-

8/3/2019 Bus 516-Case (Report)

1/58

.

1

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter One - Overview of United Commercial Bank Ltd

-

8/3/2019 Bus 516-Case (Report)

2/58

.

2

Technology Perspective on Performance in United Commercial Bank

Ltd.

1.1IntroductionThe usage of information technology (IT), broadly

referring to computers and peripheral

equipment, has seen tremendous growth in service industries in

the recent past. The most

obvious example is perhaps the banking industry, where through

the introduction of IT

related products in internet banking, electronic payments,

security investments, information

exchanges, banks now can provide more diverse services to

customers with less manpower.

Seeing this pattern of growth, it seems obvious that IT can

bring about equivalent

contribution to profits.

In most countries, but essentially in emerging ones, there are

two types of banks: state-

owned, private domestic and private foreign. The roles of these

banks are important for the

development of the economy but it is widely observed that

private owned banks perform

much better that their government counterparts. For instance,

United Commercial Bank Ltd.,

the first generation private bank, has relatively poor IT

infrastructure than other private banks

in Bangladesh. Though the bank has taken initiations to upgrade

their IT system to keep up

with the industry trend, still lack in execution. However,

competitive pressures have emerged

as more and more foreign banks entering domestic markets.

Consumers have become more

astute in their buying, less loyal to a particular bank, and

more demanding of products and

services that fit their specific financial needs and time

schedules. Consequently, they have

attained the position to dictate where, how, and when they will

conduct their financial affairs.

To respond to consumer and market demands, local private bankers

must provide greater

convenience, increase accessibility of financial services and

products, and deliver at a faster

pace new and better targeted products and services. At the same

time, total costs of

operations and development must be maintained or reduced. All of

this must be done to

acquire or maintain a significant percentage of the consumers

financial transactions and

establish an acceptable profit margin. And this is possible

through Information technology

giving necessary competitive advantage.

The western world has continued to dominate the world of IT and

set the pace in the

transformation of the world economy. Likewise, the banking

industry has in the last decade

been characterised by increasing investment in IT.

-

8/3/2019 Bus 516-Case (Report)

3/58

.

3

Technology Perspective on Performance in United Commercial Bank

Ltd.

1.2 Historical Background of the United Commercial Bank

Limited

Sponsored by some dynamic and reputed entrepreneurs and eminent

industrialists of the

country and also participated by the Government, UCBL started

its operation in mid 1983

and has since been able to establish one of the largest networks

of 108 branches among the

first generation banks in the private sector. With its firm

commitment to the economic

development of the country, the Bank has already made a distinct

mark in the realm of

Private Sector Banking through personalized service, innovative

practices, dynamic approach

and efficient Management. The Bank, aiming to play a leading

role in the economic activities

of the country, is firmly engaged in the development of trade,

commerce and industry

thorough a creative credit policy. The Bank has in its

Management a combination of highly

skilled and eminent bankers of the country of varied experience

and expertise successfully

led by Mr. M. Shahjahan Bhuiyan, a dynamic banker, as its

Managing Director and well

educated young, energetic and dedicated officers working with

missionary zeal for the

growth and progress of the institution.

From the very inception it is the firm determination of UCBL to

play a vital role in the

national economy. They are determined to bring back the long

forgotten taste a banking

services and flavors. They want to serve each promptly and with

a sense of dedication and

dignity. UCBL has its prosperous past, glorious present,

prospective future and under

processing projects and activities. UCBL is fully Bangladeshi

entrepreneurs owned private

bank. The members of the board of directors are creative

business men and leading

industrialist of the country. To keep rate of knots with time

and in synchronization with

national and international economic activities and for rendering

all modern services, UCBL,

as a financial institution automated all its branches with

computer network in accordance

with the competitive commercial demand time. Moreover,

considering its forth-coming future

the infrastructure of the bank is rearranging. The expectation

of all class businessman,

entrepreneurs and general public is much more to UCB.

-

8/3/2019 Bus 516-Case (Report)

4/58

.

4

Technology Perspective on Performance in United Commercial Bank

Ltd.

1.3. Objectives of United the Commercial Bank Limited

The objectives of United Commercial Bank are as follows:

y To provide best quality service among the others Banky To

provide quick and superior service by applying modern information

technology.y By improving congenial relationship between the bank

and the customers, come

closer to play a vital role in national development.

y By investing the income generating projects, giving

shareholders maximumdividend.

y In the competitive market, the bank is to provide new

innovative banking services toits valued customers and build up its

own image.

y To ensure the improvement of professional quality of manpower

by increasing thework efficiency and technological knowledge.

1.4. Mission of United the Commercial Bank Limited

To offer financial salutations that create, manage and increase

our clients wealth while

improving the quality of life in the communities we serve. And

To assist in bringing high

quality service to our customers and to participate in the

growth and expansion of our

national economy.

1.5. Vision of United the Commercial Bank Limited :

UCBLs vision is to have poverty free Bangladesh in course of a

generation in the new

millennium, reflecting the national dream. Building a society

where human dignity and

human rights receive the highest consideration along with

reduction of poverty to set high

standards of integrity and bring total satisfaction to our

clients, shareholders and employees.

To become the most sought after bank in the country, rendering

technology driven innovative

services by our dedicated team of professionals. The main vision

of UCBL is to be the first

choice through maximizing value for our client, shareholders

& employee and contributing to

the national economy with social commitments.

-

8/3/2019 Bus 516-Case (Report)

5/58

.

5

Technology Perspective on Performance in United Commercial Bank

Ltd.

1.6 Values United Commercial Bank Limited

y We put our customer firsty We emphasize on professional

ethicsy We maintain quality at all levelsy We say what we believe

iny We foster participate management

1.7. Business Motto of United the Commercial Bank Limited

United we achieve

1.8. Special Features of the United Commercial Bank Limited

1) The Bank has introduce the duel credit card system for

clients benefit so that they can

make transaction anywhere of the world

2) The UCBL has introduced monthly saving scheme and educational

saving scheme to

encourage the limited and fixed income group of people.

3) The Bank is committed to continuous research and development

to match with modern

banking.

4) The operations of the Bank are computerized oriented to

ensure efficient services to the

customers.

5) The Bank has introduced camera surveillance system (CCTV) to

strengthen the security

services inside the Bank premises.

6) The United Commercial Bank has introduced customer relations

management system to

resolve client problem and also provided Online Banking facility

at low charge.

-

8/3/2019 Bus 516-Case (Report)

6/58

.

6

Technology Perspective on Performance in United Commercial Bank

Ltd.

1.9. Organizational Development of the United Commercial Bank

Limited

In the 1450s and 1960s a new integrated type of training

originated knows was organizational

development. Organizational development is an intervention

strategy that uses group

processes to focus on the whole culture of an organization in

order to bring about planned

change, it seeks to change belief attitudes, values structure

and practices so that organization

can better adapt to technology and live with the fast pace of

change. The general objective of

organization development is to change all parts of the

organization in order to make humanly

responsive, more effective, and more capable of

self-renewal.

The organizational development process does not preclude the use

of conventional training

method, which is useful for some purpose. The management of

United Commercial Bank is

also concern about the training for its development. They

believe that if the employees will

be trained enough they would contribute more for the development

of the banking business

that is why; they send some employee in every batch.

1.10. Organizational Structure of United Commercial Bank

Limited

The development of on organization depends on the management

style of their organizations

the same the development if the bank is being occurred only for

the good management team.

Management of the UCBL controlling of all the resources of the

organization. To achieve the

ultimate objective of making UCBL the finest banking of the

country, the workforce will be

futuristic in outlook, professional in attitude and honest in

reputation. The board of directors

wants to repose in the management all executive powers to run

this service industry

administration and credit portfolio independently without any

undue influence from outside.

The board formulates policy and gives policy directives to the

management. Transparency

and accountability are strictly ensured at all leaves of the

bank. Bank operate with integrity,

competence and farsightedness abiding by all the principals and

provisions laid down in the

bank company act 1991, 1994 and the guidelines of Bangladesh

Bank. The bank is committed

to pursue a straight forward, upright legitimate banking

business, never be tempted by the

abnormal prospect of large returns to do anything. It will only

do what may be done under the

national policy.

-

8/3/2019 Bus 516-Case (Report)

7/58

.

7

Technology Perspective on Performance in United Commercial Bank

Ltd.

1.11. Customer Services and Automation of UCBL

To error human and forgiveness divines a proverb, the bank

believes but the customers will

not accept. Because for a service they pay for they want it 100%

defect free. So improvement

of the customer service should always be their motto altered

expectations of the customer

have shifted the focus from resource base productivity.

To operate in the globalize environment, the banks future plan

is to equip all the units of the

bank with the modern technology, such as online computer network

telex, fax, e-mail etc. for

the service of the customer round the clock, it has ATMs service

in different places in Dhaka

and other cities of the country. The Bank has also contract with

DBBL to use their ATMs

without any charge for better service of the customer and UCBL

provides Western Union

Money Service as well.

1.12. Social Commitment of United Commercial Bank Limited

The purpose of the banking business is, obviously, to earn

profit, but the promoters and the

equity holders of United Commercial Bank Ltd are aware of their

commitment to the society

to which they belong. A chunk of the profit is kept aside and/or

spent for socio-economic

development through trustee and in patronization of art; culture

and sports of the country and

the bank want to make a substantive contribution to the society

where we operate, to the

extent of our separable resources

1.13. Corporate Culture of United Commercial Bank Limited

This bank is one of the most disciplined Banks with a

distinctive corporate culture. Here we

believe in shared meaning, shared understanding and shared sense

making. Our people can

see and understand events, activities, objects and situation in

a distinctive way. They mould

their manners and etiquette, character individually to suit the

purpose of the Bank and the

needs of the customers who are of paramount importance to us.

The people in the Bank see

themselves as a tight knit team/family that believes in working

together for growth. The

corporate culture they belong has not been imposed; it has

rather been achieved through their

corporate conduct. The Bank achievement has been possible

because of the able leadership;

-

8/3/2019 Bus 516-Case (Report)

8/58

.

8

Technology Perspective on Performance in United Commercial Bank

Ltd.

dedicated and committed services provided by all levels of

management and staff which all

possible because of a good and quality full corporate

culture.

1.14. Main Services & Product Offerings

1.14.1. Consumer Banking:

UCB provide Mortgages, Credit Cards, Personal Loans, Auto Loans,

and Wealth

Management products. In order to maximize customer convenience,

they offer 24-

hour Phone Banking, eStatements, SMS Banking, ATM Cards and VISA

Debit Cards,

as well as Online Banking and state of the art branches.

1.14.2. Wholesale Banking:

Wholesale banking provides Transactional banking, Debt Capital

Markets, Corporate

Finance, Derivatives & Fx Options, Commodity Finance and

deposit products.

1.15. Customer

One of the most important tasks UCB has is to serve its

customers as specifically as possible

in terms of consultancy, sales and additional services, and, at

the same time, to operate

efficiently. The optimisation of costs in relation to income, or

cost-income ratio, is crucial

for UCB if they are to reap market success.

Where it seems sensible, UCB also orientate their strategy

towards the development of new

product and service areas. However, the prospects for rapid

growth are limited, since there

are few growth areas in the Technology field.

-

8/3/2019 Bus 516-Case (Report)

9/58

.

9

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Two-Competitor Analysis

-

8/3/2019 Bus 516-Case (Report)

10/58

.

10

Technology Perspective on Performance in United Commercial Bank

Ltd.

2.0 Competitors

2.1. CitiDirect

To gain more control over ones cash positions, one needs easy

access to accounts and

information in real time. One needs an application that is

easily customized by individual

users and streamlines day-to-day operations. One will need the

convenience of local banking

and the global solutions of an industry leader. The solution is

CitiDirect Online Banking.

The motto of CitiDirect is Money isnt everything but it can be

everywhere.

2.2. Eastern Bank Limited

Eastern Bank Limited Internet banking application addresses the

needs of small, individual

and corporate account holders of the bank. This application

provides a comprehensive range

of banking services that enable the customer to meet most of

their banking requirements over

the net. The transactions that are supported by the internet

banking provided by Eastern Bank

Limited are Account operations and Inquiries, Fund Transfers and

Payments, Utility Bill

Payments, Deposits, Loans, Session Summary etc.

2.3. Bank Asia

Bank Asia symbolizes modern banking with innovative services in

Bangladesh. It has

centralized Database with online ATM, SMS and Internet query

service. The significant

delivery channel of Bank Asia is the shared ATM Network. Bank

Asia has 21 ATMs as a

member ofETN along with eleven other banks. Bank Asia is

maintaining its competitiveness

by leveraging on its Online Banking Software and modern IT

infrastructure. It is the pioneer

amongst the local banks in introducing innovative products like

SMS banking, and under the

ATM Network the Stellar Online Banking software enables direct

linking of a clients

account, without the requirement for a separate account.

2.4. BRAC Bank

BRAC Bank deployed a layer of security system for its Internet

Banking. These measures

extend from data encryption to firewalls. BRAC Bank uses the

most advanced commercially

-

8/3/2019 Bus 516-Case (Report)

11/58

.

11

Technology Perspective on Performance in United Commercial Bank

Ltd.

available Secure Socket Layer (SSL) encryption technology to

ensure that the information

exchange between the customers Computer and BRACBank.com over

the internet is secure

and cannot be accessed by any third party. SSL has been

universally accepted on the World

Wide Web for authenticated and encrypted communication between

customers computers

and servers.

2.5. Arab Bangladesh Bank Ltd.

The first private bank of Bangladesh with a long standing

experience in domestic and

international banking. Its 153 branches in all the major

commercial centers of the country and

152 correspondents worldwide provide proficient banking services

to its customers.

2.6. HSBC

Business Banking Account enables a person to receive credit of

all the cash or cheque

deposits along with inward remittance and make all local

payments and provide access to the

wide range of services for the business requirements. A person

may deposit upto BDT50,000

cash per transaction and any BDT amount in cheque 24 hours a

day, 7 days a week through

the ATM Machines, conveniently located Sales and Service

Centers. EasyPay Machines are

also available for deposit of BDT 50,000 cash per transaction

and any BDT amount in cheque

to the Business Banking Account. With EasyPay Machines both HSBC

and Non-HSBC

customers can make deposits and pay their utility bills, credit

card payments and etc.

2.7. SCB

Standard Chartered offers the client a comprehensive range of

Cash Management services.

Whether it is a financial institution, a multi-national

corporation or a domestic company,

Electronic Banking application has the capability to support

full range of Cash Management

reporting and transaction initiation needs. It provides the

secure, reliable and effective link

between the client and clients accounts anywhere across the

Standard Chartered network.

Electronic Banking provides various types of support through a

wide range of operating

systems, sweeping transaction accessories with the provision of

reporting features or other

special functions. There are 10 offices and 50 employees under

this division, which operates

in 26 countries.

-

8/3/2019 Bus 516-Case (Report)

12/58

.

12

Technology Perspective on Performance in United Commercial Bank

Ltd.

2.8. Competitive Position of UCB

UCB has been rated A+ in long term and ST-2 in the short term by

credit rating information

and services limited based on the financials up to December 31,

2010 and other relevant

qualitative and quantitative information up to the date of

rating. Currently UCB is holding

10th position in the banking industry.

2.8.1. Rating Strengths

y Commendable improvement of asset quality in the recent yearsy

Steady growth in business (funded and non funded)y Efficient top

management teamy Management focus on implementation of modern risk

management practicesy Strong liquidity profile

2.8.2. Rating Concerns

y MIS & IT infrastructure require further improvementy

Inability to hold annual general meetings and pay dividends

-

8/3/2019 Bus 516-Case (Report)

13/58

.

13

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Three- Information System in UCB

-

8/3/2019 Bus 516-Case (Report)

14/58

.

14

Technology Perspective on Performance in United Commercial Bank

Ltd.

3.0. Information System in United Commercial Bank Ltd.

United Commercial Bank is one of the private commercial bank in

Bangladesh which was

more like other public banks that are technically unsound. By

evolving IT into the system, the

bank has positioned itself as a brand competing with other

foreign banks. Now, one can send

money from abroad using systems like Western Union, Moneygram

etc. Previously UCB had

to maintain data manually which is now auto generated through

customized software.

However, the bank still lack in various fields of operation

which can be resolved by IT

solutions.

As Time is money, and due to IS, UCB make thousands of

transactions per day. In fact, IS

makes whole process much more quick, simple and reliable. Due to

IS employees can easilyconnect with other branches, customer

service gets improved, online banking emerged and lot

of others benefits.

UCB Online is an innovative Online Banking service that one can

tailor to suit ones precise

banking needs. It gives one convenient, round-the-clock banking

services ranging from day-

to-day account transfer transactions to real-time valuable

financial information. Now one can

manage ones finances anytime, anywhere.

3.1. Organization Transaction Processing System

A Transaction Processing System (TPS) is a type of information

system. TPSs collect, store,

modify, and retrieve the transactions of an organization. A

transaction is an event that

generates or modifies data that is eventually stored in an

information system. From a

technical perspective, a Transaction Processing System (or

Transaction Processing Monitor)

monitors transaction programs, a special kind of programs. The

essence of a transaction

program is that it manages data that must be left in a

consistent state.

3.1.1.TPS in UCB:Effective transaction processing system is

working in UCB that offer enterprise the means to

rapidly process transactions to ensure the smooth flow of data

and the progression of

processes throughout the enterprise.

-

8/3/2019 Bus 516-Case (Report)

15/58

.

15

Technology Perspective on Performance in United Commercial Bank

Ltd.

3.1.2.Payroll TPSIn UCB payroll TPS is designed to get

information and record of the employ and then to

calculate his/her annual earning.

It get information about the employee from the employees

department and from general

ledger and send it to payroll TPS from where it links that

information with the previous

record and prepare a report which is forwarded to management.

Management takes notice the

LN record of the employees efficiency to work and may declare

added bonus or other

incentive. This report is checked and approved by the branch

manager after which check is

issued to the employee. And when that check is cashed, the

record is updated in the general

ledger as well as the master payroll (HUB).

3.1.3. Customer Identification

In UCB there is their own information management named software

Virses is working

which is connected to NADRA. So if any new client wants to open

an account in the bank the

system automatically send a request to NADRA to check and verify

the customer ID number.

Which helps the management to identify whether he/she is using

his original ID card or not.

Employee Data

General Led er

Payroll TPS

Payroll Master

File (HUB)

Management Reports

Check Passes

by Manager

Check Issued to

GeneralLedger

-

8/3/2019 Bus 516-Case (Report)

16/58

.

16

Technology Perspective on Performance in United Commercial Bank

Ltd.

Input

(ID #)

Virses

Management

HUB

NADRA

(Customer identification)

Employee Job Login

Biometric Device

& LN

HUBEmployee Job

Logout

3.1.4. Employees Record

All employees are supposed to login when they enter the bank and

logout on leaving, by

tracing their thumb impressions on biometric device. This device

is connected with the HUB

which continuously makes record of their hours spent in the

bank. Moreover, the bank has

their own setup named LN which makes records of all the

transactions made by an

employee. This would help management to monitor the working

efficiency of an employee.

-

8/3/2019 Bus 516-Case (Report)

17/58

.

17

Technology Perspective on Performance in United Commercial Bank

Ltd.

Customer Queries Customer Service TPSIdentify

Problem

Send to Concerned

De t.

Account

Alert

Management

Advices Send to Customer

Customer Service TPS

HUB

3.1.5. Online Complains:

UCB allows the customer the option of online complains. The

customer submits the online

complain which is then processed by Customer Service TPS which

is linked by management

and after the problem identification it is send to the concerned

department.

3.1.6. Advices:

As all of the record of the customers are stored in main server

(HUB) of UCB, so incase if

someone account balance is getting near to zero the system

automatically alert the

management about that. Then manager take manual action and send

him/her the advice (a

letter, mail or phone call) to check the account balance.

-

8/3/2019 Bus 516-Case (Report)

18/58

-

8/3/2019 Bus 516-Case (Report)

19/58

.

19

Technology Perspective on Performance in United Commercial Bank

Ltd.

3.1.9. ATM Card

Purpose: Easy with draw of cash.

Input: Give bio data, income summary, company name, NIC.

Process: NIC no. and bio data send to virses which directly

linked to NADRA. If

information is correct then it is forward to customer service

centre.

Output: Issue of credit card.

Nevertheless, a management information system is a system or

process that provides the

information necessary to manage an organization effectively. MIS

and the information it

generates are generally considered essential components of

prudent and reasonable business

decisions.

Applicant Identification

Virses

A/C Dept.

Customer Service TPS

HUB

New A/C Opened

ATM Issued

-

8/3/2019 Bus 516-Case (Report)

20/58

-

8/3/2019 Bus 516-Case (Report)

21/58

.

21

Technology Perspective on Performance in United Commercial Bank

Ltd.

4.0 Business process model:

The business process model of United Commercial Bank Ltd. Shows

how different activities

take place in different division along with the process of the

whole business.

However, UCB business process model includes the Secondary

activity and Primary activity

which generates the ultimate value of the organization. The

primary activity includes the

primary functioning of the bank, like-General Banking,

Credit/Advance, Foreign Exchange,

Retail Banking, Priority Banking, and Foreign Remittance and so

on. On the other hand the

secondary activities includes the administrative work of a bank,

like HRM, IT, Accounts etc.

General

Banking

Foreign

Remittance

Credit/

Advance

Retail

Division

Organization

Value ChainComputerized Ordering System

Technology Development

HRM

Administration and Management

Foreign

ExchangePrimary

Activities

Secondary

Activities

-

8/3/2019 Bus 516-Case (Report)

22/58

.

22

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Five-Softwares used in Different Business Process

-

8/3/2019 Bus 516-Case (Report)

23/58

.

23

Technology Perspective on Performance in United Commercial Bank

Ltd.

5.0 Softwares used in different business process:

5.1. PCBank2000

5.1.1 Deposit: All institutional and individual deposit

services, including account opening,

deposit/withdrawal, account closing, lose reporting and account

management etc.

5.1.2 Loan: All round support to the bank credit business, such

as advance, interest

deduction, renewal, collection,

automatic payment etc. Flexibly

support institutional and

individual loan services:

commission loan, acceptance

bill, packing loan, Bill advance

etc.

5.1.3 Discount: Including the

disposal of ordinary discount,

-

8/3/2019 Bus 516-Case (Report)

24/58

.

24

Technology Perspective on Performance in United Commercial Bank

Ltd.

inter-bank discount, rediscount, discount withdrawal etc.

5.1.4 Borrowing: Including the disposal of internal borrowing in

the system and exterior

borrowing beyond the system.

5.1.5 Investment business: Short term investment, long term

investment; arrange accounts

according to the bonds type, and set up registration book for

inquiry and management.

5.1.6 Term-end business:

Including deposit and loan

interest calculation and

deduction, income transfer,

profit allocation, tax

calculation etc.

5.1.7 Client management:

Including client information

management, client accounts

management, client credit

management etc

5.2 Western Union

Its a software program with 2 features which can be used

separately for your needs.

5.2.1 MTCN scanner: is searching for active transactions which

correspond with clients

criteria (country and amount) or through MTCN which can lead to

the next feature.

5.2.2 MTCN tracking:MTCN or the name of sender / beneficiary,

will find all the details

which correspond searching, this would track the full list about

a specific transaction (full

name and country of sender and beneficiary, amount and

MTCN).

-

8/3/2019 Bus 516-Case (Report)

25/58

.

25

Technology Perspective on Performance in United Commercial Bank

Ltd.

5.3. UCB Remit

5.3.1. Remit Out Form:

Save senders Name address and ID checked and date of ID Checked.

Reminds instantly for date for ID Check Save Receivers names for

each sender Allow to send transfer through any network Saves

collection points address for each network Generate security

code at random

-

8/3/2019 Bus 516-Case (Report)

26/58

.

26

Technology Perspective on Performance in United Commercial Bank

Ltd.

5.3.2. Receipt for Customer:

Pints Duplicate Receipt on normal paper and normal printer one

for customer andother for office copy.

Shows Sender Account No and details Shows Calculation and

Outstanding amount if any Show Address of Collection Point or Bank

Brach address Show Receivers details

5.3.3. Instruction for Payments

Generates report instruction formoney transfer payments

abroad

Different styles with respect toorientation and columns to

be

included

Can be exported to MS ExcelFormat or MS Word Format

Can be email with one click

-

8/3/2019 Bus 516-Case (Report)

27/58

.

27

Technology Perspective on Performance in United Commercial Bank

Ltd.

5.4. Credit Card Bill Collection System

Credit Card billing system includes:

y Interest calculations y Processing of bill payments and cash

withdrawal using card chequey Processing of cheques, card etc.y

Customer managementy Customer account

management

-

8/3/2019 Bus 516-Case (Report)

28/58

.

28

Technology Perspective on Performance in United Commercial Bank

Ltd.

5.5. BACPS (Bangladesh Automated Cheque Processing System)

5.5.1. Payment interface:The direct connection with macro/micro

payment system realizes

remittance and cashing, inter-bank transaction, real time

transfer.

5.5.2. Internal clearing:Regulate and manage the cash position

in a real time way; realize

inter-bank settlement, cash pooling and borrowing; and support

automatic settlement and

clearing.

-

8/3/2019 Bus 516-Case (Report)

29/58

.

29

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Six- Growth in Internet Banking

-

8/3/2019 Bus 516-Case (Report)

30/58

.

30

Technology Perspective on Performance in United Commercial Bank

Ltd.

6.0 Growth in Internet Banking

Numerous factors including competitive cost, customer service,

and demographic

considerations are motivating banks to evaluate their technology

and assess their electronic

commerce and Internet banking strategies. The challenge is to

make sure the savings from

internet banking technology more than offset the costs and risks

associated with conducting

business in cyberspace. Some of the market factors that may

drive a banks strategy towards

internet banking include the following:

6.1. Competition: The competitive pressure is the chief driving

force behind

increasing use of internet banking technology, ranking ahead of

cost reduction and

revenue enhancement. Banks see internet banking as a way to keep

existing customers

and attract new ones to the bank.

6.2. Cost-efficiencies: Banks can deliver banking services on

the internet at

transaction costs far lower than traditional ways. The actual

costs to execute a

transaction will vary depending on the delivery channel used.

These costs are

expected to continue to decline.

6.3. Geographical Reach: Internet Banking allows expanded

customer contact

through increased geographical reach and lower cost of delivery

channels. In fact

some banks are doing business exclusively via the internet they

do not have

traditional banking offices and only reach their customers

online.

6.4. Branding: Relationship building is a strategic priority for

most banks. Internet

banking technology and products can provide a means for banks to

develop and

maintain an ongoing relationship with their customers by

offering easy access to a

broad array of products and services. By capitalizing on brand

identification and by

providing a broad array of financial services, banks hope to

build customer loyalty,

and enhance repeat businesses.

6.5.Customer Demographics:Internet banking allows banks to offer

a wide array of

options to their banking customers. Some customers will rely on

traditional branches

to conduct their banking business. Other customers are early

adopters of new

technologies that arrive in the marketplace. The challenge to

banks is to understand

-

8/3/2019 Bus 516-Case (Report)

31/58

.

31

Technology Perspective on Performance in United Commercial Bank

Ltd.

their customer base and find the right mix of delivery channels

to deliver products and

services profitably to their various market segments.

As use of the internet continues to expand, more banks are using

the web to offer

products and services or otherwise enhance communications with

consumers. The

internet offers the potential for safe, fast, and convenient new

ways to shop for

financial services and conduct banking business, any day, any

time.

-

8/3/2019 Bus 516-Case (Report)

32/58

.

32

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Seven- SWOT Analysis

-

8/3/2019 Bus 516-Case (Report)

33/58

.

33

Technology Perspective on Performance in United Commercial Bank

Ltd.

7.0 SWOT Analysis:

7.1. Strength

y In UCB online banking is fully automated.y Although first

generation bank, keeping pace with the modern industry trend

than

others.

y Prompt service, hence percentage ofcustomers waiting is less

than a given fixed time.

7.2. Weakness

y Limited skilled human resourcesy Employee base has low-level

of computer literacyy Less investment in Information Technology and

looking for last mile solution. IT

employment was done partly because of lack of fund and

knowledge

7.3. Opportunities

y The internet services are becoming very common to us. So a

service offered throughthe internet will be widely accepted in the

near future. Hence the overhead costs

would decrease and increse profit of the bank.

y Better and improved IT solutions that would ease banking

transaction even more.

7.4. Threat

y High cost associated with IT deploymenty In the field of IT

new technology is coming everyday. The one which is very

popular

today might get obsolete tomorrow. So to have a competitive edge

over the

competitors UCB must always update their services.

-

8/3/2019 Bus 516-Case (Report)

34/58

.

34

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Eight- Proposed Changes: Technology in Business

-

8/3/2019 Bus 516-Case (Report)

35/58

.

35

Technology Perspective on Performance in United Commercial Bank

Ltd.

United C mmercial Bank Ltd

8.0. Proposed Changes: Technology in Business

Technology in the business will give the general idea about

technology in the banking sector,why it is used and how to produce

it.

8.1. Only Electrons move in the Bank

Although banks still use paper and fax a lot to make work happen

efforts are now afoot to

reduce this. Paper is currently still used to pass work in

progress from one department or

building to another. Many of the documents that are faxed /

moved are produced by systems

internal to the bank. Printing, manual handling and

thenre-keying data is high cost and

banks are enhancing their use of email and intranets, already

universally available to bank

staff, to drive this cost out.

Documentation required from a source external to the bank from

what we can see, will be

captured as an image at the first point of entry to the bank and

then filed with either a

customer or account record. Apart from eradicating manual

handling, the use of images

Technology

Management

Politics and corruption,

Organizational Culture

Competencies:Use of technology

Cost effectivenessTechnical Capability

Competencies:Hierarchy

FlexibilityEmployee selection

Performance Affects

Performance

-

8/3/2019 Bus 516-Case (Report)

36/58

.

36

Technology Perspective on Performance in United Commercial Bank

Ltd.

allows multiple departments to see the entire file (e.g. for a

loan application) at the same

time, hence speeding up processing by allowing activities that

previously had to be serial, to

run in parallel.

8.2. Simple CRM for Customer Contact

Customer Relationship Management (CRM) as a phrase ended up

covering a vast plethora of

business ideas from sales pipeline management through to complex

analytics on call routing.

Given the very large customer bases that banks have, with

significant variations in customer

behaviours and preferences it is inevitable that a given service

proposition will have to be

supported through a number of delivery channels. As a

consequence many banks are seeking

to maintain a record of customer interactions, particularly for

service, that is independent of

delivery channel; i.e. outside the branch, call centre, and

product processing centre.

8.3. All Forms will be filled in Electronically, Preferably by

the customer

Much of the documentation that moves within a bank and between a

bank and its customers

are paper forms. The ambition for many banks is to see every

customer form available on the

Internet. If a customer fills in a form via the internet/Email

there are great benefits. Software

can sift the customer keyed data and input it into core systems

(A/C opening, credit

applications) and so avoid bank staff having to key data; and

the customer should never get

faced with an out of date form.

Customer signatures would still is required in many cases

(although digital certificates might

alleviate this) and the customer would have to print and sign a

version of the form, which

would get mailed to the bank as follow up (and probably scanned

in as an image).

UCB can also apply the same ideas to internal forms. The aim is

for bank staff to retrieve

them from the intranet, key them and Email them.

8.4. Legacy Software will be an Important Design Point

We have not heard of anyone in a branch based bank saying lets

design our processes as if

branches dont exist, and the reason is that it is such a large

part of the current state of the

-

8/3/2019 Bus 516-Case (Report)

37/58

.

37

Technology Perspective on Performance in United Commercial Bank

Ltd.

bank that it has to be a major consideration. In many respects,

the legacy software base is as

large an investment as the branch network.

8.5.Web Browser to bring together lots of systems on the

desktop

Currently a member of staff in a branch or call centre can only

access a limited number of the

banks product engines. For example they might be able to logon

to the Bank Customer

Accounting system to access current and savings account details

but not be able to access the

groups mortgage, credit cards or insurance systems. The

principal reason for this is the

technical incompatibility of the different product engine

systems. Banks are increasingly

standardising on web browser interfaces to all systems and hence

opening up the opportunity

to allow staff to carry out work (e.g. customer service work)

across a wider range of products

than was hitherto possible.

-

8/3/2019 Bus 516-Case (Report)

38/58

-

8/3/2019 Bus 516-Case (Report)

39/58

.

39

Technology Perspective on Performance in United Commercial Bank

Ltd.

9.0 Information Communication Technology (ICT) Policies

In Bangladesh decision makers are generally reluctant about

advancement of technology. If

Govt. doesnt take proper incentives to spread the

computerization process then there will be

no benefit. The parliamentary members of the country must be

aware of the benefits of

Information and Communication Technology (ICT) otherwise it can

not be successful. It

wont bring any dramatic changes in the economy. Entrepreneurship

Development fund

(EDF) of Bangladesh bank is should be utilized properly.

However, the government has formulated a policy on the national

information and

communication technology as part of its announced plan for

digitization of the nation. The

policy has earmarked activities in three phases in the short,

medium and long-term plans to be

implemented within 2021.

The first step towards automation started with the launching of

the Bangladesh Automated

Clearing House (BACH) in 2010. Funded by UK Department for

International Development,

BACH replaced the physical movement of cheques to the clearing

house through image

based transfer of cheques to the central bank.

This shows the intention of Bangladesh Bank to the betterment of

the services. This will

eventually lead to internet banking to a requirement for all

banks in the near future. With all

the strategies we have set for us we can enter into a new world

of internet banking.

The Ministry of Science, Information and Communication

Technology has given out the

policy for the development in the IT sector. The ministry has

concentrated on the following

sections:

y Human Resources Development through Education and Trainingy

ICT Infrastructure developmenty Research and Development in ICTy

Development of ICT Industryy Development ofE-Commercey E-Government

/ E-Governance establishmenty Establishment of Legal Issues

-

8/3/2019 Bus 516-Case (Report)

40/58

.

40

Technology Perspective on Performance in United Commercial Bank

Ltd.

The Government spending in ICT is going to increase by at least

2% of ADP in coming

years. The new budget provision encouraged the investment in the

application of ICT in trade

and finance. The ICT companies will get preferential terms which

will be able to meet up

20% of its revenue expenditure. BCC has created a centralized

fund for R&D which would

encourage contributing 1% of all profits from ICT-enabled

services to the HRD fund. This

will greatly help the development if ICT in Bangladesh. The

software support for internet

banking, i.e. FLEXCUBE is available in Bangladesh. Again

Bangladesh Government is

working on the copyright law and the preservation of

intellectual property act. After the

successful implementation of all these policies and strategies

we are expecting that more than

50% of the banks will be offering internet banking facilities

which is now 12% only.

Another important issue in extending the internet banking

services throughout the country is

gaining popularity. The sense of security is of great importance

Regulatory issues relating to

security measures of electronic banking can be improved through

the following ways:

a) Analyzing the potential risks in the electronic payments

systems;

b) Existence of tradeoff between the efficiency of the financial

system and the amount

of risk incurred;

c) Competitive pressures that may encourage the banks to engage

in competitive

deregulation;

d) Effective provision and arrangement for cryptography and its

applications;

e) More customers are willing to accept e-business as

psychological patterns of the

customers have been changing.

-

8/3/2019 Bus 516-Case (Report)

41/58

.

41

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Ten- The Supporting IT Infrastructure

-

8/3/2019 Bus 516-Case (Report)

42/58

-

8/3/2019 Bus 516-Case (Report)

43/58

.

43

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Eleven- The Proposed IS model in UCB

-

8/3/2019 Bus 516-Case (Report)

44/58

.

44

Technology Perspective on Performance in United Commercial Bank

Ltd.

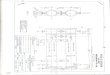

CORE

11.0 The Proposed IS model in UCB: Long-Term Decision

Manking

The IS model

11.1 System description

The proposed system is a modular system. Individual modules can

be freely combined

according to the specifi c needs of the bank or payment

provider. Additional modulesncan be

added gradually as needed by the client or when the client

becomes ready for

implementation. This flexibility makes it possible to start with

a set of key modules and to

continue step-by-step up to the complete coverage of company

processes.

All modules share a common central database. All data is kept in

the database in singular

form with no duplication or replication necessary. This ensures

data consistency and effi

ciency.

-

8/3/2019 Bus 516-Case (Report)

45/58

.

45

Technology Perspective on Performance in United Commercial Bank

Ltd.

11.2. CORE

The core module is the main building block providing the

functionality for accounts,

transactions and the audit trail. The module defines the core

data structures used by all other

modules. The core module is required in all implementation

scenarios except when a bank

wants to use its own legacy system and use just the Internet and

Mobile Banking modules.

11.3. WebOffice

The system weboffice allows remote mode of work using the

light-weight intra/internet

application.The application is optimized for high performance

even on slower connection

lines which makes it ideal for external users like third-party

outsourcing partners (call

centers, bank agent networks), or other business partners. As

security is a big concern, the

authentication of users adheres to the highest security

requirements and all communication is

encrypted

11.4. Module for Term Deposits and Loans

The module administering term deposits and loans automates the

lifecycle of various types of

term deposits and loans and projects the fi nancial aspects of

term deposits and loans into the

G/L.

11.5. Module for Payment Card Administration

The payment card administration module administers communication

with payment card

production and the processing company. The card branches and the

types of the payment

cards are fully customizable.

The module exports in batches all requests for new plastic cards

and provides support for the

export of payment card balances and limits and the import of

card authorizations and settled

transactions. All information concerning card authorizations and

transactions becomes an

integral part of the core transactions, which enables the

incorporation of it into the

consolidated account statements and a detailed overview of

payment card history.

11.6. Statements and Reports Module

The reporting module allows for the defining of complex

consolidated account statements

and virtually any reports from the data kept in the central

database.

-

8/3/2019 Bus 516-Case (Report)

46/58

.

46

Technology Perspective on Performance in United Commercial Bank

Ltd.

11.7. e-Commerce Module

The e-Commerce module provides B2C and B2B functionality. The

module exposes

automated secured Internet XML interfaces allowingm eShops to

automate ePayments for

their tangible and non-tangible goods and services. The

interface allows both single

individual payments and combined payments stemming from

microPayments.

11.8. Communication Modules

The module provides a versatile communication allowing the defi

nition of formats and

contents for the import and export of any data from the central

database. Once configured, the

communication via batch data files can be fully automated or

manually controlled. The rich

operation reports allow the monitoring of the smooth processing

and provide prompt

notification of potential problems.

11.9. Internet Banking Module

The Internet Banking provides bank clients with a secure,

efficient, flexible and fully confi

gurable interface to all banking products and services. The

graphic design, menu structure,

supported languages and integration with the core banking system

is fully customizable. The

products and services exposed by the Internet Banking module

range from a standard banking

portfolio to state-of-the-art electronic payment or microPayment

tools.

11.10. Multi-Generation Mobile Banking

The system comes with a wide range of mobile banking

technologies using a broad set of

GSM technologies allowing clients to communicate with the bank

anytime from anywhere in

their preferred manner. All information exposed via ARBES OBS

Mobile Banking comes

directly from the core database; the active operations are sent

directly to the core banking

system for immediate processing.

-

8/3/2019 Bus 516-Case (Report)

47/58

.

47

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Twelve- Investment Forecast & Return on

Investment

-

8/3/2019 Bus 516-Case (Report)

48/58

.

48

Technology Perspective on Performance in United Commercial Bank

Ltd.

12.0 Investment Forecast & Return: NOPAT

Cash flows from investing activities 2011 2010

Payments for purchase of securities (893,752,343)

124,808,388

Investment in IT (258,954,622) -

Acquisition of Other Fixed Assets (539,494,343) 393,731,611

Proceeds from sale of fixed assets 1,780,052 2,109,821

Net cash ouflow from investing activities (1,69

0,42

1,256) (5

16,43

0,1

78)

NOPAT 2011 2010

Net interest Income 3,835,360,138 2,617,086,773

Investment income 1,972,538,276 963,452,759

Other operating income 5,807,898,414 3,580,539,532

Total operating income (A) 7,854,634,893 5,192,054,616

Total operating expenses (B) (3,122,306,942) (2,066,885,136)

Net income before provision (C) = (A-B) 4,732,327,951

3,125,169,480

Total Provision (D) (1,100,529,879) (1,583,304,987)

Net income before Tax (C-D) 3,631,798,072 1,541,864,493

Provision for Tax (1,450,162,647) (608,966,603)

Net profit after tax (NOPAT) 2,181,635,425 932,897,890

-

8/3/2019 Bus 516-Case (Report)

49/58

.

49

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Thirteen- Decision Analysis

-

8/3/2019 Bus 516-Case (Report)

50/58

.

50

Technology Perspective on Performance in United Commercial Bank

Ltd.

13.0 Decision Analysis

The use of appropriate software systems constitutes an important

pillar of banking operations.

Besides the use of suitable software, what is critical for banks

commercial success is that

different applications and processes should be well integrated,

and that users should actually

accept and deploy them in practice. Naturally, good software

systems cannot guarantee

success on their own. But they are able to make a significant

contribution.

13.1. Increase Employee Confidence and Motivation

Using a new banking system can be scary and intimidating for

employees at a financial

institution, as they are directly responsible for using it on a

daily basis. In order to properly

use the system and accurately process transactions, employees

must first have an introduction

to what it is and a clear understanding of how to use it.

By receiving proper training, associates will practice and learn

all aspects of the system in a

self- paced, safe and non-threatening learning environment that

looks and feels like the real

system.

Through the use of motivating, challenging and interactive

content, activities, exercises and

hands-on practice of system functionality, employees will be

more confident about using the

new system. These interactive exercises will enable employees to

gain a new understanding

of their job responsibilities and will equip them with the

knowledge and skills that they need

to excel in performing their tasks every day.

Providing training that is customized to each job position at

the bank will also help

employees to feel confident about using the new system on a

daily basis. Targeted,

comprehensive and customized training will help employees in

every area of the bank to

confidently and efficiently use any system out there.

13.2. Maintain Customer Experience

During the conversion to a new system, it is important to keep

every customer's banking

experience consistent. Financial institutions should conduct a

seamless transfer to a new

system while maintaining an optimal customer experience.

Customers should not be able to

-

8/3/2019 Bus 516-Case (Report)

51/58

.

51

Technology Perspective on Performance in United Commercial Bank

Ltd.

sense that a transition at their bank is even occurring, or be

able to notice any bumps in the

road during the transfer.

System Simulation Training produces knowledgeable, proficient

employees who provide

reassurance to customers who will return based on their positive

experiences at the bank. If

customers are continually satisfied with their banking

experience they will likely tell their

family and friends, resulting in even more business for the

bank.

13.3. Reduce Risk

Training for employees on the new banking system provides

numerous benefits, including

reducing risk at the bank. Knowledgeable and confident employees

will make fewer mistakes

and costly errors. And unlike classroom training, each session

is identical so you can be

confident in the consistency of the training. A team of

employees who are all receiving

consistent, quality training will help to make the conversion to

a new system seamless and

risk-free.

-

8/3/2019 Bus 516-Case (Report)

52/58

.

52

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Fourteen- Cost-Benefit Analysis:

-

8/3/2019 Bus 516-Case (Report)

53/58

.

53

Technology Perspective on Performance in United Commercial Bank

Ltd.

14.0. Cost-Benefit Analysis:

Information Technology (IT) is important to reduce the long-term

cost and save time whendealing with services. It also helps to

drive the countrys economy because banking sectors

development has a relation with economic development. Few

traditional business companies

philosophy about IT is a pressure of implementation and

investment. It also problem about

managing and allocation of the responsibility when change

management system required by

the organization. Traditional bank management psychologically

feel burden to organize IT as

a strategy.

Though the solution will require a higher initial investment,

the operating expenses will be

much lower However, IT reduces the companys long-term cost;

again customers will be

satisfied through fast, accurate, easy-to-use, comprehensive

delivery of the services. So a

complete IS solution will be much more beneficial to UCB as well

as customers.

-

8/3/2019 Bus 516-Case (Report)

54/58

.

54

Technology Perspective on Performance in United Commercial Bank

Ltd.

Chapter Fifteen- Conclusion

-

8/3/2019 Bus 516-Case (Report)

55/58

.

55

Technology Perspective on Performance in United Commercial Bank

Ltd.

15.0. Concluding Remarks

United Commercial Bank Ltd is under pressure from the forces of

globalisation to adopt IT in

order to fit into the evolving global banking system. So the

motivation is principally that of

survival. The current level of investment in and implementation

of IT is not impressive, and

very few banks can claim to have realised some of their

expectations in investing in IT.

However, in order to offer its customers the best services

available, banks and financial

institutions need to stay up-to-date on the newest technologies

available, no matter what the

cost. However, regardless of how advanced, high-tech or costly

these systems are, they will

fail without proper training for employees. In order for a

financial institution to get its

money's worth and reap the many long-term benefits that these

systems can provide, Systems

Simulation Training is the obvious choice.

-

8/3/2019 Bus 516-Case (Report)

56/58

.

56

Technology Perspective on Performance in United Commercial Bank

Ltd.

References:

y Andersen, T. J., (2001) Information Technology, Strategic

decision makingapproaches and organizational performance in

different industrial settings, journal of

strategic information system, Vol. 10, pp. 101-119

y Alexander, D. & Chistropher, N (2010) Financial

Accounting: An internationalintroduction, pp.1-477, 4ht Edition,

Pearson Education, UK

y Asian Development Bank, (2009) Restructuring state own

financial institutions:lessons from Bank Rakyat Indonesia,

Philippines, pp. 1-35

y Bauman, P., Bauman, C. & Hasley, R. F., (2000) Do Firms

Use the Deferred TaxAssetValuation Allowance to Manage Earnings?,

Working Paper Series, JEL

Classifications: M41, M43, M44, K22, pp.1-41,Available at

SSRN:

http://ssrn.com/abstract=239054 ordoi:10.2139/ssrn.239054,

USA

y Banker, R. D. & Kauffman, R. J. (1988) Strategic

Contributions of InformationTechnology (IT): an empirical study of

ATM networks, Center for Research on

Information Systems, pp. 1-22, New York

y Basel Committee on Banking Supervision (BCBS) (1999) Enhancing

CorporateGovernance for

y Banking, Risk Management Group of Basel committee on Banking

Supervision, pp.1-11

y Performance: An International Comparison, Office of the

Comptroller of theCurrencyn Economics Working Paper Beck, T,

Demirgu Kunt, A., & Levine,

R.(2006) Bank concentration, competition and crises: First

results , Journal of

Banking & Finance 30 , pp.15811603

y Berger, A. & Hannan,T.,1998.The efficiency cost of market

power in the bankingindustry: A test of the quiet life and related

hypotheses. The Review ofEconomics

and Statistics 80,pp. 454465.

y Berger and Humphrey (1997) provide a detailed review of the

literature on bankingefficiency, which is also updated by Bergerand

Mester (2003).

-

8/3/2019 Bus 516-Case (Report)

57/58

.

57

Technology Perspective on Performance in United Commercial Bank

Ltd.

y Binter, M. J., Ostrom, A.L., &Meuter, M. L. (2002)

Implementing successful self-service technologies, Journal of

Academy of Management Executive, Vol.16, No. 4

Blumberg, B., Cooper, D. R., & Schindler, P. S., (2008)

Business research Method,

2ndede. Uk

y http://h71028.www7.hp.com/enterprise/downloads/iflex_sb.pdfy

http://www.bccbd.org/html/itpolicy.htmy

http://www.bttb.net/bttb_home_ddn_rate.htm).y

http://www.theage.com.au/news/Breaking/Bangladesh-net-users-cross-y

1m/2005/04/29/1114635721380.html?from=moreStories&oneclick=true)y

http://www.fnc.gov/Internet_res.htmly

http://www.it.iitb.ernet.in/~sriy

http://info.isoc.org/internet/history/brief.html

-

8/3/2019 Bus 516-Case (Report)

58/58

.

Technology Perspective on Performance in United Commercial Bank

Ltd.

APPENDIX