Embed Size (px)

Citation preview

BULGARTABAC – HOLDING AD INTERIM SAPARATE FINANCIAL STATEMENTS FOR THE RERIOD ENDED 30 MARCH 2016

Bord of directors :

Chairman Vencislav Cholakov Deputy chairman Miglena Hristova Member of the BD Radoslav Rahnev Executive director Radoslav Rahnev

Chief legal adviser Svetlana Marteva Chief accountant Stratiya Stratiev

Address of managment Sofia city 62, Graf Ignatiev str.

Bankers Citibank Europa AD, Bulgaria branch UniCredit Bulbank AD Fibank AD

Auditor Deloitte Audit EOOD

Bulgartabac-Holding AD

INTERIM SEPARATE STATEMENT OF COMPREHENSIVE INCOME for the period 1 January - 31 March 2016

31 March 2016 31 March 2015 BGN '000 BGN '000

Revenue 11 532 13 582Dividend income from subsidiaries - - Other operating gains and losses 392 263Changes in stock of finished products - - Costs of materials (917) (896) Personnel expenses (2 011) (2 519) Depreciation / amortisation expenses (433) (455) Costs of hired services (7 965) (7 141) Book value of goods sold (291) (9) Reversed/(Accrued) impairment of assets, net (76) (75) Other operating expenses (663) (673) Operating profit (432) 2 077

Investment income and losses (28) 135Finance costs (2) (111) Profit before income tax (462) 2 101

Income tax benefit/(expense) - (210) Net profit for the period (462) 1 891

Components not to be subsequently reclassified in profit or loss:

Actuarial gains/(loss) from long-term payables to personnel - - Taxes on other comprehensive income - - Other comprehensive income - -

Total comprehensive income for the period (462) 1 891

Basic earnings per share (BGN) (0,06) 0,26

25 April 2016

Executive Director: Chief Accountant:(preparer)

(Vencislav Cholakov) (Stratiya Stratiev)

The interim separate financial statements shall be read together with the notes, which are an integral part of these financial statements.

1

Bulgartabac-Holding AD

INTERIM SEPARATE STATEMENT OF FINANCIAL POSITIONas at 31 March 2016

BGN '000 BGN '000

ASSETSNon-current assets Property, plant and equipment 13 425 12 784 Intangible assets 2 367 2 453 Investment property 456 456 Investments in subsidiaries 37 635 37 635 Investments available for sale 100 100 Long-term receivables from related parties 782 526 Deferred tax assets 59 59 Other non-current assets 680 819

55 504 54 832

Current assets Inventories 2 094 1 788 Receivables from related parties 27 384 28 391 Trade and other receivables 17 569 15 812 Corporate income tax refundable 228 343 Other current assets 1 218 1 005 Cash and cash equivalents 9 843 9 059

58 336 56 398

TOTAL ASSETS 113 840 111 230

EQUITY AND LIABILITIES

EQUITY Share capital 7 367 7 367 Statutory reserve 737 737 Revaluation reserve 4 228 4 228 Retained earnings 84 725 85 187 Total equity 97 057 97 519

LIABILITIESNon-current liabilitiesLong-term payables to financial entities 416 - Retirement benefit obligations 236 229

652 229

Current liabilitiesShort-term payables to financial entities 18 26 Payables to related parties 2 655 1 606 Trade and other payables 10 973 9 634 Payables to personnel and for social security 2 485 2 216

16 131 13 482

TOTAL LIABILITIES 16 783 13 711

TOTAL EQUITY AND LIABILITIES 113 840 111 230 - -

25 April 2016

Executive Director: Chief Accountant:(preparer)

(Vencislav Cholakov) (Stratiya Stratiev)

31 March 2016 31 December 2015

The interim separate financial statements shall be read together with the notes, which are an integral part of these financial statements.

2

Bulgartabac-Holding AD

INTERIM SEPARATE CASH FLOW STATEMENT for the period 1 January - 31 March 2016 31 March 2016 31 March 2015

BGN '000 BGN '000

Cash flows from operating activityCash receipts from customers 16 352 14 035 Cash paid to suppliers (11 257) (10 664) Dividends received from subsidiaries 110 798 Cash paid to employees and for social security (2 191) (3 136) Taxes paid (other than corporate income tax) (1 780) (1 520) Loans to related parties (55) - Loans repaid by related parties 110 - Donations and sponsorship (55) (110) Bank charges paid (6) (3) Other (payments)/proceeds, net (294) (142) Net cash flows used in operating activity 934 (742)

Cash flows from investing activityProceeds from sale of investments - 910 Purchases of property, plant and equipment (133) (16) Proceeds from sale of property, plant and equipment - 1 Purchases of intangible assets - (50) Interest received on deposits granted 2 - Net cash flows (used in)/from investing activity (131) 845

Cash flows from financing activityLoans repaid (8) (21) Dividends paid (4) (1) Net cash flows used in financing activity (12) (22)

Net change in cash and cash equivalents 791 81

Cash and cash equivalents at 1 January 9 059 9 113 Effect of foreign currency translation of cash and cash equivalents (7) (26)

Cash and cash equivalents at 31 December 9 843 9 168

25 April 2016

Executive Director: Chief Accountant:(preparer)

(Vencislav Cholakov) (Stratiya Stratiev)

The interim separate financial statements shall be read together with the notes, which are an integral part of these financial statements.

3

Bulgartabac-Holding AD

SEPARATE STATEMENT OF CHANGES IN EQUITY

for the period 1 January - 31 March 2016 Share capital

Statutory reserve

Revaluation reserve

Additional reserves

Retained earnings Total equity

BGN'000 BGN'000 BGN'000 BGN'000 BGN'000 BGN'000

Balance on 31 December 2014 (audited) 7 367 737 5 105 82 712 95 921

Net profit/(loss) for the period 01.01 - 31.03.2015 - - - - 1 891 1 891

Other comprehensive income - - - - - -

Other changes in equity - - - - - -

Total comprehensive income for the period 01.01 - 31.03.2015 - - - - 1 891 1 891

Balance on 31 March 2015 7 367 737 5 105 - 84 603 97 812

Distribution of profit for: (30 942) (30 942) * dividends (30 942) (30 942)

Net profit/(loss) for the period 01.04 - 31.12.2015 - - - - 30 885 30 885

Total other comprehensive income - - - - (82) (82) * effect of actuarial gains and losses - - - - (82) (82) * taxes on other comprehensive income - - - - - -

Other changes in equity - - - (877) 723 (154)

Total comprehensive income for the period 01.03 - 31.12.2015 - - - (877) 584 (293)

Balance on 31 December 2015 7 367 737 5 105 (877) 85 187 97 519

Distribution of profit for: - - - - - -

Net profit/(loss) for the period 01.01 - 31.03.2016 - - - - (462) (462)

Other comprehensive income - - - - - -

Other changes in equity - - - - -

Total comprehensive income for the period 01.01 - 31.03.2016 - - - - (462) (462)

Balance on 31 March 2016 7 367 737 5 105 (877) 84 725 97 057 (unaudited)

25 April 2016

Executive Director: Chief Accountant:(preparer)

(Vencislav Cholakov) (Stratiya Stratiev)

The interim separate financial statements shall be read together with the notes, which are an integral part of these financial statements.

4

CONTENTS INTERIM SEPARATE STATEMENT OF COMPREHENSIVE INCOME…………….1 INTERIM SEPARATE STATEMENT OF FINANCIAL POSITION……………………2 INTERIM SEPARATE STATEMENT OF CASH FLOWS……………………………….3 INTERIM SEPARATE STATEMENT OF CHANGES IN EQUITY…………………….4 NOTES TO THE INTERIM SEPARATE FINANCIAL STATEMENTS

1. CORPORATE INFORMATION ............................................................................................................ 5 2. SUMMARY OF THE SIGNIFICANT ACCOUNTING POLICIES OF THE COMPANY ................. 6 1. STRUCTURE OF BULGARTABAC GROUP ..................................................................................... 17 4. EQUITY AND DEBT INSTRUMENTS ............................................................................................... 18 5. DIVIDENDS........................................................................................................................................... 18 6. RELATED PARTIES ............................................................................................................................ 18 7. CONTINGENT LIABILITIES AND COMMITMENTS ..................................................................... 19 8. FINANCIAL RISK MANAGEMENT .................................................................................................. 20 9. LIQUIDATION AND INSOLVENCY PROCEDURES....................................................................... 32 10. EVENTS AFTER THE END OF THE REPORTING PERIOD ...................................................... 33 11. CLAIMS TO THE COMPANY ......................................................................................................... 33

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

5

1. CORPORATE INFORMATION

Bulgartabac - Holding AD is a commercial entity incorporated in November 1993 through the transformation of State Organisation Bulgartabac into Bulgartabac - Holding EAD (the Holding) and 22 joint-stock companies with state participation. By decision of the General Meeting of Shareholders of 1997 the company Bulgartabac - Holding EAD was transformed into Bulgartabac - Holding AD. As a result of the publicly announced tender, in pursuance of a decision 3219-P dated 18 April 2011 (promulgated in the State Gazette, issue 34 of 10 May 2011) of the Agency of Privatisation and Post Privatisation Control (the Agency), a privatisation contract between the Agency and BT Invest GmbH, Austria, was signed on 12 September 2011 for the privatisation of 79.83% of the capital of Bulgartabac-Holding AD, Sofia. On 14 October 2011, the Agency, in its capacity of a seller, transferred to BT Invest GmbH, Austria, 5,881,380 shares, or 79.83% of the capital of Bulgartabac-Holding AD. The Company’s registered address and address of management is at 62 Graf Ignatiev Street, Sofia city. The court registration of the Company dates back to 1994, Decision No. 1 of 05 April 1994 of the Sofia City Court. The Company was entered into the Trade Register at the Registry Agency under UIC 831636680. Bulgartabac - Holding AD is a public company under the terms of the Public Offering of Securities Act.

The distribution of the Company’s share capital as at 31 March 2016 was as follows:

BT Invest GmbH, Austria 79.83 % Other legal entities 19.19 % Individual participants – individuals 0.98 %

As at 31 March 2016 Bulgartabac - Holding AD had a one-tier management system – Board of Directors (BD). The Board of Directors comprises 3 members. The Chairman of BD is Vencislav Zlatkov Cholakov. The Company is managed and represented by Vencislav Zlatkov Cholakov.

An extraordinary General Meeting of Shareholders (GMS) of Bulgartabac-Holding AD was held on 31 March 2016. The GMS changed the number of the members of the Board of Directors (BD) from 3 to 5. The members Vencislav Zlatkov Cholakov and Miglena Petrova Hristova were discharged from the BD. Vladimir Gechev Zhekov, Svetlana Raykova Marteva, Shreyas Kishor Phadnis, and Rahul Dattatrya Nimkar were elected as new members of BD. At the date of preparation of these financial statements, these circumstances were not entered into the batch of the Company at the Commercial Register. The Company has an unlimited permit for industrial processing of tobacco No. 1011 dated 21 December 2004 issued by the Council of Ministers. The object of activity of the Company in 2015 included the following types of transactions and deals:

share participation and financial resources management; foreign and domestic trade; buying-up and industrial processing of tobacco; participation in Bulgarian and foreign companies and in their management.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

6

These interim separate financial statements will be published with the Financial Supervision Commission and Bulgarian Stock Exchange – Sofia AD.

2. SUMMARY OF THE SIGNIFICANT ACCOUNTING POLICIES OF THE COMPANY

The Company presents condensed interim separate financial statements for the period ended 31 March 2016 on

the grounds of Art. 100o para.1 of the Public Offering of Securities Act and with reference to the provisions of

Art. 31, para. 1, i. 2 of Ordinance No 2 on the Prospectuses to be Published When Securities are Offered to the

Public of Admitted to Trading on a Regulated Market and on Disclosure of Information by the Public

Companies and the Other Issues of Securities.

The financial statements have been prepared in accordance with the requirements of International Accounting

Standard 34 Interim Financial Reporting and therefore, not all the information and disclosures being required in

relation to the annual financial statements have been included herein.

The accounting policies of Bulgartabac - Holding AD comprise principles, positions of attention, concepts,

rules, bases and procedures for reporting the company’s activity, presenting information in its financial

statements, they have been developed in accordance with the requirements of International Financial Reporting

Standards endorsed by the Commission of the European Union. In addition, the accounting policies have been

made consistent with the specifics of the industry.

The accounting policies and methods of calculation applied in the preparation of the interim financial statements

have not been changed compared to those applied in the preparation of the annual financial statements of

Bulgartabac - Holding AD for 2015.

2.1. CONSOLIDATED FINANCIAL STATEMENTS The Company commenced the process of preparation of its interim consolidated financial statements for the

period ended 31 March 2016 and these separate financial statements will be included therein. According to the

planned dates, management expects that the consolidated financial statements will be approved for issue by the

Board of Directors of the Company not later than 30 May 2016 and then, the financial statements will be made

available to third parties.

2.2. NEW AND AMENDED INTERNATIONAL FINANCIAL REPORTING STANDARDS The Company has adopted all new and/or revised standards and interpretations issued by the International

Accounting Standards Board (IASB) and approved by the Commission of the European Communities, which

are relevant to its activity. The Company’s current accounting policies have not necessitated amendments for

adapting the application of all new and/or revised IFRS in effect for the current reporting year beginning on 1

January 2016, since they do not refer to its activities and the usual composition and characteristic of its assets

and liabilities, or during the period there has not existed any objects or transactions that have been affected by

the changes in the amended IFRS. The effect of changes in IFRS for the Company consists only of the

introduction of new and the expansion of already established disclosures and also of changes in the presentation

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

7

of the financial statements without this affecting the amounts stated therein. At the date of approval of these

financial statements for issue, the following amendments and improvements to effective standards have been

made:

First-time adoption of new amendments to existing standards and interpretations, which have entered into force in the current reporting period The following new amendments to the existing standards and new interpretations issued by the International Accounting Standards Board (IASB) and adopted by the EU have entered into force in the current reporting period: Amendments to various standards Annual improvements to IFRSs (2011-2013 Cycle), as a result of the

annual project for improvement of IFRS (IFRS 3, IFRS 13 and IAS 40) mainly with the purpose to eliminate inconsistences and to clarify the wording – adopted by the EU on 18 December 2014 (the amendments are effective for annual periods beginning on or after 1 January 2015);

IFRIC 21 Levies adopted by the EU on 13 June 2014 (effective for annual periods beginning on or after 17 June 2014).

The adoption of these amendments to existing standards and interpretations has not resulted in changes in the accounting policies of the Company. Amendments to existing standards issued by IASB and adopted by the EU but not yet effective At the date of approval of these financial statements the following amendments to existing standards issued by IASB and adopted by the EU are not yet effective:

Amendments to various standards Annual improvements to IFRSs (2010-2012 Cycle), as a result of the annual project for improvement of IFRS (IFRS 2, IFRS 3, IFRS 8, IFRS 13, IAS 16, IAS 24 and IAS 38) mainly with the purpose to eliminate inconsistences and to clarify the wording – adopted by the EU on 17 December 2014 (the amendments are effective for annual periods beginning on or after 1 February 2015);

Amendments to IAS 16 Property, Plant and Equipment and IAS 41 Agriculture – Agriculture: Bearer Plants – adopted by the EU on 23 November 2015 (effective for annual periods beginning on or after 1 January 2016);

Amendments to IAS 16 Property, Plant and Equipment and IAS 38 Intangible assets – Clarification of Acceptable Methods of Depreciation and Amortization - adopted by the EU on 2 December 2015 (effective for annual periods beginning on or after 1 January 2016);

Amendment to IAS 19 Employee benefits – Defined Benefit Plans: Employee Contributions – adopted by the EU on 17 December 2014 (effective for annual periods beginning on or after 1 February 2015);

Amendment to IFRS 11 Joint Arrangements – Accounting for Acquisitions of Interests in Joint Operations - adopted by the EU on 24 November 2015 (effective for annual periods beginning on or after 1 January 2016);

Amendments to IAS 1 Presentation of Financial Statements: Disclosure Initiative - adopted by the EU on 18 December 2015 (effective for annual periods beginning on or after 1 January 2016);

Amendments to IAS 27 Separate Financial Statements – Equity Method in Separate Financial Statements - adopted by the EU on 18 December 2015 (effective for annual periods beginning on or after 1 January 2016);

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

8

Amendments to various standards Annual improvements to IFRSs (2012-2014 Cycle) , as a result of the annual project for improvement of IFRS (IFRS 5, IFRS 7, IAS 19 and IAS 34) mainly with the purpose to eliminate inconsistences and to clarify the wording - adopted by the EU on 15 December 2015 (the amendments are effective for annual periods beginning on or after 1 January 2016).

New Standards and Interpretations issued by IASB but not yet adopted by the EU

At present, IFRS adopted by the EU do not differ significantly from those adopted by IASB, except for the following standards, amendments to existing standards and interpretations that are not yet adopted by the EU as at the date of approval of these financial statements:

IFRS 9 Financial Instruments (effective for annual periods beginning on or after 1 January 2018);

IFRS 14 Regulatory Deferral Accounts (effective for annual periods beginning on or after 1 January 2016) – the European Commission passed a decision not to commence the process of adoption of this interim standard and to wait until the final standard is issued;

IFRS 15 Revenue from Contracts with Customers (effective for annual periods beginning on or after 1 January 2018);

IFRS 16 Lease (effective for annual periods beginning on or after 1 January 2019)

Amendments to IFRS 10 Consolidated Financial Statements and IAS 28 Investments in Associates and Joint Ventures: Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (effective for annual periods beginning on or after 1 January 2016);

Amendments to IFRS 10 Consolidated Financial Statements, IFRS 12 Disclosures of Interests in Other Entities, and IAS 28 Investments in Associates and Joint Ventures: Applying the Consolidation Exception (effective for annual periods beginning on or after 1 January 2016);

The Company expects that the adoption of these standards, amendments and interpretations will have no material impact on the financial statements of the Company in the period of initial application. At the same time, the hedge accounting relating to portfolios of financial assets and liabilities, the principles of which have not been adopted by the EU, is not yet regulated. According to the management’s judgment, the application of hedge accounting relating to portfolios of financial assets and liabilities in accordance with IAS 39 Financial Instruments: Recognition and Disclosure will not have a material effect on the financial statements, if applied at the reporting date. The comparatives in this interim separate statement of financial position as at 31 March 2016 are extracted from the audited annual financial statements of Bulgartabac – Holding AD for 2015. In the interim separate statement of comprehensive income and cash flow statement, comparatives are from the same period (01 January – 31 March) of the previous year. Where necessary, comparatives are reclassified in order to achieve comparability in view of the current year presentation changes.

2.3. FUNCTIONAL CURRENCY The Company’s functional currency and the currency of presentation of the Company’s financial statements is the Bulgarian lev (BGN).

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

9

2.4. INCOME TAXES Current income taxes are determined in accordance with the requirements of the Bulgarian tax legislation – the Corporate Income Taxation Act (CITA). The nominal income tax rate for 2016 is 10% (2014: 10%).

Deferred income taxes are determined using the liability method on all temporary differences existing at the end of the reporting period between the carrying amounts of the assets and liabilities and their tax bases.

2.5. PROPERTY, PLANT AND EQUIPMENT Property, plant and equipment (fixed tangible assets) are stated in the financial statements at revalued amount less accumulated depreciation and impairment losses.

Measurement at recognition

Upon their initial acquisition items of property, plant and equipment are valued at cost, which comprises the purchase price, including customs duties, non-refundable purchase taxes and any directly attributable costs of bringing the asset to working condition for its intended use. The directly attributable costs include the cost of site preparation, initial delivery and handling costs, installation costs, professional fees for people related to the project, etc.

The Company has set a materiality level of BGN 700 bellow which the assets acquired regardless of whether they possess the characteristics of a fixed asset or not are treated as current expenses at the time they are available for use as intended by management.

Subsequent expenditure

Subsequent costs are recognised only if it is probable that the entity will obtain economic benefits. Repair and

maintenance expenses are recognised as current for the period when incurred. Subsequent expenses relating to

an item of property, plant and equipment that have the nature of replacement of certain components, key parts

and aggregates, or of improvements and restructuring, respectively, are capitalised to the carrying amount of the

relevant asset and its remaining useful life to the date of capitalisation is assessed accordingly. At the same time,

the carrying amount of the replaced components is derecognised and then recognised as current expenses for the

period of restructure.

Measurement after initial recognition

The Company has chosen the revaluation model in accordance with IAS 16 as its approach to recognise

property, plant and equipment. The revalued amount is the asset’s fair value at the date of the revaluation less

any subsequent accumulated depreciation and subsequent accumulated impairment losses.

Where an item of property, plant and equipment is revalued, the entire class of property, plant and equipment to which this asset belongs is revalued. Depreciation

The Company begins to depreciate an item of property, plant and equipment when it is installed and available

for use or with respect to self-constructed assets – from the date the asset is completed and ready for use.

Depreciation is recognised up to the initial cost of the asset less the estimated residual value of the asset by

applying the straight-line depreciation method over the estimated useful life of each item of property, plant and

equipment. Land is not depreciated.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

10

Useful life The useful life of an asset is the evaluation of the number of reporting periods in which the entity expects to

consume economic benefits from the asset. The useful life may be shorter than the economic life of an asset.

The evaluation of the useful life of an item of property, plant and equipment is a matter of judgement based on

the entity’s experience with similar assets.

Useful lives by groups of assets are determined pursuant to their physical wear and tear, specifics of the

equipment, the future intentions for use and the estimated obsolescence, and are as follow:

Asset classes Useful life Buildings 20 – 70 years Plant and equipment 7 – 18 years Motor vehicles 5 – 18 years Fixtures and fittings 2 – 8 years Hardware and equipment 2 – 4 years Promotional equipment 2 – 3 years

The assets’ method of depreciation, useful lives and residual values are reviewed at each reporting date, and

adjusted, if appropriate.

Revaluation of fixed tangible assets

Where the carrying amount of an asset is increased as a result of revaluation, the increase is recognised in other

comprehensive income and is accumulated in the equity as a revaluation reserve, unless it reverses a decrease

made in a previous revaluation of the same asset which has been recognised as a loss. Where the carrying

amount of an asset is decreased as a result of revaluation, the decrease is recognised in other comprehensive

income to the point of the existing credit balance of the revaluation reserve in respect of the said asset and the

amount of the revaluation reserve accumulated in the equity is thereby reduced. The decrease of the carrying

amount of an asset over the amount of the revaluation reserve accumulated therefore is recognised as a loss for

the period.

Impairment of property, plant and equipment The carrying amounts of property, plant and equipment are reviewed for impairment when events or changes in circumstances indicate that the carrying amount might significantly differ from their recoverable amount. If any such indications exist that the estimated recoverable amount is lower than their carrying amount, then the latter is written-down to the recoverable amount of the assets. The recoverable amount of property, plant and equipment is the greater of the two: the fair value less costs to sell and the value in use. Impairment losses are recognised immediately (net profit / loss) for the period, unless a revaluation reserve has been set aside for the specific asset. If this is the case, the impairment loss is recognised against the revaluation reserve and included in other comprehensive income.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

11

2.6. INTANGIBLE ASSETS

Measurement at recognition and subsequent measurement Intangible assets acquired by the Company and having finite useful lives are stated at cost, less any accumulated amortisation and impairment losses.

Subsequent costs

Subsequent costs are capitalised only when these costs will increase the future economic benefits associated with the asset. All other costs, including expenses on internally generated goodwill, are recognised as an expense in the period in which they were incurred.

Measurement after initial recognition Subsequent to their initial recognition, an intangible asset is carried at its cost, less any accumulated amortisation and any accumulated impairment losses. Amortisation. Useful lives. Residual amount

Intangible assets are amortised within the useful life through profits and losses based on their estimated useful lives from the date on which they are ready for use.

The estimated useful lives are as follows:

Asset classes Useful lives Software 2 – 4 years Other industrial property rights 10 years

The residual value of these assets is assumed to be zero unless there is a commitment by a third party to purchase the asset at the end of its useful life and there is an active market for the asset and its residual value can be determined by reference to that market and it is probable that such a market will exist at the end of the asset’s useful life. The assets methods of amortisation, useful lives and residual values are reviewed at each reporting date, and adjusted, if appropriate. Intangible assets with indefinite useful lives are not amortised. They are impaired (in accordance with IAS 36 Impairment of Assets) annually and whenever there is an indication that the intangible asset may be impaired.

Recoverability of the carrying amount—impairment losses

Intangible assets with finite lives are tested for impairment annually in accordance with IAS 36 Impairment of Assets, by comparing the carrying amount and the recoverable amount of an asset. The recoverable amount of an asset is the greater of its fair value less costs to sell and the value in use. Where the carrying amount of an asset exceeds its recoverable amount, the asset is written down to its recoverable amount. Impairment losses are recognised in the income statement.

An assessment is made on an annual basis whether there is any indication that previously recognised impairment losses may no longer exist or may have decreased. If such indication exists, the carrying amount is increased but up to the carrying amount that would have been determined had no impairment loss been recognised for the asset in prior years. Such reversal is recognised in the income statement.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

12

2.7. INVESTMENT PROPERTY Investment property is property to earn rentals or for capital appreciation or both, rather than for sale in the ordinary course of business, use in the production and supply of goods or services, or for administrative purposes.

Measurement at recognition. Measurement after initial recognition

An investment property is measured initially at its cost or at subsequent measurement – at fair value with the changes being recognised in profit and loss. The cost comprises any expenditure directly attributable to the acquisition of the investment property.

2.8. FINANCIAL ASSETS AND FINANCIAL LIABILITIES

Financial assets The Company classifies its financial assets in the following categories: “Loans and receivables” and

“Investments available for sale”. The classification depends on the substance and purposes of the financial assets at the date of their acquisition. Management determines the classification of the financial assets of the Company at the date of their initial recognition in the statement of financial position.

Usually, the Company recognises its financial assets in the statement of financial position on the date whet it has become a party to a contractual arrangement to acquire a financial asset. All financial assets are valued initially at their fair value plus, in the case of financial assets that are not measured at fair value through profit or loss, the direct transaction costs.

Financial assets are derecognised from the Company’s statement of financial position when the rights to receive the cash flows from these assets have expired or have been transferred, and the Company has transferred substantial part of all the risks and rewards of ownership of the asset to a third party (entity). Where the Company has retained substantially all the risks and rewards of ownership of a certain transferred financial asset, the asset is still recognised in the Company’s statement of financial position, but the Company recognises also a secured liability (loan) for the consideration received.

a) Available-for-sale financial assets Available-for-sale financial assets are those non-derivative financial assets that are designated as

available for sale or are not classified in other categories. Usually, these are shares and interests in other companies, acquired for investment purposes. They are included in non-current assets, unless the Company intends to sell them within the next 12 months and seeks actively a buyer.

Investments held by the Company, representing shares in other companies, are measured and represented at cost, less any impairment losses, as these shares are not quoted in active markets and therefore, no active market price quotations are available for them, and the assumptions needed for application of alternative valuation techniques are connected with uncertainties.

At the end of the reporting period, an impairment test of available-for-sale financial assets is carried out in order to determine whether there are any indications of impairment.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

13

b) Loans and receivables

Receivables and loans granted (monetary loans) are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. These assets are included in the group of current assets when they mature within either 12 months or the usual operating cycle of the Company, and the others - in the group of non-current assets. This group of financial assets includes: loans granted, trade receivables, other receivables from contractors and third parties, cash and cash equivalents. Loans and receivables are recognised in the statement of financial position at their amortised cost using the effective interest method less any allowance for impairment.

Interest income on loans granted and receivables is recognised based on the effective interest rate, except for short-term receivables less than 12 months where the recognition of such interest is accepted unjustifiable as immaterial and within the usual loan terms. Interest income on receivables is presented in the statement of comprehensive income under “Other operating gains and losses”, and interest income on loans granted under “Revenue”.

The Company assesses at the end of each reporting period whether events and circumstances have occurred that indicate the existence of objective evidence that an individual financial asset or a group of assets carried at amortised amount is impaired.

An expense on impairment of loans and receivables is formed when there is objective evidence that the Company will not be able to collect the entire amount of the receivable in accordance with the original terms and conditions. The amount of the impairment loss is measured as the difference between the receivable’s carrying amount and the present value of estimated future cash flows discounted at the original effective interest rate. The carrying amount is adjusted by using an allowance account in which all impairment amounts are accumulated while the sum of the impairment loss for the period is recognised in the statement of comprehensive income under “Reversed /(Accrued) impairment of assets, net”. In case of subsequent recovery of an impairment loss, the latter is stated as part of “Reversed /(Accrued) impairment of assets, net” against a decrease in the allowance account.

Bad debts are written off when the legal grounds for that are identified or when a particular trade receivable is assessed as fully uncollectible. The write off is made against the allowance formed and/or is recognised as an expense in the current period.

Financial liabilities

The Company’s financial liabilities include payables to suppliers and other contractors. They are recognised initially in the statement of financial position at their fair value on the date of the

transaction, net of any direct transaction costs based on the consideration received, and are subsequently measured at amortised cost using the effective interest rate method.

Short-term payables that are interest-free are measured at their original value as the effect of discounting is immaterial.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

14

2.9. KEY ESTIMATES AND ASSUMPTIONS OF HIGH UNCERTAINTY The preparation of the interim financial statements of the Company requires management to apply judgements, estimates and assumptions, which have effect on the reported values of assets and liabilities, income and expenses (and in the conditions of financial crisis the uncertainty is even bigger). Each uncertainty related to these assumptions and estimates may lead to actual results requiring adjustments in the carrying amounts of the respective assets or liabilities in the future. The estimates and assumptions made are reviewed on a regular basis. Any adjustments therein are recognised in the financial statements for the period in which the adjustment has been made as well as in all subsequent financial periods. Information about significant estimates, evaluations and assumptions that have the most significant impact on the recognition and measurement of assets, liabilities, income and expenses, is presented below.

Fair value measurement Some of the accounting policies and disclosures of the Company require fair value measurements for financial and non-financial assets and liabilities. The Company uses observable inputs to measure fair value of an asset or a liability, where possible. Fair values are categorised within the fair value hierarchy, described as follows, based on the inputs in the valuation techniques:

Level 1 — quoted (unadjusted) market prices in active markets for identical assets or liabilities Level 2: input data other than quoted market prices, included in Level 1, that may be found for

the asset or liability either directly (as prices) or indirectly (derived from prices). Level 3: input data for the asset of liability that are not based on available market data

(unobservable inputs).

If the inputs used to measure fair value of an asset or a liability can be categorised within the fair value hierarchy, then the fair value measurement is categorised as a whole at that level of the fair value hierarchy that is significant to the fair value measurement as a whole. The Company recognises transfers between levels in the fair value hierarchy at the end of the reporting period in which the transfer has occurred.

2.9.1. Write down of investments in subsidiaries At the date of each set of financial statements, management conducts an analysis and evaluation of the existence of indications of impairment of its investments in subsidiaries and decides on the probable amount of impairment losses.

In pursuance with the company’s accounting policy, management conducted an analysis and evaluation of the existence of indications of impairment of its investments in subsidiaries. Based on the review, management judged that there were not any indications of impairment of its investments in subsidiaries as of 31 December 2016.

2.9.2. Write down of inventories At the end of the interim period (31 December 2016), a review of available inventories had been carried out. Based on the review, indications of impairment were not established at the time of preparation of these financial statements.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

15

2.9.3. Impairment of financial assets At the date of each set of financial statements management estimates the losses from doubtful and bad debts. Receivables, which are not collected within the initially set contractual terms and where difficulties in collecting are observed, are subject to analysis in order to determine the actually collectible portion thereof while the remaining portion to the nominal value is recognised in the statement of comprehensive income as an impairment loss.

In assessing the collectability of receivables, for which there are indications of impairment, management performs an analysis of the total exposure of receivables for each contractor with a view of assessing the actual collectability and not only at the level of the overdue individual receivables from the contractor, including the potential possibility to collect interests for offsetting the overdue amounts. Where the collectability of a receivable (group of receivables) is highly uncertain, an estimate is made on what portion thereof is secured (bank guarantee, pledge, surety) and thus, their collection is guaranteed (through a future possible sale of collateral or payment by a guarantor). Receivables, or part thereof, for which management has judged that there is high uncertainty as to their collectability are 100 % impaired.

Based on a review of the possibility for collecting overdue receivables as of 31 December 2015 and on an analysis of the information available at the date of preparation of the interim financial statements, the Company’s management has judged that the possibility for collecting receivables amounting to BGN 617 thousand shall be assessed to zero. These receivables have been assessed as bad debts as they have not been collected within the initially established deadlines pursuant to the contractual terms and conditions, and, out of the analysis of the quality of available collateral, the company’s management have not been able to satisfy themselves that there is sufficient certainty of the future repayment of the amounts due, or these amounted are due by companies in insolvency and liquidation. Costs of write down of receivables relating to interest income and penalties on loans amounting to BGN 114 thousand have been presented net in the statement of comprehensive income under a heading “Revenue”.

Investments available for sale are subject to review at the date of each reporting period with the aim to establish whether there are any indicators for impairment. Investments available for sale are impaired when the Company finds out that their carrying amount is higher than the estimated recoverable amount.

At 31 December 2015, based on a review for the existence of indications of impairment, the Company’s management judged that there were no indications of impairment of its investments available for sale.

2.9.4. Actuarial calculations of the present value of long-term retirement benefit obligations In assessing the present value of long-term retirement benefit obligations, the calculations of certified actuaries have been used. Such calculations are made at the end of each year in connection with the preparation of the annual financial statements. At the end of each interim period, management updates the amount of the liability based on the best estimate.

At 31 March 2016, an expense amounting to BGN 8 thousand (31 March 2015: BGN 13 thousand) had been recognised.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

16

2.9.5. Revalued amounts of property, plant and equipment

The fair value measurement for Property, plant and equipment has been categorised as a fair value of Level 3 within the fair value hierarchy introduced by IFRS 13 with respect to all financial and non-financial assets and liabilities falling within the scope of the standard, based on the inputs to the employed valuation technique. The fair value is determined based on valuations made by external valuers by weighing various valuation methods depending on the probability of realisation of the hypotheses made when applying the presumption, introduced by IFRS 13, for measuring fair values on the basis of market expectations for maximising the asset’s value depending on its use. Therefore, the comparative sales method is assigned the highest weight in evaluating the above assets, complemented by the revenue approach when fair values are measured.

It is accepted by the Company that the revaluation of the property, plant and equipment to their fair values shall be made by independent licensed appraisers at 5-year period, since management believes this is the usual term, in which more typical trends and changes in prices of property and other basic equipment, installations and machinery occur. However, where their fair value changes materially in shorter periods of time, the revaluation may be conducted at shorter periods of time. Such revaluations were conducted as of 31 December 2000, 31 December 2005, 31 December 2009, and 31 December 2014.

2.9.6. Changes in the volume of production and sales

In March 2016, management of Bulgartabac Group announced that as a result of the reduction in orders, as also in order to prevent any more significant business risks, a decision was passed to discontinue the manufacture and sales of products to the Middle East Region as of 1 April 2016.

As a consequence, there are certain risks and uncertainty with regard to the future financial results from the Group companies’ activities, including from those of Bulgartabac Holding AD, as also significant risks and uncertainty as to the assessment of the assets of subsidiaries and associates. At the date of preparation of these financial statements,

The Group’s management conducted an analysis of the occurred and potential consequences of the above circumstances, as also of the necessary measures to reduce and neutralize their effects on business of the Group companies. Based on the already analysed information, the management’s estimate is that all Group companies will continue their business activities by taking short-term measures to optimise their economic indicators in light of the individual circumstances.

In the preparation of these financial statements, based on information available and the best estimate of management of Bulgartabac Holding AD, the above risks and uncertainty have no effect on the recoverable amount of the assets presented in these financial statements, including of investments and receivables from subsidiaries. And respectively, there is no need to recognize additional impairment as at 31 March 2016.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

17

1. STRUCTURE OF BULGARTABAC GROUP

The activity of Bulgartabac - Holding AD includes management of share participation and financial resources, foreign and domestic trade, buying-up and industrial processing of tobacco, participation in Bulgarian and foreign companies and in their management. Bulgartabac - Holding AD holds the ownership of trademarks of cigarettes manufactured by the Group.

Structure of the Group at the end of the reporting period:At 31 March 2016 Bulgartabac Group included Bulgartabac - Holding AD and the entities controlled, directly or through subsidiaries, by Bulgartabac - Holding AD.

At 31 March 2016 the following group companies were in liquidation proceedings – Haskovo Tabac D and Asenovgrad Tabac AD.

At 31 March 2016 Bulgartabac-Holding AD held the control, directly or through subsidiaries, on the following companies:

Blagoevgrad BT AD, town of Blagoevgrad Sofia BT AD, Sofia city Pleven BT AD, Yassen village, Pleven Region Baranko OOD, Plovdiv city Fabrika Duvana AD, town of Banja Luka in the Republic of Serbia, Bosnia and Herzegovina Bulgartabac Logistics LLC. Russia Global Tobacco Traiding, SL. Spain Global Tobacco Trading, SRL. Romania Global Tobacco Trading, DOO. Serbia EMEA Market Establishment Shumen Tabac AD, town of Shumen Asenovgrad Tabac AD (in liquidation), town of Asenovgrad Haskovo Tabac AD (in liquidation), town of Haskovo

The object of activity of the subsidiaries is as follows:

manufacture of cigarettes – Blagoevgrad BT AD, Sofia BT AD and Fabrika Duvana AD. These companies hold durable licences for production of cigarettes;

industrial processing of raw tobacco - Pleven BT AD;

trade in tobacco products – Bulgartabac Logistics LLC. – Russia, Global Tobacco Trading, SL. – Spain, and Global Tobacco Trading, SRL. – Romania. At 31 March 2016 Bulgartabac-Holding AD exercised significant influence, directly or through subsidiaries, on the following companies:

Tabac Market AD Yurii Gagarin AD Express Logistics and Distribution OOD

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

18

Changes in the structure of the Group during the reporting periodDuring the first quarter of 2016 there have been no charges in the ownership structure of Bulgartabac Group.

In September 2015 the subsidiaries Sofia BT AD and Blagoevgrad BT AD acquired 45 % of the shares of Express Logistics and Distribution OOD.

In May 2015 the subsidiaries Sofia BT AD and Blagoevgrad BT AD acquired 66% of the shares of Baranko OOD.

4. EQUITY AND DEBT INSTRUMENTS

Equity and debt instruments have neither been issued nor settled or redeemed for the period 1 January – 31 March 2016.

5. DIVIDENDS

Dividends were not distributed in 2016. The regular General Meeting of Shareholders of Bulgartabac-Holding AD, held on 16 July 2015,

passed a decision to distribute to the shareholders dividends amounting to BGN 4.20 per share, or the total amount of BGN 30,942 thousand, as follows:

BGN 1,731 thousand chargeable to the company’s profit for the financial year of 2014; and BGN 29,211 thousand chargeable to Prior Year’s Retained Earnings Fund.

6. RELATED PARTIES

During the period 01 January – 31 March 2016 Bulgartabac-Holding AD has conducted transactions with related parties, including sales of inventories and provision of services (including royalties, commissions, IT services and other services), and purchases of services and materials.

In February 2016 the Company granted a tranche from a loan amounting to EUR 28 thousand (BGN 55 thousand) to Global Tabaco Trading Bucharest, Romania. At the date of these financial statements, the total amount of EUR 71 thousand (BGN 140 thousand) was granted out of the total agreed loan amount of EUR 100 thousand.

In July 2015 the Company extended a loan amounting to BGN 450 thousand to its associated company Tabac Market AD. The loan bears an annual interest rate of 5%. A pledge of property is provided as collateral.

Dividends amounting to BGN 31,333 thousand were received in 2015 from the subsidiaries Sofia BT and Blagoevgrad BT.

In the reporting period purchases from related parties amount to BGN 936 thousand and sales amount to BGN 11,371 thousand (including interest and penalties charged amounting to BGN 49 thousand).

At the period-end, related party receivables amounted to BGN 28,165 thousand and related party payables amounted to BGN 2,655 thousand. The maturities of related party receivables are presented in the maturity analysis table in Note 8.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

19

7. CONTINGENT LIABILITIES AND COMMITMENTS

7.1. OPERATING LEASE

Operating lease liabilities – Bulgartabac-Holding AD as a lessee At 31 March 2016 the company is a party to operating lease agreements as a lessee. The future minimum lease

payments under operating lease rental are as follows:

31.03.2016 31.12.2015BGN '000 BGN '000

Within 1 year 723

839

After 1 year but not more than 5 years 296 412Total 1,019 1,251

Operating lease receivables – Bulgartabac-Holding AD as a lessor The future minimum lease receivables under operating lease rental are as follows:

31.03.2016 31.12.2015 BGN '000 BGN '000

Within 1 year 564 570After 1 year but not more than 5 years 132 269Total 696 839

7.2. COURT AND EXECUTIVE CASES

Cases initiated by Bulgartabac-Holding ADBurgas Regional Court, civil case No 4481/2012. Claimant - Bulgartabac-Holding AD. Defendants –Tarpina Petrova and Sofiyka Koleva. A negative declaratory claim to establish the right of ownership. Burgas Regional Court issued a decision in favour of Bulgartabac-Holding AD. The decision was appealed against by Tarpina Petrova and Sofiyka Koleva before the Burgas District Court. A civil case ( ) No. 599/2014 was constituted before the Burgas District Court, Civil Division, V panel. The decision of the Burgas District Court was not in favour of Bulgartabac-Holding AD. This decision was appealed against by Bulgartabac-Holding AD before the SCC.

Court cases relating to trademark rightsThe company is a party to disputes for rights of trademarks in the country, as also in Turkey, Greece, Argentina, Israel, Macao, and Chili. Part of the cases are initiated by Bulgartabac – Holding AD for deletion of rights of trademarks registered by foreign persons, for which Bulgartabac – Holding AD has either made the registration already. There are cases constituted against the company for deletion of already registered trademarks.

Executive casesThe Company institute legal proceedings for collecting receivables from prior periods. Writs of execution have been issued in connection with these cases for the total amount of BGN 167 thousand, including principle of the receivables and court charges.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

20

Court cases to which Bulgartabac Holding AD is an interested party:Sofia Administrative Court - a court case was constituted at an appeal of Dunhill Tobacco of London LTD against a decision of the Chairman of the Patent Agency of the Republic of Bulgaria in connection with an opposition against the registration of the trademark BT NANO. A decision was issued in favour of Bulgartabac-Holding AD. The decision of Sofia Administrative Court was appealed against before the Supreme Administrative Court. A hearing is scheduled to be held on 05 December 2016.

7.3. COLLATERAL PROVIDED

At 31 March 2016 cash of the Company amounting to BGN 8,997 thousand, of which the amount of BGN 8,703 thousand denominated in EUR (EUR 4,450 thousand), was restricted as collateral to secure the issuance of bank guarantees (Note 7.3).

7.4. GUARANTEES ISSUED

The Company has issued a guarantee in favour of Citibank Russia to secure the performance of the obligations of a third party in accordance with the terms and conditions of a loan contract concluded in October 2013; Term – until 30 April 2016; Amount – BGN 8,703 thousand (31 December 2014: BGN 8,703 thousand).

A guarantee is issued by Bulgartabac-Holding AD in favour of Julius Meinl Austria Gmbh, Austria, to secure trade payables; Term – until 15 May 2016; Amount: BGN 294 thousand (31 December 2015: BGN 294 thousand).

8. FINANCIAL RISK MANAGEMENT In the ordinary course of its business activities, the Company is exposed to a variety of financial risks the most important of which are: market risk (including currency risk, interest rate risk and other price risk), credit risk, and liquidity risk. The overall risk management is focused on the difficulties of forecasting the financial markets and minimising the potential negative effects that might affect the financial performance and position of the Company. The financial risks are currently identified, measured and monitored through various control mechanisms introduced in order to establish adequate prices for the products and services, provided by the Company, to appropriately assess the market circumstances related to the Group companies’ investments and forms for maintenance of free liquid funds through preventing undue concentration of a particular risk. Risk management in the Company is currently executed by the management and the respective structural units, depending on the type and specific features of various risks to which the Company is exposed in its operations. Below are presented the types of risks to which the Company is exposed upon performing its commercial transactions and the approach adopted for managing these risks.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

21

Structure of financial assets and liabilities by categories:

Loans and receivables Available-for-sale

assets

Total

31 March 2016 BGN’000 BGN’000 BGN’000 Financial assets Investments available-for-sale - 100 100 Long-term related party receivables 781 - 781 Other long-term financial assets 680 - 680 Related party receivables 27,371 - 27,371 Trade receivables 2,157 - 2,157 Deposits placed with commercial banks 294 - 294 Cash and cash equivalents 9,843 - 9,843 Court and awarded receivables 7 - 7 Other receivables 152 - 152 Total 41,285 100 41,385

Other financial

liabilities Total

BGN’000 BGN’000Financial liabilities Long-term payables to financial entities 416 416

Payables to related parties 2,655 2,655

Short-term payables to financial entities 212 212Trade payables 10,436 10,436Dividends payable 242 242Other liabilities 45 45Total 14,006 14,006

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

22

Loans and receivables Available-for-

sale assets

Total

31 December 2015 BGN’000 BGN’000 BGN’000Financial assets Investments available-for-sale - 100 100Long-term related party receivables 526 - 526Other long-term financial assets 708 - 708Related party receivables 28,391 - 28,391Trade receivables 1,930 - 1,930Deposits placed with commercial banks 294 - 294Cash and cash equivalents 9,059 - 9,059Court and awarded receivables 7 - 7Other receivables 148 - 148Total 41,063 100 41,163

Other financial liabilities Total

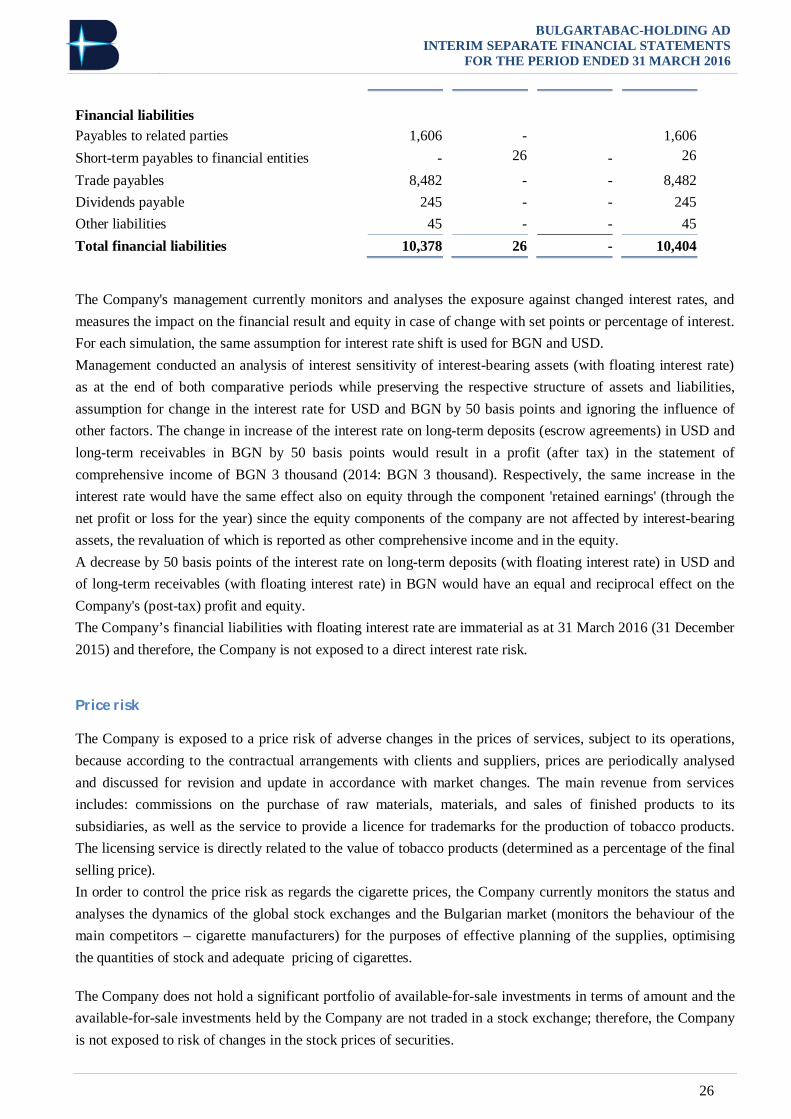

BGN’000 BGN’000 Financial liabilities Payables to related parties 1,606 1,606Short-term payables to financial entities 26 26Trade payables 8,482 8,482Dividends payable 245 245Other liabilities 45 45Total 10,404 10,404

MARKET RISK

Currency riskThe main part of the economic operations of the Company is executed in BGN or EUR. An immaterial part of the Company’s financial assets and liabilities are denominated in USD (primarily cash deposited for long time in escrow accounts and cash in current accounts). The Company is exposed to currency risk primarily with regard to its USD exposure.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

23

The tables below summarise the Company's exposure to currency risk:

Foreign currency structure analysis In EUR In USD In other foreign

currency

In BGN Total

31 March 2016 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 Financial assets Investments available-for-sale - - - 100 100 Long-term related party receivables - - - 781 781 Other long-term financial assets - 680 - - 680 Related party receivables 55 - 27,316 27,371 Trade receivables 420 68 - 1,669 2,157 Deposits placed with commercial banks 294 - - - 294 Cash and cash equivalents 9,552 72 1 218 9,843 Court and awarded receivables - - - 7 7 Other receivables 25 15 5 107 152 Total financial assets 10,346 858 6 30,122 41,385

Financial liabilities Long-term payables to financial entities 416 416 Payables to related parties 172 - - 2,483 2,655 Short-term payables to financial entities 18 - - 194 212 Trade payables 1,688 1,068 188 7,492 10,436 Dividends payable - - - 242 242 Other liabilities - - - 45 45 Total financial liabilities 1,878 1,068 188 10,872 14,006

Foreign currency structure analysis In EUR In USD In other foreign

currencyIn BGN Total

31 December 2015 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 Financial assets Investments available-for-sale - - - 100 100 Long-term related party receivables - - - 526 526 Other long-term financial assets - 708 - - 708 Related party receivables 180 62- - 28,149 28,391 Trade receivables 107 4 - 1,819 1,930 Deposits placed with commercial banks 294- - - - 294 Cash and cash equivalents 8,735 45 1 278 9,059 Court and awarded receivables - - - 7 7 Other receivables 25 15 5 103 148 Total financial assets 9,341 834 6 30,982 41,163

Financial liabilities Payables to related parties 172 - - 1,434 1,606 Short-term payables to financial entities 26 - - - 26 Trade payables 832 911 159 6,580 8,482 Dividends payable - - - 245 245 Other liabilities - - - 45 45

Total financial liabilities 1,030 911 159 8,304 10,404

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

24

Foreign currency sensitivity analysis USD

31.03.2016 31.12.2015 BGN’000 BGN’000

Financial result (profit) + 19 7Equity (component - retained earnings) + 19 7Financial result (loss) - (19) (7)Equity (component - retained earnings) - (19) (7)

The analysis is based on the structure of the currency exposures in USD at the end of the reporting period, with all other variables held constant, including interest rates. A 10-percent increase in the exchange rate of the USD to the BGN as at 31 March 2016 would decrease the Company's profit (after tax) by BGN 19 thousand (2015: BGN 7 thousand) due to the effect of the increased BGN value of financial liabilities, net of the effect of the increase in the BGN value of financial assets. Respectively, a 10-percent increase in the exchange rate would have the same effect also on equity through the component 'retained earnings' (through the current profit or loss) since the equity components of the Company are not affected by the foreign currency assets and liabilities, the revaluation of which is reported as other comprehensive income or directly in the equity. A decrease by 10% of the exchange rate of the USD to BGN would have an equal and reciprocal effect of that described above, on the Group's profit (after taxes) and the equity. The profit/(loss) after taxes is more sensitive to currency risk in the period than that in the comparative period due to the increase in the Company’s exposure to foreign currency liabilities denominated in USD, net of foreign currency assets denominated in USD (- USD 122 thousand) compared to the net exposure in 2015 (- USD 43 thousand).

Interest rate risk

Interest rate risk is the risk that the fair value or the future cash flows of the financial instruments, held by the Company, will vary due to changes in market interest rates. Fixed-rate instruments are exposed to interest rate fair value risk - the price of Company's fixed-rate financial assets will decrease with the increase in the market interest rate, and vice versa. Floating-rate financial assets and liabilities are exposed to a cash flow risk - the future cash flows from floating-rate financial instruments will vary due to changes in market interest rates. Interest-bearing fixed-rate financial assets in the structure of the Company’s assets are represented by cash and loans granted.

The Company holds interest-bearing assets with floating interest rates that are exposed to risk of cash flows. These assets comprise amounts deposited (in USD) through an escrow agent appointed by the Company.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

25

Interest-

free With

floating interest %

With fixed interest %

Total

31 March 2016 BGN’000 BGN’000 BGN’000 BGN’000 Financial assets Investments available-for-sale 100 - - 100 Long-term related party receivables - - 781 781 Other long-term financial assets - 680 - 680 Related party receivables 26,924 - 447 27,371 Trade receivables 2,157 - - 2,157 Deposits placed with commercial banks - - 294 294 Cash and cash equivalents 8,756 - 1,087 9,843 Court and awarded receivables 7 - - 7 Other receivables 152 - - 152 Total financial assets 38,096 680 2,609 41,385

Financial liabilities Long-term payables to financial entities 416 416

Payables to related parties 2,655 - - 2,655 Short-term payables to financial entities - 18 194 212

Trade payables 10,436 - - 10,436 Dividends payable 242 - - 242 Other liabilities 45 - - 45 Total financial liabilities 13,378 18 610 14,006

31 December 2015

Interest-free

With floating

interest %

With fixed interest %

Total

BGN’000 BGN’000 BGN’000 BGN’000 Financial assets Investments available-for-sale 100 - - 100 Long-term related party receivables - - 526 526 Other long-term financial assets - 708 - 708 Related party receivables 27,786 - 605 28,391 Trade receivables 1,930 - - 1,930 Deposits placed with commercial banks - - 294 294 Cash and cash equivalents 8,756 - 303 9,059 Court and awarded receivables 7 - - 7 Other receivables 148 - - 148 Total financial assets 38,727 708 1,728 41,163

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

26

Financial liabilities Payables to related parties 1,606 - 1,606 Short-term payables to financial entities - 26 - 26

Trade payables 8,482 - - 8,482 Dividends payable 245 - - 245 Other liabilities 45 - - 45 Total financial liabilities 10,378 26 - 10,404

The Company's management currently monitors and analyses the exposure against changed interest rates, and measures the impact on the financial result and equity in case of change with set points or percentage of interest. For each simulation, the same assumption for interest rate shift is used for BGN and USD. Management conducted an analysis of interest sensitivity of interest-bearing assets (with floating interest rate) as at the end of both comparative periods while preserving the respective structure of assets and liabilities, assumption for change in the interest rate for USD and BGN by 50 basis points and ignoring the influence of other factors. The change in increase of the interest rate on long-term deposits (escrow agreements) in USD and long-term receivables in BGN by 50 basis points would result in a profit (after tax) in the statement of comprehensive income of BGN 3 thousand (2014: BGN 3 thousand). Respectively, the same increase in the interest rate would have the same effect also on equity through the component 'retained earnings' (through the net profit or loss for the year) since the equity components of the company are not affected by interest-bearing assets, the revaluation of which is reported as other comprehensive income and in the equity. A decrease by 50 basis points of the interest rate on long-term deposits (with floating interest rate) in USD and of long-term receivables (with floating interest rate) in BGN would have an equal and reciprocal effect on the Company's (post-tax) profit and equity. The Company’s financial liabilities with floating interest rate are immaterial as at 31 March 2016 (31 December 2015) and therefore, the Company is not exposed to a direct interest rate risk.

Price risk The Company is exposed to a price risk of adverse changes in the prices of services, subject to its operations, because according to the contractual arrangements with clients and suppliers, prices are periodically analysed and discussed for revision and update in accordance with market changes. The main revenue from services includes: commissions on the purchase of raw materials, materials, and sales of finished products to its subsidiaries, as well as the service to provide a licence for trademarks for the production of tobacco products. The licensing service is directly related to the value of tobacco products (determined as a percentage of the final selling price). In order to control the price risk as regards the cigarette prices, the Company currently monitors the status and analyses the dynamics of the global stock exchanges and the Bulgarian market (monitors the behaviour of the main competitors – cigarette manufacturers) for the purposes of effective planning of the supplies, optimising the quantities of stock and adequate pricing of cigarettes. The Company does not hold a significant portfolio of available-for-sale investments in terms of amount and the available-for-sale investments held by the Company are not traded in a stock exchange; therefore, the Company is not exposed to risk of changes in the stock prices of securities.

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

27

CREDIT RISK

When performing its activities, the Company is exposed to credit risk related to the risk that some of its counterparts might not be able to discharge their obligations in full and within the agreed deadlines. The Company’s receivables are presented in the statement of financial position net, less any impairment. Such impairment has been accrued for receivables where and when there have been events identifying losses due to uncollectability based on past experience. The Company's financial assets are concentrated primarily in the following groups: other long-term financial assets, available-for-sale investments, and cash – cash on hand and in bank accounts (current and deposit), trade receivables, and related party receivables (subsidiaries), and other receivables. The maximum exposure to credit risk at the end of the reporting period is the carrying amount of each class of financial assets as disclosed in this Note (Structure of financial assets and financial liabilities by categories). In view of the credit risk of cash flows in bank accounts, the Company has adopted best practices and methods for selection of financial organisations to provide cash and cash equivalent management services, as also payment and other services related thereto. By working with a number of financial organisations, the concentration of risks for the Company has been minimised and its stability and steadiness have been guaranteed. The Company has not a significant concentration of credit risk with respect to related party receivables, except for the receivables from related parties in a worsened financial position. In relation to the credit risk of uncollectability of its receivables, the Company undertakes the following security measures:

with regard to loan agreements - collateral is required at the time of signature (pledge of fixed tangible assets, mortgage of real estate, etc). In addition, in some cases it is required a promissory note to be issued in favour of Bulgartabac-Holding AD - in an amount equal to the sum of the principal and interest under the loan agreement as per the repayment schedule;

with regard to trade and other receivables, which are past due and have not been secured on their origination, agreements are being concluded for their deferral and collateral is agreed in an amount that may not be lower than the initially recognised amount of the receivable. The collateral usually represents an established mortgage of property(ies);

with regard to other agreements, which have not been secured in advance, the following common actions are undertaken in the event of overdue payment by the debtor company - setoff of payables to the company against overdue receivables and where the payable amount is not sufficient to cover the receivable of Bulgartabac-Holding AD, then other out-of-court options are sought to settle the receivables (transactions related to purchases of assets owned by the debtor, which are settled by setoff).

In the Company, the servicing of receivables, the reasons for them being past due and the changes in the financial capacity of the debtor companies, are currently monitored and analysed, with the status and quality of collateral provided being subject to control as well. Regarding the other clients, the Company's policy is that deferred payments (credit sales) are offered as an exception only to clients having long account of business relations with the Company, good financial position and no history of credit terms violations. Receivables are controlled jointly by the trade and financial departments of the Company, by following the implemented common practices and monitoring the observance

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

28

of contractual terms and conditions. Sales to other clients are performed mainly through advance payments (partial or full) or through payment on the date of the transaction.

LIQUIDITY RISK

Liquidity risk is the adverse situation when the Company encounters difficulties in meeting unconditionally its obligations within their maturity. The liquidity management policy of the Company's is conservative maintaining a constant optimal liquid reserve, cash and a good capability for funding its business activities, including continuous control monitoring of the actual and forecast cash flows by periods ahead, and matching maturity profiles of assets and liabilities. The Company manages its liquidity by ensuring an optimal balance between own and borrowed capital. Therefore, the Company maintains sufficient cash as to be able to meet at any time its liabilities according to their maturity.

Maturity analysis The financial and accounting departments monitor currently the maturity and the timely payments by maintaining day-to-day information about the available cash and by analysing the forthcoming payments. Free cash is invested usually in short-term deposits placed with commercial banks.

The Company's financial non-derivative assets and liabilities at the end of the reporting period are presented below. The table is prepared on the basis of undiscounted cash flows and the earliest date on which the receivable and respectively, the payables, become due for payment. Amounts include principal and interest. The Company's assets and liabilities, analysed in terms of the remaining useful lives as of the end of the reporting period, are as follows:

31 March 2016 On

demand within 1 month 1-3

months 3-6 months 6-12

months 1-2 year 2-5 years over 5 years With no

maturity Total

BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000

Financial assets Investments available-for-sale - - - - - - - - 100 100Long-term receivables from related parties - - - - - 810 -

- - 810

Other long-term financial assets - - - - - - 680

- - 680

Receivables from related parties 23,183 3,312 74 111 691 - - - - 27,371

Trade receivables 1,946 127 84 - - - - - - 2,157Deposits placed with commercial banks - - - 294 - - - - - 294

Cash and cash equivalents 1,087 - - - 8,703 - - - 53 9,843Court and awarded receivables 7 - - - - - - - - 7Other receivables - - - - - - - - 152 152

Total financial assets 26,223 3,439 158 405 9,394 810 680 - 305 41,414

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

29

Financial liabilities Long-term payables to financial entities

230 213

443

Payables to related parties 2,001 654 - - - - - - - 2,655Short-term payables to financial entities 18 18 38 57 114 - -

- - 245

Trade payables 8,779 1,655 2 - - - - - - 10,436Dividends payable 242 - - - - - - - - 242Other liabilities - - - - - - - - 45 45

Total financial liabilities 11,040 2,327 40 57 114 230 213 - 45 14,066

31 December 2015 On

demand within 1 month 1-3

months 3-6 months 6-12

months 1-2 year 2-5 years over 5 years With no

maturity Total

BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000 BGN’000

Financial assets

Investments available-for-sale - - - - - - - - 100 100

Long-term receivables from related parties - - - - - 561

- - 561

Other long-term financial assets - - - - - - 708

- 708

Receivables from related parties 21,339 6,636 74 111 231 - - - - 28,391

Trade receivables 1,779 151 - - - - - - - 1,930

Deposits placed with commercial banks - - - 294 - - - - - 294

Cash and cash equivalents 302 - - 8,757 - - - - 9,059

Court and awarded receivables 7 - - - - - - - - 7

Other receivables - - - - - - - - 148 148

Total financial assets 23,427 6,787 74 405 8,988 561 708 - 248 41,198

Financial liabilities

Payables to related parties 1,486 120 - - - - - - - 1,606

Short-term payables to financial entities 26 - - - - -

- - 26

Trade payables 6,542 1,866 74 - - - - - - 8,482

Dividends payable 245 - - - - - - - - 245

Other liabilities - - - - - - - - 45 45

Total financial liabilities 8,299 1,986 74 - - - - - 45 10,404

BULGARTABAC-HOLDING AD INTERIM SEPARATE FINANCIAL STATEMENTS

FOR THE PERIOD ENDED 31 MARCH 2016

30

Capital risk management

The capital management objectives of the Company are to build and maintain capabilities to continue its operation as a going concern and to provide return on the investments of shareholders and economic benefits to the other stakeholders and participants in its business, as well as to maintain an optimal capital structure to reduce the cost of capital. The Company currently monitors, plans and manages the structure of capital by ensuring and optimal balance between own and borrowed capital.

Fair values Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

The fair value concept presumes realisation of the financial instruments through sale. However, in most cases especially with regards to trade receivables and payables as well as loans granted and deposits, the Company expects to realise these financial assets also through their total refund or respectively, settlement over time. Therefore, they are presented at their amortised cost which is accepted as being fairly close to their fair value.