Embed Size (px)

Citation preview

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

1

FINAL REPORT

CONSULTANCY SERVICES FOR BUSINESS DEVELOPMENT SERVICES (BDS) MARKET

DIAGNOSTIC IN RWANDA

CONDUCTED BY:

SUBMITTED TO:

EAST AFRICA DAIRY DEVELOPMENT (EADD) PROJECT

JANUARY 2009

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

2

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

3

CONTENTS

Background and introduction 3

Methodology and activities 3

Preplanning 4

Training 5

Field work 5

Sampling 6

Key challenges of fieldwork 7

Data processing 7

Presentations 8

Key conclusions of the methodology 8

Findings of fieldwork and data analysis 9

CONSUMER SURVEY by location 9

Locations covered and key informants interviewed 9

Targeted SME consumers interviewed 9

Market profiles 11

Key demand side constraints and opportunities 25

Business development services that address those constraints and opportunities 26

Specific policy constraints that are affecting MSE product markets 28

SUPPLIER DIAGNOSTIC by location 29

Existing providers/ services and their locations 29

A workable data base of the BDS actors 30

BDS suppliers interviewed 30

Types of services and price of services, how providers cover costs, profitability, existing contractual arrangements and promotional/marketing strategies

31

Capacity gaps of interviewed suppliers 34

Priority supply side constraints, market failures, and market opportunities 34

Comparison of interviewed suppliers 36

The enabling environment for BDS 37

Conclusions 38

Characteristics of the market for BDS in each specific region in relation to existing supply, demand and transactions

38

An insight into the potential of each target market location 39

Level of market distortion 40

Comparative information on the in-country sites and the 3 markets 41

Recommendations 42

Other current or proposed dairy sector interventions 42

Sustainable solutions to address priority market constraints and market failures 42

Illustrative market based interventions 51

Approaches and methodologies 55

Strategies which ensure effectiveness and efficiency 56

Strategies which ensure sustainability 59

Suggested BDS providers/delivery channels to target for future interventions 62

Selecting appropriate BDS providers 63

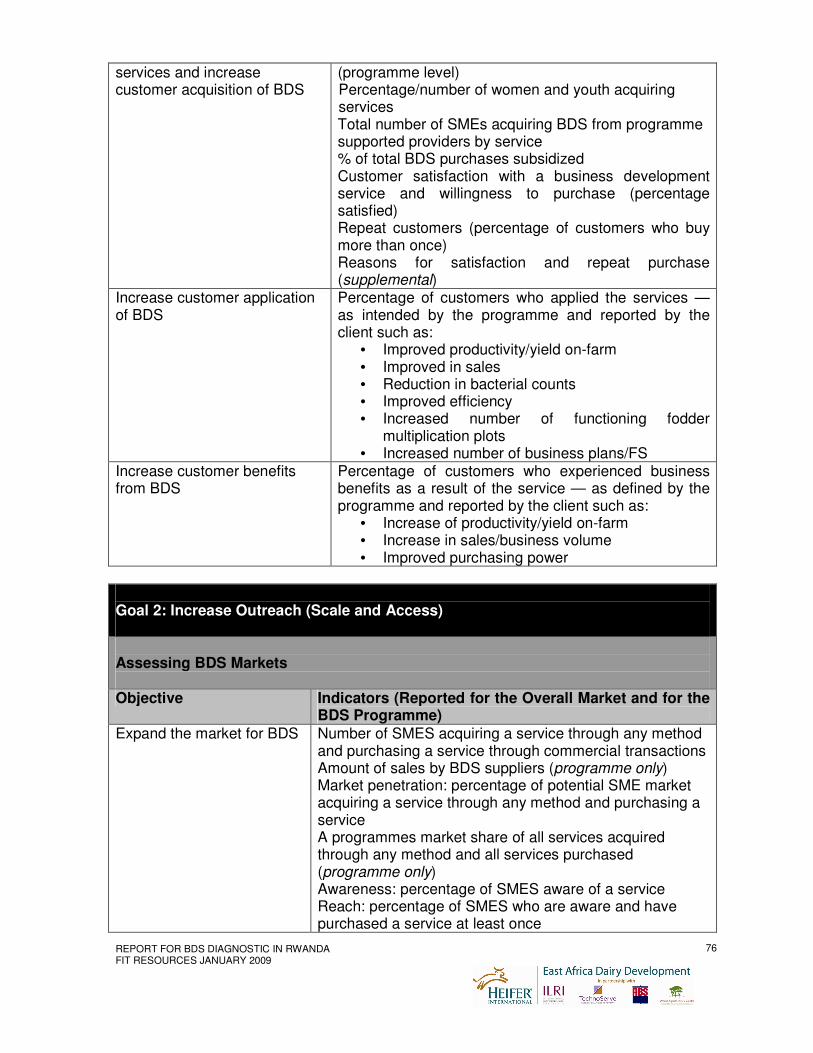

BDS performance measurements at the BDS market level 63

Annexes 67

Database of SME actors including persons interviewed

Database of BDS suppliers including persons interviewed

Database of targeted suppliers

Itinerary

FIT/RI scope of work

Final instruments

Data collected

BDS training report

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

4

Researcher training report

Background and Introduction

In a bid to improve life through poverty reduction, a consortium of organisations comprising of Heifer International as lead, TechnoServe Inc, ILRI, ABS-TCM and ICRAF launched a 4 year program dubbed EADD (East Africa Dairy Development) funded by Bill and Melinda Gates Foundation. The programme aims to move smallholder farmers out of poverty by delivering farmer-focused, value-chain activities that are implemented simultaneously to stimulate dairy farm production, dairy-sector services, business development and dairy market pull. The vision of success for the EADD is that the lives of 179,000 families—or approximately one million people—are transformed by doubling household dairy income by 2018 through integrated interventions in dairy production, market-access and knowledge application. The consortium deemed it important to carry out a market assessment to understand the characteristics of the BDS markets in relation to existing supply, demand and transactions in the dairy sectors in some key sites in Kenya, Uganda and Rwanda. The information would:

• Provide an insight into the potential of each market

• Clarify opportunities for interventions

• Define broad strategic approaches FIT Resources Kenya (FIT) in collaboration with Research International East Africa Ltd (RIEAL) were contracted to coordinate the market diagnostic in key locations in Kenya. The findings and recommendations of this consultancy will contribute to the market focused, sub sector approach of the EADD aimed at improving the functioning of BDS markets. The final scope of work is attached to this report (Annexes/Final Revised SOW). FIT Resources act as the lead agency and contract holder, to provide strategic leadership in devising and conducting the business development service consumer research and supplier diagnostic. Research International conduct the field work as a sub contractor, to collect primary and secondary qualitative and quantitative information, analyse, process and present the data. Methodology and activities To achieve the above results the following activities were agreed on:

• Preplanning (planning meetings, research boundaries on the basis of project resources, existing sub sector information, market assessment goal/ objectives/research hypothesis, developing and testing the tools, screening interviewers, target locations in each country, preliminary key informants, other current or proposed interventions)

• Training (training of EADD staff, field research teams and BDS training workshop)

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

5

• Field work (target groups, sample size, areas covered, team structure, consumer survey and supplier diagnostic)

• Data processing (developing the data base of BDS actors, profiling the markets, choose priority constraints, identifying and scoping out sustainable solutions, defining ‘illustrative’ market based interventions and strategies, suggest appropriate BDS providers, establishing comparative information, identifying BDS performance measurements)

• Presentations (stakeholder workshops and final presentation) Preplanning

Relevant background information was sourced via a series of planning meeting with Technoserve and EADD consortium members. Meeting presentations and minutes are attached to this report (Annexes/Process meetings). These meetings also included setting the research boundaries on the basis of project resources, preliminary selection of target locations and the agreed definition of ‘small holder farmer’. The market assessment goal, objectives and research hypothesis were agreed as follows: The market assessment goal is: To understand the characteristics of the BDS markets in relation to existing supply, demand and transactions in key sites in Rwanda. The market assessment objectives are:

• To provide an insight into the potential of each market • To clarify opportunities for interventions • To define broad strategic approaches

The research hypothesis is: If current BDS market dynamics are better understood then strategic approaches and interventions can be devised to develop BDS markets in a sustainable manner and benefit SMEs. It was agreed that the FIT/RI team would build capacity of the project staff to undertake future market assessments during the life of the project. Due to budget constraints a targeted number of sites were discussed that affords the best opportunities to kick-off the project and generate some ‘quick wins’. A training itinerary was also agreed upon to capacitate EADD project staff in BDS and research skills. FIT Resources provided lead for the overall assignment and liaison with Technoserve and the country offices on all the pre planning activities. FIT Resources coordinated the field preparation with Research International and Technoserve including: tool development and testing, researcher selection and training and itinerary development. Different tools were developed to cover the demand (consumer) side and supply (supplier) side of the market. The final instruments and itinerary are attached to this report (Annexes/Final Instruments). The following activities were undertaken prior to the commencement of fieldwork: screening of team members, preparation and translation of questionnaires and preparation of reporting tools and manuals. Research International personnel met field staff/counterparts and finalised the selection of target locations and identification of key informants in each country. Research International finalised the training of field researchers including EADD project staff and preparations for field research.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

6

No secondary information was used as the project is building on a baseline survey and existing value chain assessments in each country. The comprehensive examination of targeted BDS markets and value chains will assist EADD in designing systemic solutions to key market problems. The two subsystems—BDS markets and value chains—are complementary components of the larger market system into which MSEs must integrate.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

7

Training

1. BDS training workshop - FIT Resources personnel implemented an indepth EADD

staff stakeholder training in Uganda (to include Uganda and Rwanda stakeholders). This 2 day formal training in diagnostic skills covered the principles and practices of BDS, BDS market development, BDS market assessment and BDS market development programme design and performance measurement. The aim of this training was to capacitate project staff and provide stakeholders with a contextual framework for the research. The workshop presentations, training materials and training reports are attached (Annexes/BDS Training).

2. Training of field research teams - teams including Technoserve and consortium

member staff, were subject to an in country briefing session prior to fieldwork commencement. The training sessions covered methodology of the assessment stages, sampling, tools and stimulus methods to use with market players and how to complete reporting formats. The aim of this training was to capacitate project staff to engage in further market diagnostics beyond the life of this collaboration. The workshop presentation and training reports are attached (Annexes/Research Training).

Field work

In order to complete this assignment within the defined period, a large teams of interviewers, team-leaders and supervisors were assigned. Team members were recruited from the RIEAL regional offices, according to specifications based on experience and qualifications. The RIEAL Principle Researcher and a field coordinator coordinated the research at all stages, and focused on ensuring that outputs were planned in advance so time-schedules were met. They worked alongside the RIEAL existing field management structure that forms the line management for the field departments. Daily reporting of results and activities from each team was channeled back through this central management team. Research International led and implemented the field research in collaboration with EADD project staff. Consultations and market observation were undertaken during the fieldwork which included visiting identified target locations plus identifying and holding interviews with key informants and targeted dairy sector stakeholders relevant to the selected sites. Consumer survey - Consumer research was implemented with a selection of consumers from the core market itself with a focus on farmers and chilling plant stakeholders. However the definition regarding ‘small holder farmer’ was reviewed and altered during a process meeting and the ceiling lifted of the number of cows as many farmers in Uganda and Rwanda are large compared to Kenya’s extensive small holder population. Constraints and opportunities were then identified in the areas of market access, input supply, technology/product development, management and organisation, policy, finance and infrastructure. The size and strength of the market in each specific area of the country for those services was estimated broadly plus key sub sector constraints, market failures and market opportunities defined from the demand side. Key business development services were identified that address the specific constraints and opportunities.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

8

Supplier diagnostic - Based on the identified priority services, relevant suppliers were identified and a supplier survey implemented with service providers from the support markets to determine who is supplying BDS and how. Constraints, market failures and opportunities were then determined from the supply side. A comparison of suppliers was also undertaken and the level of market distortion anticipated. Stakeholders from the business environment such as local authorities, regulators/policy makers were contacted as required to provide an overview of the business environment. The BDS Market Assessment Survey took place in Rwanda from 14th - 25th November, 2008. The area of coverage of the survey research was Nyagatare and Gatsibo Districts covering the following sectors and sampling points:

Nyagatare BMN

Nyagatare Mbare

Gatsibo

• Bushoga • Karangazi • Kiramuruzi

• Tabagwe

New sites not included will be covered by Technoserve staff beyond the life of this consultancy. Sampling

� The sample included 316 interviews spread across the 3 sites. � 302 farmers were interviewed. � As per the briefing instructions, the teams covered a 20KM radius from the location

of the chilling plant. Depending on the number of locations located within the 20 KM radius, an equal number of sampling points were picked in each location to ensure spread of interviews.

� For each location, the team leader picked the starting point randomly, and using the random route method, farmers who fitted the set criteria were interviewed: Selection criteria included:

• Dairy farmer • Have mature milking cows

� Interviews were conducted on farmers who possessed up to 20 cows either being milked or dry currently. There was a shift from the earlier limit of 5 cows due to the widespread ownership of traditional cows in the region. Again it was also realized that even when farmers owned vast herds here, their milk production remained low as they keep indigenous cows that produce an average of between 1 and 4 liters each per day.

� The team traveled as one and on reaching the research site (village) members were dispatched in different directions. The left hand rule applied in selecting the dairy farmer to interview starting from a given landmark. This meant that once an interview took place, the interviewer moved 3 households keeping on the left hand side then interviewed the 4th household.

� However, the above rule was only applied where the population was dense and where farms were relatively big (over 10 acres), the skipping was limited to 1 household. At the household, the interviewers first spoke to the adult member of the family, mainly the husband or wife though at some instances, some other family members who were directly responsible for dairy farming gave information.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

9

� In Rwanda, farmers are allocated grazing land by Government in accordance with the size of cattle herd one has. A centralized area is then set aside where people are allowed to build their homes and the farms are located at a considerable distance away from their homes. This state of affairs meant that our interviewers in most cases could not physically see the cows to ascertain some claims by farmers.

� As for suppliers (14 were interviewed), the team picked supplier names from the farmers, other suppliers and also those they came across in the trading centres. From the list, a score was given to each and every supplier based on set criteria (capacity to deliver services, closeness to SMEs e.g. in terms of understanding their culture and geography, commercial focus e.g. level of profitability, focus on services, SMEs or BDS, organizational independence- especially from donor funds, legally registered and willingness/interest/ability to partner). This set of requirements not withstanding, and because of their scarcity, all suppliers listed were sought for interview, although a few could not be found.

Key challenges of the fieldwork

• Late start in Rwanda due to technical hitches and strict protocols e.g. Government requirement of research license

• Accessibility of some sectors o Transport – lack of efficient public transport. Tabagwe Sector is

approximately 20 kilometers away from Nyagatare Township and the only available mode of public transport was motorbikes.

o Rains – the timing of the study coincided with rainy season and this affected the movement.

• Special events – the arrest of a senior Rwanda Government official in Germany and the visit to Gatsibo district by Kenya’s President Kibaki coincided and interrupted fieldwork as farmers were called on to participate in the demonstrations and rallies that were organized by the Government countrywide.

• Few/ uncooperative BDS suppliers. Some of the BDS suppliers were either uncooperative or hard to find. There were very few BDS suppliers of dairy products and services and as such farmers have limited choices.

• Research fatigue – a good number of farmers complained of having participated in other recent agricultural and other types of surveys whose results and benefits they had no idea of.

• Questionnaire duration. Some respondents complained it was taking too long to go through a questionnaire. This was particularly so during the first few days when most of the interviewers took over one and a half hours (90 minutes).

Data processing

Research International processed all the data collected on an ongoing basis. Research International personnel have developed a database of actors (BDS providers in each of the areas under study are listed, categorized by service provision and their location recorded). A further database defines specific provider gaps and capacities including a score against agreed selection criteria for determining target partner providers. A database of the small and micro enterprises (SMEs) interviewed has also been developed. The full data set is attached to this report (Annexes/Databases). To understand the markets, RI examined three key issues - demand, supply and transactions (the interaction between demand and supply) during the market assessment.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

10

The outcome of analyzing this information forms a picture of each BDS market showing how it works, where the opportunities for growth are, and where significant problems lie. Data analysis was undertaken to profile the markets, establish comparative information on the in-country sites and the 3 markets and draw conclusions from the data. A round table meeting was held in early December 08 with stakeholders to overview the methodology and process of data processing and analysis and reach consensus on the priority constraints/opportunities and identify possible solutions. The meeting presentation is attached to this report (Annexes/ Process meetings). Sustainable solutions that address priority supply side and demand side constraints were discussed. Illustrative market based interventions were also developed with a focus on potentially sustainable/profitable services that are replicable in the private sector. Strategies which ensure effectiveness, efficiency and sustainability were also discussed alongside suggested BDS performance measurements. The data processing plan was then circulated for stakeholder feedback during the analysis process and the data plan is attached to this report (Annexes/Process meetings). Comparative information on the in-country sites and 3 BDS markets was also produced. Presentations

FIT Resources and Research International personnel collaboratively implemented a presentation and action planning at a stakeholder workshops in Rwanda with staff, consortium members and key informants on 9th January 09. This workshop included a short training presentation on the basic principles and practices of BDS and the Market Development Paradigm. All the research findings were presented and proposed illustrative solutions and performance measurements discussed. Feedback was recorded and an action plan developed. FIT Resources then prepared this final draft report and will present the final report to Technoserve with support from Research International in Nairobi, Kenya by FIT Resources and Research International on January 30th 2009. Key conclusions of the methodology

• Outsourcing the MA to a research company ensured a more effective and efficient MA process.

• A combination of outsourcing and internal capacity building ensured the best possible results. The likelihood of useful research results was ensured as EADD stayed close to the MA process.

• The ability of EADD staff to remain consistent to the process was questionable. Staff members were not always available for the trainings and meetings as required plus EADD field staff were not available to partner on the field work in some locations drawing into question the long term ability of field staff to implement further diagnostics in new locations.

• Determining a clear hypotheses and outlined MA goal and objectives ensured a more effective delivery of analysed data from Research International.

• The MA focused on a holistic picture of the market and incorporated both sides of the market equation—demand and supply.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

11

Findings of fieldwork and data analysis

CONSUMER SURVEY by location

Locations covered and key informants interviewed

Nyagatare BMN Bushoga Tabagwe

Nyagatare Mbare Karangazi

Gatsibo Kiramuruzi

Targeted SME consumers interviewed The consumer survey in Rwanda covered 302 respondents. The respondents qualified to be interviewed if they were small scale milk producers and specifically for Rwanda if they had less than 20 traditional cows. For every site covered, a minimum of 100 farmers were interviewed. Of the 302 respondents interviewed, 80 percent (243) were males while 20 percent (59) were females. A majority of the male respondents (26%) were aged between 36 – 45 years while for the females the majorities (32%) were aged 46 – 55 years. Only few respondents (4%) were aged between 18 – 25 years and above 64 years. Distribution of Respondents by age BASE=302

% of total sample interviewed

Males 80

Females 20

Most of the farmers practiced mixed farming –crop growing and cattle keeping. Expectedly and as per the recruitment procedure all respondents were dairy farmers. This was followed by food crop farming at 81%. Cash crop farming in the region is insignificant as only 3% of the respondents reported growing cash crop. As per the recruitment procedure all the respondents interviewed were the key decision makers on dairy farming activities. Currently, a majority (88%) of the farmers milk between 1 – 5 cows despite most of them having more than 5 cows. In terms of herds kept, Majority of the farmers in Nyagatare claimed to own more than 5 cows while in Gatsibo the proportion of those who have more than five was small. Farmers in the three sites were found to be keeping mixed breeds. However, a majority of them (84%) keep indigenous breeds. About half of the farmers interviewed also keep cross breeds 46% while those who keep pure breeds are less than 10%. The findings also indicated that Nyagatare-BMN had more pure breeds (14%) compared to Gatsibo and Nyagatare-Mbare where farmers claimed to own 8% and 4% of pure breeds.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

12

TOTAL Nyagatare

Mbare Nyagatare

BMN Gatsibo

BASE: 302 101 100 101

%

Pure breed 9 4 14 8

Cross breed 46 47 54 39

Indigenous 84 88 88 76

On average, farmers with pure breeds reported to produce 17 liters of milk per day while cross breeds produced 8.5 litres per day. Expectedly, the productivity for traditional breeds was reported to be the lowest. In terms of regions, Nyagatare BMN and Mbare farmers produce more milk per day with an average of about 10 litres per day compared to Gatsibo where daily production average was reported to be around 6.6 liters. Expectedly, the amount of milk sold per day on average within the three sites is less than the amount produced as some milk is spared for domestic use. The table below indicated the average amount of milk sold by farmers:

District Average liters produced per day per farm

Average liters sold per day

Difference (unsold milk - liters)

Nyagatare-Mbare 9.5 6.7 2.8 Gatsibo 6.6 5.5 1.1 Nyagatare-BMN 10.1 7.3 2.8

Across the three sites covered in the research, most of the farms were between 1 – 5 acres in size.

Market profiles

Awareness and affordability of services/ inputs When respondents were asked the dairy inputs/ services they are aware of, AI, mineral supplements, vet treatment services and veterinary vaccination were mentioned by more than 90% of the farmers. Other inputs that were mentioned by more than 60% of the respondents include insecticide and tick sprays and supplementary feeds. However, despite AI ranking as the service majority of the farmers were aware of (98%), complete familiarity of its benefit was rated below average. Across all services/ inputs in totality, farmers were least aware of chaff cutters and hay balers. Expectedly, almost all farmers were not familiar with the benefit of the two farm equipments. In terms of affordability, of the 7 top most inputs/ services that farmer were aware of, supplementary feeds, veterinary vaccination and AI were rated as highly unaffordable to farmers. The table below summarises some key inputs/ services that farmers are aware of

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

13

in regard to familiarity with the benefits, availability, affordability and most important overall.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

14

On enquiring from the farmers the services/ inputs they have purchased or received in the past for their dairy animals, supplementary feeds and disinfectants were ranked lowest among the 7 top services farmers were aware of as shown in the figure below. However, farmers expressed concerns on the adequacy of most inputs/ services that they have received in the past 12 months. In terms of services/ inputs that were being used nowadays, only three performed averagely and above. These were mineral supplements 77%, insecticide and tick sprays 66% and veterinary treatment services 52%.

47

58

63

84

91

93

96

98

23

46

84

63

80

84

24

59

21

47

30

79

84

71

92

70

Aware

Completely familiar with benefit of Easily available

Information/training on animal husbandry

Disinfectants for Cleaning

Supplementary feeds

Insecticide and Tick sprays

Veterinary vaccination

Vet Treatment Services

Mineral supplements

Artificial Insemination (AI)

80

84

74

89

87

82

87

84

Very strongly needed

37

31

56

26

54

29

16

34

Most important overall

Not affordable even after saving up

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

15

Services/inputs ever purchased or received Generally, the 3 markets do not indicate any significant differentials in the demand for services and inputs purchased or received. However, some slight differences were noted in Nyagatare (BMN & Mbare) where almost all farmers claimed to have vaccinated their animals and in Nyagatare Mbare where AI services were claimed to have been used by over 80% of the farmers. This may mean that the drive to transform herds from indigenous to cross breeds is at a higher level in Nyagatare which conforms to the breeds kept.

Services/Inputs ever purchased or received TOTAL

Nyagatare Mbare Gatsibo

Nyagatare BMN

BASE: Total Sample 302 101 101 100 %

Artificial Insemination (AI) 77 83 72 77 Veterinary treatment services 80 82 82 76 Veterinary vaccination 91 88 87 97 Supplementary feeds 34 33 38 31 Mineral supplements 94 96 99 87 Disinfectants - for cleaning and sterilizing 46 51 44 43

Insecticides & tick sprays 84 76 89 87 Although some farmers observed that through savings, they could purchase some of the services or inputs, milk coolers, supplementary feeds and veterinary vaccination were perceived to be out of reach by a majority. Those who said services/ inputs were not

47

58

63

84

91

93

96

98

7

46

34

84

91

80

94

77

Aware

1

33

12

66

48

52

77

40

67

39

71

37

23

45

30

52

Used nowadays Ever purchased

Inadequate amount

Purchased in P12M

Information/training on animal husbandry

Disinfectants for Cleaning

Supplementary feeds

Insecticide and Tick sprays

Veterinary vaccination

Vet Treatment Services

Mineral supplements

Artificial Insemination (AI)

4

45

24

82

82

74

92

62

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

16

affordable were asked why they thought so. The following table provides a breakdown of some of the reasons advanced (sample: all who said not affordable):

Service/ product Total sample

So expensive could never

consider using

May be able to use if saves

up %

Artificial Insemination (AI) 79 34 66 Veterinary treatment services 104 29 71

Veterinary vaccination 57 54 46 Supplementary feeds 140 56 44 Mineral supplements 90 16 84 Disinfectants - for cleaning and sterilizing

85 31 69

Insecticides & tick sprays 126 26 74 Seeds to grow fodder 82 46 54

Milk testing kits 90 44 56 Hay bailers 87 47 53 Milk coolers 140 68 32 Metal milk churns 115 37 63 Information/training on animal husbandry

94 39 61

For the services/ inputs that farmers have received in the past, a majority of the farmers reported having paid something the last time to access certain services/ products. The fees paid ranged depending on the type of service, distance from where the service provider was coming from, among other things. The table below provides an average cost of different products and services offered to the farmers:

Artificial Insemination (AI)

Veterinary treatment services

Veterinary vaccination

Supplementary feeds

Mineral supplements

Disinfectants - for cleaning and sterilizing

Insecticides & tick sprays

BASE: All who ever received.... 234 242 274 102 284 139 254

%

Yes 93 98 95 86 98 96 97

No 7 2 5 14 2 4 3 Amount paid (mean in Fr) 4100 8900 1900 19100 10800 14400 11300

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

17

Level of satisfaction with service/inputs received The following table shows the level of satisfaction with services/inputs received:

Level of satisfaction with service received last time

Art

ific

ial

Insem

inatio

n

(AI)

Vete

rinary

tr

eatm

ent

serv

ices

Vete

rinary

vaccin

ation

Supple

menta

ry f

ee

ds

Min

era

l supple

ments

Dis

infe

cta

nts

-

for

cle

anin

g

an

d

ste

riliz

ing

Insecticid

es

& tic

k s

pra

ys

BASE: All ever purchased/received service 234 242 274 102 284 139 254

Completely satisfied 42 74 94 54 87 77 85

Partly satisfied 34 21 6 34 12 22 13

Not at all satisfied 24 4 - 12 1 1 2

A majority of the farmers who accessed the seven most popular services/ inputs reported being satisfied with the quality and nature of services provided. For those reporting complete satisfaction, the lowest reported complete satisfaction was recorded among farmers who received Artificial Insemination (42%) while the highest was registered among farmers receiving veterinary vaccination at 94%. Other levels of satisfaction stood at 74% for veterinary treatment services, 54% for supplementary feeds, 87% mineral supplements, 85% for insecticides and tick sprays, and 77% for disinfectants for cleaning and sterilizing.

While there is room for improvement among those reporting complete satisfaction, particularly among those reporting lower than 90%, there is more to be done among those reporting partial satisfaction and those claiming not satisfied at all.

Areas where milk could be sold Respondents mentioned a number of possible areas where milk could be sold as presented below:

Area

Areas could sell milk TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN BASE: Total Sample 302 101 101 100

% Bulking/ cooling center 75 88 60 75 Hawker/ brokers 57 70 29 72 Farmers cooperative /group /association 47 49 38 54 Direct to homes e.g. Neighbours or family members 47 49 49 45

Direct to institutions e.g. school, hospital, food kiosk 25 25 31 19

Milk bar 26 32 31 16

There were more farmers reporting milk bulking and collection centers as places where they could sell their milk. This was reported by 75% of the farmers. It was followed by

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

18

hawkers/ brokers at 57%, and neighbors/ relatives and cooperatives/farmer groups tying at 47%, milk bars 26%, institutions 25%. However on being asked where they are selling milk currently a majority of them reported selling to brokers/ hawkers (52%) followed by neighbours/ family members, milk bulking/ cooling centers or to farmers associations. Interestingly, hawkers are not a popular buyer in Gatsibo district, while selling to neighbours and family members seem to be the most preferred here.

Types of customers TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN

BASE: Total Sample 302 101 101 100

% Hawker 52 62 26 67 Cooling plant 47 51 47 42 Direct to homes e.g. Neighbours or family members 47 49 49 45 Farmers cooperative/group/association 47 49 38 54 Milk bar 26 32 31 16 Direct to institutions e.g. school, hospital, food kiosk 25 25 31 19

Bulking center 11 12 8 12 Processor 10 11 4 15 Broker at farm gate 5 8 3 5

However, in terms of preference among those who sell to more than 1 channel, ‘direct to homes’ and ‘farmers co-operatives’ emerged as the preferred buyers. Adequacy of information received on where could sell milk Asked to explain what they felt about the information they received regarding where they could sell their milk, a majority of the farmers indicated they received just enough information (72%). Only a paltry 2% reported receiving what they considered as a lot of information. However, farmers in Nyagatare BMN seem to be divided almost equally among those claiming to receive just enough information (52%) and those saying they received very little information (46%).

Info received TOTAL Nyagatare

Mbare Nyagatare

BMN Gatsibo BASE 302 101 100 101 %

Very little 26 23 46 11 Just enough 72 75 52 87

A lot 2 2 2 2 Asked to indicate the other services they enjoyed from their main buyers besides buying their milk, the majority of farmers (57%) reported receiving no other services at all. The table below shows some of the services received by farmers from some milk buyers:

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

19

Services received TOTAL

Nyagatare Mbare

Gatsibo Nyagatare

BMN

BASE: Total Sample 302 101 101 100 %

Advance on milk payments 20 22 19 20 Farm inputs - seeds, fertilizer 5 2 6 8 Animal feeds/ supplements 7 6 6 8 Milk collection from the farm or near farm

6 5 4 10

AI services 7 4 4 12 Animal health services- treatment, vaccination and drugs

19 21 16 20

Training on animal husbandry 12 4 18 14 Information on market prices 8 11 5 9 Delivery/ transport of farm inputs and animal feeds 3 3 3 4 None 57 53 63 55

Of the services received, some farmers claimed to have paid for them while some were either not sure or did not pay anything. The main mode of payments for these services was the check-off system with only 28% claiming to pay in cash.

Services paid for (%)

Advance on milk payments 30

Farm inputs - seeds, fertilizer 31

Animal feeds/ supplements 50

Milk collection from the farm or near farm 26

AI services 50

Animal health services- treatment, vaccination and drugs 65

Training on animal husbandry 14

Information on market prices 8

Delivery/ transport of farm inputs and animal feeds 10

Extra services required from milk buyers When asked if they would require extra services from the milk buyers, majority of the farmers responded positively. Below is the list of services they would expect to get from the milk buyers:

Services/ inputs required TOTAL

Nyagatare Mbare

Gatsibo Nyagatare

BMN

BASE: Total Sample 302 101 101 100

%

Advance on milk payments 37 30 37 46

Farm inputs - seeds, fertilizer 18 14 22 18

Animal feeds/ supplements 30 23 36 33 Milk collection from the farm or near farm 25 23 25 27

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

20

AI services 25 23 23 30 Animal health services- treatment, vaccination / drugs 29 28 35 26 Training on animal husbandry 30 25 31 35

Information on market prices 28 24 27 33 Delivery/ transport of farm inputs and animal feeds 18 16 19 18

None 33 31 41 29 In regard to payments for milk, 2/3 of the farmers indicated they are paid in cash after a specified period as shown in the table below. However, in Gatsibo, a significant number of farmers confirmed to receive money through their bank accounts. Two modes of payments also emerged as the most preferred means of receiving payments by farmers:

Mode of payment for sold milk TOTAL Nyagatare

Mbare Nyagatare

BMN Gatsibo BASE: Total Sample 302 101 100 101 % Paid cash on delivery 8 4 9 11

Paid in cash after a specified period 62 73 64 50 Cash deposited to a financial institution 14 9 14 18 Barter - exchange milk for other services 0 - - 1

Farmers who deliver milk to the formal market were asked how they deliver milk to the market. ¾ of the respondents claimed to deliver milk on their own to the market. However, in terms of the preferred mode, over ¾ of the farmers would prefer their milk to be picked up at farm gate. This pattern was similar in all the 3 markets:

Current milk delivery system TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN Base 181 60 58 63

% The buyer provides for transport from the farm or near farm 25 33 12 29 Use your own means to transport (bike, walk) etc 75 67 88 71

Overall, among the farmers whose milk is collected by the buyer, slightly less than half felt it was either reliable or very reliable. However, in Gatsibo (though the base was small) the majority of the farmers rated the transport to be unreliable.

Buyer reliability TOTAL Nyagatare

Mbare Nyagatare

BMN Gatsibo BASE: All provided transport by the buyer 45 20 18 7

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

21

% [wt=5] Very reliable 24 15 44 - [wt=4] Reliable 20 15 28 14

[wt=3] average 16 15 11 29 [wt=2] Poor unreliable 13 20 6 14 [wt=1] Very unreliable 27 35 11 43

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

22

Frequency of milk collection Milk is collected generally once a day across the three regions:

Milk collection TOTAL

Nyagatare

Mbare

Nyagatare

BMN Gatsibo BASE: All provided transport by the buyer 45 20 18 7 %

Once in a day 93 95 89 100 Two times a day 4 - 11 - Three times 2 5 - -

Asked to express their feeling on whether they thought this was adequate or inadequate, a majority (62%) felt it was inadequate. However, in Nyagatare BMN, 56% of the respondents felt it was adequate.

Adequacy of Milk collection TOTAL

Nyagatare Mbare

Nyagatare BMN Gatsibo

BASE: All provided transport by the buyer 45 20 18 7

%

Adequate 38 30 56 14

Inadequate 62 70 44 86 Awareness of cooling plant Almost all respondents were aware of a cooling plant near them. Some of the cooling plants mentioned include:

• Mudakos

• Nyagatare cooling plant

• Mbare

• Terimbere mworozi (Karangazi)

• Rwabiharamba dairy

• Musenyi

• Bashumbambeza

• Karama

• Mubyatarama

• Kirebe

• Cyangarama

• Kamate A majority of the farmers (90%) also claimed that the cooling plants were owned by farmers’ cooperative groups in the region. Farmers stated they would expect to get the following services from the cooling plants:

Cooling plant services Total Nyagatare

Mbare Gatsibo Nyagatare

BMN BASE: Total Sample 302 101 101 100

Credit facility 74 69 72 81

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

23

Farm inputs - seeds, fertilizer 46 42 48 48 Animal feeds 62 51 67 67 Milk collection from the farm or near farm 54 55 44 62 AI services 57 51 57 63

Animal health services - treatment and prevention 74 70 78 72 Vaccination and drugs 71 64 69 80 Training on animal husbandry 58 58 50 66 Information on market prices 74 69 72 81

Credit facility, animal health services – treatment and prevention and information on market prices emerged as the key services farmers need, although most of the other services and inputs are also needed at varying levels which reflects a very high demand. Asked if they would be happy with check-off as mode of payment for their milk, nearly all farmers (93%) said that they would be very happy.

Reaction to check-off payment system TOTAL

Nyagatare Mbare Gatsibo

Nyagatare BMN

BASE: Total Sample 302 101 101 100

% Happy 93 92 92 95 Not sure 4 2 7 3 Unhappy 3 6 1 2

Skills/ information needed by farmers Majority of the farmers (83%) indicated they do not have the skills needed for good dairy farming across the 3 regions. When asked to mention the areas they needed more information on, the following emerged:

Skills/info required TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN

BASE: Total Sample 302 101 101 100

Disease id, treatment & prevention 72 76 77 63

Improvement of milk production 66 71 61 66

Drug administration 61 62 60 59

New animal feeds 60 64 55 59

Milk prices 55 53 55 57

Cattle breeding 54 57 41 64

Dairy farm record keeping 30 34 25 31

Record keeping 25 21 26 28

Public health issues and requirements 22 19 27 21

Awareness of government policies 19 17 20 21

Buyers 13 11 14 13

Whether ever received any useful information Farmers were asked whether they had ever received any useful information about dairy farming. About 69% reported not to have received any. The same trend was recorded

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

24

from the three regions. Those reporting having received useful information were then asked to indicate what services they had received. The advice/ information were mainly stated to be from government extension workers and to some extent, the NGO’s. The following Table shows the breakdown:

Info received TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN BASE: All ever received information 93 24 36 33 %

Improvement of milk production 54 50 56 55 Awareness of government policies 33 25 28 45 Cattle breeding 32 33 25 39 New animal feeds 24 25 25 21 Disease identification, treatment and prevention 19 17 25 15 Drug administration 18 8 28 15

Dairy farm record keeping 10 13 8 9 Record keeping 2 - 3 3 Public health issues and requirements 1 - 3 - Milk prices 1 - - 3

Whether plans to change anything Asked whether they planned to change anything about their dairy farming in the next 1 year, nearly all farmers indicated they have some plans in mind. However, 85% of the farmers highlighted breed improvement as the key change they would like to implement. The figure below shows areas farmers mentioned they would like or plan to improve on in the next 1 year. Planned changes for farm and dairy improvement:

11%

12%

15%

15%

23%

23%

85%

33%

32%

31%

30%

30%

28%

23%

Improve breeding / breed of cattle through breeding

methods / use AI

Improve building

Change feeding to zero grazing

Improve feed through growing better / more feed

Enlarge size of herd / Buy more cattle

Improve the veterinary treatment / drugs used on

cattle

Improve my knowledge about dairy farming

Improve feed by buying supplements

Group together with other farmers / join association

/ join coop / join producer group

Improve the management of my dairy as a business

Grouping with other farmers to get cheaper inputs

Buy farm equipments

Improve feed storage methods

Improve the quality of my milk / improve my milk

handling skills

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

25

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

26

To achieve the above desired changes farmers mentioned the following measures as drivers they are definitely likely to adopt:

• Grouping together with other farmers or joining co-operative to benefit from economies of scale - e.g. cheap farm inputs

• Use of AI services

• Growing of more and quality feed

• Enlarging size of herd

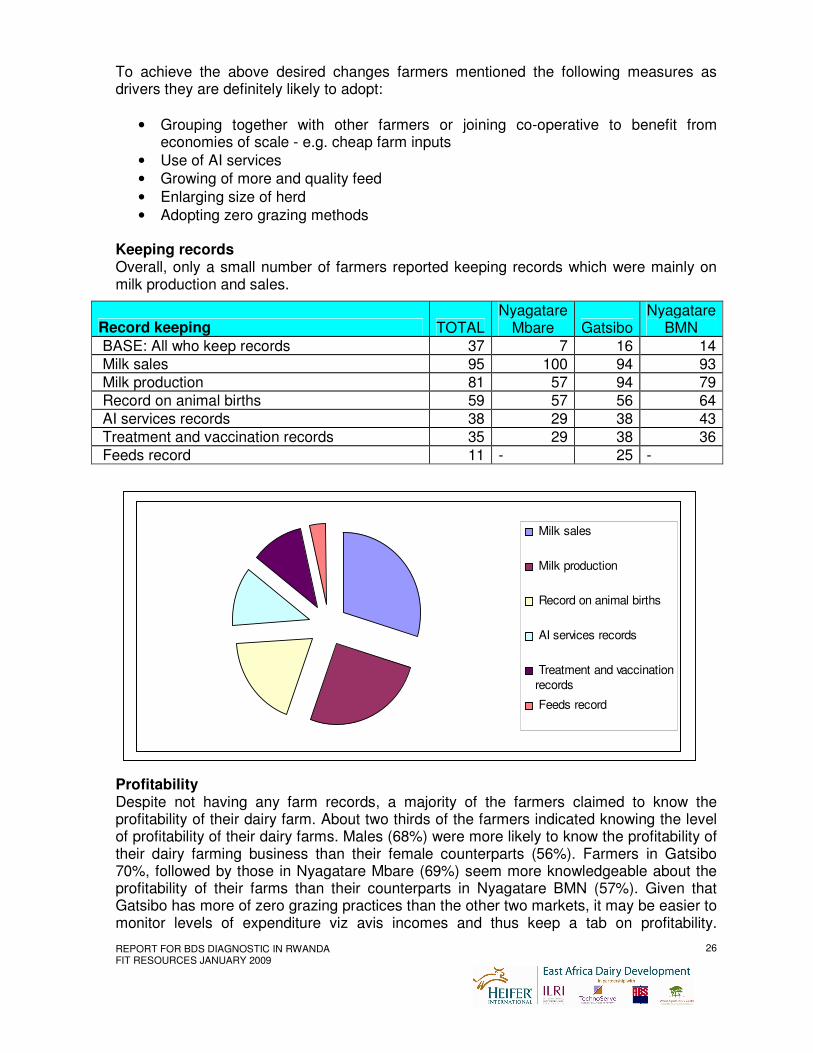

• Adopting zero grazing methods Keeping records Overall, only a small number of farmers reported keeping records which were mainly on milk production and sales.

Profitability Despite not having any farm records, a majority of the farmers claimed to know the profitability of their dairy farm. About two thirds of the farmers indicated knowing the level of profitability of their dairy farms. Males (68%) were more likely to know the profitability of their dairy farming business than their female counterparts (56%). Farmers in Gatsibo 70%, followed by those in Nyagatare Mbare (69%) seem more knowledgeable about the profitability of their farms than their counterparts in Nyagatare BMN (57%). Given that Gatsibo has more of zero grazing practices than the other two markets, it may be easier to monitor levels of expenditure viz avis incomes and thus keep a tab on profitability.

Record keeping TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN

BASE: All who keep records 37 7 16 14

Milk sales 95 100 94 93

Milk production 81 57 94 79

Record on animal births 59 57 56 64

AI services records 38 29 38 43

Treatment and vaccination records 35 29 38 36

Feeds record 11 - 25 -

Milk sales

Milk production

Record on animal births

AI services records

Treatment and vaccination

records

Feeds record

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

27

Nyagatare BMN, which has bigger herds of the indigenous cattle, may still have more farmers who keep cattle for traditional values rather than as business.

Awareness on farm profitability TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN

BASE: Total Sample 302 101 101 100

Yes 66 69 70 57

No 34 31 30 43 Technology (mobile phones) Penetration of mobile phone within the three areas is high as attested by the table below. Generally, about 82% of the farmers reported owning/ having access to a mobile phone. This was almost uniformly distributed across all segments.

Mobile phone access TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN BASE: Total Sample 302 101 101 100 %

Yes 82 80 84 82 No 18 20 16 18

Asked which services they would like to access via the mobile phone sms service, cow disease alerts, milk prices, and market for breeds, availability of new products, and training/ field days/ dairy farming workshops emerged as the five leading pieces of information they would require.

Info required by phone TOTAL Nyagatare

Mbare Gatsibo Nyagatare

BMN BASE: All with/ have access to a mobile phone 248 81 85 82 Cow disease alerts 75 73 73 78 Milk prices 72 70 64 83

Market for breeds 71 69 69 74 Availability of new products and services 62 63 64 60 Trainings/ field days/ dairy farming workshops 61 58 64 61 Availability of milk payments 50 47 44 60 New markets 50 48 39 65 Sale of cows 50 57 41 52

Quantity of milk supplied 48 51 45 49 New market opportunities 48 44 40 60 Access to loans 38 32 41 39

Farmers indicated high willingness to pay fees ranging from Fr 1000- 2100 to be able to access these services. See the figure below:

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

28

Capital Almost all farmers indicated that they require capital to develop their dairy farming business. Most of the farmers (61%) say they would seek credit from banks. See table below:

Credit options TOTAL Nyagatare

Mbare Gatsibo Nyagatare

Bmn BASE: All need lump sum/ capital 278 90 99 89

Banks 61 61 64 58 Micro finance institutions 13 12 12 16 Cooperative SACCO 8 6 8 11

Cooling plant 6 7 7 4 No source 4 4 4 4 NGOs 3 4 4 1

Family/ friends 3 4 1 2 Suppliers 1 1 - 1 Government 0 - - 1

Awareness of farmer lobby organization Only a few farmers were aware of an organisation that looks after their needs apart from Gatsibo where 45% claimed to be aware:

72

71

62

61

50

50

50

48

48

38

37

68

67

65

54

57

42

45

44

40

41

35

33

75 Cow disease alerts

Milk prices

Market for breeds

Availability of new products and services

Trainings/field days/dairy farming workshops

Availability of milk payments

New markets

Sale of cows

Quantity of milk supplied

New market opportunities

Access to loans

Milk rejected at processor level to inform farmer

Info would be ready to pay for

Info would like to access via mobile phone

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

29

Awareness of organization TOTAL

Nyagatare Mbare Gatsibo

Nyagatare Bmn

BASE: Total Sample 302 101 101 100 %

Yes 38 30 45 39 No 62 70 55 61

In regard to membership to a farmer’s co-operative majority of the farmers belongs to none. However, in Nyagatare BMN slightly over half claimed to be members of a cooperative.

Whether member of a Cooperative TOTAL

Nyagatare Mbare Gatsibo

Nyagatare Bmn

BASE: Total Sample 302 101 101 100

Yes 45 34 49 53

No 55 66 51 47

Challenges faced by farmers Low and fluctuating milk prices coupled with delayed payments, inadequate and low quality foliage for feeding cattle – e.g. grass and Napier grass, irregularity and unaffordability of AI services and unaffordable/ unreliable animal treatment services were some of the key challenges farmers highlighted as major constraints to their dairy farming. Low milk prices combined with fluctuating milk prices and delayed milk payments accounted for the highest single challenge at 67%. In terms of gender, there were no significant variations although the findings seem to indicate that male farmers were significantly (74%) more likely to complain about low / fluctuating milk prices/ delayed payments compared to their female counterparts (37%), while female farmers were significantly (82%) more inclined to complain about inadequate/ low quality animal foliage than their male colleagues (58%). The same trend was noticed for irregular/ unaffordable AI services. Age wise, there were no significant differentials across except that farmers aged less than 35 years were significantly less likely to complaint about the adequacy/ quality of foliage than their counterparts in higher age groups. As per the markets, Gatsibo records the lowest complaint about low milk prices (51%) as compared to the 2 Nyagatare Sectors – BMN 82%, and Mbare 68%. Perhaps this can be explained by the fact that Gatsibo reports the lowest milk output, (and thus higher prices) and less dependence on milk brokers unlike the other two. However, Gatsibo reports the highest complaint (72%) regarding adequacy/ quality of foliage available in the region – reflecting its bigger dependency on zero grazing for its dairy farming. BMN records the lowest at 55% mirroring its larger grazing fields. Other challenges mentioned are as per the table below:

Main

Gender Age Region

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

30

challenges/ constraints facing farmers

TOTAL Male

Female

18-35

36-55

56+ Nyagatare Mbare

Gatsibo

Nyagatare BMN

BASE: Total Sample 302 243 59 76 143 83 101 101 100

Low/fluctuating milk prices/ delayed payments 67 74 37 71 60 74 68 51 82

Inadequate/ low quality foliage - e.g. grass, napier grass etc 63 58 82 38 68 70 62 72 55 Irregular/ unaffordable AI services 55 58 41 58 47 66 61 45 59 Unreliable/ unaffordable animal health services 46 46 46 46 44 53 38 45 56 Unreliable source/ unaffordable supplementary feeds 43 44 37 46 37 48 45 33 52 Inaccessible loan facilities (high interest etc) 37 38 32 41 35 31 30 42 40 Poor climatic conditions 32 34 24 33 37 27 38 26 33 Lack of various dairy management skills 19 20 16 9 20 27 19 13 26

Disease outbreaks 13 14 8 13 15 12 12 10 18

Insecurity 10 10 10 3 13 12 5 23 3 Exploitation by middle men 8 9 3 10 6 11 11 1 12 Unavailability of quality seed for growing feed on farm 7 7 7 7 6 8 9 5 6 Unavailability of milk cooling facility 5 5 5 6 4 8 6 5 4 High transport cost 4 5 3 2 5 7 4 5 4 Inaccessible roads 2 2 - 1 2 3 2 - 3

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

31

Key demand side constraints and opportunities

The following are the constraints and potential opportunities. Constraint Opportunity

Inadequate foliage and grass to feed animals due to poor climatic conditions – draught.

• Provide seed to grow fodder to selected farmers who have larger farms. They can thus sell to others at competitive prices

• Introduce supplementary feeds Irregular and unaffordable AI services

• More AI providers needed at main trading centres at village level

• Establish scheduled visits by AI providers to all villages

• Train farmers on basic procedures of conducting AI

Inaccessible/ unaffordable loans to promote dairy farming.

• Provide easily accessible/ affordable financial products that are developed/ tailored to meet farmer needs

Low and fluctuating milk prices hindering farmers from planning their future

• Establish more strategic milk collection/ cooling centres

• Improve on roads to facilitate easy/ cheaper milk transport

• Establish a local dairy processing plant Poor/ unreliable animal treatment and vaccination services

• Additional veterinary doctors needed at village level

• Further training for skill upgrading for vet technicians

Unaffordable supplementary feeds beyond the reach of many small scale farmers Unreliable source of supplementary feeds

• More suppliers needed

• Use of locally available raw materials need to be explored to make them affordable

• More farmers should be trained on how to prepare them

Disease outbreaks • Modern lab testing facility established in the region

• Vaccination of cattle strengthened

Business development services that address those constraints and opportunities

The following table outlines the BDS that address these constraints and opportunities: Constraint Opportunity BDS that address those

constraints & opportunities

Inadequate foliage and grass to feed animals due to poor climatic conditions – draught.

• Provide seed to grow fodder

• Supplementary feeds

INPUT SUPPLY such as creating links between farmers and suppliers and enabling suppliers to reach more farmers and develop their capacity to offer better quality inputs.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

32

Irregular and unaffordable AI services

• More AI providers needed at main trading centres at cell level

• Scheduled visits by AI providers to all villages

INPUT SUPPLY such as facilitating links between farmers and AI suppliers and enabling suppliers to reach more farmers and develop their capacity to offer better, less expensive inputs.

Inaccessible/ unaffordable loans to promote dairy farming.

• Easily accessible/ affordable financial products developed tailored to meet farmer needs by banks and MFIs

• Major milk buyers e.g. dairy cooperatives consider introducing simple financial products that are affordable by the farmers

FINANCE such as helping farmers identify and access funds through formal and alternative channels that include supplier or buyer credits, factoring companies, equity financing, venture capital, credit unions and commercial banks (letters of credit, etc.)

Low and fluctuating milk prices hindering farmers from planning their future

• Establish more milk collection /cooling centres

• Improve on road networks

• Establish locally a dairy processing plant to take advantage of the excess milk.

MARKET ACCESS such as identifying and establishing new markets for products plus the creation of links between all the actors and helping buyers to expand their outreach to, and purchases from, farmers. This may also include helping farmers to produce to buyer specifications. INFRASTRUCTURE such as establishing sustainable infrastructures that enable farmers to increase sales and income e.g. refrigeration, processing facilities, transport systems, communication centers, and improved roads.

Poor /unreliable animal treatment and vaccination services

• Additional veterinary/vaccination doctors needed at village level

• Further training for skill upgrading

• Scheduled visits to villages to attend to farmer needs

INPUT SUPPLY as above TRAINING & TECHNICAL ASSISTANCE such as workshops to develop the capacity of farmers and suppliers to better plan and manage their operations and improve their technical expertise. This may also include fostering links between service providers and farmers.

Unaffordable supplementary feeds beyond the reach of many

• More suppliers needed

• Use of locally available raw materials need to

INPUT SUPPLY as above. This may also include encouraging more potential suppliers to meet

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

33

small scale farmers Unreliable source of supplementary feeds.

be explored to make them affordable

the market demand. TECHNOLOGY & PRODUCT DEVELOPMENT such as identifying new technologies.

Disease outbreaks • Modern lab testing facility established in region

• Vaccination of cattle strengthened

INFRASTRUCTURE as above

Poor transport/ road networks that slows growth of the dairy sector

• Improved road networks in the deep rural areas

• improvement of the transport systems e.g. introduction of minibuses to compete with the motor bikes and help farmers to market their milk cheaply

INFRASTRUCTURE as above

The following are some of the policy constraints that are affecting the MSE product markets:

1. Locating households away from dairy farm

The Government of Rwanda has introduced a land development and resettlement policy in this region where farmers are settled in centralised areas while the grazing farms are allocated a considerable distance away. Managing the farm becomes tricky and there are added costs of travelling and a worker to keep watch and graze the animals. Milking may also not be properly done and accounted for in the absence of the farm owner and there could be cases of cheating about the milk output.

2. Strict legal and public health regulatory requirements

The strict enforcement of minimum regulatory standards for suppliers particularly milk handling/ collection, may be responsible for keeping very few suppliers engaged in this business. As a result, farmers cannot access certain services easily and affordably as the supply competition is limited. In order for the BDS market to be stimulated for faster growth, the strict legal/ health requirements may need to be relaxed a bit until such a time suppliers have grown and the need for strict enforcement is really needed.

3. Government continued involvement in service provision

Government policy of providing subsidised AI and veterinary treatment and

Specific policy constraints that are affecting MSE product markets

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

34

vaccinations, though positive in its intentions can only serve to establish the sector from infancy. However, sustained growth can only be achieved where market forces of supply and demand are left free to operate. The government should reduce its involvement to regulating and creating an enabling environment. Its continued presence and active participation in service provision only serves to discourage and choke private sector competition. This situation where effective competition is lacking, has led to poor services being dispensed judging by some of the complaints received during fieldwork. For instance there were reports of poor quality semen which led to farmers getting poorer grade calves in contrast to what was promised during insemination. The tragedy of this is that farmers only discover the problem after nine months when birth takes place. Again farmers reported waiting for days before a veterinary doctor arrives in their village to treat their cattle.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

35

SUPPLIER DIAGNOSTIC by location

Existing providers/ services and their locations The following breakdown shows how suppliers were distributed across this region. A total of seven suppliers were identified in Nyagatare/ Tabagwe sectors. However, only six were found/ interviewed. In Karangazi sector, six suppliers were listed but only five were found/ interviewed. In Kiramuruzi sector four suppliers were identified but only three were found and interviewed. A workable data base of the BDS actors A workable data base of these BDS providers is attached to this report (Annexes/Databases). BDS suppliers interviewed

List of suppliers interviewed as attached above.

Types of services and price of services, how providers cover costs, profitability, existing contractual arrangements/relationships and promotional/marketing strategies Types of services The common services/ inputs provided in this area include veterinary treatment and vaccination services, mineral supplements, insecticide and tick sprays, and disinfectants for cleaning and sterilizing, and supplementary feeds. Others are information/ training in animal husbandry and artificial insemination (AI). Across the two districts, it appears that the services provided are similar although Nyagatare District could be defined as more of a cattle keeping district while Gatsibo would qualify more as an area of mixed farming practices with less land for cattle rearing. Grazing fields are therefore bigger in Nyagatare than in Gatsibo.

Services/ inputs provided Nyagatare BMN (No of suppliers –

BASE=6)

Nyagatare Mbare (No of suppliers

BASE=5)

Gatsibo (No of suppliers

BASE=3)

Vet treatment services 6 5 3

Disinfectants - for cleaning and sterilizing

6 5 3

Mineral supplements 3 5 3 Info/training in animal husbandry

5 4 2

Insecticides & tick sprays 6 2 2 Supplementary feeds 2 1 2 Milk testing kits 2 3 1

Seeds to grow feed 2 2 2

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

36

One of the AI providers told of cases where they are sometimes forced to forego payments when they come across needy farmers who are unable to pay for services.

Such costs are absorbed through government subsidiaries like ERAGIC – an institution that promotes modern dairy development through easy access to AI services.

Price of services and how providers cover costs/ profitability Across the 3 sites, suppliers interviewed indicated that they do not charge their customers for any information they dispense concerning dairy farming. They make their money and profits by selling/ charging for the conventional products and services provided like selling drugs, AI provision or treatment of cows. When pricing services and inputs suppliers considered several factors to arrive at a given price, as follows:

• Wholesale price of input from source

• Transport cost/ distance covered if it is an outreach service

• Taxes payable on service/ input

• Rent

• Whether demand for input/ service is high or low

• Competition

• Profit margin

• Big suppliers like Agrotech Nyagatare who is associated with Agrotech chain of animal drug shops, explained that they do not determine prices, but that the prices are dictated from the head office in Kigali.

• For instance, some AI providers reported buying semen to fertilize one cow at 500 fr from the Government agents only to sell this at 1500 fr to the dairy farmer. Besides, the farmer pays transport cost separately. Usually, this will be the cost of hiring a motor bike by the AI provider.

The commonest form of payment for services/ inputs rendered was cash after service, across all types of service providers. When the service provider is a Cooperative or an Association of farmers, members enjoy the check-off system facility which allows them to pay later through deductions from their weekly/ monthly payment for milk deliveries. Other forms of payment options are delayed/ staggered payment and payment by cheque. Staggered payment is normally allowed for instance where a cow is either dry or sick until it heals and resumes being milked. Should it die, then the charges are written off - if it is only one. The following table shows the common modes of payments for services and the associated challenges.

Vet vaccination 2 1 Milk collection/ bulking 2 2 Milk advance payments or credit services

2

Artificial Insemination 2 2

Information on dairy markets

1 1 1

Metal milk churns 2 1

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

37

Nature/ type of business

Common payment modes

Challenges associated with payment modes

Supplier preferred modes of payment

Cooperatives Check off, cash, delayed/ staggered

Follow ups expensive/ time consuming

Check-off, cash

Private firm/ proprietor Cash, cheque Bouncing cheques Cash

Government/ NGOs Cash (subsidized), delayed/free

Expensive & time consuming follow ups

Cash/free

However, suppliers reported that they face some challenges using the check-off system. Some suppliers complained that there were occasions when farmers called them for treatment emergencies on their cows only to be informed after the treatment that there was no money for payment until later. The biggest complaints with the various forms of payments were associated with cheques due to dishonesty and staggered/ delayed payments as it was both time consuming and expensive to make a follow-up on the farmer. Suppliers prefer to deal in cash with their customers as it is easy and efficient. Check-off is preferred only where members of associations or cooperatives are involved. Contracts In terms of contractual arrangements for supply of goods and services, a good number of the suppliers had ever entered into such arrangements. Of the 14 suppliers interviewed, 7 reported being in some form of contractual arrangements with Nyagatare Sector having 5 and Gatsibo 2. In Nyagatare BMN one supplier reported having entered into contractual arrangements with 10 groups of farmers and another with 300 individuals. In Nyagatare Mbare, a supplier had entered into a contractual arrangement with one group of farmers, while another had entered with 4 individual farmers while yet another had entered with both a group of farmers and individual farmers. In Gastibo, 2 suppliers reported having entered into contractual arrangements with individual farmers. One of these agreements was for the supply of semen/ hormones to fertilize cows. Another one was simply an Agrotech branch in Nyagatare getting supplies from Agrotech head office in Kigali. The contracts were both written and verbal and were entered mostly with farmer groups and individuals as well. In terms of Contractual arrangements we can say that Nyagatare BMN is more advanced than the other two markets. The following table provides an outline of the suppliers and the various aspects of contractual arrangements:

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

38

Who entered Contracts with

Number in contracts in each market

Nyagatare BMN

Nyagatare Mbare Gatsibo

With a group 10 1 None

With an individual 300 4 2 Both individuals & groups None 2 None NA 4 2 1 Nature of Contracts

Written 1 2 1 Verbal 1 1 2

None 4 2 - Reasons for signing Contracts For better/ easier follow-up & auditing Yes Yes - Encourage farmers to buy our products Yes - - To reach small scale farmers in deep rural areas

Yes - -

To ensure farmers can pay us later - Yes - To be able to advance loan facilities - - Yes

Promotional strategies The commonest marketing strategies in the 3 sites include public meetings, use of satisfied customers (word of mouth) signboards and posters. In Gatsibo and BMN suppliers said they ensure their shops are located in strategic points for maximum visibility and access. In Nyagatare BMN, radio adverts, outreach services and use of regional representatives are also used in addition.

How suppliers create awareness Nyagatare BMN

Nyagatare Mbare

Gatsibo

Public meetings Yes Yes Yes Signboards/ posters Yes Yes Yes Satisfied customer/ word of mouth Yes Yes Yes Providing quality products/ services Yes Yes - Strategic locations for business premises

Yes - Yes

Outreach visits Yes - -

Media adverts (Radio) Yes - - Use regional reps to penetrate areas Yes - -

Capacity gaps of interviewed suppliers The key capacity gaps identified among BDS suppliers include the following

• Lack of capital to improve and expand business. This is particularly acute in the transport of milk to the market centers both locally and outside the region.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

39

• Lack of training on how to do conduct certain services like AI. This means some suppliers have to depend on others to do things they would have done – with some training.

• Lack of proper/ sufficient equipment and facilities. For instance some suppliers need basic lab equipment in order to diagnose animal diseases with some accuracy and thereby provide the correct drugs.

• Identifying/ accessing the skilled experienced Vet Technicians to support the suppliers is a major challenge.

• Lack of well trained staff to handle milk as required in accordance with public health.

• Ignorance and lack of knowledge is also common among some suppliers. Suppliers need to be knowledgeable enough in particular with the BDS sector they are dealing in.

• Keeping to the required regulatory/ sectoral standards has become difficult for some like premises, official documents, and mandatory training etc.

Priority supply side constraints, market failures, and market opportunities Key supply side constraints/ market failures

• Long distances and bad roads that farmers have to cover to reach suppliers and vice versa.

• Lack of an efficient public means of transport.

• Limited demand of dairy services and products owing to a depressed farmer income due to low milk sales/ price.

• Lack of stock of highly demanded products services.

• Farmers lack efficient communication tools like mobile phones that can ease communication between them and their suppliers.

• Few qualified technical staff hence sometimes delayed response to farmers’ requests.

• Government and NGO interference in service/ input provision at subsidized rates hence creating an artificial market environment. The price levels existing are not sustainable if subsidies are removed.

• Some of the AI providers have not been trustworthy and on many occasions they have promised farmers certain type of crossbreed/ pure breed and charged them accordingly, only for the farmers to get poor quality calves. In other words, what AI providers promise is not what farmers always receive.

• Lack of access to affordable capital was also mentioned by many suppliers as a key constraint. This became an issue when they wanted to expand their businesses. The situation is made worse by local banks who demand security for any credit advanced.

• Limited laboratory services that can boost accuracy in diagnosis of animal diseases and proper drug administration.

• Meeting the mandatory minimum legal requirements is sometimes a big challenge for suppliers to set up or expand their businesses.

• Lack of adequate back-up power/ maintenance skills to assure good milk even when there was power failure. Sometimes power goes off and the back-up generators fail to work due to poor maintenance practices. When this happens, all milk collected goes to waste. Farmers cannot also sell their next days milk until the problem is sorted out.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

40

Market opportunities In view of the foregoing discussion, the following were found to be potential market opportunities:

• Need to enhance milk collection/ bulking: The survey established that in each of the three markets there existed one or two cooling plants/ milk collection points. None of these cooling plants had the capacity to collect all the milk coming in from farmers in their catchment areas. As a result, some milk is returned to farmers when the tanks get filled up to capacity. This, coupled with the national campaign to transform cows to higher milk producing grades among farmers, means that the need for more storage and transport facilities is very urgent. More cooling plants will need to be established to cater for the increased milk in a site far away from the current cooling plant. This would reduce distances traveled to access the milk collection centers by dairy farmers. Reduced distances may also encourage farmers to deliver their milk instead of relying on middlemen and thereby increase their earnings.

• There is need for improved milk transportation from farms to the collection centers in additional to milk tankers being added to assist in efficient transporting of milk to the markets in Kigali and other parts of Rwanda. This may call upon local investors to introduce pick-up trucks to transport the milk efficiently and thus do away with the numerous exploitative milk middlemen.

• Efficient supply of affordable supplementary feeds, foliage and mineral supplements: This is an area that has the potential to grow very fast in the next few years. This is particularly so given the government drive to have farmers adopt modern dairy farming techniques. As farmers discard the traditional cows in favour of the higher grade cows, there will be a commensurate demand for appropriate feeds/ fodder and mineral supplements. This is also strengthened by the fact that land for grazing is getting smaller and zero grazing is being seen as the solution for the future.

• Improved AI services: With the shift to modern dairy farming in top gear in the region, there is need to enhance the provision of reliable AI services to assist in the transformation of local herds.

• Under the same assumption, another potential opportunity is the provision of seed to grow fodder. This would provide feed to the higher grade cows with zero grazing being encouraged.

REPORT FOR BDS DIAGNOSTIC IN RWANDA FIT RESOURCES JANUARY 2009

41

Comparison of interviewed suppliers

The following table provides a summarized synthesis of the comparison of the interviewed providers:

Aspect being rated Nyagatare BMN Nyagatare Mbare Gatsibo TOTAL

Capacity to deliver services

4 5 3 5 5 3 4 4 4 5 5 4 5 56

Closeness to SMEs (In terms of understanding their culture and geography

5 5 3 5 4 3 4 2 4 5 4 4 4 52

Commercial focus e.g. level of profitability

4 3 3 4 5 4 5 5 4 4 3 4 4 52

Focus on services, SMEs or BDS

4 4 3 3 4 3 5 3 4 4 4 4 4 49

Organizational independence- especially from donor funds

5 3 4 4 5 4 5 5 4 4 4 4 4 55

Legally registered 5 5 4 5 5 1 5 1 5 5 5 5 5 56

Willingness/interest/ability to partner

3 5 3 5 5 2 5 2 5 5 3 5 5 53

TOTAL 30 30 23 31 33 20 33 22 30 32 28 30 31 373 Mean 4.

28 4.28

3.28

4.42

4.71

2.85

4.71

3.14

4.28

4.57

0 4 4.28

4.42 28.69

27.8 3.97 29.25 4.17 29.66 4.23

Interviewers/ moderators were asked to rate their perceptions of services rendered by the suppliers whom they had just interviewed, using a rating of 1-5 where 1 was lowest and 5 the highest. From this scale it has emerged that most suppliers were rated highly in various aspects of service provision. The following points illustrate this.

• Suppliers scored a total of 373 out of an overall score of 455. This is a high score.

• Most of the aspects of business measurement scored impressively – between 49 and 56 marks out of a possible 65 points.