Embed Size (px)

Citation preview

URBANICS CONSULTANTS LTD.

CAMPBELL RIVER EMPLOYMENT LAND STRATEGY STUDY

City of Campbell River

EMPLOYMENT LANDS STRATEGY STUDY

Prepared for: the City of Campbell River

August 2019

Prepared by: Urbanics Consultants Ltd.

Suite 1207 – 409 Granville Street, Vancouver BC, V6C 1T2

1

Executive Summary Urbanics Consultants Ltd. was retained by the City of Campbell River to conduct an Employment Lands Study for the City. The primary objectives of the study are to: • Create a comprehensive inventory of lands which includes:

o Existing supply of “employment lands” (industrial and commercial zoned land) of both developed and undeveloped employment lands;

o Size, ownership and potential best use of parcels according to industry trends; o Existing types of jobs and industry sectors in the City.

• Develop an employment strategy which addresses:

o General socio-economic conditions and trends in the City; o “Business ready” SWOT analysis of the City; o Highest and best use of land and identifying viable business classes that the City can consider pursuing.

To achieve these objectives, this study examines the socio-economic profile and economic base (aggregation of companies/ employers that generate jobs in the City). The study also projects future employment levels in the City to estimate potential demand for employment land over the next 20 years. The study uses a comprehensive employment land inventory and utilization analysis to estimate the available supply of employment land in the City. The reconciliation of the employment land supply, demand assessment, feedback received from the survey, stakeholder interviews and stakeholder consultation form the basis of the following findings and recommendations. The primary findings from the study are: EMPLOYMENT LAND SUPPLY

The City of Campbell River has 1,875 acres of land zoned for industrial uses and 615 acres of land zoned for commercial uses. The Table below sets out the gross area and percentage of each industrial and commercial land use type. As for commercial land, parcels zoned C–3, C–6, C–7 and C–8 represents a comparatively small percentage of the total number and land area, and as such, have been omitted from the Table.

2

LAND UTILIZATION • Industrial land utilization: In terms of utilization of the

industrially zoned land in the City, 80 percent of the I–1 zoned industrial land is fully utilized, with only 8.8 acres of land classified as vacant and 6.8 acres classified as underutilized land. By contrast, utilization for I–2 zoned industrial land is significantly lower than the other Industrial Zone classes. Only 18 percent of the zoned I–2 Industrial land is fully utilized, with 37 percent and 45 percent, respectively, classified as vacant or underutilized. Both of these land bases have strategic locations within the city and accommodate the largest number and broadest cross-section business activity.

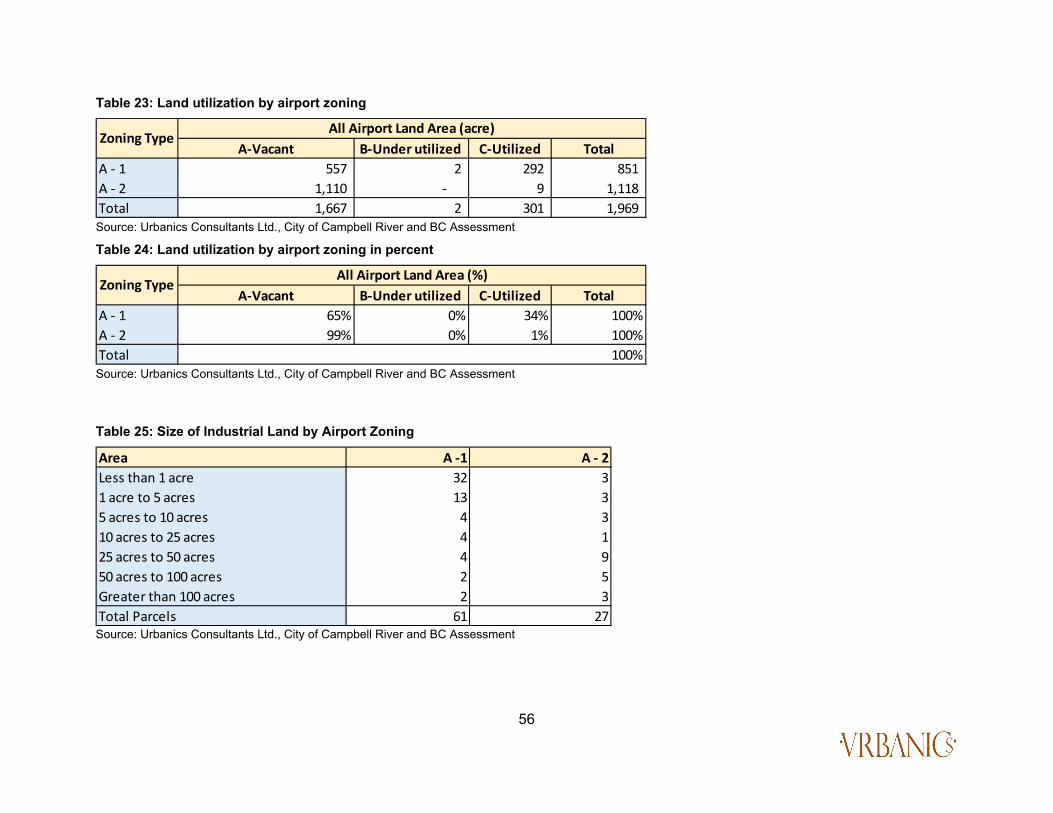

• Airport land utilization: In terms of utilization of the Airport zoned land, 65 percent of the A–1 zoned airport land is classified as vacant. Lands zoned A-1 are airside and include both the runway area and the linear series of parcels on the east boundary of the airport.

Only 1 percent of A -2 airport land is utilized, which leaves 99 percent (approximately 1,110 acres) as vacant land. However, much of the A-2 land adjacent to the airport has practical limitations to its development - primarily physical characteristics, and ownership. However, A-2 lands that straddle Jubilee Parkway, east of the Airport have potential for development with lands north of the Parkway having more favourable topography, comparatively few riparian limitations, and lands south having a significantly higher degree of riparian sensitivity impacting the physical development.

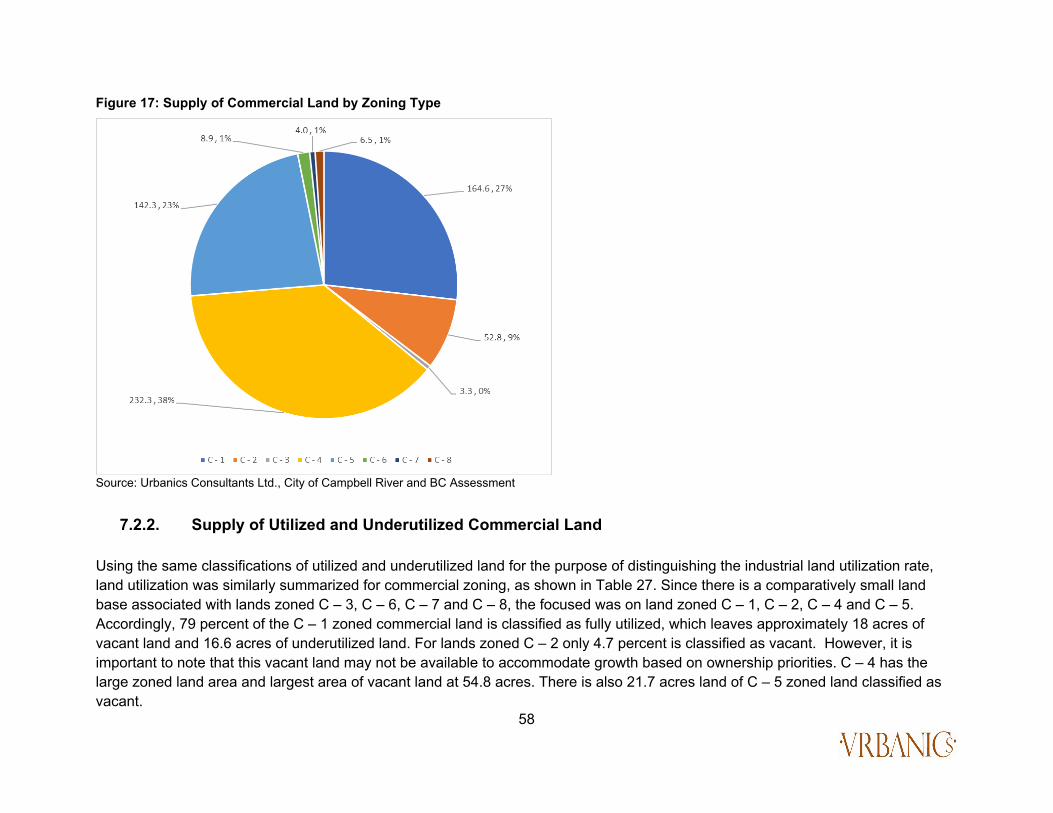

• Commercial land utilization: Since there is comparatively small land base associated with parcels zoned: C–3, C–6, C–7 and C – 8, the study’s focus is on C–1, C–2, C–4 and C–5 zoned commercial land. With regard to C-1 Zoned lands, 79 percent (130 acres) is classified as fully utilized (discounting building condition),11% (18 acres) of the C–1 zoned commercial land is classified as vacant and 10% (16.6 acres) of the C–1 zoned commercial land is classified as underutilized. C–2 has only 4.7 acres of vacant land available. C–4 has the largest zoned land area and 54.8 acres of vacant land available. There are also 21.7 acres land available in C–5 zoning.

ZONE PERCENT SIZE (ACRES)

I-1 4 75

I-2 40 750

I-3 48 900

I-4 8 150

TOTAL 100 1875

C-1 27 166

C-2 9 55

C-4 38 234

C-5 23 142

TOTAL 97 597

Table 1: Breakdown of Industrial & Commercial Zoned Areas

3

EMPLOYMENT LAND DEMAND

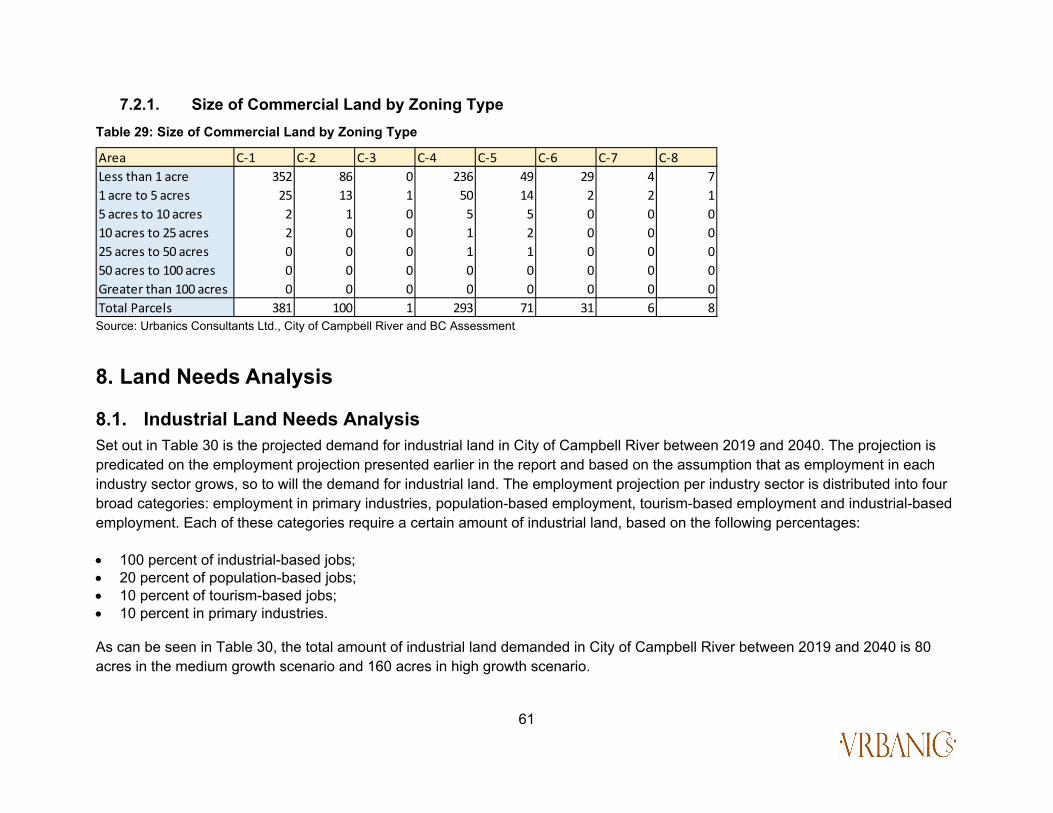

• Industrial land demand In low-density development scenario, a total of 160 acres of industrial land will be needed by 2040; a high-density development scenario requires a total of 80 acres of industrial land by 2040.

• Commercial land demand

Office space. There is no new demand projected for office space within the period scope of the study. Office employment is expected to grow from 919 jobs in 2016 to 1,213 jobs in 2040. Warranted office space will grow from approximately 276,000 square feet to 364,000 square feet. However, the current total office space (369,000 square feet) is considered to be an adequate supply until 2040 (discounting building condition).

Retail space. There is projected demand for approximately 140,000 square feet of additional retail floorspace by 2035. About 380,000 accumulated retail space will be needed by 2040. With a FAR (floor area ratio – the ratio of the total floor area of a building (gross floor area) to the size of the associated parcel of land) of 0.35, there is estimated new demand for approximately 9 acres of commercial land by 2035. About 16 acres can be expected to be added by 2040, totalling about 25 acres of required new commercial land by 2040.

CAPACITY AND ADEQUACY OF EMPLOYMENT LANDS

• Capacity and adequacy of industrial lands: In terms of the total industrial land supply, there is sufficient inventory for future employment growth as a whole. However, there are caveats that include the potential limitations to practical development potential of some Industrially zoned land. In addition, land zoned for light industrial will be expected to grow faster than heavy industrial. There will not be a sufficient supply of zoned and serviced light industrial land to accommodate future growth.

• Capacity and adequacy of commercial lands: Given the current supply of commercially zoned land, the additional need for 25 acres for future development can be accommodated by the current vacant commercial land supply, potential in-fill development or otherwise redevelopment of low FAR properties adjacent to and within the downtown core. Little additional demand is anticipated for the primary village centers such as Dogwood/ 2nd Avenue, Dogwood/ Merecroft, Dogwood/ Hilchey, Dogwood/ Jubilee, Willow Point, and Campbellton.

4

RECOMMENDATIONS

• Capitalize on existing industrial base: Capitalize on the existing, established industrial base of the City by promoting manufacturing, especially related to value-added wood industries. There is an opportunity to enhance research and development to increase innovation in processing and manufacturing of value-added wood products. These can include such commodities as fabrication of specialized construction materials, log homes and furniture. The focus of a marketing strategy would be on innovation, synergy, quality, and location.

• Shift to more light industrial usage: The industrial base of the City is displaying lower demand for heavy industry and greater

demand for light industry. However, there can be a synergistic relationship between heavy and light industries. The sectors of forestry, aquaculture and aerospace can be a key focus. However, floorspace and vacant land to accommodate growth in the light industrial sector is low compared and warrants further attention and potential supply interventions.

• Pursue/ attract businesses that are involved in high-tech and consulting services: Businesses that are involved in high-

tech and consulting services rely less on transportation and place greater value on the quality of life for innovation employees. Maintaining an excellent work-life balance is a great attraction for people working in This sector. The City’s broadband network (CRadvantage) is a significant locational inducement for business and people working in high-tech and consulting services. In addition, such businesses can complement the resource-based economy by providing niche research and innovation such as for value-added wood products.

• Office space utilization: Due to the high vacancy rate for office space, the City could investigate the viability of developing an

“incubation center” or “collaboration space” for entrepreneurs by collaborating with associated property owners to facilitate the utilization of vacant office space – this also contributes to a sense of economic vibrancy of the downtown. If priced appropriately and marketed, such space could attract start-ups. High-tech and consulting service entrepreneurs do not need or seek a large floor space commitment at business start-up. However, they do need a space to launch their business, meet clients, and potentially collaborate with other entrepreneurs. An incubation center or collaboration space would be attractive to start-up entrepreneurs and, in the future, can be the place to promote the City’s programs for business attraction.

• Enhance downtown vibrancy: there is a relatively high commercial vacancy rate in the City though recent information from

local relators indicates that relative vacancy rates are beginning to trend downward. To reduce the commercial vacancy rate, the City can consider a number of options that range from minor to major intervention:

5

o Supporting the efficiency and effectiveness of the downtown BIA by increasing the budget allocated to downtown BIA for

advertisement and promotion; o Collaborating with merchants in the City to create a complete shopping experience for local residents, as well as, tourists, for

example:

- by continuing to organize people enticing events such as a 4-season festival event schedule, - facilitating retail merchandising workshops by professional merchandisers to maximize the visual impact on passing foot

traffic, - maintaining a façade improvement program, - establishing relatively similar business hours particularly during summer months when foot traffic can be expected to be

higher and in association with downtown events. o Building on previous work such as “Refresh Downtown Campbell River”, a continued focus of strategic investment in

programmed downtown place-making and experience enrichment, will boost downtown shopping visits and stays both of which typically translate into increased trade. An iconic downtown experience can also be a significant tourism draw. This can translate into greater economic vibrancy, which in turn, promotes reinvestment and employment.

o A continued emphasis of facilitating the development of downtown residential can also contribute to the economic vibrancy of

the downtown.

o Continue to invest in and develop more anchor attractions such as the Tidemark Theatre, Community Center, art gallery, Spirit Square, and public library for instance, in addition to investment in streetscape beautification projects and iconic public art installations, for example.

• Prepare for long term growth in the downtown: over the long term, the downtown can expect to add more commercial

floorspace to the existing inventory. While some infill and redevelopment opportunities exist, there is value in strategic planning for expansion of commercial floorspace in the area north of Shoppers Row to Dogwood Street. Under certain land ownership scenarios, land assembly can make future development more complicated and uncertain. Consider opportunities to partner with North Island College for downtown student housing.

6

• Promote tourism: Capitalize on the existing tourism resource base of the City and continue to both market the exceptional Campbell River and District experience and invest in the complementary infrastructure, such as the Discovery Fishing Pier or the Elk Falls Suspension Bridge, for example. Explore opportunities to reinforce and market Campbell River as an off-season mountain sports hub given its location between Mount Washington and Mount Cain.

• Promote education and skills development: Promote education in the City at the post-secondary level. Innovative industries

will need skilled labor, especially in the aviation industry. The City can consider the possibility of collaborating with North Island College and the major aviation employers to design a work-study program for students, for example.

• Possibility of light industrial park: The City can investigate the possibility of facilitating the development of a new light industrial park located on the A-2 zoned land. The Airport zoned land (A-2) is almost vacant and has access to both a major highway and airport. A major employer in aviation industry has located in the airport and is expecting to expand operations in the next few years. A state-of-the-art light industrial park accommodating innovative industries can be a business attraction advantage for the City.

LIMITATIONS

This study relies on data from a variety of sources, including Statistics Canada, BC Stats, and many others. Though efforts have been taken to ensure the completeness and accuracy of the information provided, it must be stated that this study may be impacted by the quality and availability of its underlying data. It should also be noted that this study does not assess the impact of industrial development on the First Nation Lands nor the challenges posed by contamination in any of the industrial areas in the City of Campbell River. It is expected that these two factors will potentially affect industrial and commercial development in the City of Campbell River, and efforts should be made to explore their potential impact.

7

Table of Contents Executive Summary ........................................................................................................................................................................... 1

List of Figures .................................................................................................................................................................................... 9

List of Tables .................................................................................................................................................................................... 11

1. Introduction ............................................................................................................................................................................... 13 1.1 Contextual overview ........................................................................................................................................................ 13 1.2 Employment Land Study ................................................................................................................................................. 14 1.3 Methodology ..................................................................................................................................................................... 14

1.3.1 Review of previous studies and policies governing land use ............................................................................................................ 14 1.3.2 Demographics analysis .................................................................................................................................................................. 15 1.3.3 Economic base analysis ................................................................................................................................................................ 15 1.3.4 Supply analysis .............................................................................................................................................................................. 15 1.3.5 Demand Analysis ........................................................................................................................................................................... 15 1.3.6 Community engagement ................................................................................................................................................................ 15 1.3.7 Findings and Recommendations ................................................................................................................................................... 16 1.3.8 Limitations ...................................................................................................................................................................................... 16

2. Demographic Analysis ............................................................................................................................................................. 17 2.1. Vancouver Island and Coast Context ............................................................................................................................. 17 2.2. The City of Campbell River Context ............................................................................................................................... 19

2.2.1. Historical Population Growth ......................................................................................................................................................... 19 2.2.2. Historical Population Composition ................................................................................................................................................ 21 2.2.3. Population Projection .................................................................................................................................................................... 24

3. Economic Base Analysis ......................................................................................................................................................... 27 3.1. Provincial economy ......................................................................................................................................................... 27 3.2. Historical Employment Trends ....................................................................................................................................... 28 3.3. Location Quotient Analysis ............................................................................................................................................. 33 3.4. Employment Projection ................................................................................................................................................... 35

8

3.5. Online Survey Summary .................................................................................................................................................. 39 3.6. Businesses Profile ........................................................................................................................................................... 39 3.7. Potential growth industries ............................................................................................................................................. 41

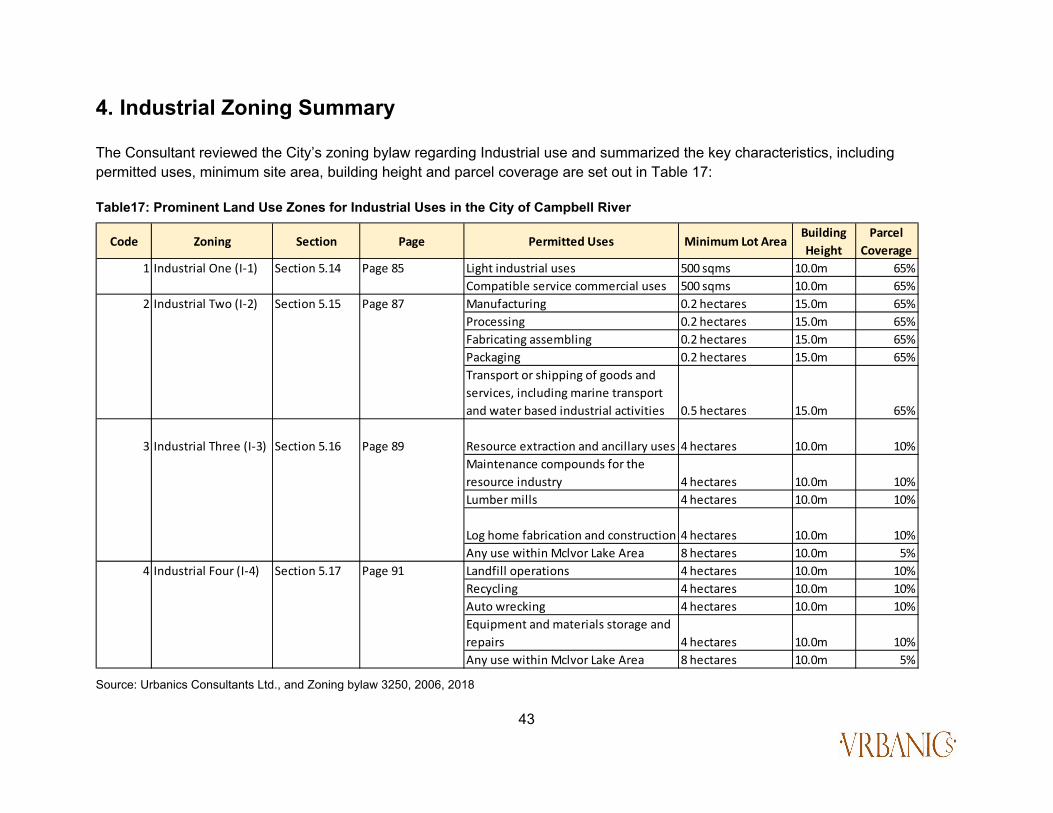

4. Industrial Zoning Summary ..................................................................................................................................................... 43

5. SWOT Synopsis ........................................................................................................................................................................ 45

6. Competitive Position in the Employment Land Market ......................................................................................................... 47

7. Land Supply Analysis ............................................................................................................................................................... 48 7.1. Supply of Land by Zoning Type ...................................................................................................................................... 48

7.1.1. Supply of Industrial Land by Zoning Type ..................................................................................................................................... 50 7.1.2. Supply of Utilized and Underutilized Industrial Land ..................................................................................................................... 51 7.1.3. Size of Industrial Land by Zoning Type ......................................................................................................................................... 52 7.1.4. Airport land .................................................................................................................................................................................... 52

7.2. Supply of Commercial Land ............................................................................................................................................ 57 7.2.1. Supply of Commercial Land by Zoning Type ................................................................................................................................ 57 7.2.2. Supply of Utilized and Underutilized Commercial Land ................................................................................................................ 58 7.2.1. Size of Commercial Land by Zoning Type .................................................................................................................................... 61

8. Land Needs Analysis ................................................................................................................................................................ 61 8.1. Industrial Land Needs Analysis ...................................................................................................................................... 61 8.2. Office Needs Analysis ...................................................................................................................................................... 64 8.3. Commercial Land Needs Analysis .................................................................................................................................. 65

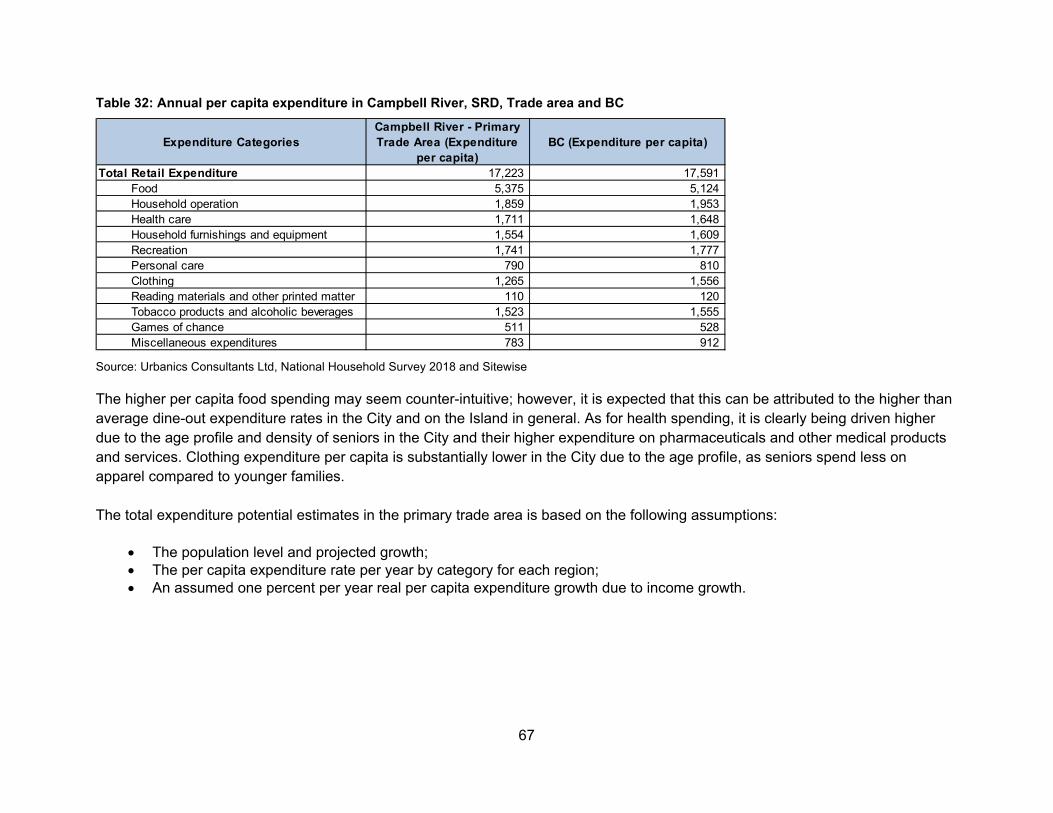

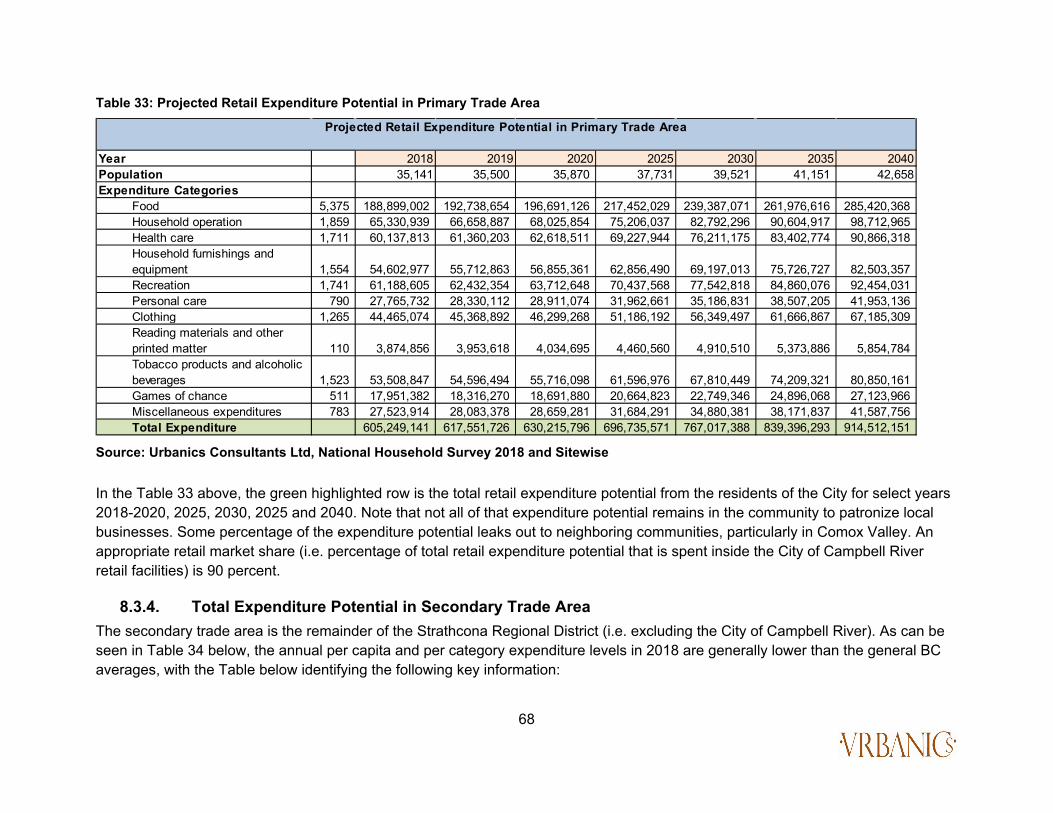

8.3.1. Trade Area Delineation ................................................................................................................................................................. 65 8.3.2. Per Capita Retail Expenditure ....................................................................................................................................................... 66 8.3.3. Total Expenditure Potential in Primary Trade Area ....................................................................................................................... 66 8.3.4. Total Expenditure Potential in Secondary Trade Area .................................................................................................................. 68 8.3.5. Warranted Floor Space ................................................................................................................................................................. 70

9. Main Findings ............................................................................................................................................................................ 76

10. Recommendations ............................................................................................................................................................... 78

9

Appendix 1 ........................................................................................................................................................................................ 81

Appendix 2 ...................................................................................................................................................................................... 108

Examples/ Typologies of Tenant Mix in Industrial Zones and Airport Zoned Lands .............................................................. 115 Campbellton Neighborhood ..................................................................................................................................................................... 115 North Campbell River Neighborhood ....................................................................................................................................................... 116 Northwest of Campbell River ................................................................................................................................................................... 117 Campbell River Airport ............................................................................................................................................................................. 118 Quinsam Heights Neighborhood .............................................................................................................................................................. 119 West of middle Inland Island Highway ..................................................................................................................................................... 119

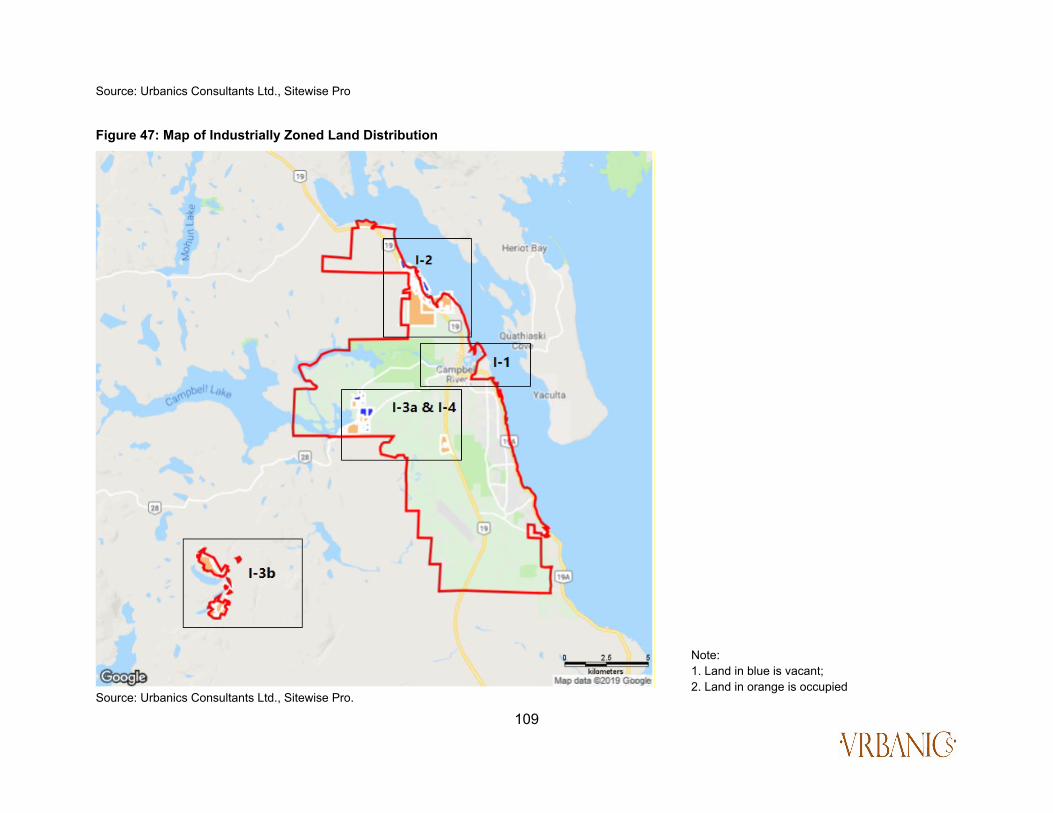

List of Figures Figure 1: Map of City of Campbell River, Study Area ....................................................................................................................... 13 Figure 2: Population Projections by Age Groups, Vancouver Island & Coast DR ........................................................................ 18 Figure 3: Historical Population in Campbell River & SRD ............................................................................................................... 20 Figure 4: Age Distribution in the City of Campbell River ................................................................................................................. 21 Figure 5: Historical Population by Age-cohort & Median Age ......................................................................................................... 22 Figure 6: Age Distribution in the SRD ................................................................................................................................................ 23 Figure 7: Past & Projected Population of Campbell River In Moderate & High Growth Scenarios .............................................. 25 Figure 8: Population Projection Distribution – the City of Campbell River (2019-2040) ............................................................... 26 Figure 9: Business Profile ................................................................................................................................................................... 40 Figure 10: Light Industry Property Tax In 2018 ................................................................................................................................. 47 Figure 11: Major industry property tax in 2018 ................................................................................................................................. 47 Figure 12: Total Supply of by Land Zoning Type .............................................................................................................................. 49 Figure 13: Supply of Industrial Land by Zoning Type ...................................................................................................................... 50 Figure 14: Employment Land in A-1 and A-2 Zoning ....................................................................................................................... 53 Figure 15: Employment Land in A - 1 Zoning .................................................................................................................................... 54 Figure 16: Employment Land in A - 2 Zoning .................................................................................................................................... 55 Figure 17: Supply of Commercial Land by Zoning Type .................................................................................................................. 58 Figure 18: Warranted Office Space Projection from 2016 to 2040 .................................................................................................. 64

10

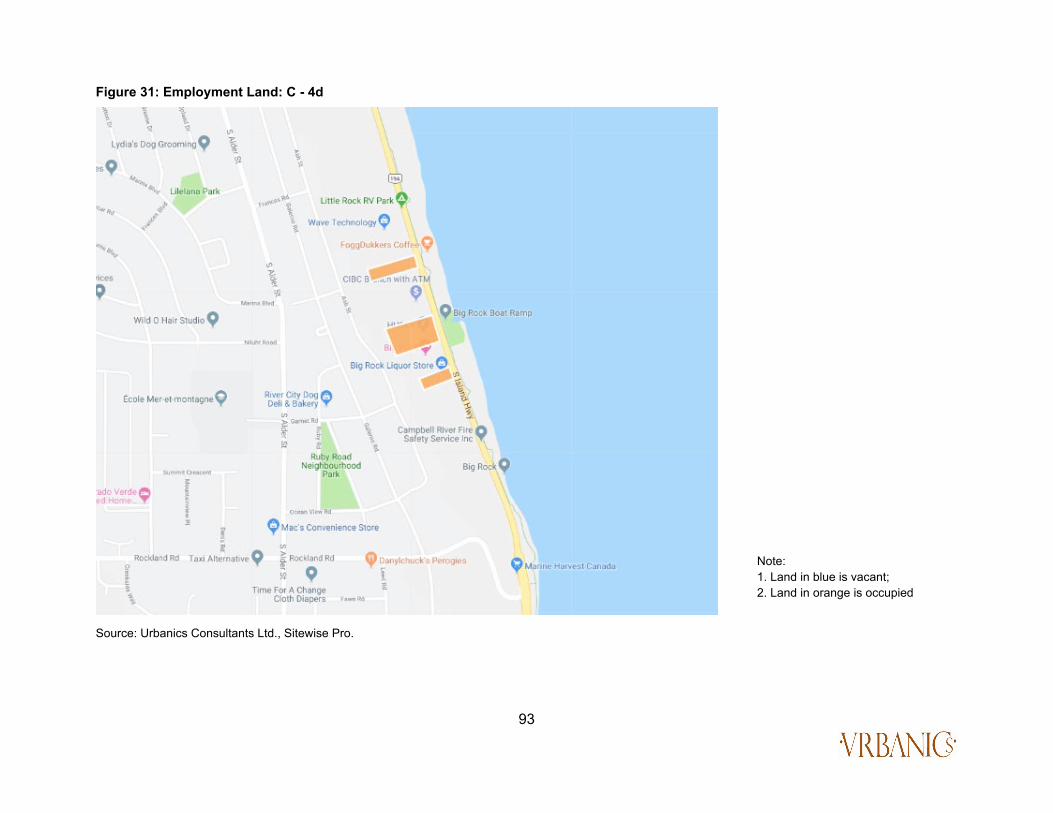

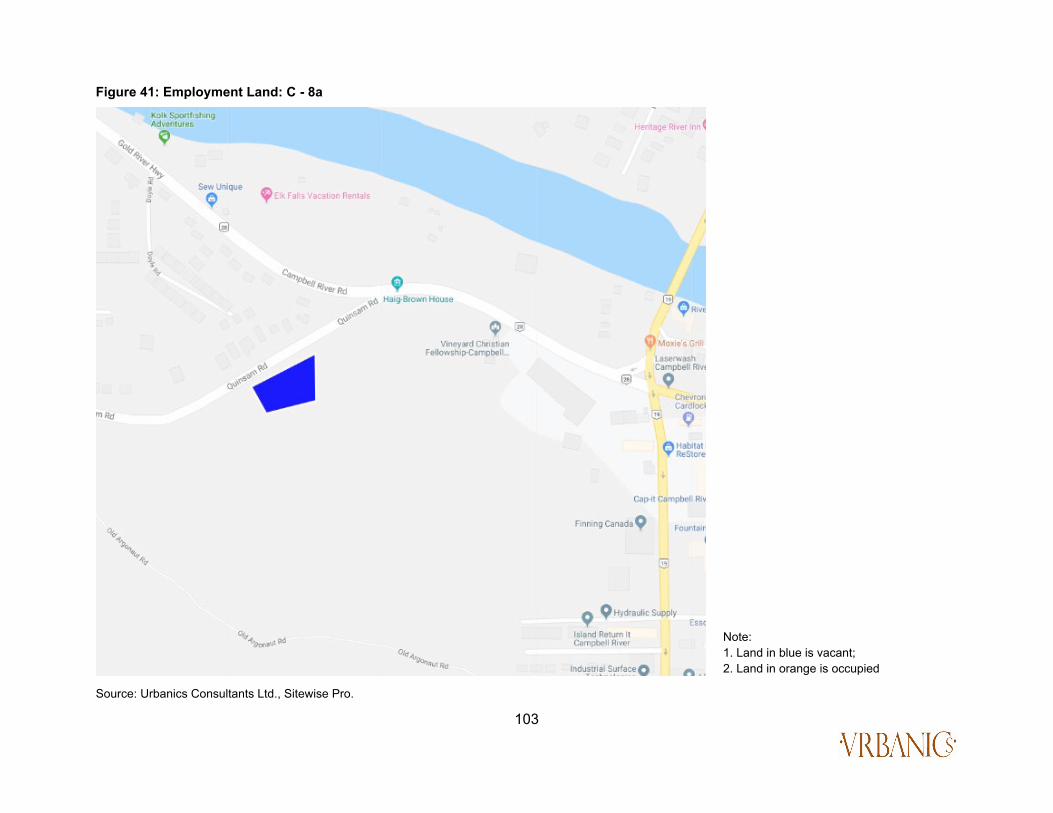

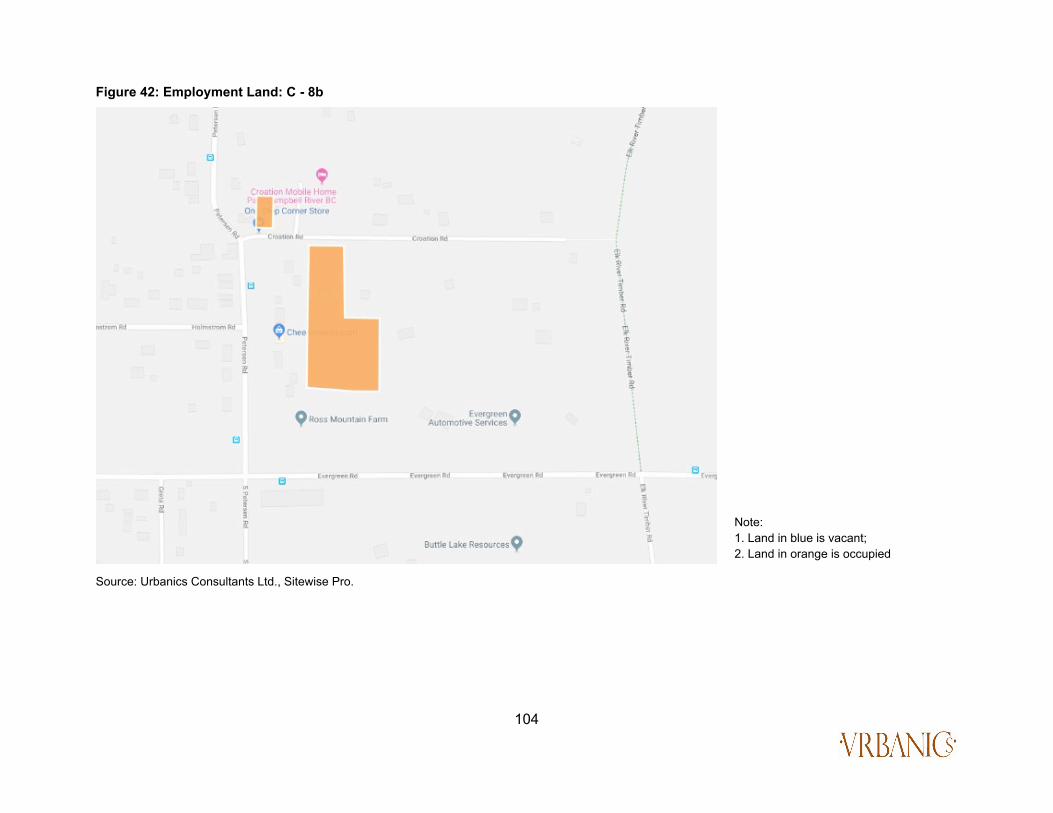

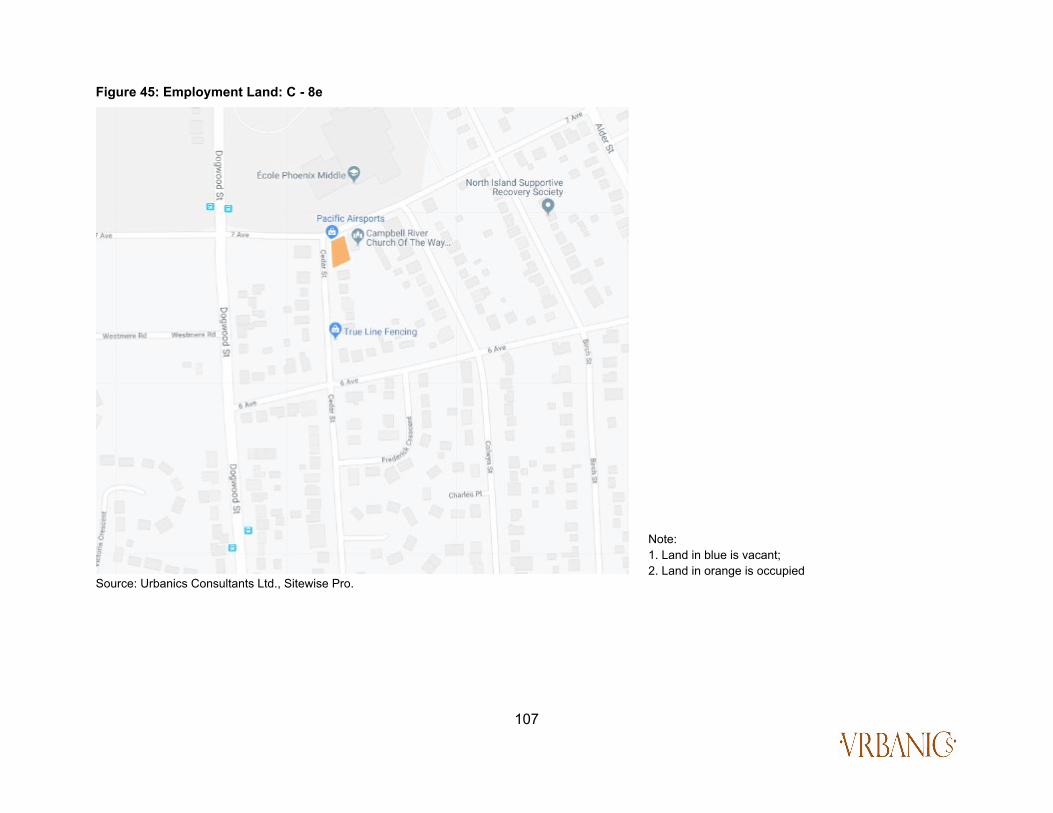

Figure 19: Commercial Land Distribution: C - 1 - C - 3 .................................................................................................................... 81 Figure 20: Commercial Land Distribution: C - 4 ............................................................................................................................... 82 Figure 21: Commercial Land Distribution: C - 5 ............................................................................................................................... 83 Figure 22: Commercial Land Distribution: C – 6 ............................................................................................................................... 84 Figure 23: Commercial Land Distribution: C - 7 & C – 8 .................................................................................................................. 85 Figure 24: Employment Land: C - 1 .................................................................................................................................................... 86 Figure 25: Employment Land: C - 2a .................................................................................................................................................. 87 Figure 26: Employment Land: C - 2b ................................................................................................................................................. 88 Figure 27: Employment Land: C - 3 .................................................................................................................................................... 89 Figure 28: Employment Land: C - 4a .................................................................................................................................................. 90 Figure 29: Employment Land: C - 4b ................................................................................................................................................. 91 Figure 30: Employment Land: C - 4c .................................................................................................................................................. 92 Figure 31: Employment Land: C - 4d ................................................................................................................................................. 93 Figure 32: Employment Land: C - 4e .................................................................................................................................................. 94 Figure 33: Employment Land: C - 5a .................................................................................................................................................. 95 Figure 34: Employment Land: C - 5b ................................................................................................................................................. 96 Figure 35: Employment Land: C - 5c .................................................................................................................................................. 97 Figure 36: Employment Land: C - 6a .................................................................................................................................................. 98 Figure 37: Employment Land: C - 6b ................................................................................................................................................. 99 Figure 38: Employment Land: C - 6c ................................................................................................................................................ 100 Figure 39: Employment Land: C - 6d ............................................................................................................................................... 101 Figure 40: Employment Land: C - 7 .................................................................................................................................................. 102 Figure 41: Employment Land: C - 8a ................................................................................................................................................ 103 Figure 42: Employment Land: C - 8b ............................................................................................................................................... 104 Figure 43: Employment Land: C - 8c ................................................................................................................................................ 105 Figure 44: Employment Land: C - 8d ............................................................................................................................................... 106 Figure 45: Employment Land: C - 8e ................................................................................................................................................ 107 Figure 46: Current Employment Land Distribution in the City of Campbell River ....................................................................... 108 Figure 47: Map of Industrially Zoned Land Distribution ................................................................................................................ 109 Figure 48: Industrial Land: I – 1 ........................................................................................................................................................ 110 Figure 49: Industrial Land: I - 2 ......................................................................................................................................................... 111

11

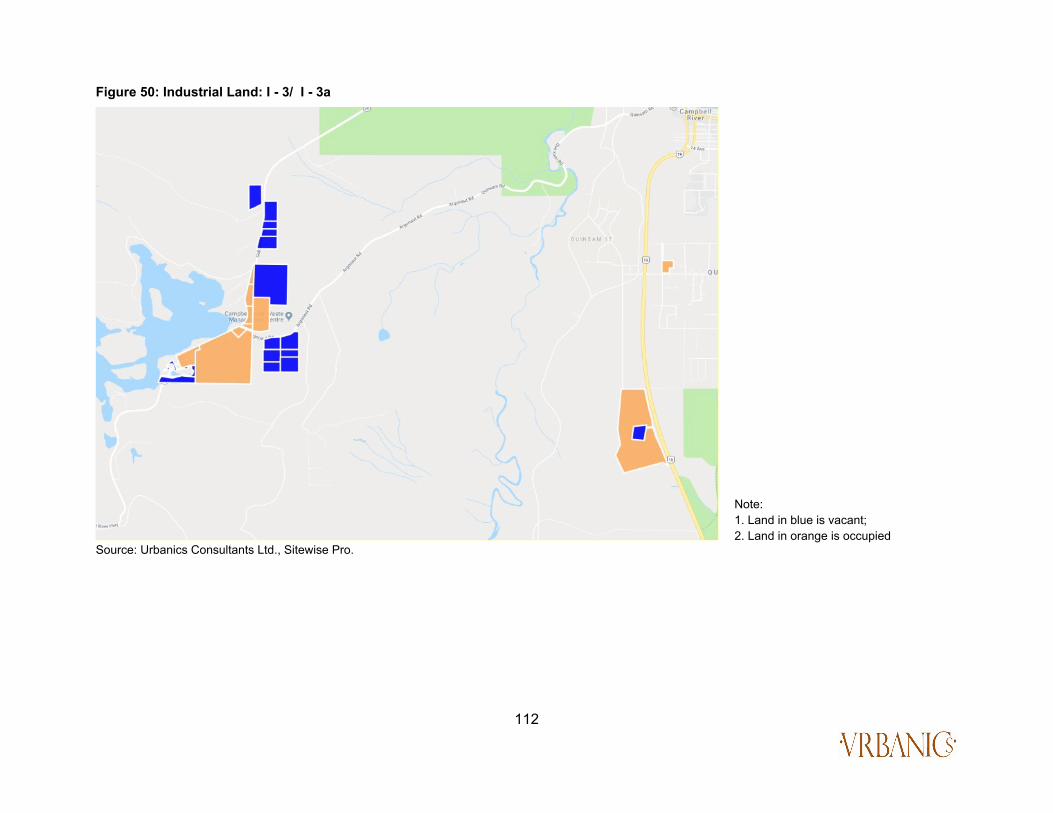

Figure 50: Industrial Land: I - 3/ I - 3a ............................................................................................................................................. 112 Figure 51: Industrial Land: I - 3/ I - 3b ............................................................................................................................................. 113 Figure 52: Industrial Land: I - 4 ......................................................................................................................................................... 114

List of Tables Table 1: Breakdown of Industrial & Commercial Zoned Areas ......................................................................................................... 2 Table 2: Population Distribution in the Development Regions, BC ................................................................................................ 18 Table 3: Population Projections by Age Groups, Vancouver Island & Coast DR .......................................................................... 19 Table 4: Age Distribution in the City of Campbell River .................................................................................................................. 21 Table 5: Age Distribution in the SRD ................................................................................................................................................. 23 Table 6: Population Projection Distribution – City of Campbell River (2019-2040) ....................................................................... 24 Table 7: Population Projection Distribution – City of Campbell River (2019-2040) ....................................................................... 25 Table 8: Economic Indicators: British Columbia .............................................................................................................................. 28 Table 9: Employment Trends in City of Campbell River .................................................................................................................. 30 Table 10: Historic Employment by Employment Categories ........................................................................................................... 31 Table 11: Employment by Industry - City of Campbell River, Vancouver Island & Coast, British Columbia (2016) .................. 32 Table 12: Location Quotient – Campbell River & Vancouver Island & Coast Economic Region (2016) ...................................... 34 Table 13: Employment Projection By Population-Based Method ................................................................................................... 36 Table 14: Population-Based Employment Projection By Employment Categories ....................................................................... 37 Table 15: Employment Projection by Constant-Share Method........................................................................................................ 37 Table 16: Constant Share Employment Projection By Employment Categories ........................................................................... 38 Table17: Prominent Land Use Zones for Industrial Uses in the City of Campbell River .............................................................. 43 Table18: Prominent Land Use Zones for Industrial Uses in the City of Campbell River .............................................................. 44 Table 19: Supply of Industrial Land by Zoning Type ........................................................................................................................ 50 Table 20: Land utilization by industrial zoning ................................................................................................................................. 51 Table 21: Land utilization by industrial zoning in percent ............................................................................................................... 51 Table 22: Size of Industrial Land by Zoning Type ............................................................................................................................ 52 Table 23: Land utilization by airport zoning ...................................................................................................................................... 56 Table 24: Land utilization by airport zoning in percent .................................................................................................................... 56 Table 25: Size of Industrial Land by Airport Zoning ......................................................................................................................... 56

12

Table 26:Supply of CommercialLand by Zoning Type ..................................................................................................................... 57 Table 27: Land utilization by commercial zoning ............................................................................................................................. 59 Table 28: Land utilization by commercial zoning as a percentage ................................................................................................. 59 Table 29: Size of Commercial Land by Zoning Type ........................................................................................................................ 61 Table 30: Industrial Land Demand Projection ................................................................................................................................... 62 Table 31: Annual per capita expenditure in Campbell River, SRD, Trade area and BC ................................................................ 66 Table 32: Annual per capita expenditure in Campbell River, SRD, Trade area and BC ................................................................ 67 Table 33: Projected Retail Expenditure Potential in Primary Trade Area ....................................................................................... 68 Table 34: Per Capita Retail Expenditure – Secondary Trade Area vs. BC ...................................................................................... 69 Table 35: Projected Retail Expenditure Potential in Secondary Trade Area .................................................................................. 70 Table 36: Total Projected Retail Expenditure Potential - Capture - Warranted Floorspace- Commercial Land Demand .......... 75

13

1. Introduction 1.1 Contextual overview This study applies to the City of Campbell River. The City of Campbell River is on the east coast of Vancouver Island at the south end of Discovery Passage, along the important Inside Passage shipping route. At over 35,000 people, the City is the most populous community in the Strathcona Regional District (SRD) and third largest City on Vancouver Island. The primary economic activities in the City include aerospace, forestry and technology. This study was commissioned by the City to gain a better understanding of the supply-demand characteristics of its employment lands (lands zoned for industrial and commercial uses) and to develop strategies that inform the economic development and business pursuits of the City. Urbanics Consultants Ltd. has been retained by the City of Campbell River to undertake an Employment Lands Study which will aid in creating an inventory of employment land, estimating the need for employment land over the next 20 years, and developing an employment land strategy for the City of Campbell River. The study area is shown as in Figure 1.

Figure 1: Map of City of Campbell River, Study Area

Source: Urbanics Consultants Ltd., Sitewise

14

1.2 Employment Land Study The study evaluates the capacity of existing employment lands within the City and the scale of demand for various categories of employment land. The study has greatly benefitted from feedback from key stakeholders and staff from the City. Much of the feedback was obtained through three methods of engagement: online survey, stakeholder interviews and a stakeholder consultation session (conducted at the Comfort Inn on Friday, March 22, 2019). Key stakeholders participating in the consultation included major industrial property & business owners, and City staff. The purpose of the consultation was to inform stakeholders of preliminary study findings, receive feedback and to engage stakeholders in confirming their perceived challenges and opportunities in relation to business and investment in the City. The workshop included participant engagement exercises that tested ideas and encouraged dialogue among the different stakeholders. Consultation participants provided important and insightful anecdotal information related to a sector based economic outlook for the City, the challenges faced by various industry sectors in the City and the opportunities that can be capitalized on for achieving long-term economic stability. These insights are applied throughout the report and to develop approaches for creating an employment strategy for a more sustainable City. The key highlights are aggregated in the SWOT (Strengths, Weaknesses, Opportunities, Threats) summary below. 1.3 Methodology The Consultant utilized a broad and deep methodology for conducting the Employment Lands Strategy study. This process is set out below. 1.3.1 Review of previous studies and policies governing land use The Consultant collected and reviewed pertinent policies and regulations governing employment land use as well as studies related to employment lands in the City, including:

• City of Campbell River – Community Profile (2016 and 2019) • Airport Master Plan - Sept 2016 • Sustainable Official Community Plan • Zoning bylaw 3250, 2006, 2018

15

• GPRA’s City of Campbell River Downtown Growth Analysis 2016 • State of the Island Economic Report (2017 and 2018)

1.3.2 Demographics analysis Publicly available datasets from Statistics Canada and BC Stats were used to examine the demographic characteristics of the City. Projected population growth estimates from BC Stats were utilized to identify the impacts of growth in the region.

1.3.3 Economic base analysis Publicly available datasets from Statistics Canada, BC Stats, and the Canadian Labour Force Survey were used to examine the provincial, regional and local economic markets. These datasets included regional employment trends, with a focus on employment sectors that are key to the City. The study also examines the growth of small-business employment in the City, with a focus on small, innovative companies locating in industrial areas.

1.3.4 Supply analysis Parcel-level BC Assessment data and consolidated parcel-level zoning information was analyzed to document a quantitative and qualitative inventory of the existing supply of employment land within the City. This included the determination of utilized, vacant and underutilized industrial lands, servicing characteristics, and location attributes of the employment lands (i.e., in terms of proximity to work force, customer base and transportation and utility infrastructure).

1.3.5 Demand Analysis Based on the projected population growth, employment-based growth and historical employment land growth rates, the Consultant has projected how economic drivers could shape the employment land market over the next 20 years (2020 through to 2040). These employment land demand projections are corroborated by historical industrial and commercial permit information. Reconciling the results of these two methods enabled the Consultant to quantify employment land use demand in the City as well as evaluate whether the current supply of employment land could accommodate projected demand.

1.3.6 Community engagement The study methodology utilized a three-step method of engagement that began with identifying and informing the affected stakeholders, moved forward with a stakeholder survey and interviews to engage stakeholders and solicit strategic and general feedback, and a stakeholder consultation event to engage stakeholder and the broader community on the study results and their

16

implications. The results from the stakeholder consultation along with feedback from key stakeholders has provided insightful information regarding employment lands in the City and has greatly enriched this study.

1.3.7 Findings and Recommendations The final section of the study provides the most notable findings from an in-depth employment land supply and demand analysis in the City forecasted over the next 20 years (2020 through to 2040) and recommendations.

1.3.8 Limitations This study involves macro-level analyses of the City of Campbell River, which relies on data from a variety of sources, including the Statistics Canada, BC Stats and many others. Background data for this study was obtained from a variety of public (federal, provincial, regional, and municipal) and private sector sources during the period of Jan to May 2019. As a result, similar to market studies of this nature, this study has several limitations that might arise from the quality of background data, for example, the study relies on population growth projections from P.E.O.P.L.E. 2018, BC Stats, which makes several assumptions regarding the economy, migration and population trends. Moreover, this study makes a number of forecasts and assumptions regarding the state of the economy, future competitive influences, and population and employment projections, that may shift due to changes in regulatory environment, regional, provincial and global economy as well as natural triggers. These assumptions are made with great care and are based on the most recent and reliable information developed from research of the market and knowledge of the industry. Should these or any of the other assumptions noted in this study, be undermined by the course of future events, the Consultant recommends that the study’s findings be re-examined. It should also be noted that this study does not assess the impact of employment land development on the First Nation Lands within the City. It is expected that these two factors will affect industrial and commercial development in the City and there is value in exploring the projected impact.

17

2. Demographic Analysis 2.1. Vancouver Island and Coast Context The Vancouver Island and Coast Development Region1 is one of the eight development regions in the Province of BC. The others include:

• Mainland / Southwest Cariboo • Thompson – Okanagan Kootenay • North Coast Nechako • Northeast.

The Vancouver Island and Coast Development Region extends from Vancouver Island to the areas north of the Mainland/ Southwest development region. The Vancouver Island and Coast Development Region itself is comprised of nine Regional Districts (Alberni-Clayoquot, Capital, Central Coast, Comox Valley, Cowichan Valley, Mount Waddington, Nanaimo, Powell River and Strathcona). Naturally, each District possesses a relatively locationally indicative economic profile. The Capital Regional District (CRD), one of the most urbanized and populated of the regional districts, depends largely on service industries, public administration, post-secondary activities, and tourism as major economic drivers. The other regional districts are highly dependent on goods-producing industries such as logging and forest products, manufacturing, and mining. In addition, several communities on the east coast of Vancouver Island have become popular destinations for retirees. The Vancouver Island and Coast Development Region is the second-most populous, urbanized and dense regions in the Province. Due in part to increased migration rates, the region is expected to grow steadily over the 2016-2036, from a population of 805,870 in 2016 to 970,280 by 2036. However, the growth rate is expected to slow down to 0.6 percent during the period from 2036 to 2041. This translates into an annual growth rate of approximately 0.8 percent during the period 2016 to 2021, and 1.0 percent during the period 2016 to 2021 (Table 2). Overall, the Vancouver Island and Coast Development Region has a high proportion of its population aged 65 years and over. More specifically, 23 percent of the Region’s entire population (or approximately 184,457 people) is aged 65 years and over in 2016.

This share is expected to grow to 30 percent by 2041 (approximately 304,263 people). Further, while the population in the age group 18-65 will maintain its dominant share, its overall proportion is expected to decline from 64 percent in 2016 to 58 percent by 2041 (Table 2 and Figure 2).

1 Development Regions are large geographical regions that are formed by grouping several Regional Districts (geographical regions created by the Provincial Government for delivery of certain services). Development Regions provide a better unit for economic analysis, labour force surveys and employment projections.

18

Table 2: Population Distribution in the Development Regions, BC

Source: Urbanics Consultants Ltd., BC Stats

Year 2001 2006 2011 2016 2016/B.C. 2021 2026 2031 2036 2041 2041/B.C.1 B.C. 4,076,881 4,241,691 4,499,139 4,757,658 100% 5,039,706 5,343,319 5,644,989 5,923,919 6,178,287 100%2 Mainland/Southwest 2,402,949 2,529,711 2,725,373 2,933,973 62% 3,126,149 3,344,031 3,565,368 3,774,709 3,969,202 64%3 Vancouver Island and Coast 710,867 744,293 772,912 805,870 17% 848,779 892,335 933,805 970,280 1,001,694 16%4 Thompson Okanagan 480,059 502,454 529,617 552,023 12% 587,196 618,501 648,461 674,923 698,350 11%5 Cariboo 166,133 157,582 157,201 154,277 3% 155,177 156,677 157,429 157,144 156,111 3%6 Kootenay 147,041 143,351 148,470 148,580 3% 149,709 151,934 153,688 154,740 155,204 3%7 North East 62,100 65,505 67,822 67,987 1% 71,510 75,625 79,585 83,426 87,344 1%8 North Coast 65,620 59,775 57,201 54,083 1% 54,511 56,323 57,626 58,728 59,664 1%9 Nechako 42,112 39,020 40,543 40,865 1% 46,675 47,893 49,027 49,969 50,718 1%

Figure 2: Population Projections by Age Groups, Vancouver Island & Coast DR

Source: Urbanics Consultants Ltd.

19

Table 3: Population Projections by Age Groups, Vancouver Island & Coast DR

2.2. The City of Campbell River Context BC Stats has improved the efficacy of raw census data and it is held that the data from BC Stats depicts a more accurate picture of the population estimation in British Columbia. Therefore, the BC Stats population estimates and projections were applied in the population projection for Strathcona Regional District and the City of Campbell River.

2.2.1. Historical Population Growth Given the fact that there is no population projection by BC Stats specifically for the City of Campbell River, a historical population analysis was conducted for Strathcona Regional District (SRD) and the City. The analysis shows a distinct relationship between the population growth in the SRD and the City. The Consultant applied this relationship to derive the population projection of the City of Campbell River from the population projection of the SRD. According to BC Stats population estimates for the period between 2001 to 2018, the population in the SRD grew from 41,786 to 48,135, indicating an average annual growth rate of 0.84 percent. In contrast, the population in the City grew from 29,173 to 35,141

Year 1986 1991 1996 2001 2006 2011 2016 2021 2026 2031 2036 2041 0-4 36,839 39,704 40,425 32,977 31,727 33,881 34,631 35,422 36,967 37,358 36,850 36,797 5-14 71,620 81,644 91,200 85,409 78,195 71,469 71,266 76,645 79,864 82,869 84,910 84,518 15-24 82,767 79,611 87,133 90,066 94,419 91,796 91,271 86,093 85,409 91,451 95,446 98,997 25-44 172,356 201,295 217,509 195,563 182,319 183,443 187,580 205,158 215,907 216,555 219,918 220,575 45-64 111,518 127,598 158,600 188,473 227,047 242,212 236,665 225,049 219,131 224,856 237,969 256,544 65+ 81,668 99,065 109,913 118,379 130,586 150,111 184,457 220,412 255,057 280,716 295,187 304,263 All Ages 556,768 628,917 704,780 710,867 744,293 772,912 805,870 848,779 892,335 933,805 970,280 1,001,694

Share of Population(%) 15-64 66% 65% 66% 67% 68% 67% 64% 61% 58% 57% 57% 58% 65+ 15% 16% 16% 17% 18% 19% 23% 26% 29% 30% 30% 30%

Annual Growth Rate(%), All Ages 2.5% 2.3% 0.2% 0.9% 0.8% 0.8% 1.0% 1.0% 0.9% 0.8% 0.6%

Source: Urbanics Consultants Ltd. and BC Stats

20

with an average annual growth rate of 1.10 percent. The following Figure depicts the population growth trend in both the SRD and the City. The BC Stats projection of the SRD population is considered to be reliable for this purpose due to the fact that BC Stats uses a methodology that accounts for fertility rates, mortality rates, and migration rates. As shown in Figure 3, the City has a greater population growth rate than that of the SRD. Therefore, the City represents an increasing share of the SRD’s population. It is expected that this trend will continue and has applied this trend as the assumption for the population projection for the City. It is assumed that the its population will continue to grow with respect to the SRD as reflected in the historical trends.

Figure 3: Historical Population in Campbell River & SRD

Source: Urbanics Consultants Ltd., BC Stats

21

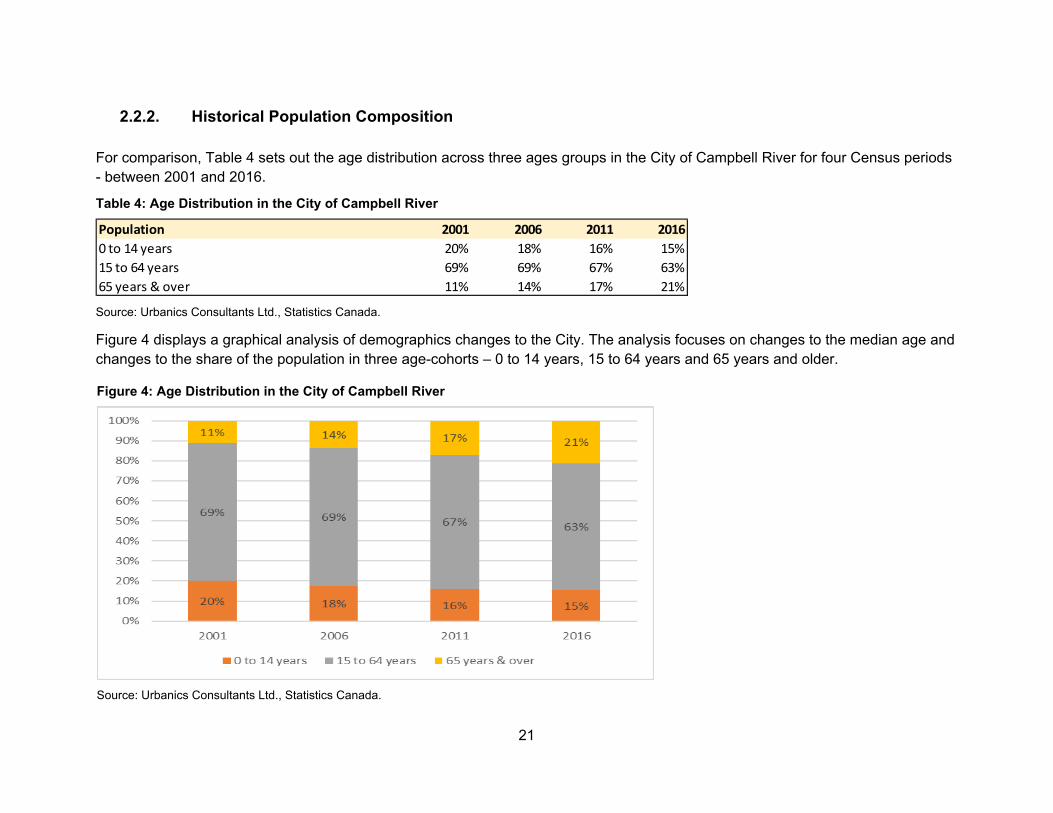

2.2.2. Historical Population Composition For comparison, Table 4 sets out the age distribution across three ages groups in the City of Campbell River for four Census periods - between 2001 and 2016.

Table 4: Age Distribution in the City of Campbell River

Source: Urbanics Consultants Ltd., Statistics Canada. Figure 4 displays a graphical analysis of demographics changes to the City. The analysis focuses on changes to the median age and changes to the share of the population in three age-cohorts – 0 to 14 years, 15 to 64 years and 65 years and older.

Population 2001 2006 2011 20160 to 14 years 20% 18% 16% 15%15 to 64 years 69% 69% 67% 63%65 years & over 11% 14% 17% 21%

Figure 4: Age Distribution in the City of Campbell River

Source: Urbanics Consultants Ltd., Statistics Canada.

22

Figure 5: Historical Population by Age-cohort & Median Age

Source: Urbanics Consultants Ltd., Statistics Canada. The median age of the City increased from 38.1 in 2001 to 46.5 in 2016. The size of the 15 to 64 years age-cohort (i.e., the working-age cohort), decreased from 69 percent of the population in 2001 to 63 percent in 2016 (decrease of 1,025). The share of the population under the age of 14 also decreased from 20 percent to 15 percent (decrease of 680) while the share of the population in the 65 year and older age-cohort increased from 11 percent to 21 percent (increase of 3,775). Similar to Vancouver Island and Coast Development Region, it is evident that the population of the City is becoming more concentrated in the 65 and over demographic. The implications of these demographic shifts will be addressed in the employment projection section and employment land demand section of this report.

23

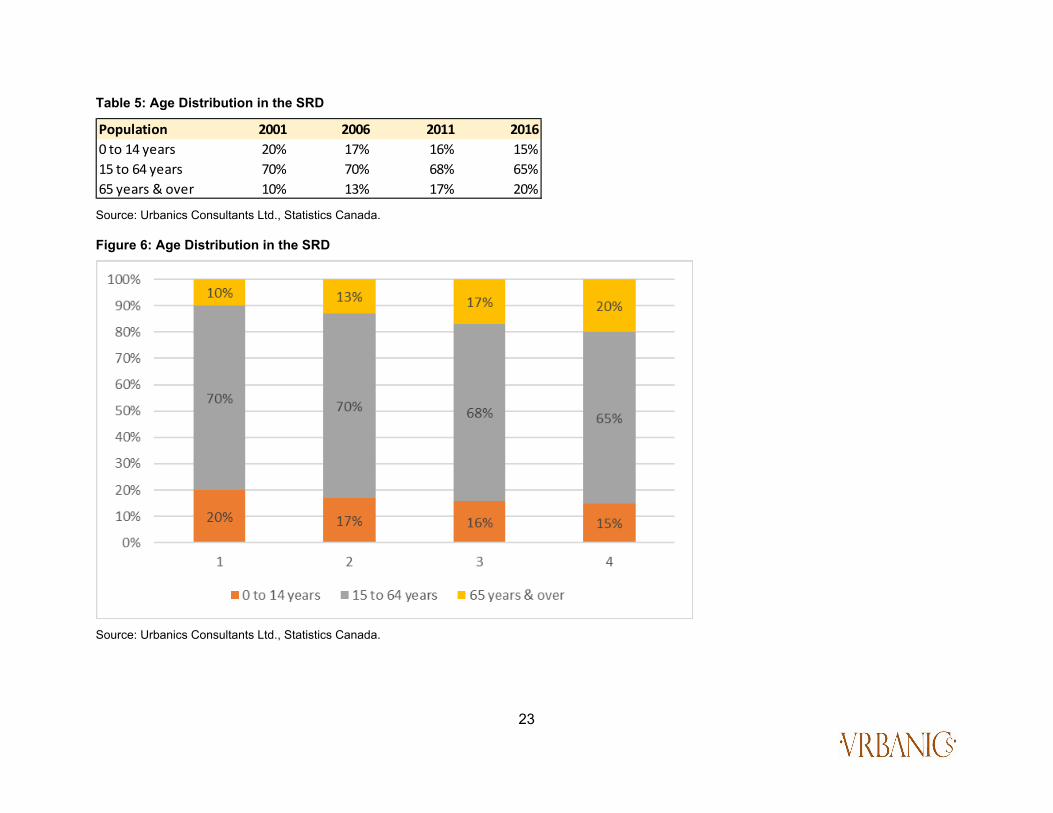

Table 5: Age Distribution in the SRD

Source: Urbanics Consultants Ltd., Statistics Canada. Figure 6: Age Distribution in the SRD

Source: Urbanics Consultants Ltd., Statistics Canada.

Population 2001 2006 2011 20160 to 14 years 20% 17% 16% 15%15 to 64 years 70% 70% 68% 65%65 years & over 10% 13% 17% 20%

24

During the period 2001 to 2016, the population composition in the SRD was similar to the City across three age-cohorts as a percentage of the total population. The assumption has been made that the population composition of the City will resemble the population composition of the SRD in the future, which forms the second factor for the population projection.

2.2.3. Population Projection Based on the assumptions that the City’s population will continue to grow as a commensurate percentage of the SRD, a population projection was prepared for City of Campbell River using 2018 as a base year and projecting growth to the year 2040. The projections were conducted by forecasting population growth in the City by age-cohort and gender utilizing BC stats projection for the SRD. In view of the projection analysis, moderate and high growth projection scenarios were selected for development. In the moderate growth scenario, the projections were conducted by forecasting population growth in the City by age-cohort and gender utilizing the BC stats projection for the SRD as described above. In the high growth scenario, a 0.2 percent additional increase per year was included specifically as a result of the completion of CRadvantage and the successful attraction of high speed, broadband fibre optic network reliant employment drivers moving to the City. There can be other drivers from established employment sectors that can also experience significant growth and commensurate employment. Examples can include aquaculture, value-added wood processing and aeronautics. However, the 0.2 percent increase was ascribed to the CRadvantage given its potential significance as a cross-cutting economic generator. As shown in the Figure 7, the population of the City is expected to grow from 35,141 in 2018 to 42,658 in 2040 in the moderate growth scenario and to 44,470 in 2040 in the high growth scenario. Table 6: Population Projection Distribution – City of Campbell River (2019-2040)

Source: Urbanics Consultant Ltd., Statistics Canada and BC Stats

Population 2019 2020 2025 2030 2035 20400-14 years 14% 14% 14% 13% 13% 13%15-64 years 61% 60% 57% 55% 56% 57%65+ years 25% 26% 29% 31% 31% 30%Total Population 100% 100% 100% 100% 100% 100%

25

Figure 7: Past & Projected Population of Campbell River In Moderate & High Growth Scenarios

Source: Urbanics Consultants Ltd., BC Stats.

Table 7: Population Projection Distribution – City of Campbell River (2019-2040)

Source: Urbanics Consultant Ltd., Statistics Canada and BC Stats

Population 2019 2020 2025 2030 2035 20400-14 years 14% 14% 14% 13% 13% 13%15-64 years 61% 60% 57% 55% 56% 57%65+ years 25% 26% 29% 31% 31% 30%Total Population 100% 100% 100% 100% 100% 100%

26

The City of Campbell River has a high proportion of population aged 65 years and over and the share of the population is expected to grow to 30 percent by 2040 (approximately 12,797 people) of this age cohort. While the population in the age group 18 – 64 years old will maintain its dominant share of the population, its share of the population is expected to decline significantly from 63 percent in 2016 to 55 percent by 2030, however age group from 18 – 64 years old is expected to increase beginning in 2030. Of particular importance is the growth of the working-age cohort, or those between the ages of 15 and 64, as this age-cohort will be utilized for the employment projection. The share of the working-age cohort is expected to decrease from 61 percent of the population in 2019 to 57 percent in 2040, however, in absolute terms it is expected to grow by 2,660 people between 2019 and 2040. Conversely, the share of the 65 and over age-cohort is expected to increase from 25 percent to 30 percent and the 14 years and under age-cohort is remain stable around 14 percent. It is expected that the population of the City will realize growth in each age-cohort, with the working-age cohort growing modestly, and the population share concentrated among the 65 years old and over cohort increasing significantly.

Figure 8: Population Projection Distribution – the City of Campbell River (2019-2040)

Source: Urbanics Consultant Ltd., Statistics Canada and BC Stats

27

3. Economic Base Analysis 3.1. Provincial economy

This section provides a brief economic outlook of the provincial economy. These macro-economic indicators are some of the important drivers at the provincial level. The following terms may be defined as:

• Real Gross Domestic Product (GDP) is an inflation-adjusted measure that reflects the value of all goods and services produced by an economy in a given year, expressed in base-year prices;

• Nominal Gross Domestic Product is a measure of the value of all finished goods and services produced by a country at their current market prices;

• Employment is number of people who have a job as a percentage of the working age population; • Unemployment rate is the share of the labor force that is jobless, expressed as a percentage; • Retail sales refers to purchases of finished goods and services by consumers and businesses; • Housing starts the number of new houses begun during a particular period; and, • Consumer Price Index an index of the variation in prices paid by typical consumers for retail goods and other item

The Province of British Columbia is expected to display stable GDP growth in 2019, primarily as a result of strong job growth and a robust housing market. According to RBC Economics Provincial Outlook March 2019, British Columbia’s Real GDP output grew by an estimated 1.7 percent in 2018 and is projected to grow by 2.5 percent in 2019 and 2.5 percent in 2020 (Table 8). According to RBC Economics Provincial Outlook March 2019, the Province is expected to display growth in employment in 2019 at a higher percent change as compared to the previous year (1.1 percent in 2018 as compared to 1.8 percent in 2019). The anticipated growth in employment as well as increase in home value gains are expected to lead to increases in consumer spending in the retail sales in the Province. The Province is expected to display strong growth in retail sales in 2019 (3.7 percent in 2019) and a higher rate of growth in 2020 (3.9 percent in 2020). However, housing starts are expected to decrease in 2019 and 2020 as compared to the last few years (from 40,900 in 2018 to 36,900 in 2019). The decline may be due to a low inventory of affordable housing across the Province with rising construction costs and cost of land. Overall, the Province is expected to experience continued economic growth and strong demand for housing in the near future. However, this also assumes that the impact of wildfires on the economy is localized and that the softwood lumber trade conflict with the US does not escalate further; the latter is of particular importance to the City.

28

The following section will address economic trends in the City of Campbell River and Vancouver Island and Coast that will have an affect on the demand for employment lands.

3.2. Historical Employment Trends Displayed in Table 9 are jobs by industry sector in Campbell River between 2006 and 2016. Industry sectors are classified using the North American Industry Classification System (NAICS), which segments industries into twenty distinct sectors that are categorized as either goods-producing or service-producing industries. The central economic activity classes in the City, in terms of employment numbers, are:

• agriculture; forestry; fishing and hunting (primarily forestry); • construction; • manufacturing; • retail trade; • transportation and warehousing; • professional; scientific and technical services

Table 8: Economic Indicators: British Columbia

Source: RBC Economics, Provincial Outlook (March 2019)

2012 2013 2014 2015 2016 2017 2018F 2019F 2020FReal GDP

% change 2.5 2.2 3.7 2.1 3.2 3.8 1.7 2.5 2.5Nominal GDP

% change 2.1 3.4 5.7 2.9 6 6.9 4.1 3.9 4.9Employment

% change 1.6 0.1 0.6 1.2 3.2 3.7 1.1 1.8 0.7Unemployment Rate (%)

rate % 6.8 6.6 6.1 6.2 6 5.1 4.7 4.7 4.8Retail Sales

% change 1.9 2.8 6.3 7 7.7 9.3 2 3.7 3.9Housing Starts 000's of

units 27.5 27.1 28.4 31.4 41.8 43.7 40.9 36.9 34Consumer Price Index

% change 1.1 -0.1 2.6 1.1 1.9 2.1 2.7 1.8 2.2

Economic Indicators

29

• health care and social assistance; and, • accommodation and food services (tourism). Among these eight industry classes, employment numbers (highlighted yellow in Table 9) within health care and social assistance class has experienced the highest annual growth rate of 5 percent during the period 2006 to 2016. Construction has the second highest annual growth rate at 4.4 percent for the same period. The annual growth rate for transportation and warehousing, together with professional, scientific and technical services was at 2.4 percent and 2.2 percent respectively. Despite the employment numbers decreasing slightly during the 2006 to 2016 period, agriculture, forestry, fishing and hunting (9 percent), retail trade (14 percent) and accommodation and food services (9 percent) combine to provide 32 percent of the total jobs in the City in 2016 (These three industries are highlighted green in Table 9). It is important to note that jobs in the manufacturing sector (highlighted blue in Table 9) have declined from 1,505 to 650. This can be accounted for, in part, by the 2009 closure of the Elk Falls Division of Catalyst Paper that saw a loss of over 500 jobs. In terms of percent distribution of all industries, manufacturing (10 percent) ranked second among all industries in 2006, but this percentage has dropped from 10 percent in 2006 to 4 percent in 2016 (a total loss of 855 jobs). According to the most recent Statistics Canada data, Campbell River experienced an employment rate of 54.1 percent which is significantly lower than the provincial average at 59.6 percent. In summary, the highest concentration of jobs in Campbell River are in the following industry sectors: • Agriculture, forestry, fishing and hunting: 9% or 1,495 jobs • Construction: 10% or 1,510 jobs • Retail trade: 14% or 2,170 jobs • Health care and social assistance: 13% or 2,125 jobs • Accommodation and food services: 9% or 1,475 jobs

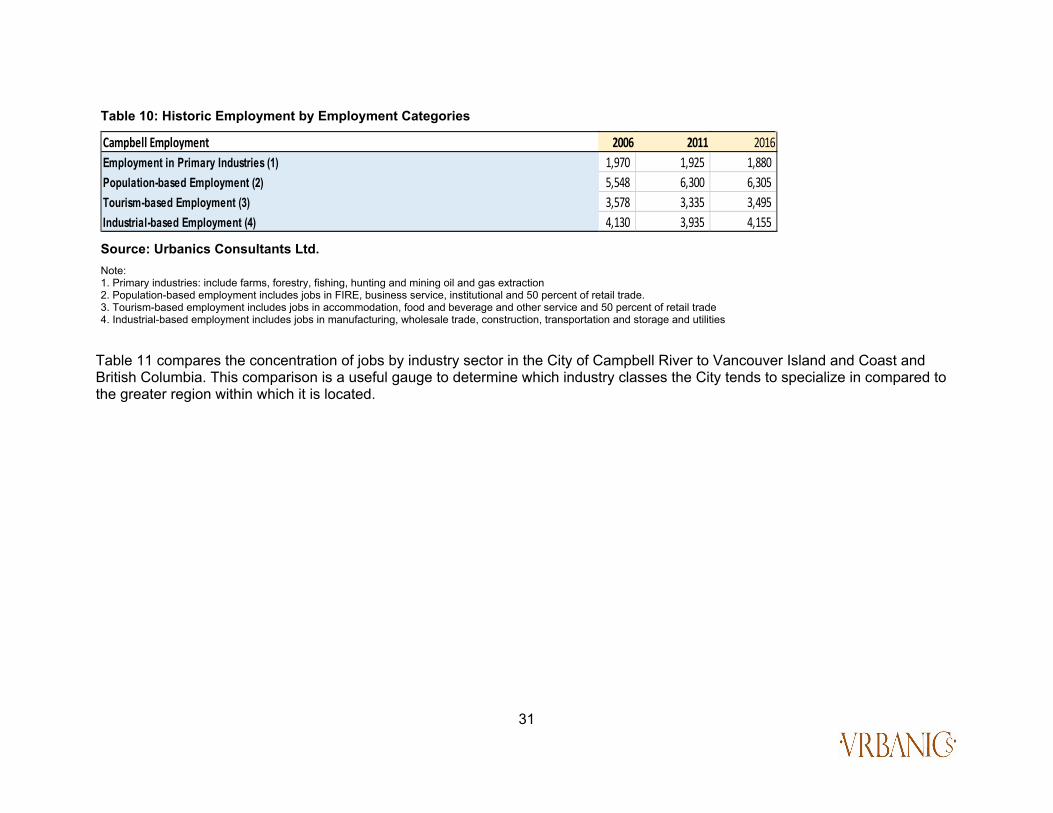

Jobs in all industries were disaggregated into the four categories in Table 10; these include employment in primary industries, population-based employment, tourism-based employment and industrial-based employment. As seen in Table 10, most of the jobs increase came from population-based employment from for the three Census periods 2006, 2011, and 2016. Tourism based employment was at 3,495, while industrial-based employment was at 4,155 in 2016. Employment in primary industries is the least significant within these categories (which is reflective of the on-going shift in this sector).

30

Table 9: Employment Trends in City of Campbell River

Source: Urbanics Consultants Ltd. & Statistics Canada

Employment Trends in City of Campbell River 2006 2011 2016 2006-2016(Annualized 10 year growth rate)Total Labour Force population (15 years+) by Industry - NAICS 2012 15,625 15805 16185 0.4% Industry - NAICS2012 - not applicable 365 310 350 -0.4% All industry categories 15,255 15495 15835 0.4% 11 Agriculture; forestry; fishing and hunting 1535 (10%) 1215 (8%) 1495 (9%) -0.3% 21 Mining; quarrying; and oil and gas extraction 435 710 385 -1.2% 22 Utilities 75 140 105 3.4% 23 Construction 985 (6%) 1350 (9%) 1510 (10%) 4.4% 31-33 Manufacturing 1505(10%) 665(4%) 650 (4%) -8.1% 41 Wholesale trade 335 390 345 0.3% 44-45 Retail trade 2210 (14%) 2445 (16%) 2170 (14%) -0.2% 48-49 Transportation and warehousing 580 (4%) 730 (5%) 735 (5%) 2.4% 51 Information and cultural industries 240 230 175 -3.1% 52 Finance and insurance 320 480 380 1.7% 53 Real estate and rental and leasing 325 335 300 -0.8% 54 Professional; scientific and technical services 650 (4%) 660 (4%) 810 (5%) 2.2% 55 Management of companies and enterprises 15 0 20 2.9% 56 Administrative and support; waste management and remediation services 625 515 600 -0.4% 61 Educational services 875 765 805 -0.8% 62 Health care and social assistance 1305 (9%) 1815 (12%) 2125 (13%) 5.0% 71 Arts; entertainment and recreation 275 425 340 2.1% 72 Accommodation and food services 1560 (10%) 1180 (8%) 1475 (9%) -0.6% 81 Other services (except public administration) 775 720 765 -0.1% 91 Public administration 615 725 665 0.8%

31

Table 11 compares the concentration of jobs by industry sector in the City of Campbell River to Vancouver Island and Coast and British Columbia. This comparison is a useful gauge to determine which industry classes the City tends to specialize in compared to the greater region within which it is located.

Table 10: Historic Employment by Employment Categories

Source: Urbanics Consultants Ltd. Note: 1. Primary industries: include farms, forestry, fishing, hunting and mining oil and gas extraction 2. Population-based employment includes jobs in FIRE, business service, institutional and 50 percent of retail trade. 3. Tourism-based employment includes jobs in accommodation, food and beverage and other service and 50 percent of retail trade 4. Industrial-based employment includes jobs in manufacturing, wholesale trade, construction, transportation and storage and utilities

Campbell Employment 2006 2011 2016Employment in Primary Industries (1) 1,970 1,925 1,880 Population-based Employment (2) 5,548 6,300 6,305 Tourism-based Employment (3) 3,578 3,335 3,495 Industrial-based Employment (4) 4,130 3,935 4,155

32

Table 11: Employment by Industry - City of Campbell River, Vancouver Island & Coast, British Columbia (2016)

Source: Statistics Canada, Urbanics Consultants Ltd.

Employment by Industry Campbell River British ColumbiaEmployment %Base Employment %Base Employment %Base

Total Labour Force population (15 years+) by Industry - NAICS 2012 16,185 100.0% 403,190 100.0% 2,471,665 100.0% Industry - NAICS2012 - not applicable 350 2.2% 7,145 1.8% 43,805 1.8% All industry categories 15,835 97.8% 396,045 98.2% 2,427,865 98.2% 11 Agriculture; forestry; fishing and hunting 1,495 9.2% 13,640 3.4% 65,205 2.6% 21 Mining; quarrying; and oil and gas extraction 385 2.4% 2,925 0.7% 25,920 1.0% 22 Utilities 105 0.6% 1,295 0.3% 12,445 0.5% 23 Construction 1,510 9.3% 32,090 8.0% 199,985 8.1% 31-33 Manufacturing 650 4.0% 17,945 4.5% 157,560 6.4% 41 Wholesale trade 345 2.1% 7,810 1.9% 82,105 3.3% 44-45 Retail trade 2,170 13.4% 49,290 12.2% 283,135 11.5% 48-49 Transportation and warehousing 735 4.5% 16,480 4.1% 128,400 5.2% 51 Information and cultural industries 175 1.1% 7,385 1.8% 67,225 2.7% 52 Finance and insurance 380 2.3% 11,255 2.8% 93,805 3.8% 53 Real estate and rental and leasing 300 1.9% 7,605 1.9% 54,995 2.2% 54 Professional; scientific and technical services 810 5.0% 27,650 6.9% 196,670 8.0% 55 Management of companies and enterprises 20 0.1% 345 0.1% 4,320 0.2% 56 Administrative and support; waste management and remediation services 600 3.7% 18,365 4.6% 109,095 4.4% 61 Educational services 805 5.0% 29,470 7.3% 173,820 7.0% 62 Health care and social assistance 2,125 13.1% 53,455 13.3% 270,855 11.0% 71 Arts; entertainment and recreation 340 2.1% 10,130 2.5% 57,940 2.3% 72 Accommodation and food services 1,475 9.1% 34,980 8.7% 207,045 8.4% 81 Other services (except public administration) 765 4.7% 17,770 4.4% 112,335 4.5% 91 Public administration 665 4.1% 36,155 9.0% 125,000 5.1%

Vancouver Island and Coast

33

The City of Campbell River, relative to Vancouver Island and Coast and British Columbia, has a high concentration of employment in the category agriculture, forestry, fishing and hunting (9.2 percent versus 3.4 percent versus 2.6 percent), mining; quarrying; and oil and gas extraction (2.4 percent versus 0.7 percent versus 1.0 percent), construction (9.3 percent versus 8.0 versus 8.1 percent), retail trade (13.4 percent versus 12.2 percent versus 11.5 percent) and accommodation and food services (9.1 percent versus 8.7 percent versus 8.4 percent).

3.3. Location Quotient Analysis In addition to the previous analysis of employment trends, this study also uses what is referred to as “location quotient analysis” to assess the economic base of the City of Campbell River. The location quotient analysis compares the local share of employment in an industry to the greater area’s share of employment in the same industry and identifies basic industries (i.e., industries that export from the region and bring in revenue from outside) and non-basic industries (i.e., industries that primarily serve locally and support basic industries) in an economy. This is expressed as LQ>one, LQ=one and LQ<one. An LQ value that is greater than one suggests a higher level of local employment in comparison to a greater area and provides evidence of basic employment for a given industry. An LQ value that is equal to one suggests similar levels of local employment in comparison to the greater area and signifies that the local employment is exactly sufficient to meet the local demand for a given good or service (i.e., the industry is non-basic in nature). Similarly, a LQ value of less than one suggests lower level of employment in an industry and suggests that all employment in the local industry is not meeting local demand and is non-basic in nature. This study compares the employment levels by industries for the City of Campbell River to Vancouver Island and Coast Economic Region in 2016. The analysis suggests that the goods-producing industries: agriculture, forestry, fishing, and hunting, mining, quarrying, oil/gas extraction, utilities and construction had a location quotient greater than one in 2016. Manufacturing, on the other hand, had an LQ less than one in 2016. This is indicative of the importance of agriculture, forestry, fishing, and hunting; mining, quarrying, oil/gas extraction, utilities and construction to the local economy in comparison to the Vancouver Island and Coast Economic Region as shown in Table 12. In the case of service-producing industries, the location quotient for wholesale trade, retail trade, management of companies and enterprises, accommodation and food services, and other services (except public administration) is higher than one. This LQ suggests that these industries employ a higher proportion of employment as compared to the same industries in Vancouver Island and Coast Economic Region, indicating that they are basic industries of the City of Campbell River. As stated, all of the industries with a location quotient greater than 1 suggest that they are basic industries of the City or an exporter of these services to the greater area.

34

Table 12: Location Quotient – Campbell River & Vancouver Island & Coast Economic Region (2016)

Source: Urbanics Consultants Ltd. and Statistics Canada

Goods-producing industries 11 Agriculture; forestry; fishing and hunting 2.73 21 Mining; quarrying; and oil and gas extraction 3.28 22 Utilities 2.02 23 Construction 1.17 31-33 Manufacturing 0.90Service-producing industries 41 Wholesale trade 1.10 44-45 Retail trade 1.10 48-49 Transportation and warehousing 1.11 51 Information and cultural industries 0.59 52 Finance and insurance 0.84 53 Real estate and rental and leasing 0.98 54 Professional; scientific and technical services 0.73 55 Management of companies and enterprises 1.44 56 Administrative and support; waste management and remediation services 0.81 61 Educational services 0.68 62 Health care and social assistance 0.99 71 Arts; entertainment and recreation 0.84 72 Accommodation and food services 1.05 81 Other services (except public administration) 1.07 91 Public administration 0.46

Location Quotient - Campbell River & Vancouver Island and Coast (2016)

35