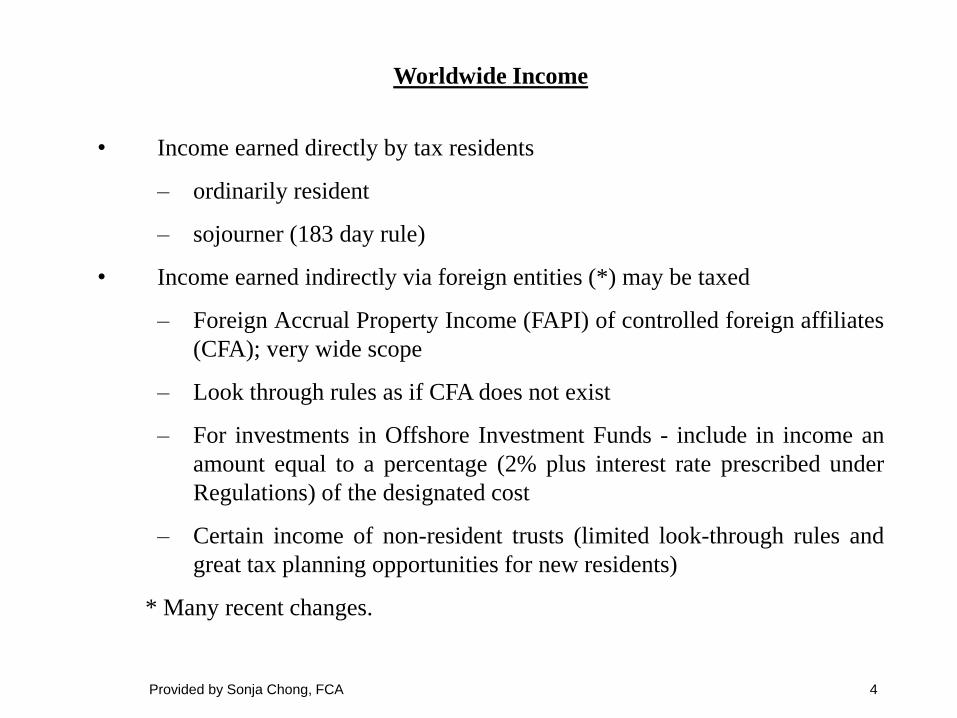

Worldwide Income

• Income earned directly by tax residents

– ordinarily resident

– sojourner (183 day rule)

• Income earned indirectly via foreign entities (*) may be taxed

– Foreign Accrual Property Income (FAPI) of controlled foreign affiliates

(CFA); very wide scope

– Look through rules as if CFA does not exist

– For investments in Offshore Investment Funds - include in income an

amount equal to a percentage (2% plus interest rate prescribed under

Regulations) of the designated cost

– Certain income of non-resident trusts (limited look-through rules and

great tax planning opportunities for new residents)

* Many recent changes.

Provided by Sonja Chong, FCA 4

Foreign Affiliate (FA)

• To be a controlled foreign affiliate (CFA), it must first be a FA.

• To be a FA of a person, the person must have at least a 1% direct or indirect

interest, and at least an aggregate 10% direct or indirect interest in the non-

resident corporation held by the person and all related persons

• Is ForCo a FA of Mr. A?

Provided by Sonja Chong, FCA 5

ForCo

Canada

Foreign

Father of A Third Party

39% 60%

1%

A

Controlled Foreign Affiliate (CFA)

• a CFA at anytime of a resident taxpayer:

1. is a FA which at that time is controlled by the particular taxpayer, or

2. is a FA of the taxpayer and would be controlled by the taxpayer. In

determining control, the taxpayer would include all shares of the FA

that he/she owns, and:

(a) persons (include residents and non-residents) who deal at

non-arm’s length (“NAL”) with the taxpayer,

(b) all shares of the FA owned by any set of resident

persons not exceeding four persons, and

(c) any person who does not deal at arm’s length with any other

Canadian resident shareholder .

Provided by Sonja Chong, FCA 6

CFA

An Illustration

• A, B and C are not related to and deals at arm’s length with each other

• Is ForCo a FA and/or CFA of each of A and B?

• ForCo is A’s FA since A has more than 10%.

• ForCo is B’s FA as B has 10%.

• Is ForCo A’s CFA?

• Is ForCo B’s CFA?

Provided by Sonja Chong, FCA 7

ForCo

Canada

Foreign

A B

C

10%

49%

41%

Foreign Affiliates

Tax Free Repatriation of Active Business Income

Canada Canada

Treaty Country Treaty Country

Tax rate = 45%

Profit = $100,000

Canadian tax = $45,000

Carries on active

business directly

(branch)

Profit = $100,000

Tax rate = 20%

Withholding tax = 10%

Carries on active business

($)

Profit 100,000

ForCo’s foreign tax (20,000)

Dividend to CanCo (exempt surplus) 80,000

Foreign withholding tax (8,000)

CanCo’s cash retention 72,000

$80,000 dividend income received by CanCo free of Canadian tax. A tax savings of $27,000, being $80,000 less $8,000 less $45,000

Provided by Sonja Chong, FCA 8

CanCo

A

100%

CanCo

ForCo

A

100%

100%

Controlled Foreign Affiliates

Foreign Accrual Property Income (FAPI)*

Canada

($)

Dividend Income 80

Deduct: FAPI (20)

Deduct: Foreign Tax ($20 x 3) (60)

Net Dividend Income 0

Net cash retained in CanCo 75

* Now includes active business income earned in non-treaty and non-TIEA countries.

Any Foreign

Country FAPI 100

Deduct: Foreign Tax ($20) x 4 (80)

Subject to Canadian Tax 20

Canadian Tax @ 25% (38% - 13%) 5

Summary

Foreign Tax 20

Canadian Tax 5

Total 25

CanCo

ForCo

100%

FAPI (generally means

property income, sometimes

business income deemed to

be property income)

Provided by Sonja Chong, FCA 9

Importance of Record Keeping

• required in order to prepare financial statements

• facilitate analysis for tax planning

• facilitate budgeting for business

• typical types of taxes, withholding and remittances

- income tax (includes tax on capital gains)

- harmonized goods and services tax

- withholding of employee tax, EI and CPP

- property tax

- land transfer tax

- business licence tax

- workplace safety insurance

• crucial in the removal of conditions for immigrants under the business entrepreneur

category

Provided by Sonja Chong, FCA 10

Tax and Information Returns

• income tax returns - calendar year for individuals and inter-vivos trusts, any

year end for corporations

• information returns - foreign assets

• tax evasion versus tax planning to avoid or minimize tax

• tax evasion is a criminal offence

• failure to file income tax or information returns could attract significant

interest and penalties

• timely and effective tax planning can save taxes and eliminate unnecessary

stress

• tax returns are one of the documents that are reviewed for purposes of

establishing residency for immigration purposes

Provided by Sonja Chong, FCA 11

Accountants’ Reports on Financial Statements

• Notice to Reader

• Review Engagement

• Auditor’s Report

Provided by Sonja Chong, FCA 12

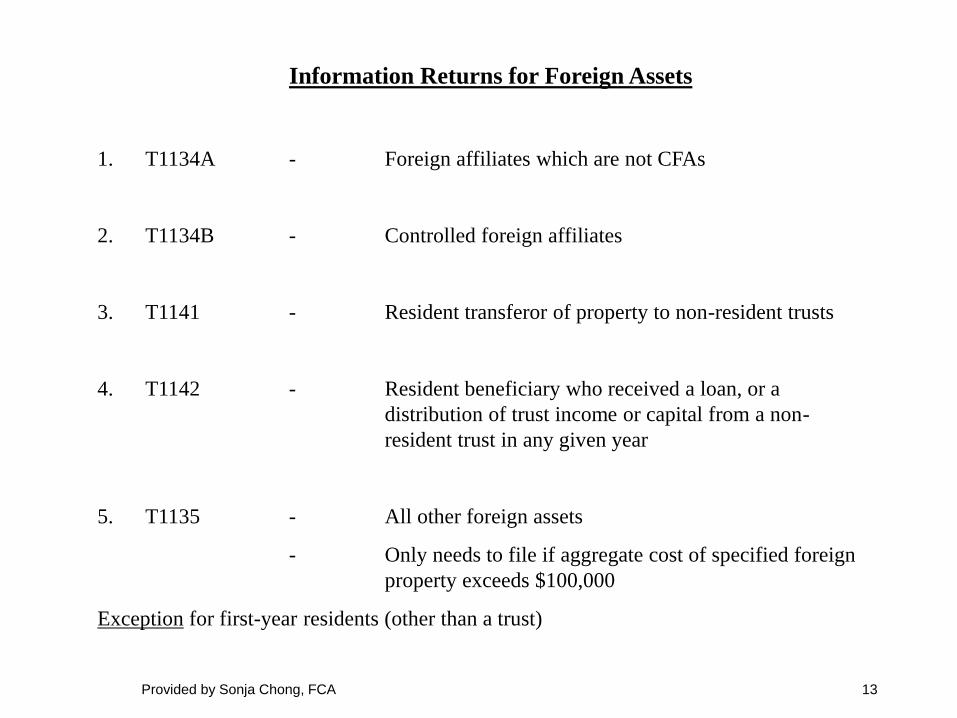

Information Returns for Foreign Assets

1. T1134A - Foreign affiliates which are not CFAs

2. T1134B - Controlled foreign affiliates

3. T1141 - Resident transferor of property to non-resident trusts

4. T1142 - Resident beneficiary who received a loan, or a

distribution of trust income or capital from a non-

resident trust in any given year

5. T1135 - All other foreign assets

- Only needs to file if aggregate cost of specified foreign

property exceeds $100,000

Exception for first-year residents (other than a trust)

Provided by Sonja Chong, FCA 13

T1135

Information Return for Specified Foreign Property (“SFP”)

Three Levels of Penalties

1. Failure to file return

S.162(7) Greater of $100, and $25 per day not exceeding 100 days ($2,500)

2. Fails to file knowingly or amounting to gross negligence

1st 24 months

Maximum

S.162(10)(a) & S.162(10.1)(a) $500/month per S.162(10)(a) 5% of the greatest of all amounts each of which is the total of the cost amount to the taxpayer at any time during the year of a SFP less any penalty under S.162(7) & S.162(10)(a)

3. Knowingly or under circumstances amounting to gross negligence, fails to comply with a CRA demand to file

1st 24 month Maximum

S.162(10)(b) & S.162(10.1)(b) $1,000/month per S.162(10)(b) 5% of the greatest of all amounts each of which is the total of the cost amount to the taxpayer at any time during the year of a SFP less any penalty under S.162(7) & S.162(10)(b)

Provided by Sonja Chong, FCA 14

Selection of Business Form/Structure

Depends on:

• business risks, and the need to limit business liabilities to business assets

• minimization of income tax

• effective and multiple use of the lifetime $750,000 capital gains exemption

(CGE)

• personal cash needs

• other considerations

Provided by Sonja Chong, FCA 15

Business Form/Structure

1. Sole proprietorship

2. Partnerships - registration required

- general versus limited

3. Joint Ventures

4. Corporations

5. Trusts

6. A creative combination of one or more of the above

Provided by Sonja Chong, FCA 16

Business Form/Structure

Personal Trusts

• legal ownership versus beneficial ownership

• four elements - settlor/transferor, trustee, trust property, beneficiaries

• inter-vivos (taxed at highest marginal individual tax rate) versus testamentary trusts (taxed at graduated rates)

• can be a flow-through entity (much like partnerships)

Provided by Sonja Chong, FCA 17

Resident

Trust

Settlor/Transferor Beneficiaries

Trust Property

Trustee

Business Structure

1. Sole proprietorship/Joint Venture/Partnership

- family members can be joint venturers or partners

- take advantage of the graduated tax rate system to reduce aggregate

tax liability for family

- business losses can be deducted against other types of income

- highest marginal individual tax rate for 2011 and 2012 is 46.41%

(Federal – 29%; Ontario – 17.4096%)

Provided by Sonja Chong, FCA 18

Business Structure

2. Corporations

- limited liability

- family members can be shareholders (watch under 18 children and grandchildren)

- 2011 combined Federal (11%) and Ontario (4.50%) tax rate on first $500,000 of active business income (“ABI”) of Canadian controlled private corporations (CCPC) is 15.5%

- compare this 15.5% rate to highest personal tax rate of 46.41%

- personal cash requirements can be extracted from the corporation via salary, dividends, loans or a combination thereof

- consider using Structure 1 (on page 18) for start-ups (with expected losses), then change business structure (can be done on a tax-free basis) to corporate structure (generally lower tax rates on the first $500,000 of ABI) on the upswing

Provided by Sonja Chong, FCA 19

Top Marginal Combined Tax Rates (%) - Ontario Resident Individuals

2012 2011

Employment & Other Income

46.41

46.41

Capital Gains 23.20 23.20

Canadian dividends – Non-eligible 32.57 32.57

Canadian dividends – Eligible 29.54 28.19

Provided by Sonja Chong, FCA 20

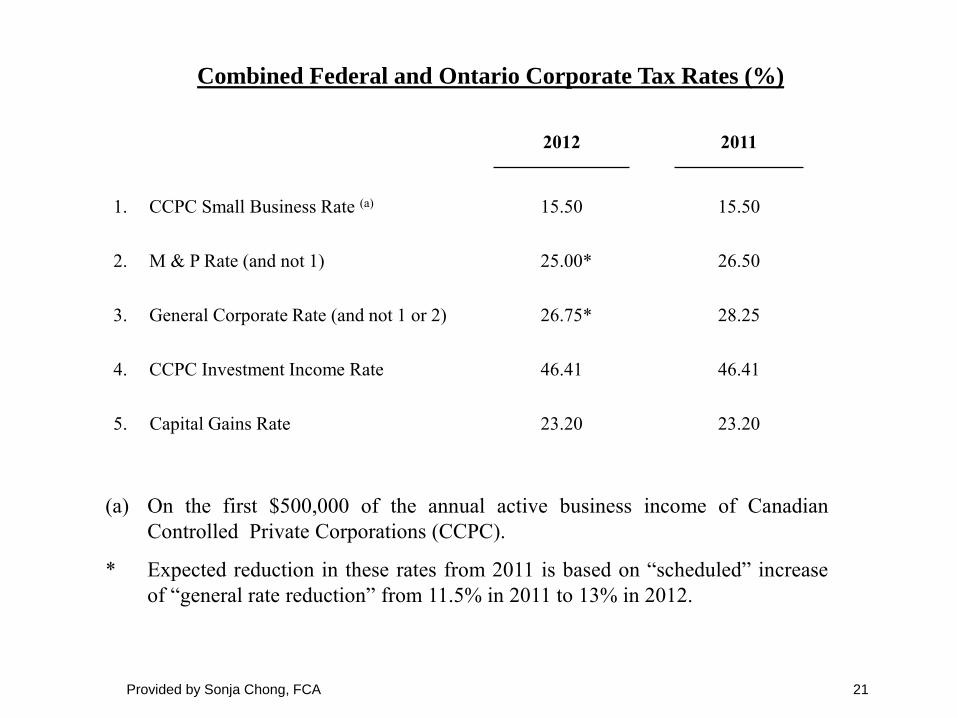

2012 2011

1. CCPC Small Business Rate (a)

15.50

15.50

2. M & P Rate (and not 1) 25.00* 26.50

3. General Corporate Rate (and not 1 or 2) 26.75* 28.25

4. CCPC Investment Income Rate 46.41 46.41

5. Capital Gains Rate 23.20 23.20

Combined Federal and Ontario Corporate Tax Rates (%)

(a) On the first $500,000 of the annual active business income of Canadian

Controlled Private Corporations (CCPC).

* Expected reduction in these rates from 2011 is based on “scheduled” increase

of “general rate reduction” from 11.5% in 2011 to 13% in 2012.

Provided by Sonja Chong, FCA 21

Concept of Tax Deferral - Example One

CCPC Sole-Proprietorship

Active business income 300,000 300,000

Tax rate (2011) 15.5% Graduated Rates

Corporate tax (A) 46,500 N/A

After-tax earnings, i.e. dividends 253,500 N/A

Individual tax (graduated rates) on

- dividend

(B) 63,594

N/A

- business income N/A 123,156

Total corporate and individual taxes

(C) = (A) + (B) 110,094

(D) 123,156

Tax Savings (D) - (C) 13,062

Tax deferral (25.55% !)

(D) - (A) 76,656

Provided by Sonja Chong, FCA 22

Concept of Tax Deferral - Example Two

CCPC Sole-Proprietorship

Active business income 300,000 300,000

Tax rate (2010) 15.5% Highest Rate

Corporate tax (A) 46,500 N/A

After-tax earnings, i.e. dividends 253,500 N/A

Individual highest marginal rates on

- dividend (32.57%)

(B) 82,565

N/A

- business income (46.41%) N/A 139,230

Total corporate and individual taxes

(C) = (A) + (B) 129,065

(D) 139,230

Tax Savings (D) - (C) 10,165

Tax deferral (30.91% !)

(D) - (A) 92,730

Provided by Sonja Chong, FCA 23

Advantages of Corporate Structure

• huge 30.91% (46.41% versus 15.5%) tax deferral for those at top marginal

rate

• individual residents can each receive about $38,500 of dividend paid out

of small business rate retained earnings, and about $51,500 of dividend paid

out of general business rate earnings completely tax-free (except for $450

and $750 of Ontario Health Premium - OHP)

• up to $750,000 of capital gains on sale of shares of small business

corporations can be exempt from tax (CGE)

• use of trusts with corporations

- to create multiple use of CGE

- to take advantage of tax-free dividends

- for credit proofing purposes

- for estate planning purposes

- to reduce probate fees

• tax-effective Wills

Provided by Sonja Chong, FCA 24

Life Cycle of a Business

1. Start-up

Mr. A Mr. A and Mrs. A

carries on business carry on business

2. Profitable (reorganize Structure 1 to 2 on a tax-free basis

Mr. A

common shares

CanCo

carries on active business

Provided by Sonja Chong, FCA 25

Life Cycle of a Business

3. Mature - reorganize Structure 2 to 3 on a tax-free basis

Mr. A Trustee

A

B

A - voting shares B - non-voting shares

- preferred shares - growth shares; captures

- value frozen appreciation in value of CanCo

CanCo/CCPC

carries on active business

Resident

Trust

Mr. A, Mrs. A, children,

grandchildren can be

beneficiaries, if structured

properly

Provided by Sonja Chong, FCA 26

Tax Planning for New Tax Residents

• deemed acquisition at fair market value (“FMV”) before becoming resident

• collect all income prior to becoming resident, if home country tax liability is lower

• reorganize foreign company structure so up to FMV can be extracted tax-free (!!!) - watch home country taxation rules

• select appropriate business structure - see Life Cycle of Business

• about $38,000 non-eligible dividend tax-free every year if individual has no other sources of income (except for $450 Ontario Health Premium or OHP)

• about $51,500 eligible dividend tax-free every year if individual has no other sources of income (except for $750 OHP)

• effective use of offshore trusts

• watch FAPI of controlled foreign affiliates

• watch active business income of controlled foreign affiliates sourced from non-treaty or non-TIEA countries - proposed to be deemed FAPI

Provided by Sonja Chong, FCA 27

Case Study

Tax-free Extraction of Value Accrued

1. Original 2. On Becoming Resident

HKCo

Mr. Omar

Cost = $100

FMV = $1 million

PUC = $100 100%

HKCo

Mr. Omar

Cost = FMV = $1 million

PUC = $100 100%

Foreign

HoldCo

Mr. Omar

Cost = FMV = $1 million

- takes back shares worth $1 and loan (promissory note of $999,999)

3. To reorganize structure

HKCo

100%

Provided by Sonja Chong, FCA 28

100%

Offshore Trusts

• legal ownership versus beneficial ownership

• four elements – settlor/transferor, trustee, trust property, beneficiaries

• typically additional element for offshore trusts - protector as a watchdog over the

trustee

• taxation rules of non-resident trusts first proposed to be changed in the 1990

Federal Budget; latest changes (significant) released in 8/27/2010 Draft

Legislation (DL)

• Complex taxation rules proposed in 8/27/2010 Draft Legislation and 9/28/2010

Notice of Ways and Means Motion for contributions by long-term tax residents

• benefits remain particularly for new residents/immigrants, and those who stand to

receive or inherit significant assets from foreign resident relatives/friends

• key is the cumulative period of residency of the settlor/transferor

Provided by Sonja Chong, FCA 29

Offshore Trusts

Immigrant Trust

Bahamian Trust

Company

Bahamian

Trust

Mr. A gifted $3 million to trust

say prior to moving to Canada

Beneficiaries could be Mr. A’s spouse

and children who also move to Canada

$3 million of portfolio

investments

• provided income earned in a year by the trust is not distributed to resident beneficiaries in the same year, income on $3 million capital accumulates free of tax for maximum 60 months

• assumes home country does not levy tax based on say citizenship

• cash requirements can be met by distribution out of trust capital - tax-free

• trust to be restructured/wound up before 60-month deadline

• Form T1141 - to be filed every year by Mr. A

• Form T1142 - upon distribution of trust income and/or trust capital, and/or loans made to beneficiaries; resident beneficiaries to file

Provided by Sonja Chong, FCA 30

Offshore Trusts

Inheritance/Testamentary Trust/Inter-Vivos

Bahamian Trust

Company

Bahamian

Trust

Grandmother’s will provides that $5

million be settled in a trust for the benefit

of her children and grandchildren in

Canada (or grandmother makes a gift

while alive)

Beneficiaries can be children and

grandchildren resident in Canada

and/or other non-resident relatives

$5 million of portfolio

investments

• tax exempt status of trust is perpetual as grandmother never resided in Canada

• no information reporting necessary until trust income or trust capital distributed to or loans made to

resident beneficiaries (T1142)

• watch foreign income and estate tax rules

Provided by Sonja Chong, FCA 31