Embed Size (px)

Citation preview

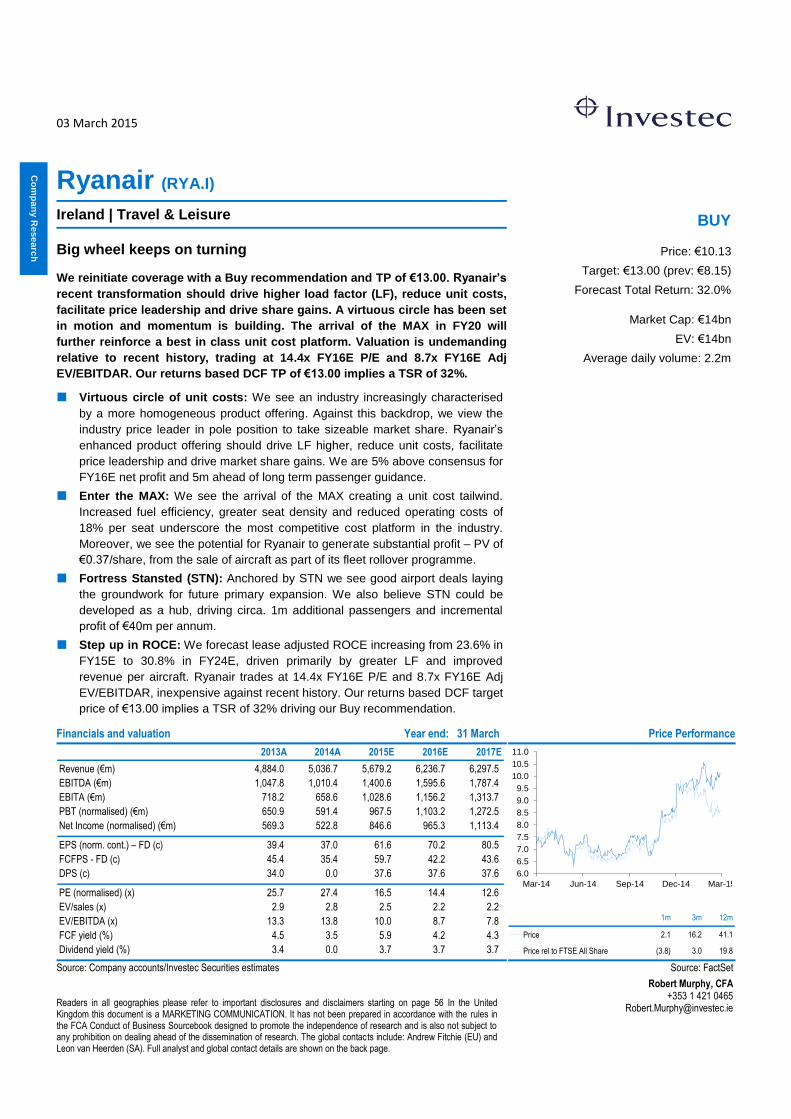

03 March 2015

Readers in all geographies please refer to important disclosures and disclaimers starting on page 56 In the United Kingdom this document is a MARKETING COMMUNICATION. It has not been prepared in accordance with the rules in the FCA Conduct of Business Sourcebook designed to promote the independence of research and is also not subject to any prohibition on dealing ahead of the dissemination of research. The global contacts include: Andrew Fitchie (EU) and Leon van Heerden (SA). Full analyst and global contact details are shown on the back page.

Robert Murphy, CFA +353 1 421 0465

Co

mp

an

y R

ese

arc

h

Ryanair (RYA.I)

Ryanair (Buy - TP: €13.00)

Ireland | Travel & Leisure

Buy

Big wheel keeps on turning

€10.1 €13.00

We reinitiate coverage with a Buy recommendation and TP of €13.00. Ryanair’s

recent transformation should drive higher load factor (LF), reduce unit costs,

facilitate price leadership and drive share gains. A virtuous circle has been set

in motion and momentum is building. The arrival of the MAX in FY20 will

further reinforce a best in class unit cost platform. Valuation is undemanding

relative to recent history, trading at 14.4x FY16E P/E and 8.7x FY16E Adj

EV/EBITDAR. Our returns based DCF TP of €13.00 implies a TSR of 32%.

Robert Murphy +353 1 421 0465

Virtuous circle of unit costs: We see an industry increasingly characterised

by a more homogeneous product offering. Against this backdrop, we view the

industry price leader in pole position to take sizeable market share. Ryanair’s

enhanced product offering should drive LF higher, reduce unit costs, facilitate

price leadership and drive market share gains. We are 5% above consensus for

FY16E net profit and 5m ahead of long term passenger guidance.

Enter the MAX: We see the arrival of the MAX creating a unit cost tailwind.

Increased fuel efficiency, greater seat density and reduced operating costs of

18% per seat underscore the most competitive cost platform in the industry.

Moreover, we see the potential for Ryanair to generate substantial profit – PV of

€0.37/share, from the sale of aircraft as part of its fleet rollover programme.

Fortress Stansted (STN): Anchored by STN we see good airport deals laying

the groundwork for future primary expansion. We also believe STN could be

developed as a hub, driving circa. 1m additional passengers and incremental

profit of €40m per annum.

Step up in ROCE: We forecast lease adjusted ROCE increasing from 23.6% in

FY15E to 30.8% in FY24E, driven primarily by greater LF and improved

revenue per aircraft. Ryanair trades at 14.4x FY16E P/E and 8.7x FY16E Adj

EV/EBITDAR, inexpensive against recent history. Our returns based DCF target

price of €13.00 implies a TSR of 32% driving our Buy recommendation.

Financials and valuation Year end: 31 March Price Performance

Source: Company accounts/Investec Securities estimates Source: FactSet

BUY

Price: €10.13

Target: €13.00 (prev: €8.15)

Forecast Total Return: 32.0%

Market Cap: €14bn

EV: €14bn

Average daily volume: 2.2m

2013A 2014A 2015E 2016E 2017E

Revenue (€m) 4,884.0 5,036.7 5,679.2 6,236.7 6,297.5

EBITDA (€m) 1,047.8 1,010.4 1,400.6 1,595.6 1,787.4

EBITA (€m) 718.2 658.6 1,028.6 1,156.2 1,313.7

PBT (normalised) (€m) 650.9 591.4 967.5 1,103.2 1,272.5

Net Income (normalised) (€m) 569.3 522.8 846.6 965.3 1,113.4

EPS (norm. cont.) – FD (c) 39.4 37.0 61.6 70.2 80.5

FCFPS - FD (c) 45.4 35.4 59.7 42.2 43.6

DPS (c) 34.0 0.0 37.6 37.6 37.6

PE (normalised) (x) 25.7 27.4 16.5 14.4 12.6

EV/sales (x) 2.9 2.8 2.5 2.2 2.2

EV/EBITDA (x) 13.3 13.8 10.0 8.7 7.8

FCF yield (%) 4.5 3.5 5.9 4.2 4.3

Dividend yield (%) 3.4 0.0 3.7 3.7 3.7

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

1m 3m 12m

____________________________Price 2.1 16.2 41.1

____________________________Price rel to FTSE All Share (3.8) 3.0 19.8

Page 2 | 03 March 2015| Ryanair

Ryanair at a glance Figure 1: Sales by region FY14 Figure 2: Network seat capacity by country, February 2015

Source: Company reports Source: Innovata

Figure 3: 12 month LF step change narrows the gap vs peers Figure 4: EBIT per passenger to eclipse pre-crisis levels, €

Source: Company reports Source: Company reports, Investec Securities Estimates

Figure 5: Step up in ROCE Figure 6: Higher quality revenue generation

Source: Investec Securities estimates Source: Investec Securities estimates

Ireland, 11%

United Kingdom,

25%

Other European countries,

65%

Italy22.9%

UK19.5%

Spain14.8%

Ireland7.8%

Poland4.8%

France4.7%

Germany4.6%

Belgium4.3%

Portugal3.4%

Greece2.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0%

1%

2%

3%

4%

5%

6%

7%

8% RYA EZJ EZJ vs. RYA (RHS)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2004

A

2005

A

2006

A

2007

A

2008

A

2009

A

2010

A

2011

A

2012

A

2013

A

2014

A

2015

E

2016

E

2017

E

2018

E

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

0%

5%

10%

15%

20%

25%

30%

35% Lease adj ROCE Historical Average

€0

€2

€4

€6

€8

€10

€12

€14

€16

€18

€20

-10%

-5%

0%

5%

10%

15%

20%

25% NOPAT / % of sales (LHS) Sales / Aircraft €m (RHS)

Page 3 | 03 March 2015| Ryanair

Ryanair investment thesis

Move to the centre plays to RYA’s strengths

The fundamentals underlying the intra-European commercial passenger market are

undergoing significant structural change. The low cost carrier (LCC) platform is

evolving with both an improved product offering and service level perception. In

parallel, competitive pressure has resulted in product unbundling by legacy carriers.

We see the end result as an increasingly homogenised marketplace. With less

product differentiation, we believe the price leader stands to take significant share.

The opportunity space is large with too many operators in Europe. Step forward

Ryanair. Armed with a significant cost of production advantage, we see the carrier

as positioned to benefit substantially from the industry shift.

Figure 7: An increasingly homogenous marketplace

Source: Investec Securities estimates

New strategy and primary airports sets virtuous circle in motion

Ryanair’s enhanced product offering should drive LF higher, reduce unit costs,

facilitate price leadership and drive market share gains. A virtuous circle has been

set in motion and momentum is gaining.

Figure 8: Higher LF spin the wheel of unit costs

Source: Investec Securities estimates

At the heart of Ryanair’s transition is a move into the last bastion of European

legacy carriers - the primary airport. We estimate that the carrier already operates

BA SH

Ryanair

Finnair SH

AF/KLM SH

Easyjet

LH SH

Air Berlin

SASNorwegian

Price point

Product offering /service level

A move to the centre

A more homogeneous product offering

lends itself to the price leader

Primary airport growth to drive both

volume and LF driving lower unit costs

- Primary airports to provide a

3.2% yield uplift

- Yield upside to be reinvested in

the market in pursuit of volume

- A virtuous circle of unit costs

has begun

Page 4 | 03 March 2015| Ryanair

from half of Europe’s primary airports representing 60% of Ryanair’s current seat

capacity, a figure we see reaching 80% by FY20E. Assuming primary airports merit

an average fare uplift of €10, group average revenue per passenger could be

boosted by 3.2% - upside that we believe Ryanair will reinvest in the market for

share gain and higher LF.

Max will reinforce Ryanair’s competitive position

We estimate Ryanair’s ex-fuel unit costs per passenger to be 28% below that of its

closest rivals. From this position, we see the arrival of the MAX in FY20 providing

opportunities for Ryanair to widen the gap vs. competition. Costs stand to benefit

from an increase in seat density of 4.2%, an 18% improvement in fuel burn per seat

and importantly a potential 1.1% delta over NEO customers in terms of fuel

efficiency. Moreover, we forecast that a 6% delta in depreciation costs vs. peers will

widen the ownership cost gap. We see the potential for Ryanair to generate €519m

in profit from the sale of assets as part of its upcoming fleet rollover programme,

with a PV per share of €0.37. To cap it all off, the MAX offers incremental annual

revenue with an estimated PV/share of €0.09.

Building out fortress Stansted

Ryanair’s airport strategy, centred on Stansted, should allow the carrier to enhance

its competitive position while maintaining cost discipline. Airport charges are backed

by good deals at airfields, with an estimated 25% of network capacity locked in at

declining rates. We view existing deals driving an estimated cumulative network

wide 2% per passenger saving through FY24E, laying the groundwork for future

primary airport expansion. Industry consolidation and opportunistic deals should

further underscore unit cost performance. Furthermore, Ryanair may look to turn

Stansted into a hub, which would connect network traffic flows, driving higher

volume and LF. We think such a move could result in an initial 785k additional

passenger, 0.7pts of LF and €40m EBIT per annum.

LF to the fore

We believe that the changes at Ryanair will allow the company to drive sustainably

higher LF, while also providing greater revenue per seat potential. Traffic data

indicates that the strategy is already working with rolling 12 month LF +3pts to 86%

and Q3:15 +6.4pts to 88.4%. While consensus is bullish, we see further upside to

Ryanair’s traffic and subsequent LF performance.

Table 1: Summary Ryanair forecasts

Operational statistics 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E

Investec passenger numbers (m) 90.3 100.6 107.0 115.2 122.4 131.3 139.8 148.2 156.4 165.0

Guided passenger numbers (m) 90.0 100.0 106.0 114.0 120.0 128.0 136.0 143.0 150.0 160.0

Delta 0.3% 0.6% 0.9% 1.1% 2.0% 2.6% 2.8% 3.7% 4.3% 3.1%

Investec capacity growth 3.9% 11.3% 6.0% 7.0% 6.0% 7.0% 6.0% 5.0% 5.0% 5.0%

Investec LF 88.3% 88.4% 88.7% 89.3% 89.5% 89.7% 90.1% 91.0% 91.4% 91.8%

Investec ex fuel unit costs 0.4% -0.7% -0.4% -0.2% -0.5% 0.7% -0.8% -0.5% -0.2% -0.3%

Source: Company presentations, Investec Securities estimates

We forecast a 10 year CAGR in volume growth of 7.3% vs. company guidance of

6.9%, driving materially higher LF and unit cost gains. We estimate annualised LF

peaking at 91.8% in FY24 vs. a FY15E LF of 88.3%, outstripping the broader

market LF growth by 1.3pp. In parallel, ex-fuel unit costs are forecast to decline by

2.9% between FY15E and FY24E, driven by higher LF and new aircraft technology.

…..We estimate that a 1% increase in LF is worth 4% in FY16E EPS.

MAX to generate a unit cost tailwind. We

see:

- 4.2% seat density improvement

- 18% fuel burn improvement

- Potential 1.1% fuel efficiency

delta vs. peers

- 6% delta in ownership costs

- Aftermarket sales offer upside

of €0.37 per share

Fortress Stansted – to anchor the network

- STN as a hub could drive 785k

passengers, 0.7pts of LF and

€40m in annual EBIT

Market share and LF gains to be

prioritised with unit costs the beneficiary

- A 1% increase in LF is worth 4%

in FY16 EPS

Page 5 | 03 March 2015| Ryanair

Leading the LCC model does not equate to low ROCE

Ryanair continues to show that the LCC model does not equate to a low return on

capital employed (ROCE). Continued execution of the group’s commercial strategy,

underscored by a sustainable unit cost position, will allow volumes and LF to drive

improved profitability. Ryanair has historically generated robust ROCE, averaging

15.5% since FY04. We forecast lease adjusted ROCE increasing from 23.6% in

FY15E to 30.8% in FY24E, driven primarily by greater LF and improved revenue per

aircraft. We outline our lease adj ROCE calculation in the appendix (p. 51). Over our

10 year forecast horizon, we expect the capital base to grow by a CAGR of 5.9%,

which should be more than offset by an EBIT CAGR of 13.3% on our forecasts.

Figure 9: Ryanair ROCE FY04A-FY24E Figure 10: More profitable revenue from the capital base

Source: Investec Securities estimates Source: Investec Securities estimates

Undemanding valuation

In our view Ryanair’s valuation is undemanding against its own history as well as

relative to that of its closest peer, Easyjet (Not Rated). On a 12 month forward price

to earnings multiple, Ryanair trades on 14.4x, a 3% premium to its 3 year average

and in line with its 10 year average. Assessed alongside Easyjet, Ryanair trades on

a relative premium of 19% versus a 3 year average premium of 18% and a 10 year

average premium of 9%.

Figure 11: Ryanair 1 year forward P/E, trading above 3 year average Figure 12: RYA relative premium to EZJ below its 3 year average

Source: Bloomberg Source: Bloomberg

TP of €13.00 implies 32% upside

We value Ryanair on a returns-driven 10 year DCF basis (page 43). Our DCF maps

an improving return outlook to a target price of €13.00, implying 28% capital upside

from current levels on a 12 month view. With the strong possibility of further capital

returns in FY16E, Ryanair shares look attractive in our view. On our forecasts

Ryanair is trading at 14.4x FY16E and 8.7x Adj EV/EBITDAR. Under new analyst

coverage, we reinitiate with a retained positive stance– BUY.

0%

5%

10%

15%

20%

25%

30%

35% Lease adj ROCE Historical Average

€0

€2

€4

€6

€8

€10

€12

€14

€16

€18

€20

-10%

-5%

0%

5%

10%

15%

20%

25% NOPAT / % of sales (LHS) Sales / Aircraft €m (RHS)

10 x

11 x

12 x

13 x

14 x

15 x

16 x

17 x

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

RYA fwd P/E 3 yr avg 10 yr avg

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

RYA fwd P/E premium 3 yr avg 10 yr avg

Page 6 | 03 March 2015| Ryanair

Move to the centre plays to RYA’s strengths

We believe the fundamentals underlying the intra-European commercial passenger

market are undergoing significant structural change. The Low cast carrier (LCC)

platform is evolving, with both an improved product offering and service level

perception. Legacy carriers continue their retrenchment, with service attributes

being stripped back to better align cost of production to an increasingly competitive

operating environment. We see the end result as an increasingly homogenised

marketplace. With less product differentiation, the price leader should take

significant share. The opportunity space is large with too many operators in Europe.

Step forward Ryanair. Armed with a significant cost of production advantage the

carrier is positioned to substantially benefit from the industry shift.

Figure 13: An increasingly homogenous marketplace

Source: Investec Securities estimates

LCCs pressure forcing legacy unbundling

Ryanair was arguably not the first European LCC to recognise the benefits of an

enhanced product line and brand image. Several players such as Easyjet and Wizz

Air have made product upgrades, albeit less dramatic than Ryanair. We view the

trend as now widespread across the LCC space, accelerating a move to a more

homogeneous marketplace. In parallel to the LCC product upgrades, the European

short haul P2P market has witnessed flag carriers unbundling and scaling back

premium product offerings in an attempt to reduce costs and remain competitive.

Most notably, table 2 below highlights several recent moves taken by legacy

carriers in order to better align the cost competitiveness of their short haul

operations in the face of continued LCC pressure.

Table 2: European carriers adjusting short haul operations to remain competitive

Carrier Year(s) Changes

Air France / KLM 2013-2015 P2P short haul growth through LCC arm Transavia as opposed to mainline

British Airways 2014/2015 Short haul business seat pitch reduced from 34 to 30 inches

British Airways 2013 Lowest lead in short haul fare no longer includes a checked bag

Lufthansa 2013-2015 P2P short haul transitioning to LCC arm Germanwings

Lufthansa 2014/2015 Business class seat pitch moves down from 34 to 32

Lufthansa 2014/2015 Economy seat pitch moves down to 29 from 30

Source: Company reports

BA SH

Ryanair

Finnair SH

AF/KLM SH

Easyjet

LH SH

Air Berlin

SASNorwegian

Price point

Product offering /service level

A move to the centre

A more homogeneous product offering

lends itself to the price leader

LCC competitive pressure has seen

product unbundling by legacy carriers

Page 7 | 03 March 2015| Ryanair

A crowded middle with price as the key variable

The below table provides a snapshot of the intra-European P2P short haul market-

increasingly homogeneous in its core offering, both in economy and business.

Table 3: An equivalent P2P short haul product offering

Business Class Economy Class

Carrier Allocated seating Seat Pitch (inches) Seat Pitch (inches)

Ryanair Yes 30 30

BA short haul Yes 30 30

Lufthansa short haul (Germanwings) Yes 29 29

Norwegian Yes 30 30

Easyjet Yes 29 29

Vueling Yes 30 30

Wizz Yes 30 30

Source: SeatGuru

Following the parallel moves from Ryanair, LCCs and legacy carriers, we view the

product offering as broadly equivalent. Logically, a market with less differentiation

places price to the fore. In this environment, we expect Ryanair to be even more

successful in gaining market share.

European P2P short haul now

commoditised, placing a greater

emphasis on price

Page 8 | 03 March 2015| Ryanair

Ryanair is eradicating the value perception gap In our view, a series of strategic initiatives by Ryanair - under the auspice of the

‘Always Getting Better’ program – are eradicating the value perception gap that had

existed in the marketplace. In doing so, Ryanair increases its addressable market,

places increased competitive pressure on incumbent legacy carriers and facilitates

traffic and share growth.

A move to primary airports: We estimate that the carrier already operates

from half of Europe’s primary airports and that these airports account for 60%

of Ryanair’s seat capacity. Based on the company’s growth guidance, we

forecast that this exposure will increase to 80% by FY20E. Assuming primary

airports merit an average fare uplift of €10 group average revenue per

passenger could be boosted by 3.2%, with upside reinvested in the market in

pursuit of share gain and higher LF. We see Amsterdam Schiphol (AMS),

Dusseldorf (DUS), Munich (MUC), Oslo (OSL) and Zurich (ZRH) as the logical

next steps for Ryanair expansion.

Increasing frequency and schedule quality: Ryanair continues to place

competitive pressure on peers, both LCC and legacy incumbents, through

enhancing its network with increased frequencies on core business routes. The

carrier’s most recent February schedule sees Ryanair seat capacity +13% with

the number of routes served declining by 1%. As a result, route thickness (total

seats per route) increases 14%. Ryanair’s summer 2015 schedule highlights

the continuation of this trend.

Expanded product offering: Allocated seating, fast track access, and

business products are some of the headline product improvements rolled out

by the carrier in 2014. The overhaul of legacy revenue management strategies

has resulted in a linear yield curve favouring far out booking accumulation and

supporting higher LF performance.

Brand and distribution overhaul: Beginning with its shop window -

Ryanair.com - the carrier has refreshed its product positioning. The revamped

website and increased social media interaction represent a step change in

marketing and brand awareness activities. We see further scope for the carrier

to narrow the brand perception gap through a cabin interior refit coinciding with

the arrival of 40 new aircraft in FY16.

Is the strategy working? The proof is in the LF

Brand surveys suggest this change is well received by customers with Ryanair

ranking at the top of the recent YouGov airline brand improvement survey.

Ryanair.com is now the most searched for airline website in the UK. The end

result is clearly visible, with rolling 12 month LF performance +4pp yoy and

rolling 3 month performance +8.7pp yoy.

Primary airport capacity rising from 60%

to 80% by FY20E to drive 3.2% uplift in

average revenue per passenger

LF highlights a strategy gaining

momentum:

- Rolling 12 month LF +4pp yoy

- Rolling 3 month LF +8.7pp yoy

Page 9 | 03 March 2015| Ryanair

Primary airports – growing the addressable market

The Winter 2014/2015 schedule saw Ryanair build out frequencies at Dublin (DUB),

STN and a host of other central airports. Ryanair has effectively continued its

expansion into the last bastion of European legacy carriers - the primary airport.

This trend is set to continue with 50% of summer capacity growth guided by

management for primary airports. By changing its network and frequency, Ryanair

is eradicating the value perception gap thereby creating a more homogeneous

marketplace. The endgame is to fulfil ambitious growth plans by increasing the

addressable market size. Primary airports appear attractive; they offer higher

yielding passengers, reduce seasonality of traffic flows and provide economies of

scale (marketing, support costs etc.).

Significant progress already made

We believe that Ryanair is already deep into its program of changing its network

footprint. Primary airports that have or will soon hear the arrival jingle from a

Ryanair Boeing 737 aircraft include: Athens (ATH), Brussels (BRU), Copenhagen

(CPH), Lisbon (LIS), Rome Fiumicino (FCO), as well as more central level 2 airports

such as Cologne (CGN), Glasgow Intl (GLA) and Gdansk (GDN). The carrier

already has greater than 50% coverage at primary airports, a fact that we believe is

underappreciated by the market. While much debate persists over the definition of a

primary airport, we adopt IATA’s definition of a Level 3 airport to be a primary

airport. According to the following classification:

Level 3 (Fully Coordinated Airport): Demand for the airport infrastructure

significantly exceeds the airport’s capacity. We view IATA level 3 airports as

primary airports.

Level 2 (Schedules Facilitated Airport): Demand exceeds supply only during

certain time periods. We view IATA level 2 airports as secondary airports.

Level 1 (Non-Coordinated): The capacity of the airport is sufficiently

adequate to meet demand at all times. We view IATA level 1 airports as

secondary airports.

We highlight below Ryanair’s presence at Level 3 (primary) and Level 2 airports.

Table 4: Snapshot of Ryanair’s primary airport coverage

Classification Number RYA coverage Examples

Level 3 100 50% DUB, BRU and STN

Level 2 74 42% Edinburgh (EDI), GLA, and Budapest (BUD)

Source: IATA

Wasting no time, more new routes than any other airline

No other global carrier launched more routes in 2014 than Ryanair, with 134 routes

launched - 50 more routes than its closest peer, Germanwings. Germanwings - the

LCC subsidiary of Deutsche Lufthansa - can attribute the majority of its 2014 route

launches to the legacy parent retrenching from intra-European point to point (P2P)

flying. This legacy retrenchment echoes the move to the centre and a more

homogeneous product environment.

50% of summer2015 capacity growth is

guided for Primary Airports

Supply and demand imbalances highlight

primary airports

Page 10 | 03 March 2015| Ryanair

Figure 14: Top airline for new route launches in 2014

Source: Anna Aero

What is left on the table?

Management has recently stated that Charles De Gaulle (CDG) and Frankfurt Main

(FRA), both Level 3 primary airports, are off the table for future Ryanair operations.

We see 48 Level 3 airports in contention and highlight below the primary European

airports, with both the greatest passenger throughput and Ryanair operations in

2014.

Table 5: Current and potential primary airports for Ryanair

Current primary airports Ryanair operate from Potential primary airports Ryanair could move to

Airport IATA Code 2014 Passenger volume (m) yoy growth Airport IATA Code 2014 Passenger volume (m) yoy growth

Madrid MAD 41.8 5.3% Heathrow LHR 73.3 1.4%

Gatwick LGW 38.1 7.4% Amsterdam AMS 55.0 4.6%

Rome Fiumicino FCO 38.0 5.1% Munich MUC 40.0 3.5%

Barcelona BCN 37.6 6.7% Paris Orly ORY 28.9 2.1%

Copenhagen CPH 25.6 6.5% Zurich ZRH 25.4 2.5%

Palma Majorca PMI 23.1 1.5% Oslo OSL 24.3 4.8%

Brussels BRU 22.0 15.2% Stockholm Arlanda ARN 22.5 8.9%

Dublin DUB 21.7 7.7% Vienna VIE 22.5 2.3%

Stansted STN 19.9 11.6% Dusseldorf DUS 22.0 3.6%

Lisbon LIS 17.9 11.9% Berlin Tegel TXL 20.8 6.4%

Malaga AGP 13.7 6.4% Helsinki HEL 15.9 4.4%

Source: Anna Aero, IATA

Where next for Ryanair?

We see the logical next steps for Ryanair in its primary airport build out as AMS,

DUS, MUC, ZRH and OSL. We also view a partial move from Paris Beauvais

(BVA) to Paris Orly (ORY) as a reasonable step for the carrier. However ORY - a

level 3 airport - is highly slot constrained, with existing operators such as Easyjet

reportedly waiting in the wings should slots materialise. Finally, LHR remains in

play as management has stated that it “would look at LHR if slots became

available, however a 25 min turnaround would be hard”.

28

28

28

29

33

33

36

41

43

46

50

58

68

80

83

84

134

0 20 40 60 80 100 120 140

Germania

Jetairfly

Volaris

Meridiana

Aegean

Delta

Flybe

United

Norwegian

SAS

Wizz Air

Southwest

Frontier

Vueling

Easyjet

Germanwings

Ryanair

2014 Route launches

Several key primary airports in the mix for

future expansion

With the exception of CDG and FRA, all

Primary airports are in play. We see AMS,

MUC, ZRH, and OSL as the next steps.

Page 11 | 03 March 2015| Ryanair

Table 6: Recent commentary on primary airport growth

Market(s) Airport Recent Announcements

The Netherlands, Ireland, UK & Europe AMS Ryanair intends to increase its Dutch market share, estimated at 4%. Signalling future operations at AMS linking both DUB and STN builds out the primary airport footprint. A new secondary airport leisure base at

Leystadt (LEY) has been flagged and we believe this compliments existing Eindhoven operations.

Italy FCO Ryanair grows Italian presence at Rome FCO with destinations doubling from 5 to 10 for Summer 2015. In

contrast Vueling are reducing domestic Italian services and increasing its international FCO operations.

Belgium & Ireland BRU Ryanair indicates that they have secured ca. 50% market share on the key primary airport business route

within 3 months of the inaugural service

UK LHR Ryanair indicates that it would look at London Heathrow (LHR) slots should they become available. The

carrier states that it would not however conform to its 25 minute turn business model.

Source: Company presentations

Primary airports yield uplift - a snapshot

Primary airports are characterised by passengers with a lower price elasticity of

demand, a higher proportion of business travellers, less seasonality in the traffic

flows and ultimately a passenger mix that has a higher propensity to book later in

the booking cycle.

In table 7 below, we highlight average fares and yield per passenger kilometre on

two intra-European P2P routes from London. While a health warning should be

placed on the below example, the findings highlight that even in an increasingly

homogenised market, passengers are willing to pay a €60 premium to fly from LHR

and LCY compared to STN. We see the continued move by Ryanair to primary

airports providing yield uplift for the carrier, which will be reinvested in the market as

the airline pursues its market share ambitions.

Table 7: Yield analysis from London metro area to Amsterdam (AMS) and Geneva (GVA)

London airport

AMS GVA

Code Fare Yield Fare Yield

London Heathrow LHR €108.80 €0.30 €149.60 €0.20

London Gatwick LGW €64.80 €0.18 €61.60 €0.09

London Stansted STN €42.40 €0.14 €53.60 €0.07

London Luton LTN €43.20 €0.12 €56.00 €0.07

London City LCY €104.80 €0.30 €155.20 €0.21

Source: IATA

While primary airports will bring obvious

yield uplift, we view near term gains as

being reinvested in the market

Page 12 | 03 March 2015| Ryanair

Increased frequencies backfill an already strong network

Ryanair continues to place competitive pressure on peers through enhancing its

network with increased frequencies on core business routes. The carrier’s February

2015 schedule sees its seat capacity rising +13% with the number of routes served

declining -1%. As a result route thickness (total seats per route) increases +14%.

Table 8: Ryanair winter frequency build out

Winter 13/14 Winter 14/15 Variance

Seat capacity 5,719,896 6,451,326 13%

Routes 1,649 1,635 -1%

Thickness 3,469 3,946 14%

Source: Innovata

Ryanair’s summer 2015 schedule highlights the build out of frequency at primary

airports. Figure 9 below highlights the airports benefitting from a flexing of frequency

with weekly departures driving a 6.2% increase in seat capacity for the summer

2015 season.

Figure 15: Increase in weekly departures on Ryanair’s network, August’15 vs. August’14

Source: Anna Aero

24

24

25

28

38

39

44

54

58

58

63

65

75

99

127

0 20 40 60 80 100 120 140

Porto (OPO)

Berlin (SXF)

Edinburgh (EDI)

Copenhagen (CPH)

Barcelona (BCN)

Milan (BGY)

Colgone (CGN)

Glasgow (GLA)

Lisbon (LIS)

Warsaw (WMI)

Rome (FCO)

Dublin (DUB)

Athens (ATH)

Madrid (MAD)

London (STN)

Route thickness increased 13% in winter

14/15 and summer schedules indicate

further build out.

Page 13 | 03 March 2015| Ryanair

Legacy carrier P2P operations at primary airports under pressure

With an increased primary airport mix and a thickening of route frequencies

Ryanair’s competitive presence on traditional primary P2P routes is growing.

Utilising its cost of production advantage, the carrier can ‘price for growth’. The fare

gap between LCC and legacy airlines is evident on traditional routes linking two

primary airports, for example Rome and Brussels. Here we see Ryanair 75% and

82% cheaper on leisure and corporate fares respectively.

Table 9: Rome Fiumicino (FCO) to Brussels Zaventum (BRU) market

Ryanair

Vueling

Depart Arrive Depart Arrive

Depart Arrive Depart Arrive

07:35 09:50 10:15 12:20

08:00 10:15 10:50 12:50

18:30 20:50 15:40 17:55

18:05 20:20 21:00 23:00

Lead in fare €98.98

Lead in €87.00

Business Plus €199.98

Excellence Fare €309.98

Alitalia

Brussels Airlines

08:20 10:35 11:25 13:30

06:30 08:40 07:50 09:50

15:00 17:15 18:15 20:20

10:30 12:40 15:05 17:10

17:55 20:00 20:40 22:40

Lead in €399.72

Lead in €338.72

Business Basic €1,085.72

Flex & Fast €498.72

Source: Airline direct websites. Date of travel 26/2/2015. Date of capture 27/1/2015

Fare structure gap is striking on a key

European P2P city pair

Page 14 | 03 March 2015| Ryanair

Expanded product line, enhanced brand

Under the auspice of the ‘Always Getting Better’ program, Ryanair has also rolled

out a series of radical improvements to eradicate the product differentiation gap in

the intra-European short haul market. By refreshing its brand and expanding its

product portfolio, the carrier is seeking to increase its addressable market by

appealing to a wider consumer base. We see the end result as an airline that no

longer pushes away subsets of the corporate and leisure market. Early indications

in both brand perception and LF performance indicate the strategy is working.

Figure 16:Ryanair ‘Always Getting Better’

Source: Company presentation

Scope to narrow the gap further, an accelerated cabin refresh

The above chart summarises product enhancements already announced by

Ryanair. We see potential for further improvements. For example, we see scope for

a cabin refresh to begin in Q116, some 16 quarters earlier than guided by

management. The Boeing Sky Interior concept, highlighted in Fig.10 below, is

currently scheduled to form part of Ryanair’s MAX200 delivery with the first aircraft

scheduled for arrival in FY20. Our view is that management will look for an

accelerated roll out of the upgraded cabin appearance as part of their 3 year

‘Always Getting Better’ program. By doing so Ryanair could further narrow the

product perception gap currently present in the European marketplace thereby

growing its addressable market potential.

Figure 17: Current Ryanair cabin interior Figure 18: Future Ryanair sky interior cabin

Source: SeatGuru Source: Boeing

Brand refresh and expanded product line

targets a larger traffic base

Digital improvements drive conversion

factors, traffic volumes and LF

Page 15 | 03 March 2015| Ryanair

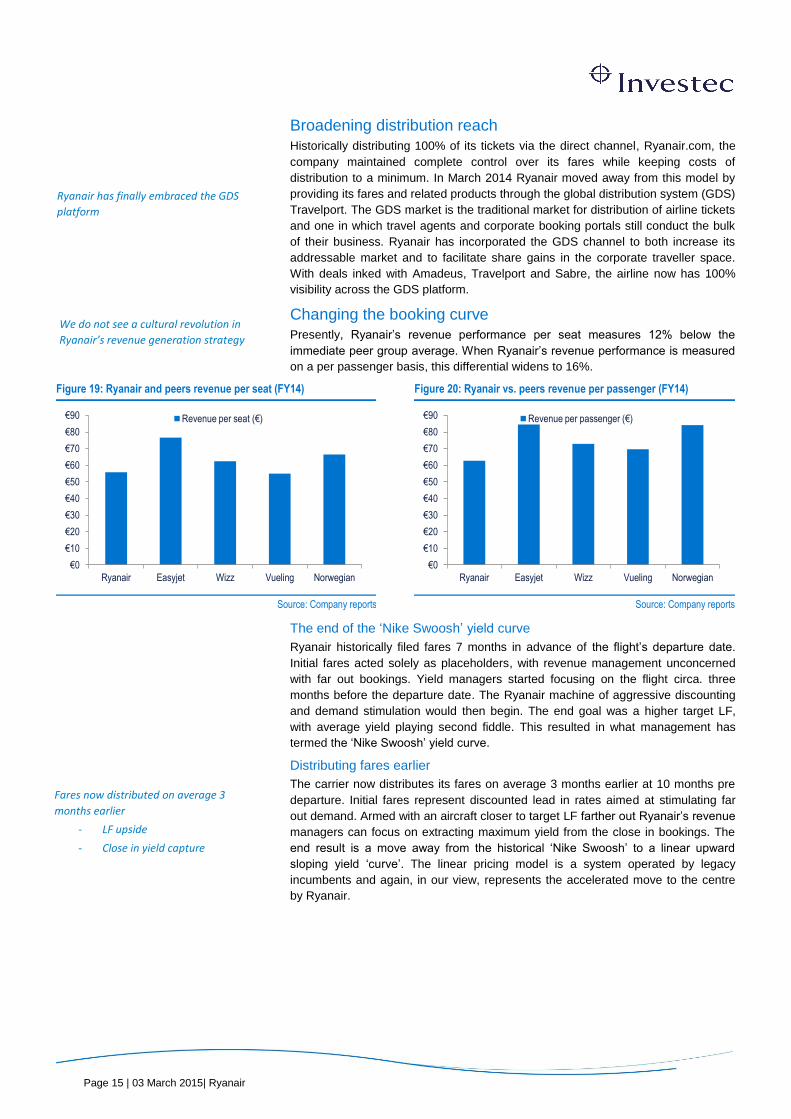

Broadening distribution reach

Historically distributing 100% of its tickets via the direct channel, Ryanair.com, the

company maintained complete control over its fares while keeping costs of

distribution to a minimum. In March 2014 Ryanair moved away from this model by

providing its fares and related products through the global distribution system (GDS)

Travelport. The GDS market is the traditional market for distribution of airline tickets

and one in which travel agents and corporate booking portals still conduct the bulk

of their business. Ryanair has incorporated the GDS channel to both increase its

addressable market and to facilitate share gains in the corporate traveller space.

With deals inked with Amadeus, Travelport and Sabre, the airline now has 100%

visibility across the GDS platform.

Changing the booking curve

Presently, Ryanair’s revenue performance per seat measures 12% below the

immediate peer group average. When Ryanair’s revenue performance is measured

on a per passenger basis, this differential widens to 16%.

Figure 19: Ryanair and peers revenue per seat (FY14) Figure 20: Ryanair vs. peers revenue per passenger (FY14)

Source: Company reports Source: Company reports

The end of the ‘Nike Swoosh’ yield curve

Ryanair historically filed fares 7 months in advance of the flight’s departure date.

Initial fares acted solely as placeholders, with revenue management unconcerned

with far out bookings. Yield managers started focusing on the flight circa. three

months before the departure date. The Ryanair machine of aggressive discounting

and demand stimulation would then begin. The end goal was a higher target LF,

with average yield playing second fiddle. This resulted in what management has

termed the ‘Nike Swoosh’ yield curve.

Distributing fares earlier

The carrier now distributes its fares on average 3 months earlier at 10 months pre

departure. Initial fares represent discounted lead in rates aimed at stimulating far

out demand. Armed with an aircraft closer to target LF farther out Ryanair’s revenue

managers can focus on extracting maximum yield from the close in bookings. The

end result is a move away from the historical ‘Nike Swoosh’ to a linear upward

sloping yield ‘curve’. The linear pricing model is a system operated by legacy

incumbents and again, in our view, represents the accelerated move to the centre

by Ryanair.

€0

€10

€20

€30

€40

€50

€60

€70

€80

€90

Ryanair Easyjet Wizz Vueling Norwegian

Revenue per seat (€)

€0

€10

€20

€30

€40

€50

€60

€70

€80

€90

Ryanair Easyjet Wizz Vueling Norwegian

Revenue per passenger (€)

Ryanair has finally embraced the GDS

platform

We do not see a cultural revolution in

Ryanair’s revenue generation strategy

Fares now distributed on average 3

months earlier

- LF upside

- Close in yield capture

Page 16 | 03 March 2015| Ryanair

Figure 21: Reshaping the yield curve (illustrative)

Source: Investec Securities estimates

Incorporating modular product offering

The introduction of a modular product offering allows Ryanair to maintain its

industry leading fares, preserve its linear pricing model and increase the size of its

target market through the introduction of Business Plus, Family Extra and allocated

seating.

By allowing passengers to customise their travel experience Ryanair’s revenue

managers are effectively price discriminating a linear curve, increasing yield capture

and most importantly facilitating higher LF. We see LF moving to the fore as a result

of: 1) fares distributed earlier allowing for a longer booking window, 2) a linear

pricing curve favouring LF capture and 3) an expanded product portfolio increasing

the addressable market size.

Figure 22: Modular product offering

Source: Investec Securities estimates

10 9 8 7 6 5 4 3 2 1

Linear Pricing Model Historic Nike Swoosh

Months pre departure

Extended distribution period

Business Plus/ Fast Track

Allocated Seating

Baggage

Air Ticket

Linear pricing model resembles that of

legacy competition highlighting the

‘move to the centre’

Modular product offering protects lead in

airfare and allows product customisation

Page 17 | 03 March 2015| Ryanair

Is Ryanair’s brand strategy working?

Early indications suggest that Ryanair’s brand strategy is starting to work. Public

perception in the UK indicates that Ryanair’s brand improvement is outpacing that

of its airline industry peers. The change in brand perception results in table 10

below are based on the YouGov Brand Index Buzz Tracker survey which asks

respondents, “If you’ve heard anything about the brand in the last two weeks was it

positive or negative? Ryanair’s brand perception improved by a measure of 5 index

points between Jan-Jun 2014.

Table 10: Change in brand perception, (Jan–Jun’14 vs. Jan-Jun’13)

Rank Brand Improvement Jan-Jun'14 Score Jan-Jun'13 Score

1 Ryanair 5.0 -15.4 -20.4

2 Easyjet 3.9 2.8 -1.1

3 British Airways 2.8 8.9 6.2

4 Flybe 1.5 0.8 -0.7

5 Jet2.com 1.0 0. 1.1

Source: CAPA

Brand perception gaining momentum

In a broader contect, the Ryanair brand improvement is gaining traction, with an

improvement of 10.6 index points at the time of the FY14 results (Table 11).

Table 11: FY:14 Change in brand perception, YouGov Brand Index Buzz Tracker (2014-2013)

Rank Brand Improvement

1 Lidl 11.6

2 Ryanair 10.6

3 Aldi 10.0

4 Findus 9.8

5 HMV 7.5

Source: Company presentation

Increased addressable market driving higher LF

Ryanair’s UK website visit ranking has been transformed moving from 3rd

to 1st, on

Hitwise data, further evidence that the brand transformation is gaining traction.

Importantly, Ryanair’s efforts are translating into a clear pick up in passenger

volumes and LF since its recent transformation.

Figure 23:UK’s most searched airline websites Dec13-Sep14 Figure 24: Ryanair LF Performance (% change)

Source: Company presentation Source: Company reports

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

0%

1%

2%

3%

4%

5%

6%

7%

8% Load Factor (LHS) Capacity (RHS)

Brand Depth: Ryanair value change

starting to resonate with the public.

LF transformation

- Rolling 12 month LF + 4pp yoy

- Rolling 3 month LF +8.7pp yoy

Page 18 | 03 March 2015| Ryanair

New strategy sets virtuous circle in motion

Ryanair growth was historically perpetuated on the basis of its lowest cost base,

permitting it to discount fares aggressively and stimulate demand to secondary

airports that European consumers would previously have not considered.

Figure 25: Unit costs per passenger, € (FY14) Figure 26: Ex fuel unit costs per passenger, € (FY14)

Source: Company reports Source: Company reports

Contrary to popular belief, we do not now see a cultural revolution underway at the

carrier. Ryanair is playing to its strengths as the lowest unit cost producer in an

increasingly homogeneous market (P2P intra-European air travel) allowing it a price

advantage over legacy and LCC carriers alike (average fares estimated at 26%

below that of closest peer, Easyjet). Ryanair can push its unit costs down even

farther, reinforcing its structural advantage, by driving increased traffic and higher

LF. Armed with a reinforced cost position, the carrier is positioned to ‘price for

growth’. We see this as a ‘virtuous circle’ of unit costs.

Figure 27: Ryanair’s virtuous circle of unit costs

Source: Investec Securities estimates

0

10

20

30

40

50

60

70

80

Ryanair Wizz Easyjet Vueling

0

10

20

30

40

50

60

Ryanair Wizz Easyjet Vueling

Ex fuel unit cost per passenger 28% below

that of rivals

Higher LF and passenger growth spins the

wheel of unit costs

Page 19 | 03 March 2015| Ryanair

Higher LF

We believe that the changes at Ryanair will allow the company to drive sustainably

higher LF while also providing greater revenue per seat potential.

Figure 28: Ryanair LF Progression Figure 29: Industry LF Performance Snapshot (%)

Source: Company reports Source: Innovata

Fig 29 above shows a Ryanair lagging peer improvements over recent years before

a change in strategic direction transformed LF performance. Traffic data indicates

that the strategy is already working with rolling 12 month LF+3pts to 86% and Q3:15

+6.4pts to 88.4%. While consensus is bullish, we see further upside to Ryanair’s

traffic and subsequent LF performance. Fig. 30 below shows Ryanair closing the

monthly LF performance gap vs. Easyjet at an impressive rate. With momentum

behind Ryanair and a comercial department favouring LF over yield. We see asset

utilisation levels eclipsing that of Easyjet. We forecast annualised LF peaking at

91.8%, outstripping broad market LF growth by almost 3pp.

Figure 30: RYA and EZJ year on year LF performance (LHS) and monthly LF spread (RHS)

Source: Company reports

Raising the bar on traffic

Ryanair is on course to achieve 10.5% passenger growth in FY15 and the carrier

has guided to passenger growth of between 5% and 11% per annum out through

FY24. This clear growth strategy will see passengers carried move from 81.7m in

FY14 to a company guided 160m in FY24. Fig. 31 below outlines company guided

traffic against implied seat capacity growth from the fleet delivery pipeline. We

believe that with seat capacity in its arsenal the company is well poised to raise the

bar on traffic forecast.

60%

65%

70%

75%

80%

85%

90%

95%

20

03

20

03

20

04

20

04

20

05

20

05

20

06

20

07

20

07

20

08

20

08

20

09

20

10

20

10

20

11

20

11

20

12

20

12

20

13

20

14

20

14

Ryanair Monthly Load Factor

70%

75%

80%

85%

90%

2006 07 08 09 10 11 12 13 2014

Ryanair

Easyjet

Wizz Air

Vueling

BA

Norwegian

Transavia

LF

0%

2%

4%

6%

8%

10%

12%

14%

16%

0%

1%

2%

3%

4%

5%

6%

7%

8% RYA EZJ EZJ vs. RYA (RHS)

Fuller, more profitable planes operating

on Ryanair’s growing network

Closing the gap on the league leaders of

LF in just 12 months

Page 20 | 03 March 2015| Ryanair

Figure 31: Guided passenger growth vs. aircraft delivery implied seat growth

Source: Company presentations

We estimate a 10 year CAGR of 5.3% in terms of seat capacity growth based on

the fleet evolution profile out through FY24. We believe that not only will Ryanair fill

its additional capacity, but that it will outstrip capacity growth with traffic growth.

Table 9: Fleet evolution highlights capacity outlook

Fleet development 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E

Beginning Fleet 300 308 342 370 402 420 474 483 497 512

737NG Deliveries 11 40 50 50 29 0 0 0 0 0

MAX 200 Deliveries 0 0 0 0 0 62 34 42 40 22

737NG Exits (3) (6) (22) (18) (11) (8) (25) (28) (25) (14)

Ending Fleet 308 342 370 402 420 474 483 497 512 520

Additional seat capacity (millions)

737NG 2.5 10.6 8.7 9.9 5.6 (2.5) (7.8) (8.7) (7.8) (4.3)

MAX200 0.0 0.0 0.0 0.0 0.0 20.1 11.0 13.6 12.9 7.1

Net seat change 2.5 10.6 8.7 9.9 5.6 17.6 3.2 4.9 5.2 2.8

Total network seats 102.3 112.9 121.5 131.5 137.1 154.6 157.9 162.8 168.0 170.7

% change in seats

10.3% 7.7% 8.2% 4.2% 12.8% 2.1% 3.1% 3.2% 1.7%

% change in fleet units

11.0% 8.2% 8.6% 4.5% 12.9% 1.9% 2.9% 3.0% 1.6%

Source: Investec Securities estimates

Unit costs to benefit from higher traffic and LF

With renewed emphasis on traffic, share growth and increased seat occupancy, we

see higher LF performance driving yet lower unit costs per seat. Flexing our LF

assumptions drives healthy drop-through margins. We estimate that for every 1%

increase in LF, unit costs decrease by 0.8%. All else being equal, as a result of a

1% increase in our FY16E LF assumption, EPS receives a 4% uplift.

0%

2%

4%

6%

8%

10%

12%

14%

0%

2%

4%

6%

8%

10%

12%

14%

2015E 2016E 2017E 2018E 2019E 2020E 2012E 2022E 2023E 2024E

Guided passenger growth Implied seat capacity growth

Passenger and capacity growth

underscored by fleet evolution

A 1% increase in LF results in a 4%

increase in FY16E EPS.

Page 21 | 03 March 2015| Ryanair

Greater market share, a fragmented market ripe for consolidation

While questions have been raised on how Ryanair will deliver passenger growth

amounting to a 10year CAGR of 5.9%, we believe there remains a significant

opportunity for Ryanair to grab market share in Europe. The European commercial

aviation market is fragmented with a total of 34 carriers holding 80% of intra-

European seat capacity. In contrast, the domestic U.S. market currently has 4

carriers providing 80% of seat domestic capacity. We see both an aggregation of

capacity providers and suppliers exiting the market as a result of increased and

prolonged competitive pressure.

Supply and demand dynamics in equilibrium

Against a backdrop of 3% forecast average annual growth in regional European

economic activity over the next 10 years (according to the IMF), we expect

passenger traffic to increase by 3.5% per annum as measured by revenue

passenger kilometres (RPKs) and based on Airbus’ Global Market Forecast. Such

passenger growth is equivalent to a 1.2x GDP multiple, reflective of a relatively

mature industry underpinned by an improving macroeconomic environment.

Meanwhile, we forecast capacity increasing by 3.2% annually, marginally outpaced

by demand. As a result we forecast industry wide load factor increasing modestly

over our forecast period by circa 25bps per annum from 80.8% to 83.0%.

Figure 32: Long run rational capacity allocation observable in European short haul market

Source: IATA

Figure 32 above highlights a European marketplace exhibiting rational capacity

deployment over the last 10 years. We expect net intra-European seat capacity

growth to remain relatively benign, with continued retrenchment of legacy carriers

from non-hub P2P flying and carriers exiting the industry counter balancing the LCC

capacity coming on-stream.

The evolution of LCC capacity in Europe

LCC share growth dynamics are well embedded in the intra-European market. Over

the past decade, LCC capacity growth has averaged 14% per annum. In contrast,

the legacy carrier model has produced average capacity growth rates of 1% per

annum Figure 33 below depicts the growth of the broader LCC and hybrid LCC

capacity share growth in the European market.

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

Passenger Demand (RPKs) Capacity (ASKs)

80% of seat capacity delivery:

Domestic US: 4 carriers

Intra-Europe: 34 carriers

European passenger capacity deployment

has followed a rational path over the last

10 years

Page 22 | 03 March 2015| Ryanair

Figure 33: The evolution of the broader LCC movement in the European market

Source: CAPA

Ryanair to lead LCC share gains

Ryanair has already taken sizeable market share, with a 10 year CAGR in

passenger growth of 13%. We estimate that Ryanair commands 14% total market

share, a figure that we see rising to 25% by 2024. We see the LCC space leading

European market consolidation, with Ryanair as best positioned to lead the charge

supported by its fleet order book.

Order books highlight the growth trajectory in Europe

The individual order books of both LCC and legacy carriers, alongside assumed

retirement profiles for the European commercial fleet, support our share thesis. Our

analysis highlights a European capacity environment adding 3% CAGR of

incremental seat capacity between 2014 and 2024, with Ryanair, Easyjet,

Norwegian Air and Wizz Air together accounting for between 47-66% of annual seat

capacity deployment in any given year.

Figure 36: LCC share of intra-European capacity growth

Source: Ascend, Investec Securities estimates

Delivery / Retirement profiles highlight a changing hierarchy

Based on current order books and aircraft retirement profiles, we estimate that

Ryanair’s share of seat capacity will increase by c.4pp by 2019 in an intra-European

context, equating to 30m additional passengers. We view this as a relatively

conservative assumption, exiting Ryanair jets at c.15 years to maintain an average

fleet age profile of c.6 years, Easyjet aircraft at 15 years and the remaining

European peer base at an average age of 21 years.

5%

8%

14%

18%

21%

24%

29%

31% 32%

35% 36%38%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0%

1%

2%

3%

4%

5%

6%

40%

45%

50%

55%

60%

65%

70% LCC share of capacity growth (LHS) European capacity growth (RHS)

We estimate Ryanair market share could

reach 25% by 2024

LCCs to account for 47%-66% of annual

seat capacity deployment in any given

year

Page 23 | 03 March 2015| Ryanair

Table 13: European seat forecast to 2019, assuming fleet retirements and new orders

Carrier 2014 closing fleet 2015 2016 2017 2018 2019

Ryanair 57,078 63,693 72,387 82,026 87,129 90,100

Easyjet 37,056 39,936 43,176 49,296 55,236 57,876

Norwegian 17,035 18,003 21,141 26,643 30,187 32,115

Wizz 9,900 14,220 17,900 21,200 21,020 21,020

IAG 47,577 46,182 47,982 50,202 53,865 57,333

Lufthansa Passenger Group 63,187 54,976 56,714 57,273 56,275 56,175

Air France / KLM Group 45,803 44,734 43,840 42,408 42,118 41,279

Other 247,111 255,871 239,067 242,028 247,704 256,798

Total Europe 524,747 537,615 542,207 571,076 593,534 612,696

Source: Ascend, Investec Securities estimates

Table 14: Relative % size of fleet seat capacity assuming fleet retirements and new orders

Carrier 2014 closing fleet 2015 2016 2017 2018 2019

Ryanair 10.9% 11.8% 13.4% 14.4% 14.7% 14.7%

Easyjet 7.1% 7.4% 8.0% 8.6% 9.3% 9.4%

Norwegian 3.2% 3.3% 3.9% 4.7% 5.1% 5.2%

Wizz 1.9% 2.6% 3.3% 3.7% 3.5% 3.4%

IAG 9.1% 8.6% 8.8% 8.8% 9.1% 9.4%

Lufthansa Passenger Group 12.0% 10.2% 10.5% 10.0% 9.5% 9.2%

Air France / KLM Group 8.7% 8.3% 8.1% 7.4% 7.1% 6.7%

Other 47.1% 47.6% 44.1% 42.4% 41.7% 41.9%

Total Europe 100% 100% 100% 100% 100% 100%

Source: Ascend, Investec Securities estimates

Share gains should remain on track

No company is immune to periodic economic down-cycles, Ryanair included.

Potential macroeconomic shocks and irrational competitor activity, while disruptive,

should not derail our investment thesis. A high degree of operational flexibility and a

best in class unit cost platform provide protection in downturns, allowing the

company to continue its pursuit of volume growth and aggregation of intra-European

P2P market share.

High degree of operational flexibility: Ryanair has a high degree of

operational flexibility in its business model, enabling it to scale back production

and variable costs in the event of an economic downturn. In FY12 the carrier

grounded 30% of its fleet as a result of a weak economic backdrop and high

fuel prices. During that year, net profit increased 50% yoy with lease adjusted

ROCE + 1.5% yoy.

Lowest average fares: Operating from an industry leading cost position

allows the carrier to charge the lowest average fares in the European sector

(estimated at 26% below that of peers – see Figure 37 below) while continuing

to generate economic returns. As a result, we see any potential destabilisation

from lower industry yields as short term, with the long term sustainability of

discounting by peers unviable.

Ryanair’s fleet to become the largest

provider of intra-Euro seat capacity

Ryanair’s business model has been ‘stress

tested’ for macroeconomic downturns

Page 24 | 03 March 2015| Ryanair

Figure 37: Ryanair average fare 26% below that of its closest peer

Source: Company reports, Investec Securities estimates

Ryanair, the leader of the pack

LCC share of intra-European capacity indicates a divergence in growth ambitions

vs. legacy carriers. A fragmented market presents ample scope for carriers to exit

the industry providing upside to share projections. We estimate that Ryanair will

take its share from 14% to 25% of the total market by 2024, leading the LCC sector.

We view 25% market share as achievable for Ryanair as it grows its forecasted

traffic base by 102% from 81.7m in FY14 to 165m in FY24E. Share gains are

consistent with historical trends exhibited by the carrier. We see potential for some

rationalisation in future short haul deliveries to European carriers, with any deferrals

or cancellations providing scope for further share gain by Ryanair. Furthermore,

with 34 carriers currently providing 80% of intra-European short haul capacity vs. 4

in the domestic US, we see large scope for consolidation through carriers exiting

the market and LCCs, led by Ryanair, absorbing share. After only a month of

trading in 2015, we have seen the demise of 2 capacity providers - Cyprus Airways

and Eurolot.

Table 15: The virtuous circle of unit costs driving share gain to 25% in FY24E

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E

Passenger growth 10.5% 11.5% 6.3% 7.7% 6.3% 7.3% 6.5% 6.0% 5.5% 5.5%

Capacity growth 3.9% 11.3% 6.0% 7.0% 6.0% 7.0% 6.0% 5.0% 5.0% 5.0%

LF 88.3% 88.4% 88.7% 89.3% 89.5% 89.7% 90.1% 91.0% 91.4% 91.8%

Ex fuel unit costs 0.4% -0.7% -0.4% -0.2% -0.5% 0.7% -0.8% -0.5% -0.2% -0.3%

Source: Investec Securities estimates

And the circle continues… Market share gains will facilitate Ryanair’s impressive roll out of capacity. Higher

volumes will drive down unit costs reinforcing Ryanair’s competitive pricing. And the

circle continues…

€0

€20

€40

€60

€80

€100

€120

€140

Ryanair Easyjet Norwegian Air Berlin AF / KLM short haul

We forecast 25% market share by 2024

Page 25 | 03 March 2015| Ryanair

Enter the Max

While Ryanair’s new strategy is building LF and reducing unit costs, we believe the

introduction of the MAX in FY20 will provide scope for the carrier to increase its

competitive advantage vs. the competition. Increased fuel efficiency and reduced

operating costs alongside reduced noise and emissions underscore what is widely

aknowledged to be the most competitive unit cost platform in the industry.

Refreshed cabin interiors, improved range and best in class seat capacity

accelerate a brand refresh and leverage the volume driven revenue generation

strategy. Finally, in transitioning to the MAX we see scope for revenue generation

opportunities in the aftermarket before the wheels leave the tarmac.

Figure 38: Ryanair’s MAX order will see the carrier reach new heights

Source: Boeing

Fleet strategy sees Ryanair reaching new heights

We forecast that the cost gap enjoyed over competitors will not only be maintained,

but should actually widen. Costs stand to benefit from an increase in seat density of

4.2%, an 18% improvement in fuel burn per seat and importantly a potential 1.1%

per seat delta over competitors in fuel efficiency. An estimated 6% delta in

depreciation costs per seat vs. peers should widen the ownership cost gap.

Furthermore, we see the potential for Ryanair to generate €519m in after tax profits

from asset sales as part of its upcoming fleet rollover program, with a PV / share of

€0.37 on our estimates. In addition, we believe the MAX offers incremental annual

revenue generation with a PV/share of €0.09.

The arrival of the MAX in FY20 provides

scope for revenue, cost and brand refresh

opportunities

Unit cost tailwind:

- 4.2% seat density improvement

- 18% fuel burn improvement

- Potential 1.1% fuel efficiency

per seat delta vs. peers

- 6% delta in ownership costs per

seat vs. peers

Page 26 | 03 March 2015| Ryanair

Seat density underscores unit costs

Ultimately seat density represents the trump card when assessing unit costs. By

increasing the maximum potential passenger count per aircraft the denominator of

the unit costs equation is driven ever lower. Aircraft manufacturers are acutely

aware of this trend. While Airbus’ recent patent application for bicycle style airplane

seating may be a bridge too far, it nevertheless highlights the industry wide

acknowledgement that by increasing capacity you lower unit costs.

Figure 39:The pursuit of seat density, patented bicycle airline seating

Source: Airbus

Ryanair currently has a 2% advantage against a best in class industry peer, Wizz

Air and an 8% seat density advantage vs. a selection of its short haul peers. When

compared against the global industry average (Fig.40), the extent of Ryanair’s

advantage is clear, with a 20% seat density differential. We see this seat density

differential as placing Ryanair at a structural advantage in terms of maintaining its

industry leading unit cost position.

Figure 40:Seat density vs. peers Figure 41: Staying ahead of the curve - industry seat density trends

Source: Innovata, SeatGuru Source: Airbus, SeatGuru

100110120130140150160170180190200

120

140

160

180

200

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Current Ryanair Average (189 seats)

Current industry average (157 seats)

Ryanair seat density:

- 20% above the industry

- 8% above peers

- 2% above best in class Wizz Air

Page 27 | 03 March 2015| Ryanair

Greater seat density

Boeing’s MAX aircraft provides prospective airlines with a 200 seat configuration,

while the NEO offers a maximum seat layout of 189. Ryanair’s proposed 197 seat

configuration for the MAX would offer an additional 8 seats per aircraft representing

an increase of 4.2% in seat capacity vs. the carriers’ industry leading B737-800NG

configuration. Meanwhile, A320NEO recipients look set to configure aircraft with

186 seats, an increase of 3.3% vs. the current in service A320CEO jets. Assuming

configurations remain as indicated we see the potential for Ryanair to widen the

relative seat density gap vs. the competition as it introduces the MAX in FY20.

Table 10: Maximum manufacturer specifications vs. forecast configurations

Maximum seat configuration Forecasted seat configuration

A320CEO /NEO

B737NG/ MAX200

Est LCC peers Ryanair

Current generation technology 180 189 Current generation technology 180 189

Next generation technology 189 200 Next generation technology 186 197

Potential upside 5% 6% Potential upside 3% 4%

Source: Company presentations, Investec Securities estimates

Better fuel efficiency

The emergence of the NEO and MAX, iterations of the long standing 737 and A320

families, offers approximately 20% fuel burn savings to prospective purchasers.

Ryanair stands to decrease its fuel burn per seat by 18% with the arrival of the MAX

in FY20. While competitors are re-fleeting and deriving similar benefits, we see

scope for Ryanair to widen its unit cost gap vs. NEO customers by an estimated

1.1% delta in structural payload efficiency.

Table 17: NEO and MAX customer snapshot

Airbus NEO Boeing MAX

British Airways Ryanair

Easyjet Norwegian

Lufthansa Icelandair

Norwegian Monarch

Swiss Southwest

SAS American

Vueling Westjet

Wizz Air Canada Source: Ascend

Page 28 | 03 March 2015| Ryanair

Ryanair and the industry to benefit from next generation technology

In FY15E, fuel will represent 44% of Ryanair’s operating cost - 13% above that of

the industry average. The arrival of the MAX should offer Ryanair 18% fuel burn per

seat savings vs. its current 737-800NG, offering a projected fuel savings of €51m

upon introduction.

Table 18: Ryanair’s MAX fuel efficiency forecast

737-800NG MAX200

Seats 189 197

Fuel burn/seat - -18%

2020E Fuel cost - €2,277.6

Relative MAX fleet composition - 38%

Projected fuel saving (m) €51

Source: Investec Securities estimates

Weight is the key to fuel efficiency

As both the NEO and MAX are yet to enter service, we are reliant on marketing

material from both manufacturers for the relative benefits of each unit. In assessing

whether any competitive advantage is to be derived from choosing the NEO over

the MAX, or vice versa, one must return to the overriding principal in the

determinant of fuel efficiency - weight.

Aircraft suffer a performance penalty in terms of fuel efficiency for every pound (lb)

of weight they have to lift. The majority of this weight is unavoidable as it is tied to

making flight possible (airframes, engines etc.). Weight over and above this can be

used for revenue generation by means of transporting passengers and freight. This

extra weight – the payload - is paid for by passengers. The structural payload is the

carrying capacity of the aircraft. It is calculated by taking the Operating Empty

Weight (OEW) from the Zero Fuel Weight (ZFW).

We measure the percentage of structural payload utilised by both the Airbus

A320CEO and the Boeing 737-800NG using seat configurations employed by the

best in class LCC peers and those of Ryanair. We then assess this differential vs.

the maximum specifications of the next generation technology, namely the 189 seat

layout for the NEO and 200 seat layout for the MAX. Finally, we evaluate the seat

configurations that are being indicated for the first wave of next generation

deliveries with 186 seats for the NEO and 197 for Ryanair’s MAX200 cabin. Taking

an average weight of 210lb per passenger plus checked and hand luggage, we

assess the relative percentage of payload utilised.

Table 1911: A320 CEO and B737-800NG structural payload comparison (lb)

LCC peers Ryanair Variance

Aircraft A320 CEO B737-800NG

Seats 180 189

ZFW 137,789 136,000

OEW 93,476 91,300

Structural Payload 44,313 44,700

210lb per passenger / baggage 37,800 39,690

Payload utilised 85.3% 88.8% 3.5%

Source: Ascend, Investec Securities estimates

New engine technology with the MAX to

reduce fuel burn / seat by 18%

The structural payload weight is the

revenue carrying capacity of an aircraft.

The percentage of payload utilised

highlights relative efficiency.

Page 29 | 03 March 2015| Ryanair

Table 20: A320 NEO and MAX200 payload comparison (full density) Table 21: A320 NEO and MAX200 payload comparison (Est density)

LCC peers Ryanair Variance

Aircraft A320 NEO B737MAX

Seats 189 200

ZFW 141,789 140,000

OEW 97,476 95,300

Structural Payload 44,313 44,700

210lb per passenger/ baggage 39,690 42,000

Payload utilised 89.6% 94.0% 4.4%

LCC peers Ryanair Variance

Aircraft A320 NEO B737MAX

Seats 186 197

ZFW 141,789 140,000

OEW 97,476 95,300

Structural Payload 44,313 44,700

210lb per passenger/ baggage 39,060 41,370

Payload utilised 88.1% 92.6% 4.4%

Source: Ascend, Investec Securities estimates Source: Ascend, Investec Securities estimates

Ryanair’s relative fuel efficiency differential is set to widen

Based on our estimates the NEO is using 88.1% of its structural payload. In

contrast, the MAX uses 92.6% of its structural payload for passenger transport.

Conceivably excess capacity could be used to transport freight, however, the LCC

model strays away from freight transport. We forecast the payload use gap to widen

by 1.1% to 4.4% when comparing the Ryanair configured MAX200 to the 186 seat

NEO configuration. In our view, this positive delta underscores Ryanair’s fuel

efficiency advantage and, in our view, provides scope to drive the gap wider.

Ownership costs to remain best in class

We believe that Ryanair’s current order book preserves the carrier’s industry

leading ownership cost differential. Ryanair currently has a 23% unit cost per seat

advantage in ownership costs. Given Ryanair’s order book was secured at above

industry average discounts we see this gap widening by 2%. Furthermore, we see

Ryanair generating €519m from the disposal of some 140 737-800NG units as part

of its fleet rollover program targeting an average fleet age of ca. 6yrs.

Ownership costs, leading the charge

Ownership costs comprise maintenance, aircraft hire and depreciation. Depreciation

of aircraft represents 62% of Ryanair’s FY15E ownership costs, it is through this line

item that we estimate Ryanair will widen its cost differential by 6% vs. peers.

Figure 42:Ryanair has a 23% advantage in unit ownership costs Figure 43: GDP projections and major Ryanair aircraft orders

Source: Company reports Source: Company reports, OECD

Ryanair has an impressive track record in both the timing and negotiating of its

aircraft orders. We estimate that the airline has secured above industry average

discounts from manufacturers, lowering its book value per aircraft. We estimate that

on a BV per seat basis, Ryanair’s most recent 180 737-800NG order delivers a 35%

delta vs. the average of peer Airbus A320 CEO orders. We estimate the BV per

seat gap as being secured and widening by 6%, driven by a 14% differential when

comparing the MAX orders vs. the average of peers’ NEO orders.

€0

€2

€4

€6

€8

€10

€12

€14

€16

€18

Ryanair Easyjet Wizz Vueling -1%

0%

1%

2%

3%

4%

5%

6% 2002 Boeing contract 737NG order MAX order

Ryanair fuel efficiency:

4% per seat ahead of rivals

Scope for gap to widen

Ryanair has a 23% unit cost per seat

ownership cost advantage.

A 5% lower book value per seat drives

ownership cost savings

Page 30 | 03 March 2015| Ryanair

Table 22: Ownership cost delta as carriers transfer to the next generation of aircraft

Operator Aircraft Variant Seats Unit price BV/seat Delta Operator Aircraft Variant Seats Unit price BV/seat Delta

Est. LCC peer average Airbus A320 CEO 180 $40.0m $0.22m

Est. LCC peer average Airbus NEO 186 $45.0m $0.24m

Ryanair Boeing 737-800NG 189 $31.0m $0.16m -35% Ryanair MAX200 197 $41.0m $0.21m -14%

Source: Investec Securities estimates

In table 22 above we have summarised our estimates on delivery prices for both

Ryanair’s oldest B737-800NG and its MAX200 aircraft vs. an average A320CEO

and A320 NEO of its LCC competitors. Our estimates are based on market

commentary and observed tranactions at the time of aircraft delivery.

Maintenance and aircraft hire capped by industry leading order book

Ryanair’s order book is the largest of its peer group, representing 50% of the total

group backlog. We see this as tangible as it:

Reduces Ryanair’s future requirements for aircraft hire vs. peers

Maintains Ryanair’s average fleet age at 6.9 years vs. peers’ at 7.9 by FY24

Figure 44: Ryanair’s order book vs. peers, aircraft units

Source: Ascend, Investec Securities estimates

Maintenance related charges, at 16% of Ryanair’s ownership costs are highly

correlated to aircraft age. With Ryanair guiding average fleet age relatively flat out

to FY24 (moving from 5.4 years to 6.9 years between FY15-FY24) we forecast

maintenance charges will remain relatively stable. In contrast, we forecast a gradual

ageing of LCC peers’ fleets from a FY15 starting point of 4.4 years to a FY24

average age of 7.9 years).

Figure 45: Average fleet age of current LCC peer group Figure 46: Forecasted average fleet age of select LCC peer group

Source: Ascend Source: Ascend, Investec Securities estimates

0

10

20

30

40

50

60

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Easyjet Wizzair Vueling Ryanair

4.0

5.4

6.4

7.4

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Wizz Ryanair Easyjet Vueling

3

4

5

6

7

8

9

10 Norwegian Ryanair Wizz Air

Easyjet Peer Average

Ryanair’s delivery pipeline represents 50%

of its immediate peer’s backlog

Page 31 | 03 March 2015| Ryanair

Capturing more revenue

The MAX offers Ryanair clear revenue upside with increased range bringing new

markets and primary airports into scope. With 8 extra seats vs. the current

generation of Boeing jets, we forecast 4% revenue per aircraft uplift with the advent

of the MAX. We estimate that the additional seats, when fully in place by FY24, will

generate €128m in additional EBIT, which when discounted by our WACC of 8.5%

implies a present value per share of €0.09.

Table 23: MAX capacity provides revenue opportunity, €

737-800NG MAX200 Variance

Flights/Day 5 5 0

Seats 189 197 8

Seats/Day 945 985 40

Seats/Year 344,925 359,525 14,600

Passengers (target LF 91%) 13,360

Average fare

€60

Additional revenue per aircraft

€804,005

Number of MAX aircraft

200

Total additional MAX revenue, €m

€160.8m

Additional EBIT (80% drop through) €128.6m

PV per share, € cent

€0.09

Source: Investec Securities estimates

MAX to drive increased revenue per

aircraft equating to a PV/share of €0.09

Page 32 | 03 March 2015| Ryanair

Ryanair’s fleet renewal, a solid cost base with aftermarket profit potential

We highlight our fleet evolution projections for Ryanair in table 24 below. Not only

does this fleet evolution profile drive reduced ownership costs but it highlights the

exit of some 160 737-800NG units through FY24. We see this as significant in both

size and scope and we detail below how we believe Ryanair could benefit from

€519m in profit with a PV of €0.37 / share through disposal of aircraft.

Table 24: Fleet renewal program highlights a profitable opportunity

Fleet Evolution FY15E FY16E FY17E FY18E FY19E FY20E FY21E FY22E FY23E FY24E

Beginning year fleet 300 308 342 370 402 420 474 483 497 512

Deliveries -737-800NG 11 40 50 50 29 0 0 0 0 0

Deliveries - 737MAX200 0 0 0 0 0 62 34 42 40 22

Returns/Disposals -3 -6 -22 -18 -11 -8 -25 -28 -25 -14

Year End Fleet 308 342 370 402 420 474 483 497 512 520

- 737-800NG 308 342 370 402 420 412 387 359 334 320

- 737MAX200 0 0 0 0 0 62 96 138 178 200

Average fleet age (yrs.) 6.5 6.6 6.2 6.1 6.4 6.2 6.0 6.1 6.3 6.9

Source: Investec Securities estimates

Extracting value from the aftermarket

With an upcoming fleet rollover program we believe that Ryanair is set make further

gains from its order book. Between Mar’99 and Mar’13 Ryanair took delivery of 348

B737-800NG (NG) aircraft and exited 43 units (26 disposals and 17 lease hand

backs). We estimate that the period FY15-FY24 will see the company exit 160 NG

aircraft with 20 lease hand backs. We take our estimated BV of Ryanir’s oldest NG

units and benchmark this against observed half-life market values for 12 year old

units to arrive at a potential gain on disposal.

Table 25: Ryanair stands to materially benefit from its fleet rollover program, millions

B737-800NG list price $81.00

Assumed Ryanair discount of 62% $50.22

Estimated unit price $30.78

Book Value (BV) $30.78

Residual Value (RV) 15% $4.62

Depreciation per annum $1.14

(Straight line over 23yrs to RV)

12yr old Ryanair 737-800NG BV $17.13

12yr old 737-800NG Half-Life Market Value (MV) $22.00

Gain on disposal $4.87