Embed Size (px)

Citation preview

BUY THIS REPORT

TRUSTED UNIQUE DETAILED

Written by MEEDs experts, with chapters from Colin Foreman,

Andrew Roscoe, Jennifer Aguinaldo, Indrajit Sen. Curated

and reviewed by Richard Thompson.

Includes unique expert analysis of how the market is changing and the impact of

these market changes.

Detailed assessment of the outlook, opportunities and

challenges in all of the major business areas.

"The quality of information provided by MEED Insight enabled us to quickly focus on critical areas as well as providing in-depth research into future opportunities."

300+ pages mega projects 10 key business sectors review on the Vision 2030

SAUDI ARABIA 2019Trends, opportunities and challenges

in the Middle East's biggest market

CLICK HERE

Anne BunchConsultancy company based in Dubai

Saudi Arabia 2019

Kuwait Projects 2016

3

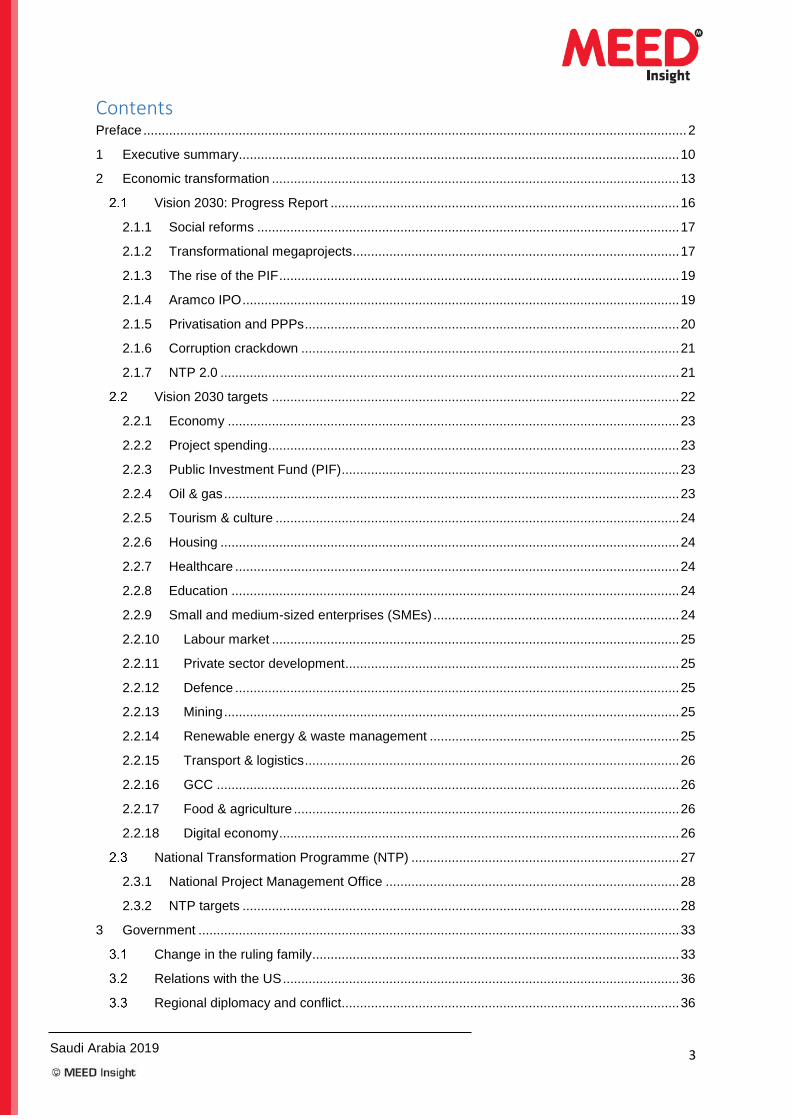

Contents Preface .................................................................................................................................................... 2

1 Executive summary ........................................................................................................................ 10

2 Economic transformation ............................................................................................................... 13

Vision 2030: Progress Report ............................................................................................... 16

2.1.1 Social reforms ................................................................................................................... 17

2.1.2 Transformational megaprojects ......................................................................................... 17

2.1.3 The rise of the PIF ............................................................................................................. 19

2.1.4 Aramco IPO ....................................................................................................................... 19

2.1.5 Privatisation and PPPs ...................................................................................................... 20

2.1.6 Corruption crackdown ....................................................................................................... 21

2.1.7 NTP 2.0 ............................................................................................................................. 21

Vision 2030 targets ............................................................................................................... 22

2.2.1 Economy ........................................................................................................................... 23

2.2.2 Project spending................................................................................................................ 23

2.2.3 Public Investment Fund (PIF) ............................................................................................ 23

2.2.4 Oil & gas ............................................................................................................................ 23

2.2.5 Tourism & culture .............................................................................................................. 24

2.2.6 Housing ............................................................................................................................. 24

2.2.7 Healthcare ......................................................................................................................... 24

2.2.8 Education .......................................................................................................................... 24

2.2.9 Small and medium-sized enterprises (SMEs) ................................................................... 24

2.2.10 Labour market ............................................................................................................... 25

2.2.11 Private sector development ........................................................................................... 25

2.2.12 Defence ......................................................................................................................... 25

2.2.13 Mining ............................................................................................................................ 25

2.2.14 Renewable energy & waste management .................................................................... 25

2.2.15 Transport & logistics ...................................................................................................... 26

2.2.16 GCC .............................................................................................................................. 26

2.2.17 Food & agriculture ......................................................................................................... 26

2.2.18 Digital economy ............................................................................................................. 26

National Transformation Programme (NTP) ......................................................................... 27

2.3.1 National Project Management Office ................................................................................ 28

2.3.2 NTP targets ....................................................................................................................... 28

3 Government ................................................................................................................................... 33

Change in the ruling family .................................................................................................... 33

Relations with the US ............................................................................................................ 36

Regional diplomacy and conflict............................................................................................ 36

Saudi Arabia 2019

Kuwait Projects 2016

4

3.3.1 Yemen ............................................................................................................................... 38

3.3.2 Arms sales ......................................................................................................................... 38

Diplomatic disputes ............................................................................................................... 38

Saudi Arabia and global oil markets ..................................................................................... 39

Economic and social development ....................................................................................... 40

Social reforms ....................................................................................................................... 41

4 Economy ........................................................................................................................................ 43

GDP ....................................................................................................................................... 43

4.1.1 GDP by sector ................................................................................................................... 44

Inflation .................................................................................................................................. 45

Oil production ........................................................................................................................ 46

Government finances ............................................................................................................ 47

4.4.1 Anti-corruption drive .......................................................................................................... 48

4.4.2 Government debt............................................................................................................... 49

Trade flows ............................................................................................................................ 51

Banking and monetary policy ................................................................................................ 52

4.6.1 Interest rates ..................................................................................................................... 53

Stock market ......................................................................................................................... 53

Foreign direct investment ...................................................................................................... 54

Labour market ....................................................................................................................... 55

The economy in 2018-20 ...................................................................................................... 57

4.10.1 The oil market ................................................................................................................ 58

4.10.2 Budget 2019 .................................................................................................................. 60

4.10.3 Medium-term financial strategy ..................................................................................... 62

MEED forecast to 2020 ......................................................................................................... 65

4.11.1 GDP ............................................................................................................................... 65

4.11.2 The budget .................................................................................................................... 66

4.11.3 Government debt........................................................................................................... 68

4.11.4 Exports, imports and the current account ..................................................................... 69

Saudi Aramco IPO ................................................................................................................ 70

The IMF view ......................................................................................................................... 71

Credit ratings agencies ......................................................................................................... 72

5 Projects market .............................................................................................................................. 73

Spending drivers ................................................................................................................... 76

Outlook .................................................................................................................................. 77

Leading contractors ............................................................................................................... 78

Leading clients ...................................................................................................................... 79

Megaprojects ......................................................................................................................... 80

Saudi Arabia 2019

Kuwait Projects 2016

5

6 Oil and Gas .................................................................................................................................... 84

Overview ............................................................................................................................... 84

Vision 2030 targets ............................................................................................................... 87

Market structure .................................................................................................................... 87

Saudi Aramco ........................................................................................................................ 88

6.4.1 Aramco IPO ....................................................................................................................... 91

6.4.2 Aramco’s Downstream Strategy ........................................................................................ 92

Upstream oil .......................................................................................................................... 93

6.5.1 Revised Proven Reserves ................................................................................................. 93

6.5.2 Oil Production .................................................................................................................... 94

6.5.3 Resource depletion ........................................................................................................... 95

6.5.4 Exploration ........................................................................................................................ 99

6.5.5 Export infrastructure .......................................................................................................... 99

Natural gas .......................................................................................................................... 100

6.6.1 Liquified Petroleum Gas (LPG) ....................................................................................... 103

6.6.2 Wasit gas development ................................................................................................... 103

6.6.3 Fadhili Gas Plant ............................................................................................................. 103

6.6.4 Unconventional gas ......................................................................................................... 104

6.6.5 Shaybah NGL .................................................................................................................. 105

6.6.6 Empty Quarter ................................................................................................................. 105

6.6.7 Midyan project ................................................................................................................. 106

6.6.8 Gas demand .................................................................................................................... 106

6.6.9 Fuel reforms .................................................................................................................... 106

Refining ............................................................................................................................... 107

6.7.1 Refinery projects ............................................................................................................. 110

Projects market ................................................................................................................... 112

6.8.1 Leading contractors ......................................................................................................... 115

7 Petrochemicals ............................................................................................................................ 117

Petrochemical Industry overview ........................................................................................ 117

Feedstock issues ................................................................................................................ 118

Refining petrochemicals integration initiative ...................................................................... 119

Key companies .................................................................................................................... 121

7.4.1 Sabic ............................................................................................................................... 121

7.4.2 Saudi Aramco .................................................................................................................. 124

7.4.3 Sipchem .......................................................................................................................... 125

7.4.4 Tasnee ............................................................................................................................ 125

7.4.5 Chevron Phillips .............................................................................................................. 126

Projects market ................................................................................................................... 126

Saudi Arabia 2019

Kuwait Projects 2016

6

8 Mining and natural resources ...................................................................................................... 128

Investment ........................................................................................................................... 132

Gold and base metals ......................................................................................................... 134

8.2.1 Base Metals ..................................................................................................................... 136

Phosphate ........................................................................................................................... 136

Aluminium and bauxite ........................................................................................................ 138

Industrial minerals ............................................................................................................... 139

Exploration .......................................................................................................................... 139

Vision 2030 targets ............................................................................................................. 140

Talent and experience ......................................................................................................... 141

9 Industry ........................................................................................................................................ 142

Diversification ...................................................................................................................... 143

9.1.1 Incentives ........................................................................................................................ 144

9.1.2 Industrial cities ................................................................................................................. 145

9.1.3 Challenges ...................................................................................................................... 148

9.1.4 Employment .................................................................................................................... 149

Automotive .......................................................................................................................... 150

Polysilicon ........................................................................................................................... 151

Cement ................................................................................................................................ 152

Steel .................................................................................................................................... 154

Aluminium ............................................................................................................................ 157

Fertilisers ............................................................................................................................. 158

Defence ............................................................................................................................... 159

9.8.1 Vision 2030 targets and impact ....................................................................................... 160

Outlook ................................................................................................................................ 162

10 Power ...................................................................................................................................... 165

Overview ............................................................................................................................. 165

Market Structure .................................................................................................................. 166

Supply and demand ............................................................................................................ 167

10.3.1 Installed Capacity ........................................................................................................ 167

10.3.2 Power Generation ....................................................................................................... 170

10.3.3 Power Consumption .................................................................................................... 171

10.3.4 Peak Load Demand .................................................................................................... 172

Power generation projects .................................................................................................. 175

Upcoming projects .............................................................................................................. 176

Conversion projects ............................................................................................................ 177

Steam plants ....................................................................................................................... 178

Decommissioning ................................................................................................................ 178

Saudi Arabia 2019

Kuwait Projects 2016

7

Private power market .......................................................................................................... 179

Developers ...................................................................................................................... 182

SEC privatisation ............................................................................................................. 183

SWCC privatisation ......................................................................................................... 185

Fuel sources .................................................................................................................... 185

Nuclear ............................................................................................................................ 186

Energy efficiency ............................................................................................................. 187

Transmission & distribution ............................................................................................. 189

11 Renewable energy .................................................................................................................. 194

Overview ............................................................................................................................. 194

NREP projects ..................................................................................................................... 198

Other projects ...................................................................................................................... 200

12 Desalination............................................................................................................................. 203

Market structure .................................................................................................................. 204

Supply/demand ................................................................................................................... 204

Saline Water Conversion Corporation ................................................................................ 206

Private developers .............................................................................................................. 208

Future private projects ........................................................................................................ 210

Decommissioning ................................................................................................................ 211

Future projects .................................................................................................................... 212

Privatisation ......................................................................................................................... 213

13 Wastewater ............................................................................................................................. 214

Management contracts ........................................................................................................ 215

13.1.1 Future private sector partnerships .............................................................................. 218

Past and future spending .................................................................................................... 219

13.2.1 PPP water projects ...................................................................................................... 221

13.2.2 Water masterplans ...................................................................................................... 221

Groundwater........................................................................................................................ 223

Treated sewage effluent ...................................................................................................... 223

Marafiq ................................................................................................................................ 226

14 Construction ............................................................................................................................ 228

Overview ............................................................................................................................. 228

Projects market ................................................................................................................... 230

14.2.1 Major projects under execution ................................................................................... 230

14.2.2 Projects on hold........................................................................................................... 230

14.2.3 Projects pipeline .......................................................................................................... 231

14.2.4 Leading clients ............................................................................................................ 232

Contractors and the government......................................................................................... 233

Saudi Arabia 2019

Kuwait Projects 2016

8

14.3.1 Leading contractors ..................................................................................................... 234

PPP projects........................................................................................................................ 235

Real estate .......................................................................................................................... 236

14.5.1 Major project pipeline .................................................................................................. 237

14.5.2 Housing ....................................................................................................................... 240

Healthcare ........................................................................................................................... 243

Education ............................................................................................................................ 244

Roads .................................................................................................................................. 245

15 Tourism ................................................................................................................................... 248

Overview ............................................................................................................................. 248

Vision 2030 and the tourism sector ..................................................................................... 254

Cultural tourism ................................................................................................................... 255

Hospitality ............................................................................................................................ 256

Leisure projects ................................................................................................................... 258

Retail projects...................................................................................................................... 260

16 Rail .......................................................................................................................................... 262

Railway masterplan ............................................................................................................. 263

Structure of the rail industry ................................................................................................ 264

Mainline rail infrastructure ................................................................................................... 266

16.3.1 North-South Railway ................................................................................................... 266

16.3.2 Haramain high-speed railway ...................................................................................... 269

16.3.3 Saudi Landbridge ........................................................................................................ 269

16.3.4 Other lines ................................................................................................................... 269

16.3.5 Mainline railways – PPP .............................................................................................. 270

Metro/light rail transit ........................................................................................................... 271

16.4.1 Urban rail – PPP.......................................................................................................... 271

16.4.2 Riyadh Metro ............................................................................................................... 272

16.4.3 Mecca Metro ................................................................................................................ 275

16.4.4 Medina Metro .............................................................................................................. 276

16.4.5 Jeddah Metro .............................................................................................................. 277

16.4.6 Dammam Metro ........................................................................................................... 280

Monorail ............................................................................................................................... 280

17 Aviation .................................................................................................................................... 282

Airport projects .................................................................................................................... 285

17.1.1 Planned and unawarded projects................................................................................ 289

Market liberalisation ............................................................................................................ 291

17.2.1 Privatisation of the aviation sector .............................................................................. 293

18 Ports ........................................................................................................................................ 296

Saudi Arabia 2019

Kuwait Projects 2016

9

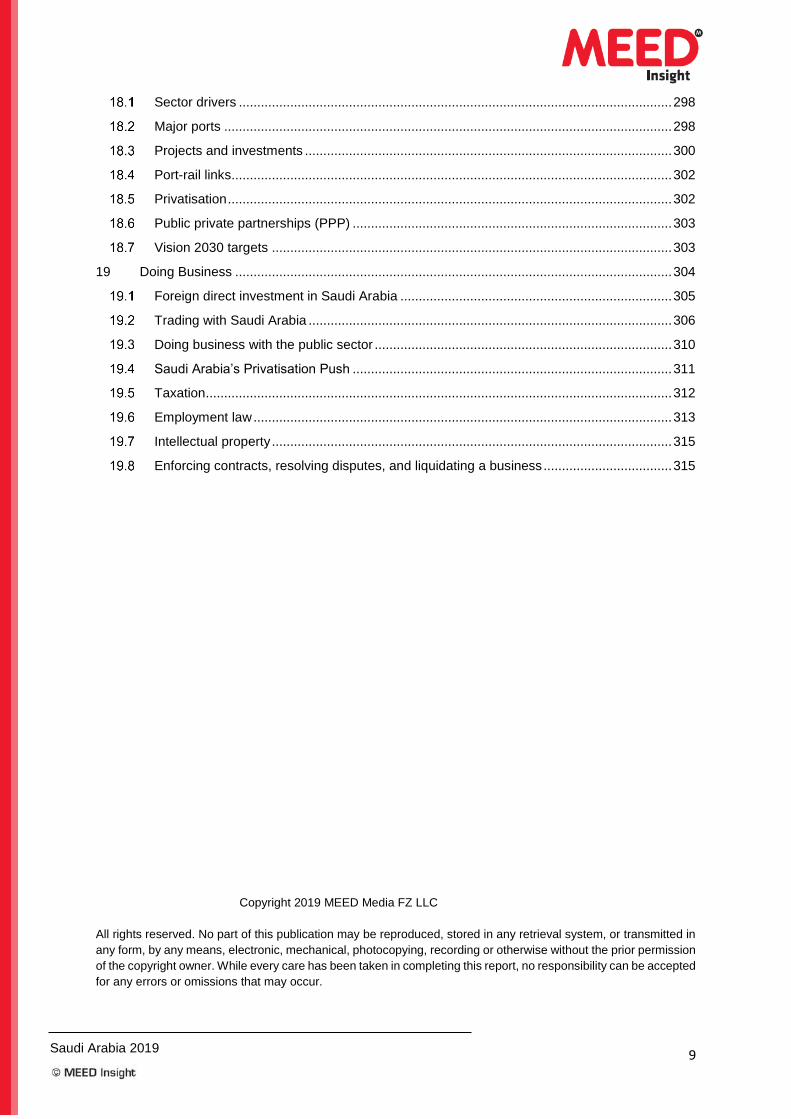

Sector drivers ...................................................................................................................... 298

Major ports .......................................................................................................................... 298

Projects and investments .................................................................................................... 300

Port-rail links........................................................................................................................ 302

Privatisation ......................................................................................................................... 302

Public private partnerships (PPP) ....................................................................................... 303

Vision 2030 targets ............................................................................................................. 303

19 Doing Business ....................................................................................................................... 304

Foreign direct investment in Saudi Arabia .......................................................................... 305

Trading with Saudi Arabia ................................................................................................... 306

Doing business with the public sector ................................................................................. 310

Saudi Arabia’s Privatisation Push ....................................................................................... 311

Taxation ............................................................................................................................... 312

Employment law .................................................................................................................. 313

Intellectual property ............................................................................................................. 315

Enforcing contracts, resolving disputes, and liquidating a business ................................... 315

Copyright 2019 MEED Media FZ LLC

All rights reserved. No part of this publication may be reproduced, stored in any retrieval system, or transmitted in

any form, by any means, electronic, mechanical, photocopying, recording or otherwise without the prior permission

of the copyright owner. While every care has been taken in completing this report, no responsibility can be accepted

for any errors or omissions that may occur.

BUY THIS REPORT

TRUSTED UNIQUE DETAILED

Written by MEEDs experts, with chapters from Colin Foreman,

Andrew Roscoe, Jennifer Aguinaldo, Indrajit Sen. Curated

and reviewed by Richard Thompson.

Includes unique expert analysis of how the market is changing and the impact of

these market changes.

Detailed assessment of the outlook, opportunities and

challenges in all of the major business areas.

"The quality of information provided by MEED Insight enabled us to quickly focus on critical areas as well as providing in-depth research into future opportunities."

300+ pages mega projects 10 key business sectors review on the Vision 2030

SAUDI ARABIA 2019Trends, opportunities and challenges

in the Middle East's biggest market

CLICK HERE

Anne BunchConsultancy company based in Dubai

Saudi Arabia 2019

Kuwait Projects 2016

45

The second biggest area of activity is the government services sector, which is essentially

funded by oil revenues and includes items such as public administration, defence and other

activities.

The third largest area of activity is financial and business services, followed by wholesale

and retail trade, restaurant and hotels – a sector which is being boosted by growing

demand for services for pilgrims and should also benefit from the ongoing development of

the general tourism industry – and then manufacturing industry, such as petrochemicals,

steel and aluminium.

Saudi GDP by sector, 2017 (% of total)

Source: Sama

Inflation

Saudi inflation, 2007−2018 (%)

Source: IMF

Oil and gas, 28.2

Govt services , 19.1

Finance, real estate & business

services, 13.1Trade, restaurants & hotels, 10.7

Manufacturing, 9.7

Transport & communications,

6.4

Construction, 6.0

Agriculture, 2.5

Community, social & personal

services, 2.3

Utilities, 1.6

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Saudi Arabia 2019

Kuwait Projects 2016

74

After two challenging years in which the value of contracts awarded in Saudi Arabia

plummeted to about half of the 2010–15 average, the kingdom’s projects industry received

a welcome boost in October 2017 from Crown Prince Mohammad bin Salman’s

announcement of a series of mega-projects aimed at transforming the Saudi economy.

These mega-projects included the $500bn Neom project. However, there are doubts about

how quickly such schemes will move forward.

Overall, between 2010 and 2018, Saudi Arabia awarded close to $366bn of contracts

across all sectors; $228bn of contracts are still under execution.

Total value of contract awards, 2010−18 ($m)

Source: MEED Projects

Contract awards by sector, 2010−18 ($m)

Source: MEED Projects

31,560

49,591

40,354

58,299

50,896

57,624

27,320 28,810

21,389

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2010 2011 2012 2013 2014 2015 2016 2017 2018

130,712

82,267

16,176

26,164

47,087

24,545 29,458

9,434

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Saudi Arabia 2019

Kuwait Projects 2016

83

Ministry of Housing. Saudi Arabia and South Korea have signed an agreement to build

100,000 houses in the Al-Fursan region over the next seven years.

Another major deal due to be signed this year is a $16bn contract for the construction of

the Mecca Metro by the Makkah Mass Rail Transit Company (MMRTC), which involves

four new metro lines – A, B, C and D – complementing the Al-Mashaaer Al-Mugaddassah

metro line.

Largest projects due for award in 2019

Owner - Project Budget

($m) Status Completion

PIF - Neom: Infrastructure and Utilities 100,000 Study 2025

MOH - Dahiyat Alfursan 20,000 Study 2025

MMRTC - Mecca Metro 16,000 Bid Evaluation 2030

Jeddah Metro Company - JPTP: Jeddah Metro 13,000 Main Contract PQ 2023

PIF - Red Sea Project 10,000 Main Contract PQ 2030

Makkah Region Development Authority - Al Faisaliah City

10,000 Study 2025

GACA - KAIA: Phase 2 10,000 Study 2026

REPDO - Renewable Energy Program: Round II 10,000 Main Contract PQ 2023

Jeddah Metro Company - Jeddah Metro: Orange & Blue Lines

8,000 Main Contract PQ 2023

MMRTC - Mecca Metro: Lines B and C 8,000 Bid Evaluation 2024

SAR - Saudi Landbridge 7,000 Main Contract PQ 2023

Maaden - Third Phosphate Fertiliser Manufacturing Facility

6,400 Study 2024

PIF - New Jeddah Downtown 5,000 Study 2029

Satorp - Mixed Feed Cracker & Derivatives complex

5,000 Study 2024

SRO - Yanbu Jeddah Jizan and Taif Khamis Mushayt Abha Rails

4,200 Study 2025

MMRTC - Mecca Metro: Line D 4,000 Study 2024

MMRTC - Mecca Metro: Line A 4,000 Study 2024

WEC - Jubail 3 IWPP 4,000 Main Contract PQ 2022

MMRTC - Mecca Metro: Phase 1 (Lines B, C): Part 1: Package 3 (SYS)

3,547 Bid Evaluation 2024

Jeddah Metro Company - Jeddah Metro: Red Line 3,500 Main Contract PQ 2023

SB Energy - Solar PV Project at Sudair 3,000 Bid Evaluation 2023

Ministry of Municipal and Rural Affairs - Riyadh Storm Water Drainage Project

2,900 Design 2022

Shomoul Holding - The Avenues Riyadh: Mixed Use Development

2,700 Design 2021

MMRTC - Mecca Metro: Phase 1 (Lines B, C): Part 1: Civil: Package 1

2,653 Bid Evaluation 2024

SCTA - Al Rayis Development 2,500 Design 2027

SEC - Shuqaiq Power Plant Expansion: Phase 1 2,500 Study 2022

SEC - Jeddah South Power Plant: Phase 2 Expansion

2,500 Study 2023

YALJ - Kaaki Development in Mecca 2,000 Design 2022

PQ: Pre-Qualification; Source: MEED Projects

BUY THIS REPORT

TRUSTED UNIQUE DETAILED

Written by MEEDs experts, with chapters from Colin Foreman,

Andrew Roscoe, Jennifer Aguinaldo, Indrajit Sen. Curated

and reviewed by Richard Thompson.

Includes unique expert analysis of how the market is changing and the impact of

these market changes.

Detailed assessment of the outlook, opportunities and

challenges in all of the major business areas.

"The quality of information provided by MEED Insight enabled us to quickly focus on critical areas as well as providing in-depth research into future opportunities."

300+ pages mega projects 10 key business sectors review on the Vision 2030

SAUDI ARABIA 2019Trends, opportunities and challenges

in the Middle East's biggest market

CLICK HERE

Anne BunchConsultancy company based in Dubai

Saudi Arabia 2019

Kuwait Projects 2016

93

parent Hyundai Heavy Industries (HHI). This adds to Aramco’s existing 64.3 per cent stake

in S-Oil Corp, South Korea’s third-largest refiner.

Aramco is expected to continue shopping for refining assets going forward. The company’s

downstream capacity covers only a third of its production – a much lower ratio than the oil

majors Aramco wants to compete with. Greater downstream integration would also provide

a key hedge against low oil prices in the future.

Upstream oil

Hydrocarbons resources in Saudi Arabia are limited to a relatively small geographical

region and a number of large oil fields. Production primarily comes from 12 reservoirs in

the north-eastern corner of the kingdom, along with the Shaybah field in the south.

The kingdom has three of the world’s six giant fields in Khurais, Safaniya and Ghawar,

which each have the capacity to produce over 1 million b/d. Ghawar is the world’s largest

oil field, and is capable of producing about 5 million b/d. Safaniya and Khurais each

possess a production capacity of 1.2 million b/d.

Other large fields in the kingdom include Shaybah, Zuluf and Abu Safah, which produce

750,000-850,000 b/d. The Marjan and Qatif are also major fields, with production

capacities of 450,000-500,000 b/d each. Saudi Arabia’s allocation from the Divided Zone

is about 350,000 b/d. Other smaller fields include Haradh and Berri, each with capacities

of over 300,000 b/d.

Saudi oil and gas fields

Source: Arab Oil & Gas Directory

6.5.1 Revised Proven Reserves

In January 2019, Aramco revealed Saudi Arabia’s hydrocarbons reserves after a third-

party audit – a process carried out as part of its plans to prepare for a stock market listing.

Saudi Arabia 2019

Kuwait Projects 2016

137

Maaden Phosphate Company

MPC’s main source of phosphate rock is the Al-Jalamid mine in the north, near the border

with Iraq. The site includes a beneficiation plant and supporting infrastructure. The mine

produces about 11.6 million tonnes a year (t/y) of ore, which is processed into about 5

million t/y of dry concentrate.

The phosphate concentrates at Al-Jalamid, which has a measured resource of 534 million

tonnes, is transported by rail to Ras Al-Khair on the Gulf coast for processing into fertiliser.

Ras Al-Khair, 90km north of Jubail, hosts MPC’s $5bn integrated chemicals and fertiliser

production plant, which manufactures saleable products from Al-Jalamid concentrate.

The fertiliser complex contains a phosphoric acid plant, sulphuric acid plant, ammonia

plant, di-ammonium phosphate (DAP) granulation plant, a co-generation, and

desalinisation plant and associated facilities.

Railways supporting Ras Al-Khair minerals city

Source: Maaden

The DAP granulation plant started production in February 2012 and has a capacity of 3

million t/y. The offtake from the plant is sold on the international market, with 400,000 t/y

of surplus ammonia being sold domestically or internationally.

The complex also has the capability to produce mono-ammonium phosphate (MAP) if

market requirements demand it. A new ammonia plant began production at Ras Al-Khair

in January 2017.

The process for establishing a third sulphuric acid plant (DAP3) at the site is underway. In

November 2018, Maaden signed the financing agreement of $266m with Industrial

Development fund for the development of the project. The main contract tender issue for

the project is expected in the third quarter of 2019.

Saudi Arabia 2019

Kuwait Projects 2016

171

Package (82 per cent completed); and PP13 Combined Cycle Power Plant: Early &

General Civil Works Package (85 per cent completed).

The £925m SEC PP14 Combined Cycle Power Plant covers three projects: PP14

Combined Cycle Power Plant: Electro-mechanical Installation Package (95 per cent

completed); PP14 Combined Cycle Power Plant: Industrial Buildings Package (96 per cent

completed); and PP14 Combined Cycle Power Plant: Early & General Civil Works Package

(completed).

Major power plants under construction

Project Owner Main Contractor Estimated contract

value ($m)

Scheduled commissioning

Jizan Refinery IGCC Power Plant: Package 4: CCPP

Saudi Aramco SEPCO 2,500 2020

Yanbu Power Plant: Phase 3 SWCC/Marafiq JV SEPCO III Electric Power Construction Corp

1,370 2020

Jizan Refinery IGCC Power Plant: Package 1: Gasification Unit

Saudi Aramco Saipem 1,000 2019

Jizan Refinery IGCC Power Plant: Package 2: Sulphur Recovery Unit

Saudi Aramco Saipem 1,000 2019

Waad Al Shamal Integrated Solar Combined Cycle (ISCC) Power Plant

SEC General Electric/Abener JV

980 2019

Fadhili IPP Saudi Aramco/SEC

Doosan Heavy Industries & Construction Co.

896 2019

PP13 Combined Cycle Power Plant: Electro-mechanical Installation Package

SEC GAMA 320 2019

PP14 Combined Cycle Power Plant: Electro-mechanical Installation Package

SEC SEPCO III Electric Power Construction Corp

293 2019

PP14 Combined Cycle Power Plant: Industrial Buildings Package

SEC Alkifah Contracting 160 2019

Upgrade Sulfur Handling and Export Facilities at Berri Gas Plant

Saudi Aramco M R Al Khathlan for Contracting

130 2019

PP14 Combined Cycle Power Plant: Early & General Civil Works Package

SEC Archirodon 120 2019

PP13 Combined Cycle Power Plant: Early & General Civil Works Package

SEC Assad Said Contracting

118 2019

PP13 Combined Cycle Power Plant: Industrial Buildings Package

SEC Alfanar Bena Contracting

61 2019

Source: MEED Projects

10.3.3 Power Consumption

Power consumption in the kingdom has increased due to rising economic activity, as well

as buoyant residential consumption.

The residential sector was the largest consumer of electricity in the kingdom in 2017,

accounting for 48 per cent of total energy consumption that year. The industrial sector was

the second largest user, accounting for 18 per cent, followed by commercial users with 16

per cent and government with 13 per cent.

BUY THIS REPORT

TRUSTED UNIQUE DETAILED

Written by MEEDs experts, with chapters from Colin Foreman,

Andrew Roscoe, Jennifer Aguinaldo, Indrajit Sen. Curated

and reviewed by Richard Thompson.

Includes unique expert analysis of how the market is changing and the impact of

these market changes.

Detailed assessment of the outlook, opportunities and

challenges in all of the major business areas.

"The quality of information provided by MEED Insight enabled us to quickly focus on critical areas as well as providing in-depth research into future opportunities."

300+ pages mega projects 10 key business sectors review on the Vision 2030

SAUDI ARABIA 2019Trends, opportunities and challenges

in the Middle East's biggest market

CLICK HERE

Anne BunchConsultancy company based in Dubai

Saudi Arabia 2019

Kuwait Projects 2016

189

Transmission & distribution

The kingdom has comfortably been the region’s largest spender on transmission and

distribution (T&D) infrastructure since 2008, with about $28.9bn-worth of contracts

awarded until the end of December 2018. The largest of these was a $550m contract

awarded in 2008 to Middle East Engineering & Development Company for the construction

of the Qassim-Medina Transmission Line project.

Transmission & Distribution contract awards, 2011−18 ($m)

Source: MEED Projects

Investment in the transmission sector increased from 2011 to 2014 when it peaked at a

total value of nearly $6bn. Investment in the transmission sector is divided between

investment in cables and overhead lines, as well as substations and control centres.

Investment in the latter accounted for an average of 66 per cent of total investment

between 2011 and 2014.

Post-2014, there was a declining trend in investment in the transmission sector. Between

2017 and 2018, there was a marginal increase in investment, particularly in cables and

overhead lines.

Selected T&D contract awards, 2018–2019*

Project name Contractor Value ($m)

230/115/69 kV Abqaiq Central Substation Al Babtain Contracting 80

380/132/13.8 kV Al-Remal Substation (9046) Al Babtain Contracting 64 380kV OHTL from Arar BSP and Waad Shamaal BSP National Contracting Company 64 380KV OHTL Fadhili Gas Plant S/S to Wadi Al Summan 380/115/33kv BSP

Arabia Electrical Transmission Line Construction Company 62

380/230 kV Haradh & Hawaiyah OHTL Middle East Engineering & Development Co 60

Construction of EIC S/S 1 & 2 and Transmission Line Larsen & Toubro 60 380 kV UG for Al Rawabe(9047) BSP to Riyadh Metro (9054) BSP & 9017

Saudi Services for Electro Mechanic Works 60

2,7653,114

3,324

5,980

3,740

1,855

910 997

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2011 2012 2013 2014 2015 2016 2017 2018

Saudi Arabia 2019

Kuwait Projects 2016

205

Historically, the kingdom opted for desalination rather than alternatives such as large water

transfer projects or further over-exploitation of deep groundwater. However, much of the

existing desalination capacity was built before 1990 and needs to be replaced over the

coming decade.

Existing desalination plants

Source: SWCC

In 2000-08, very little new capacity was commissioned as a result of budgetary problems

for the government and SWCC; this was exacerbated by the fact that several contractors

faced serious payment issues for projects undertaken in the late 1990s.

However, rising oil prices and the launch of a utility privatisation programme resulted in an

increase in investment. In 2010, Saudi Arabia regained its position as the leading

desalination producer after two of the world’s largest plants – the Shuaibah IWPP on the

Red Sea and the Jubail IWPP on the Gulf coast – were commissioned. The plants boosted

Water supply by source (million cm/d), 2017

Sources: SWCC

6.5

3.3

0.2

0

1

2

3

4

5

6

7

Desalination water Ground water Surface water

Saudi Arabia 2019

Kuwait Projects 2016

225

Demand for TSE in Riyadh, Jeddah, Medina, Mecca and Greater Dammam, 2012−30

(thousand cm/d)

Source: NWC

To address this area, NWC is planning to spend an average of $600m a year on TSE

projects until 2028, including $1.5bn on projects in three major cities over the next four

years. Among its plans, the company will invest $800m in Riyadh, $530m in Jeddah and

$160m in Mecca.

All NWC’s new treatment projects will employ tertiary technology as a minimum. This is a

prerequisite, given that NWC is aiming for a significant increase in TSE reuse.

NWC has signed more than 12 agreements and memorandums of understanding (MoUs)

with companies for bulk TSE supply. Under the 20–25-year contracts, the private sector is

responsible for distributing the TSE from the STPs.

Forecast of TSE usage in the kingdom’s six major cities, 2011−30 (cm/d)

Source: NWC

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2012 2013 2014 2015 2016 2020 2024 2028 2030

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

Riyadh Jeddah Makkah Madinah Dammam & khober.

Saudi Arabia 2019

Kuwait Projects 2016

249

Saudi Arabia tourism contract awards, 2010−18

Source: MEED Projects

The biggest project currently on hold is the construction of four-star hotels in Group 4A of

Dar Al Hijrah’s Pilgrim City project. Dar Al Hijrah, a body owned by the Public Investment

Fund, is planning to develop an integrated mixed-use project called Pilgrim City comprising

100 buildings to accommodate over 120,000 pilgrims and 31,000 employees.

Major tourism projects on hold in Saudi Arabia

Project Value ($m)

Client

Pilgrim City: Four Star Hotels: Group 4 A 1,000 Dar Al Hijrah Company

Ishbiliyah City Centre 800 Majid Al Futtaim

Salboukh Mall in Riyadh 600 Arabian Centres

Grand Mosque Expansion: Utilities Bldg 540 General Presidency for Grand Mosque and Prophet Mosque Affairs

Botanical Gardens In Riyadh: Phase 3 500 King Abdullah International Gardens

Riyadh Land: Kingdom Oasis: Four Seasons

500 Kingdom Holdings

Mecca Museum 500 Saudi Commission for Tourism & National Heritage

Four Seasons Hotel in Jeddah 480 Midad Real Estate Investment & Development Co

Sharma Complex: Hotels & Accomodation 360 PIF

Riyadh Walk 320 Raj Real Estate

Jeddah Gate: Radisson Blu Hotel & Residence

300 Al Tawfeeq for Development & Investment

Sofitel Luxury 5 Star Hotel In Riyadh 300 King Abdullah bin Abdulaziz Foundation for Housing Dev

Millennium Jeddah (Corniche Jeddah) 250 Al Sharif Mansour Bin Saleh Abu Rayash Investment & Development Co

Source: MEED Projects

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2010 2011 2012 2013 2014 2015 2016 2017 2018

Cultural Hospitality Leisure Retail

BUY THIS REPORT

TRUSTED UNIQUE DETAILED

Written by MEEDs experts, with chapters from Colin Foreman,

Andrew Roscoe, Jennifer Aguinaldo, Indrajit Sen. Curated

and reviewed by Richard Thompson.

Includes unique expert analysis of how the market is changing and the impact of

these market changes.

Detailed assessment of the outlook, opportunities and

challenges in all of the major business areas.

"The quality of information provided by MEED Insight enabled us to quickly focus on critical areas as well as providing in-depth research into future opportunities."

300+ pages mega projects 10 key business sectors review on the Vision 2030

SAUDI ARABIA 2019Trends, opportunities and challenges

in the Middle East's biggest market

CLICK HERE

Anne BunchConsultancy company based in Dubai

Saudi Arabia 2019

Kuwait Projects 2016

275

16.4.3 Mecca Metro

Mecca has a light rail system in operation, but it is only used during peak pilgrimage times,

which is about seven days a year, to transport worshippers between various holy sites.

The pilgrim metro line, also known as the Al Mashaaer al Mugadassah Metro, links the

holy sites of Mecca, Mina, Arafat and Muzdalifah. It spans 18km, and has the capacity to

transport 72,000 passengers an hour.

The metro was built by Chinese contractors under a $1.77bn contract between the

Municipal & Rural Affairs Ministry and China Railway Construction Corporation (CRCC)

signed in February 2009. The contract covered the construction of the scheme and a three-

year O&M concession.

After a limited capacity test run during the 2010 Hajj, the metro was used at full capacity

from 2011 to 2013. CRCC operated the trains from 2011 to 2013, incurring net losses

estimated at $607m prior to transferring the project to the client. In May 2015, Malaysia’s

Prasarana Berhad won a SR807m three-year O&M contract for the service.

A further multi-phased light rail project has also been proposed for the city. The proposed

Mecca mass rail transit project (MMRT) will include the construction of four new metro

lines, A, B, C and D, complementing the Al Mashaaer Al Mugaddassah line. The new lines

will have a total length of 180km and will link about 88 stations.

The project aims to address the city’s traffic congestion issues, caused by a consistently

growing population and the rising number of pilgrims, whose number is expected to exceed

25 million by 2030.

Mecca Metro

Source: Development Commission of Mecca and Mashaer

Saudi Arabia 2019

Kuwait Projects 2016

297

Due to its location on the Red Sea coast and its relative proximity to the Suez Canal, KAP

is being touted as Saudi Arabia’s response to Jebel Ali port in Dubai, catering not only to

the domestic market but to transhipment cargo as well.

Saudi ports

Sources: Saudi Ports Authority; Ports Development Company; MEED

Annual cargo throughput at Saudi ports (million tonnes), 2013−17

Source: Saudi Ports Authority (SPA)

0

50

100

150

200

250

300

2013 2014 2015 2016 2017

Import Export

Saudi Arabia 2019

Kuwait Projects 2016

307

Petroleum products form a large majority of exports (78.5 per cent in 2018), followed by

petrochemicals products such as propylene and ethylene. Automobiles represent the

largest share of imports, followed by telecoms devices and medicine.

The kingdom exports mainly to the UAE, China, India, Singapore and Kuwait. It imports

mainly from China, the US, Germany, Japan, South Korea and the UAE.

Riyadh usually enjoys a trade surplus, although its scale varies with the fluctuations in

global oil prices. Exports grew rapidly in 2018, aided by rising oil prices, to reach SR1.1

trillion ($294bn). Its imports in 2018 were SR507bn, leaving a surplus of SR597bn, the

highest since 2015.

Saudi imports and exports (SRm)

Source: GSAT

Those wishing to sell products and services to Saudi Arabia are not required to establish

a direct or permanent presence in the kingdom. Instead, they can trade on open account

and deal with Saudi customers by phone and email without even sending an employee

into the country; this is often adequate for small companies and those that do not attach

great significance to the local market. For others, however, the option of establishing a

direct or indirect presence has to be seriously considered to take advantage of the

opportunities the market offers, and to conform to local law.

The simplest way to establish a local presence is by appointing a Saudi company as a

local agent or representative. There is no standard approach to this, although there is a

set of commercial agency regulations that define the parameters of any arrangement.

The first condition is that the Saudi agent or representative is properly incorporated under

the kingdom’s regulations for companies. This entails a Saudi national or corporation

registering with the Commerce & Industry Ministry and other relevant bodies and stating

which activities it wishes to pursue. Foreign firms working with individuals or entities that

are not properly incorporated and registered will quickly discover that few advantages will

be secured by taking this route.

Foreign firms appointing a Saudi company as an agent or representative are free to define

the relationship by contract within the terms of the commercial agencies’ regulations. This

can be registered in a foreign jurisdiction, although it will make the enforcement of

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2013 2014 2015 2016 2017

Imports Exports

BUY THIS REPORT

TRUSTED UNIQUE DETAILED

Written by MEEDs experts, with chapters from Colin Foreman,

Andrew Roscoe, Jennifer Aguinaldo, Indrajit Sen. Curated

and reviewed by Richard Thompson.

Includes unique expert analysis of how the market is changing and the impact of

these market changes.

Detailed assessment of the outlook, opportunities and

challenges in all of the major business areas.

"The quality of information provided by MEED Insight enabled us to quickly focus on critical areas as well as providing in-depth research into future opportunities."

300+ pages mega projects 10 key business sectors review on the Vision 2030

SAUDI ARABIA 2019Trends, opportunities and challenges

in the Middle East's biggest market

CLICK HERE

Anne BunchConsultancy company based in Dubai