Embed Size (px)

Citation preview

California | Illinois | Michigan | Texas | Washington, D.C.

www.dykema.com

Independent Contractors Independent Contractors Do’s and Don’tsDo’s and Don’ts

Independent Contractors Independent Contractors Do’s and Don’tsDo’s and Don’ts

James P. GreeneDykema

2723 South State StreetAnn Arbor, Michigan 48104

(734) [email protected]

James P. GreeneDykema

2723 South State StreetAnn Arbor, Michigan 48104

(734) [email protected]

2

Advantages to EmployersAdvantages to Employers

3

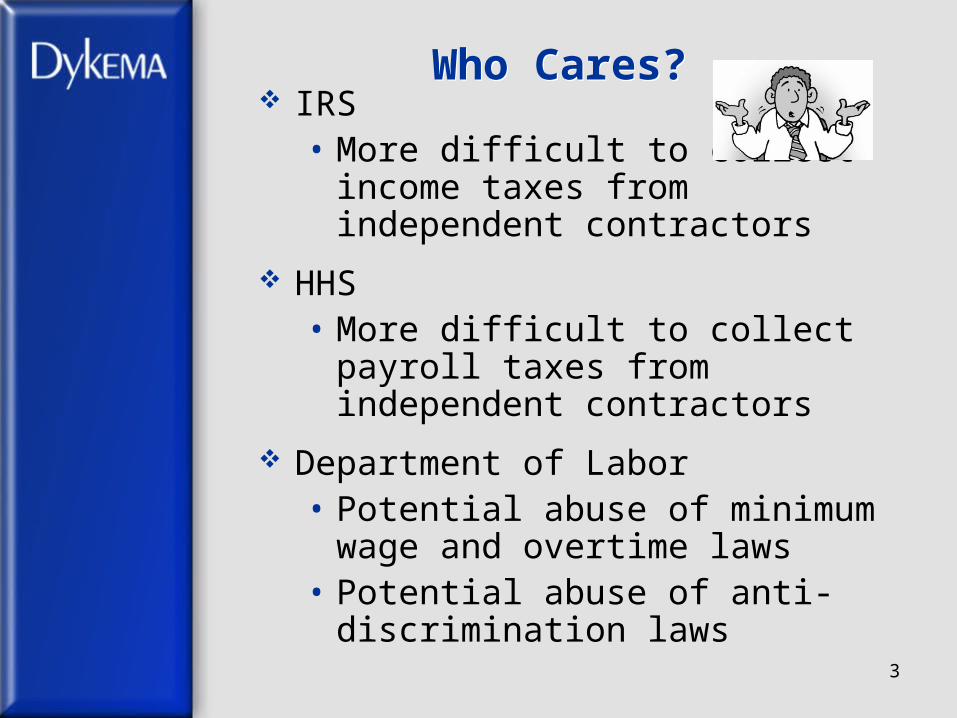

Who Cares?Who Cares?

IRS• More difficult to collect income taxes

from independent contractors

HHS• More difficult to collect payroll taxes

from independent contractors

Department of Labor• Potential abuse of minimum wage

and overtime laws• Potential abuse of anti-discrimination

laws

4

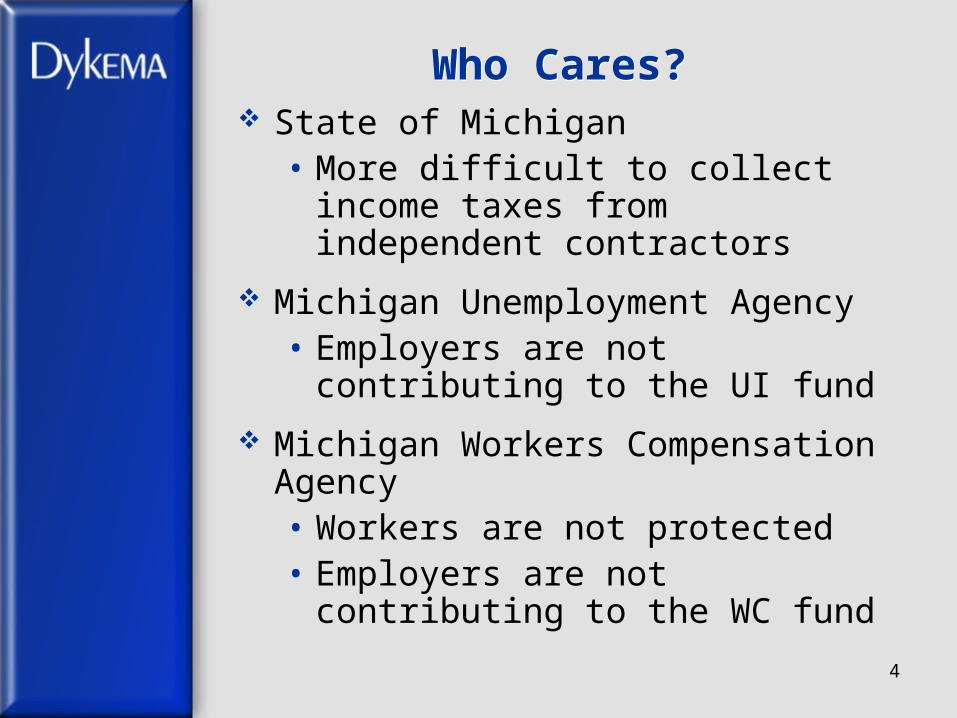

Who Cares?Who Cares?

State of Michigan• More difficult to collect income taxes

from independent contractors

Michigan Unemployment Agency• Employers are not contributing to the

UI fund

Michigan Workers Compensation Agency• Workers are not protected• Employers are not contributing to the

WC fund

5

How Big of a Problem?How Big of a Problem?

6

What’s Being Done?What’s Being Done?

Department of Labor• 2011 FY Budget included $25 million

to combat misclassification of employees as independent contractors, including:–$12M and 90 FTE to WHD for

targeted investigations–$11.25M and 2 FTE for grants to

states to focus on misclassification–$1.6M and 10 FTE to Solicitor of

Labor to pursue misclassification litigation

7

What’s Being Done?What’s Being Done?

Department of Labor• 2012 FY Budget request of $50

million to pursue misclassification• 2013 FY Budget of $14 million for

same

8

Michigan Task ForceMichigan Task Force

In February 2008, the State of Michigan created an “Interagency Task Force on Employee Misclassifications.”

The task force was established to discover classification violations by working cooperatively with local, state and federal law enforcement agencies, including the IRS.

9

Risks Associated with Employee Misclassification

Risks Associated with Employee Misclassification

10

Risks (continued)Risks (continued)

Insurance Premiums• Back payment of premiums (if insurer

permits)

Penalties• Government fines• Payment of employment taxes

– 100% of FICA contribution– Employer may not collect

employee amount from misclassified worker

11

Who is an independent contractor?

Who is an independent contractor?

Each governmental unit and/or agency uses its own analysis to determine if a worker is an “independent contractor”

No unit/agency has a precise definition – the totality of the circumstances must be analyzed.

12

Michigan Economic Reality TestMichigan Economic Reality Test

The Michigan Unemployment Agency, based upon court decisions, uses the “economic reality test” to determine if a worker is an employee or an independent contractor.

No one consideration used in the test answers the question; they must all be considered together.

13

Economic Reality TestEconomic Reality Test

Whether the employer will incur liability if the relationship terminates at will

Whether the work performed is an integral part of the employer’s business

Whether the employee depends upon the wages for living expenses

Whether the employee furnishes equipment and materials

Whether the employee holds himself out to the public as able to perform the same tasks

14

Economic Reality TestEconomic Reality Test

Whether the work involved is customarily performed by an independent contractor

The factors of control, payment of wages, maintenance of discipline, and the right to hire and fire employees

15

IRS TestIRS TestThe IRS looks at the degree of control the employer exerts over the worker and the degree of independence exhibited by the worker.

The IRS considers facts that provide evidence in the following three categories:

Behavioral Control

Financial Control

Type of Relationship

16

Behavioral Control Behavioral Control

Control over when and where the work will be done

Whether or not the employer provides instruction on how the work will be done

Whether the worker uses the employer’s or his/her own tools and equipment

Whether or not the employer provides training to the worker

How the worker is evaluated (details or end result)

17

Financial ControlFinancial Control

Extent of unreimbursed business expenses

Extent of worker’s investment in equipment and facilities

Extent to which the worker’s services are made available to the relevant market

Extent to which the worker can realize a profit or loss

Method of payment

18

Type of RelationshipType of Relationship

Whether or not the employer provides the worker with employee-type benefits

• Insurance• Pension plan• Vacation, holiday, or sick pay

Whether or not the worker is provided a copy of the employee handbook

Whether or not the worker is engaged with the expectation that the relationship will continue indefinitely

The extent to which the worker’s services are a key aspect of the employer’s regular business

19

US Supreme CourtUS Supreme Court

In resolving disputes under the Fair Labor Standards Act, the US Supreme Court has said that no single factor is determinative, but depends upon the whole activity. The factors the Court has considered significant include:

The extent to which the worker’s services are an integral part of the employer’s business

The permanency of the relationship

20

US Supreme Court cont.US Supreme Court cont.

The amount of the worker’s investment in facilities and equipment

The nature and degree of control by the principal

The worker’s opportunities for profit and loss

The level of skill require in performing the job and the amount of initiative, judgment, or foresight in open market competition with others required for the success of the claimed independent enterprise

Painter BobPainter Bob

A Straightforward ExampleA Straightforward Example

Painter Bob• Bob advertises in the local

newspaper to get jobs• He maintains his own brushes,

ladders, and drop cloths, and buys his own paint

• He is paid by the job• When the paint job is complete, Bob

no longer works for the customer/employer

• Bob is an independent contractor

Painter JohnPainter John

A Straightforward Example – Part 2A Straightforward Example – Part 2 Painter John

• John reports to work at the same company every day

• The company provides John with the paint, brushes, ladders and other materials to do the job

• The company sets John’s working hours

• John works for the company full time• John is an employee of the

company

Painter PaulPainter Paul

A Little MurkyA Little Murky Painter Paul

• Paul reports to work at the same company 3 or 4 days a week. He works only 3-4 hours each evening.

• Paul advertises in the local newspaper to get additional day jobs.

• The company provides Paul with the paint, brushes, ladders and other materials to do the job.

• The company pays Paul by the hour and Paul has some discretion on the days he works.

• Paul has worked for the company in this capacity for several years.

Treated as an EmployeeTreated as an Employee

Did you give the worker an employee handbook?

Did you give the worker some employee benefits? (paid sick days, access to EAP or reduced membership to gym?)

Did you evaluate the worker using the same forms as are used for employees?

How you treat a worker is part of the total picture in determining his/her classification as an employee or independent contractor.

Employment Agencies Solve the Problem,…Right?Employment Agencies Solve the Problem,…Right?

Employment agencies hire, fire and pay the workers.

Employment agencies are responsible for withholding income and payroll taxes, paying the employer’s portion of FICA, and possibly providing fringe benefits to the workers.

The contracting company pays the agency with a vendor check.

So what could go wrong?

“Joint Employers”“Joint Employers”

A contracting company may be considered a “joint employer” depending upon the amount of control it exercises over the worker during the term of the assignment.

A determination is made by looking at the entire relationship.

“Joint Employers”“Joint Employers”

Factors to consider in determining if there is a joint employment relationship include:

The nature and degree of control over the worker

The degree of supervision exercised over the work

The furnishing of work space and/or equipment

The power each has to determine the pay rates or method of payment

The right each has to hire, fire or modify working conditions

Liability of a Joint EmployerLiability of a Joint Employer

Anti-discrimination• May be liable for discriminatory

treatment or hostile work environment

FMLA• Leased employees who work for a

full workweek are counted toward the 50 minimum for FMLA coverage

• Agency responsible for notices• Contracting employer may be

responsible for accepting a leased worker returning from FMLA leave

Liability of a Joint EmployerLiability of a Joint Employer

FLSA• Both employers are liable for

minimum wage and overtime requirements

NLRA• Temporary employees from an

agency may be included in a bargaining unit if they share a “community of interests”

• Both employers may be held liable in an unfair labor practice

Liability of a Joint EmployerLiability of a Joint Employer

OSHA• Leasing employer will likely be liable

for work-related injuries

Best Practices When Leasing Employees

Best Practices When Leasing Employees

Seek an indemnity agreement in the contract with the staffing agency so that the agency retains liability for employment-related claims and agrees to indemnify the client for any losses they may incur attributable to the actions of the agency

Contract should include a provision making the agency responsible for payment of all employment taxes

Best Practices When Leasing Employees

Best Practices When Leasing Employees

Employers should verify that the employees are covered under the agency’s workers’ compensation policy.

Employers should accommodate the needs of a worker with a disability, unless it would be an undue hardship.

Employers should ensure that leased workers are not subjected to discriminatory treatment or harassment.

Employers should review their policies and benefit plans to ensure that leased employees are not eligible for company benefits.

IRS Voluntary Classification Settlement ProgramIRS Voluntary Classification Settlement Program

IRS Voluntary Classification Settlement ProgramIRS Voluntary Classification Settlement Program

Eligibility• Are currently treating the workers as

non-employees• Have satisfied Form 1099

requirements for the workers for the past 3 years

• Have no current dispute with the IRS or the DOL regarding the workers’ status

• Have not been previously audited by the IRS or if so, have complied with the results of the previous audit.

IRS Voluntary Classification Settlement ProgramIRS Voluntary Classification Settlement Program

Requirements• Employer agrees to prospectively

treat the workers as employees in the future

• Employer agrees to extend the period of limitations on assessment of employment taxes for 3 years beginning after the date of the agreement

IRS Voluntary Classification Settlement ProgramIRS Voluntary Classification Settlement Program

Benefits• Employer will pay 10% of

employment tax liability that may have been due on compensation paid to workers for the most recent tax year

• No interest or penalties on the liability

DODO

Review all relationships with independent contractors and their duties under the guidelines for all agencies (IRS, DOL, State of Michigan)

Review all contracts/agreements with leasing agencies

Review all contracts/employment agreements with individual independent contractors

DON’TDON’T

Treat independent contractors as employees

Automatically refuse to address ADA accommodation requests by independent contractors

42

Thank You