Embed Size (px)

Citation preview

BUSINESS DOCUMENTS

Stages of Financial Recording

Business Documents Sequence

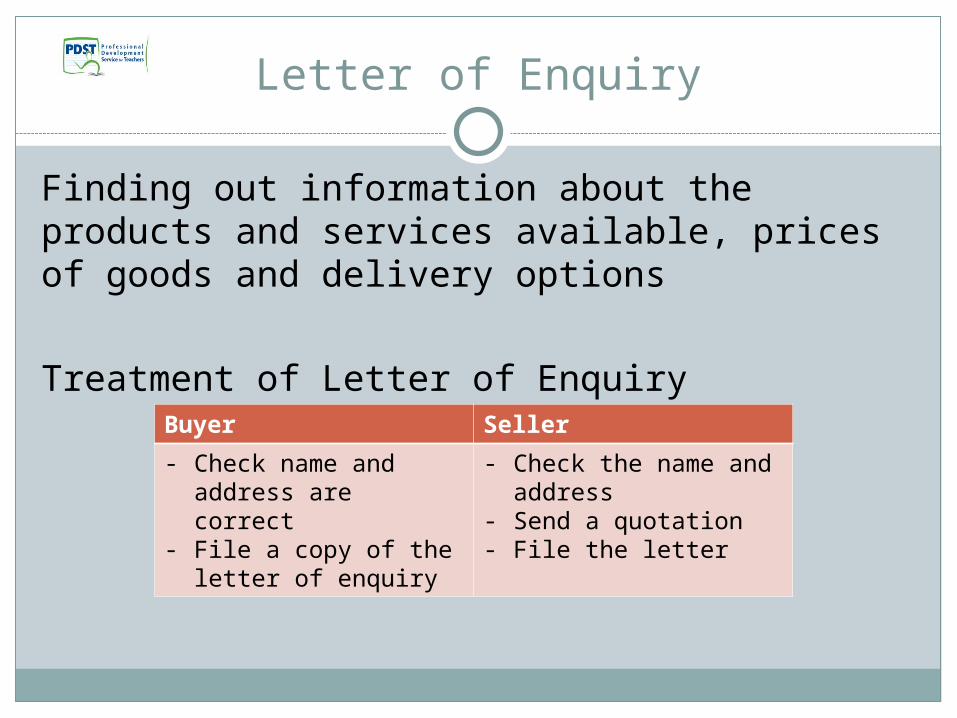

Letter of Enquiry

Finding out information about the products and services available, prices of goods and delivery options

Treatment of Letter of EnquiryBuyer Seller

- Check name and address are correct

- File a copy of the letter of enquiry

- Check the name and address

- Send a quotation- File the letter

Quotation

It is sent based on the letter of enquiry giving information of the goods available, price and any discounts and delivery options

Treatment of Quotation

Buyer Seller

- Compare all the quotations for the best deal

- File the quotation

- Check name and address are accurate

- File a copy of the quotation sent

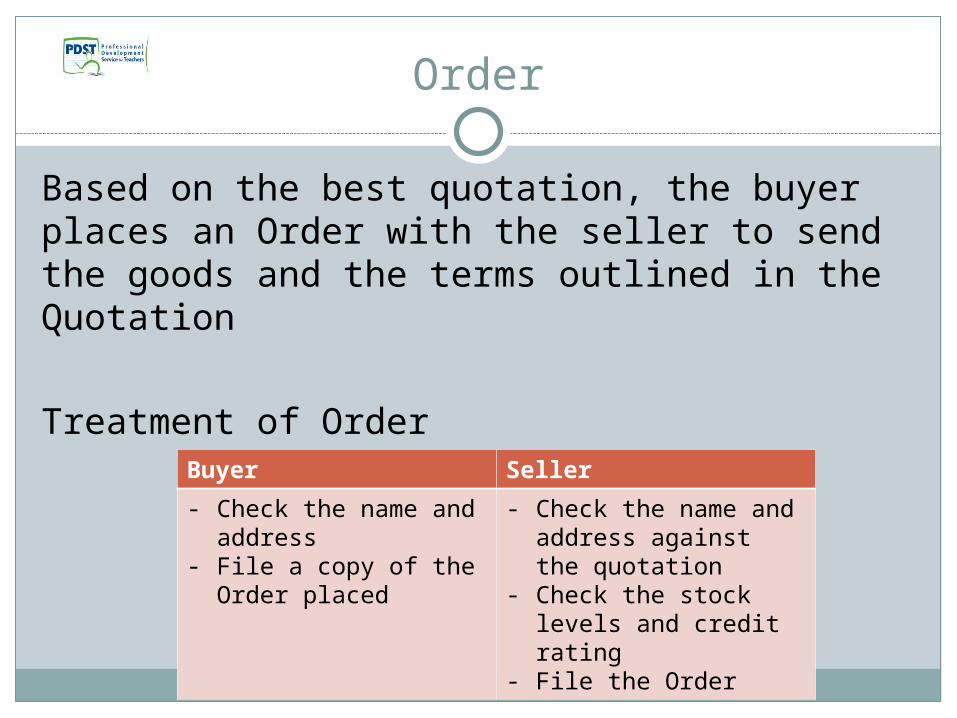

Order

Based on the best quotation, the buyer places an Order with the seller to send the goods and the terms outlined in the Quotation

Treatment of Order

Buyer Seller

- Check the name and address

- File a copy of the Order placed

- Check the name and address against the quotation

- Check the stock levels and credit rating

- File the Order

Delivery Docket

This document provides proof that the goods were delivered and have them checked before signing the docket

Treatment of Delivery Docket

Buyer Seller

- Check the name and address

- Check that they are the correct goods ordered

- File a the delivery docket

- Check the name and address

- Check the details according to the order

- File a copy of the delivery docket

Invoice

Sent by the Seller outlining the quantity, description and price of the goods and any discount which has been offered.

Treatment of Invoice

Buyer Seller

- Check the name and address are correct

- Check that they are the correct goods as per order

- Check the calculations

- File the invoice

- Check the name and address

- Check the details are correct

- Check the calculations

- File a copy

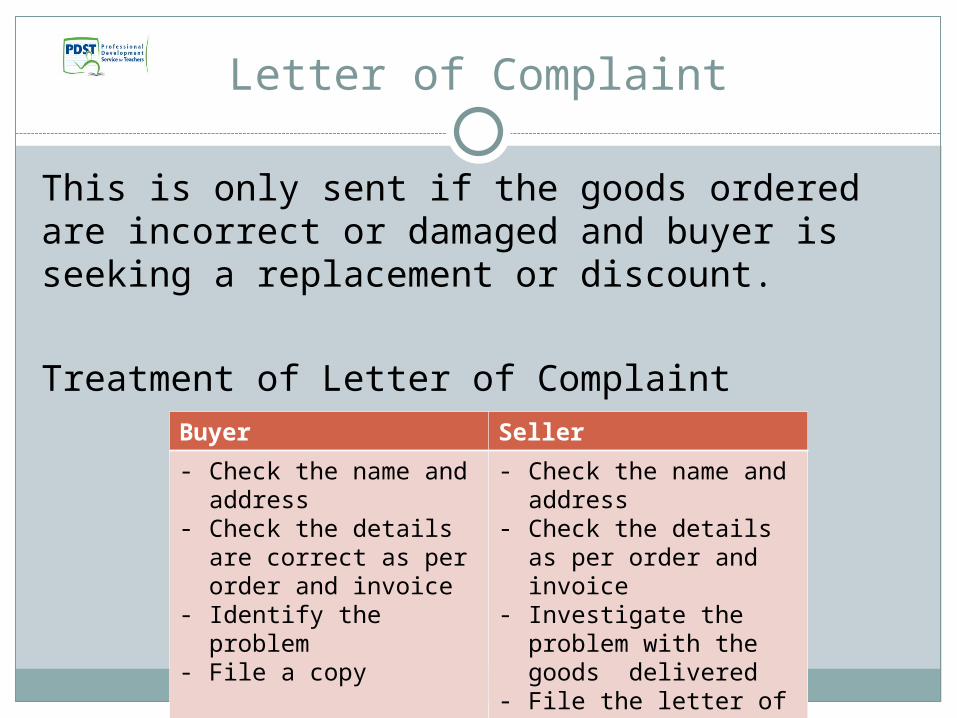

Letter of Complaint

This is only sent if the goods ordered are incorrect or damaged and buyer is seeking a replacement or discount.

Treatment of Letter of ComplaintBuyer Seller

- Check the name and address

- Check the details are correct as per order and invoice

- Identify the problem - File a copy

- Check the name and address

- Check the details as per order and invoice

- Investigate the problem with the goods delivered

- File the letter of complaint

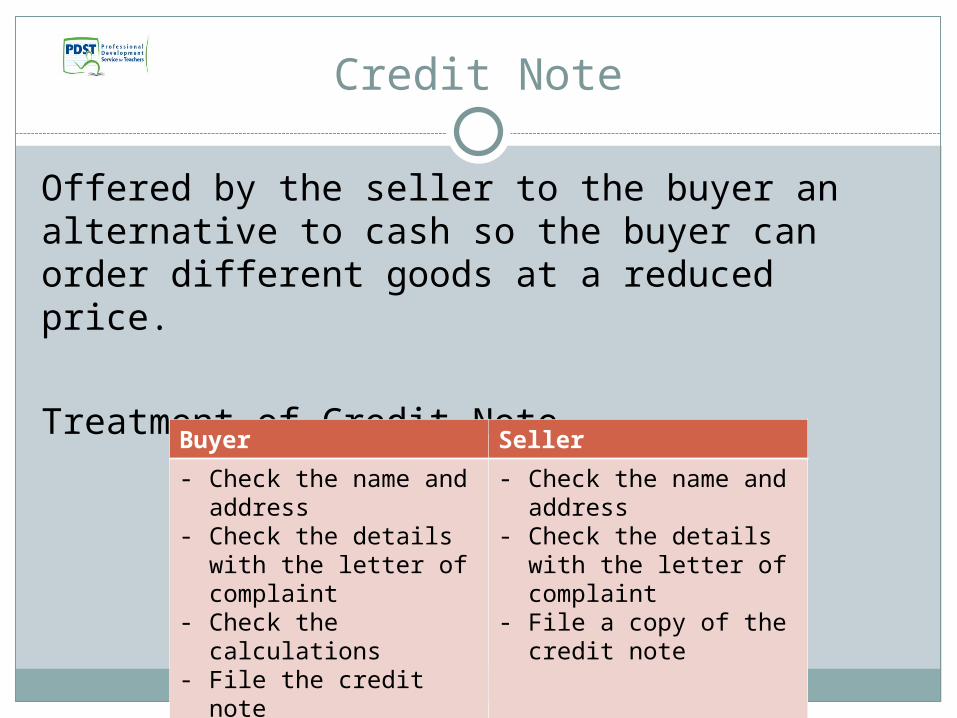

Credit Note

Offered by the seller to the buyer an alternative to cash so the buyer can order different goods at a reduced price.

Treatment of Credit Note

Buyer Seller

- Check the name and address

- Check the details with the letter of complaint

- Check the calculations

- File the credit note

- Check the name and address

- Check the details with the letter of complaint

- File a copy of the credit note

Statement of Account

The seller issues this to the buyer at the end of the month outlining the transactions that have taken place and the money owed.

Treatment of Statement of AccountBuyer Seller

- Check the name and address

- Check the calculations

- File the statement

- Check the name and address

- Check the calculations

- File a copy of the statement of account

Cheque

Payment made by the buyer to the seller for goods purchased on the amount owing.

Treatment of Cheque

Buyer Seller

- Complete the cheque correctly and counterfoil

- Check the name and amount is correct

- Check the details are correct on the cheque

Receipt

A receipt is proof of purchase by the buyer and that the goods were paid for.

Treatment of Receipt

Buyer Seller

- Check the details are correct on the receipt

- File the receipt

- Complete the receipt- Check the name and

the amount is correct

Mark – up Formula

Profit x 100% Cost Price 1

An item costing €40 is sold for €55. Calculate the mark-up?

€15 x 100 % €40 1

= 37.5%

Margin Formula

Profit x 100 %Selling Price 1

Cost price €40 and the selling price is €50. Calculate the profit margin.

€10 x 100 % €50 1 = 20%

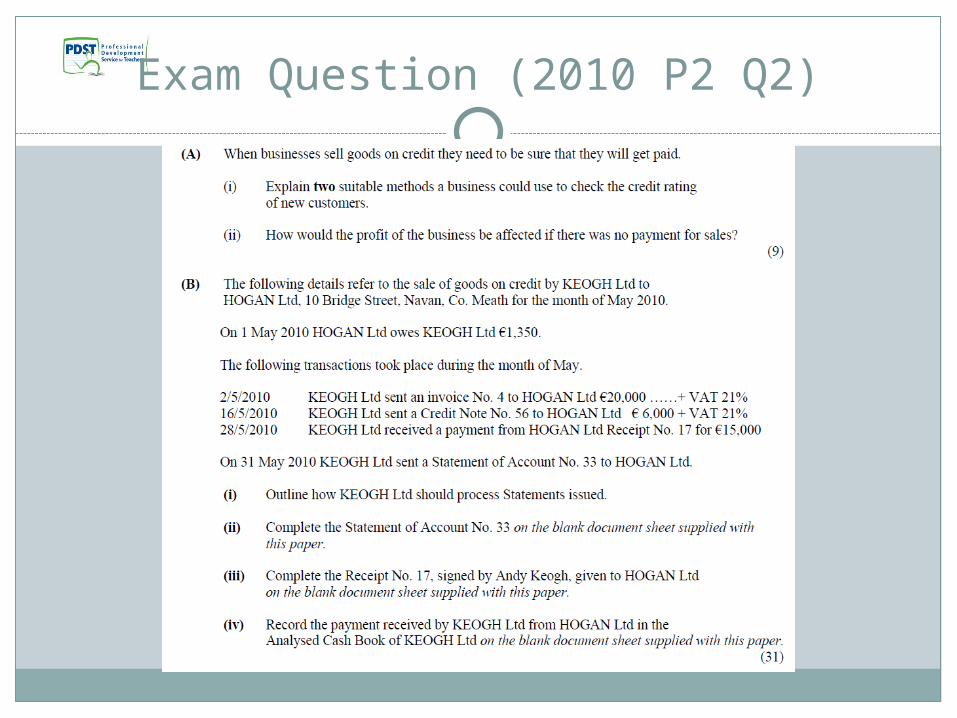

Exam Question (2010 P2 Q2)